14

FAQs on Entrepreneurship Television Shows—with Answers

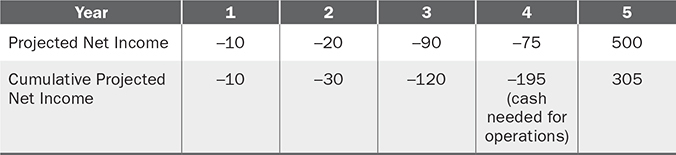

Question 1: How much money do you need?

Answer 1: The cash needed to purchase assets such as equipment, machines, desks, computers, etc., is very simple. Identify the cost of each item, multiply it by the number of units needed, and then add together to determine the money needed to purchase fixed assets. The cash needed for operations is determined by analyzing the pro forma (projections) income statement (profit and loss) and calculating the cumulative net income for each year. The year with the largest negative cumulative net income number is the amount of cash needed to operate your company (Chapter 4, “Financial Statement Analysis,” and Chapter 5, “Cash Flow Management”).

Therefore, the total cash needed is the sum of cash for fixed assets plus cash needed for operations.

Question 2: What is the value of your company if you want an investment of $250,000 for 7% of equity in your company?

Answer 2: The value of the company is $3,571,428 calculated by dividing the investment by the equity stake: $250,000/0.07 (Chapter 6, “Valuation”).

Question 3: Is the $3,571,428 valuation a premoney or postmoney valuation?

Answer 3: It is the postmoney valuation because it reflects the value of the company after the $250,000 has been invested. The premoney valuation is the company’s value before the investment is made. It is calculated by subtracting the investment from the postmoney valuation, or $3,571,428 minus $250,000 = premoney valuation of $3,321,428 (Chapter 6, “Valuation”).

Question 4: Your valuation is crazy! How can you justify that high valuation?

Answer 4: Premoney valuation can be calculated by using several valuation models, including the price/earnings ratio, multiple of EBITDA, or multiple of revenue. The $3,321,428 valuation could be justified by using a multiple of revenue model, where the company’s most recent annual revenue was $1,660,714. Therefore, the premoney valuation was calculated by multiplying 2 times the annual revenue. And this multiple is the same as the industry average of publicly owned companies (Chapter 4, “Financial Statement Analysis,” and Chapter 6, “Valuation”).

Question 5: What is your company’s EBITDA?

Answer 5: EBITDA is an acronym for earnings before interest, taxes, depreciation, and amortization. It is the company’s cash flow that is calculated by getting the sum of the net income plus interest expenses plus taxes plus depreciation expenses plus amortization expenses. EBITDA of at least 7% of revenue is considered excellent (Chapter 4, “Financial Statement Analysis,” and Chapter 6, “Valuation”).

Question 6: Do you want debt or equity financing?

Answer 6: Debt financing is a loan. Equity financing is selling part of the company. Debt is usually a cheaper cost of capital than equity. But debt must be repaid from the company’s cash flow. If the company is not profitable, it typically cannot raise debt, but must raise equity (Chapter 8, “Debt Financing,” and Chapter 9, “Equity Financing”).

Question 7: Who would you rather have as an investor, him or me?

Answer 7: The ideal is to raise money from investors you respect, can work with, and who bring value greater than their money. Entrepreneurs should raise capital from “value-added investors” who can invest money, give your company credibility, and introduce the entrepreneur to new customers, supplies, and employees (Chapter 7, “Raising Capital”).

Question 8: What are the company’s gross margins?

Answer 8: Investors love companies with nice, fat, high gross margins! The calculation is revenue minus cost of goods sold equals gross profit. Gross profit divided by revenue equals gross margin. This tells how much profit is generated after the product is made and sold, or in the case of a service company, after the services have been rendered. Gross margins greater than 50% are extremely attractive. For example, a company with 70% gross margin means for every dollar in revenue the company generates, it only costs 30 cents to make the product (Chapter 6, “Valuation”).

Question 9: Does your company have a subscription model?

Answer 9: Investors love companies that have a revenue subscription model because it assures multiple sales to the same customer. Repeat sales mean that revenues are more predictable, which investors love.

Question 10: What is the company’s burn rate?

Answer 10: Burn rate is the amount of money the company is losing each month, quarter, or year (Chapter 3, “Financial Statements”).

Question 11: What is the company’s customer acquisition cost?

Answer 11: Investors love this cost to be as low as possible. It is determined by identifying all costs, including marketing and advertising, associated with procuring new customers divided by the number of customers. If a company has 300,000 new customers this year and spent $2,500,000 on marketing and advertising, the customer acquisition cost was $8.33. This number should be compared to the industry average. If lower, then it is a positive trait of the company. The customer acquisition cost should also be analyzed as a percent of the company’s revenue. If this percent is too high it can be the primary reason why the company cannot make a profit. For example, if the customer acquisition cost is 40% of revenue, and the gross margins are 30%, then the company will never be profitable unless it increases its gross margins and/or reduce its customer acquisition cost (Chapter 4, “Financial Statement Analysis”).

Question 12: How do I get my money back?

Answer 12: Investors must be assured that their investment can eventually be liquid. This can happen if the company goes public and the investor sells her stock in the public markets, or the investor sells his stock to a third party or sells back to the company if the company never does an IPO. If the entrepreneur never wants to do an IPO, it may make an investor less interested because one of the options for liquidity has been eliminated (Chapter 9, “Equity Financing”).

Question 13: Why should I invest in you?

Answer 13: I can execute my plan to grow this company exponentially and profitably by using my operational skills. The result will be a fantastic ROI, cash on cash return, and IRR for you! (Chapter 9, “Equity Financing.”)