| CHAPTER 12 |

Synthetic Pricing and Arbitrage

For the questions in this section, assume that all options are European (no possibility of early exercise). All calculations should be made using simple interest, rather than compound or continuous interest. Assume that a year is made up of 365 days, 52 weeks, or 12 months. Answers should be expressed to the nearest .01 for contract prices, to the nearest .01% for interest rates, and to the nearest whole number for days to expiration.

Basic put-call parity:

call price – put price = (forward price – exercise price) / (1 + interest rate × time)

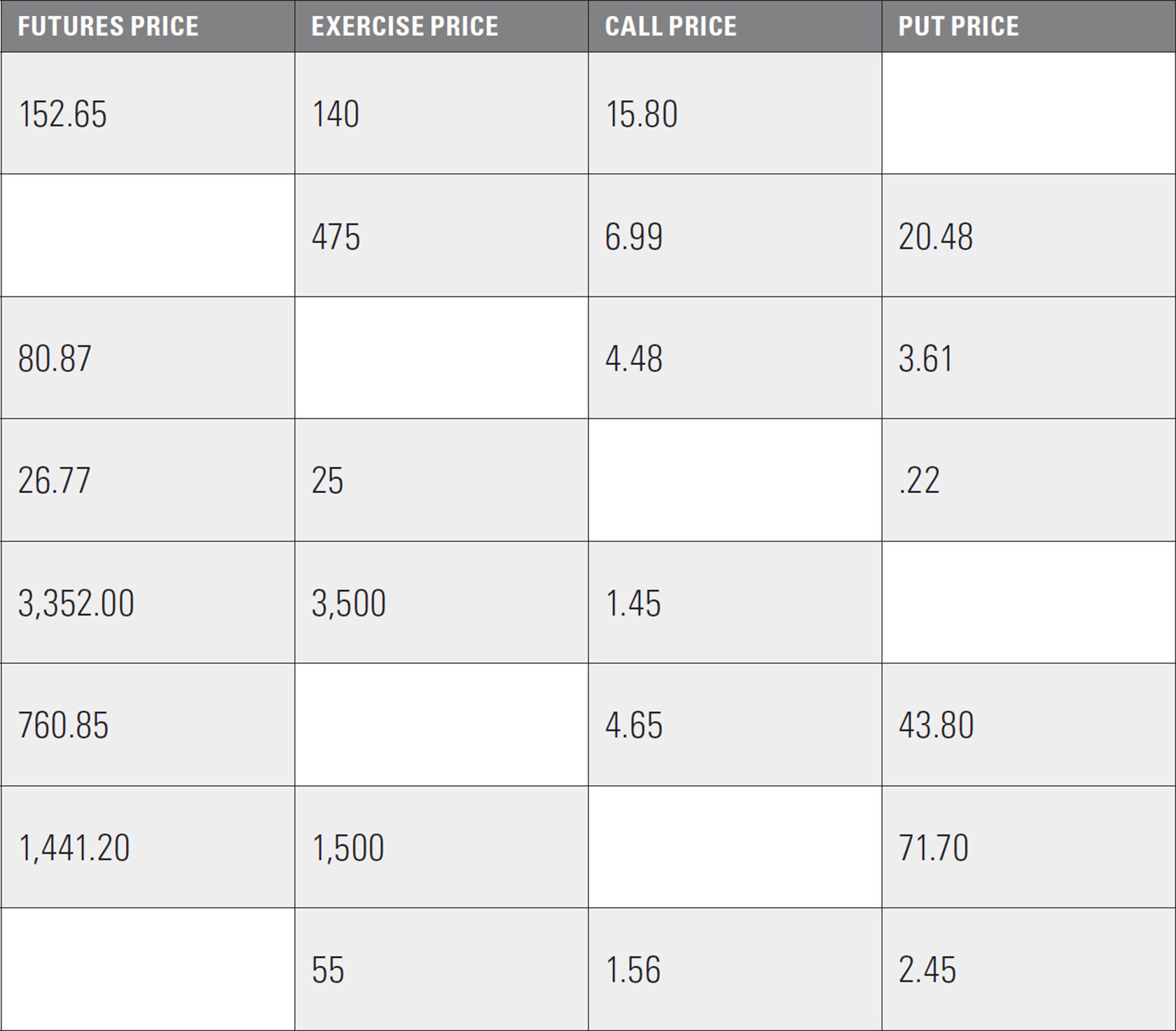

1. Options on futures; futures-type settlement (an effective interest rate of zero)

a. Fill in the missing values for options on a futures contract.

Futures price = 61.75

b. For each option below, fill in the missing value.

c.

Suppose that there are no transaction costs, but you will always have to buy at the offer price and sell at the bid price. From the bid and offer prices above, what is the best way to ...

i. buy a June futures contract?

ii. sell the June 400 call?

iii. sell the June 400 put?

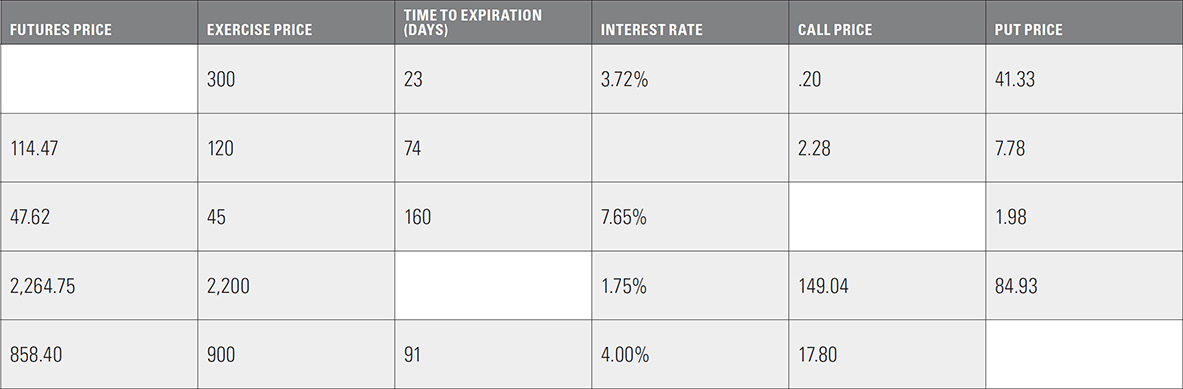

2. Options on futures; stock-type settlement

a. Fill in the missing values for options on a futures contract.

Futures price = 1,245.00

Time to expiration = 4 months

Interest rate = 6.00%

b. For each option below, fill in the missing value.

c. You have the following position:

+1 June 80 call

–1 June 80 put

–1 futures contract

If interest rates are 8.00%, using the whole number format for the delta, to the nearest .1 delta what is your total delta position if there are ...

i. 12 months to expiration?

ii. 9 months to expiration?

iii. 6 months to expiration?

iv. 3 months to expiration?

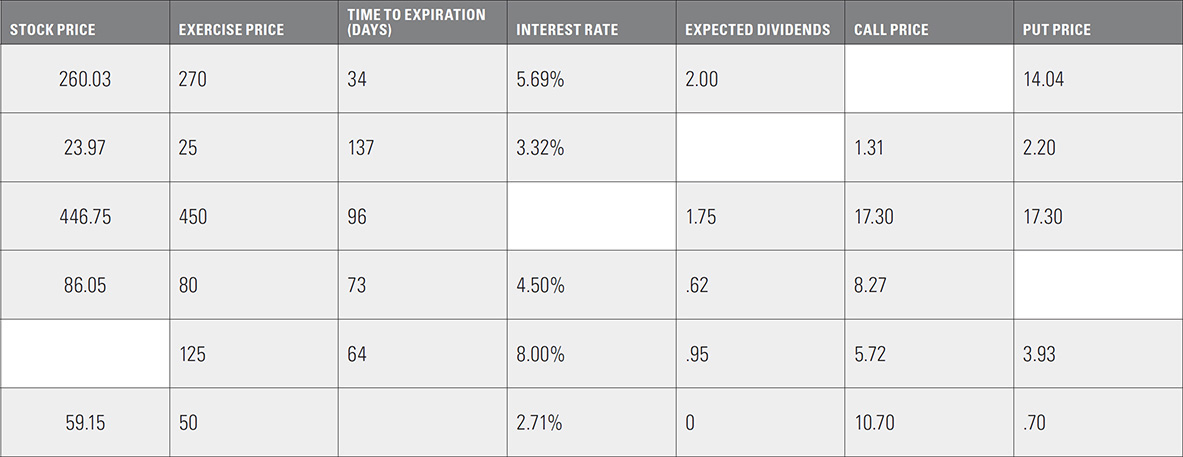

3. Options on stock

Rather than use the original form for put-call parity,

call price – put price = (forward price – exercise price) / (1 + interest rate × time)

stock option traders sometimes use this approximation in order to simplify the arithmetic:

call price – put price = stock price – exercise price + (exercise price × interest × time) – dividends

In the following questions you may use either the full form or the approximation. The approximation may result in answers slightly different than those given in the answer section.

a. Ignoring interest on dividends, fill in the missing values for options on stock.

Stock price = 150.10

Time to expiration = 2 months

Interest rate = 3.00%

Expected dividends = .85

b. For each option below, fill in the missing value.

c. You have the following position:

–1 March 80 call

+1 March 80 put

+1 stock contract

Which of the following changes in market conditions will help your position (+), which will hurt your position (–), and which will have no effect (0)?

Assume that the dividend will be paid prior to March expiration.

i. the stock price rises _______________________________________________

ii. the dividend is increased _______________________________________________

iii. implied volatility rises _______________________________________________

iv. the stock price falls _______________________________________________

v. interest rates rise _______________________________________________

vi. implied volatility falls _______________________________________________

vii. the dividend is reduced _______________________________________________

viii. interest rates fall _______________________________________________

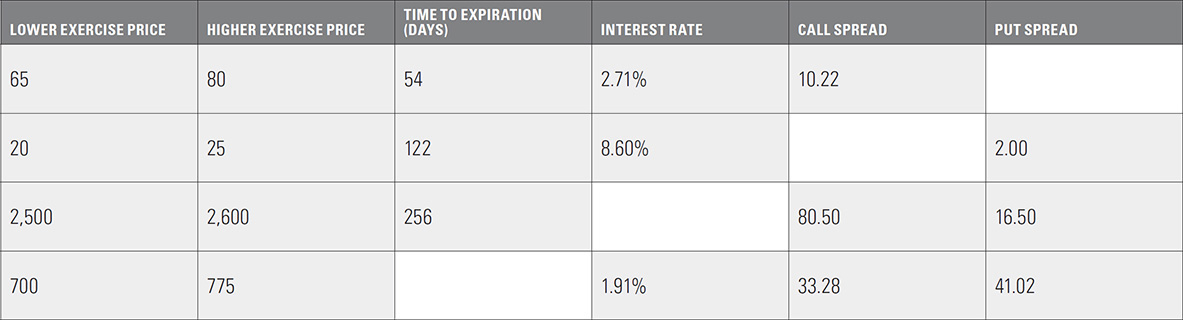

4. Boxes

A box consists of buying a synthetic underlying at one exercise price and selling a synthetic underlying at a different exercise price, where all options expire at the same time.

box value = (higher exercise price – lower exercise price) / (1 + interest rate × time)

a. If all options are subject to stock-type settlement, fill in the missing values below.

b. A box can also be thought of as the combination of a call spread and a put spread:

box value = call spread value + put spread value

If all options are subject to stock-type settlement, fill in the missing values below.

5. Rolls

A roll in the stock option market consists of buying a synthetic underlying in one expiration month and selling a synthetic underlying in a different expiration month, where all options have the same exercise price.

roll value = exercise price / (1 + interest rate × time to short-term expiration)

– exercise price / (1 + interest rate × time to long-term expiration)

– expected dividends between expirations

Rather than use the full form for the roll, stock option traders sometimes use this approximation:

roll value = exercise price × time between expirations × interest rate – expected dividends between expirations

In the following questions you may use either the full form or the approximation. The approximation may result in answers slightly different than those given in the answer section.

a. Ignoring interest on dividends, fill in the missing values below for options on stock. Assume the same interest rate applies to all expirations.

b. A roll can also be thought of as the difference between two calendar spreads:

roll value = call calendar spread value – put calendar spread value

Ignoring interest on dividends, fill in the missing values below for options on stock. Assume the same interest rate applies to all expirations.

6. From the given prices, try to fill in the missing prices for the stock options below. Assume that all options are European and fairly priced, and that the stock pays no dividend.

time to expiration = 73 days

7. The February 110 / 120 / 130 butterfly is trading at a price of 3.25. If interest rates are zero, and the February 120 straddle is trading for 9.50, what should be the price of the February 110 / 130 strangle?

8. The August 40 / 45 call spread is trading for 4.00. If interest rates are zero, and the August 40 / 45 / 55 / 60 iron condor is trading for 2.00, what should be the price of the August 50 / 55 call spread?