10

Financing for Minorities and Women

Introduction

Minority- and women-owned firms are powerful economic forces in the small-business world. Minority-owned businesses nearly doubled from 2007 to 2017, to over 11 million companies.1 The most recent Survey of Business Owners, completed by the US Census Bureau in 2017 (which reports on 2015 data), shows that:

• Over 996,000 minority firms had at least one employee.2

• Minority-owned employer companies generated $1,168,500,000 in annual revenue and employed 8 million people.3

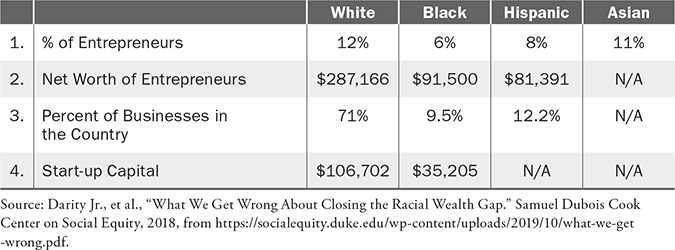

The job creation by minority entrepreneurs is one of the reasons I repeatedly state that they are my heroes and she-roes! They tend to hire a larger percentage of minority employees than nonminority entrepreneurs do. Thus, they have workforces of more African Americans and Latinos, the two groups with the highest rates of unemployment in the country. When people are gainfully employed, they are self-sufficient, and self-sufficient people tend to live happier lives in healthy communities. But as the Table 10-1 shows, financial status of minority entrepreneurs is woefully low compared to white entrepreneurs.

TABLE 10-1 Minority Entrepreneurs

My mother, Ollie Mae Rogers, was the first entrepreneur I ever met, and accordingly, I have a tremendous amount of respect and admiration for women entrepreneurs. There are more than 12 million women-owned businesses generating an estimated $1.5 trillion in annual sales and employing 9.3 million people. African American women like my mother, and other women of color who are entrepreneurs, employ 2.1 million people and generate $361 billion in annual revenue. The Kauffman Foundation’s 2018 research showed that 40% of all new start-ups are by women entrepreneurs, and the number of businesses owned by women is growing at the rate of male-owned businesses.4

Unfortunately, minority and women entrepreneurs have had to play the game of catch-up and forced the traditional small-business infrastructure to change. Thank God, we are past the era when a woman could not get a loan without her husband’s signature and it was legal to reject a loan application from a person simply because of his ethnicity or race! The laws that made such gender and racial discrimination legal had a profound effect on minority and women entrepreneurship. The inability to access capital other than from personal savings, credit cards, family, friends, and angels retarded the growth of most entrepreneurs from these two sectors. Given the absence of growth capital from financial institutions, these entrepreneurs, in essence, were involuntarily relegated to a life as mom-and-pop, or lifestyle, entrepreneurs. The result is that we have virtually no major corporations that were founded by minorities or women.

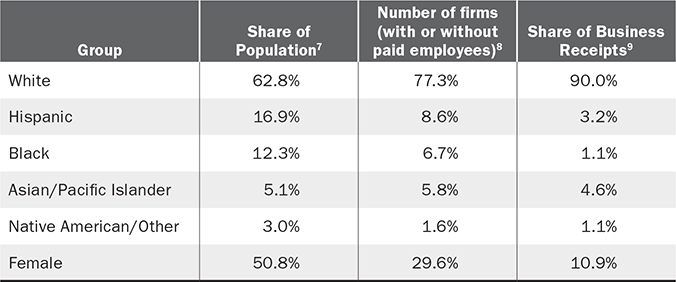

Research from the SBA also indicates that race is a significant predictor of the likelihood of opening a business and that the odds of a minority person opening a business are 55% lower than those for a nonminority. The data in Table 10-2 show the composition of the total US population side by side with a breakdown of US business receipts by race. While the situation continues to improve, these data clearly indicate that the process is still ongoing.

TABLE 10-2 Composition of US Population Versus Share of Business Receipts

And while there are federal laws that prohibit gender and racial discrimination in debt and equity financing, it is sad to report that even today, minority and women entrepreneurs are receiving a pittance of all the capital provided to entrepreneurs.

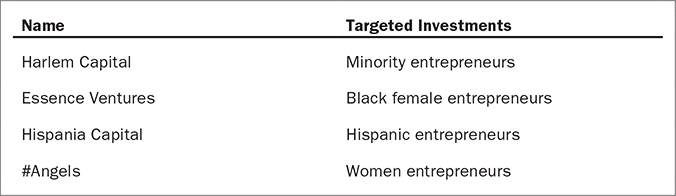

Still, there are an increasing number of investment firms that are focusing on all kinds of niches, and these firms are an important resource. For example, there are specialized firms that target entrepreneurs who are female, and/or are minorities. A few of these specialized firms are listed in Figure 10-1.

FIGURE 10-1 Niche Equity Investment Firms

Minorities—Debt Financing

Historically, the success rate of minority entrepreneurs in raising debt capital is abysmally low. Research commissioned by the Small Business Administration showed that minorities face significantly lower approval rates for credit than firms with white owners. The data in Table 10-3 show approval rates for minority-owned firms.

TABLE 10-3 Loan Approval Rates for Business Owners

Low approval rates inhibit minorities from initiating loan applications out of fear of having the loan application rejected. Minority owners are more than two and a half times more likely to not apply for a loan than white owners.

The result is that minority-owned companies use personal financing more than white-owned companies do. SBA data suggest that only 9.5% of white-owned businesses use a credit card in their business, whereas 20.6% of Islander-owned, 15% of black-owned, and 13% of Hispanic-owned businesses do.

Minority entrepreneurs who are seeking debt capital should approach those institutions that are friends to minorities. Where better to turn than the US Department of the Treasury, which as a result of Section 4112 of the Small Business Jobs Act of 2010 created the Small Business Lending Fund (SBLF) with a specific charter to increase lending to small businesses, including minority-owned businesses.

In 2017, the US Treasury invested more than $4.0 billion in 332 institutions through the SBLF program. These amounts include investments of $3.9 billion in 281 community banks and $104 million in 51 Community Development Loan Funds (CDLFs). Collectively, these institutions operate in more than 3,000 locations across 47 states and the District of Columbia. A list of the participating community banks and CDLFs is in the Appendix of the Treasury’s inaugural report on its activities.5 Local governments have also provided capital to minority entrepreneurs. For example, my favorite ice cream shop in Chicago is not Ben & Jerry’s. Instead, it is an independent business called Shawn Michelle’s Homemade Ice Cream, located on the South Side of Chicago. The founders are an African American couple who received a $250,000 grant from the city of Chicago’s Neighborhood Opportunity Fund.

The Business Consortium Fund, Inc. (BCF) is a business development and financing organization created by the National Minority Supplier Development Council (NMSDC) to exclusively support the ethnic minority–owned business community. The BCF can provide direct loans to NMSDC certified minority-owned business enterprises (MBEs) in either a term loan (of a maximum seven years) or line of credit up to a maximum of $500,000 and a minimum of $75,000.6 The list of 73 BCF lenders covers 26 states.7

Another source of debt financing is SBA lenders. The number of SBA loans has fluctuated, rising from 37,528 in 2001 to 88,912 in 2005, and declining to 44,377 in 2012.8 During this period, the share of total loans to minorities has also varied similarly, rising from 25% to 29% and then declining to 23%. In the first half of 2019 it reached 32%.9 Large financial institutions that lend to minority firms include Wells Fargo and Accion USA, the largest business lender of its kind in the United States, which make loans from $500 to $25,000.10

Internet-based portals (a.k.a. “online marketplaces”) offering efficient loan application processes to the business owner have proliferated as business owners, lenders and technology entrepreneurs have worked together. Of course, many banks today offer “online application” services to prospective borrowers, which are no more than digital substitutes for completing what used to be a paper-based loan application at a bank branch. More interesting to consider are third-party websites, essentially digital two-sided marketplaces organized by technology entrepreneurs who aggregate hundreds of lenders to bid for or look at loan applications made by business owners. It has only been in the recent couple years that such lending activity was socially acceptable online, although similar websites had been available for personal loans. And only recently have business owners become comfortable with submitting their information through this impersonal process.

While there are too many such business loan marketplaces to mention, consider Intuit QuickBooks Financing11 or Biz2Credit12 as options. The technology behind Intuit’s QuickBooks Financing was developed by Brandon Hinkle, a former commercial loan officer who earned his MBA while starting a new venture, Plura Financial Solutions, which utilized sophisticated algorithms (interconnected rules) that interpreted loan application inputs to determine the fit of an applicant to several lending institutions. Intuit purchased Hinkle’s company in 2012 and hired him to adapt his system to their community of millions of QuickBooks users. After just a few short months Hinkle generated thousands of loan applications and loans for Intuit’s community of business owners, all made possible through the convenience and comfort of a QuickBooks account.13

Minorities—Equity Financing

Less than 1% of all equity capital provided by institutional investors has gone to minority entrepreneurs. African American women have fared even worse with 0.2% of equity investment. In the history of America, only 25 black female entrepreneurs have raised $1 million. Part of the problem is participation rates. For example, only 6.9% of entrepreneurs who presented their business concepts to angels were minority entrepreneurs. Strong evidence suggests that the problem is a lack of opportunity. The yield or percentage of approved investments for minority-owned firms was 7.1%, or close to two-thirds, the general yield rate. This makes no sense in light of the fact that from 1998 to 2011, investment firms targeting minorities returned an average of 20.9% compared to 11.8% for all private equity firms.14

Virtually all of that capital has come from firms that are associated with the National Association of Investment Companies (NAIC). These NAIC-related firms explicitly target investments in minority-owned companies and work together extensively to find minority investments. As proof, a survey of these firms indicated that 100% of them had participated in syndicated deals. Some also invest proactively in women entrepreneurs. NAIC is comprised of over 50 funds. These investors have more than $90 billion. Their investors are some of the nation’s largest institutional investors, including many public pension plans, corporate pension plans, foundations, and endowments.15

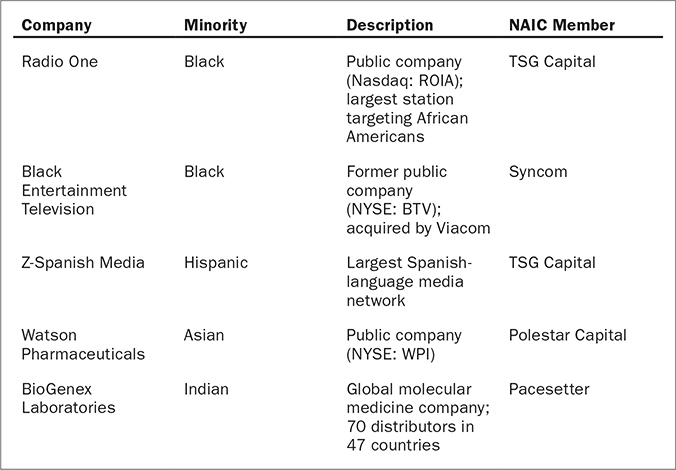

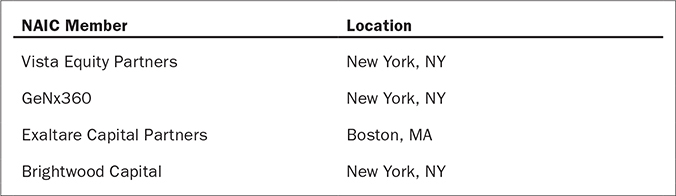

Almost every high-growth, successful, minority-owned company has received financing from an NAIC-affiliated firm. A few of the equity capital recipients are listed in Figure 10-2.

FIGURE 10-2 Various Equity Investments from NAIC Member Firms

Equity capital has also been made available to minority entrepreneurs by angel investors. Check for a local angel group in your area. The National Minority Angel Network (NMAN) was founded to identify diverse and otherwise unseen deal flow from primarily minority, woman, and veteran entrepreneurs and link them with investors and corporations that seek to invest in them or utilize their products or services. Entrepreneurs can be early-stage to late-stage and from any type of company (for-profit or not-for-profit) or industry. NMAN attempts to overcome geographical limitations by using technology services and a web-based portal for deal flow, document management, communications, and calendaring. See its website at www.nmanetwork.com.

Minority entrepreneurs who are seeking equity capital should contact the NAIC at www.naicpe.com to get a complete list of the member funds. A few are presented in Figure 10-3.

FIGURE 10-3 Various NAIC Members

Equity investments into minority entrepreneur firms often are combined with advice and coaching through organizations dedicated to their success. Together, as entrepreneurs become successful financially, the equity capital has a better chance of being returned to investors, at a multiple! Below is a list of several organizations that support minority entrepreneurs across the United States:

• ALPFA: Association of Latino Professionals in Finance and Accounting

• NBMBAA: National Black MBA Association

• NUL: National Urban League Entrepreneurship Centers

• NSBE: National Society of Black Engineers

• NMSDC: National Minority Supplier Development Council

• NSHMBA: National Society of Hispanic MBAs

• SCORE Minority Entrepreneurs

• The Latino Coalition

• UFSC: Urban Financial Services Coalition

Another great source for investors in black entrepreneurs is a Harvard Business School note titled “Sources of Capital for Black Entrepreneurs.” It includes one of the most thorough directories of investors who have invested in black entrepreneurs. It can be ordered from Harvard Business Publishing.16

Women—Debt Financing

Women have historically had a tougher time getting debt capital from institutions such as banks, but as that situation has become more visible, more organizations and programs have been developed to understand the issues and address them. The number of women-owned businesses that applied for funding in 2018 increased by 13% according to an annual study of women-owned companies by Biz2Credit, a leading online credit marketplace for small companies. It revealed that loans for women entrepreneurs were nearly one-third less than for their male counterparts.17 The study, which included 30,000 companies nationwide in more than 20 industries—including retail, healthcare, hospitality, construction, and professional services, among others—showed that the average loan amount for women-owned companies was $48,341 last year. The most common type of funding was working capital for business expansion. The study also found that average size loan for women-owned businesses was 31% less than for male-owned businesses ($70,239) in 2018.18 While the amounts shown are relatively small, the disparate differences demonstrate the point that women entrepreneurs have a different experience of debt capital than men.

Any person who is seriously interested in financing for women-owned businesses should read “The 2018 State of Women-Owned Businesses Report” commissioned by American Express. This is an outstanding must read annual document.

Women who are seeking debt financing should approach institutions that want to do business with women. Those firms include SBA lenders and banks such as Wells Fargo, which in 1994 made a commitment to lend $1 billion to women entrepreneurs. A year later, Wells Fargo became so convinced that financing women entrepreneurs was a great strategy that it increased its commitment to $10 billion, to be invested over a 10-year period. In the following 10 years, Wells Fargo lent more than $25 billion through 600,000 loans to women business owners, and it continues to be a leading lender to women.19 It is now committed to lend $55 billion to women by 2020! And its representatives say that the bank will have no problem meeting that goal and deadline.20 This additional commitment came after the National Foundation for Women Business Owners published research showing that investing in women entrepreneurs was sound business because they had a better chance of repaying business loans. This fact was proved by information showing that, on average, women-owned companies stay in business longer. Specifically, nearly 75% of women-owned firms founded in 1991 were still in business three years later, compared with 66% of all US firms.21 Other banks that have actively targeted women-owned businesses include KeyBank, through its Key4Women program,22 and Citi, which actively partners with organizations such as Women’s World Banking to help improve financial convenience and choice for borrowers, and most importantly, go the last mile to expand access for women across the globe. Both banks have successfully provided more than $1 billion in loans to women.23

As of 2019, there are 12.3 million women-owned businesses in the United States, according to a report by American Express.24 Compare that to 1972, when there were only 402,000 women-owned businesses, representing just 4.6% of all firms. Women are opening an average of 1,821 new businesses per day, and women of color founded 64% of those businesses. The study found that the number of women-owned businesses has increased 114% in the past two decades, and the number of companies owned by women of color has increased 467%. Minority women now own 46% of all women-owned firms, according to the report.

Lending activity from the SBA helps women-owned companies secure start-up and capital for growth.

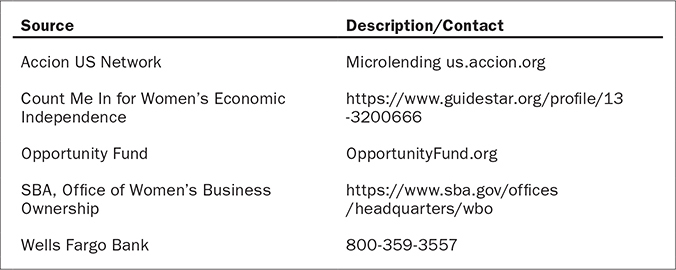

While the SBA has supported women’s businesses, the percentage of guaranteed loans going to women fell from 22% in 2004 to 14% in 2019. A few other institutional sources of debt capital for women entrepreneurs are listed in Figure 10-4.

FIGURE 10-4 Various Women-Focused Institutional Debt Sources

Women—Equity Financing

The year 2000 was the first year in which women received more than 2% of institutional equity capital. In 2000, they received 4.4%.25 According to the Robb study of firms from 2007 to 2010, women business owners generated only one-sixth of the outside equity capital compared to male business owners.26 According to a study commissioned by the Center for Women’s Business Research (formerly the National Foundation for Women Business Owners), women entrepreneurs who are seeking or have obtained equity capital find their sources of funding in three ways: word of mouth (60% of recipients, 49% of seekers), their own networks of business consultants (50% of recipients, 42% of seekers), and investors who have sought them out (38% of recipients, 39% of seekers).27

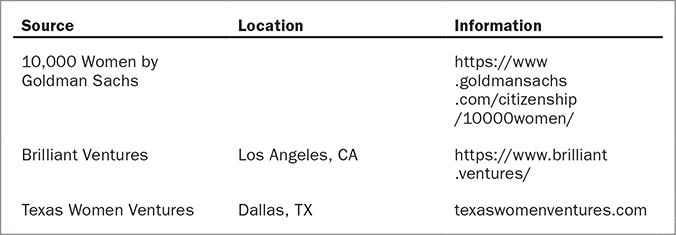

My advice would be the same as with the debt capital sources: go to sources that are interested in doing business with women. Figure 10-5 lists equity funds that target women entrepreneurs. Another great source of equity capital is angel investors. Figure 10-6 lists those investors who are interested in financing women entrepreneurs.

FIGURE 10-5 Women-Focused Private Equity Firms

FIGURE 10-6 Women-Focused Angel Investors

A leader in the campaign to accelerate women’s access to equity markets is Springboard Enterprises. Springboard states that it has assisted 769 women-led companies that participated in Springboard’s accelerator programs and subsequently have raised $9.5 billion. Overall, 83% of Springboard companies are still in business as independent or merged entities, including 19 IPOs. Springboard’s website (www.sb.co) has a Learning Center (https://sb.co/resources) that is a good resource for women entrepreneurs.

In addition to Springboard, there are several other resources and organizations devoted to helping women entrepreneurs. Some of these include:

• The Center for Women in Business (CWB), a program of the US Chamber of Commerce Foundation, promotes and empowers women business leaders to achieve their personal and professional goals (http://cwb.uschamber.com/).

• The SBA’s Online Women’s Business Center. The SBA’s Office of Women Owned Small Businesses (WOSB) and economically disadvantaged women-owned small business (EDWOSB) promotes the growth of women-owned businesses through various programs that address business training and technical assistance and provide access to credit and capital, federal contracts, and international trade opportunities. Every SBA district office has a women’s business ownership representative, providing a national network of resources for women entrepreneurs (http://www.sba.gov/wosb).

• National Association of Women Business Owners. The National Association of Women Business Owners (NAWBO.org), headquartered in the Washington, DC, metropolitan area, is the only dues-based national organization representing the interests of 10 million women entrepreneurs in all types of businesses. The organization currently has more than 80 chapters and is represented in 60 countries through its affiliation with the World Association of Women Entrepreneurs.

• Center for Women & Enterprise. CWE is the largest regional entrepreneurial training organization in Boston and Worcester, Massachusetts, and Providence, Rhode Island. Its mission is to empower women to become economically self-sufficient and prosperous through entrepreneurship (www.cweonline.org).

• Women’s Business Enterprise National Council (WBENC). WBENC, founded in 1997, is the largest third-party certifier of businesses owned, controlled, and operated by women in the United States. WBENC, a national 501(c)(3) nonprofit, partners with 14 regional partner organizations to provide its world-class standard of certification to women-owned businesses throughout the country. WBENC is also the nation’s leading advocate of women-owned businesses as suppliers to America’s corporations (www.wbenc.org).

• Women’s Business Development Center (WBDC). The WBDC, with headquarters in Chicago, offers a full-service approach to launching emerging businesses and strengthening existing businesses owned by women in a nine-state Midwestern area. Services of the WBDC include online e-learning, in-person workshops, and one-on-one counseling on all aspects of business development, including marketing, finance, business management, technology integration, and more. The WBDC has consulted with more than 66,000 women entrepreneurs, helping them to start and grow their businesses, and facilitated the receipt of more than $81 million in loans and $900 million in government and corporate contracts to women business owners (www.wbdc.org).

While things are improving for both women and minorities, it is not happening fast enough. Poor access to capital for these two groups is hurting America. Former SBA chief Aida Alvarez stated it beautifully when she said, “Businesses owned by women and minorities are multiplying at a faster rate than all other US businesses. If we don’t start investing now in the potential of the businesses, we will not have a successful economy in the new millennium.”28