| CHAPTER 7 |

Risk Measurement

1. Match each risk measure with the correct definition:

2. For stock options, which risk measure can be used to estimate the sensitivity of an option’s value to a change in the dividend?

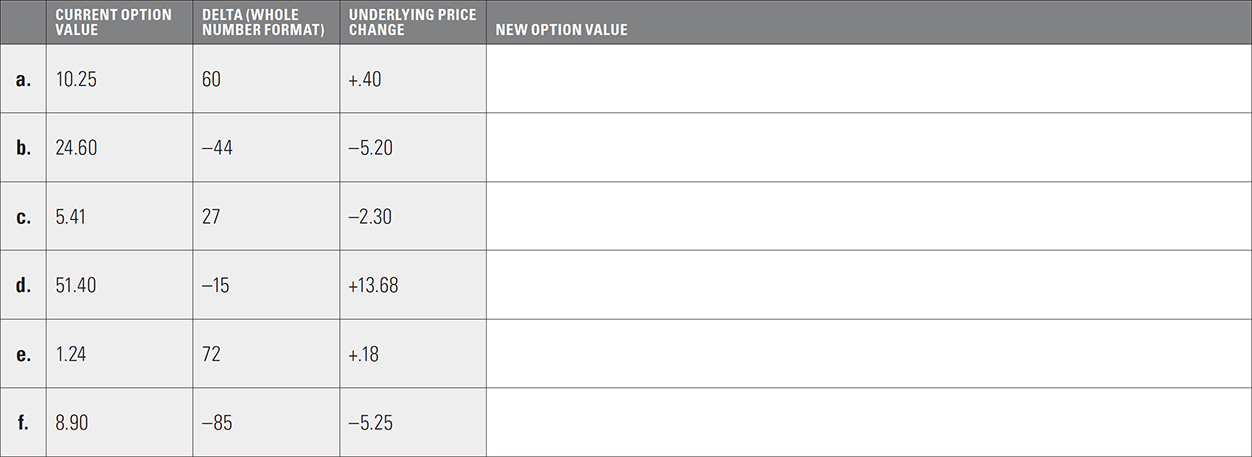

3. For each option value and delta below, to the nearest .01 estimate the option’s new value if the underlying price changes by the given amount.

Which of the above options are calls, and which are puts?

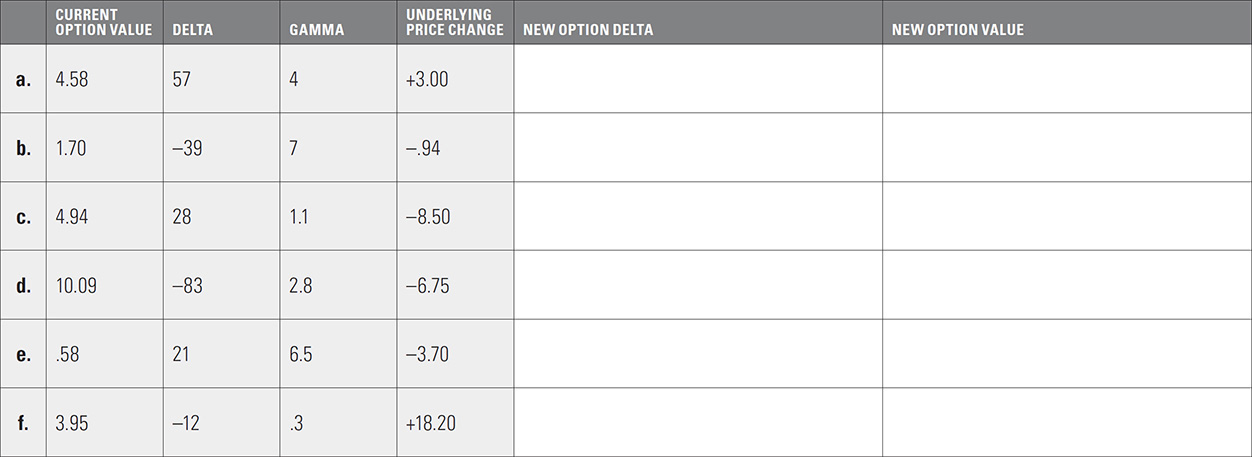

4. As the underlying price changes, the delta will change by an amount indicated by the gamma, where the gamma is expressed as the change in the delta per one point change in the underlying price. To approximate the change in an option’s value as the underlying price changes, we can use the average delta for the given price change.

For each option delta and gamma below, estimate the option’s new delta if the underlying price changes by the given amount. Then, using the option’s average delta, to the nearest .01 estimate the option’s new value if the underlying price changes by the given amount. (Delta and gamma are both given in the whole number format.)

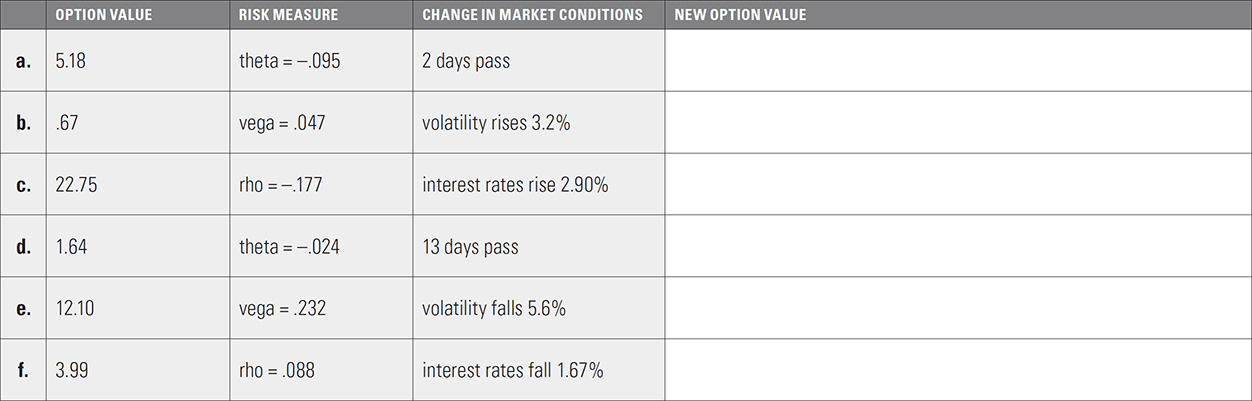

5. Theta is usually expressed as the change in an option’s value per one day’s passage of time.

Vega is usually expressed as the change in an option’s value per one percentage point change in volatility.

Rho is usually expressed as the change in an option’s value per one percentage point change in interest rates.

For each option value, risk measure, and change in market conditions below, to the nearest .01 estimate the option’s new value.

6. For each option and set of risk measures below, to the nearest .01 what will be the option’s new price if the given changes in market conditions occur?

a. current option price = 4.55

delta = 62 (whole number format)

gamma = 4.4 (whole number format)

vega = .13

The underlying price falls by 3.28 and implied volatility rises by 2.6 percentage points.

b. current option price = 8.87

theta = –.199

rho = –.135

Six days pass with no change in the underlying price and interest rates fall 1.20 percentage points (120 basis points).

c. current option price = 4.73

delta = 43 (whole number format)

vega = .217

theta = –.027

rho = .142

Four days pass, implied volatility falls 1.75 percentage points, interest rates rise .75 percentage points, and the dividend is increased by .37 (this is a stock option).

7. Complete each of the following statements:

a. A position with a positive delta wants __________________________________________

b. A position with a negative gamma wants __________________________________________

c. A position with a negative rho wants __________________________________________

d. A position with a positive vega wants __________________________________________

e. A position with a positive gamma wants __________________________________________

f. A position with a positive delta and negative gamma wants __________________________________________

8. Complete each statement below with either “increase in value” or “decline in value.”

a. If the underlying price remains unchanged, as time passes a position with a negative theta will _______________________________________________________________

b. If the underlying price remains unchanged, as time passes a position with a positive gamma will _______________________________________________________________

c. If interest rates fall, a position with a negative rho will __________________________________________

d. If implied volatility falls, a position with a negative vega will __________________________________________

e. If the underlying price makes a large move, a position with a positive theta will __________________________________________

f. If the underlying price makes a large move, a position with a positive gamma will __________________________________________

9. Fill in each blank with either “long” or “short.”

a. A trader who buys calls has a ______________ theta position.

b. A trader who sells puts has a ______________ delta position.

c. A trader who sells puts has a ______________ gamma position.

d. A trader who sells calls has a ______________ vega position.

e. A trader who buys stock option puts has a ______________ rho position.

f. A trader who sells puts has a ______________ theta position.

g. A trader who buys puts has a ______________ vega position.

h. A trader who sells stock option calls has a ______________ rho position.

i. A trader who buys calls has a ______________ gamma position.

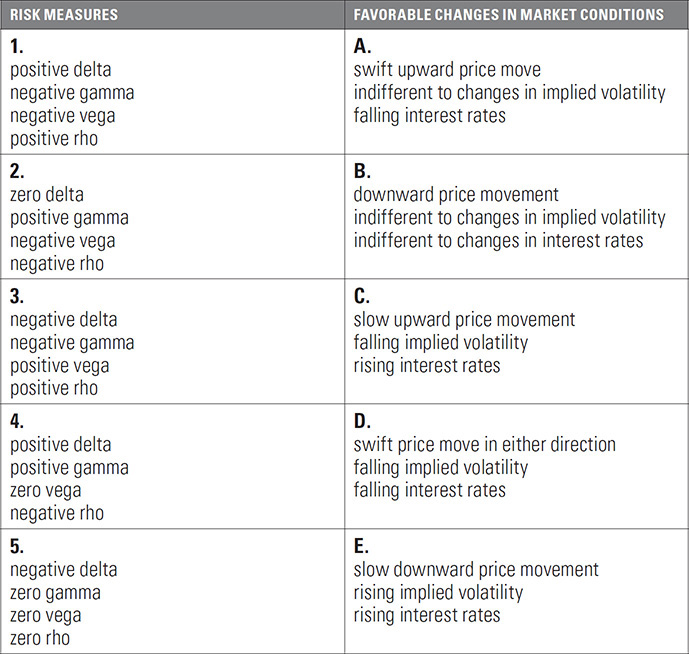

10. Match each set of risk measures below with the set of conditions that will most work in the position’s favor.

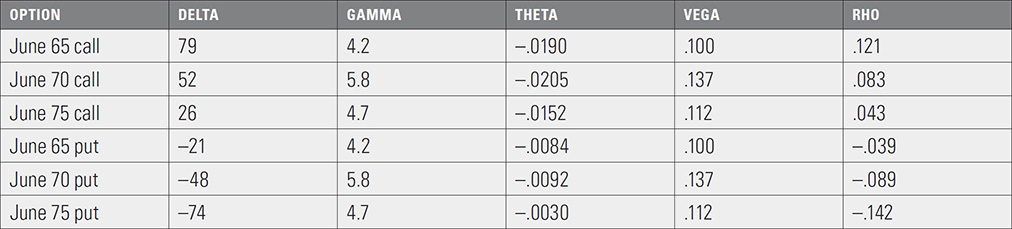

11.

From the evaluation table above, a trader has the following position:

a. What is the trader’s total ...

i. delta position? _______________________________________________________

ii. gamma position?_______________________________________________________

iii. theta position? _______________________________________________________

iv. vega position? _______________________________________________________

v. rho position? _______________________________________________________

b. Describe the changes in market conditions that will most help the position.

c. Suppose that based on your assumptions about market conditions your entire position has a positive theoretical edge of 4.65 (you expect to show a profit of 4.65). What will be your theoretical edge if all of the following occur?

the underlying price rises 3.50

three days pass

you raise your volatility estimate by 2.40 percentage points

you reduce your estimate of interest rates by .50% (50 basis points)