In Chapter 2, we introduced the concept of data import and exploration techniques. Now you are equipped with loading data from different sources and storing them in an appropriate format. In this chapter we will discuss important data sampling methodologies and their importance in machine learning algorithms. Sampling is an important block in our machine learning process flow and it serves the dual purpose of cost savings in data collection and reduction in computational cost without compromising the power of the machine learning model.

“An approximate answer to the right problem is worth a good deal more than an exact answer to an approximate problem.”

—John Tukey

John Tukey statement fits well into the spirit of sampling. As the technological advancement brought large data storage capabilities, the incremental cost of applying machine learning techniques is huge. Sampling helps us balance between the cost of processing high volumes of data with marginal improvement in the results. Contrary to the general belief that sampling is useful only for reducing a high volume of data to a manageable volume, sampling is also important to improve statistics garnered from small samples. In general, machine learning deals with huge volumes of data, but concepts like bootstrap sampling can help you get insight from small sample situations as well.

The learning objectives of this chapter are as follows:

Introduction to sampling

Sampling terminology

Non-probability sampling and probability sampling

Business implication of sampling

Statistical theory on sample statistics

Introduction to resampling

Monte Carlo method: Acceptance-Rejection sampling

Computational time saving illustration

Different sampling techniques will be illustrated using the credit card fraud data introduced in Chapter 2.

3.1 Introduction to Sampling

Sampling is a process that selects units from a population of interest, in such a way that the sample can be generalized for the population with statistical confidence. For instance, if an online retailer wanted to know the average ticket size of an online purchase over the last 12 months, we might not want to average the ticket size over the population (which may run into millions of data points for big retailers), but we can pick up a representative sample of purchases over last 12 months and estimate the average for the sample. The sample average then can be generalized for the population with some statistical confidence. The statistical confidence will vary based on the sampling technique used and the size.

In general, sampling techniques are applied to two scenarios, for creating manageable dataset for modeling and for summarizing population statistics . This broad categorization can be presented as objectives of sampling:

Model sampling

Survey sampling

Model samplingis done when the population data is already collected and you want to reduce time and the computational cost of analysis, along with improve the inference of your models. Another approach is to create a sample design and then survey the population only to collect sample to save data collection costs. Figure 3-1 shows the two business objectives of sampling. The sample survey design and evaluation are out of scope of this book, so will keep our focus on model sampling alone.

Figure 3-1. Objectives of sampling

This classification is also helpful in identifying the end objectives of sampling. This helps in choosing the right methodology for sampling and the right exploratory technique. In the context of the machine learning model building flow, our focus will be around model sampling. The assumption is that the data has already been collected and our end objective is to garner insight from that data, rather than develop a systematic survey to collect it.

3.2 Sampling Terminology

Before we get into details of sampling, let’s define some basic terminology of sampling that we will be using throughout the book. The statistics and probability concepts discussed in Chapter 1 will come handy in understanding the sampling terminology. This section lists the definition and mathematical formulation in sampling.

3.2.1 Sample

A sample is a set of units or individuals selected from a parent population to provide some useful information about the population. This information can be general shape of distribution, basic statistics, properties of population distribution parameters, or information of some higher moments. Additionally, the sample can be used to estimate test statistics for hypothesis testing. A representative sample can be used to estimate properties of population or to model population parameters.

For instance, the National Sample Survey Organization (NNSO) collects sample data on unemployment by reaching out to limited households, and then this sample is used to provide data for national unemployment.

3.2.2 Sampling Distribution

The distribution of the means of a particular size of samples is called the sampling distribution of means; similarly the distribution of the corresponding sample variances is called the sampling distribution of the variances. These distributions are the fundamental requirements for performing any kind of hypothesis testing.

3.2.3 Population Mean and Variance

Population mean is the arithmetic average of the population data. All the data points contribute toward the population mean with equal weight. Similarly, population variance is the variance calculated using all the data points in the data.

Population mean:

Population Variance: ![]()

3.2.4 Sample Mean and Variance

Any subset you draw from the population is a sample. The mean and variance obtained from that sample are called sample statistics. The concept of degrees of freedom is used when a sample is used to estimate distribution parameters; hence, you will see for sample variance that the denominator is different than the population variance.

Sample mean: ![]()

Sample variance

: ![]()

3.2.5 Pooled Mean and Variance

For k sample of size n1, n2, n3, …, nk taken from the same population, the estimated population mean and variance are defined as follows.

Estimated population mean:

Estimated population variance:

In real-life situations, we usually can have multiple samples drawn from the same population at different points in space/location and time. For example, assume we have to estimate average income of bookshop owner in a city. We will get samples of bookshop owners’ income from different parts of city at different points in time. At a later point of time, we can combine the individual mean and variance from different samples to get an estimate for population using pooled mean and variance.

3.2.6 Sample Point

A possible outcome in a sampling experiment is called a sample point. In many types of sampling, all the data points in the population are not sample points.

Sample points are important when the sampling design becomes complex. The researcher may want to leave some observations out of sampling, alternatively the sampling process by design itself can give less probability of selection to the undesired data point. For example, suppose you have gender data with three possible values—Male, Female, and Unknown. You may want to discard all Unknowns as an error, this is keeping the observation out of sampling. Otherwise, if the data is large and the Unknowns are a very small proportion then the probability to sample them is negligible. In both cases, Unknown is not a sample point.

3.2.7 Sampling Error

The difference between the true value of a population statistic and the sample statistic is the sampling error. This error is attributed to the fact that the estimate has been obtained from the sample.

For example, suppose you know by census data that monthly average income of residents in Boston is $3,000 (the population mean). So, we can say that true mean of income is $3,000. Let’s say that a market research firm performed a small survey of residents in Boston. We find that the sample average income from this small survey is $3,500. The sampling error is then $3,500 - $3,000, which equals $500. Our sample estimates are over-estimating the average income, which also points to the fact that the sample is not a true representation of the population.

3.2.8 Sampling Fraction

The sampling fraction is the ratio of sample size to population size, ![]() .

.

For example, if your total population size is 500,000 and you want to draw a sample of 2,000 from the population, the sampling fraction would be f = 2,000/50,000 = 0.04. In other words, 4% of population is sampled.

3.2.9 Sampling Bias

Sampling bias occurs when the sample units from the population are not characteristic of (i.e., do not reflect) the population. Sampling bias causes a sample to be unrepresentative of the population.

Connecting back to example from sampling error, we found out that the sample average income is way higher than the census average income (true average). This means our sampling design has been biased toward higher income residents of Boston. In that case, our sample is not a true representation of Boston residents.

3.2.10 Sampling Without Replacement (SWOR)

Sampling without replacement requires two conditions to be satisfied;

Each unit/sample point has a finite non-zero probability of selection

Once a unit is selected, it is removed from the population

In other words, all the units have some finite probability of being sampled strictly only once.

For instance, if we have a bag of 10 balls, marked with numbers 1 to 10, then each ball has selection probability of 1/10 in a random sample done without replacement. Suppose we have to choose three balls from the bag, then after each selection the probability of selection increases as number of balls left in bag decreases. So, for the first ball the probability of getting selected is 1/10, for the second it’s 1/9, and for the third it’s 1/8.

3.2.11 Sampling with Replacement (SWR)

Sampling with replacement differs from SWOR by the fact that a unit can be sampled more than once in the same sample. Sampling with replacement requires two conditions to be satisfied;

Each unit/sample point has a finite non-zero probability of selection

A unit can be selected multiple times, as the sampling population is always the same

In sampling without replacement, the unit can be sampled more than once and each time has the same probability of getting sampled. This type of sampling virtually expands the size of population to infinity as you can create as many samples of any size from this method Connecting back to our previous example in SWOR, if we have to choose three balls with SWR, each ball will have the exact same finite probability of 1/10 for sampling.

The important thing to note here is sampling with replacement technically makes the population size infinite. Be careful while choosing SWR as in most cases each observation is unique and counting it multiple times creates bias in your data. Essentially it will mean you are allowing a repetition of observation. For example, 100 people having the same name, income, age, and gender in the sample will create bias in the dataset.

3.3 Credit Card Fraud: Population Statistics

The credit card fraud dataset is a good example of how to build a sampling plan for machine learning algorithms. The dataset is huge, with 10 million rows and multiple features. This section will show you how the key sampling measure of population can be calculated and interpreted for this dataset. The following statistical measures will be shown:

Population mean

Population variance

Pooled mean and variance

To explain these measures, we chose the outstanding balance feature as the quantity of interest.

3.3.1 Data Description

A quick recap from Chapter 2 to describe the following variables in the credit card fraud data,

custID: A unique identifier for each customer

gender: Gender of the customer

state: State in the United States where the customer lives

cardholder: Number of credit cards the customer holds

balance: Balance on the credit card

numTrans: Number of transactions to date

numIntlTrans: Number of international transactions to date

creditLine: The financial services corporation, such as Visa, MasterCard, or American Express

fraudRisk: Binary variable, 1 means customer being frauded, 0 means otherwise

str(data)Classes 'data.table' and 'data.frame': 10000000 obs. of 14 variables:$ creditLine : int 1 1 1 1 1 1 1 1 1 1 ...$ gender : int 1 1 1 1 1 1 1 1 1 1 ...$ state : int 1 1 1 1 1 1 1 1 1 1 ...$ CustomerID : int 4446 59161 136032 223734 240467 248899 262655 324670 390138 482698 ...$ NumOfCards : int 1 1 1 1 1 1 1 1 1 1 ...$ OutsBal : int 2000 0 2000 2000 2000 0 0 689 2000 0 ...$ DomesTransc: int 31 25 78 11 40 47 15 17 48 25 ...$ IntTransc : int 9 0 3 0 0 0 0 9 0 35 ...$ FraudFlag : int 0 0 0 0 0 0 0 0 0 0 ...$ State : chr "Alabama" "Alabama" "Alabama" "Alabama" ...$ PostalCode : chr "AL" "AL" "AL" "AL" ...$ Gender : chr "Male" "Male" "Male" "Male" ...$ CardType : chr "American Express" "American Express" "American Express" "American Express" ...$ CardName : chr "SimplyCash® Business Card from American Express" "SimplyCash® Business Card from American Express" "SimplyCash® Business Card from American Express" "SimplyCash® Business Card from American Express" ...- attr(*, ".internal.selfref")=<externalptr>- attr(*, "sorted")= chr "creditLine"

As stated earlier, we chose outstanding balance as the variable/feature of interest. In the str() output for data descriptive, we can see the outstanding balance is stored in a variable named OutsBal, which is of type integer. Being a continuous variable, mean and variance can be defined for this variable.

3.3.2 Population Mean

Mean is a more traditional statistic for measuring the central tendency of any distribution of data. The mean outstanding balance of our customers in the credit card fraud dataset turns out to be $4109.92. This is our first understanding about the population. Population mean tells us that on average, the customers have an outstanding balance of $4109.92 on their cards.

Population_Mean_P <-mean(data$OutsBal)cat("The average outstanding balance on cards is ",Population_Mean_P)The average outstanding balance on cards is 4109.92

3.3.3 Population Variance

Variance is a measure of spread for the given set of numbers. The smaller the variance, the closer the numbers are to the mean and the larger the variance, the farther away the numbers are from the mean. For the outstanding balance, the variance is 15974788 and standard deviation is 3996.8. The variance by itself is not comparable across different populations or samples. Variance is required to be seen along with mean of the distribution. Standard deviation is another measure and it equals the square root of the variance.

Population_Variance_P <-var(data$OutsBal)cat("The variance in the average outstanding balance is ",Population_Variance_P)The variance in the average outstanding balance is 15974788cat("Standard deviation of outstanding balance is", sqrt(Population_Variance_P))Standard deviation of outstanding balance is 3996.847

3.3.4 Pooled Mean and Variance

Pooled mean and variance estimate population mean and variance when multiple samples are drawn independently of each other. To illustrate the pooled mean and variance compared to true population mean and variance, we will first create five random samples of size 10K, 20K, 40K, 80K, and 100K and calculate their mean and variance.

Using these samples, we will estimate the population mean and variance by using pooled mean and variance formula. Pooled values are useful because estimates from a single sample might produce a large sampling error, whereas if we draw many samples from the same population, the sampling error is reduced. The estimate in a collective manner will be closer to the true population statistics.

Note

As the sampling fraction is low for the various sample sizes, (for 100K sample size f = 100000/10000000 = 1/100) is too large. The variance will not be impacted by the degrees of freedom correction by 1, so we can safely use the var() function in R for sample variance.

In the following R snippet, we are creating five random samples using the sample() function. sample() is an built-in function that’s been used multiple times in the book. Another thing to note is that the sample() function works with some random seed values, so if you want to create reproducible code, use the set.seed(937) function in R. This will make sure that each time you run the code, you get the same random sample.

set.seed(937)i<-1n<-rbind(10000,20000,40000,80000,100000)Sampling_Fraction<-n/nrow(data)sample_mean<-numeric()sample_variance<-numeric()for(i in 1:5){sample_100K <-data[sample(nrow(data),size=n[i], replace =FALSE, prob =NULL),]sample_mean[i]<-round(mean(sample_100K$OutsBal),2)sample_variance[i] <-round(var(sample_100K$OutsBal),2)}Sample_statistics <-cbind (1:5,c('10K','20K','40K','80K','100K'),sample_mean,sample_variance,round(sqrt(sample_variance),2),Sampling_Fraction)knitr::kable(Sample_statistics, col.names =c("S.No.", "Size","Sample_Mean","Sample_Variance","Sample SD","Sample_Fraction"))

In Table 3-1, basic properties of the five samples are presented. The highest sample fraction is for the biggest sample size. A good thing to notice is that, as the sample size increases, the sample variance gets smaller.

Table 3-1. Sample Statistics

S.No. | Size | Sample_Mean | Sample_Variance | Sample SD | Sample_Fraction |

|---|---|---|---|---|---|

1 | 10K | 4092.48 | 15921586.32 | 3990.19 | 0.001 |

2 | 20K | 4144.26 | 16005696.09 | 4000.71 | 0.002 |

3 | 40K | 4092.28 | 15765897.18 | 3970.63 | 0.004 |

4 | 80K | 4127.18 | 15897698.44 | 3987.19 | 0.008 |

5 | 100K | 4095.28 | 15841598.06 | 3980.15 | 0.01 |

Now let’s use the pooled mean and variance formula to calculate the population mean from the five samples we drew from the population and then compare them with population mean and variance.

i<-1Population_mean_Num<-0Population_mean_Den<-0for(i in 1:5){Population_mean_Num =Population_mean_Num +sample_mean[i]*n[i]Population_mean_Den =Population_mean_Den +n[i]}Population_Mean_S<-Population_mean_Num/Population_mean_Dencat("The pooled mean ( estimate of population mean) is",Population_Mean_S)The pooled mean ( estimate of population mean) is 4108.814

The pooled mean is $4,108.814. Now we apply this same process to calculate the pooled variance from the samples. Additionally, we will show the standard deviation as an extra column to make dispersion comparable to the mean measure.

i<-1Population_variance_Num<-0Population_variance_Den<-0for(i in 1:5){Population_variance_Num =Population_variance_Num +(sample_variance[i])*(n[i] -1)Population_variance_Den =Population_variance_Den +n[i] -1}Population_Variance_S<-Population_variance_Num/Population_variance_DenPopulation_SD_S<-sqrt(Population_Variance_S)cat("The pooled variance (estimate of population variance) is", Population_Variance_S)The pooled variance (estimate of population variance) is 15863765cat("The pooled standard deviation (estimate of population standard deviation) is", sqrt(Population_Variance_S))The pooled standard deviation (estimate of population standard deviation) is 3982.934

The pooled standard deviation is $3,982.934. Now we have both pooled statistics and population statistics. Here, we create a comparison between the two and see how well the pooled statistics estimated the population statistics:

SamplingError_percent_mean<-round((Population_Mean_P -sample_mean)/Population_Mean_P,3)SamplingError_percent_variance<-round((Population_Variance_P -sample_variance)/Population_Variance_P,3)Com_Table_1<-cbind(1:5,c('10K','20K','40K','80K','100K'),Sampling_Fraction,SamplingError_percent_mean,SamplingError_percent_variance)knitr::kable(Com_Table_1, col.names =c("S.No.","Size","Sampling_Frac","Sampling_Error_Mean(%)","Sampling_Error_Variance(%)"))

Table 3-2 shows the comparison of the population mean and the variance against each individual sample. The bigger the sample, the closer the mean estimate to the true population estimate.

Table 3-2. Sample Versus Population Statistics

S.No. | Size | Sampling_Frac | Sampling_Error_Mean(%) | Sampling_Error_Variance(%) |

|---|---|---|---|---|

1 | 10K | 1000 | 0.004 | 0.003 |

2 | 20K | 500 | -0.008 | -0.002 |

3 | 40K | 250 | 0.004 | 0.013 |

4 | 80K | 125 | -0.004 | 0.005 |

5 | 100K | 100 | 0.004 | 0.008 |

Create a same view for pooled statistics against the population statistics. The difference is expressed as a percentage of differences among pooled/sample to the true population statistics.

SamplingError_percent_mean<-(Population_Mean_P -Population_Mean_S)/Population_Mean_PSamplingError_percent_variance<-(Population_Variance_P -Population_Variance_S)/Population_Variance_PCom_Table_2 <-cbind(Population_Mean_P,Population_Mean_S,SamplingError_percent_mean)Com_Table_3 <-cbind(Population_Variance_P,Population_Variance_S,SamplingError_percent_variance)knitr::kable(Com_Table_2)

Table 3-3. Population Mean and Sample Mean Difference

Population_Mean_P | Population_Mean_S | SamplingError_percent_mean |

|---|---|---|

4109.92 | 4108.814 | 0.000269 |

knitr::kable(Com_Table_3)Table 3-4. Population Variance and Sample Variance

Population_Variance_P | Population_Variance_S | SamplingError_percent_variance |

|---|---|---|

15974788 | 15863765 | 0.0069499 |

Pooled mean is close to the true mean of the population. This shows that given multiple sample the pooled statistics are more likely to capture true statistics values. You have now seen how a sample so small in size when compared to population gives you estimates so close to the population estimate.

Does this example give you a tool of dealing with big data by using small samples from them? By now you might have started thinking about the cost-benefit analysis of using sampling. This is very relevant to machine learning algorithms churning millions of data points. More data points does not necessarily mean all of them contain meaningful patterns/trends/information. Sampling will try to save you from weeds and help you focus on meaningful datasets for machine learning.

3.4 Business Implications of Sampling

Sampling is applied at multiple stages of model development and decision making. Sampling methods and interpretation are driven by business constraints and statistical methods chosen for inference testing. There is a delicate balance set by data scientists between the business implications and how statistical results stay valid and relevant. Most of the time, the problem is given by business and data scientists have to work in a targeted manner to solve the problem.

For instance, suppose the business wants to know why customers are not returning to their web site. This problem will dictate the terms of sampling. To know why customers are not coming back, do you really need a representative sample of whole population of your customers? Or you will just take a sample of customers who didn’t return? Or rather you would like to only study a sample of customers who return and negate the results? Why not create a custom mixed bag of all returning and not returning customers? As you can observe, lot of these questions, along with practical limitations on time, cost, computational capacity, etc. will be deciding factors on how to go about gathering data for this problem.

In general, the scenarios listed next are salient features of sampling and some shortcomings that need to be kept in mind while using sampling in your machine learning model building flow

3.4.1 Features of Sampling

Scientific in nature

Optimizes time and space constraints

Reliable method of hypothesis testing

Allows in-depth analysis by reducing cost

In cases where population is very large and infrastructure is a constraint, sampling is the only way forward

3.4.2 Shortcomings of Sampling

Sampling bias can cause wrong inference

Representative sampling is always not possible due to size, type, requirements, etc.

It is not exact science but an approximation within certain confidence limits

In sample survey, we have issues of manual errors, inadequate response, absence of informants, etc.

3.5 Probability and Non-Probability Sampling

The sampling methodology largely depends on what we want to do with the sample. Whether we want to generate a hypothesis about population parameters or want to test a hypothesis We classify sampling method into two major buckets—probability sampling and non-probability sampling. The comparison in Figure 3-2 provides the high-level differences between them.

Figure 3-2. Probability versus non-probability sampling

In probability sampling, the sampling methods draws each unit with some finite probability. The sampling frame that maps the population unit to sample unit is created based on the probability distribution of the random variable utilized for sampling. These types of methods are commonly used for model sampling, and have high reliability to draw population inference. They eliminate bias in parameter estimation and can be generalized to the population. Contrary to non-probability sampling, we need to know the population beforehand to sample from. This makes this method costly and sometimes difficult to implement.

Non-probability sampling is sampling based on subjective judgment of experts and business requirements. This is a popular method where the business needs don’t need to align with statistical requirements or it is difficult to create a probability sampling frame. The non-probability sampling method does not assign probability to population units and hence it becomes highly unreliable to draw inferences from the sample. Non-probability sampling have bias toward the selected classes as the sample is not representative of population. Non-probability methods are more popular with exploratory research for new traits of population that can be tested later with more statistical rigor. In contrast to probability techniques, it is not possible to estimate population parameters with accuracy using non-probability techniques.

3.5.1 Types of Non-Probability Sampling

In this section, we briefly touch upon the three major types of non-probability sampling methods. As these techniques are more suited for survey samples, we will not discuss them in detail.

3.5.1.1 Convenience Sampling

In convenience sampling, the expert will choose the data that is easily available. This technique is the cheapest and consumes less time. For our case, suppose that the data from New York is accessible but for other states, the data is not readily accessible so we choose data from one sate to study whole United States. The sample would not be a representative sample of population and will be biased. The insights also cannot generalized to the entire population. However, the sample might allow us to create some hypothesis that can later be tested using random samples from all the states.

3.5.1.2 Purposive Sampling

When the sampling is driven by the subjective judgment of the expert, it’s called purposive sampling. In this method the expert will sample those units which help him establish the hypothesis he is trying to test. For our case, if the researcher is only interested in looking at American Express cards, he will simply choose some units from the pool of records from that card type. Further, there are many types of purposive sampling methods, e.g., maximum variance sampling, extreme case sampling, homogeneous sampling etc. but these are not discussed in this book, as they lack representativeness of population which is required for unbiased machine learning methods.

3.5.1.3 Quota Sampling

As the name goes, quota sampling is based on a prefixed quota for each type of cases, usually the quota decided by an expert. Fixing a quota grid for sampling ensures equal or proportionate representation of subjects being sampled. This technique is popular in marketing campaign design, A/B testing, and new feature testing.

In this chapter we cover sampling methods with examples drawn from our credit card fraud data. We encourage you to explore more non-probability sampling in context of the business problem at your disposal. There are times when experience can beat statistics, so non-probability sampling is equally important in many use cases.

3.6 Statistical Theory on Sampling Distributions

Sampling techniques draw their validity from well-established theorems and time-tested methods from statistics. For studying sampling distribution, we need to understand two important theorems from statistics:

Law of Large Numbers

Central Limit Theorem

This section explains these two theorems with some simulations.

3.6.1 Law of Large Numbers : LLN

In general, as the sample size increases in a test, we expect the results to be more accurate, having smaller deviations in the expected outcomes. The law of large numbers formalizes this with help of the probability theory. The first notable reference to this concept was given by Italian mathematician Gerolamo Cardano in the 16th century, when he observed and stated that empirical statistics get closer to their true value as the number of trials increases.

In later years, a lot of work was done to get different form of the Law of Large Numbers. The example we are going to discuss for a coin toss was first proved by Bernoulli and later he provided proof of his observations. Aleksander Khinchin provided the most popular statement for the Law of Large Numbers, also called the weak law of large numbers. The weak law of large number is alternatively called the law of averages.

3.6.1.1 Weak Law of Large Numbers

In probability space, the sample average converges to an expected value as the sample size trends to infinity. In other words, as the number of trials or sample size grows, the probability of getting close to the true average increases. The weak law is also called Khinchin’s Law to recognize his contribution.

The weak law of large numbers states that the sample averages converge in probability toward the expected value, ![]()

Alternatively, for any positive number ∈

![]()

3.6.1.2 Strong Law of Large Numbers

It is important to understand the subtle difference between the weak and strong law of large numbers. The strong law of large numbers states that the sample average will converge to true average by probability 1, while the weak law only states that they will converge. Hence, the strong law is more powerful to state while estimating population mean by sample means.

The strong law of large numbers states that the sample average converges almost surely to the expected value ![]()

Equivalent to

![]()

Note

There are multiple representations and proofs for the Law of Large Numbers. You are encouraged to refer to any graduate level text of probability to learn more.

Without getting into the statistical details of this theorem, we will set up an example to understand. Consider a coin toss example whereby a coin toss outcome follows a binomial distribution.

Suppose you have a biased coin and you have to determine what the probability is of getting “heads” in any toss of the coin. According to LLN, if you perform the coin toss experiment multiple times, you will be able to find the actual probability of getting heads.

Please note that for a unbiased coin you can use the classical probability theory and get the probability, P(head)= Total no. of favorable outcomes/Total number of outcomes = 1/2. But for an unbiased coin, you have unequal probability associated with each event and hence cannot use the classical approach. We will set up a coin toss experiment to determine the probability of getting heads in a coin toss.

3.6.1.3 Steps in Simulation with R Code

Step 1: Assume some value of binomial distribution parameter, p=0.60(say), which we will be be estimating using the Law of Large Numbers

# Set parameters for a binomial distribution Binomial(n, p)# n -> no. of toss# p -> probability of getting a headlibrary(data.table)n <-100p <-0.6

In the previous code snippet, we set the true mean for our experiment. Which is to say we know that our population is coming from a binomial distribution with p=0.6. The experiment will now help us estimate this value as the number of experiments increases.

Step 2: Sample a point from binomial distribution (p).

#Create a data frame with 100 values selected samples from Binomial(1,p)set.seed(917);dt <-data.table(binomial =rbinom(n, 1, p) ,count_of_heads =0, mean =0)# Setting the first observation in the data frameifelse(dt$binomial[1] ==1, dt[1, 2:3] <-1, 0)[1] 1

We are using a built-in function rbinom()to sample binomial distributed random variable with parameter, p=0.6. This probability value is chosen such that the coin is biased. If the coin is not biased, then we know the probability of heads is 0.5.

Step 3: Calculate the probability of heads as the number of heads/total no. of coin toss.

# Let's run a experiment large number of times (till n) and see how the average of heads -> probability of heads converge to a valuefor (i in 2 :n){dt$count_of_heads[i] <-ifelse(dt$binomial[i] ==1, dt$count_of_heads[i]<-dt$count_of_heads[i -1]+1, dt$count_of_heads[i -1])dt$mean[i] <-dt$count_of_heads[i] /i}

At each step, we determine if the outcome is heads or tails. Then, we count the number of heads and divide by the number of trials to get an estimated proportion of heads. When you run the same experiment a large number of times, LLN states that you will converge to the probability (expectation or mean) of getting heads in a experiment. For example, at trial 30, we will be counting how many heads so far and divide by 30 to get the average number of heads.

Step 4: Plot and see how the average over the sample is converging to p=0.60.

# Plot the average no. of heads -> probability of heads at each experiment stage

plot(dt$mean, type='l', main ="Simulation of average no. of heads",

xlab="Size of Sample", ylab="Sample mean of no. of Heads")

abline(h = p, col="red")Figure 3-3 shows that as the number of experiments increases, the probability is converging to the true probability of heads (0.6). You are encouraged to run the experiment a large number of times to see the exact convergence. This theorem helps us estimate unknown probabilities by method of experiments and create the distribution for inference testing.

Figure 3-3. Simulation of the coin toss experiment

3.6.2 Central Limit Theorem

The Central Limit Theorem is another very important theorem in probability theory which allows hypothesis testing using the the sampling distribution. In simpler words, the Central Limit Theorem states that sample averages of large number of iterations of independent random variables, each with well-defined means and variances, are approximately normally distributed.

The first written explanation of this concept was provided by de Moivre in his work back in the early 18th century when he used normal distribution to approximate the number of heads from the tossing experiment of a fair coin. Pierre-Simon Laplace published Théorie analytique des probability in 1812, where he expanded the idea of de Moivre by approximating binomial distribution with normal distribution. The precise proof of CLT was provided by Aleksandr Lyapunov in 1901 when he defined it in general terms and proved precisely how it worked mathematically. In probability, this is one the most popular theorems along with the Law of Large Numbers.

In context of this book, we will mathematically state by far the most popular version of the Central Limit Theorem (Lindeberg-Levy CLT).

For a sequence of i.i.d random variables {X1, X2, …} with a well defined expectation and variance (E[Xi] = μ and Var[Xi] = σ2<![]() ), as n trends to infinity

), as n trends to infinity ![]() converge in distribution to a normal N(0, sigma2),

converge in distribution to a normal N(0, sigma2),

There are other versions of this theorem, such as Lyapunov CLT, Lindeberg CLT, Martingale difference CLT, and many more. It is important to understand how the Law of Large Numbers and the Central Limit Theorem tie together in our sampling context. The Law of Large Numbers states that the sample mean converges to the population mean as the sample size grows, but it does not talk about distribution of sample means. The Central Limit Theorem provides us with the insight into the distribution around mean and states that it converges to a normal distribution for large number of trials. Knowing the distribution then allows us to do inferential testing, as we are able to create confidence bounds for a normal distribution.

We will again set up a simple example to explain the theorem. As a simple example, we will start sampling from a exponential distribution and will show the distribution of sample mean.

3.6.2.1 Steps in Simulation with R Code

Step 1: Set a number of samples (say r=5000) to draw from a mixed population.

#Number of samplesr<-5000#Size of each samplen<-10000

In the previous code, r represented the number of samples to draw, and n represented the number of units in each sample. As per CLT, the larger the number of samples, the better the convergence to a normal distribution.

Step 2: Start sampling by drawing a sample of sizes n (say n=10000 each). Draw samples from normal, uniform, Cauchy, gamma, and other distributions to test the theorem for different distributions. Here, we take an exponential distribution with parameter (![]() )

)

#Produce a matrix of observations with n columns and r rows. Each row is one samplelambda<-0.6Exponential_Samples =matrix(rexp(n*r,lambda),r)

Now, the Exponential_Samples data frame contain the series of i.i.d samples drawn from exponential distribution with the parameter, ![]()

Step 3: Calculate the sum, means, and variance of all the samples for each sample.

all.sample.sums <-apply(Exponential_Samples,1,sum)all.sample.means <-apply(Exponential_Samples,1,mean)all.sample.vars <-apply(Exponential_Samples,1,var)

The previous step calculated the sum, mean, and variance of all the i.i.d samples. Now in next step, we will observe the distribution of the sums, means, and variances. As per CLT, we will observe that the mean is following a normal distribution.

Step 4: Plot the combined sum, means, and variances.

par(mfrow=c(2,2))hist(Exponential_Samples[1,],col="gray",main="Distribution of One Sample")hist(all.sample.sums,col="gray",main="Sampling Distribution ofthe Sum")hist(all.sample.means,col="gray",main="Sampling Distribution of the Mean")hist(all.sample.vars,col="gray",main="Sampling Distribution ofthe Variance")

Figure 3-4 shows the plots of a exponential sample and sum, mean, and standard deviation of the all r samples .

Figure 3-4. Sampling distribution plots

Figure 3-4 shows the distribution of statistics of the samples, i.e., the sum, mean, and variance. The first plot shows the histogram of the first sample from the exponential distribution. You can see the distribution of units in sample is exponential. The visual inspection shows that the statistics estimated from i.i.d samples are following a distribution close to a normal distribution.

Step 5: Repeat this experiment with other distributions and see that the results are consistent with the CLT for all the distributions.

There are some other standard distributions that can be used to validate the results of Central Limit Theorem. Our example just discussed the exponential distribution; you are encouraged to use the following distribution to validate the Central Limit Theorem.

Normal_Samples =matrix(rnorm(n*r,param1,param2),r),Uniform_Samples =matrix(runif(n*r,param1,param2),r),Poisson_Samples =matrix(rpois(n*r,param1),r),Cauchy_Samples =matrix(rcauchy(n*r,param1,param2),r),Bionomial_Samples =matrix(rbinom(n*r,param1,param2),r),Gamma_Samples =matrix(rgamma(n*r,param1,param2),r),ChiSqr_Samples =matrix(rchisq(n*r,param1),r),StudentT_Samples =matrix(rt(n*r,param1),r))

It is a good practice to not rely on visual inspection and perform formal tests to infer any properties of distribution. Histogram and a formal test of normality is a good way to establish both visually and by parametric testing that the distribution of means is actually normally distributed (as claimed by CLT).

Next, we perform a Shapiro-Wilk test to test for normality of distribution of means. Other normality tests are discussed in briefly in Chapter 6. One of the most popular non-parametric normality tests is the KS one sample test, which is discussed in Chapter 7.

#Do a formal test of normality on the distribution of sample meansMean_of_sample_means <-mean (all.sample.means)Variance_of_sample_means <-var(all.sample.means)# testing normality by Shapiro wilk testshapiro.test(all.sample.means)Shapiro-Wilk normality testdata: all.sample.meansW = 0.99979, p-value = 0.9263

You can see that the p-value is significant (>0.05) from the Shapiro-Wilk test, which means that we can’t reject the Null hypothesis that distribution is normally distributed. The distribution is indeed normally distributed with a mean = 1.66 and variance = 0.00027.

Visual inspection can be done by plotting histograms. Additionally, for clarity, let’s superimpose the normal density function on the histogram to confirm if the distribution is normally distributed.

x <-all.sample.means

h<-hist(x, breaks=20, col="red", xlab="Sample Means",

main="Histogram with Normal Curve")

xfit<-seq(min(x),max(x),length=40)

yfit<-dnorm(xfit,mean=Mean_of_sample_means,sd=sqrt(Variance_of_sample_means))

yfit <-yfit*diff(h$mids[1:2])*length(x)

lines(xfit, yfit, col="blue", lwd=2)

Figure 3-5. Distribution of sample means with normal density lines

The most important points to remember about the Law of Large Numbers and CLT are:

As the sample size grows large, you can expect a better estimate of the population/model parameters. This being said, a large sample size will provide you with unbiased and more accurate estimates for hypothesis testing.

The Central Limit Theorem helps you get a distribution and hence allows you to get a confidence interval around parameters and apply inference testing. The important thing is that CLT doesn’t assume any distribution of population from which samples are drawn, which frees you from distribution assumptions.

3.7 Probability Sampling Techniques

In this section, we introduce some of the popular probability sampling techniques and show how to perform them using R. All the sampling techniques are explained using our credit card fraud data. As a first step of explaining the individual techniques, we create the population statistics and distribution and then compare the same sample properties with the population properties to ascertain the sampling outputs.

3.7.1 Population Statistics

We will look at some basic features of data. These features will be called as population statistics/parameters. We will then show different sampling methods and compare the result with population statistics.

Populationdata dimensions

str() shows us the column names, type, and few values in the column. You can see the dataset is a mix of integers and characters.

str(data)Classes 'data.table' and 'data.frame': 10000000 obs. of 14 variables:$ creditLine : int 1 1 1 1 1 1 1 1 1 1 ...$ gender : int 1 1 1 1 1 1 1 1 1 1 ...$ state : int 1 1 1 1 1 1 1 1 1 1 ...$ CustomerID : int 4446 59161 136032 223734 240467 248899 262655 324670 390138 482698 ...$ NumOfCards : int 1 1 1 1 1 1 1 1 1 1 ...$ OutsBal : int 2000 0 2000 2000 2000 0 0 689 2000 0 ...$ DomesTransc: int 31 25 78 11 40 47 15 17 48 25 ...$ IntTransc : int 9 0 3 0 0 0 0 9 0 35 ...$ FraudFlag : int 0 0 0 0 0 0 0 0 0 0 ...$ State : chr "Alabama" "Alabama" "Alabama" "Alabama" ...$ PostalCode : chr "AL" "AL" "AL" "AL" ...$ Gender : chr "Male" "Male" "Male" "Male" ...$ CardType : chr "American Express" "American Express" "American Express" "American Express" ...$ CardName : chr "SimplyCash® Business Card from American Express" "SimplyCash® Business Card from American Express" "SimplyCash® Business Card from American Express" "SimplyCash® Business Card from American Express" ...- attr(*, ".internal.selfref")=<externalptr>- attr(*, "sorted")= chr "creditLine"Population meanfor measures

Outstanding balance: On average each card carries an outstanding amount of $4109.92.

mean_outstanding_balance <- mean(data$OutsBal)mean_outstanding_balance[1] 4109.92

Number of international transactions: Average number of international transactions is 4.04.

mean_international_trans <- mean(data$IntTransc)mean_international_trans[1] 4.04719

Number of domestic transactions: Average number of domestic transactions is very high compared to international transactions; the number is 28.9 ∼ 29 transactions.

mean_domestic_trans <- mean(data$DomesTransc)mean_domestic_trans[1] 28.93519

Population variancefor measures

Outstanding balance:

Var_outstanding_balance <- var(data$OutsBal)Var_outstanding_balance[1] 15974788Number of international transactions:

Var_international_trans <- var(data$IntTransc)Var_international_trans[1] 74.01109Number of domestic transactions:

Var_domestic_trans <- var(data$DomesTransc)Var_domestic_trans[1] 705.1033

Histogram

Outstanding balance:

hist(data$OutsBal, breaks=20, col="red", xlab="Outstanding Balance",main="Distribution of Outstanding Balance")

Figure 3-6. Histogram of outstanding balance

Number of international transactions:

hist(data$IntTransc, breaks=20, col="blue", xlab="Number of International Transactions",main="Distribution of International Transactions")

Figure 3-7. Histogram of number of international transactions

Number of domestic transactions:

hist(data$DomesTransc, breaks=20, col="green", xlab="Number of Domestic Transactions",main="Distribution of Domestic Transactions")

Figure 3-8 shows the mean, variance, and distribution of few important variables from our credit card fraud dataset. These population statistics will be compared to sample statistics to see which sampling techniques provide a representative sample.

Figure 3-8. Histogram of number of domestic transactions

3.7.2 Simple Random Sampling

Simple random sampling is a process of selecting a sample from the population where each unit of population is selected at random Each unit has the same individual probability of being chosen at any stage during the sampling process, and the subset of k individuals has the same probability of being chosen for the sample as any other subset of k individuals.

Simple random is a basic type of sampling, hence it can be a component of more complex sampling methodologies. In coming topics, you will see simple random sampling form an important component of other probability sampling methods, like stratified sampling and cluster sampling.

Simple random sampling is typically without replacement , i.e., by the design of sampling process, we make sure that no unit can be selected more than once. However, simple random sampling can be done with replacement, but in that case the sampling units will not be independent. If you draw a small size sample from a large population, sampling without replacement and sampling with replacement will give approximately the same results, as the probability of each unit to be chosen is very small. Table 3-5 compares the statistics from simple random sampling with and without replacement. The values are comparable, as the population size is very big (∼10 million). We will see this fact in our example.

Advantages:

It is free from classification error

Not much advanced knowledge is required of the population

Easy interpretation of sample data

Disadvantages:

Complete sampling frame (population) is required to get representative sample

Data retrieval and storage increases cost and time

Simple random sample carries the bias and errors present in the population, and additional interventions are required to get rid of those

Function: Summarise

Summarise is a function in the dplyr library. This function helps aggregate the data by dimensions. This works similar to a pivot table in Excel.

group_by: This argument takes the categorical variable by which you want to aggregate the measures.

mean(OutsBal): This argument gives the aggregating function and the field name on which aggregation is to be done.

#Population Data :Distribution of Outstanding Balance across Card Typelibrary(dplyr)summarise(group_by(data,CardType),Population_OutstandingBalance=mean(OutsBal))Source: local data table [4 x 2]CardType Population_OutstandingBalance1 American Express 3820.8962 MasterCard 3818.3003 Visa 4584.0424 Discover 4962.420

The call of the summarise function by CardTypeshows the average outstanding balance by card type. Discover cards have the highest average outstanding balance.

Next, we draw a random sample of 100,000 records by using a built-in function sample() from the base library. This function creates a sampling frame by randomly selecting indexes of data. Once we get the sampling frame, we extract the corresponding records from the population data.

Function: Sample

Note some important arguments of the sample() function :

nrow(data): This tells the size of data. Here it is 10,000,000 and hence it will create an index of 1 to 10,000,000 and then randomly select index for sampling.

size: Allows users to provide how many data points to sample from the population. In our case, we have set n to 100,000.

replace: This argument allows users to state if the sampling should be done without replacement (FALSE) or with replacement (TRUE).

prob: This is vector of probabilities for obtaining the sampling frame. We have set this to NULL, so that they all have the same weight/probability.

set.seed(937)# Simple Random Sampling Without Replacementlibrary("base")sample_SOR_100K <-data[sample(nrow(data),size=100000, replace =FALSE, prob =NULL),]

Now, let’s again see how the average balance looks for the simple, random sample. As you can see the order of average balances has been maintained. Note that the average is very close to the population average as calculated in the previous step for population.

#Sample Data : Distribution of Outstanding Balance across Card Typelibrary(dplyr)summarise(group_by(sample_SOR_100K,CardType),Sample_OutstandingBalance=mean(OutsBal))Source: local data table [4 x 2]CardType Sample_OutstandingBalance1 MasterCard 3822.6322 American Express 3835.0643 Visa 4611.6494 Discover 4942.690

Function: KS.test()

This is one of the non-parametric tests for comparing the empirical distribution functions of data. This function helps determine if the data points are coming from the same distribution or not. It can be done as one sample test, i.e., the data Empirical Distribution Function (EDF) compared to some preset PDF of distribution (normal, cauchy, etc.), two sample test, i.e., when we want to see if the distribution of two samples is the same or not.

As one of the important features of sampling is to make sure the distribution of data does not change after sampling (except when it is done intentionally), we will use two sample tests to see if the sample is a true representation of the population by checking if the population and sample are drawn from the same distribution.

The important arguments are the two data series and hypothesis to test, two tail, one tail. We are choosing the more conservative two tail test for this example. Two tail test means that we want to make sure the equality is used in the null hypothesis.

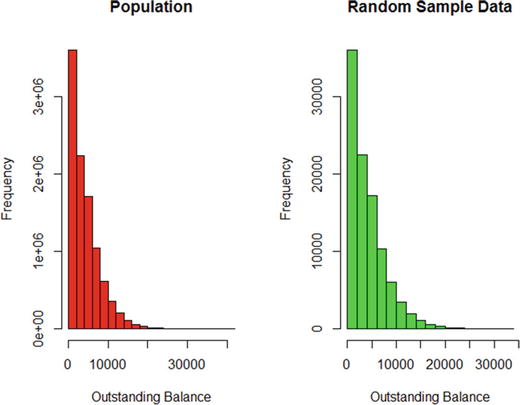

#Testing if the sampled data comes from population or not. This makes sure that sampling does not change the original distributionks.test(data$OutsBal,sample_SOR_100K$OutsBal,alternative="two.sided")Two-sample Kolmogorov-Smirnov testdata: data$OutsBal and sample_SOR_100K$OutsBalD = 0.003042, p-value = 0.3188alternative hypothesis: two-sided

The KS test results clearly states that the sample and population have the same distribution. Hence, we can say that the sampling has not changed the distribution. By the nature of sampling, the simple random sampling without replacement retains the distribution of data.

For visual inspection, Figure 3-9 shows the histograms for the population and the sample. As you can see, the distribution is the same for both.

Figure 3-9. Population versus sample (without replacement) distribution

par(mfrow =c(1,2))hist(data$OutsBal, breaks=20, col="red", xlab="Outstanding Balance",main="Histogram for Population Data")hist(sample_SOR_100K$OutsBal, breaks=20, col="green", xlab="Outstanding Balance",main="Histogram for Sample Data (without replacement)")

Now we will do a formal test on the mean of the outstanding balance from the population and our random sample. Theoretically, we will expect the t-test on means of two to be TRUE and hence we can say that the mean of the sample and population are the same with 95% confidence.

# Lets also do t.test for the mean of population and sample.t.test(data$OutsBal,sample_SOR_100K$OutsBal)Welch Two Sample t-testdata: data$OutsBal and sample_SOR_100K$OutsBalt = -0.85292, df = 102020, p-value = 0.3937alternative hypothesis: true difference in means is not equal to 095 percent confidence interval:-35.67498 14.04050sample estimates:mean of x mean of y4109.920 4120.737

These results show that the means of population and sample are the same as the p-value of t.testis insignificant. We cannot reject the null hypothesis that the means are equal.

Here we will show you similar testing performed for simple random sample with replacement. As you will see, we don’t see any significant change in the results as compared to simple random sample, as the population size is very big and replacement essentially doesn’t alter the sampling probability of record in any material way.

set.seed(937)# Simple Random Sampling With Replacementlibrary("base")sample_SR_100K <-data[sample(nrow(data),size=100000, replace =TRUE, prob =NULL),]

In this code, for simple random sampling with replacement, we set replace to TRUE in the sample function call.

The following code shows how we performed the KS test , on distribution of the population and the sample drawn with replacement. The test shows that the distributions are the same and the p-value is insignificant, which fails to reject the null of equal distribution.

ks.test(data$OutsBal,sample_SR_100K$OutsBal,alternative="two.sided")Warning in ks.test(data$OutsBal, sample_SR_100K$OutsBal, alternative ="two.sided"): p-value will be approximate in the presence of tiesTwo-sample Kolmogorov-Smirnov testdata: data$OutsBal and sample_SR_100K$OutsBalD = 0.0037522, p-value = 0.1231alternative hypothesis: two-sided

We create the histogram of population and sample with replacement . The plots look the same, coupled with a formal KS test, we see both sample with replacement and populations have the same distribution. Be cautious about this when the population size is small.

par(mfrow =c(1,2))hist(data$OutsBal, breaks=20, col="red", xlab="Outstanding Balance",main="Population ")hist(sample_SR_100K$OutsBal, breaks=20, col="green", xlab="Outstanding Balance",main=" Random Sample Data ( WR)")

Figure 3-10. Population versus sample (with replacement) distribution

The distribution is similar for population and random sample drawn with replacement . We summarize the simple random sampling by comparing the summary results from population, simple random sample without replacement, and simple random sample with replacement.

population_summary <-summarise(group_by(data,CardType),OutstandingBalance_Population=mean(OutsBal))random_WOR_summary<-summarise(group_by(sample_SOR_100K,CardType),OutstandingBalance_Random_WOR=mean(OutsBal))random_WR_summary<-summarise(group_by(sample_SR_100K,CardType),OutstandingBalance_Random_WR=mean(OutsBal))compare_population_WOR<-merge(population_summary,random_WOR_summary, by="CardType")compare_population_WR <-merge(population_summary,random_WR_summary, by="CardType")summary_compare<-cbind(compare_population_WOR,compare_population_WR[,OutstandingBalance_Random_WR])colnames(summary_compare)[which(names(summary_compare) == "V2")] <- "OutstandingBalance_Random_WR"knitr::kable(summary_compare)

Table 3-5. Comparison Table with Population Sampling with and Without Replacement

CardType | OutstandingBalance_Population | OutstandingBalance_Random_WOR | OutstandingBalance_Random_WR |

|---|---|---|---|

American Express | 3820.896 | 3835.064 | 3796.138 |

Discover | 4962.420 | 4942.690 | 4889.926 |

MasterCard | 3818.300 | 3822.632 | 3780.691 |

Visa | 4584.042 | 4611.649 | 4553.196 |

Table 3-5 shows that both with and without replacement, simple random sampling gave similar values of mean across card types, which were very close to the true mean of the population.

Key points:

Simple random sampling gives representative samples from the population.

Sampling with and without replacement can give different results with different samples sizes, so extra care should be paid to choosing the method when population size is small.

The appropriate sample size for each problem differ based on the confidence we want with our testing, business purposes, cost benefit analysis, and other reasons. You will get a good understanding of what is happening in each sampling techniques and can choose the best one that suits the problem at hand.

3.7.3 Systematic Random Sampling

Systematic sampling is a statistical method in which the units are selected with a systematically ordered sampling frame. The most popular form of systematic sampling is based on a circular sampling frame , where we transverse the population from start to end and then again continue from start in a circular manner. In this approach the probability of each unit to be selected is the same and hence this approach is sometimes called the equal-probability method. But you can create other systematic frames according to your need to perform systematic sampling.

In this section, we discuss the most popular circular approach to systematic random sampling. In this method, sampling starts by selecting a unit from the population at random and then every Kth element is selected. When the list ends, the sampling starts from the beginning. Here, the k is known as the skip factor

, and it’s calculated as follows

![]()

where N is population size and n is sample size.

This approach to systematic sampling makes this functionally similar to simple random sampling, but it is not the same because not every possible sample of a certain size has an equal probability of being chosen (e.g., the seed value will make sure that the adjacent elements are never selected in the sampling frame). However, this method is efficient if variance within the systematic sample is more than the population variance .

Advantages:

Easy to implement

Can be more efficient

Disadvantages:

Can be applied when the population is logically homogeneous

There can be a hidden pattern in the sampling frame, causing unwanted bias

Let’s create an example of systematic sampling from our credit card fraud data.

Step 1: Identify a subset of population that can be assumed to be homogeneous. A possible option is to subset the population by state. In this example, we use Rhode Island, the smallest state in the United States, to assume homogeneity.

Note

Creating homogeneous sets from the population by some attribute is discussed in Chapter 6.

For illustration purposes, let’s create a homogeneous set by subsetting the population with the following business logic. Subset the data and pull the records whose international transactions equal 0 and domestic transactions are less than or equal to 3.

Assuming the previous subset forms a set of homogeneous population, the assumption in subsetting is also partially true as the customers who do not use card domestically are likely not to use them internationally at all.

Data_Subset <-subset(data, IntTransc==0&DomesTransc<=3)summarise(group_by(Data_Subset,CardType),OutstandingBalance=mean(OutsBal))Source: local data table [4 x 2]CardType OutstandingBalance1 American Express 3827.8942 MasterCard 3806.8493 Visa 4578.6044 Discover 4924.235

Assuming the subset has homogeneous sets of cardholders by card type, we can go ahead with systematic sampling. If the set is not homogeneous, then it’s highly likely that systematic sampling will give a biased sample and hence not provide a true representation of the population. Further, we know that the data is stored in R data frame by an internal index (which will be the same as our customer ID ), so we can rely on internally ordered index for systematic sampling.

Step 2: Set a sample size to sample from the population.

#Size of population ( here the size of card holders from Data Subset)Population_Size_N<-length(Data_Subset$OutsBal)# Set a the size of sample to pull (should be less than N), n. We will assume n=5000Sample_Size_n<-5000

Step 3: Calculate the skip factor using this formula

:

![]()

The skip factor will give the jump factor while creating the systematic sampling frame. Essentially, with a seed (or starting index) of c, items will be selected after skipping k items in order.

#Calculate the skip factork =ceiling(Population_Size_N/Sample_Size_n)#ceiling(x) rounds to the nearest integer thatâ<U+0080><U+0099>s larger than x.#This means ceiling (2.3) = 3cat("The skip factor for systematic sampling is ",k)The skip factor for systematic sampling is 62

Step 4: Set a random seed value of index and then create a sequence vector with seed and skip (sample frame). This will take a seed value of index, say i, then create a sampling frame as i,i+k,i+2k …so one until it has a total of n (sample size) indexes in the sampling frame.

r =sample(1:k, 1)systematic_sample_index =seq(r, r +k*(Sample_Size_n-1), k)

Step 5: Sample the records from the population by sample frame . Once we have our sampling frame ready, it is nothing but list of indices, so we pull those data records corresponding to the sampling frame.

systematic_sample_5K<-Data_Subset[systematic_sample_index,]Let’s now compare the systematic sample with a simple random sample of the same size of 5000. As from the previous discussion, we know that the simple random sampling is a true representation of the population, so we can use that as a proxy for population properties.

set.seed(937)# Simple Random Sampling Without Replacementlibrary("base")sample_Random_5K <-Data_Subset[sample(nrow(Data_Subset),size=5000, replace =FALSE, prob =NULL),]

Here is the result of summary comparison by card type for outstanding balances. The comparison is important to show what differences in mean will appear if we would have chosen a simple random sample instead of a systematic sample.

sys_summary <-summarise(group_by(systematic_sample_5K,CardType),OutstandingBalance_Sys=mean(OutsBal))random_summary<-summarise(group_by(sample_Random_5K,CardType),OutstandingBalance_Random=mean(OutsBal))summary_mean_compare<-merge(sys_summary,random_summary, by="CardType")print(summary_mean_compare)Source: local data table [4 x 3]CardType OutstandingBalance_Sys OutstandingBalance_Random1 American Express 3745.873 3733.8182 Discover 5258.751 4698.3753 MasterCard 3766.037 3842.1214 Visa 4552.099 4645.664

Again, we will emphasize on testing the sample EDF with population EDF to make sure that the sampling has not distorted the distribution of data. This steps will be repeated for all the sampling techniques, as this ensures that the sampling is stable for modeling purposes.

ks.test(Data_Subset$OutsBal,systematic_sample_5K$OutsBal,alternative="two.sided")Warning in ks.test(Data_Subset$OutsBal, systematic_sample_5K$OutsBal,alternative = "two.sided"): p-value will be approximate in the presence oftiesTwo-sample Kolmogorov-Smirnov testdata: Data_Subset$OutsBal and systematic_sample_5K$OutsBalD = 0.010816, p-value = 0.6176alternative hypothesis: two-sided

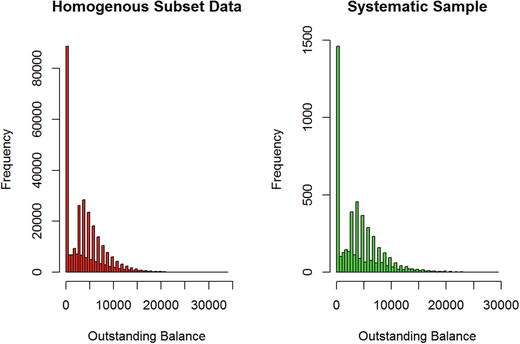

The KS test results show that the distribution is the same and hence the sample is a representation of the population by distribution. Figure 3-11 shows the histograms to show how the distribution is for a homogeneous data subset and a systematic sample. We can see that the distribution has not changed drastically.

Figure 3-11. Homogeneous population and systematic sample distribution

par(mfrow =c(1,2))hist(Data_Subset$OutsBal, breaks=50, col="red", xlab="Outstanding Balance",main="Homogenous Subset Data")hist(systematic_sample_5K$OutsBal, breaks=50, col="green", xlab="Outstanding Balance",main="Systematic Sample ")

Key points:

Systematic sampling is equivalent to simple random sampling if done on a homogeneous set of data points. Also, a large population size suppresses the bias associated with systematic sampling for smaller sampling fractions.

Business and computational capacity are important criteria to choose a sampling technique when the population size is large. In our example, the systematic sampling gives a representative sample with a lower computational cost. (There is no call to random number generator, and hence no need to transverse the complete list of records.)

3.7.4 Stratified Random Sampling

When the population has sub-populations that vary, it is important for the sampling technique to consider the variations at the subpopulation (stratum) level and sample them independently at the stratum level. Stratification is the process of identifying homogeneous groups by featuring that group by some intrinsic property. For instance, customers living in the same city can be thought of as belonging to that city stratum. The strata should be mutually exclusive and collectively exhaustive, i.e., all units of the population should be assigned to some strata and one unit can only belong to one strata.

Once we form the stratum then a simple random sampling or systematic sampling is performed at the stratum level independently. This improves the representativeness of sample and generally reduces the sampling error. Dividing the population in stratum also helps you calculate the weighted average of the population, which has less variability than the total population combined.

There are two generally accepted methods of identifying stratified sample size:

Proportional allocation, which samples equal proportions of the data from each stratum. In this case, the same sampling fraction is applied for all the stratum in the population. For instance, your population has four types of credit cards and you assume that each credit card type forms a homogeneous group of customers. Assume the number of each type of customers in each stratum is N1+N2+N3+N4=total, then in proportional allocation you will get a sample having the same proportion from each stratus (n1/N1=n2/N2=n3/N3=n4/N4=sampling fraction).

Optimal allocation, which samples proportions of data proportionate to the standard deviation of the distribution of stratum variable. This results in large samples from strata with the highest variability, which means the sample variance is reduced.

Another important feature of stratified sampling is that it makes sure that at least one unit is sampled from each strata, even if the probability of it getting selected is zero. It is recommended to limit the number of strata and make sure enough units are present in each stratum to do sampling.

Advantages:

Greater precision than simple random sampling of the same sample size

Due to higher precision, it is possible to work with small samples and hence reduce cost

Avoid unrepresentative samples, as this method samples at least one unit from each stratum

Disadvantages :

Not always possible to partition the population in disjointed groups

Overhead of identifying homogeneous stratum before sampling, adding to administrative cost

Thin stratum can limit the representative sample size

To construct an example of stratified sampling with credit card fraud data, we first have to check the stratums and then go ahead with sampling from stratum. For our example, we will create a stratum based on the CardType and State variables.

Here, we explain step by step how to go about performing stratified sampling.

Step 1: Check the stratum variables and their frequency in population.

Lets assume CardTypeand State are stratum variables. In other words, we believe the type of card and the state can be used as a criteria to stratify the customers in logical buckets. Here are the frequencies by our stratum variables. We expect stratified sampling to maintain the same proportion of records in the stratified sample.

#Frequency table for CardType in Populationtable(data$CardType)American Express Discover MasterCard Visa2474848 642531 4042704 2839917#Frequency table for State in Populationtable(data$State)Alabama American Samoa Arizona Arkansas California20137 162574 101740 202776 1216069Colorado Connecticut Delaware Florida Georgia171774 121802 20603 30333 608630Guam Hawaii Idaho Illinois Indiana303984 50438 111775 60992 404720Iowa Kansas Kentucky Louisiana Maine203143 91127 142170 151715 201918Maryland Massachusetts Michigan Minnesota Mississippi202444 40819 304553 182201 203045Missouri Montana Nebraska Nevada New Hampshire101829 30131 60617 303833 20215New Jersey New Mexico New York North Carolina North Dakota40563 284428 81332 91326 608575Ohio Oklahoma Oregon Pennsylvania Rhode Island364531 122191 121846 405892 30233South Carolina South Dakota Tennessee Texas Utah152253 20449 203827 812638 91375Vermont Virginia Washington West Virginia Wisconsin252812 20017 202972 182557 61385Wyoming20691

The cross table breaks the whole population by the stratum variables , CardType and State. Each stratum represents a set of customers having similar behaviors as they come from the same stratum. The following output is trimmed for easy readability.

#Cross table frequency for population datatable(data$State,data$CardType)American Express Discover MasterCard VisaAlabama 4983 1353 8072 5729American Samoa 40144 10602 65740 46088Arizona 25010 6471 41111 29148Arkansas 50158 12977 82042 57599California 301183 78154 491187 345545Colorado 42333 11194 69312 48935Connecticut 30262 7942 49258 34340Delaware 4990 1322 8427 5864

Step 2: Random sample without replacement from each stratum, consider sampling 10% of the size of the stratum.

We are choosing the most popular way of stratified sampling , proportional sampling. We will be sampling 10% of the records from each stratum.

Function : stratified()

The stratified function samples from a data.frame or a data.table in which one or more columns can be used as a “stratification” or “grouping” variable. The result is a new data.table with the specified number of samples from each group. The standard function syntax is shown here:

stratified(indt, group, size, select = NULL, replace = FALSE, keep.rownames = FALSE, bothSets = FALSE, ...) group: This argument allows users to define the stratum variables. Here we have chosen CardType and State as the stratum variables. So in Total, we will have 4 (card types) X 52 (states) stratum to sample from.

size: In general, size can be passed as a number (equal numbers sample from each strata) or a sampling fraction. We will use the sampling fraction of 0.1. For other options type ?stratified in the console.

replace: This allows you to choose sampling with or without replacement. We have set it as false, which means sampling without replacement.

We will be using this function to perform stratified random sampling.

We can also do the stratified sampling using our standard sample() function as well with following steps:

Create subsets of the data by stratum variables.

Calculate the sample size for sampling fraction of 0.1, for each stratum.

Do a simple random sampling from each stratum for the sample size as calculated.

The previous results and the stratified() results will be the same. But the stratified() function will be faster to execute. You are encouraged to implement this algorithm and try out the other functions.

set.seed(937)#We want to make sure that our sampling retain the same proportion of the cardtype in the sample#Do choose a random sample without replacement from each startum consisting of 10% of total size of stratumlibrary(splitstackshape)stratified_sample_10_percent<-stratified(data, group=c("CardType","State"),size=0.1,replace=FALSE)

Step 3: Check if the proportions of data points in the sample are the same as the population.

Here is the output of stratified sample by CardType, State, and by cross tabulation. The values show that the sampling has been done across the stratum with the same proportion. For example, number of records Alabama and American Express is 4980, in stratified sample the number of Alabama and American Express cardholders is 1/10 of the population, i.e., 498. For all other stratum, the proportion is the same.

#Frequency table for CardType in sampletable(stratified_sample_10_percent$CardType)American Express Discover MasterCard Visa247483 64250 404268 283988#Frequency table for State in sampletable(stratified_sample_10_percent$State)Alabama American Samoa Arizona Arkansas California2013 16257 10174 20278 121606Colorado Connecticut Delaware Florida Georgia17177 12180 2060 3032 60862Guam Hawaii Idaho Illinois Indiana30399 5044 11177 6099 40471Iowa Kansas Kentucky Louisiana Maine20315 9113 14218 15172 20191Maryland Massachusetts Michigan Minnesota Mississippi20245 4081 30455 18220 20305Missouri Montana Nebraska Nevada New Hampshire10183 3013 6061 30383 2022New Jersey New Mexico New York North Carolina North Dakota4056 28442 8133 9132 60856Ohio Oklahoma Oregon Pennsylvania Rhode Island36453 12219 12184 40589 3023South Carolina South Dakota Tennessee Texas Utah15225 2046 20382 81264 9137Vermont Virginia Washington West Virginia Wisconsin25281 2002 20297 18255 6138Wyoming2069#Cross table frequency for sample datatable(stratified_sample_10_percent$State,stratified_sample_10_percent$CardType)American Express Discover MasterCard VisaAlabama 498 135 807 573American Samoa 4014 1060 6574 4609Arizona 2501 647 4111 2915Arkansas 5016 1298 8204 5760California 30118 7815 49119 34554Colorado 4233 1119 6931 4894Connecticut 3026 794 4926 3434Delaware 499 132 843 586

You can see that the proportion has remained the same. Here, we compare the properties of sample and population. The summarise() function shows the average of outstanding balance by strata. You can perform a pairwise t.test to see that the sampling has not altered the means of outstanding balance belonging to each strata. You are encouraged to do testing on the means by t.test(), as shown in the simple random sampling section.

# Average outstanding balance by stratum variablessummary_population<-summarise(group_by(data,CardType,State),OutstandingBalance_Stratum=mean(OutsBal))#We can see below the want to make sure that our sampling retain the same proportion of the cardtype in the samplesummary_sample<-summarise(group_by(stratified_sample_10_percent,CardType,State),OutstandingBalance_Sample=mean(OutsBal))#Mean Comparison by stratumsummary_mean_compare<-merge(summary_population,summary_sample, by=c("CardType","State"))

Again, we will do a KS test to compare the distribution of the stratified sample. We can see that the KS test shows that both have the same distribution.

ks.test(data$OutsBal,stratified_sample_10_percent$OutsBal,alternative="two.sided")Two-sample Kolmogorov-Smirnov testdata: data$OutsBal and stratified_sample_10_percent$OutsBalD = 0.00073844, p-value = 0.7045alternative hypothesis: two-sided

Figure 3-12 shows the histograms to show how the distribution of outstanding balance looks for the sample and population. The visual comparison clearly shows that the sample is representative of the population.

Figure 3-12. Population and stratified sample distribution

par(mfrow =c(1,2))hist(data$OutsBal, breaks=50, col="red", xlab="Outstanding Balance",main="Population ")hist(stratified_sample_10_percent$OutsBal, breaks=50, col="green", xlab="Outstanding Balance",main="Stratified Sample")

The distribution plot in Figure 3-12 reemphasizes the test results, both population and stratifies random sample have the same distribution. The stratified random sample is representative of the population.

Key points:

Stratified sampling should be used when you want to make sure the proportion of data points remains the same in the sample. This not only ensures representativeness but also ensures that all the stratum gets a representation in the sample.

Stratified sampling can also help you systematically design the proportion of records from each stratum, so you can design a stratified sampling plan to change the representation as per business need. For instance, you are modeling a binomial response function, and the even rate or the proportion of 1 is very small in the dataset. Then you can do a stratified random sampling from stratum (0 or 1 response) and try to sample so that proportion of 1 increases to facilitate modeling.

3.7.5 Cluster Sampling

Many times, populations contain heterogeneous groups that are statistically evident in the population. In those cases, it is important to first identify the heterogeneous groups and then plan the sampling strategy. This technique is popular among marketing and campaign designers, as they deal with characteristics of heterogeneous groups within a population.

Cluster sampling can be done in two ways:

Single-stage sampling: All of the elements within selected clusters are included in the sample. For example, you want to study a particular population feature that’s dominant in a cluster, so you might want to first identify the cluster and its element and just take all the units of that cluster.