chapter 3

PROCESSING DATA THROUGH THE ACCOUNTING SYSTEM

DOUBLE-ENTRY ACCOUNTING SYSTEMS

Statement of Financial Position

UNDERSTANDING THE ACCOUNTING CYCLE

Recording Transactions in a Journal

RECORDING IN JOURNAL, LEDGER, AND TRIAL BALANCE

Preparing an Adjusted Trial Balance

PREPARING FINANCIAL STATEMENTS AND CLOSING ENTRIES

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Explain the role of debits and credits in the accounting system.

- Explain the difference between permanent and temporary accounts.

- Identify and explain the steps in the accounting cycle.

- Build a chart of accounts based on transactions that affect the company's assets, liabilities, and/or shareholder equity.

- Analyze transactions and record them in journal entry format.

- Post transactions from the journal to the ledger.

- Prepare a trial balance and use it to identify errors.

- Make adjusting entries to prepare an adjusted trial balance.

- Prepare financial statements.

- Explain closing entries and why they are necessary.

Learning to Handle the Dough

For generations, grandmothers in Grant Hooker's family would make a pastry of flattened, whole-wheat dough as a special treat, called a BeaverTail®, which became a Sunday staple with Mr. Hooker's own kids during the 1970s.

Mr. Hooker sold the family secret to the public for the first time in 1978, at a music festival near Killaloe, Ontario. The crowd loved it. The delectable dough was then served up at several Ottawa Valley agricultural fairs throughout that fall. Encouraged by the enthusiasm for his treats, Mr. Hooker, a builder by trade, trademarked the name “BeaverTails” and built his own booth in Ottawa's Byward Market in 1980 to sell them full-time. However, sales weren't as swift as at the fairs.

Undaunted, Mr. Hooker secured permission to sell BeaverTails on the Rideau Canal during Ottawa's Winterlude festival. “We had lineups down the lake,” he says. The whole family—Mr. Hooker's wife Pamela, and teenage son Nicholas and daughter Lisa—pitched in, giving out free samples and letting people know the treats were for sale year-round in the Market.

Within three years, BeaverTails Canada Inc. had the contract to sell all the food on the Rideau Canal and employed 450 people. The business continued to grow; BeaverTails began franchising in 1990 and now includes 97 locations across Canada, 2 in the United States, and 2 in the Kingdom of Saudi Arabia.

At first, keeping track of the money was straightforward and didn't require a formal accounting system. It meant little more than staying on top of how much was owed to suppliers and staff, and in rent and utilities. Mr. Hooker, who has no formal business training, got along fine simply managing the chequebook.

But this changed with franchising. “We weren't just selling products to people for cash, putting the cash in the bank, and then writing cheques for what we owed,” says Mr. Hooker. “We were into receivables; people owed us money.” The company also had liabilities—in the form of an operating loan from a bank.

Mr. Hooker hired an accountant to build the accounting system, working closely with him to learn how it worked. The breakthrough point for him, he says, was understanding that “cash is a debit on the balance sheet.” Assets (from the balance sheet) and expenses (from the statement of earnings) have normal debit balances. Liabilities and shareholders' equity (from the balance sheet) and revenues (from the statement of earnings) have normal credit balances. To increase the amount in an account, an entry has to be the same type as the balance, he adds. That is, debits increase debit accounts and credits increase credit accounts.

Now that he understands the basics of the accounting system, Mr. Hooker monitors it very closely. He insists that his accountant provide him with “TAMFS”—timely, accurate, monthly financial statements. “That is an absolute necessity any time a business grows to where the owner puts his trust in somebody else to handle the money,” he says. A lesson this entrepreneur learned as his business grew.

Now that you understand the basic accounting equation and can work through the analysis of some transactions, we are going to take you further into the practical side of accounting. We are going to show you how data is recorded in an accounting system so that organizations can easily extract information and summarize it into financial statements and other reports.

When you were working through Chapter 2, you used columns in tables to record the effects of transactions on the basic accounting equation. You could probably see that if you had to handle large volumes of accounts and transactions, this type of framework would become awkward to manage. Since real companies typically have hundreds of accounts and thousands of transactions, the accounting system for recording, summarizing, and reporting information about their economic activities requires something more elaborate than columnar tables.

USER RELEVANCE

Why is it important for users to have a good understanding of how accounting data are collected, stored, and reported? All business owners, such as Grant Hooker of BeaverTails, must understand how the financial statements reflect the company's business activities, especially if the owner intends to use the financial results to make decisions.

Investment analysts, who advise others on buying or selling shares, should also have in-depth knowledge of how an accounting system works. In order to understand what the numbers on financial statements mean, financial analysts need to know how the numbers are determined, and how relevant they are in understanding a company's overall profitability and financial position. Creditors, such as loan officers, need an in-depth understanding of the accounting process so that they can assess whether future cash flows will be adequate to meet the existing obligations, plus any future ones being contemplated. To do so, they need to understand what types of transactions affect which financial statement amounts.

Users should also be aware that decisions should not be made on single amounts or ratios. Rather, decision-makers should review the full set of results, because changes in one area of the financial statements will often have implications for other areas, which could affect the conclusions that are drawn.

DOUBLE-ENTRY ACCOUNTING SYSTEMS

The recording of transactions in a table or spreadsheet that has columns reflecting the basic accounting equation is sufficient if the entity has only a few transactions to record. This type of system is usually called a synoptic journal, and is used, for example, by community clubs that only need to maintain information about the dues they collect and the limited number of activities they undertake. However, using columnar tables or spreadsheets is cumbersome when large numbers of accounts and transactions are involved. To overcome this problem, accountants have developed a special system to record trans actions, which utilizes debits and credits and is known as the double-entry accounting system.

Before we introduce the role of debits and credits in an accounting system, we should point out that the method that we used to record transactions in Chapter 2 was a type of double-entry system, because each transaction affected two columns. In this way, we were able to keep the basic accounting equation in balance as each transaction was recorded. This principle also applies to double-entry accounting systems that use debits and credits rather than pluses and minuses, and that record the effects of transactions in accounts rather than columns.

LEARNING OBJECTIVE 1

Explain the role of debits and credits in the accounting system.

Debits and Credits

We will demonstrate the debit-credit system by using a simplified form of accounts, called T accounts. In the illustration below, notice that when this method is used to depict accounts the basic shape is a large letter T. Note also that the left side of a T account is known as the debit side, and the right side as the credit side.

GENERAL FORM OF A “T ACCOUNT”

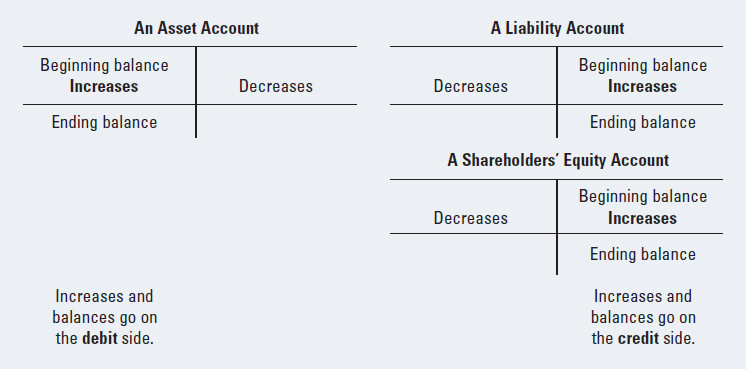

Thus, at the most basic level, the words “debit” and “credit” in accounting simply refer to the left and right sides of an account. As you will soon see, whether an entry on the debit (left) or credit (right) side of an account indicates an increase or a decrease depends on the type of account involved.

The T account concept can be used for each specific asset, liability, and share-holders' equity account. Therefore, instead of the columns that we used for recording transactions in Chapter 2, from this point onward each asset, liability, and shareholders' equity item will have its own T account.

Regardless of the type of account (asset, liability, or shareholders' equity), items recorded on the left side are called debits and items recorded on the right side are called credits. However, note this key distinction: for asset accounts, the balances are debits (i.e., recorded on the left side of the account), while for liability and shareholders' equity accounts, the balances are credits (i.e., recorded on the right side of the account). This is the basic “rule” regarding debits and credits in accounting.

This allows us to express the balancing nature of the accounting system in terms of debits and credits, rather than in terms of the basic accounting equation. By recording asset balances on the left side of their accounts and liability and shareholders' equity balances on the right side of their accounts, we can maintain the basic accounting equation (i.e., Assets = Liabilities + Shareholders' Equity) by ensuring that the sum of all the debits in the accounts equals the sum of all the credits (i.e., Debits = Credits). If transactions are recorded correctly, in terms of debit entries and credit entries, the total debits will always equal the total credits and the accounting system will be “balanced.”

HELPFUL HINT

To remember which side of an account is the debit side and which is the credit side, think of the equation Debits = Credits. The word “Debits” is on the left side of this equation, and debit entries are always recorded on the left side of an account. Similarly, the word “Credits” is on the right side of the equation, and credit entries are always recorded on the right side of an account.

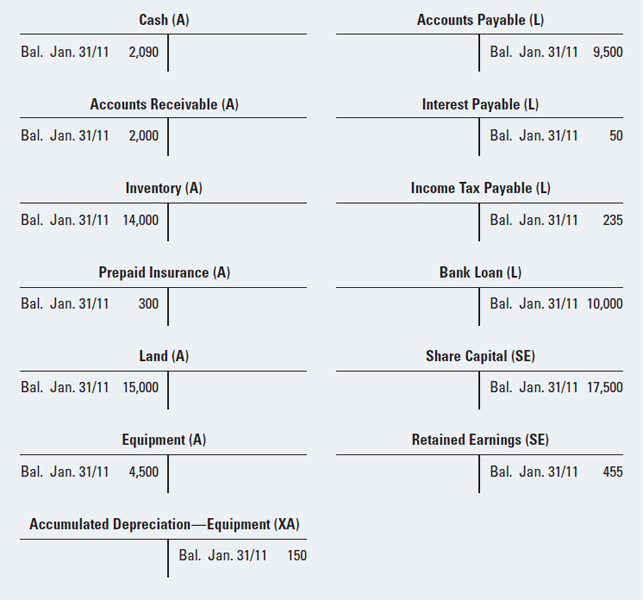

For example, Exhibit 3-1 shows how the balances for Demo Company at the end of January 2011 would be presented in T accounts. (As you probably recall, Demo Company was used to illustrate transactions in Chapter 2.) The accounts and balances are the same as those shown on Demo's statement of financial position for January 31, 2011, which was presented on page 105.

EXHIBIT 3-1 ACCOUNTS SHOWING THE BALANCES FOR DEMO COMPANY AS OF JANUARY 31, 2011

Notice the letters in the illustration, beside each of the account names. These letters will be used throughout this book to designate the type of account: (A) indicates an asset account, (L) a liability account, and (SE) a shareholders' equity account. These letters are intended to remind you of the type of account involved, and help you deal with it correctly.

HELPFUL HINT

To remember the sides on which different types of account balances should appear, think of the basic accounting equation (Assets = Liabilities + Shareholders' Equity). Assets are on the left side of this equation; hence, balances for assets are recorded on the left side of their T accounts. Similarly, liabilities and shareholders' equity are on the right side of the equation; hence, balances for liabilities and permanent shareholders' equity accounts are recorded on the right side of their T accounts.

In addition to these basic account categories, we will use (XA) to represent a contra-asset. At this point, we have only encountered one contra-asset, Accumulated Depreciation. However, other contra accounts will be introduced later. Remember that, when a statement of financial position is prepared, contra-assets are reported as deductions from their related assets. That is why the balance in Demo's contra-asset account, Accumulated Depreciation, is a credit while the balance in its related asset account, Equipment, is a debit. The fact that they are opposites indicates that one partially offsets the other.

Note that all of Demo's assets have debit balances, recorded on the left side of their T accounts, while all of its liabilities and shareholders' equity accounts have credit balances, recorded on the right side of their T accounts. Also remember that the accounting system ensures that Assets = Liabilities + Shareholders' Equity by keeping the total of the debit amounts equal to the total of the credit amounts.

We can now extend the basic rule regarding debits and credits, as follows:

- Because asset accounts have debit balances, increases in asset accounts are recorded as debits. It logically follows that decreases in assets are recorded as credits.

- Because liability and shareholders' equity accounts have credit balances, increases in liability and shareholders' equity accounts are recorded as credits. It logically follows that decreases in liabilities and shareholders' equity are recorded as debits.

Notice that asset accounts are treated in the opposite manner to liability and shareholders' equity accounts, in terms of debits and credits: debits increase assets, but decrease liabilities and shareholders' equity; credits increase liabilities and shareholders' equity, but decrease assets. Thus, whether the term “debit” or “credit” indicates an increase or decrease depends on the type of account.

Exhibit 3-2 illustrates the appropriate entries for asset, liability, and shareholders' equity accounts. This summarizes what are often referred to as “the rules of debit and credit.”

EXHIBIT 3-2 ENTRIES TO T ACCOUNTS:

A Summary of the Rules of Debit and Credit

HELPFUL HINT

Remember that increases in accounts are recorded in the same way as the account balances:

- Asset account balances are debits; increases in assets are also recorded as debits.

- Liability and Shareholders' Equity account balances are credits; increases in liabilities and shareholders' equity are also recorded as credits.

The easiest way to remember these rules is to focus on how increases are recorded for each type of account. Logically, decreases are recorded on the opposite side of the account. Also, since there will be more increases than decreases (because you cannot take more out of an account than you put into it), account balances will be on the same side as the increases.

As you would expect, since contra-assets are deductions from their related assets, they are recorded in the same way as decreases in asset accounts (i.e., as credits). In terms of balances, since asset accounts have debit balances, it is logical that contra-asset accounts have the opposite (i.e., credit balances).

Statement of Financial Position

One way to think about the accounts and debits and credits is to imagine that the accounting system is a warehouse that is balanced on a central point (like the equal sign between the two parts of the basic accounting equation). In the warehouse, the company has boxes on both sides, which maintain the balance. The boxes themselves are weightless, which means you do not need to have the same number of boxes on each side. Weight is added when something is put in a box. Each box represents an account. When the company needs to keep track of information about a specific financial item, it creates a new box, and labels it so that everyone knows what is in that box. For example, there would be a box (or account) labelled Cash on one side of the warehouse and another labelled Share Capital on the other side.

As financial activities are recorded, things are added to or removed from the appropriate boxes. In order to preserve the balance, if you add something to an asset box on one side of the warehouse, you have to either take something out of another asset box, on the same side of the warehouse, or go to the other side of the warehouse and add something to one of the boxes there (a liability or a shareholders' equity box).

Debiting and crediting accounts is like putting things into boxes and taking things out. All the asset boxes are kept on the left side of the warehouse, and each time you add something to an asset box, you debit it; each time you take something out of an asset box, you credit it. All the liability and shareholders' equity boxes are on the right side of the warehouse, where the opposite is true. Each time you put something into a liability or shareholders' equity box, you credit it; each time you take something out, you debit it. If you are careful to ensure that every debit to a box is counterbalanced with a credit to another box, the warehouse will remain balanced. Periodically, you can check all the boxes to see what is in each one, and use this information to prepare a statement of financial position.

The accounts shown in Exhibits 3-1 and 3-2 are all statement of financial position accounts. Therefore, they have balances that carry over from one period to the next. (Recall that a statement of financial position shows what the entity has at that point in time, to be carried forward to future periods.) Therefore, statement of financial position accounts are sometimes called permanent accounts.

LEARNING OBJECTIVE 2

Explain the difference between permanent and temporary accounts.

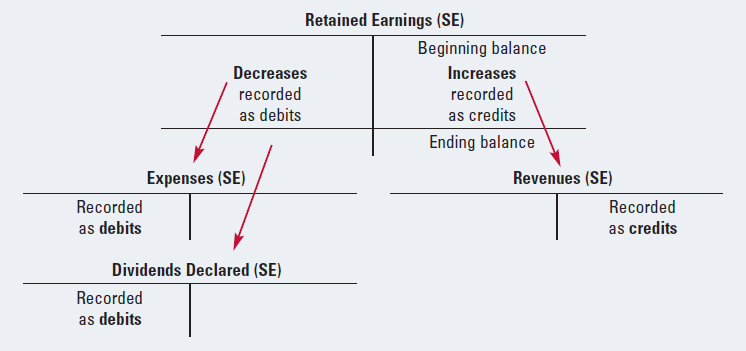

One of the permanent accounts is retained earnings. You learned in Chapter 1 that the change in retained earnings during a given period is the increase or decrease due to the net income or loss (the difference between the revenues and expenses for the period) and the decrease due to the dividends declared. In order to keep track of the individual revenue and expense amounts, as well as the dividends declared during the period, the retained earnings account can be subdivided into several separate accounts. These separate accounts are called temporary accounts because they are used temporarily, during the accounting period, to keep track of the revenues, expenses, and dividends. At the end of the accounting period, the balances in the temporary accounts are transferred into the retained earnings account.

While revenues, expenses, and dividends declared are all shareholders' equity accounts, increases and decreases in them are handled differently. For revenues, credits represent increases (and debits represent decreases). For expenses and dividends declared, the opposite is true: debits represent increases (and credits represent decreases). The logic of this is directly connected to their effect on shareholders' equity: revenues increase shareholders' equity and thus are recorded as credits, while expenses decrease shareholders' equity and so are recorded as debits. Therefore, revenue accounts have credit balances, expense accounts have debit balances, and the dividends declared account has a debit balance (until these balances are eliminated when they are transferred to the retained earnings account at the end of the period).

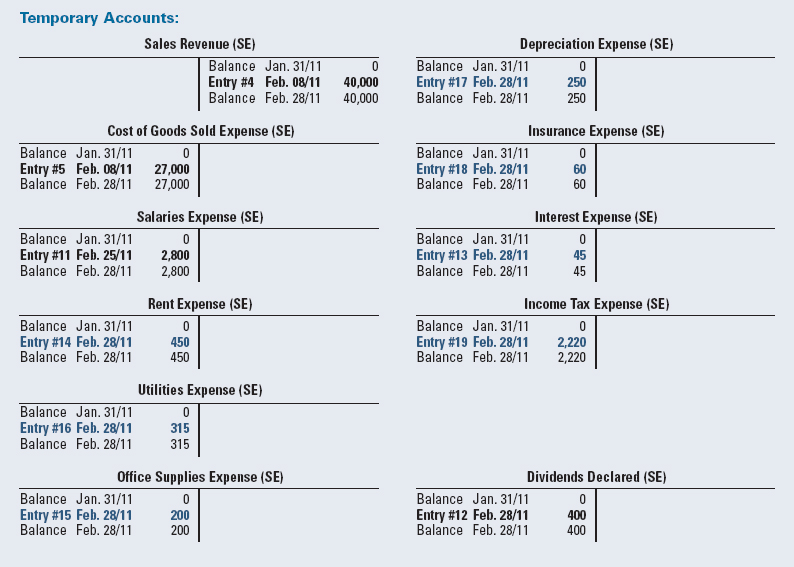

Exhibit 3-3 shows the subdivision of the retained earnings account into the temporary revenue, expense, and dividends declared accounts.

EXHIBIT 3-3 RETAINED EARNINGS:

Revenues, Expenses, and Dividends Accounts

Notice that the rules of debit and credit for these accounts follow the overall rule for shareholders' equity: increases in shareholders' equity are recorded as credits, and decreases in shareholders' equity are recorded as debits. Therefore,

- since revenues increase the shareholders' equity, they are recorded as credits

- since expenses and dividends decrease shareholders' equity, they are recorded as debits.

Several other things should be noted about the revenue, expense, and dividends declared accounts.

First, at the beginning of each new accounting period, the balance in each of these accounts is always zero. Because these accounts are used to keep track of the revenues, expenses, and dividends declared during the current period, their beginning balances must be zero so that amounts from previous periods will not be combined with those of the current period.

At the end of each accounting period, the balance in each of the temporary revenue and expense accounts is used to prepare the statement of earnings, and is then transferred into the permanent retained earnings account, along with the dividends, to produce the ending balance in the retained earnings account.

HELPFUL HINT

- Increases in revenues are recorded as credits, and revenue accounts have credit balances.

- Increases in expenses are recorded as debits, and expense accounts have debit balances.

- Dividends declared are recorded as debits, and the dividends declared account has a debit balance.

In this way, the retained earnings account keeps track of the cumulative amounts of revenues and expenses less dividends, and the temporary accounts keep track of only the amounts for the current period. In other words, using our warehouse example, the contents of the revenue, expense, and dividends declared boxes are all dumped into the retained earnings box at the end of each period. A revenue box, with a credit balance, will increase the retained earnings (which also has a credit balance). An expense or dividends declared box, with a debit balance, will decrease the retained earnings.

The debit balances in the expense and dividends declared accounts are probably best understood by remembering that they both represent decreases in the shareholders' equity. Because shareholders' equity is represented by a credit balance, decreases in it must be represented by debit balances. At the end of the period, when the balances in the temporary accounts are transferred to retained earnings, the debit balances in the expense and dividends accounts will normally be offset by the credit balances in the revenue accounts, leaving the retained earnings account with an overall credit balance.

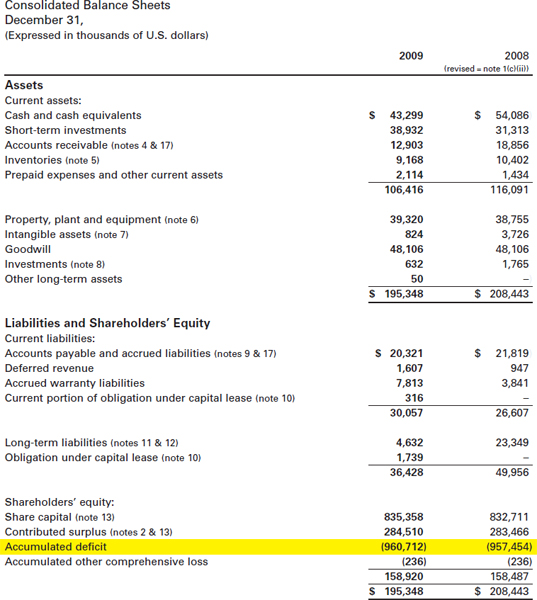

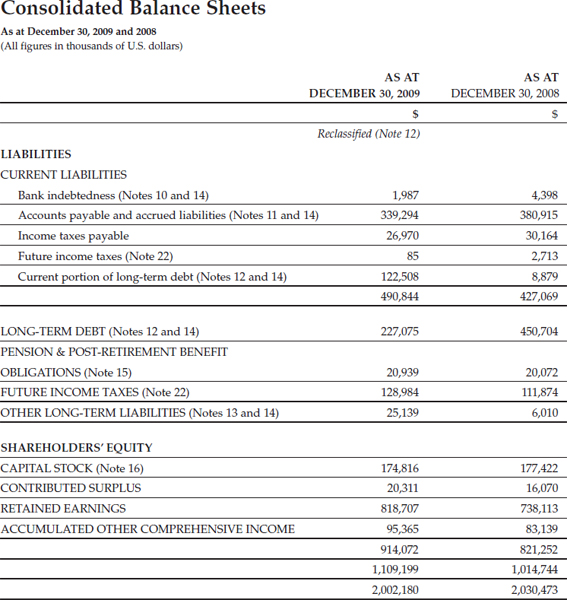

However, if expenses have exceeded revenues (i.e., the company has suffered losses), it is possible to have a debit balance in the retained earnings account. A debit balance in the retained earnings account indicates negative retained earnings, and is called a deficit. For example, if you look at the balance sheet (statement of financial position) of Ballard Power Systems Inc. in Exhibit 3-4, you will see that, rather than retained earnings, the company reported “accumulated deficit.” (Ballard Power Systems, with its head office, research and development, and manufacturing facilities in Burnaby, British Columbia, designs, manufactures, and sells fuel cells.) Most companies do not have deficits (i.e., negative amounts or debit balances in their retained earnings). However, it is not unusual for a company such as Ballard to have a deficit, as it is in the process of developing a new technology. It typically takes several years for companies to perfect such technologies to the stage where they can be commercialized widely and generate profits. In the meantime, losses are incurred and negative retained earnings are accumulated.

EXHIBIT 3-4 BALLARD POWER SYSTEMS INC. 2009 ANNUAL REPORT

BALLARD POWER SYSTEMS INC. 2009 ANNUAL REPORT

Animated Tutorials & Videos: Accounting Cycle Tutorial

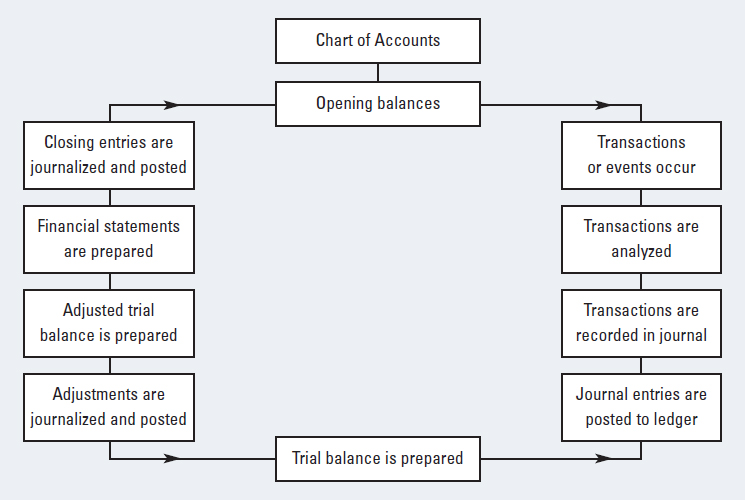

UNDERSTANDING THE ACCOUNTING CYCLE

We are now ready to look at the whole system by which transactions are first measured, recorded, and summarized, and then communicated to users through financial statements. This system is called the accounting cycle because it is repeated each accounting period.

Exhibit 3-5 illustrates the complete cycle. Each of the steps will be discussed in the subsections that follow.

As we proceed through a discussion of the accounting cycle, we will demonstrate each stage by continuing the Demo Company example that we began in Chapter 2. In that chapter, we analyzed Demo's January transactions, recorded their effects in a columnar table, and used the table to prepare the company's financial statements for the month of January. In this chapter, we will use Demo's February transactions to explain how these would be handled in a formal accounting system and illustrate each of the steps in the accounting cycle.

A system for maintaining accounting records can be as simple as a notebook, in which everything is processed by hand, or as sophisticated as an on-line system in which most of the processing is done by computers. We will use a simple manual system to illustrate the accounting cycle. However, the same underlying processes apply to any accounting system, no matter how simple or sophisticated it is.

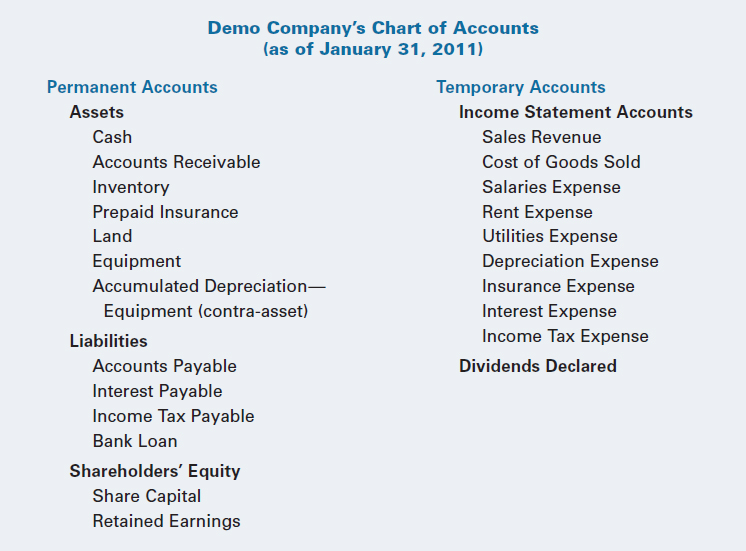

The Chart of Accounts

Imagine a company that has just been formed and whose managers need to set up an accounting system. One of the first things they must determine is what information they need to run the business. What information is important for them to make well-informed decisions? What information is needed by outside users? What is required to satisfy financial reporting standards? Accounting systems are information systems, so managers should decide at the outset what information they need in order to operate the business and satisfy the requirements of other users. These needs vary, so even companies in the same type of business will develop their own unique information systems and use different accounts.

EXHIBIT 3-5 THE ACCOUNTING CYCLE

Once a company has decided what accounts it needs to have, in order to get the information that it requires, the types of accounting information to be recorded in the accounting system (represented by the accounts to be used) are generally summarized in a chart of accounts. The chart of accounts is the starting point for the company's accounting cycle. However, the chart of accounts is dynamic, rather than something that cannot be changed. As the business changes, it may need to have different types of accounts. For example, suppose that the company did not originally provide credit to its customers; all of its sales were for cash. In that case, there would have been no need for an accounts receivable account. Later, if the company decided to allow customers to buy on credit, it would need to add an accounts receivable account to its chart of accounts.

LEARNING OBJECTIVE 4

Build a chart of accounts based on transactions that affect the company's assets, liabilities, and/or shareholder equity.

Although there are certain account titles that are commonly used, an account can be given any name that makes sense to the company and describes the account's purpose. In an actual accounting system, each of the accounts in the chart of accounts would also be identified by a number that indicates the sequence of the accounts and makes it easier to record transactions in a computerized system. In this book, accounts will be designated by their names and not by account numbers.

EXHIBIT 3-6 DEMO COMPANY'S CHART OF ACCOUNTS

Exhibit 3-6 shows the chart of accounts for Demo Company, as of the end of January 2011. It consists of all the accounts that were used to record Demo's transactions in Chapter 2.

Later in this chapter, as we record Demo's February transactions, we will need to create some new accounts; as new accounts are created, they are added to the company's chart of accounts.

Notice that the accounts are listed in the chart of accounts in the order in which they will appear on the financial statements. Accounts are kept in this order so that it is easy to locate them in the ledger, and to facilitate the preparation of the financial statements. If account numbers are assigned to the accounts, a different set of account numbers will usually be assigned to each section of the financial statements. For example, many companies using four-digit account numbers will assign numbers between 1000 and 1999 to current assets only, so that all the accounts given those numbers will be easily identifiable as current assets. When the computer system prepares a statement of financial position, in the current assets section it will list these accounts in numerical order, according to the account numbers they were assigned.

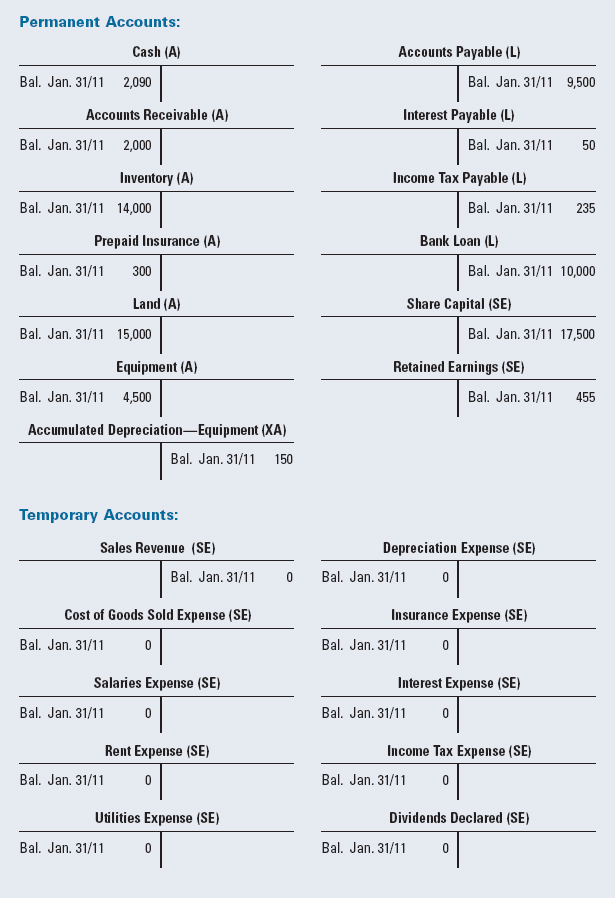

The Opening Balances

As indicated in the chart of accounts, the permanent accounts are the statement of financial position accounts: assets, liabilities, and the main shareholders' equity accounts (at this stage, the share capital and retained earnings). The balances of the permanent accounts at the beginning of each accounting period are the amounts carried forward from the end of the previous accounting period. Exhibit 3-1 shows the opening balances in Demo's permanent accounts at the beginning of February 2011 (i.e., the amounts brought forward from its statement of financial position at the end of January, as determined in Chapter 2). Demo's temporary accounts at the beginning of February will all have zero balances, since every company starts each new accounting period with zero balances in its temporary accounts.

Exhibit 3-7 presents the complete set of Demo Company's accounts at the beginning of February 2011. Note that the balances in the permanent accounts are the same as those in Exhibit 3-1, and that the balances in all the temporary accounts are zero.

Note that there is a T account for each account listed in the chart of accounts (Exhibit 3-6). Also note that the temporary accounts for revenues, expenses, and dividends declared have been segregated from the permanent accounts, since only the permanent accounts have balances brought forward from the end of the previous accounting period.

TRANSACTIONS

The next step in the accounting cycle is to identify whether an event or transaction has occurred that affects the company's assets, liabilities, and/or shareholders' equity. If so, its effects on the company's accounts will have to be analyzed and recorded.

Evidence of a transaction or event is usually some sort of “source document”—a document that is received or created by the company indicating that something that needs to be recorded has happened. Examples of source documents include invoices, cheques, cash register tapes, bank deposit slips, and shipping documents.

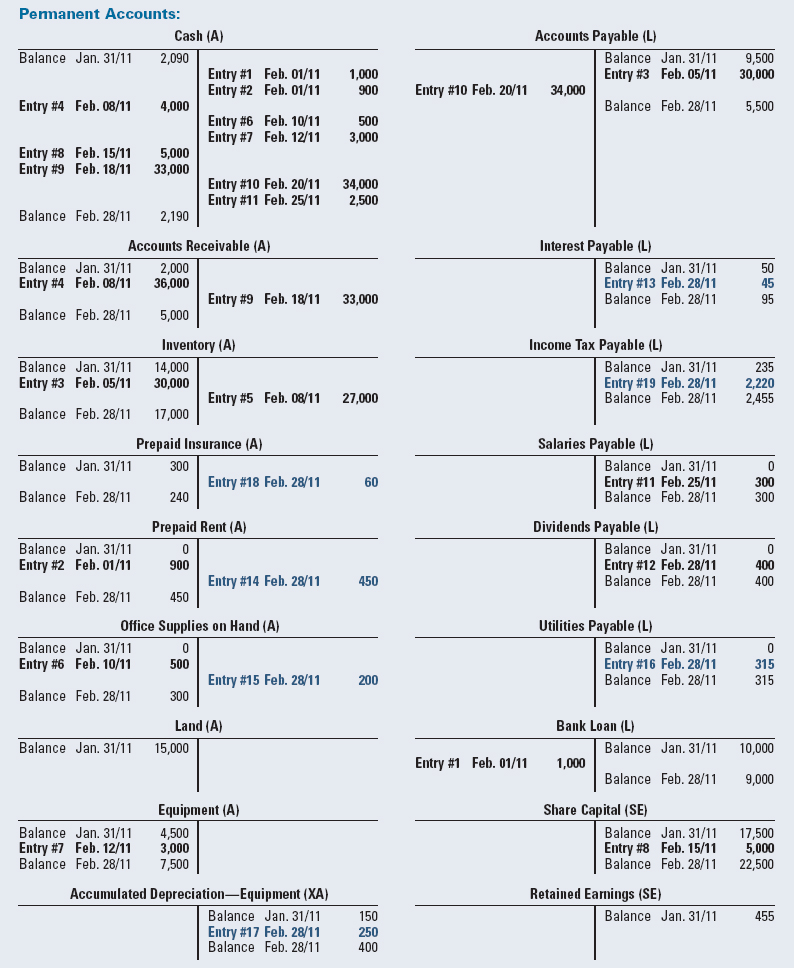

EXHIBIT 3-7 DEMO COMPANY'S T ACCOUNTS, WITH BEGINNING BALANCES AS AT FEBRUARY 1, 2011

Analyzing Transactions

When a transaction or event has occurred, the accountant must analyze it to determine what accounts have been affected and how the transaction should be recorded in the accounting system. We introduced this phase of the process in Chapter 2, where we analyzed the effects of various transactions on the basic accounting equation and recorded the results by entering positive and negative amounts in a columnar table. In this chapter—and throughout the remainder of this book—we will analyze the effects of transactions to see how they should be recorded as debits and credits in a company's accounts.

Routine transactions, such as the purchase or sale of goods, need to be analyzed only once. After that, each subsequent purchase or sale transaction is handled in the same way and can be entered into the accounting system without further analysis. Unique and unusual transactions require special analysis, however, and sometimes require the services of a professional accountant who understands the use of appropriate accounting methods, according to generally accepted accounting principles, practices, and standards.

Recording Transactions in a Journal

After an accountant has decided how to record transactions, appropriate entries must be made in the accounting system. The initial entries are usually made in what is known as a journal. A journal is a chronological listing of all the events that are recorded in the accounting system. A journal could be as simple as a piece of paper on which a chronological list of the transactions that have occurred is recorded, but most organization's journals are now kept in computerized form. Each complete entry made in the journal shows the effects of a transaction or business event on the company's accounts, and is called a journal entry.

When entries are made to record transactions in a journal, they are always dated and often each of them is given a sequential entry number. Then, the names of the accounts affected by the transaction, and the amounts involved, are listed. The accounts being debited are listed first, followed by the accounts being credited, and the credit portions are indented. Finally, an explanation of the transaction is often included with the journal entry, for future reference.

To summarize the preceding paragraph, complete journal entries typically consist of the date and entry number, a listing of the names of the accounts affected (with their account numbers, if applicable), and the amounts being debited and credited, followed by a brief explanation. In this book, we will use the following format for presenting journal entries:

BASIC FORMAT FOR A JOURNAL ENTRY

As illustrated above, when journal entries are made the customary practice is to list the accounts that are being debited before the accounts that are being credited, and to indent the accounts that are being credited. Of course, each complete journal entry must keep the accounting system balanced; that is, the amount debited must equal the amount credited. (Accounting software generally contains internal subroutines that automatically check journal entries to ensure that they are balanced, and alert the user to any problems that must be fixed before proceeding.)

HELPFUL HINT

Accountants frequently use the abbreviation Dr. and Cr. for debit and credit, respectively (even though there is no “r” in “debit”).

We will now illustrate the process of analyzing transactions and recording them as journal entries by working through Demo's February transactions. Each transaction will be presented and analyzed, to determine what accounts are affected and whether they should be debited or credited. Then the journal entry to record the transaction will be presented. You should study this material carefully to ensure that you understand how the rules of debit and credit are applied and how journal entries are used to record transactions in an accounting system.

Transaction 1: Repayment of Loan

On February 1, 2011, Demo Company pays off $1,000 of the principal of its bank loan.

ANALYSIS Since Demo is paying off part of its bank loan, this liability account should be reduced. At the same time, the company is making a cash payment, so this asset account should be reduced.

Note that repaying the principal of a loan does not involve an expense. The expense associated with a loan is the interest charged on it, which is recorded separately.

ANALYSIS OF TRANSACTION 1

Liabilities (Bank Loan) decreased by $1,000

Assets (Cash) decreased by $1,000

These changes in the accounts are now translated into debits and credits. The rules of debit and credit specify that liability accounts have credit balances. Therefore, they are reduced by making debit entries. Accordingly, the liability account Bank Loan must be debited. Conversely, asset accounts have debit balances and therefore are reduced by making credit entries. Accordingly, the asset account Cash must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 1

Transaction 2: Prepayment of Rent

On February 1, Demo Company signs a one-year lease agreement for office and storage space. The rent is to be $450 per month, and Demo pays the first and last months' rent (a total of $900) immediately. Thereafter, the monthly rent is to be paid on the first day of each month.

ANALYSIS Since the company is paying rent in advance, an asset is created (which would usually be called Prepaid Rent). At the same time, the company is making a cash payment, so this asset account should be reduced.

Like insurance, which is also paid in advance (discussed in Chapter 2), rent should not be recorded as an expense until the cost has expired (been used up). This is why rent expense is not recorded at this time.

ANALYSIS OF TRANSACTION 2

Assets (Prepaid Rent) increased by $900

Assets (Cash) decreased by $900

We now translate these changes into debits and credits for the journal entry. The rules of debit and credit specify that asset accounts have debit balances. Therefore, they are increased by making debit entries, and decreased by making credit entries. Accordingly, the asset account Prepaid Rent must be debited, and the asset account Cash must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 2

Transaction 3: Purchase of Inventory on Account

On February 5, the company buys $30,000 of additional inventory on account.

ANALYSIS As we saw in Chapter 2, when goods are purchased to be sold in the future, the asset Inventory is increased. At the same time, since the purchase is on account and payment will not be made until later, the liability Accounts Payable is increased.

ANALYSIS OF TRANSACTION 3

Assets (Inventory) increased by $30,000

Liabilities (Accounts Payable) increased by $30,000

We now translate these changes in the accounts into debits and credits. The rules of debit and credit specify that asset accounts have debit balances, and are therefore increased by making debit entries. Conversely, liability accounts have credit balances, and are increased by making credit entries. Accordingly, the asset Inventory must be debited, and the liability Accounts Payable must be credited. Thus, this transaction is recorded in the journal as follows:

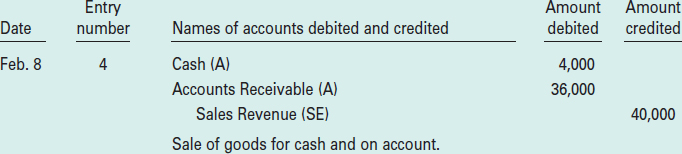

Transaction 4: Sales for Cash and on Account

On February 8, the company sells goods to customers for $40,000. Of these sales, $4,000 are for cash; the remaining $36,000 are on account.

ANALYSIS When goods are sold to customers, the company's assets are increased and revenue is earned, equal to the selling price of the goods that have been sold—i.e., the amount that is received, or will be received, from the sale. In this case, the assets Cash and Accounts Receivable are increased by $4,000 and $36,000, respectively, and revenue of $40,000 is recognized. (Remember that, under the accrual basis of accounting, revenue is generally recognized when the sale is made, not when the cash is collected.) Because it affects the net earnings and, ultimately, the retained earnings, revenue is a shareholders' equity account.

ANALYSIS OF TRANSACTION 4

Assets increased by $40,000 (Cash of $4,000 and Accounts Receivable of $36,000)

Shareholders' Equity increased by $40,000 (recorded as Sales Revenue)

These changes in the accounts are now translated into debits and credits. Assets are increased by making debit entries. Accordingly, the asset accounts Cash and Accounts Receivable must both be debited. Conversely, the rules of debit and credit specify that shareholders' equity is increased by making credit entries. Therefore, the Sales Revenue account must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 4

Notice that the above journal entry has three parts. However, the sum of the two debit parts (4,000 and 36,000) is equal to the credit part (40,000), so the entry as a whole is in balance. This illustrates the fact that, although every journal entry must have at least one debit and one credit, a journal entry can have any number of debit and credit parts, as long as the sum of the amounts debited is equal to the sum of the amounts credited. The term compound journal entry is used for a journal entry that has more than two parts.

Transaction 5: Cost of Goods Sold

The company determines that the cost of the goods that were sold on February 8 is $27,000.

ANALYSIS As you should recall from Chapter 2, when goods are sold their cost must be removed from the asset account Inventory and transferred to the expense account Cost of Goods Sold. In other words, in addition to the revenue that is earned when a sale is made, the company's assets are decreased and an expense is incurred, equal to the cost of the goods that have been sold. In this case, the asset Inventory is decreased by $27,000 and an expense of the same amount is recognized. Because they affect the net earnings and, ultimately, the retained earnings, expenses are shareholders' equity accounts.

ANALYSIS OF TRANSACTION 5

Shareholders' Equity decreased by $27,000 (recorded as Cost of Goods Sold)

Assets (Inventory) decreased by $27,000

We now translate these changes into debits and credits for the journal entry. Shareholders' equity is decreased by making debit entries. Therefore, the Cost of Goods Sold account must be debited. At the same time, since assets are decreased by making credit entries, the Inventory account must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 5

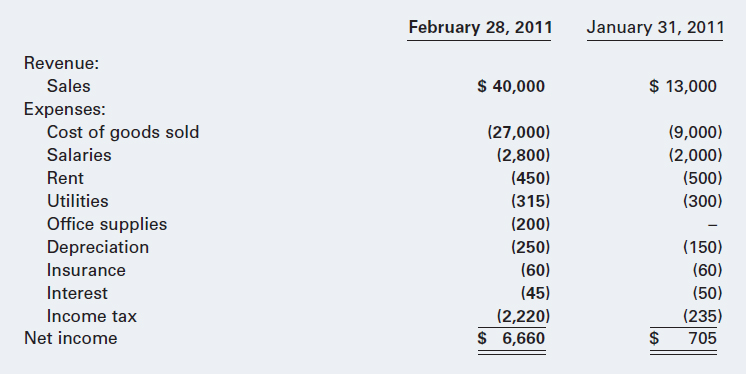

Transactions 4 and 5 are logically linked, because when goods are sold the company's assets are increased and revenue is earned (equal to the selling price of the goods that have been sold), and at the same time the company's assets are decreased and an expense is incurred (equal to the cost of the goods that have been sold). Subtracting the expense from the revenue reveals the amount of profit made on the sale. In this case, goods costing $27,000 were sold for $40,000, resulting in a gross profit of $13,000. This is referred to as gross profit because there are many other expenses—salaries, rent, utilities, etc.—that have to be deducted to determine the company's net profit or earnings for the period. (In accounting, the term “gross” is generally used to refer to the initial amount of an item, before certain deductions from it have been made; and the term “net” is used to refer to the final amount of an item, after the deductions from it have been made.)

Transaction 6: Purchase of Supplies for Cash

On February 10, Demo Company buys office supplies for $500 cash.

ANALYSIS Whenever something is purchased to be used in the future, it should be recorded as an asset. We will refer to this asset account as Office Supplies on Hand. Since cash is paid for the purchase, the asset account Cash is decreased.

Note that, since these office supplies will be used in the future operations of the business, there is no expense recorded at this point. Eventually, when the supplies are consumed, their cost will be transferred to an expense account; however, as long as they are on hand they are an asset. This is similar to the treatment of merchandise inventory, prepaid insurance, and prepaid rent.

ANALYSIS OF TRANSACTION 6

Assets (Office Supplies on Hand) increased by $500

Assets (Cash) decreased by $500

We now translate these changes in the accounts into debits and credits. The rules of debit and credit specify that asset accounts have debit balances, and are therefore increased by making debit entries and decreased by making credit entries. Accordingly, the asset Office Supplies on Hand must be debited, and the asset Cash must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 6

Transaction 7: Purchase of Equipment for Cash

On February 12, the company buys additional equipment for $3,000 cash.

ANALYSIS This is similar to Transaction 6. Equipment is purchased to be used in the future, so the asset Equipment is increased. At the same time, since it is a cash purchase, the asset Cash is decreased.

As with the office supplies in Transaction 6, the equipment will be used in the future operations of the business. Therefore, at this point it is an asset. Eventually, however, as the value of the equipment is consumed, its cost will have to be transferred to an expense account. For long-term assets like equipment, whose benefits are used up gradually over many accounting periods, this is done through the process of depreciation (discussed in Chapter 2).

Asset accounts have debit balances, and are therefore increased by making debit entries and decreased by making credit entries. Accordingly, the asset Equipment must be debited, and the asset Cash must be credited. Therefore, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 7

Transaction 8: Issuance of Shares for Cash

On February 15, shareholders invest an additional $5,000 cash in the business.

ANALYSIS As we saw in Chapter 2, when people invest cash in a business they are issued shares in the company, as evidence of their investment. Consequently, the company has an increase in its assets, in the form of Cash, and an increase in its shareholders' equity, in the form of Share Capital.

ANALYSIS OF TRANSACTION 8

Assets (Cash) increased by $5,000

Shareholders' Equity (Share Capital) increased by $5,000

Assets are increased by making debit entries. Accordingly, the asset account Cash must be debited. Conversely, the rules of debit and credit specify that shareholders' equity is increased by making credit entries. Therefore, the Share Capital account must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 8

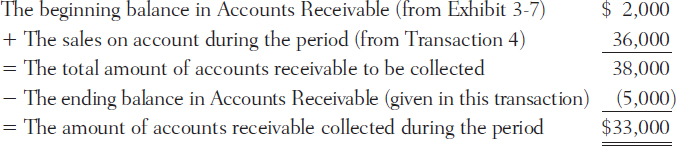

Transaction 9: Collections from Customers on Account

On February 18, Demo collects all but $5,000 of the amounts due from its customers.

ANALYSIS Notice that the amount given in the description of this transaction is not the amount of cash that was collected. Rather, it is the amount that was not collected; in other words, it is the ending balance of accounts receivable.

This illustrates an important difference in the type of information you may be given regarding a transaction, which you will encounter in some cases. Rather than simply being given the amount of the transaction, you may be given the remaining balance in a related account. In such cases, you will have to use the given information to logically determine the amount to be recorded in the journal entry.

In this case, in order to prepare the journal entry for this transaction we need to determine the amount of cash that was collected. This can be done by using the following relationships:

As discussed in Chapter 2, when a company receives payments from its customers on account, one asset (Cash) increases and another asset (Accounts Receivable) decreases. No revenue is recognized when cash is collected on account, because under the accrual basis of accounting the revenue is recognized when the sale is made, not when the cash is collected.

ANALYSIS OF TRANSACTION 9

Assets (Cash) increased by $33,000

Assets (Accounts Receivable) decreased by $33,000

Asset accounts have debit balances, and are therefore increased by making debit entries and decreased by making credit entries. Accordingly, the asset Cash must be debited, and the asset Accounts Receivable must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 9

Note again that the $5,000 given in the description of this transaction does not appear in the journal entry. Rather, since it was a balance, it was used to calculate the $33,000 recorded in the above entry. From this point onward, you will have to watch for situations like this, in which you are given information about the balance in an account, rather than the amount of a particular transaction. In these cases, you will need to bear in mind that a balance is not recorded with a journal entry; a balance is the net amount remaining in an account, as a result of all the preceding transactions affecting that account. Therefore, if you are trying to record a transaction but are given information regarding the balance in an account, you will need to use it—together with your knowledge of the logical relationships affecting that account—to calculate the amount to be recorded in the journal entry, as we did for this transaction. We will see more examples of this process in later transactions.

Transaction 10: Payments to Suppliers on Account

On February 20, Demo Company makes payments of $34,000 on its accounts payable.

ANALYSIS As we discussed in Chapter 2, when a company pays for previous purchases on account, both its liabilities (Accounts Payable) and its assets (Cash) are reduced.

ANALYSIS OF TRANSACTION 10

Liabilities (Accounts Payable) decreased by $34,000

Assets (Cash) decreased by $34,000

Liabilities have credit balances, and are therefore decreased by making debit entries. Accordingly, the liability Accounts Payable must be debited. Conversely, assets have debit balances, and are therefore decreased by making credit entries, so the Cash account must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 10

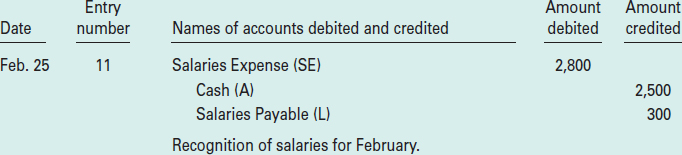

Transaction 11: Salaries Expense

On February 25, the company pays $2,500 for salaries. In addition, it still owes $300 to employees for time worked during February, which will be paid in March.

ANALYSIS According to the accrual basis of accounting, the amount of salaries expense that should be recorded each period is the amount that is incurred that period, rather than simply the amount that is paid during the period. Therefore, the amount of salaries expense to be recorded for the month of February is $2,500 + $300 = $2,800.

It should be noted that Demo did not have any salaries payable at the end of January. (This can be confirmed by checking the balances in Exhibit 3-7.) If there had been salaries payable at the beginning of February (i.e., brought forward from January), this amount would have been deducted in the calculation above. This is because, if you are calculating the amount of salaries expense to be recorded for the month of February, any salaries paid during February for the month of January should be excluded from the February expense.

Since expenses reduce net income and, ultimately, retained earnings, the salaries expense causes a decrease in shareholder's equity. At the same time, assets (in the form of Cash) are decreased by the amount paid, and liabilities (in the form of Salaries Payable) are increased by the amount owing.

ANALYSIS OF TRANSACTION 11

Shareholders' Equity decreased by $2,800 (recorded as Salaries Expense)

Assets (Cash) decreased by $2,500

Liabilities (Salaries Payable) increased by $300

Shareholders' Equity is decreased by making debit entries. Therefore, since expenses are temporary shareholders' equity accounts, the Salaries Expense account must be debited. Because assets are decreased by making credit entries, the Cash account must be credited. Since liabilities are increased by making credit entries, the Salaries Payable account must also be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 11

This is another example of a compound journal entry. Note that although it has two credits and only one debit, the amount debited equals the total amount credited.

Transaction 12: Declaration of Dividends to Be Paid Later

On February 28, dividends of $400 are declared. However, they will not be paid to the shareholders until March.

ANALYSIS Dividends have to be recorded as soon as they are declared. If they are not paid immediately, the declaration creates a legal obligation for the company to make the payment later, which means that a liability has to be recorded.

Dividends reduce shareholder's equity, by reducing the amount of retained earnings. They are usually recorded in a temporary account called Dividends Declared. At the same time, if they are not paid they increase liabilities (in the form of Dividends Payable) by the amount owing.

ANALYSIS OF TRANSACTION 12

Shareholders' Equity decreased by $400 (recorded as Dividends Declared)

Liabilities (Dividends Payable) increased by $400

Shareholders' Equity is decreased by making debit entries. Therefore, the temporary shareholders' equity account called Dividends Declared is debited. At the same time, since liabilities are increased by making credit entries, the Dividends Payable account must be credited. Accordingly, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR TRANSACTION 12

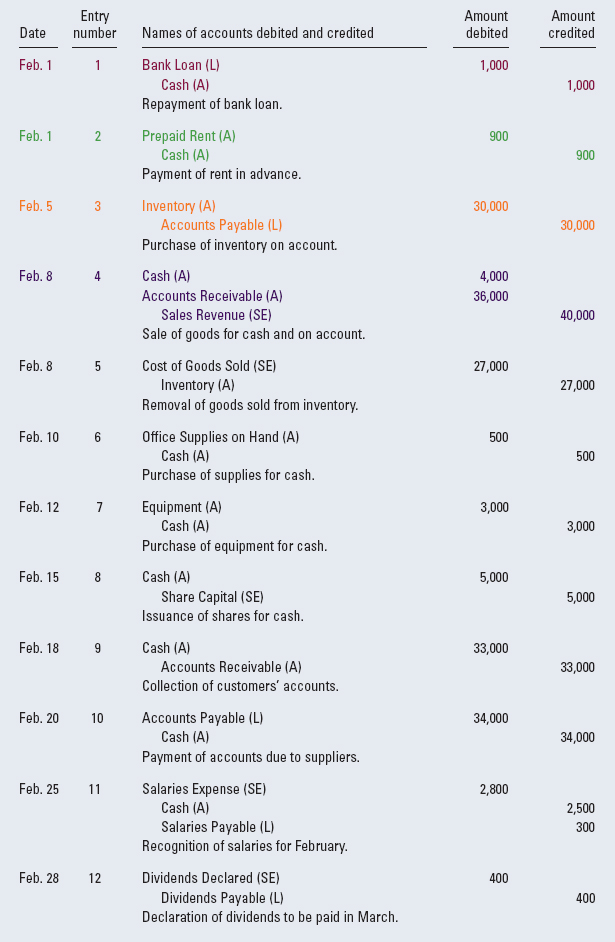

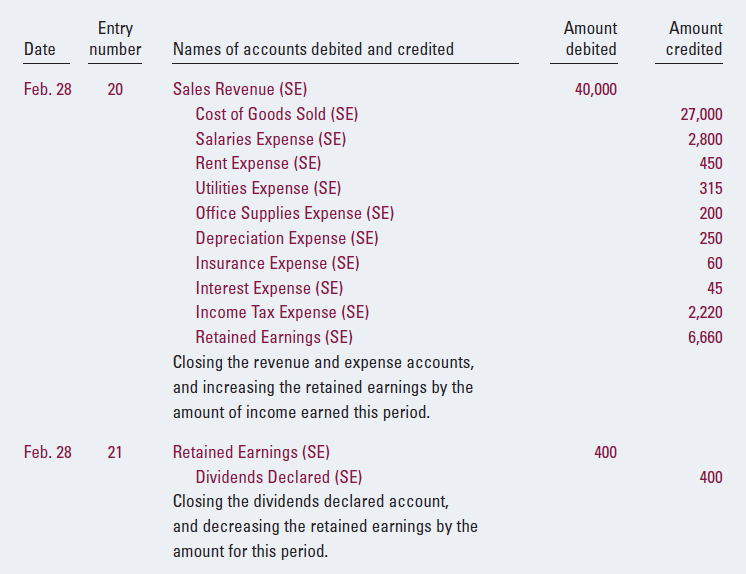

This completes Demo Company's transactions for February. Exhibit 3-8 shows the company's journal at this stage, with all the transactions recorded in it. The first four journal entries have been colour-coded for easy reference in the following section, which illustrates the posting process.

LEARNING OBJECTIVE 6

Post transactions from the journal to the ledger.

RECORDING IN JOURNAL, LEDGER, AND TRIAL BALANCE

Posting to the Ledger

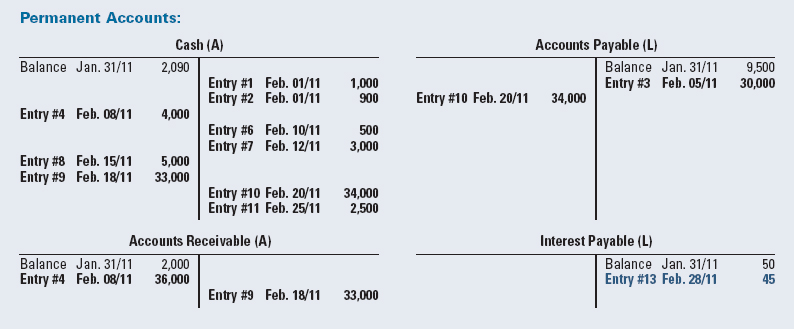

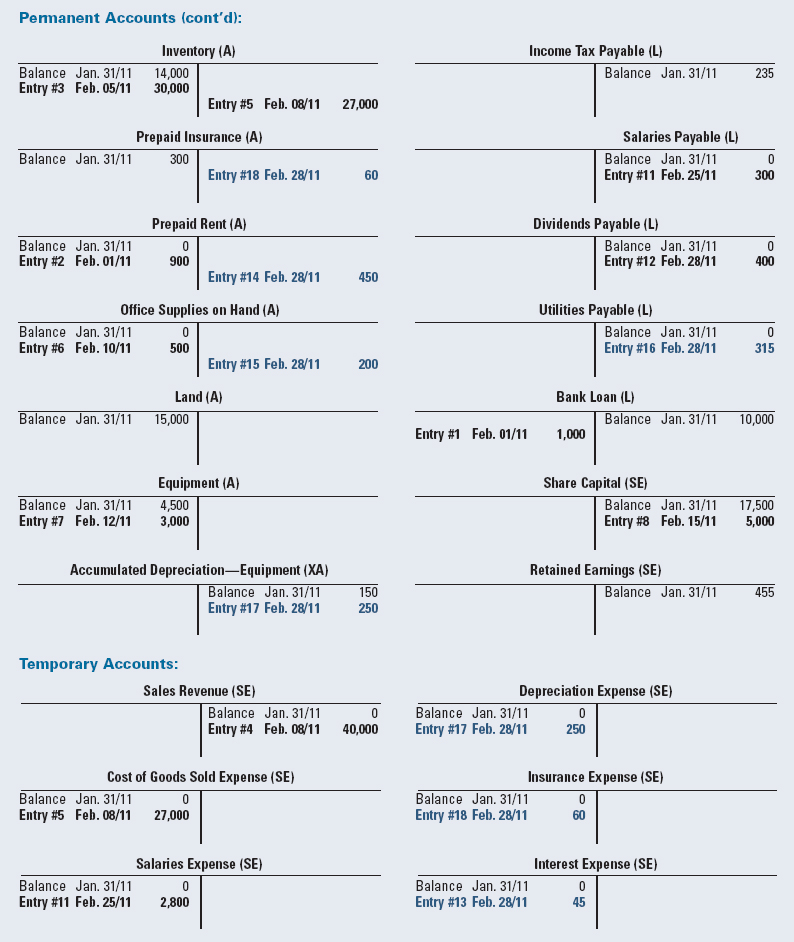

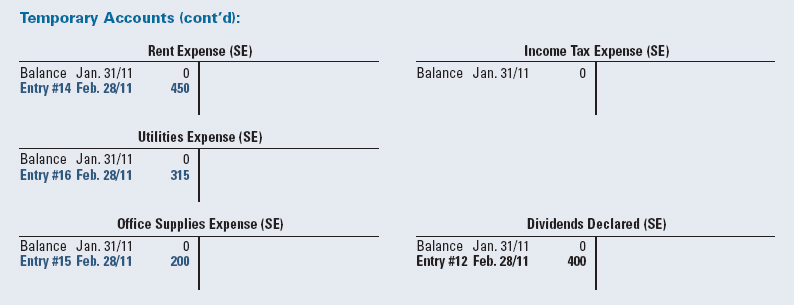

Although the journal provides an important chronological record of the effects of each transaction on the accounts, the information in the journal is not organized in a way that is very useful for most purposes. For example, if a manager wanted to know the balance in the cash account, the accountant would have to take the beginning balance of cash and add or subtract all the journal entries that affected cash. To prepare financial statements, the accountant would have to go through this process for all of the accounts, in order to determine their ending balances. If the company had hundreds of journal entries, this would be extremely time-consuming and inefficient. Therefore, to provide more efficient access to information about the cumulative effects of transactions on individual accounts, the next step in the accounting cycle transfers the data in the journal to the accounts in the ledger. This process is called posting.

The ledger is the collection of all the accounts used by a company. Posting is the process of transferring the information from the journal entries to the ledger accounts.

Each account in the ledger represents a separate, specific T account, and includes the name of the account (and its number, if applicable), its beginning balance, and then a listing of all the postings that affected the account during the period. Each posting includes the date of the transaction and the transaction number, as well as the amount debited or credited. The date and transaction number enable users to cross-reference the amounts in the ledger with the related entries in the journal, and thus determine the source of each of the amounts that has been posted to the accounts.

EXHIBIT 3-8 DEMO COMPANY'S JOURNAL SHOWING ITS TRANSACTION ENTRIES FOR THE MONTH OF FEBRUARY

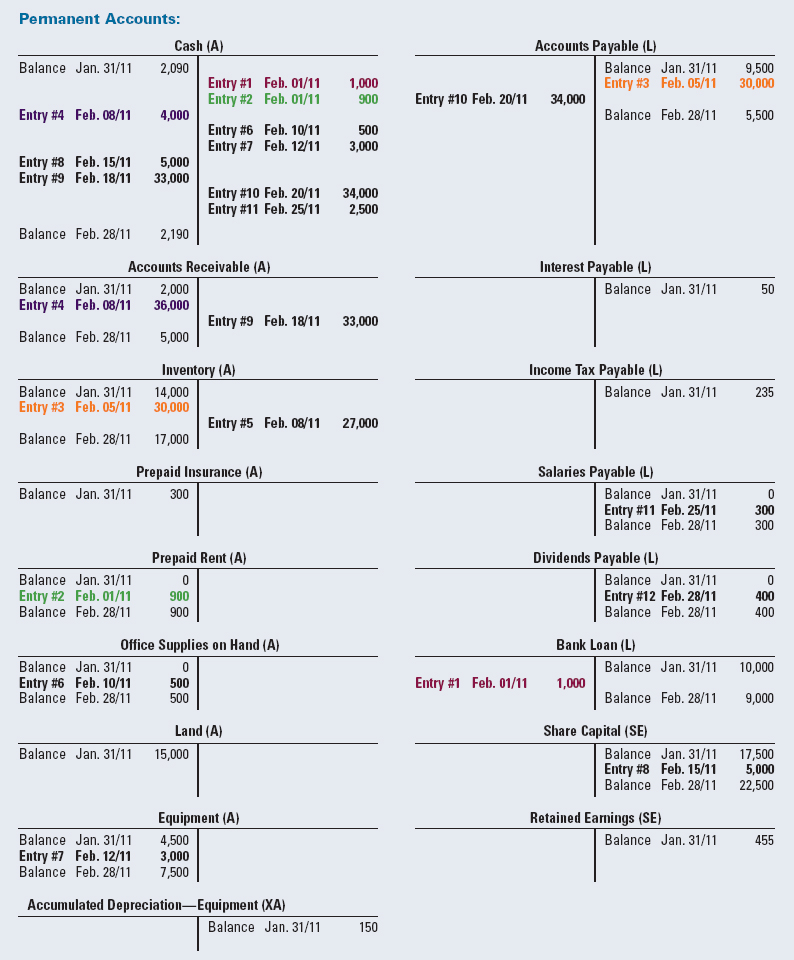

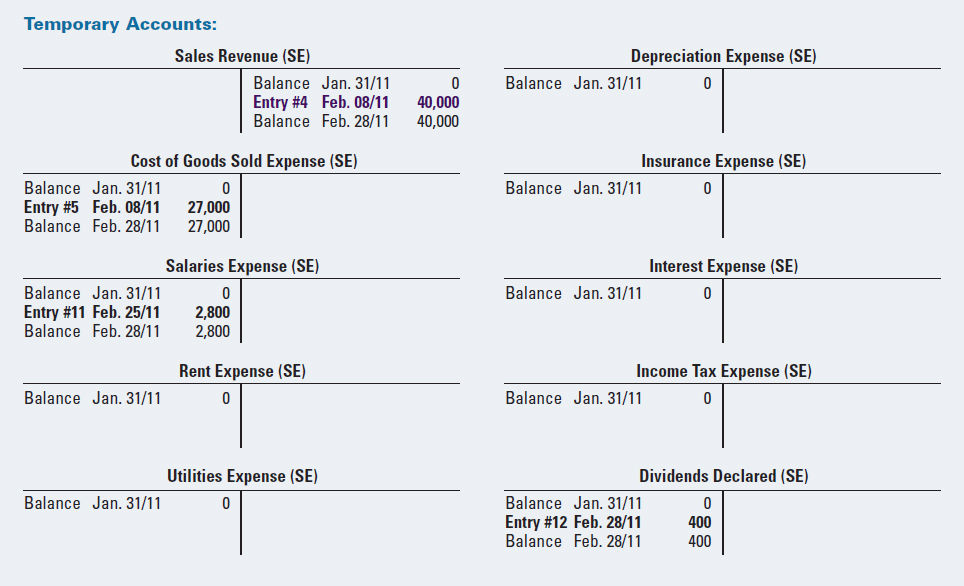

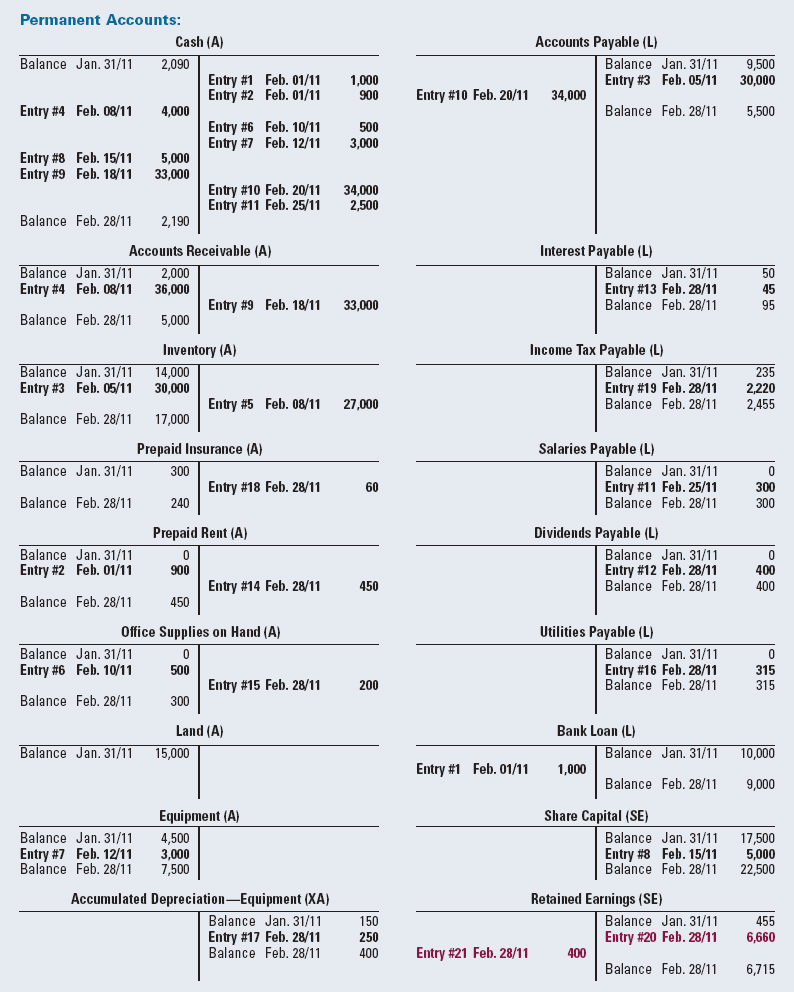

Exhibit 3-7 presented Demo Company's ledger accounts before the February transactions were posted, while Exhibit 3-9 shows its ledger after the February transactions have been posted. Four new accounts have been added (Prepaid Rent, Office Supplies On Hand, Salaries Payable and Dividends Payable), because we needed them to record new types of transactions that occurred in February. These new accounts would also be added to the company's chart of accounts, which was presented in Exhibit 3-6.

To make it easier to see how the posting process transfers the information from the journal (Exhibit 3-8) to the accounts in the ledger (Exhibit 3-9), the first four entries in the journal have been colour-coded to match the related postings in the ledger. For example, in Exhibit 3-8 the journal entry on February 1 for Transaction 1 indicates that the Bank Loan account is to be debited $1,000 and the Cash account is to be credited $1,000. In Exhibit 3-9, you will see that $1,000 has been posted as a debit to the Bank Loan account, by entering it on the left side of that T account; $1,000 has also been posted as a credit to the Cash account, by entering it on the right side of that T account; and both have been cross-referenced to the journal by the notation “Trans. #1, Feb. 01/11.”

Similarly, in Exhibit 3-8 the journal entry on February 1 for Transaction 2 indicates that the Prepaid Rent account is to be debited and the Cash account is to be credited, in the amount of $900. In Exhibit 3-9, you will see that $900 has been posted as a debit to the Prepaid Rent account (by entering it on the left side of that T account) and as a credit to the Cash account (by entering it on the right side of that T account), and both have been cross-referenced to the journal by the notation “Trans. #2, Feb. 01/11.”

You should follow this same process to see how the journal entries for Transactions 3 and 4, shown in Exhibit 3-8, have been transferred to the T accounts in the ledger in Exhibit 3-9. Once you have traced these amounts from their origins in the journal to their individual accounts in the ledger, you should have a good understanding of what “posting” means. It is a mechanical process, and all of the entries in the journal are transferred to the accounts in the ledger in the same way.

Posting to the ledger can be done monthly, weekly, daily, or at any frequency desired. The timing of the postings is determined to some extent by management's (or the shareholders') need for up-to-date information. If managers need to know the balance in a particular account, say Cash, on a daily basis, then the postings have to be done at least daily. If management needs to know the amount of cash available on an hourly basis, then the postings have to be done at least hourly.

Many computer systems account for transactions in “real time,” meaning that accounts are updated instantaneously, as each transaction occurs. Once a journal entry has been completed, such systems automatically post the information to the ledger accounts. Other computer systems collect journal entries in batches and post them all at one time (for example, at the end of each day). In general, since managers like to have information sooner rather than later, the number of real-time accounting systems continues to increase as the cost of computer technology continues to decrease.

At this point, it is important to note that a system consisting only of journal entries would make it difficult for managers to know the balances in the accounts. On the other hand, a system of only ledger accounts, without the original journal entries, would make it difficult to understand the sources of the amounts in the accounts. Accounting systems need both journal entries and ledger accounts in order to collect information in a way that makes it readily accessible and as useful as possible.

EXHIBIT 3-9 DEMO COMPANY'S LEDGER AFTER THE FEBRUARY TRANSACTIONS HAVE BEEN POSTED TO IT

Finally, it should be noted that, since each journal entry must have equal debits and credits, if the journal entries are posted properly, the ledger should always be in balance (i.e., the total of the debit amounts in the accounts should be equal to the total of the credit amounts).

LEARNING OBJECTIVE 7

Prepare a trial balance and use it to identify errors.

Preparing a Trial Balance

While most errors should be detected at the journal entry and posting phases of the accounting cycle, some errors may persist. As stated earlier, most computerized systems will not post a journal entry unless the debits equal the credits. These systems catch most errors at the input stage. In manual systems, however, errors may not be detected when journal entries are being made. Moreover, even if the debits equal the credits at the journal entry stage, it is possible for the amounts to be posted incorrectly to the accounts. A useful tool for detecting errors in the ledger is to produce a trial balance.

The trial balance is a listing of all the account balances in the ledger at a specific point in time. To use our warehouse example, we would look into each of the boxes and make a list of the final amount in each of them. A check can then be done to ensure that the total of all the balances on the debit side equals the total of all the balances on the credit side. If these amounts are not equal, a mistake has been made at some point during the process and it must be found and corrected before proceeding.

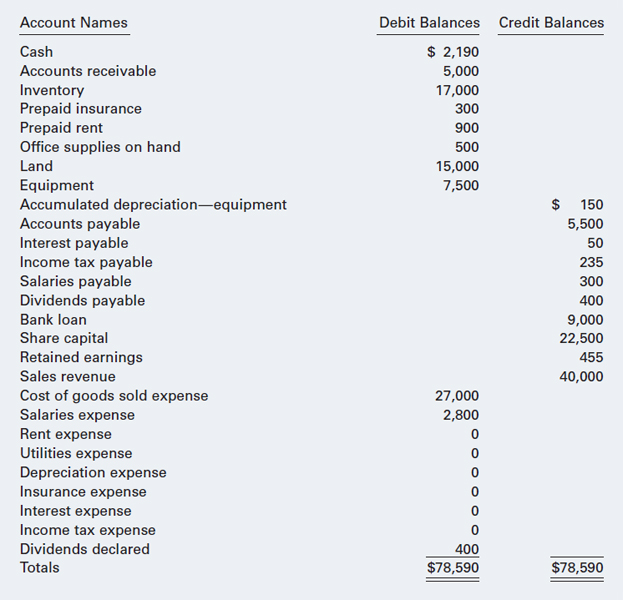

Notice in Exhibit 3-9 that, in addition to the February transactions having been posted, the ending balance in each account has been calculated (except for those accounts, such as Land, that were not affected by any transactions during the period). The account balances are found by simply adding the debit amounts and subtracting the credit amounts, or vice versa. For example, the balance in the Cash account can be found by adding the debits and subtracting the credits: 2,090 + 4,000 + 5,000 + 33,000 − 1,000 − 900 − 500 − 3,000 − 34,000 − 2,500 = 2,190. Note that, since Cash is an asset account, the balance is a debit. Similarly, the balance in the Accounts Payable account can be found by adding the credits and subtracting the debit: 9,500 + 30,000 − 34,000 = 5,500. In this case, since Accounts Payable is a liability account, the balance is a credit.

HELPFUL HINT

Do not confuse a trial balance with a balance sheet. A trial balance lists the balances in all the accounts, while a balance sheet (statement of financial position) includes only the asset, liability, and permanent shareholders' equity accounts.

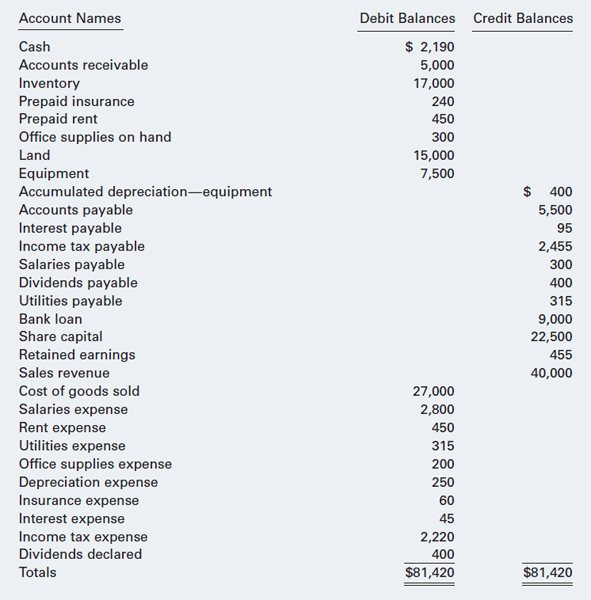

Exhibit 3-10 illustrates a trial balance, using the data presented in Exhibit 3-9.

Notice the order of the accounts in the ledger, and hence in the trial balance. The permanent accounts are presented first (in the same order as they will appear on the statement of financial position), followed by the temporary accounts (the revenues, expenses, and dividends). This makes it easier to prepare the financial statements. Also, note that although the accumulated depreciation account has a credit balance, it is not a liability; it is a contra-asset account, representing the portion of the equipment's cost that has been used up and written off, through depreciation, thus far.

EXHIBIT 3-10 DEMO COMPANY'S TRIAL BALANCE AS OF FEBRUARY 28, 2011 (before adjustments)

HELPFUL HINT

If you prepare a trial balance that does not balance, here are some tips for finding your error:

- First, calculate the difference between the total debits and the total credits, and look for this amount in either the question or your answer.

- Divide the difference from the first step by 2, and check to see whether a debit for this amount has been recorded as a credit, or vice versa.

- Divide the difference from the first step by 9. If it divides evenly—with no decimals—check for a transposition error: two digits that have been reversed (for example, 765 written as 756, or 432 written as 234).

The purpose of a trial balance is to assist in detecting errors that may have been made in the recording process. If the ledger does not balance (i.e., if the total of all the debit balances in the accounts does not equal the total of all the credit balances), this indicates that something is wrong. In such cases, there is no point in proceeding until the errors have been found and corrected. This makes the preparation of a trial balance a very useful step in the accounting cycle. However, it is important to realize that, because a trial balance only checks whether the total of the debit balances in the ledger accounts equals the total of the credit balances, it cannot detect all types of errors. For example:

- The trial balance will still balance if the correct amount was debited or credited, but to the wrong account (for example, if a purchase of office supplies was debited to the Inventory account, rather than to the Office Supplies account).

- If an incorrect amount was recorded (for example, if a $450 transaction was recorded as a $540 transaction, for both the debit and credit portions of the entry), the trial balance will still balance.

- The trial balance will also not detect the complete omission of an entire journal entry. If neither the debit nor the credit portions of a journal entry were posted, the totals on the trial balance will still be equal.

Despite these limitations, the preparation of a trial balance is very helpful in detecting many other types of common errors in the recording process, and is an important step in the accounting cycle.

LEARNING OBJECTIVE 8

Make adjusting entries to prepare an adjusted trial balance.

Recording Adjusting Entries

If an error is detected in the trial balance phase, it must be corrected. A journal entry to correct an error is one type of adjusting entry that is made at the end of the accounting period. A second, routine type of adjusting entry is made for accounting events that were not recognized and recorded during the period. These reflect the objective of the adjusting entry phase of the accounting cycle: to ensure that all the appropriate revenues and expenses have been recorded and reported for the period. Common examples of adjustments that must be made at the end of an accounting period are recording the depreciation of capital assets, recognizing the portions of prepaid expenses that have expired, recording interest and other accrued liabilities, recognizing the cost of supplies that were used up during the period, and recording income taxes. We introduced some basic adjustments in Chapter 2; in this chapter, we will continue our discussion of adjustments and demonstrate how the appropriate journal entries are made.

Notice that the types of items that need to be adjusted generally relate to the passage of time: the depreciation of capital assets, the expiration of prepaid expenses, the accrual of interest, and the consumption of supplies all occur on a daily basis. However, because recording them every day would be impractical, they are typically updated only at the end of the accounting period, through adjusting entries. In most situations there is no external transaction at the end of a period to signal that an adjustment needs to be made—only the passage of time. As a result, the ending balances in the accounts have to be carefully reviewed to determine those that need to be adjusted.

Ethics in Accounting

Many adjusting entries require management to make estimates and exercise judgement, providing opportunities for managers to manipulate earnings and statement of financial position values.

For example, suppose that you, as an accountant for a company, are asked to postpone the write-off of some old equipment. The equipment has not been used for some time, and it is clear to you that it will never be used again. You therefore think that it should be written off immediately. However, the write-off would need to be recognized as a loss (like an expense on the statement of earnings) and, since the amount involved is large, it would have a significant negative impact on the company's income for the period. Management has asked you to postpone the write-off because the company has applied for a large loan from the bank, and the loss from the write-off would have a negative impact on the bank's assessment of the company. What should you do?

As you consider your response to this, or any, ethical question, it is sometimes helpful to think about who will be affected by your decision (including yourself), and how it will help or hurt them. Particularly, think of who the users or potential users of the financial statements are, and how they might be affected by your action (or inaction). This should help you structure a fuller understanding of the situation and make an ethical decision.

It is essential that financial statements not be presented in a way that could mislead, or potentially harm, a user—such as the bank, in this case.

Under the accrual basis of accounting, companies must apply the revenue recognition principles (introduced in Chapter 2 and discussed in detail in Chapter 4) to ensure that all the revenues earned in an accounting period are identified, recorded, and reported in that period. They must also apply the matching principle to ensure that all the expenses incurred to generate those revenues are identified, recorded, and reported in that period. Therefore, in order to properly measure a company's net income and financial position, end-of-period adjustments to the revenues and expenses, and to the related assets and liabilities, are an essential step in the accounting cycle.

As stated earlier, end-of-period adjustments are very important. They ensure that all events and transactions related to the period have been accounted for, and thus make the financial statements as accurate as possible. We will illustrate the adjusting process by working through Demo Company's adjustments as of February 28, 2011.

At the end of February, Demo's accountant reviews the accounts in the trial balance and notes that adjustments need to be made for interest, rent expense, office supplies, utilities, depreciation, insurance, and income tax. This is a fairly typical set of adjustments, so we will now analyze each of these items and prepare the appropriate adjusting journal entries.

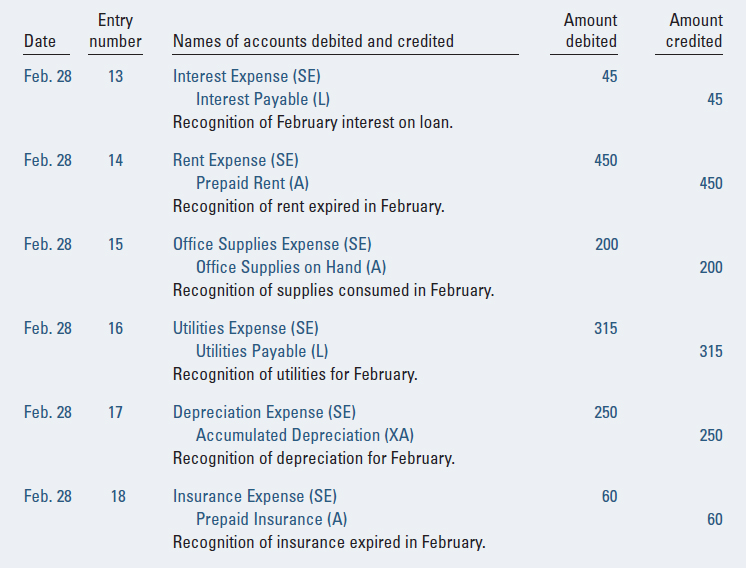

Entry 13: Interest Adjustment

Interest on the company's bank loan must be recognized for the month of February. (As noted in Chapter 2, the loan originated on January 1 and has an interest rate of 6% per year. However, the interest does not have to be paid until the end of March.)

ANALYSIS From the borrower's point of view, interest is an expense and therefore causes a decrease in shareholders' equity in the period when it is incurred. Since Demo is preparing financial statements each month, the interest for January was recognized at the end of January (in Chapter 2); the interest to be recognized now is only for the month of February. Since the company has not yet paid the interest (because it is not due to be paid until the end of March), it has to recognize a liability for its obligation to pay the interest later.

Recall that Demo Company paid off $1,000 of its bank loan on February 1 (see Transaction 1), which reduced the principal amount from $10,000 to $9,000. This can be confirmed by looking at the amount shown for the Bank Loan on the trial balance in Exhibit 3-10. To calculate the amount of interest expense for February, the principal amount of the loan is multiplied by the interest rate and the fraction of the year that has passed. In this case, the amount of interest incurred in February is $9,000 × 6% × 1/12 = $45. Shareholders' equity (retained earnings) will therefore be decreased by $45, as a result of the interest expense, and a liability (interest payable) will be increased by the same amount, to recognize the obligation to pay this interest when it is due at the end of March.

ANALYSIS OF INTEREST ADJUSTMENT

Shareholders' Equity decreased by $45 (recorded as Interest Expense)

Liabilities (Interest Payable) increased by $45

The rules of debit and credit specify that shareholders' equity is decreased by making debit entries. Accordingly, the Interest Expense account must be debited. Conversely, liabilities are increased by making credit entries, so the Interest Payable account must be credited. Thus, this adjustment is recorded in the journal as follows:

JOURNAL ENTRY FOR INTEREST ADJUSTMENT

Entry 14: Rent Adjustment

Rent expense must be recognized for the month of February.

ANALYSIS From the tenant's point of view, rent is an expense and therefore causes shareholders' equity to decrease in the period when it is incurred. Since Demo Company is operating on a monthly accounting cycle, the rent expense to be recognized at this point is only for February.

Recall that Demo signed a lease agreement on February 1 and paid $900 to cover the first and last months' rent, which was recorded as an asset called Prepaid Rent (see Transaction 2). This can also be seen by looking at the amount shown for Prepaid Rent on the trial balance in Exhibit 3-10. One month's worth of this asset, $450, was used up during the first month of the lease, February, and therefore now has to be removed from the Prepaid Rent account and put into the Rent Expense account. Shareholders' equity (retained earnings) will therefore be decreased by $450, as a result of the rent expense, and the asset (prepaid rent) will be decreased by the same amount.

This transfer—out of an asset account and into an expense account—is necessary because, as of the end of February, this $450 cost no longer relates to the future and therefore should no longer appear on the statement of financial position; it was incurred to operate the business during the past month, and therefore belongs on this period's statement of earnings.

ANALYSIS OF RENT ADJUSTMENT

Shareholders' Equity decreased by $450 (recorded as Rent Expense)

Assets (Prepaid Rent) decreased by $450

The rules of debit and credit specify that shareholders' equity is decreased by making debit entries, so the Rent Expense account must be debited. Conversely, assets are decreased by making credit entries, so the Prepaid Rent account must be credited. Thus, this adjustment is recorded in the journal as follows:

JOURNAL ENTRY FOR RENT ADJUSTMENT

Entry 15: Office Supplies Adjustment

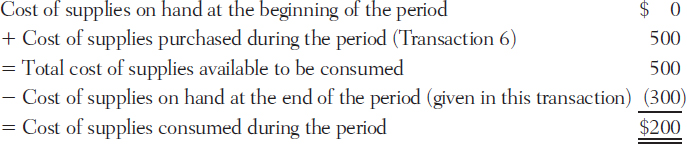

Demo Company checks its office supplies at the end of the month and determines that the cost of the items that are still on hand is $300.

ANALYSIS Recall that the company bought $500 of office supplies on February 10 and recorded them as an asset (Transaction 6). This can also be seen by looking at the amount shown for Office Supplies on Hand in the trial balance (Exhibit 3-10). However, a portion of these supplies was consumed during February and should now be recorded as an expense. Hence, an adjustment is required.

In cases such as this, accountants usually determine how much of the asset has been used up during the period indirectly, by checking how much is still on hand. The difference between the amount that was on hand previously and the amount that is on hand now represents the amount that was used up during the period. In this case, Demo originally had $500 of office supplies on hand but now has only $300 worth of supplies, which indicates that supplies costing $200 have been consumed.

The general formula to be used in such situations is as follows:

Shareholders' equity (retained earnings) will therefore be decreased by $200, as a result of the office supplies expense, and the asset (office supplies on hand) will be decreased by the same amount. As with the preceding adjustment, this transfer—out of an asset account and into an expense account—is necessary because, as of the end of February, this $200 of cost will not benefit the future and therefore should not appear on the statement of financial position; it was consumed in operating the business during the past month, and therefore belongs on this period's statement of earnings.

ANALYSIS OF OFFICE SUPPLIES ADJUSTMENT

Shareholders' Equity decreased by $200 (recorded as Office Supplies Expense)

Assets (Office Supplies on Hand) decreased by $200

Since shareholders' equity is decreased by making debit entries, the Office Supplies Expense account must be debited. Conversely, because assets are decreased by making credit entries, the Prepaid Rent account must be credited. Thus, this adjustment is recorded in the journal as follows:

JOURNAL ENTRY FOR OFFICE SUPPLIES ADJUSTMENT

Note that the $300 given in the original description of this adjustment does not appear in the journal entry. Rather, since that amount was a remaining balance, it was used to calculate the $200 recorded in the entry. Bear in mind that a balance is the net amount remaining in an account as a result of all the preceding transactions that affected the account. Therefore, if you need to make a journal entry but are only given the ending balance in an account, you have to use that information—together with your knowledge of the logical relationships affecting that account—to calculate the amount to be recorded in the journal entry, as we did here and in Transaction 9.

Entry 16: Utilities Adjustment

Demo's accountant noted that the company received a bill for $315 for utilities used in February. However, the company does not plan to pay the bill until March.

ANALYSIS According to the accrual basis of accounting, the amount of expense that should be recorded each period is the amount that is incurred that period, rather than simply the amount that is paid during the period. Therefore, utilities expense of $315 must be recorded for the month of February, even though it will not be paid until March.

Since expenses reduce net income and, ultimately, retained earnings, the utilities expense causes a decrease in shareholder's equity. At the same time, liabilities are increased by the amount owing.

ANALYSIS OF UTILITIES ADJUSTMENT

Shareholders' Equity decreased by $315 (recorded as Utilities Expense)

Liabilities (Utilities Payable) increased by $315

Since shareholders' equity is decreased by making debit entries, and expenses are temporary shareholders' equity accounts, the Utilities Expense account must be debited. Since liabilities are increased by making credit entries, the Utilities Payable account must be credited. Thus, this transaction is recorded in the journal as follows:

JOURNAL ENTRY FOR UTILITIES ADJUSTMENT

Entry 17: Depreciation Adjustment

Demo Company's accountant determined that the depreciation on the equipment for the month of February should be $250.

ANALYSIS As discussed in Chapter 2, because the value of the equipment is used up over time, some of its cost should be shown as an expense in each of the periods when it is used. The matching principle requires that we transfer some of the cost of the asset to an expense account each period, so that the cost of using the equipment will appear on the statement of earnings in the same time periods as the revenues generated from using the equipment. This process is called depreciation (or amortization).

In the preceding chapter, we illustrated how the depreciation for January could be calculated. The amount of depreciation for February will be different, because the company purchased additional equipment this month (Transaction 7). However, since depreciation calculations will be covered in detail in Chapter 8, at this point we will simply accept the amount determined by Demo's accountant, $250, as the correct amount for February.