| CHAPTER 17 |

Models and the Real World

1. The original Black-Scholes model is based on certain assumptions, even if those assumptions may not always be realistic. For each statement below, mark the statement true (T) if it is part of the Black-Scholes framework. Mark the statement false (F) if the statement does not apply.

a. ______ The prices of the underlying contract at expiration are normally distributed.

b. ______ The prices of the underlying contract at expiration are lognormally distributed.

c. ______ The percent changes in the price of the underlying contract are normally distributed.

d. ______ The percent changes in the price of the underlying contract are lognormally distributed.

e. ______ The mean of the underlying price distribution at expiration is always equal to the current price of the underlying contract.

f. ______ The volatility of the underlying contract is constant over the life of the option.

g. ______ Interest rates are constant over the life of the option.

h. ______ Over the life of an option the volatility of the underlying contract may change, depending on which direction the market is moving.

i. ______ There is an optimal time to exercise an option early.

j. ______ The underlying contract can be bought or sold, without restriction, at any time over the life of the option.

k. ______ The price of an underlying contract follows a jump-diffusion process, with occasional gaps in the prices.

l. ______ If held to expiration, the theoretical value of an option is determined by its implied volatility.

2. For each of the statements below, fill in the blank with one of the following phrases:

less often than about equal to more often than

a. For exchange-traded contracts, small price changes (less than one standard deviation) tend to occur in the real world _____________________ a true normal distribution.

b. For exchange-traded contracts, intermediate price changes (between one and three standard deviations) tend to occur in the real world _____________________ a true normal distribution.

c. For exchange-traded contracts, large price changes (more than three standard deviations) tend to occur in the real world _____________________ a true normal distribution.

d. Suppose you know the true volatility of an underlying contract. If you use this volatility in a traditional theoretical pricing model, the value generated for a far out-of-the-money option will tend to be (choose one) lower than equal to higher than the actual value of the option in the real world.

3. A trader in a futures option market owns an at-the-money straddle. For each of the statements below, fill in the blank with one of the following phrases:

negative approximately neutral positive

a. Under the assumptions of a Black-Scholes model, the trader’s delta position is ___________________.

b. If the futures market tends to become more volatile as prices rise, the trader’s delta position is ___________________.

c. If the futures market tends to become more volatile as prices fall, the trader’s delta position is ___________________.

4. For each question below, choose the appropriate answer.

a. A gap in the price of the underlying market will have the greatest effect on the value of an

(choose one) in-the-money option at-the-money option out-of-the-money option.

b. A gap in the price of the underlying market will have a greater effect on the value of a

(choose one) long-term in-the-money option short-term in-the-money option.

c. A gap in the price of the underlying market will have a greater effect on the value of a

(choose one) long-term at-the-money option short-term at-the-money option.

d. A price gap in the underlying market will work to the benefit of

(choose one) a long option position a short option position.

e. In most option markets implied volatility derived from a traditional theoretical pricing model tends to be (choose one) lower than equal to higher than the volatility of the underlying contract.

5. Suppose a trader is using a traditional theoretical pricing model to generate option values in a certain market.

a. In order to generate values that more closely reflect the real world, which of the following is the trader most likely to do? (Choose all that apply.)

______ Vary the time to expiration used to evaluate different options, even if all options actually expire at the same time.

______ Vary the underlying price used to evaluate different options, even if all options have the same underlying contract.

______ Vary the volatility used to evaluate different options, even if all options expire at the same time and have the same underlying contract.

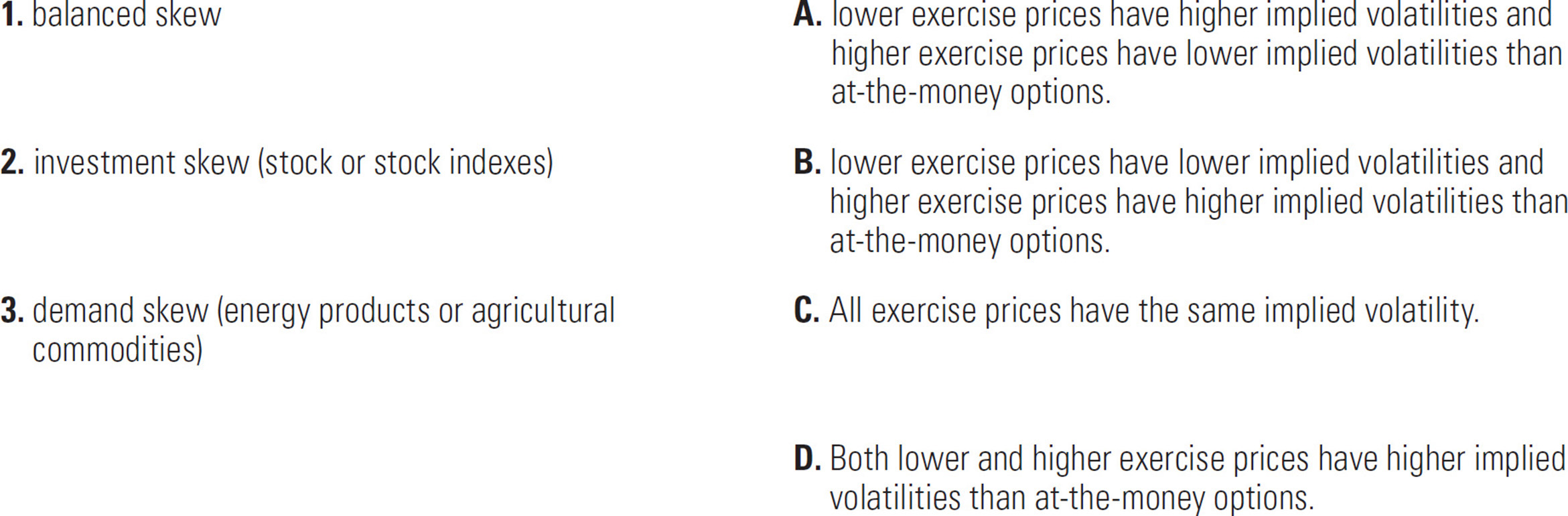

b. In a volatility skew implied volatilities vary across exercise prices, even when all options have the same underlying contract and expiration date.

Match the primary types of volatility skews below with the characteristics most commonly associated with that skew.