chapter 2

ANALYZING TRANSACTIONS AND THEIR EFFECTS ON FINANCIAL STATEMENTS

TRANSACTION ANALYSIS AND THE BASIC ACCOUNTING EQUATION

Statement of Financial Position

Variations in Statement of Financial Position Presentation

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Describe the basic accounting equation and each of its components.

- Analyze simple transactions to determine their effects on the basic accounting equation and the financial statements.

- Describe the difference between accrual-basis accounting and cash-basis accounting.

- Explain how inventory is accounted for when it is purchased and when it is sold.

- Identify operating activities and describe their effects on the financial statements.

- Explain the basic concepts of revenue recognition and expense matching.

- Prepare a simple set of financial statements, reflecting a series of business transactions.

- Explain the basic classification of items on a statement of financial position.

- Calculate three ratios for assessing a company's profitability.

- Begin to analyze the information provided by a statement of cash flows.

A Recipe for Success—The Evolution of a Business

Ever since high school, Chris Emery and Larry Finnson had known they wanted to go into business together. Sure enough, one day Mr. Emery's grandmother came up with an irresistible recipe for a vanilla fudge treat, and Krave's Candy Company was born. In 1996, with $20,000 scraped together from family and friends, the two Winnipeg entrepreneurs set up some old kettle cookers in a tiny industrial space and started churning out 80-pound batches of the sweets, which they called Clodhoppers.

In its first year of operation, Krave's sold its product mostly through local retailers and craft fairs. Ten years later, in 2006, they sold the Clodhoppers trademark to Brookside Foods Ltd., a manufacturer of chocolate-covered fruit and nuts based in Abbotsford, B.C. Today, Chris and Larry's Clodhoppers are sold in stores across Canada, including Wal-Mart, Zellers, Safeway, and The Bay, as well as in Blockbuster video outlets across North America.

While their company enjoyed remarkable success, Mr. Emery and Mr. Finnson, neither of whom had any prior business experience, learned a lot along the way. “At the beginning, we just thought we'd fire up a manufacturing plant and start making millions of pounds of candy and be rich within two years,” says Mr. Finnson. “It didn't work out that way. It was step by step for everything from manufacturing to money.”

During Krave's start-up period, the pair ran into unanticipated expenses. “First, we needed a computer; then there was the development of the packaging and artwork; plus we had to hire people to help us make the candy,” Mr. Emery recalls. “Before we knew it, the money was pretty much spent.” Meanwhile, as their sales continued to climb, the two had to find more cash to finance their expansion, including much needed upgrades to their production equipment: the large mixers, cooling tunnels, and other devices used in the manufacturing process.

When Krave's purchased two form-and-fill machines to weigh and package the candy, the company ensured adequate cash flow by financing the purchase with a term loan from its bank, which it got on the basis of its strong financial statements. During that first decade, as the company continued to grow, Mr. Emery and Mr. Finnson kept their financing balanced among several sources, including a venture capitalist, a traditional bank, and the Business Development Bank of Canada.

Clodhoppers' financial information is now included in the more complicated accounting structure of Brookside Foods, which is a large corporation. Information on production planning, warehouse management, product tracing, shipment scheduling, budgeting, and sales commissions for the Clodhoppers product line is added to similar information for other Brookside products to provide an overall picture of the company's operations. Still, whether running a large company like Brookside or the two-person start-up that Krave's once was, “The most important thing is to know your numbers,” Mr. Finnson says, “and how your business works from A to Z.”

Chris Emery and Larry Finnson started Krave's Candy as a small company and grew the business through hard work and effective marketing. They started with a product that they thought customers would want, and have proven that they were right. Now that their company has been taken over by Brookside Foods, several variations of their original Clodhoppers product are sold throughout North America.

It is well known that many new businesses do not survive, so what did Mr. Emery and Mr. Finnson do that made Krave's such a success? First, they had a product that people liked and would buy. Second, they worked hard at producing and distributing it. They had to ensure that the quality of the product remained consistent as they moved to producing it in larger batches. They also had to get the product to consumers. They chose to go to craft fairs first, and to convince local retailers to carry their product. As the name “Clodhoppers” became known, they were able to convince multi-outlet retailers such as The Bay, Zellers, and Shoppers Drug Mart to carry their product. This was the start of their real growth.

However, along with growth comes a need for additional funding. It is financing that often causes young companies their greatest problems, and Krave's was no exception. Within a very short time, the founders had exhausted their original investment of $20,000. Fortunately, however, by that time they were able to convince a bank that they were an acceptable credit risk. As the business evolved, they used multiple sources of funds (including a venture capitalist, as discussed in the Accounting in the News item on the following page). Investors were convinced that they had a good product, that the company was well managed, and that there was growth potential.

Behind all of its success and through all of its decisions, Krave's had to use its accounting information to manage the business. As young companies grow, the owners sometimes lose track of the numbers, especially if the growth is rapid. However, Mr. Emery and Mr. Finnson did not make that mistake. They knew that they had to keep track of all aspects of their business, and that the accounting numbers and financial statements were the tools that would enable them to do this. Therefore, as the company expanded its manufacturing and marketing operations, it also increased its accounting staff. In addition, it used computer technology to analyze its financial data efficiently and effectively.

The way Mr. Emery and Mr. Finnson started their business is typical of how many small businesses begin, with their funding obtained from personal savings, families, and friends. Financial institutions are often reluctant to take chances on new companies until they see some indicators of success, so alternative sources of financing are often required. One such source is called “venture capital,” which refers to financing provided to relatively new, potentially high-risk companies to enable them to get established.

accounting in the news

Canadian Venture Capital Financing

In the aftermath of the 2008 crisis in financial markets and the onset of a global recession, deal activity in the Canadian venture capital (VC) market in 2009 reached its lowest level since the mid-1990s. A total of $1.0 billion was invested across the country, a 27% decrease from the $1.4 billion invested in 2008, according to a report by Canada's Venture Capital & Private Equity Association (CVCA) and Thomson Reuters.

The number of VC-backed entrepreneurial firms in Canada also dropped in 2009, though not as much as the dollars invested. A total of 331 companies were financed, 15% fewer than the 388 companies financed in 2008. Amounts invested per company averaged $3.1 million in 2009, compared with $3.5 million in 2008 and $5.1 million in 2007.

The overall decline in domestic VC activity was partly offset by an increase in Quebec. A total of $431 million was invested in Quebec, up 10% from the $392 million invested in 2008, giving it a leading 43% share of the Canadian total last year. In contrast, $288 million was invested in Ontario in 2009, 50% below the $575 million invested in 2008. As a result, Ontario accounted for only 28% of the Canadian total, its lowest market share since the early 1990s.

CVCA news release, February 17, 2010, http://www.cvca.ca/files/News/CVCA_Q4_2009_VC_Press_Release_Final.pdf

USER RELEVANCE

If accounting information is to be useful, it must be (among other things) understandable and relevant. In order for users like Mr. Emery and Mr. Finnson to understand the information that is provided on financial statements, they must have at least some basic knowledge of the accounting system: what items are identified, measured, and recorded; how those items are recorded; and how financial statements are generated from the recorded data. Without that knowledge, they will have difficulty understanding the importance and relevance of accounting reports, and may not be able to use them effectively to make the best decisions.

The accounting system measures, records, and compiles information on the effects that economic events have on a company. To interpret the information in financial statements, you need to understand how accounting information is obtained and the guidelines for how it is presented in the financial statements. Only then can you use accounting information sensibly to make decisions. Chapter 1 provided an overview of the types of information that are presented in financial statements. This chapter and the next explain how accountants collect and classify that information.

LEARNING OBJECTIVE 1

Understand the basic accounting equation and each of its components.

THE BASIC ACCOUNTING EQUATION

In this chapter, we will demonstrate how a typical set of transactions affects a company's accounts, and how the three major financial statements are prepared using the transaction information. We will start with the basic accounting equation discussed in Chapter 1, which is the basis of all accounting systems.

A company's assets, liabilities, and shareholders' equity are reported on its statement of financial position, which is commonly referred to as the balance sheet. For this reason, the basic accounting equation is often called the balance sheet equation.

As transactions are recorded in the accounting system, the two sides of this equation must always remain equal. The statement of financial position provides readers with information about this equality at the beginning and end of the current accounting period—usually by showing the beginning amounts (from the previous period) in the outside column, and the ending amounts (from the current period) in the inside column. A statement with the amounts for two or more periods is called a comparative statement. Refer to H&M's balance sheet (statement of financial position) in Exhibit 1-4 for an example of this.

Users of financial information typically want to know more than just the statement of financial position amounts. They usually want to know how and why the company's financial position changed from the beginning of the period to the end. A statement of earnings and a statement of cash flows are both useful for this. In the remainder of this chapter, a set of accounts illustrating the basic accounting equation will be used to record typical transactions for a small company, and a statement of earnings and a statement of cash flows will be constructed from this information.

Companies are generally required to prepare financial statements at least once a year. However, because the financial statements provide information that is useful to management, owners, and other users, most companies prepare them more often (for example, semi-annually, quarterly, monthly, weekly, or even daily). The period of time that the financial statements cover is referred to as the accounting period. In the example we will use, the company prepares financial statements at the end of each month, so the accounting period is one month.

In Chapter 1, we explained that one of the components of shareholders' equity, share capital, increases when the owners invest money in the company and are issued shares. We also showed you that the other main component of shareholders' equity, retained earnings, increases when the company generates earnings or net income (which consists of revenues minus expenses), and decreases when the company declares dividends (distributions of earnings to the owners). In short, revenues increase retained earnings; expenses and dividends decrease retained earnings.

To help you understand the links between the financial statements and how various items are affected by transactions, each of the amounts in the retained earnings column will be labelled R for revenues, E for expenses, or D for dividends. Similarly, to help us prepare the statement of cash flows, we will label each of the amounts in the cash column as O for operating activities, F for financing activities, or I for investing activities, to indicate in which section of the statement they will be presented.

LEARNING OBJECTIVE 2

Analyze simple transactions and describe their effects on the basic accounting equation and the financial statements.

TRANSACTION ANALYSIS AND THE BASIC ACCOUNTING EQUATION

The basic accounting equation can now be used to illustrate the fundamentals of the accounting system and the preparation of financial statements. We will use typical transactions for a retail sales company to demonstrate the analysis of transactions and how they affect the financial statements.

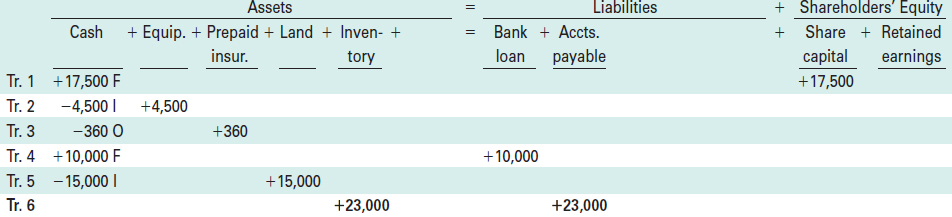

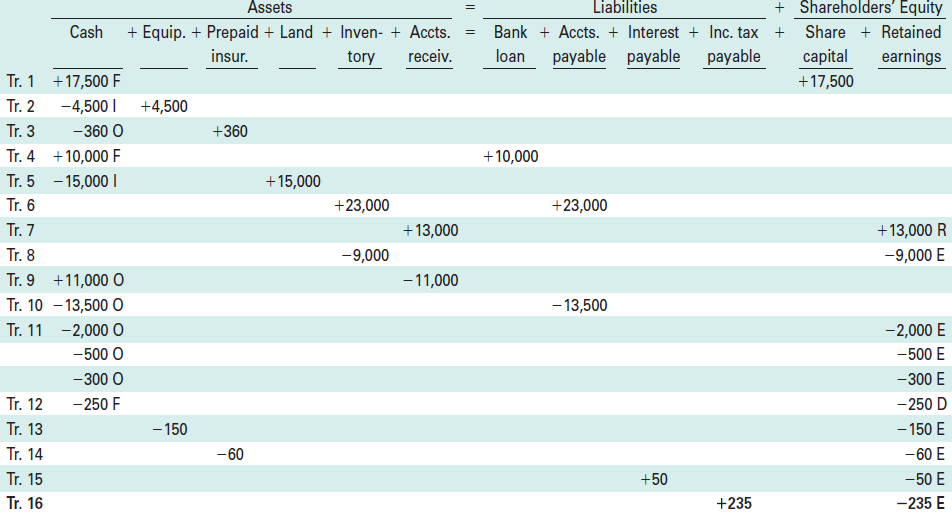

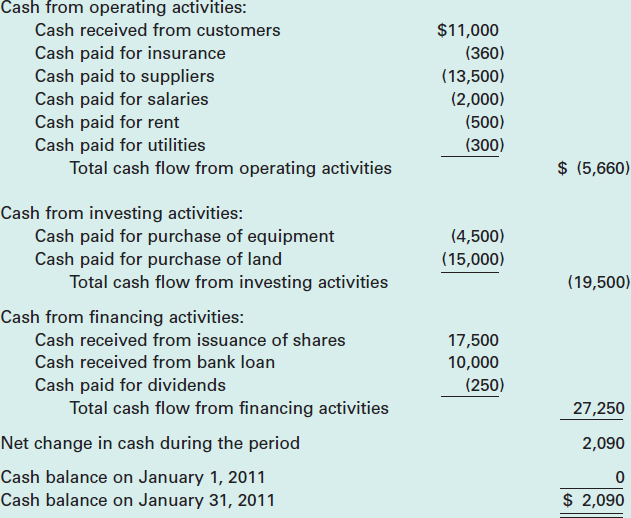

Assume that a business called Demo Company Limited is formed as a corporation on January 1, 2011. During the month of January it engages in a number of basic transactions, as described in the sections that follow. We will discuss each of the transactions to analyze its effects on the company's accounts and financial statements.

Sample Transactions

At the beginning of January:

- The owners invested $17,500 cash and Demo Company issued shares to them.

- The company used $4,500 of the cash received from the investors to buy equipment.

- Demo paid $360 cash for an insurance policy.

- To raise additional financing, the company borrowed $10,000 from its bank.

During the rest of January:

- Demo purchased some land for $15,000.

- The company bought $23,000 of inventory from suppliers, on account (i.e., Demo will pay for the goods at a later date).

- The company sold some goods to customers for $13,000, on account (i.e., Demo will receive payment for the goods at a later date).

- The cost of the goods that were sold and removed from the company's inventory in Transaction 7 was $9,000.

- Demo received $11,000 from its customers as payments on their accounts (which originated in Transaction 7.)

- The company made payments of $13,500 to its suppliers on account (which originated in Transaction 6.)

- Demo paid the following costs for the month of January: $2,000 for salaries; $500 for rent; $300 for utilities.

- Dividends in the amount of $250 were declared and paid.

At the end of January, Demo's accountant noted that the following adjustments were required:

- Depreciation expense must be recorded for the equipment. The accountant determined that the equipment should be depreciated by $150 for the month.

- Insurance expense must be recognized for January. The insurance policy (which was purchased in Transaction 3) covers the six-month period from January 1 to June 30, 2011.

- Interest expense must be recognized for the month. The interest rate charged on the bank loan (which originated in Transaction 4) is 6% per year. Although the loan itself does not have to be repaid for five years, the interest on it has to be paid quarterly.

- Income tax expense must be recognized for the month, even though the company does not have to pay the tax until later. Demo's income tax rate is 25%.

Transaction Analysis

For each event or transaction that affects an organization, accountants must analyze its economic substance to decide what accounts are affected and by how much. We call this transaction analysis. It is at this stage of the accounting process that accounting knowledge is most needed. In addition to determining the economic substance of each transaction, accountants must know the accounting principles and guidelines that apply to the various situations that arise.

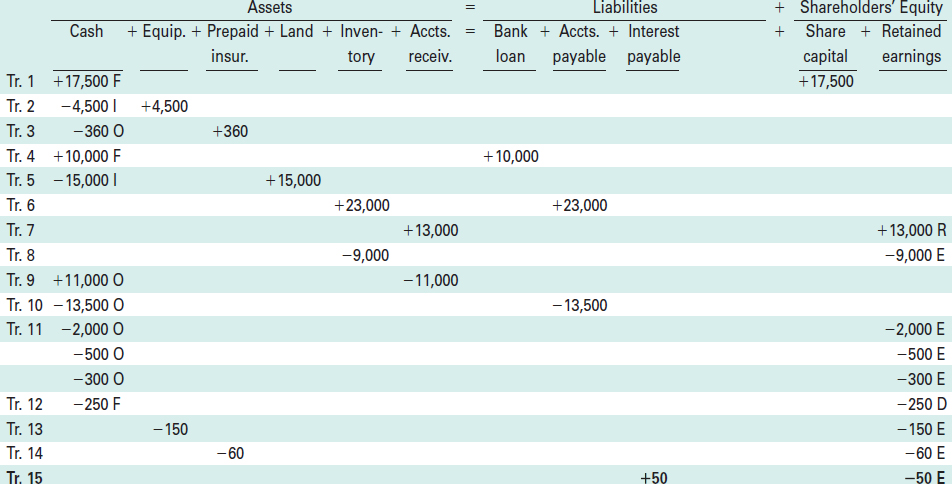

In the following subsections, we will analyze the economic substance of each of the transactions listed above, and discuss the related accounting principles underlying them. In addition, for each transaction we will show the accounts involved and the effects on the basic accounting equation, by entering the amounts in a table with columns for each of the asset, liability, and shareholders' equity accounts. Since the specific assets and liabilities that Demo Company will need are not known in advance, we will start with a basic table and add columns to it as we proceed through the analysis. Whenever we encounter a new account, we will add a new column to the table.

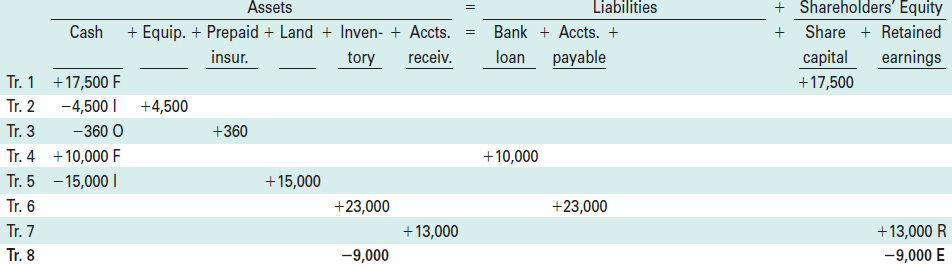

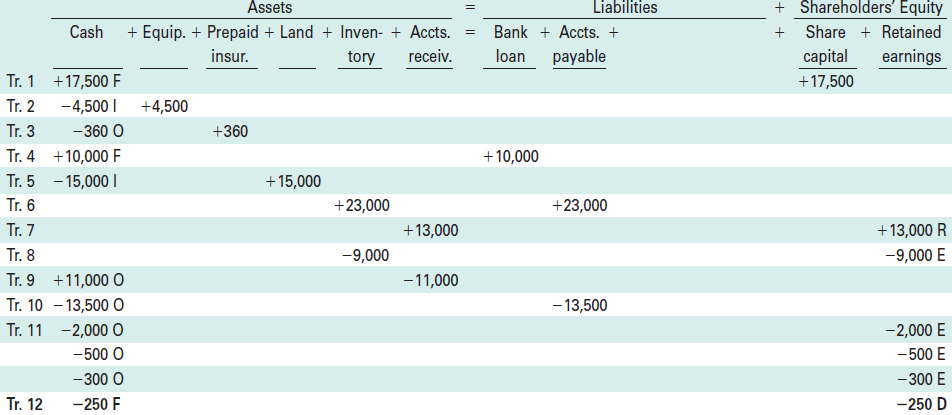

Transaction 1: Issuance of Shares for Cash

Demo Company issued shares in exchange for $17,500 received in cash from investors.

ANALYSIS The company's shareholders invested $17,500 in the company, in exchange for ownership rights represented by share certificates. The money the company received is recorded as an asset (cash), and the ownership rights are recorded as shareholders' equity (share capital).

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 1

Assets (specifically. Cash) increased by $17,500

Shareholders' Equity (specifically, Share Capital) increased by $17,500

EFFECTS ON THE BASIC ACCOUNTING EQUATION

Note that these entries keep the two sides of the basic accounting equation equal (in balance).

CASHFLOW EFFECT Since this transaction provides financing for the company, the cash inflow of $17,500 is classified as a financing activity and therefore has been designated with an F.

EARNINGS EFFECT Since this transaction does not involve revenues or expenses, there is no effect on the company's earnings.

RELATED CONCEPTS—The nature of revenue It is important to note that, although the issuance of shares results in an inflow of resources into the business, revenue cannot be recorded when a company sells shares to investors. Revenue has to be earned from operations of the business, and therefore only arises when the company sells goods or services to customers. The issuance of shares—even if the transaction is described as a “sale of shares”—does not involve customers, and consequently does not constitute sales revenue and will not be reported on the statement of earnings.

Transaction 2: Purchase of Equipment for Cash

Demo Company used $4,500 of its cash to buy equipment.

ANALYSIS Because the purchase required an outflow of cash, this asset decreased. At the same time, another asset—equipment—increased. The equipment is an asset, rather than an expense, because it will be used in the operations of the business and provide future benefits.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 2

Assets (specifically. Cash) decreased by $4,500

Assets (specifically, Equipment) increased by $4,500

EFFECTS ON THE BASIC ACCOUNTING EQUATION

Again, notice that the equilibrium of the basic accounting equation has been maintained.

The equipment purchased is regarded as a long-term asset because the company will use it over several future accounting periods. The value of this asset will be used up over those future periods, and the amount that is consumed each period will be shown as depreciation expense. The expensing of part of the cost of the equipment is shown later, as one of the adjustments that is made at the end of the accounting period.

CASHFLOW EFFECT Transactions involving long-term assets are classified as investing activities. Accordingly, the cash outflow of $4,500 has been designated with an I.

EARNINGS EFFECT Since no revenue or expense is involved in this transaction, there is no effect on the company's earnings. The equipment is an asset; the expense (depreciation) related to it will be recorded later, as the asset is used.

RELATED CONCEPTS—Accrual-basis versus cash-basis accounting The treatment of this transaction is based on an assumption of accrual-basis accounting. Under accrual accounting, costs (such as the cost of the equipment) are only classified as expenses if and when the item is consumed; until that time, the cost is recorded as an asset. In this transaction, therefore, the purchase of the equipment is not recorded as an expense. The equipment is recorded as an asset, because it will be used in the future. One asset (cash) has simply been exchanged for another asset (equipment) and there is no effect on the company's income, or change in its shareholders' equity.

LEARNING OBJECTIVE 3

Describe the difference between accrual-basis accounting and cash-basis accounting.

Accrual-basis accounting is very different from cash-basis accounting, which classifies costs as expenses whenever cash is spent. In a cash-basis system, the purchase of equipment would be recorded as an expense and reported on the statement of earnings. However, as will be discussed in detail in Chapter 4, cash-basis accounting violates generally accepted accounting principles (GAAP). The accrual basis is consistent with GAAP, is used by most businesses, and will be used throughout this book.

Transaction 3: Purchase of Insurance

Demo Company paid $360 in cash for an insurance policy.

ANALYSIS This transaction is an example of a prepaid expense. The cost of insurance coverage is paid in advance of the coverage period. Therefore, at the date of the payment the cost of the policy should be shown as an asset, since it has not been used up yet. Only as time passes will the asset (the insurance coverage) be consumed.

HELPFUL HINT

Note that this is an example of the concept that a cost can be classified as either an asset or an expense, depending on whether or not it has expired (i.e., been consumed). Unexpired costs are assets, while expired costs are expenses.

Because the purchase required an outflow of cash, this asset decreased. However, another asset—prepaid insurance—increased.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 3

Assets (specifically, Prepaid Insurance) increased by $360

Assets (specifically, Cash) decreased by $360

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT This transaction decreases cash by the $360 payment, which represents an operating cash flow and has therefore been designated with an O.

EARNINGS EFFECT Since this transaction does not involve revenue or expenses, there is no effect on the company's earnings. The insurance is not an expense until it is used up.

Transaction 4: Loan from Bank

Demo Company borrowed $10,000 from the bank.

ANALYSIS In addition to issuing shares to investors, a company can also raise money by taking out a loan. In this case, Demo borrowed $10,000 from the bank. The effect of this transaction is to increase cash and create an obligation (liability) that shows the amount owed to the bank.

The amount that was borrowed is called the principal of the loan. The principal does not include interest. As time passes, interest will be added to the amount owed to the bank. For example, if the interest rate on this loan is 6% per year (interest rates are generally stated on an annual basis), the interest added during the first year of the loan will be 6% of the $10,000 principal, $600. Using accounting terminology, interest accrues on the loan as time passes. At the point of acquiring the loan, however, only the principal is recorded; since no time has passed since the loan was taken out, no interest has accrued.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 4

Assets (specifically, Cash) increased by $10,000

Liabilities (specifically, Bank Loan) increased by $10,000

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT Since taking out a loan from the bank is a financing activity, the resulting cash inflow is designated with an F.

EARNINGS EFFECT Since no revenue or expense is involved in this transaction, there is no effect on the company's earnings.

RELATED CONCEPTS—The nature of revenue As with the issuance of shares (discussed in Transaction 1), taking out a loan creates an inflow of resources into the business; however, no revenue is recorded when a company borrows money. Revenue has to be earned from the operations of the business. Getting financing from creditors does not involve selling goods or services to customers, and consequently does not involve revenue. (In fact, as we will see in Transaction 15, the opposite occurs: when interest is charged on the debt, interest expense must be recorded.)

Transaction 5: Purchase of Land for Cash

Demo Company purchased land for $15,000.

ANALYSIS The purchase of land for cash means that cash decreases by the amount of the purchase price and another asset, land, increases by the same amount.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

Assets (specifically, Cash) decreased by $15,000

Assets (specifically, Land) increased by $15,000

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT Since purchasing a long-term capital asset such as land is classified as an investing activity, the resulting cash outflow is designated with an I.

EARNINGS EFFECT Since this transaction does not involve revenues or expenses, there is no effect on the company's earnings.

RELATED CONCEPTS Land is an asset because it has probable future value and the company holds title to it. The probable future value can be viewed as either its future sale price or the value to be derived from its future use. As with other assets, land should be recorded at its acquisition cost. Unlike other long-term capital assets, however, land is not depreciated. This is because it is not consumed the way other capital assets are. Capital assets such as buildings and equipment can be used for only a limited period of time before they wear out from use, but land can typically be used for an unlimited period.

Transaction 6: Purchase of Inventory on Account

Demo Company purchased $23,000 of inventory, on account.

ANALYSIS “On account” means that Demo has been extended credit by its suppliers and will be required to pay for the inventory at a later date.

The substance of this transaction is that the company has received an asset (inventory) from a supplier and, in exchange, has given the supplier a promise to pay for the inventory at a later date. The promise to pay represents an obligation of the company and is therefore recorded as a liability. These types of liabilities are usually referred to as accounts payable.

The term “account payable” means an account that Demo will have to pay in the future. It must be recorded as a liability on the day the inventory is purchased, even though the payment is not due until later.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 6

Assets (specifically, Inventory) increased by $23,000

Liabilities (specifically, Accounts Payable) increased by $23,000

CASHFLOW EFFECT This transaction has no immediate impact on cash, since no cash has changed hands yet. Cash will be affected later, when the company pays the amount owed to the supplier.

EARNINGS EFFECT Since no revenue or expense is involved in this transaction, there is no effect on the company's earnings. Net earnings (and therefore retained earnings) will be affected only when the inventory is sold.

RELATED CONCEPTS As with Transactions 2, 3, and 5, this transaction involves the purchase of an asset. The inventory will be held until it is sold, and should be shown as an asset on the statement of financial position until that time. The cost of goods purchased for inventory is, therefore, classified as an asset until the company sells the inventory. There is no immediate impact on the statement of earnings from this transaction. It will only affect the statement of earnings later, when the inventory is sold.

As with most other assets, the valuation principle for inventory is that it should be recorded at its acquisition cost (i.e., the price paid to obtain it). Accordingly, the inventory is recorded at the amount that the company has to pay for it (its cost), not the amount it will be sold for (its resale value).

Accounts payable are generally settled in a short time period (typically 30 days), and there is generally no interest charged on accounts payable, even though they are equivalent to loans from the supplier.

Occasionally, inventory or other assets are purchased on longer-term credit and a formal loan document called a note payable is prepared, as evidence of the liability. In the case of a note payable, interest is usually charged. The interest would be recorded as an expense and as either an outflow of cash, if it is paid, or as an additional liability (interest payable) if it is going to be paid later. Accounting for interest is explained further in Transaction 15.

LEARNING OBJECTIVE 4

Explain how inventory is accounted for when it is purchased and when it is sold.

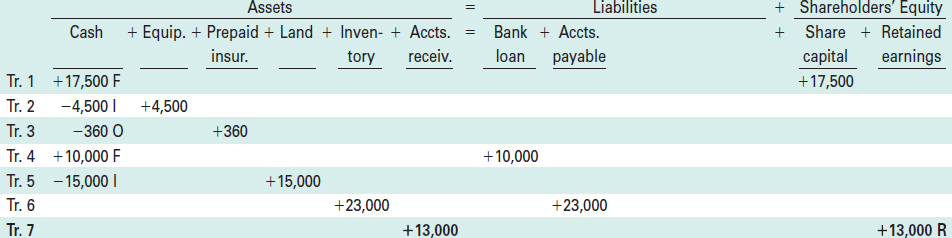

Transaction 7: Sales on Account

Demo Company sold some of its inventory to customers, on account, for $13,000.

ANALYSIS The substance of a sale transaction is that a company exchanges an asset that it has for an asset that a customer has. The sale may involve goods (items of inventory), if the company is a retailer, wholesaler, or manufacturer; or it may involve services, if the company is a service provider. In this case, Demo sells goods and the asset it provides is inventory. The asset it receives in exchange from its customers is generally cash, but other possibilities exist. For example, companies often agree to make sales based on customers' promises to pay later. These are called sales on account, or credit sales, and they result in the company getting the right to receive payment, usually called accounts receivable, in exchange for its goods. An account receivable is an amount that the seller is entitled to receive in the future, when the payment is due from the customer. It is recorded as an account receivable on the day the sale occurs, even though the amount is not due to be received until later.

Because this is an exchange, there are two parts of the transaction to consider: the inflow of the asset that is received, and the outflow of the asset that is given up. The inflow results in an increase in an asset (accounts receivable) and is also recorded as a revenue, which causes an increase in the shareholders' equity (retained earnings). The outflow results in a decrease in an asset (inventory) and is also recorded as an expense, which causes a decrease in the shareholders' equity (retained earnings). If the inflow or revenue is more than the outflow or expense, the company has generated income or a profit from the transaction. If the inflow (revenue) is less than the outflow (expense), the company has experienced a loss on the exchange.

LEARNING OBJECTIVE 5

Identify operating activities and describe their effects on the financial statements.

The increases and decreases in shareholders' equity from sales transactions such as this are typically called sales revenue and cost of goods sold (a type of expense), respectively.

Because the analysis which follows focuses on the basic accounting equation, the effects of both the sales revenue and the cost of goods sold (expense) will be shown as affecting the retained earnings portion of shareholders' equity. Remember from our earlier discussion that net income (revenues minus expenses) increases retained earnings. Therefore, it should be logical that revenues increase retained earnings and expenses decrease retained earnings. Showing revenues and expenses as increases or decreases in retained earnings is a temporary shortcut that we use in this chapter, to introduce you to the analysis of transactions. In future chapters, revenues and expenses will be recorded in their own accounts.

The remaining question in the analysis is how to value the inflow and the outflow. The inflow (revenue) should be recorded using the selling price of the goods being sold, while the outflow (expense) should be recorded using Demo's cost of the goods sold. Based on the information in Transaction 7, the selling price of the goods sold was $13,000. Therefore, retained earnings (sales revenue) and assets (accounts receivable) will both be increased by $13,000.

Transaction 7 gives no information about the cost of the goods that were sold; this is covered in Transaction 8. Although it may seem odd to analyze and record these two simultaneous events separately, it is necessary because they involve two different values: the retail price at which Demo sells the goods to its customers, and the cost price at which Demo bought the goods from its suppliers. For the same reason, when a clerk in a store rings up a sale, a record is made of the sales revenue and the increase in cash (or accounts receivable, in the case of a sale on account), but the salesperson usually does not know the cost of the item that is being sold. The cost is determined and recorded separately, as it will be for Demo in Transaction 8.

The analysis of Transaction 7 and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 7

Assets (specifically, Accounts Receivable) increased by $13,000

Shareholders' Equity (specifically, Retained Earnings) increased by $13,000

Notice that the basic accounting equation is still in balance after these entries are made.

CASHFLOW EFFECT This transaction has no immediate effect on cash. Because this sale is on account, the effect on cash will not occur until Demo collects the account receivable.

EARNINGS EFFECT Since sales are revenues that will be reported on the statement of earnings, the amount in the retained earnings column has been designated with an R.

RELATED CONCEPTS—Revenue recognition The timing of the recognition of revenues and expenses is an important decision that management must make in recording transactions and preparing financial statements. There is an underlying conflict between reporting income information in a timely manner and being assured that the information is reliable.

Consider three possible points in time for when a sale could be recorded:

- At one extreme, it might be argued that a company should record a sale as soon as a customer signs a contract for the future delivery of inventory, even though the goods have not yet been delivered and the customer has not yet paid for them.

- At the other extreme, it might be argued that the sale should not be recorded until the entire process has been completed (i.e., when the company has made the delivery and the customer has paid for the goods).

- As an intermediate position, it might be argued that the sale should be recorded when the company delivers the goods, even though the customer has not yet paid for them.

- In the first case, the company would be assuming that it will eventually deliver the goods to the customer and collect the cash from the sale. However, these are both uncertain events that may not materialize. A statement of earnings prepared on this basis would be very timely but not totally reliable, and shareholders might be misled into thinking that the company is doing better than it really is.

- In the second case, by delaying recognition of the sale until the goods have been delivered and the cash has been collected, all the uncertainty will have been resolved; however, a significant amount of time may have passed. A statement of earnings prepared on this basis would be totally reliable but not very timely, and would not provide a good measure of the company's business activity during the period(s) before the cash is collected.

- In the third case, by delaying recognition of the sale until the goods have been delivered the uncertainty about the delivery will be resolved, but not the uncertainty about the collection of the cash. A statement of earnings prepared on this basis would be less timely but more reliable than the first case, and more timely but less reliable than the second case.

LEARNING OBJECTIVE 6

Explain the basic concepts of revenue recognition and expense matching.

The accrual basis of accounting attempts to balance the trade-off between timeliness and reliability, and measures performance (by recording revenues and expenses) in the period in which the performance takes place. Under the accrual basis of accounting, revenue recognition criteria are used to determine when revenue should be recorded (i.e., when the earning process has been substantially completed). Chapter 4 discusses these criteria in detail, so the following discussion will deal only with general principles.

Generally, revenue should not be recorded when a customer places an order or signs a contract (as described in the first case above), because the company has not completed the major things it must do to earn the revenue. The company must still deliver the goods, which is a major part of the earning process. On the other hand, it would not usually be necessary for the company to wait until the cash is collected and the entire process is finished (as described in the second case above) before the revenue could be recognized. In most situations, the revenue can be recorded when the company delivers the goods (as described in the third case above), as long as it is reasonably sure that it will be able to collect the cash.

The revenue recognition criteria used under the accrual basis of accounting provide shareholders with assurance that the amounts reported as revenues and expenses on the statement of earnings are reasonable, and that it is very likely that the revenues and expenses that have been recorded will ultimately result in similar cash flows.

As mentioned earlier, the alternative to the accrual basis is the cash basis of accounting. If the cash basis were used, events would be recorded whenever their cash effects occur. For example, sales revenue would be recorded when cash is received from customers, and the cost of goods sold expense would be recorded when the cash is paid for purchases of inventory. As a result, on this basis you could record revenues from selling inventory in a later accounting period than the expenses for purchasing it. Or, if the company purchased its inventory on account (to be paid for later), you could record revenues from selling the inventory in an earlier period than you record the expenses for purchasing it. In either case, you would have the revenue recorded in one accounting period and its associated expense in another, and the statement of earnings would not show the company's performance in a meaningful way. This is the main reason why the cash basis of accounting is not used very often. (In the past, most not-for-profit organizations used the cash basis, but today most of them have switched to the accrual basis of accounting. However, the cash basis is still used by some not-for-profit organizations, farmers, fishers, and professional service companies.)

For a retail business such as Demo Company, the revenue recognition criteria are generally met when the inventory is transferred to the customer. Therefore, in the preceding analysis, the result of Transaction 7 is to recognize revenues (which increases the retained earnings). We assume that once the goods have been delivered, Demo knows how much it has earned and is reasonably sure that it will be able to collect its accounts receivable. Therefore, it should recognize revenues when the goods are transferred to customers, and not wait until the cash is collected.

Another equally important aspect of accrual-basis accounting is the matching concept. This principle of accounting requires that all the costs that are associated with generating sales should be matched on the statement of earnings with the revenue that has been earned. That is, the cost of goods sold (and any other expenses) related to this revenue should be recognized in the same period and reported on the same statement of earnings as the sales revenue. Transaction 8 deals with the cost of goods sold related to this transaction.

Transaction 8: Cost of Goods Sold

The cost of the items that were sold and removed from inventory during January was $9,000.

ANALYSIS As explained in the analysis of Transaction 7, there are two parts to sales transactions. Transaction 7 dealt with the revenue side of the January sales. In this transaction, the costs or expenses that are to be matched with the revenues are analyzed.

The effect of the outflow of the items that were sold is to decrease both the assets (inventory) and the shareholders' equity (retained earnings) by the cost of the goods that have been sold to customers. The cost of goods sold is an expense, which decreases the net income and retained earnings. It is one of the many expenses that the company will show on its statement of earnings.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 8

Assets (specifically, Inventory) decreased by $9,000

Shareholders' Equity (specifically, Retained Earnings) decreased by $9,000

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT This transaction has no effect on cash. The cash flow effects of inventory transactions occur when payments are made for the goods that were purchased.

EARNINGS EFFECT The cost of goods that have been sold is an expense that will be reported on the statement of earnings. Accordingly, the amount in the retained earnings column has been designated with an E.

RELATED CONCEPTS—The matching principle As explained earlier, in the analysis of Transaction 7, when revenues are recognized the matching concept requires that the expenses associated with those revenues be recognized as well. Under accrual-basis accounting, the cost of inventory is held in an asset account until it is sold; when it is sold, it is transferred to an expense account. This illustrates a very important concept, so further elaboration is warranted: Under accrual-basis accounting, a cost can be classified as either an asset or an expense, depending on its nature.

- If the cost represents something that still has value to the company and will be of economic benefit to it in the future, it is classified as an asset and reported on the statement of financial position.

- If the cost represents something that has already given up its value to the company and will not be of further benefit to it in the future, it is classified as an expense and reported on the statement of earnings.

Many costs are initially classified as assets but eventually reclassified as expenses. For example, while Demo holds the inventory, its cost is recorded as an asset (inventory); but when the inventory is sold, its cost ceases to be an asset and must be transferred to an expense account (cost of goods sold). For a retailer such as Demo, the inventory's cost is the wholesale price that Demo paid to acquire it.

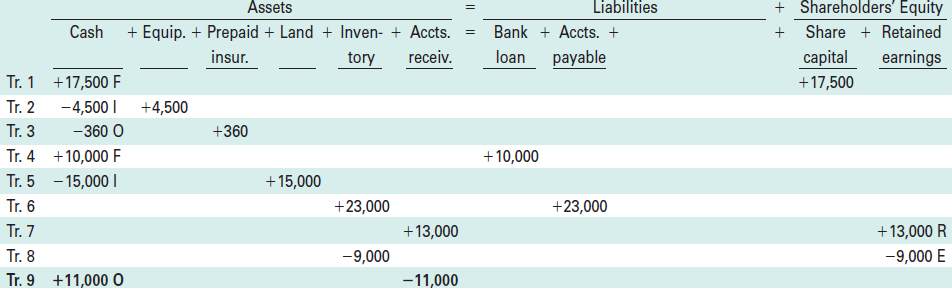

Transaction 9: Collections from Customers on Account

During the month, Demo Company received $11,000 from customers as payments on their accounts.

ANALYSIS The receipt of cash from customers increases Demo's cash. Because the company received this money from its customers as payments on their accounts, the value of the accounts receivable decreases by the amount of the payments received.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 9

Assets (specifically, Cash) increased by $11,000

Assets (specifically, Accounts Receivable) decreased by $11,000

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT Since collecting cash from customers is a basic operating activity for a business, the amount in the cash column has been designated with an O to indicate that it will be reported under operating activities on the statement of cash flows.

EARNINGS EFFECT It is extremely important to note that this transaction does not involve revenues, and therefore does not affect the company's earnings.

RELATED CONCEPTS The effect on the company's earnings was recorded earlier, in Transaction 7, when the original sale occurred and the revenue was earned. Since the revenue was already recognized when the sale was made, there is no revenue recorded when the account is collected; one asset (accounts receivable) is simply replaced by another asset (cash).

Accounts receivable are generally short-term credit arrangements (typically for a period of 30 days), and do not usually involve interest charges. If this were a note receivable (indicating that a formal document had been prepared and signed, as evidence of the obligation), interest charges would probably be specified. When the customer's payment includes interest, the amount of cash received is more than the selling price and the extra amount is recorded as interest revenue.

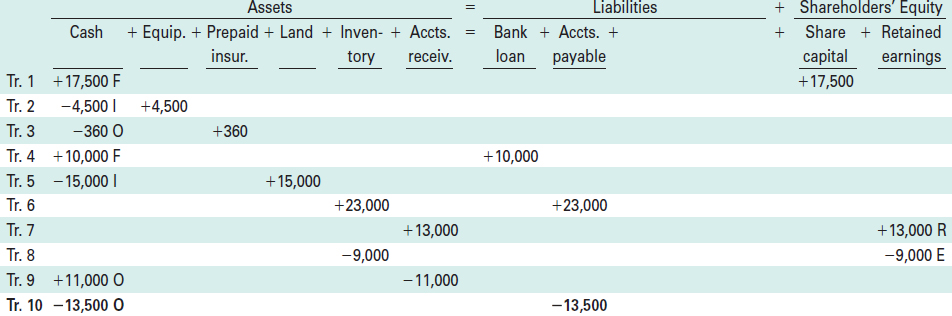

Transaction 10: Payments to Suppliers on Account

Demo Company made payments of $13,500 on its accounts payable.

ANALYSIS Cash payments made by the company result in a decrease in an asset—cash. In this case, because the payment is being made for goods that were purchased earlier, on account, there is a corresponding decrease in a liability—accounts payable.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 10

Assets (specifically, Cash) decreased by $13,500

Liabilities (specifically, Accounts Payable) decreased by $13,500

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT Because paying cash to its suppliers is a basic operating activity for a business, the amount in the cash column has an O beside it to indicate that the cash outflow will be reported under operating activities on the statement of cash flows.

EARNINGS EFFECT Note that paying this debt does not result in an expense being recorded; there is simply a decrease in an asset and a corresponding decrease in a liability. Therefore, there is no effect on the company's earnings.

RELATED CONCEPTS Accounts payable are, of course, the opposite of accounts receivable. Whenever a purchase or sale is made on account, the party making the purchase records an account payable, and the party making the sale records an account receivable.

With accounts payable, there are typically no interest charges (unless the accounts are overdue). However, longer-term financing arrangements (usually represented by notes payable) almost always involve interest charges. When interest is involved, the total amount paid to settle the obligation has to be divided between the amount that is repayment of the original liability (i.e., the principal amount of the debt) and the amount that is payment of the interest expense.

Note again that shareholders' equity (retained earnings) is not affected by Transaction 10. The income effects related to inventory are recorded in the period when the inventory is sold, because that is when the cost of the inventory is transferred to an expense account (cost of goods sold). This could occur either before or after the payment of cash to the supplier.

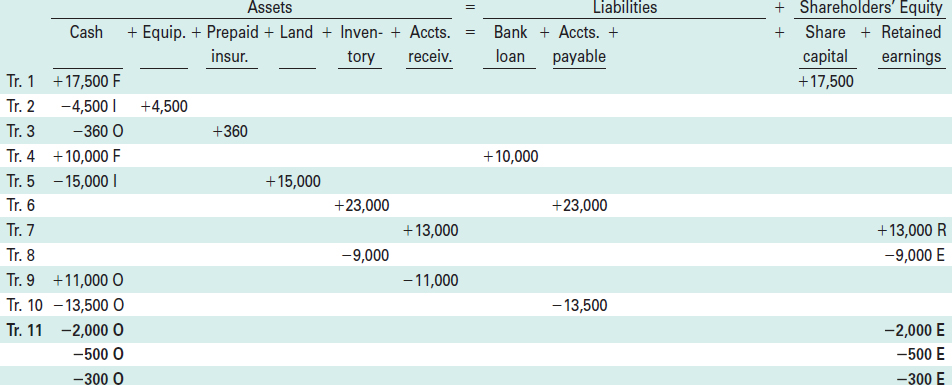

Transaction 11: Cash Expenses

Demo Company paid the following costs for the month of January: $2,000 for salaries; $500 for rent; $300 for utilities (telephone, electricity, water, etc.).

ANALYSIS Because they were incurred to operate the business for the month of January, rather than to acquire something that will be used up in the future, the costs in this transaction should be recorded as expenses for January. (Remember that unexpired costs are assets, and expired costs are expenses.) Expenses reduce net earnings for the period, which will reduce retained earnings.

Because the payments of these costs required outflows of cash, the asset cash is decreased. This is counter-balanced (i.e., the accounting equation is kept in balance) by a decrease in the retained earnings portion of shareholders' equity, representing the effect of the expenses. Note that, in order to provide as much information as possible about the operation of the business, each of these expenses is listed separately. This ensures that when the statement of earnings is prepared the details of the company's expenses can be shown.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 11

Assets (specifically, Cash) decreased by $2,000, $500, and $300

Shareholders' Equity (specifically, Retained Earnings) decreased by $2,000, $500, and $300

CASHFLOW EFFECT Since these payments are related to the operation of the business, they are classified as operating cash flows. Accordingly, the amounts entered in the cash column have an O beside them.

EARNINGS EFFECT Since these costs are expenses, the amounts listed in the retained earnings column have an E beside them and will be reported on the statement of earnings.

Transaction 12: Declaration and Payment of Dividends

Demo Company declared and paid dividends of $250.

ANALYSIS Dividends are payments to the shareholders of the company, as authorized by the company's board of directors. They distribute part of the company's earnings to its owners. They are not expenses, because they are not incurred to operate the business and generate revenues.

When dividends are declared (i.e., announced by the directors of the company), the effect is to reduce the shareholders' equity (retained earnings) and either to decrease the assets (cash), if the dividends are paid immediately, or to increase the liabilities (dividends payable), if they are to be paid later. In this case, the dividends were declared and paid, so cash is reduced.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 12

Assets (specifically, Cash) decreased by $250

Shareholders' Equity (specifically, Retained Earnings) decreased by $250

CASHFLOW EFFECT Because dividends are related to the company's shares (which are a primary source of financing for a business), the payment of dividends is generally classified as a financing activity. Accordingly, the outflow in the cash column has an F beside it.

EARNINGS EFFECT Notice that, in the shareholders' equity section of the equation, the decrease in the retained earnings column has a D beside it to indicate that this amount represents dividends, not expenses. This is an important distinction because, although dividends and expenses both reduce a company's retained earnings, dividends are not part of the calculation of net income and do not appear on the statement of earnings.

RELATED CONCEPTS Dividends are determined and announced (declared) by a vote of a company's board of directors. On the date of declaration, they become a legal obligation of the company. If there is a delay between the date the dividends are declared and the date they are paid, a liability (dividends payable) exists between these dates. In the case of Demo Company, however, the dividends are declared and paid in the same accounting period, so the dividends payable account is ignored.

Dividends explain part of the change in retained earnings from the beginning of the period to the end of the period. As discussed previously, net earnings (consisting of revenues minus expenses) increase a company's retained earnings, and dividends declared decrease the retained earnings.

Finally, note once again that dividends are not expenses and do not appear on the statement of earnings.

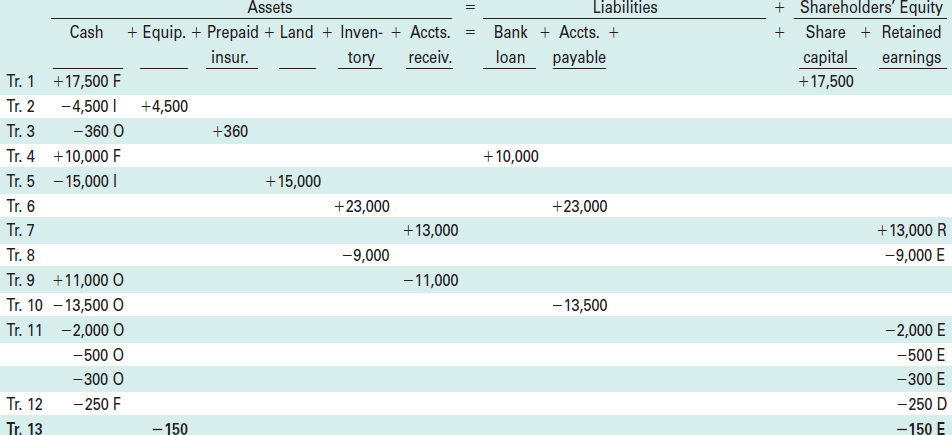

Transaction 13: Depreciation Expense

Demo Company's accountant determined that the equipment should be depreciated by $150 for the month of January.

ANALYSIS Whenever an expenditure is made to acquire an asset, there are three general questions to ask about the nature of the transaction:

- Has an asset been created?

- If so, what is the value of the asset?

- When is the value of the asset consumed, or when does the asset cease to exist?

To answer the first question, the criteria for recognizing an asset must be considered. Does the item have probable future value, and does the company own it or have the exclusive right to use it? If the answers to both of these questions are yes, an asset exists and should be recorded.

When Demo originally purchased its equipment, the answer to both of these asset recognition questions was yes. Demo owned the equipment and it had future value, because the equipment was to be used to help operate the business and thus generate revenues. The equipment, therefore, was recorded as an asset when it was purchased (in Transaction 2).

The answer to the second question, regarding the value of the asset, is simply that, according to GAAP, the equipment is valued at its acquisition cost (sometimes called historical cost). In this example, the $4,500 that was paid for the equipment when it was purchased represents its historical cost.

The third question (When is the value of the asset consumed, or when does the asset cease to exist?) is a little more difficult to answer. For an asset such as inventory, the answer is relatively simple: the value of the asset is consumed and the asset ceases to exist when it is sold. As a result, inventory simply stays on the statement of financial position as an asset until it is sold; when it is sold, its cost is transferred to an expense (cost of goods sold) on the statement of earnings. For an asset such as equipment, the answer is more complicated. In the case of a long-term asset such as equipment, the asset's value is consumed as time passes and the equipment is used. Consequently, the asset's useful life (the time until it will cease to have value) must be estimated. For example, the equipment may be expected to last for five years, at which time it will either be sold, traded in for a new piece of equipment, or discarded.

Because an asset such as equipment is used up over time, its value does not simply stay unchanged on the statement of financial position from one period to another. Instead, to fairly measure the company's net income and satisfy the matching principle, some of its cost should be shown as an expense for each of the periods in which it is used. In other words, we should transfer some of the cost of the asset to an expense account each period, so that the cost of using the equipment will appear on the statement of earnings at the same time as the revenues that are generated from using it. The portion of the asset's cost that is transferred to expense each period is called depreciation or amortization.

The amount of depreciation (or amortization) expense in any particular period should reflect the portion of the asset's value that was used up during that time. There are many factors to consider in determining the appropriate amount, and therefore many methods for calculating how much the depreciation expense should be each period. Chapter 8 discusses these methods in detail.

The simplest and most common method is straight-line depreciation. It assumes that an asset's value is consumed evenly throughout its life and therefore charges the same amount of depreciation expense in each accounting period. The formula for calculating straight-line depreciation is:

Note that two estimates are required in this calculation. First, the useful life of the asset must be estimated. This could be expressed in years or months, depending on the length of the accounting period. In the Demo Company example, we will be preparing financial statements at the end of each month, so the depreciation expense should be calculated as an amount per month. The second estimate is the residual value of the asset. This is how much the asset is expected to be worth at the end of its useful life. For example, if Demo's equipment is expected to have a useful life of two years (24 months) and a residual value of $900 at the end of its life, the monthly depreciation would be calculated as follows:

At the end of each month, Demo would reduce the value of the asset (the equipment) on the statement of financial position by $150, and show a $150 expense (depreciation) on the statement of earnings.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 13

Assets (specifically, Equipment) decreased by $150

Shareholders' Equity (specifically, Retained Earnings) decreased by $150

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT This transaction has no effect on cash. The cash outflow for the equipment occurred in the period when it was purchased. There might be a cash inflow in the future, when the equipment is sold at the end of its useful life. However, during the asset's life, depreciation simply transfers a portion of the equipment's cost from the asset account to an expense account; it does not involve cash.

EARNINGS EFFECT Notice that the amount deducted in the retained earnings column has an E beside it, indicating that it is an expense and will therefore be reported on the statement of earnings.

HELPFUL HINT

The process of depreciating a capital asset is just one example of how a cost can be initially recorded as an asset but eventually transferred to an expense as time passes and the cost expires (i.e., the benefits provided by the asset are consumed). Conceptually, it is similar to how a prepaid expense is handled, as illustrated in Transaction 14.

RELATED CONCEPTS—Depreciation As will be discussed further in Chapter 8, the choice of which depreciation method should be used is influenced by several factors, including the nature of the asset and how the company will use it. To achieve a good matching of revenues and expenses, a company should choose the depreciation method that best reflects the pattern of the economic benefits that will be received from using the asset.

Note that, in the table above, the $150 reduction of the asset's value has been taken directly out of the equipment account. In actual practice, however, the reduction in the value of a capital asset due to depreciation is kept in a separate account, called accumulated depreciation. Over time, this account collects (i.e., accumulates) all the reductions in the asset's value. When a statement of financial position is prepared, the balance in the accumulated depreciation account is deducted from the balance in the capital asset account, and the net amount (i.e., the remaining cost of the asset) is shown. You will see this in Demo Company's statement of financial position, on page 105. An account such as accumulated depreciation is called a contra-asset, because it is offset against, or deducted from, the related asset.

By using a separate account for the accumulated depreciation, both the original cost of the asset and the amount that has been written off through depreciation can be reported. This is desirable, because users of financial statements often find it helpful to know both the original cost of an asset and its remaining cost.

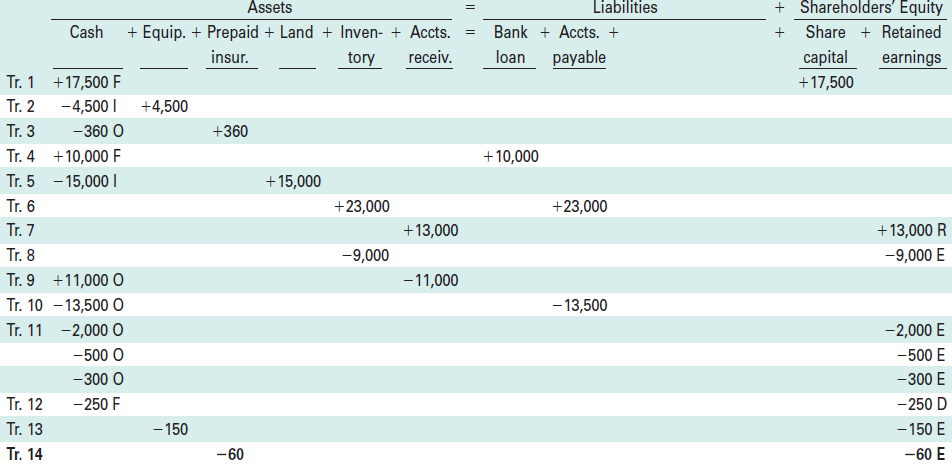

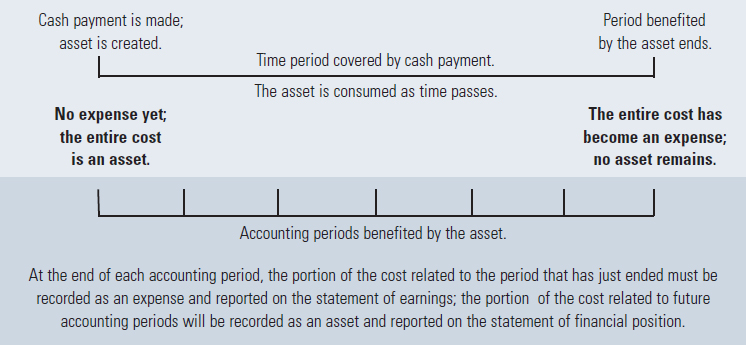

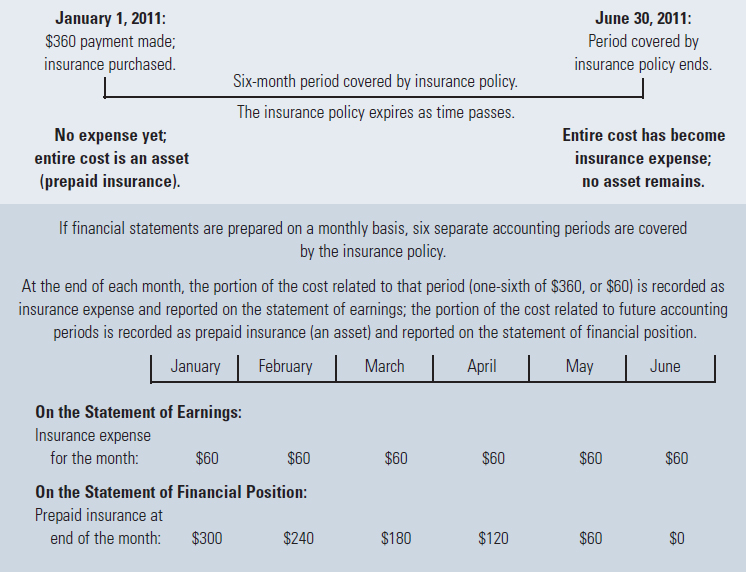

Transaction 14: Insurance Expense

Insurance expense has to be recorded for January. The insurance policy (which was purchased in Transaction 3) covers the six-month period from January 1 to June 30, 2011.

ANALYSIS As discussed in the analysis of Transaction 3, insurance is an example of a prepaid expense because the cost of the insurance coverage was paid in advance of the coverage period. Therefore, at the beginning of January when the insurance policy was purchased, it was recorded as an asset since it had not been used up yet. Only as time passes is the asset (the insurance coverage) consumed.

HELPFUL HINT

Remember that costs can be classified as either expenses or assets, depending on whether or not they have expired (i.e., been consumed). Expired costs relate to the past and are reported on the statement of earnings as expenses; unexpired costs relate to the future and are reported on the statement of financial position as assets.

In this example, the portion of the coverage that is consumed as each month passes is one month out of six, or one-sixth of the total cost. Therefore, we should charge 1/6 × $360 = $60 to expense each month, to spread the cost of the insurance evenly over the coverage period. Accordingly, for the month of January, $60 of the insurance cost should be treated as an expense. The remaining $300 of the insurance cost at the end of January should be treated as an asset, representing the value of the remaining coverage that will be consumed in the future (i.e., between February 1 and June 30).

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

Shareholders' Equity (specifically, Retained Earnings) decreased by $60

Assets (specifically, Prepaid Insurance) decreased by $60

EFFECTS ON THE BASIC ACCOUNTING EQUATION

CASHFLOW EFFECT This transaction is similar to the preceding one, and has no effect on cash. The cash outflow for the insurance was shown when the asset was purchased. During each period of the asset's life, adjustments such as this are made to transfer a portion of the cost of the insurance from the asset account to an expense account; these adjustments do not involve cash.

EARNINGS EFFECT Notice that the deduction under retained earnings has an E beside it, indicating that this is an expense which will be reported on the statement of earnings for January.

You should also note that the balance in the prepaid insurance account will now be the correct amount as of the end of January ($300, representing five remaining months of insurance coverage), because when we recorded Transaction 3 we added $360 to the prepaid insurance column and in this transaction we deducted $60 from it.

RELATED CONCEPTS—The matching principle The initial handling of prepaid expenses as assets is dictated by the accrual basis of accounting and the principle of matching expenses with revenues in the proper accounting periods. In this case, although the cash payment for the insurance is made in January, we cannot classify the entire $360 as an expense of that month. Rather, the cost must be spread over the six-month period of the insurance coverage. As each month goes by, one-sixth of the insurance cost must be transferred to an expense account.

Exhibit 2-1 shows a timeline illustrating the effects of a prepaid expense and the timing issue involved. Part of the cost will be an expense on the statement of earnings in the current period, and the remaining portion will be an asset carried forward on the statement of financial position into the following period.

EXHIBIT 2-1 PREPAID EXPENSES: General Model

Exhibit 2-2 illustrates how the general concepts related to prepaid expenses are applied to the specific case of Demo's insurance policy.

EXHIBIT 2-2 PREPAID EXPENSES: Insurance Example

Transaction 15: Interest Expense

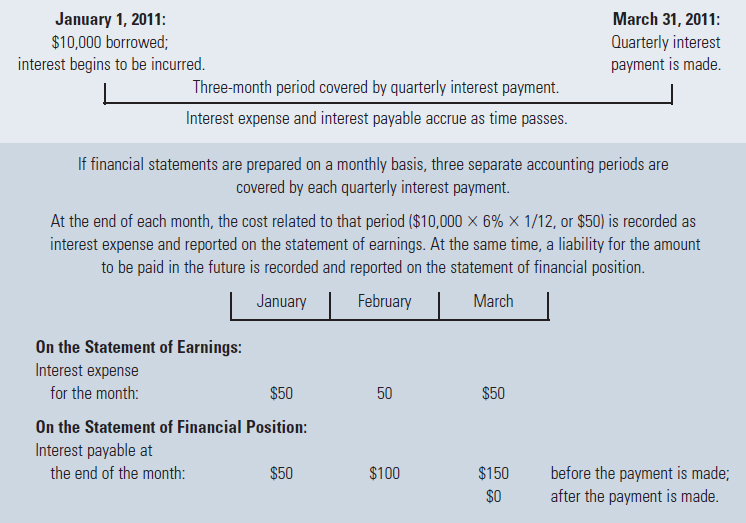

Interest expense has to be recognized for the month of January. The interest rate on the bank loan (which originated in Transaction 4) is 6% per year, and interest payments are to be made quarterly (i.e., at the end of every three months).

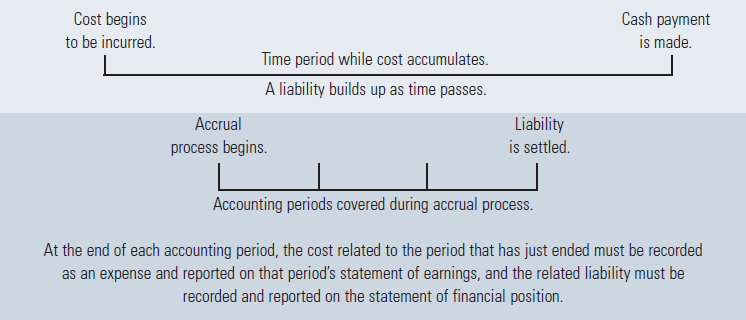

ANALYSIS Interest is the amount charged by lenders for the use of their money. From the borrower's point of view, interest is an expense and therefore results in a decrease in the shareholders' equity during the period when it is incurred. By the end of January, the $10,000 loan has been outstanding for one month; therefore, one month's interest expense should be recognized. Since Demo has not yet paid the interest (and will not pay it until the end of March), it has to recognize a liability now for its obligation to pay the interest later. This is an example of an accrued expense: a cost that has been incurred but not yet paid.

To calculate the amount of interest expense each period, you multiply the amount of the loan (known as the principal) by the interest rate and then by the fraction of the year that has passed (since the interest rate is always expressed as a yearly rate). In Demo's case, the amount of interest incurred in January is $10,000 × 6% × 1/12 = $50. The shareholders' equity (retained earnings) will therefore be decreased by $50, to recognize the interest expense, and a liability (interest payable) will be increased by $50, to recognize the obligation to pay the interest when it is due at the end of the quarter.

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 15

Shareholders' Equity (specifically, Retained Earnings) decreased by $50

Liabilities (specifically, Interest Payable) increased by $50

CASHFLOW EFFECT This transaction does not affect cash. Because the interest on this loan is only paid quarterly, the effect on cash will not occur until the end of the quarter.

EARNINGS EFFECT Even though it has not been paid, the interest on the loan is an expense and will be reported on the statement of earnings for the month of January. Accordingly, the amount deducted in the retained earnings column has an E beside it.

EFFECTS ON THE BASIC ACCOUNTING EQUATION

RELATED CONCEPTS—Accrued expenses Accrual-basis accounting requires that expenses be recognized in the period when they are incurred, rather than when they are paid. This is so they appear on the statement of earnings in the appropriate period and are matched against the revenues that they help to generate. Accrued expenses therefore result in liabilities that appear on the statement of financial position at the end of the period, representing the expenses that have been incurred by that date and will be paid at a future date.

Exhibit 2-3 illustrates how accrued expenses are recognized on the statement of earnings in the period when they are incurred, and result in a related liability on the statement of financial position until they are paid in a future period.

EXHIBIT 2-3 ACCRUED EXPENSES: General Model

Exhibit 2-4 illustrates how the general concepts related to accrued expenses are applied to the specific example of the interest on Demo Company's loan.

EXHIBIT 2-4 ACCRUED EXPENSES: Interest Example

Transaction 16: Income Tax Expense

Income tax expense must be recognized each accounting period, even though the company does not have to pay the tax until later. Demo's income tax rate is 25%.

ANALYSIS Businesses that are incorporated, such as Demo Company Limited, must pay taxes on the income they earn. This income tax is an expense of doing business in Canada, and therefore must be recognized on the company's statement of earnings. In addition, if the tax has not yet been paid, the amount owed must be reported on the statement of financial position as a liability. This is another example of an accrued expense (i.e., a cost of operating the business that has been incurred but not yet paid).

Like any expense, income tax expense reduces the shareholders' equity (because it reduces the company's net earnings, and hence its retained earnings). If the tax were paid immediately, the company's assets (in the form of cash) would be reduced. In this case, however, the company will not pay the tax until later; therefore, its cash is not affected at this time, but its liabilities are increased (in the form of income tax payable).

In order to calculate the amount of income tax expense, we need to first determine the company's income before tax. This can be done quite easily by examining the retained earnings column in the table we have been constructing, and subtracting the expenses from the revenue. Since revenue minus expenses equals income, this calculation will give us the amount of income before tax.

To illustrate this process for Demo Company, refer to the table on page 98 that shows the effects of all the preceding transactions on the basic accounting equation. The retained earnings column lists revenue of $13,000 and expenses of $9,000, $2,000, $500, $300, $150, $60, and $50. Note that dividends are not an expense, and are therefore not included in this calculation. By subtracting the expenses from the revenue, Demo's income before tax is found to be $940 (i.e., 13,000 − 9,000 − 2,000 − 500 − 300 − 150 − 60 − 50 = 940). Applying the income tax rate of 25% to this amount, Demo's income tax expense is found to be $235 (i.e., 0.25 × 940 = 235).

The analysis of this transaction and its effects on the basic accounting equation are summarized below:

ANALYSIS OF TRANSACTION 16

Shareholders' Equity (specifically, Retained Earnings) decreased by $235

Liabilities (specifically, Income Tax Payable) increased by $235

CASHFLOW EFFECT This transaction does not affect cash. The effect on cash will occur later, when the income tax liability is paid.

EARNINGS EFFECT The income tax that will have to be paid for January is an expense and will be reported on the statement of earnings for the month. Accordingly, the amount deducted in the retained earnings column has an E beside it.

RELATED CONCEPTS—The accrual basis of accounting As stated earlier, the accrual basis of accounting requires that expenses be recognized in the period when they are incurred so they appear on the statement of earnings in the appropriate period. This means that even if a company does not have to pay its income tax until later, it must still record the income tax expense that has been incurred during the current accounting period. At the same time, cash will be reduced for any portion of the tax that is paid, and a liability will be recorded for any portion of it that will be paid later. This accrual process ensures that the tax expense appears on the statement of earnings in the period that it relates to, and that a tax liability for the amount owing appears on the statement of financial position at the end of that period. Doing this enables the financial statements to present a true picture of the company's economic performance and financial position.

Although profit-oriented companies have long adhered to these requirements, governments have been slower to move to the accrual basis of accounting, as the following report illustrates.

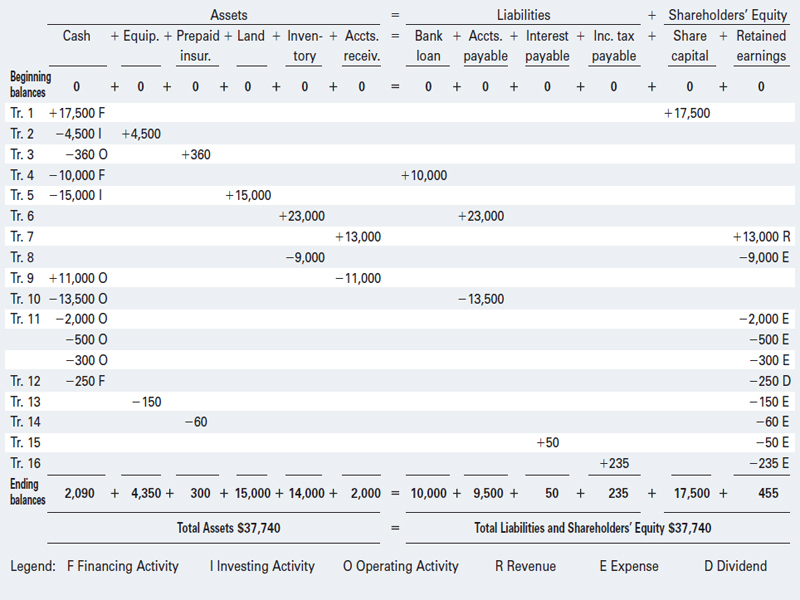

This completes the analysis of the transactions of Demo Company Limited, for the month of January. Exhibit 2-5 shows the combined effects of these transactions on the basic accounting equation, and the resulting account balances at the end of January.

accounting in the news

Accrual-based Accounting in the Federal Government

Since 2003, the Canadian government has presented its financial statements using the full accrual basis of accounting. The move to full accrual accounting from the previous standard of “modified accrual accounting” shifted the focus of financial reporting from expenditures (recorded when funds are spent) to expenses (recorded when resources are used). This change resulted in the recording of tens of billions of dollars in additional assets and liabilities in the country's financial statements, including:

- inventories and prepaid expenses

- capital assets such as land, buildings, ships, and aircraft

- taxes receivable and taxes payable

- liabilities for pension plans for employees and veterans, as well as for health, dental, disability, and worker's compensation benefits

- liabilities related to such items as the cleanup of contaminated military sites, obligations under capital lease arrangements, and additional liabilities for Aboriginal claims

Prior to 2003, these items did not appear on Canada's statement of financial position, or balance sheet. Instead, they were charged against the annual surplus or deficit in the year the assets were acquired, the cash was received, or the liabilities were paid.

The Finance Department reports that the adoption of full accrual accounting provides a more complete measure of the government's financial position. It also reduces the distortions that arise through the timing of cash receipts and payments, and it properly allocates the costs of expensive capital items over the periods of their use, rather than simply the period when they were acquired. The result is a better estimation of the costs of government programs from year to year.

Source: Finance Canada

Note that, because this is a new company, the beginning balances in all the accounts are zero. However, if a company has account balances from previous periods it is essential to include them, because the statement of financial position totals must be cumulative.

Exhibit 2-5 provides all the information required to prepare Demo's financial statements: the statement of earnings, the statement of financial position, and the statement of cash flows. We will now look at each of these.

EXHIBIT 2-5 EFFECTS OF DEMO COMPANY'S TRANSACTIONS IN JANUARY 2011 ON THE BASIC ACCOUNTING EQUATION

LEARNING OBJECTIVE 7

Prepare a simple set of financial statements, reflecting a series of business transactions.

FINANCIAL STATEMENTS

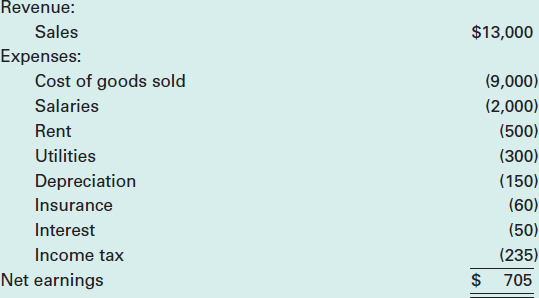

Statement of Earnings

If necessary, you should refer to Chapter 1 for a description of the statement of earnings.

The statement of earnings can be constructed from the information recorded in the retained earnings column in Exhibit 2-5. Since we labelled each of the amounts that affected retained earnings with an R to indicate a revenue, an E to indicate an expense, or a D to indicate dividends, this will be an easy task. Each of the revenue and expense items in the retained earnings column of Exhibit 2-5 has to be reported on the statement of earnings.

In its simplest form, the statement of earnings would be presented as follows. While it would normally be prepared on a comparative basis, because this is Demo's first month of operations there are no figures from previous periods for comparison.

DEMO COMPANY LIMITED

STATEMENT OF EARNINGS

FOR THE MONTH ENDED JANUARY 31, 2011

There are many other ways to organize and present the information on the statement of earnings; however, the net result would be the same. There is a detailed discussion of the statement of earnings and its alternative formats in Chapter 4.

Note that, because they are not an expense, dividends do not appear on the statement of earnings. Rather, they are a distribution of a portion of the earnings to the shareholders, and therefore affect retained earnings. The combination of the income earned and the dividends declared during the period explains the change in retained earnings, as follows:

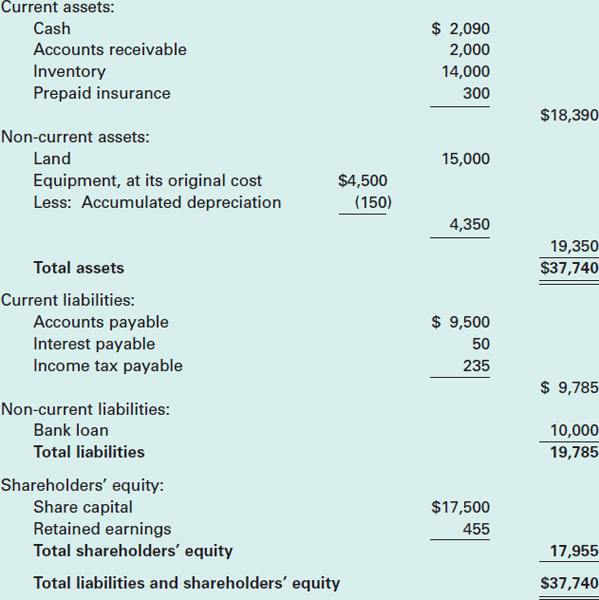

Statement of Financial Position

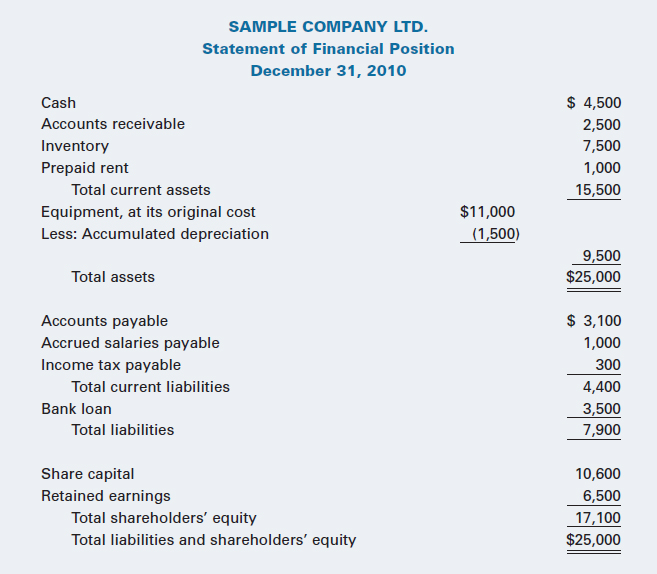

At the bottom of Exhibit 2-5, you can see the net result of Demo's January transactions. These figures represent the amounts that should appear on the company's statement of financial position at the end of the month. However, the table presented in Exhibit 2-5 is not a statement of financial position. Although the same ending balances from Exhibit 2-5 will be shown on the statement of financial position, we have to reorganize the data and present it in a more formal manner.

The statement of financial position could be presented as shown below. Like all the financial statements, the statement of financial position would normally be prepared on a comparative basis; however, this being Demo's first month, there are no comparative figures.

Notice that the equipment is first shown at its original cost of $4,500; then the portion that has been written off (i.e., the $150 of depreciation that has been charged to date) is deducted, leaving the remaining amount of $4,350. This net amount is usually referred to as the asset's book value or carrying value.

You should also note that Demo's statement of financial position is indeed balanced; that is, the company's total assets are equal to the sum of its liabilities and shareholders' equity (as they must be, to satisfy the basic accounting equation).

DEMO COMPANY LIMITED

STATEMENT OF FINANCIAL POSITION

JANUARY 31, 2011

This is a classified statement of financial position, which means that the assets and liabilities have been categorized as current and non-current.

LEARNING OBJECTIVE 8

Explain the basic classification of items on a statement of financial position.

As you may recall from Chapter 1, current assets include short-term items such as cash, accounts receivable (that will be converted to cash within a year), and inventory and prepaid expenses (that will be sold or consumed within a year). Within the current assets section, the individual items are generally listed in the order of their liquidity—i.e., how quickly they can be converted into cash. Thus, the most liquid current assets, cash and accounts receivable, are listed first, followed by inventory and then items such as prepaid expenses (the least liquid).

Assets that will last more than one year, such as land and equipment, are classified as non-current assets. Within the non-current assets section, the items are typically listed in order of permanency, starting with the assets with the longest lives. Thus, land will usually be listed first, followed by buildings, and then equipment, vehicles, and so on—based on the length of time these assets will be useful to the company.