| CHAPTER 13 |

Early Exercise of American Options

All options have a lower arbitrage boundary. If the option is trading at a price below this lower arbitrage boundary, and there are no transaction costs, then a trader can be certain of a profit by buying the option and hedging the option position against the underlying contract.

The lower arbitrage boundary for European options:

call: maximum [forward price – exercise price) / (1 + interest rate × time),0]

put: maximum [exercise price – forward price) / (1 + interest rate × time),0]

The lower arbitrage boundary for American options:

maximum [European lower arbitrage boundary, intrinsic value]

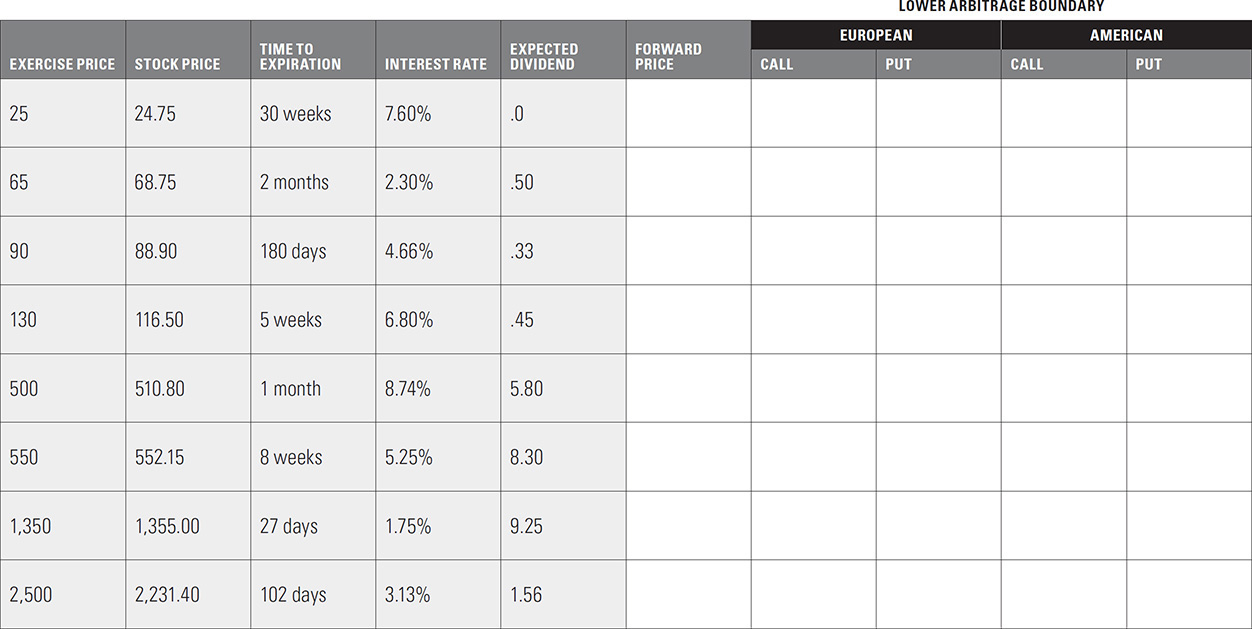

In questions 1 and 2, what are the lower arbitrage boundaries for the given options if they are both European and American? In other words, if there are no transaction costs, what is the lowest price at which the option can trade such that there is no arbitrage profit available? All calculations should be made using simple, rather than compound or continuous, interest. A year consists of 12 months, 52 weeks, or 365 days. Answers should be expressed to the nearest .01.

1. Options on futures; stock-type settlement

2. Options on stock. You can ignore interest on dividends. Assume that there are no restrictions on the short sale of stock, and that the same interest rate applies to all transactions.

b. From your answers above, do you think the following statements are true or false?

i. If the lower arbitrage boundary for a European stock option call is a positive value, the lower arbitrage boundary for a European stock option put with the same exercise price and expiration date must be zero.

ii. If the lower arbitrage boundary for an American stock option call is a positive value, the lower arbitrage boundary for an American stock option put with the same exercise price and expiration date must be zero.

c. Under what conditions will the lower arbitrage boundaries for a European call and put with the same exercise price and expiration date both be zero?

d. Using your answers to question 2a above, suppose you are able to buy the 90 put for .85.

i. If the option is American, what can you do to ensure a profit?

ii. If you take the appropriate action, what will be your total profit?

e. Using your answers to question 2a above, suppose you are able to buy the 25 call for .60.

i. If the option is European, what can you do to ensure a profit?

If you take the appropriate action, what will be your total profit at expiration if ...

ii. the stock price at expiration is 30?

iii. the stock price at expiration is 20?

3. Options on futures

For a futures option to be an early exercise candidate, the option must be subject to stock-type settlement. In addition, the following must also hold true over the entire life of the option, as well as over the next day:

interest earned through early exercise > volatility value.

where

the interest that can be earned is the interest on the option’s intrinsic value.

the volatility value over the life of the option is approximately equal to the price of the companion out-of-the-money option.

the volatility value over the next day is approximately equal to the theta of the companion out-of-the-money option.

Futures price = 1,325.00

time to March expiration = 26 days

interest rate = 6.00%

You own a March 1200 call that can be exercised early. All options are subject to stock-type settlement.

a. What must be the price of the March 1200 put in order for the March 1200 call to be an early exercise candidate? Why?

b. What must be the daily theta of the March 1200 put for you to want to exercise the March 1200 call right now?

4. Call options on stock

For a stock option call to be an early exercise candidate, the following must hold true over the entire life of the option, as well as over the next day:

dividend > interest cost + volatility value

where

the interest cost is equal to exercise price × interest rate × time.

the volatility value over the life of the option is approximately equal to the price of the companion out-of-the-money option. The volatility value over the next day is approximately equal to the theta of the companion out-of-the-money option.

stock price = 60.00

time to May expiration = 35 days

interest rate = 4.00%

dividend = .50, payable in 15 days

You own a May 50 call that can be exercised early.

a. Suppose there are only two choices, exercise now or hold the option to expiration. If the May 50 put is trading at a price of .20, which choice is best? Why?

b. If this is a true American call, allowing for exercise at any time prior to expiration, when will you optimally decide whether to exercise the option?

c. If the stock price remains unchanged at 60, on the day you must optimally decide whether to exercise the option, at what price must the May 50 put be trading in order for you to exercise the May 50 call?

d. If you decide to exercise the May 50 call but want the same protective characteristics offered by the May 50 call, what should you do?

e. If you take the appropriate action in question 4d, how much better off will you be with your new position than if you had not exercised the May 50 call?

5. Put options on stock

In the following questions ignore any short stock considerations.

For a stock option put to be an early exercise candidate, the following must hold true over the entire life of the option, as well as over the next day:

interest earned > dividend + volatility value

where

the interest earned is equal to exercise price × interest rate × time.

the volatility value over the life of the option is approximately equal to the price of the companion out-of-the-money option. The volatility value over the next day is approximately equal to the theta of the companion out-of-the-money option.

The “blackout period” for a stock option put is the period prior to the payment of the dividend when it is not possible to earn enough interest through early exercise to offset the loss of the dividend.

stock price = 82.50

time to July expiration = 54 days

interest rate = 5.00%

dividend = .25

You own a July 95 put that can be exercised early.

a. What is the blackout period, in days, for this option? (Within what number of days prior to the dividend payment would you never consider exercising the July 95 put?)

b. If there are 37 days until the dividend payment, at what price must the July 95 call be trading for you to consider immediate early exercise of the July 95 put?

c. In addition to the price of the July 95 call, what must be the daily theta of the July 95 call for immediate exercise of the July 95 put to be optimal?

d. If the daily theta of the July 95 call is .015 (in absolute value), would you exercise the July 95 put now?

e. If there are 10 days until the dividend payment date, at what price must the July 95 call be trading for you to want to immediately exercise the July 95 put?

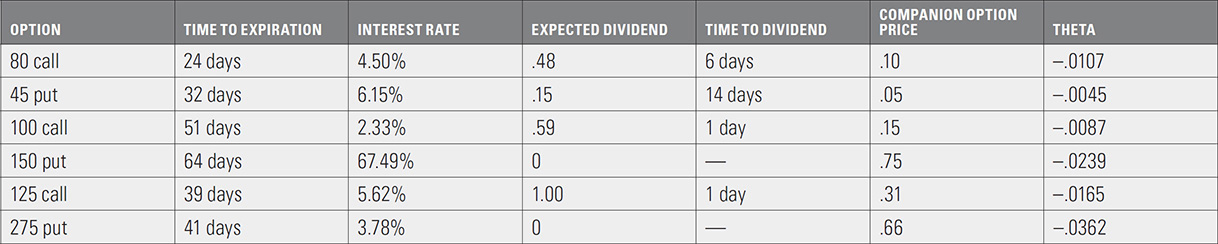

6. Assuming that each of the stock options below is in-the-money, which of the options should be exercised immediately?

a. 80 call?

b. 45 put?

c. 100 call?

d. 150 put?

e. 125 call?

f. 275 put?

7. A stock that is currently trading at a price of 61.00 is expected to pay a dividend of .75 approximately 10 weeks prior to option expiration. If interest rates are 8.00% what can you say about the likelihood of the 50 call being exercised early?

8. a. You are considering early exercise of an option. Would you be more likely to exercise the option early if implied volatility rises, implied volatility remains unchanged, or implied volatility falls?

b. Assume that you will earn less interest on a short stock position than the normal prevailing interest rate.

i. You are considering early exercise of a stock option call. Would you be more likely to exercise the call early if you currently are long stock, have no stock position, or are short stock?

ii. You are considering early exercise of a stock option put. Would you be more likely to exercise the put early if you currently are long stock, have no stock position, or are short stock?

9. In this question, ignore any short stock considerations.

Consider a June 150 /175 box under the following conditions:

time to June expiration = 38 days

interest rate = 7.50%

dividend = 1.15

time to dividend payment = 16 days

a. What should be the minimum value of the box? Under what market conditions is this likely to occur?

b. What should be the value of the box if both the June 150 call and the June 175 call should optimally be exercised early? Under what conditions is this likely to occur?

c. What should be the value of the box if both the June 150 put and the June 175 put should optimally be exercised early?

d. What should be the value of the box if only the June 150 call should optimally be exercised early?

e. What should be the value of the box if only the June 175 put should optimally be exercised early?

f. What should be the value of the box if both the June 150 call and the June 175 put should optimally be exercised early? Under what market conditions is this likely to occur?