chapter 9

CURRENT LIABILITIES, CONTINGENCIES, AND COMMITMENTS

RECOGNITION CRITERIA FOR LIABILITIES

VALUATION METHODS FOR LIABILITIES

Current Liabilities Related to Operating Activities

Current Liabilities Related to Financing Activities

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Describe the recognition criteria and valuation methods for liabilities.

- Explain why accounts payable are sometimes thought of as “free debt.”

- Understand the issues in accounting for a company's payroll.

- Explain warranty obligations and how they are accounted for.

- Explain unearned revenues and describe situations where they must be recorded.

- Describe the nature of non-financial liabilities and provisions.

- Understand the concept of constructive obligations.

- Explain why companies use working capital loans and lines of credit.

- Calculate the amount of interest owed on various types of short-term notes payable.

- Explain why any portion of long-term debt that is due within a year is classified as a current liability.

- Calculate the accounts payable turnover rate and average payment period.

- Explain contingencies and how they are accounted for.

- Explain what commitments are and how they are handled.

Good Payroll Systems Help Keep Employees Happy

Mountain Equipment Co-op sells outdoor clothing and gear in stores across Canada, and worldwide through its catalogue and website. Founded in 1971, MEC has a reputation among its members for its helpful, knowledgeable staff, with some 1,670 employees working at its stores in Victoria, Vancouver, North Vancouver, Edmonton, Calgary, Winnipeg, Burlington, Toronto, Ottawa, Montreal, Longueuil, Quebec City, and Halifax, as well as its Vancouver call centre.

As a consumer co-operative—customers pay $5 for a lifetime membership—MEC depends on the dedication of its personnel, including sales staff, who are all active outdoor enthusiasts themselves and do not receive commissions. This is why Controller Doug Wong considers payroll to be the most important aspect of MEC's accounting for liabilities. “Payroll is a huge area,” he explains. “In fact, it is our biggest operating expense. It's also an area where there is little margin for error—pay reflects how valued employees feel, and they are understandably sensitive about it. So we endeavour to have accurate payroll, and we do.”

Four full-time staff members at MEC's Vancouver head office handle all payroll functions for the stores across Canada, which have salaried and hourly, full- and part-time employees. While inventory, general accounting, and warehouse operations are managed by one program, MEC uses a separate system for payroll. The routine calculations for pay, deductions (for income taxes, the Canada Pension Plan, and Employment Insurance), and benefits (both statutory benefits and supplemental disability and premium health-care plans) is straightforward with today's computerized accounting systems. However, exceptions, such as provincial variations in rules for holiday pay, enhancements to company-sponsored employee benefits like bike and computer loans, or employees leaving, require human intervention or additional calculations.

In the past, hourly employees would fill in time sheets manually, and payroll clerks would then manually enter that data. But MEC implemented an automated time-capture system in 2004. Hourly workers, who are the majority of MEC staff, swipe a card as they arrive and leave, and the number of hours they work is automatically entered into the system, Mr. Wong explains. “This has eliminated much of the data entry work of the payroll group. Now, most of their time is spent dealing with employment changes—new hires, pay changes, leaves of absence, end of employment issues, etc. They also do a fair bit of labour analysis reporting for store and other managers.”

MEC can configure the system to track time in many ways, to not only produce accurate results but also provide information that is useful to management. For example, employees can swipe their cards every time they work in a different area of the store—the floor area, the cash area, the stock room, and so forth—keeping store managers informed about how their resources are being allocated. In addition, when employees are scheduled to work in different areas, the time and attendance system can calculate their pay according to their schedules. “This is an example of where MEC leverages technology to effectively and efficiently manage a business process,” says Mr. Wong.

People like Doug Wong of Mountain Equipment Co-op understand that good employee relations are important to a successful business. Knowing that errors in payroll can affect employee morale, one way that MEC fosters good relations is through strict attention to detail in its payroll. Smaller businesses, and even some medium-sized and large companies, often find it more cost-effective to use an outside group with expertise in a particular accounting area (such as payroll) rather than to hire employees for this function. MEC once used an outside contractor for its payroll function. However, having grown to the point where it wants more information from its payroll data, MEC has chosen to customize its information flow by making the payroll function an internal one.

Successful businesses also pay attention to obligations owed to people outside the company. A good reputation for paying debts on time enables a company to use credit to operate effectively and to take on new initiatives. A poor credit rating, on the other hand, limits a company's options for outside financing.

In this and the next two chapters, our attention turns to the credit side of the statement of financial position and the accounting for liabilities and shareholders' equity. The common factor is that both liabilities and shareholders' equity can be viewed as sources of assets. Liability holders contribute assets in return for a promise of repayment at some future date, usually with interest. Shareholders contribute assets to the company in return for an ownership interest and the right to share in company profits.

In this chapter, the general nature of liabilities is discussed first, followed by various types of current liabilities. Chapter 10 deals with major non-current liabilities, and shareholders' equity issues are covered in Chapter 11.

USER RELEVANCE

Current liabilities represent obligations that the company must settle within the next year (or operating cycle of the business, if that is longer). Most of these obligations—accounts payable, income taxes payable, wages payable, notes payable, and so on—will require outflows of cash. Users can examine the current liabilities to determine how much cash will be required and to estimate when that cash will need to be paid. Examining the current assets, especially cash, accounts receivable, and short-term investments, provides users with information about the availability of cash. We have already talked about determining how quickly inventory is sold and accounts receivable are collected, using turnover ratios. These help users estimate whether enough cash will be available when the various liabilities come due. If there will not be sufficient cash available, the company will have to go to outside sources—taking on additional short- or long-term debt, or issuing more shares—in order to raise additional cash. Understanding a company's short-term cash needs is essential to determining its current financial health and what may need to be done to ensure its long-term viability.

RECOGNITION CRITERIA FOR LIABILITIES

Liabilities represent the company's obligations arising from past transactions or events. Specifically, to be classified as a liability an item must have the following three characteristics:

- It represents a duty, responsibility, or obligation that imposes an economic burden (i.e., it requires the transfer of assets, the performance of services, or the conferring of some other benefit).

LEARNING OBJECTIVE 1

Describe the recognition criteria and valuation methods for liabilities.

- It is enforceable; the entity has little or no discretion to avoid the obligation. If the entity does not settle it, the creditor usually has the right to pursue legal action.

- The obligation exists at the present time. The exact amount may not be determined until a later event has occurred, but the underlying transaction or event creating the obligation has already occurred.

What is uncertain about liabilities is usually the dollar value of the assets, services, or other benefits to be given up, and when they will be given up. To avoid uncertainty about the amount and timing of the settlement, some liabilities, such as accounts payable and most loans, have fixed payment schedules and due dates. For example, in loan agreements the interest and principal payments are specified, as are the dates on which those payments are to be made. Other liabilities, such as warranty obligations, have neither fixed amounts nor fixed dates. For example, the settlement of a warranty obligation will depend on when the customer detects a warranty problem and how much cost the company incurs to fix it. Liabilities, therefore, differ in their degree of uncertainty.

If the obligation is conditional upon some future event, a liability might not be recognized in the financial statements. Suppose, for example, that a company is under investigation by the government for alleged chemical contamination of a river. If the company is found negligent, there could be a significant liability if it is required to clean up the contamination and/or a fine is imposed. However, the company may insist that it is not responsible for the contamination and that the probability that it will be found negligent is low. In such a case, no liability will be recorded in the accounts. However, because a significant amount of assets may have to be transferred in the future, the company would generally disclose information about the investigation and the potential obligation in the notes to its financial statements. Under IFRS, such an item is referred to as a contingent liability, meaning that the liability has not been recorded in the accounts, because the obligation is conditional, dependent, or contingent on the occurrence of a low-probability future event.

The ownership criterion that is used for assets does not strictly apply to liabilities, but a similar notion does. Companies should record only those obligations that they will be required to satisfy. For example, if a customer falls on the company's property, sues the company for medical costs, and wins, the company may not be obliged to make the payment. If the company is insured against such claims, the insurance company will make the payment. The company, therefore, would not record the obligation to settle the customer's claim as a liability on its books, because it is the insurance company's obligation. (However, if the insurance does not cover the full amount, the company would record a liability for its portion of the payment.)

It is sometimes hard to determine whether the event giving rise to the obligation has already occurred. For example, in the case of the lawsuit mentioned above, what is the event that gives rise to the obligation? Is it the customer falling, the filing of a lawsuit, or the court's decision? In this case, the probability that an obligation exists increases as each subsequent event occurs. However, the event that gives rise to the ultimate obligation is debatable. More will be said about this later.

Another potentially difficult situation to evaluate can arise when a company signs a binding contract. Suppose, for example, a company signs a contract to purchase 1,000 units of inventory at $30 per unit, to be delivered 60 days from now. Is the signing of the contract the event that gives rise to the obligation to pay for the inventory, or is it the delivery of the inventory? The company's obligation is conditional upon the seller performing its part of the contract, by delivering the goods on time. If the goods are not delivered, then the company will not be obliged to pay. The contract signing creates what is known as a mutually unexecuted contract because, at the time of signing, neither the buyer nor the seller have performed their part of the contract. The seller has not delivered any inventory, and the buyer has not paid any cash. Such contracts are normally not recorded in the accounting system, although the company may include information about them in the notes to its financial statements.

A partially executed contract is one in which one party has performed part or all of its obligation. In the example just given, the contract would be viewed as partially executed if the buyer paid a $3,000 deposit. The buyer would show an outflow of cash of $3,000, and create an asset account for the right to receive inventory valued at $3,000, called “deposits on purchase contracts” (or something similar). The seller would show an inflow of cash of $3,000 and create a liability account to represent its obligation to deliver inventory valued at $3,000. The liability account would probably be called “unearned revenue.” Once inventory valued at $3,000 is delivered to the customer, the obligation will be satisfied and the revenue will be earned. Note that only the amount of the deposit ($3,000) would be recorded at this time, not the full amount of the contract (1,000 units × $30 per unit = $30,000).

VALUATION METHODS FOR LIABILITIES

Just as there are different methods for valuing assets, there are different methods for valuing liabilities. Theoretically, a liability should be valued at its present value on the date it is incurred. In practice, however, there are several other possible valuation methods to be considered.

One way to value a liability is to record it at the gross amount of the obligation—i.e., the total of the payments to be made. For example, if an obligation requires a company to pay $1,000 each month for the next three years, the gross obligation would be $36,000. However, while this amount accurately measures the total payments to be made, it may not accurately measure the company's obligation at the time it is reported on the statement of financial position. For example, suppose the obligation is a rental agreement for a piece of machinery. If the rental agreement can be cancelled at any time, the company is only obligated to pay $1,000 each month. The remaining payments will be an obligation only if it keeps using the machinery. If the contract cannot be cancelled, valuing the liability at the full $36,000 would make more sense.

Another reason why the gross obligation may not adequately measure the liability's value is that it ignores the time value of money. Suppose that, rather than being a rental payment, the $1,000 each month is to repay a loan (including both interest and principal). In this case, the total payments of $36,000 include both the repayment of principal and the payment of interest. However, since interest only accrues as an obligation as time passes, the only liability that exists initially is for the principal of the loan. For example, if the principal amount of the loan is $30,000 the company could settle the obligation at the outset with a payment of $30,000. The difference ($6,000) between this amount and the $36,000 gross amount is the interest that accrues over time. If the initial liability was recorded at the full $36,000, the company's obligation at the present time would be overstated.

To recognize the time value of money, whenever the interest component is significant companies should record their liabilities at their present values. To do so, both the future principal payments and the interest payments are discounted back to the present time, using the appropriate interest rate. (Present value concepts and calculations are discussed in detail in Chapter 10.) Under this valuation system, the company initially records the obligation at its net present value, rather than the gross amount of the future payments to be made. As time passes, interest expense is recorded, which recognizes the cost of the loan and increases the liability, and payments are made, which decrease the liability.

What Is Canadian Practice?

As stated above, liabilities should, theoretically, be recorded at the present value of the future payments. The interest rate that is used should reflect the type of liability, the duration of the obligation, and the company's creditworthiness. Accordingly, short-term notes payable should be recorded at their present values, and the interest on them should be accrued over time.

However, present-value calculations are generally not used for most short-term liabilities, because either no interest is charged on them or the amounts involved are small and the time to maturity is so short that the difference between the present value of the obligations and the gross amount of the payments would not be material. Therefore, they are simply recorded at the gross amounts that are to be paid.

CURRENT LIABILITIES

Current liabilities are those obligations that require the transfer of assets or services within one year or one operating cycle of the company. As just discussed, most of them are carried on the books at their gross amounts. In order for a company to stay solvent (able to pay its debts when they become due), it must have sufficient current assets on hand and/or generated by its operations to pay the current liabilities. Creditors, such as bankers, will often compare a company's total current assets to its total current liabilities to assess its ability to remain viable. Frequently encountered current liabilities are discussed in the following subsections.

LEARNING OBJECTIVE 2

Explain why accounts payable are sometimes thought of as “free debt.”

Current Liabilities Related to Operating Activities

Accounts Payable

As you know from earlier chapters, accounts payable occur when a company buys goods or services on credit. They are often referred to as trade accounts payable. Payment is generally deferred for a relatively short period of time, such as 30 to 60 days, although longer credit periods are allowed in some industries.

Accounts payable generally do not carry explicit interest charges and are commonly thought of as “free debt.” However, there is sometimes a provision for either a discount for early payment or a penalty for late payment. In such cases, not taking advantage of the discount, or paying a penalty for being late, can be viewed as equivalent to interest charges.

LEARNING OBJECTIVE 3

Understand the issues in accounting for a company's payroll.

Wages and Other Payroll Liabilities

Wages owed to employees can be another significant current liability. The magnitude depends, in part, on how often the company pays its employees, because the balance in the account reflects the wages that have accrued since the last pay period.

In addition to the wages themselves, most companies provide fringe benefits for employees. These costs—for medical insurance, pensions, vacation pay, and other benefits provided by the employer—must also be recognized in the periods in which they occur. Because these may be paid in periods other than when they are earned by the employees, any unpaid costs have to be accrued and liabilities recorded for them.

Canadian companies are also required to act as government agents in collecting certain taxes. For example, companies must withhold income taxes from employees' wages and remit them to the government. The amounts paid to the employees are reduced by the amounts withheld. While these taxes are not an expense to the company (because they come out of the employees' earnings), the company must nevertheless keep track of the amounts deducted from employees' earnings and report a liability to pay these amounts to the government.

The amount of income tax to be deducted from employees' earnings depends on many factors, including their expected annual earnings and their personal exemptions for income tax purposes. Therefore, in the examples and problems in this text we will simply state the amount of personal income tax that is to be withheld from the employees' pay.

Other items, such as Canada Pension Plan (CPP) or Quebec Pension Plan (QPP) and Employment Insurance (EI) contributions, are also deducted from employees' wages and remitted to the government. This further reduces the net amounts that are received by the employees.

In addition to the amounts that are deducted from employees' wages, companies must make their own payments to the government for CPP or QPP, EI, workers' compensation plan premiums, and in some provinces, public health-care premiums. These amounts are recorded as an expense to the employer and are shown as liabilities until they are remitted to the government.

As of mid-2010, CPP was deducted from employees' earnings at the rate of 4.95%, while the rate for EI deductions was 1.73%. (However, there are exemptions and maximums that can complicate the calculations, and these rates can change from year to year.) In addition to collecting the amounts deducted from employees, employers were also required (at the time of writing) to contribute an amount equal to the employees' deductions for CPP, and 1.4 times the amount deducted from their employees for EI.

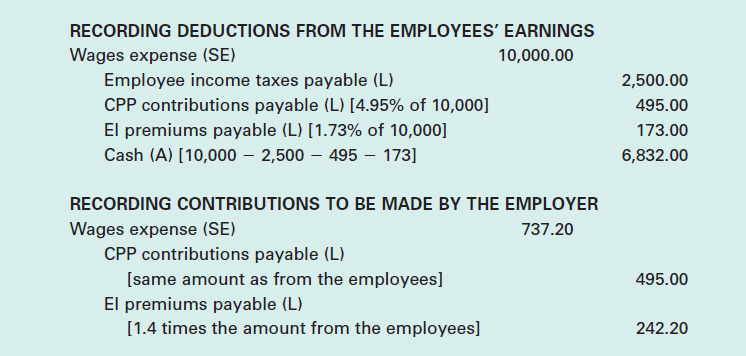

For example, assume that the employees of Angelique's Autobody Shop have earned wages of $10,000, and that income tax totalling $2,500 is deducted from the employees' cheques. In addition, $495 (4.95% of $10,000) is deducted for CPP and $173 (1.73% of $10,000) is deducted for EI. Beyond these amounts, the employer has to pay an additional $495 (the same amount as deducted from the employees) for CPP, and $242.20 (1.4 times the $173 deducted from the employees) for EI, as the company's contributions. The journal entries to record the payroll would be as follows:

Note that, although the employees earned $10,000, the amount actually paid to them in this example, after deductions, is only $6,832.00. This is referred to as their net pay.

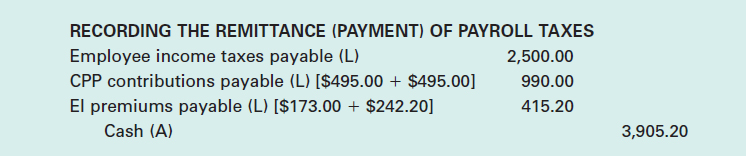

The amounts in the three liability accounts are remitted periodically to the government, according to its regulations. The following journal entry illustrates the remittance of both the employees' deductions and the employer's contributions:

Note that the total amount recorded by the employer as an expense ($10,000.00 + $737.20 = $10,737.20) exceeds the amount it agreed to pay the employees ($10,000.00). Because of these extra amounts that the government requires businesses to pay, companies are concerned each time the government makes changes to the Canada/Quebec Pension Plan, Employment Insurance scheme, or other compulsory programs—unless of course, the government reduces the rates. Employers must always take these additional amounts (which are commonly referred to as payroll taxes) into account in managing their businesses, because they increase the costs of hiring employees. Workers' Compensation Plan premiums and, in some provinces, public health-care premiums also fall into this category.

Corporate Income Taxes

Canadian companies that are incorporated pay both federal and provincial corporate income taxes, and may also be subject to taxation in other countries in which they operate. As mentioned earlier, the regulations governing the calculation of income for tax purposes differ in many respects from the accounting standards for the calculation of income. (The discussion in Chapter 8 concerning deferred income taxes highlighted this difference; deferred income taxes are discussed in greater detail in Chapter 10.) Nevertheless, the taxes that are payable according to the regulations of the taxing authorities must be recorded as a liability.

accounting in the news

Proposed Pension Plan Increases Called Costly Job Killers

In June 2010, the Canadian Federation of Independent Business (CFIB) spoke out against proposed changes to the Canada Pension Plan (CPP), saying increased premiums would kill jobs in small businesses. Before a meeting of the federal and provincial finance ministers, trade unions proposed doubling CCP premiums and benefits, but the CFIB said that more than 70 percent of small business owners oppose these changes.

The CFIB pointed out the huge up-front cost for any business setting up a pension plan. One of the major challenges for small businesses is whether employees and employers have enough income to dedicate to a pension plan. Nearly half of all small-business owners surveyed by the CFIB said they are unable to provide retirement savings benefits for employees.

The CFIB described the mandatory nature of payroll taxes as “the worst form of taxation for small businesses.” It said that if the ministers enacted the proposed increases, the decision would be a “major job killer.”

Source: Andrew Binet, “CFIB Opposes Proposed Pension Hikes: Survey,” The Globe and Mail, June 10, 2010.

The payment of income taxes does not always coincide with the incurrence of the taxes. In Canada, companies are generally required to make monthly income tax payments, usually based on the taxes paid the previous year, so that the government has a steady flow of cash coming in during the year. The deadline for filing a corporate income tax return is six months after the company's fiscal year end, but the balance of taxes owed for the year must generally be paid within two months of the year end and therefore often has to be estimated. Penalties are imposed if the company significantly underestimates the amount of tax payable.

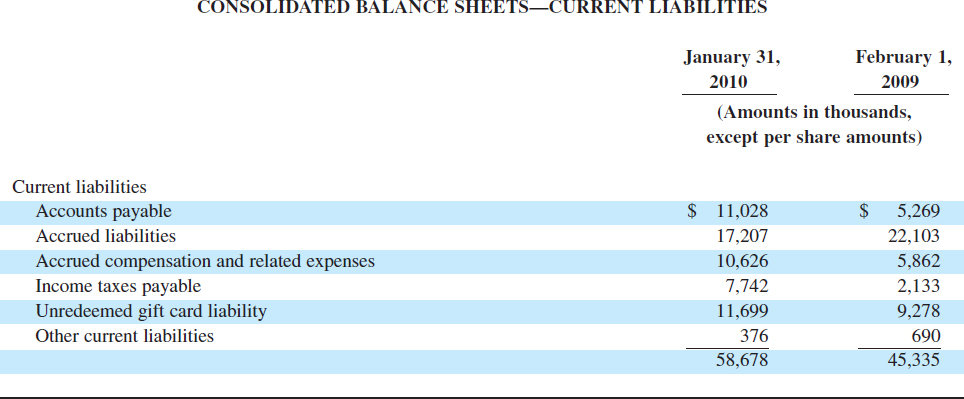

Exhibit 9-1 contains the current liability section of the balance sheet for Lululemon Athletica Inc. and illustrates many of the current liabilities related to operating activities discussed so far. Lululemon produces and sells athletic apparel for yoga, running, and dance. Note the size of the liabilities for accounts payable (which would be primarily for inventory acquisition costs), accrued liabilities (which would include a variety of expenses that have been incurred but not yet paid), accrued compensation and related expenses (which would include unpaid salaries and wages, fringe benefits, and payroll taxes), and income taxes payable (which would be based on the company's earnings). The liability for unredeemed gift cards will be explained in a later section of this chapter.

Warranty Obligations1

When companies sell goods or services, there are often either stated or implied guarantees, or warranties, to the buyers. If a product proves to be defective, the company that manufactured or sold it may have to provide warranty services to repair or replace it. Companies sometimes charge extra for warranties; in other cases they provide warranty coverage at no explicit additional charge. Warranties that are sold separately to customers (i.e., those that have an explicit extra charge) are discussed in the following section on unearned revenues; here we deal only with warranties that are provided at no additional charge.

EXHIBIT 9-1 LULULEMON ATHLETICA INC. 2009 ANNUAL REPORT

LULULEMON ATHLETICA INC. 2009 ANNUAL REPORT

Although, at the time of the product's sale, the company cannot know how much the cost of the warranty services will ultimately be, it should still estimate and accrue the warranty cost in order to match the expense from the warranty to the revenue from the sale. In other words, to satisfy the matching principle, in each accounting period a warranty expense and a warranty liability must be recognized, based on an estimate of the future warranty costs that will be incurred on sales made that period. If the company has been in business for a long time, this estimate can probably be made fairly easily, based on the history of past warranty claims. For new products and new companies, estimating what the future costs will be may be much more difficult.

LEARNING OBJECTIVE 4

Explain warranty obligations and how they are accounted for.

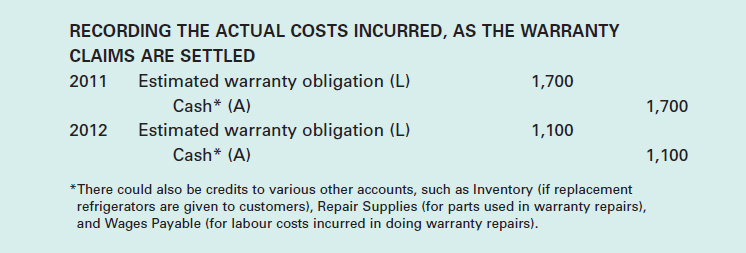

As an example of a warranty situation, suppose a home appliance company sells 200 refrigerators in 2010, and that each refrigerator has a two-year warranty against mechanical defects. Although the company buys quality merchandise from its suppliers, it is very likely that within two years of sale some of these refrigerators will require warranty services. After reviewing its record of past warranty services, the company estimates that approximately 6% of the refrigerators it sells require warranty services during the first year following their sale, and another 4% require warranty services during the second year after their sale. It also determines that the average cost to repair a refrigerator under the warranty is $150. Over the two-year period of the warranty, the company therefore expects that it will have to spend about $3,000 (10% of 200 units = 20 units; 20 units @ $150 per unit = $3,000) on warranty services for the refrigerators sold in 2010. Of course, this is just an estimate based on averages; the actual costs may be more, or less, than $3,000. However, experience and knowledge of their merchandise usually enable companies to make reasonably accurate estimates of their future warranty costs.

To record the estimated warranty obligation in the period of the sale, the company would make the following journal entry:

HELPFUL HINT

Warranty expense is estimated and recorded in the period when the sales revenue is recorded. At the same time, a liability account is created.

When actual costs are subsequently incurred under the warranty, there is no expense recorded. Instead, the warranty liability account is reduced.

Note that the entire estimated warranty cost is recorded as an expense in the year of sale, regardless of the length of time covered by the warranty. Whether the warranty costs will be incurred over two years (as in this example) or some other time period is irrelevant for determining the expense to be reported on the statement of earnings. On the statement of financial position, the portion of the obligation that is expected to be settled within a year would be reported as a current liability, and any portion that extends beyond one year would be reported as a non-current liability.

If, during 2011 and 2012 our company spent $1,700 and $1,100, respectively, for warranty work on these refrigerators, it would record these expenditures by reducing the warranty liability account, as follows:

In this case, it appears that the company overestimated its warranty costs slightly. It estimated that the costs would total $3,000, but the costs were actually $2,800 ($1,700 + $1,100). As a result, the liability account will have a balance of $200 remaining in it. If this pattern continues for several periods, the company may want to reduce its estimates. However, there will probably be some years when the actual warranty costs are higher than estimated, and in the long run things may average out.

As you can see in the foregoing journal entries, no expense is recorded when actual warranty costs are incurred. Rather, the warranty liability account is debited, to reflect the fact that a portion of the company's obligation has been satisfied.

By estimating its expected future obligation at the same time that it records the sale, the company records the warranty expense in the same accounting period as when the sales revenue is recorded. In this way, the statement of earnings provides a better indication of the profitability of that period's operations. If the company delayed recognizing any expense until it actually incurred the warranty costs, in our example the revenue would be in the 2010 statement of earnings and the expenses would be in the 2011 and 2012 statements of earnings. As a result, the profit reported in 2010 would be overstated. For this reason, if warranty costs are material, companies are required to estimate their expected future warranty obligation, and to record this liability and the related warranty expense at the time of sale.

Warranties thus provide another illustration of the importance of ensuring that the statement of earnings shows a complete picture of the operating results each period, and that the statement of financial position shows the company's true financial position at the end of each period. By recording warranty liabilities, accountants recognize that when goods are sold with warranties companies incur obligations to honour the future claims that will be made.

IFRS INSIGHTS

Recent standards under IFRS have moved towards measuring warranty liabilities as the sales value of the goods or services that will be required to satisfy the warranty claims, rather than the company's acquisition cost for these goods and services. To illustrate this, recall our example in which the home appliance company estimated that the cost of repairing defective refrigerators would be $3,000 and therefore recorded a warranty obligation of $3,000. Under the new approach, if the repair services that are expected to be required under the warranty could have been sold for, say, $4,000, the company would record a liability (in the form of unearned revenue) of $4,000. As a result, the current period's earnings would be $1,000 lower, compared to the method we used. However, if the warranty repairs were eventually done at a cost of $3,000, the company would report a profit of $1,000 on the warranty work in the later period's earnings.

Effectively, the new approach assumes that—even when warranties are provided without any explicit additional charge—part of the sales price of the goods or services is related to the warranties that are provided with them. Put another way, it treats the original sale as a “bundle” consisting of the initial goods or services that have been provided at that point plus the additional goods or services that may be provided in the future under the warranty. This makes the treatment of these warranties consistent with the treatment of warranties that are, in fact, sold separately (discussed in the following section on Unearned Revenues).

LEARNING OBJECTIVE 5

Explain unearned revenues and describe situations where they must be recorded.

Unearned Revenues

In many businesses, customers are required to pay deposits or make down payments prior to receiving goods or services. This creates partially executed contracts between buyers and sellers. Because the sellers have not fulfilled their part of the contract, it would be inappropriate for them to recognize revenue at this point. Therefore, sellers t must defer the recognition of revenue from deposits and down payments. These deferrals create liabilities that are known as unearned revenues or deferred revenues.

Businesses that require prepayments show unearned revenues in the liability section of the balance sheet because, by accepting the money in advance, they incur an obligation to provide the related goods or services (or, failing that, to return the money). Magazine and newspaper publishers that sell subscriptions are among these types of businesses. They receive money for subscriptions in advance, and must initially record this as an asset (cash) offset by a liability (unearned revenue). They earn the revenue later, when they deliver the magazines and newspapers. At that time, they reduce the liability account and record the revenue.

Airlines are another example of businesses that receive payments in advance. When a customer pays for a ticket for a future flight, the amount received by the airline must be treated as unearned revenue (a liability) until the flight has been provided; when the flight occurs, the revenue is earned and the liability is eliminated. For example, the current liability section of the balance sheet for WestJet Airlines as at December 31, 2009, included $286,361,000 for Advance Ticket Sales. The accompanying notes stated that “Guest revenues, including the air component of vacation packages, are recognized when air transportation is provided. Tickets sold but not yet used are reported in the consolidated balance sheet as advance ticket sales.”

HELPFUL HINT

Remember that revenues cannot be recorded until they have been earned. Consequently, unearned (or deferred) revenues are reported as liabilities, on the statement of financial position, rather than as revenues on the statement of earnings. Once the related goods have been delivered or services performed, these amounts are considered earned and an adjusting entry is made to transfer them out of liabilities and into revenues.

Gift Certificates and Prepaid Cards

The sale of gift certificates and prepaid cards is a major source of unearned revenue for many businesses. According to accounting standards, gift card revenue is recognized only when the cards are redeemed for goods or services. When a gift certificate or prepaid card is sold, the business records the cash received and an offsetting liability, representing its obligation to provide goods or services equal to the value of the card. Later, when the gift card is used, the liability is eliminated and revenue is recognized.

The popularity of gift cards is having a major effect on the sales patterns of many retail businesses. The November-December holiday shopping season is very important to most retailers. However, much of the money spent on gift cards late in the current year shows up in sales revenues early in the next year, when the gift cards are redeemed. Thus, in terms of revenue recognition, selling gift cards during the holiday shopping period shifts revenues to January and February. In particular, gift card activations (when cards are purchased) drop off sharply after December. In contrast, January redemptions (when gift cards are used to purchase something) are very significant. As a result, the usual drop-off in sales from December to January has moderated. The recognition of December gift card sales as revenues in January has given the start of the new year a significant financial boost, in a time that has traditionally been a slow one for retail businesses.

The following example illustrates the journal entries required to record gift certificates or prepaid cards, and their impact on the financial statements.

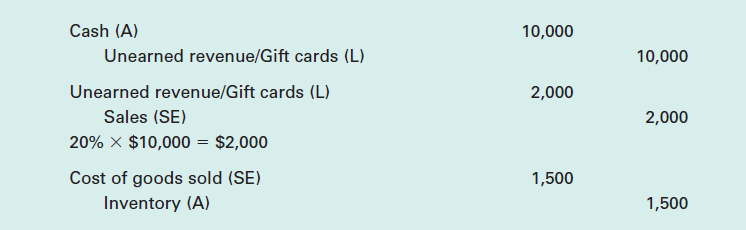

In December 2011, a company sells gift cards worth $10,000. Twenty percent of these are redeemed in December, for merchandise with a cost of $1,500. Sixty percent of the cards are redeemed in January 2012, for merchandise with a cost of $5,000. The remaining 20 percent of the cards are still outstanding at the end of January.

The journal entries for December 2011 would be as follows:

The December 31, 2011, statement of financial position would report a liability of $8,000 ($10,000 − $2,000) of unearned revenue related to the outstanding gift cards. The statement of earnings for the month of December would include sales revenue of $2,000 and cost of goods sold of $1,500, for a gross profit of $500 from the gift cards that were redeemed in December.

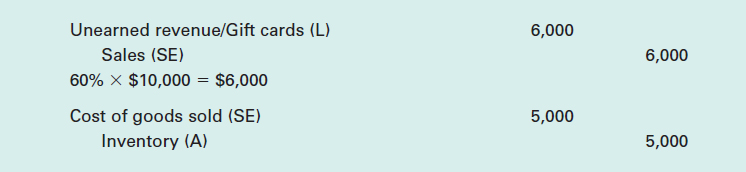

The journal entries for January 2012 would be as follows:

The January 31, 2012, statement of financial position would report a liability of $2,000 ($10,000 − $2,000 − $6,000) of unearned revenue related to the gift cards that are still outstanding. The statement of earnings for January would include sales revenue of $6,000 and cost of goods sold of $5,000, for a gross profit of $1,000 from the gift cards that were redeemed in January.

The current liabilities section of Lululemon Athletica Inc.'s balance sheet (which was presented in Exhibit 9-1) shows that, even though the company has a January 31 year end and many of its gift cards were probably redeemed in January, Lululemon still has a large liability related to unredeemed gift cards included in its current liabilities.

accounting in the news

No End to the Value of Gift Cards

In February 2010, Nova Scotia joined other provinces in banning expiry dates and fees on gift cards. There are two types of gift cards: those for a specific good or service, and those with an associated dollar value. In Nova Scotia, gift cards with a dollar value can no longer have an expiry date. Cards for goods and services purchased before February 1, 2010, will expire as scheduled because the value of the goods or services increase over time; however, cards purchased after this date will not have expiry dates. The regulations also indicate that no fees, such as inactivity fees, can be charged, except customizing or replacement fees, and that the refund policy and contact information must now be included with the cards.

While card buyers benefit from the convenience of gift cards, businesses benefit through both “floatage” and “slippage” (sometimes referred to as “breakage”). Floatage refers to the fact that a gift card-issuing company receives the customer's money without having to deliver the goods or services right away. Slippage refers to the estimated 10 to 15 percent of gift cards that are never redeemed.

Although a little slippage is good, having a large number of unredeemed cards outstanding can create accounting difficulties for companies. This is why many businesses opted to impose expiry dates–that is, until the restrictions introduced by governments. In many provinces, expiry dates are now either not allowed or permitted only in certain circumstances. For example, Nova Scotia's regulations do not apply to charity and promotional cards, prepaid telecom cards, or prepaid cards from credit card companies like Visa or Mastercard.

Sources: Rob Carrick, “Not All Gift Cards Are Created Equal,” The Globe and Mail, December 1, 2009. Access Nova Scotia, “Nova Scotia Gift Cards,” June 6, 2010, http://www.gov.ns.ca/snsmr/access/individuals/nova-scotia-gift-cards

Customer Rewards or Loyalty Programs

Many businesses have customer loyalty programs to encourage their customers to buy from them. Under these programs, points (or other forms of credits) are awarded to customers when they make purchases, and these points can later be redeemed for free goods or services. Some companies participate in general rewards programs, such as Air Miles, that are operated by independent entities. In other cases, the loyalty programs are specific to particular companies, such as the Optimum rewards program operated by Shoppers Drug Mart.

The accounting issues related to these customer loyalty programs are similar to those for warranties. Traditionally, the usual approach was to estimate the cost of the free goods and services that were expected to be provided in the future, and accrue this as an expense in the period when the sales revenue was recorded. The offsetting credit was to a liability account with a title such as Loyalty Program Obligations. Later, when customers redeemed their points for free goods or services, their cost was debited to this liability account, because the obligation had been satisfied. This process ensured that the cost of providing the rewards was matched against the revenues that were generated when the sales were made. Note that this treatment parallels the way in which warranty obligations (discussed earlier) have traditionally been accounted for.

However, as with warranty obligations, recent standards under IFRS have moved towards measuring loyalty program liabilities as the sales value of the goods or services that will be required to satisfy the reward redemptions, rather than the company's acquisition cost for these goods and services. Thus, if a company estimated that the points awarded in a particular accounting period will be redeemed for goods or services that could have been sold for $4,000, it would record a liability (in the form of unearned revenue) of this amount. If the rewards were later provided at a cost of $3,000, the company would report a profit of $1,000 from the rewards program in the later period's earnings.

Essentially, the new approach to accounting for customer loyalty programs is to treat the original sale as a “bundle” consisting of two parts: the initial goods or services that are provided at that point, plus the additional goods or services that may be provided in the future under the rewards program. In other words, part of the amount that customers pay when they make purchases is deemed to be for the rewards that will be provided later. Accordingly, the selling company should allocate a portion of the sales revenue to the rewards program and treat it as unearned revenue, until the rewards are delivered.

LEARNING OBJECTIVE 6

Describe the nature of non-financial liabilities and provisions.

Warranty Sales2

As a final illustration of a situation involving unearned revenues, consider the case of retailers such as Future Shop who sell warranty coverage (either basic or extended warranties) on the products they sell. When customers purchase these warranties, the company has to record the amount received as unearned revenue and carry this as a liability on its statement of financial position, until either the warranty services are provided or the warranty period ends.

Under IFRS, liabilities arising from unearned revenues such as gift certificates or prepaid cards, customer rewards or loyalty programs, and warranty sales are referred to as non-financial liabilities, because they will normally be settled through the delivery of goods or the performance of services, rather than the payment of cash. The accounts used for these obligations are often labelled provisions, to indicate that they are liabilities for which the amount or timing of the future outflows is uncertain.

LEARNING OBJECTIVE 7

Understand the concept of constructive obligations.

Constructive Obligations

In addition to the traditional types of liabilities arising from laws or contracts, IFRS also recognizes a type called a “constructive” liability. Constructive obligations can arise when a company has, through its past or present practices, indicated to other parties that it will accept specific responsibilities, and the other parties reasonably expect it to do so. For example, a company might have a long-standing practice of paying a bonus of 5 percent of employees' annual salaries at the end of each year. Therefore, even though it may not be required by law or contract to pay the 5 percent bonus, the company has created the expectation that it will continue to provide it. As a result of its consistent past actions, the company has a constructive obligation. Consequently, if the bonus has not been paid it would be accrued as a liability.

IFRS VERSUS ASPE

Under current Canadian accounting standards for private enterprises (ASPE), only liabilities that arise from legal or contractual obligations are recognized. Under IFRS, a broader range of liabilities is recognized, including “constructive obligations” as well as legal and contractual ones. These constructive obligations can arise from an organization's own actions, if they have led other parties to have valid expectations that they rely on.

LEARNING OBJECTIVE 8

Explain why companies use working capital loans and lines of credit.

Current Liabilities Related to Financing Activities

Working Capital Loans and Lines of Credit

Companies need to have sufficient current assets or inflows of cash from operations to pay their debts as they become due. At times the current assets may not be converted into cash quickly enough to meet current debt obligation deadlines. To manage these shortfalls, companies have a few options. For example, they can arrange a working capital loan with a bank. (As discussed earlier in this book, working capital refers to the amount by which a company's current assets exceed its current liabilities.) This type of short-term loan is often guaranteed (secured) by the company's accounts receivable, inventory, or both. As the inventory is sold and money is collected from the accounts receivable, the amounts received are used to pay off the loan.

Loans or other debts are said to be secured whenever specific assets have been pledged to guarantee repayment of the debt. Assets that have been pledged as security for debts are referred to as collateral. If the borrower defaults on a secured debt, the lender has the legal right to have the collateral seized and sold, and the proceeds used to repay the debt. If debts are unsecured, this means that no specific assets have been pledged as collateral to guarantee their repayment; in such cases, the creditors simply rely on the general creditworthiness of the company.

Another way that companies can deal with temporary cash shortages is to arrange a line of credit with a bank. In this case, the bank assesses the company's ability to repay short-term debts and establishes a short-term loan limit that it feels is reasonable. If cheques written by the company exceed its cash balance in the bank, the bank covers the excess by immediately activating the line of credit and establishing a short-term loan. The bank uses subsequent cash deposits by the company to repay the loan. A bank line of credit provides the company with greater flexibility and freedom to take advantage of business opportunities and/or to settle debts.

A company that is using a working capital loan or a line of credit might have a negative cash balance. If so, it must be shown with the current liabilities. For example, at the end of its 2010 fiscal year, Magnotta Winery Corporation had an operating line of credit with a limit of $11,500,000. Of this amount, the company had borrowed $5,249,398 on January 31, 2010, which was down from $5,881,325 a year earlier. These amounts were due on demand, and were reported as bank indebtedness in the current liabilities section of Magnotta's balance sheet. The interest rate applicable to this line of credit was the prime rate—the loan rate that is offered by banks to their best customers—plus 0.875%. (As you may recall from earlier examples, Magnotta Winery has vineyards in Ontario and Chile and produces, imports, exports, and retails beer and spirits, as well as wine and ingredients for making wine).

LEARNING OBJECTIVE 9

Calculate the amount of interest owed on various types of short-term notes payable.

Short-Term Notes and Interest Payable

Short-term notes payable represent company borrowings that require repayment in the next year or operating cycle. They either carry explicit interest or are structured so that the difference between the original amount received and the amount repaid represents implicit interest. In either case, interest expense should be recognized over the life of these loan agreements.

Of course, every note payable that is recorded by one party (the borrower or debtor) is recorded as a note receivable by the other party to the transaction (the lender or creditor). Accordingly, the treatment of notes payable and interest expense in the following discussion parallels the treatment of notes receivable and interest revenue that was discussed in Chapter 6.

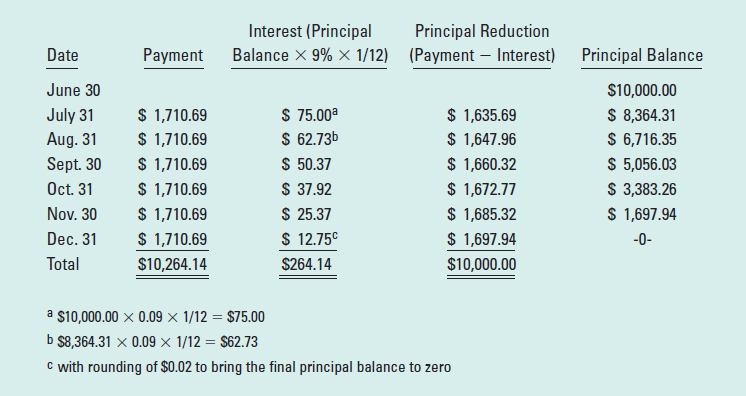

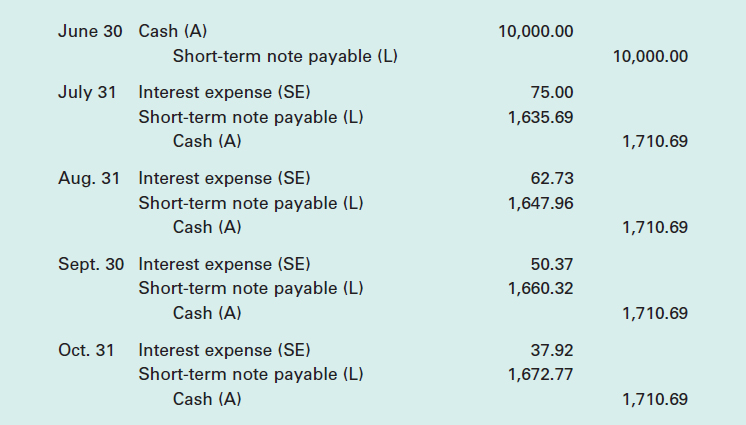

Illustration of a loan with equal monthly payments that include both interest and principal: Assume that a company borrows $10,000 from a bank at 9% on June 30, to be repaid in equal monthly instalments over six months. (This type of loan is called an instalment loan, to indicate that payments are made periodically rather than only at the end of the loan.) The bank determines that the required amount of each monthly payment is $1,710.69. The monthly instalments include reductions of the principal (which is initially $10,000) as well as interest (at the rate of 9% per annum, calculated on the decreasing amount of principal outstanding each month). The following table illustrates how the interest and the reductions of the principal are calculated:

This type of table is called a loan amortization table because it shows how the original amount of the loan is reduced as time passes. The periodic payments on this type of loan are referred to as blended payments, because they contain both interest and principal components. Although the total payment is the same amount each period, the portion of each payment that is consumed by interest is reduced as the principal balance is reduced.

Notice that the total interest on the loan ($264.14) is much less than it would have been if the entire $10,000 debt had been outstanding for six months ($10,000 × 9% × 6/12 = $450). This is because monthly payments were made and large portions of these payments were applied to the principal, which reduced the principal amount owing and made the average loan balance outstanding during the six-month period much less than $10,000.

The journal entries to record this loan and the payments on it are as follows:

As shown in the loan amortization table, the principal balance in the short-term note payable account will gradually be reduced as each monthly payment is made, and should be zero when the final payment is made on December 31.

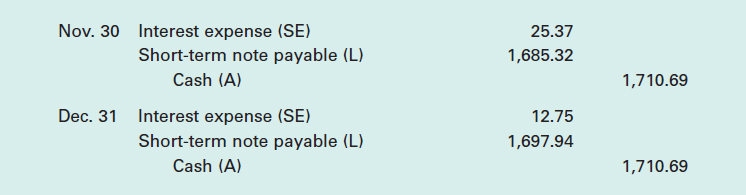

Illustration of a loan with monthly payments of interest only: To illustrate a different type of loan arrangement, we will now consider the case of a company that takes out a six-month loan for $10,000 at 9% on June 30, but with terms that specify that only the interest on the loan is to be paid each month; the principal is to be repaid as a lump sum on December 31.

Note the key difference between this situation and the previous one: in this case, there are no reductions in the principal of the loan during its life. In this type of situation, a loan amortization table is not necessary, because the principal balance remains the same from the start of the loan on June 30 until it is repaid in full on December 31. Consequently, the amount of interest is the same each month, calculated as $10,000 × 9% × 1/12 = $75.

The journal entries to record this loan and the payments on it are as follows:

We chose to use the account title Short-Term Note Payable for this liability. However, alternatives such as Short-Term Bank Loan are also commonly used.

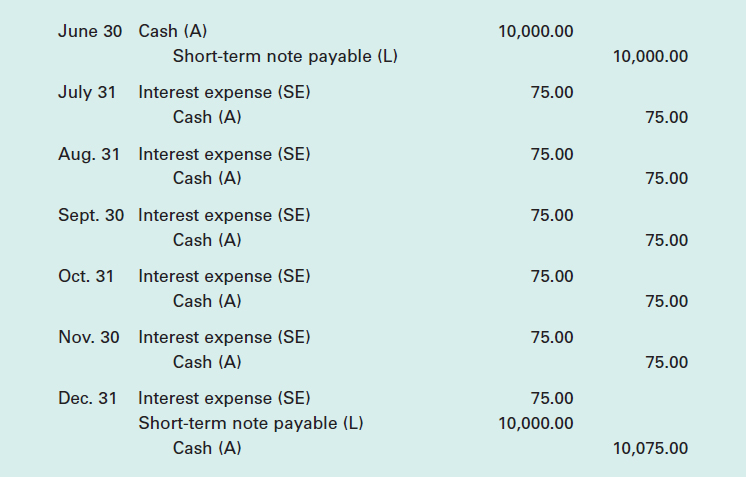

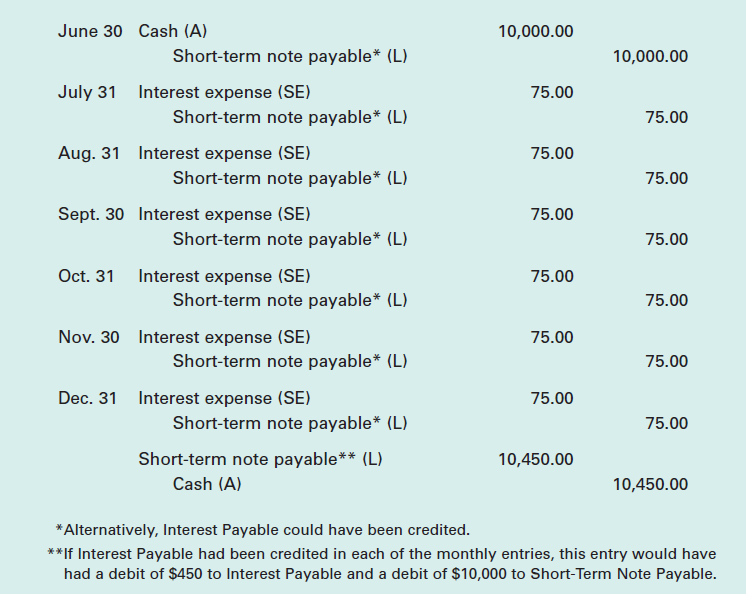

Illustration of a loan with no explicit interest charge: Another type of loan arrangement would be for a company to borrow $10,000 on June 30 and sign a note promising to repay $10,450 on December 31. In this case, even though there is no mention of interest, the extra $450 that has to be paid is clearly an interest charge. Over the six-month period of the loan, this interest should be recognized at the rate of $75 per month ($450 ÷ 6 months). In essence, this situation is almost the same as the previous one. The only real difference is that none of the interest is paid until the note becomes due.

The journal entries to record this loan and its repayment are as follows:

Notice that although the note payable states an amount of $10,450, it is initially recorded at its principal amount (or present value) of $10,000. The $450 of interest only arises as time passes. Over the term of the loan, the carrying value of the liability increases by $75 per month and reaches its maturity value of $10,450 on December 31, when it is repaid.

LEARNING OBJECTIVE 10

Explain why any portion of long-term debt that is due within a year is classified as a current liability.

Current Portion of Long-Term Debt

When long-term debts (which will be discussed in Chapter 10) come within a year of being due, they must be reclassified as current liabilities. This reclassification enables users to estimate the expected outflow of cash during the following year. Therefore, this liability category, generally known as the current portion of long-term debt, is used for all the debt that was originally long-term but is now within one year, or one operating cycle, of being paid off or retired.

In the case of long-term loans, mortgages, or other debt obligations that require monthly or annual payments, the portion that should be reported as a current liability is the amount of principal and any accrued interest from past periods that will be paid within the next year. Remember that interest for future periods is not recorded until it accrues or is paid.

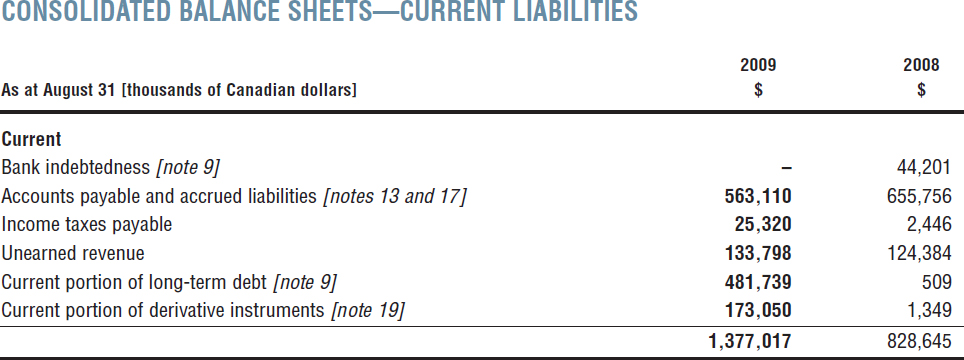

Exhibit 9-2 shows the current liabilities section of the balance sheet for Shaw Communications Inc. as of August 31, 2009. Shaw is a diversified Canadian communications company that provides cable television, high-speed Internet, digital phone, mobile telecommunications, and satellite direct-to-home services to subscribers. Notice that the exhibit includes some of the current liabilities related to financing activities discussed in this section of the chapter—working capital loans and lines of credit, and current portions of long-term debts—as well as accounts payable and accrued liabilities, income taxes payable, and unearned revenue. More details of Shaw's current liabilities are provided in the notes that accompany the statements, and users should refer to these for a complete picture of the company's current obligations.

EXHIBIT 9-2 SHAW COMMUNICATIONS INC. 2009 ANNUAL REPORT

LEARNING OBJECTIVE 11

Calculate the accounts payable turnover rate and average payment period.

STATEMENT ANALYSIS CONSIDERATIONS

Current liabilities are, of course, a key component of both the current ratio (i.e., current assets ÷ current liabilities) and the quick ratio (i.e., [current assets − inventories − prepaid expenses] ÷ current liabilities), which were introduced in Chapter 6.

In addition to the current and quick ratios, we can also calculate various turnover ratios related to current liabilities. The most common of these is the accounts payable turnover rate, which is calculated as follows:

The amount of purchases is not usually reported directly in the financial statements. However, the cost of goods sold can be used as a starting point. Making an adjustment for the change in inventories during the period will convert the cost of goods sold to the cost of goods purchased. As you should recall from Chapter 7, Beginning inventory + Purchases − Ending inventory = Cost of goods sold. Rearranging these terms, the formula to calculate the purchases is as follows:

Purchases = Cost of goods sold − Beginning inventory + Ending inventory

For example, using the financial statements in Appendix A we can calculate H&M's purchases as SEK 40,659 (SEK 38,919 − SEK 8,500 + SEK 10,240). Its accounts payable turnover rate for 2009 can then be calculated as follows:

H&M's accounts payable turnover ratio indicates that its payables were paid off and replaced by new accounts payable 11.1 times during the year. To make this result easier for users to relate to, many analysts convert the accounts payable turnover rate to an average payment period or days to pay ratio. This is done by simply dividing the previous result into 365 days per year. Using H&M's data, this produces the following:

365 days ÷ 11.1 = 32.9 days

This indicates that, on average, H&M took 32.9 days to pay its accounts payable in 2009. To assess whether this is a good or bad result, we should compare this to the payment period allowed by the company's creditors, to the results from previous years, and/or to the results for other companies in the same industry.

LEARNING OBJECTIVE 12

Explain contingencies and how they are accounted for.

CONTINGENCIES

The term contingent liability (also sometimes referred to as contingent loss) refers to a situation in which a liability is conditional; that is, whether there will be a liability depends on some future event. Under IFRS, contingent liabilities are not recorded in the accounts, but they must be disclosed in the notes to the financial statements if they could have a material impact on the company's financial position.

For example, a contingent liability exists when a company has guaranteed another company's debt.3 This often happens when a subsidiary company takes out a loan and the parent company (the company that owns all or most of the subsidiary's shares) guarantees repayment of the loan. For the parent company, the obligation to repay the loan is a contingent liability because it will only arise if the subsidiary company defaults on the loan; if the subsidiary repays the loan according to its terms, the parent will have no liability. Another kind of contingent liability exists when a company is the defendant in a lawsuit; it may or may not incur a liability, depending on the outcome of the case.

Because of the uncertainty in such situations, guidelines have been developed to distinguish contingent liabilities (which are disclosed in the notes but not recorded in the accounts) from estimated liabilities or provisions (which are recorded in the accounts).

Under IFRS, when there is a contingency a liability should be recorded and reported on the statement of financial position (and a loss recognized and reported on the statement of earnings) if the following criteria are met:

- It is probable that some future event will result in the company incurring an obligation that will require the use of assets or the performance of a service.

- The amount of the resulting liability (and loss) can be reasonably estimated.

HELPFUL HINT

If a possible loss/liability is considered probable and can be reasonably estimated, it should be reported as a loss on the statement of earnings and a liability on the statement of financial position. If the contingency does not satisfy these two criteria but could have a material impact on the financial statements, it should be disclosed in a note.

With respect to point 1, notice that the recognition criterion for assessing the uncertainty of a confirming future event is whether the event's occurrence is considered “probable.” This is generally interpreted to mean simply “more likely than not.” Clearly, this will often be a very subjective assessment and considerable judgement will have to be exercised.

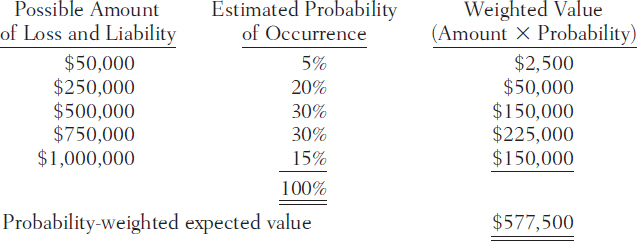

With respect to point 2, notice that if the amount cannot be measured reliably, no liability is recognized. In the past, companies often avoided having to record probable future liabilities on the basis that they could not be reliably estimated. For example, they sometimes argued that the amount of the liability could range anywhere from a few thousand dollars to hundreds of millions of dollars, and that such a wide range of possible outcomes meant that the amount could not be reasonably estimated. However, under IFRS this should be the case only in very rare circumstances, because, when necessary, an “expected value” method is to be used to measure the liability. If a range of possible outcomes is available, this approach assigns weights to each of the possible outcomes according to their associated probabilities.

To illustrate the calculation of the probability-weighted expected value of a liability, consider the following set of estimated possible outcomes and estimated probabilities:

Therefore, in this example, if it is considered probable (more likely than not) that there will be a liability, it would be recorded at its expected value of $577,500.

If either of the two criteria is not met (i.e., if the future event that would confirm the obligation is not considered probable, or if it is not possible to estimate the amount reliably), then the liability is not recorded in the accounts. Rather, it is classified as a contingent liability, which means that the company should provide users with information about it in a note disclosure (unless the potential loss is not significant).

Under Canada's accounting standards for private enterprises (ASPE), the term contingent liabilities is used for the entire spectrum of possible obligations that depend on the occurrence of future events to confirm their existence and/or amount. Some of these are recorded in the accounts, others are only disclosed in the notes, and some are not referred to in the financial statements at all. Under IFRS, the term contingent liabilities is only used for those that are not recorded in the accounts.

In addition to this difference in terminology, there are some differences in the criteria for recognizing and measuring these liabilities under Canadian accounting standards for private enterprises, in comparison to IFRS.

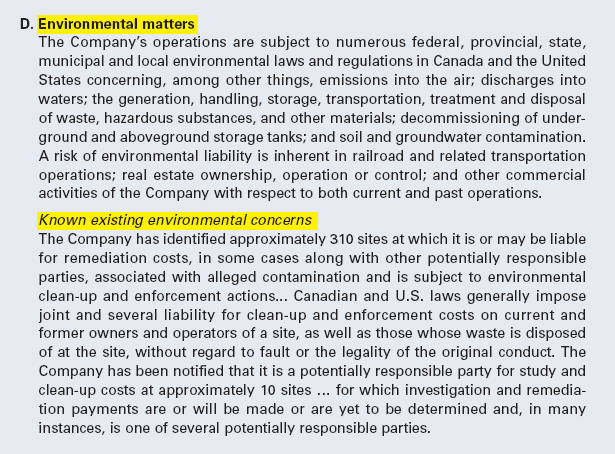

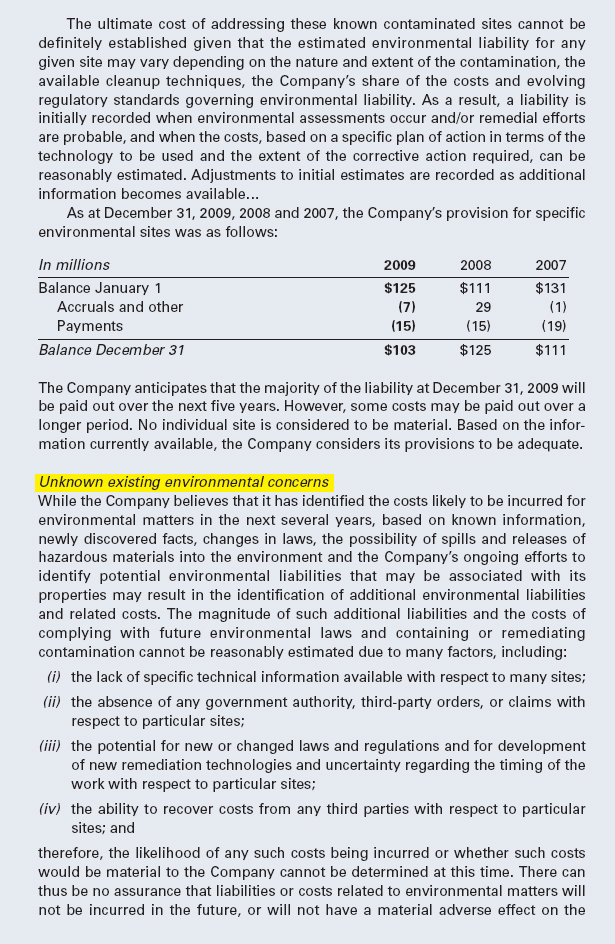

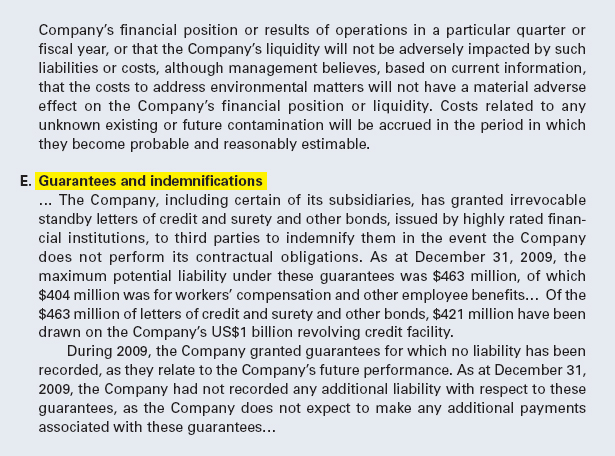

With its headquarters in Montreal and operations in eight Canadian provinces and 16 American states, Canadian National Railway Company has the largest rail network in Canada and the only transcontinental network in North America. The excerpts from Note 17 to CN's 2009 financial statements presented in Exhibit 9-3 provide details of the company's contingencies related to environmental matters, in par D, and guarantees and indemnifications, in part E. Although the exhibit is a long one it includes a discussion of some of the difficulties associated with determining the existence and amount of potential obligations, and provides a good example of how contingent liabilities can be disclosed.

EXHIBIT 9-3 CANADIAN NATIONAL RAILWAY COMPANY 2009 ANNUAL REPORT

Excerpts from Note 17 to Consolidated Financial Statements

As another example of a contingency, the selling of accounts receivable with recourse creates a contingent liability for the selling company4 because it may be required to buy back the receivables under the recourse provision if the customers default on their payments. (Refer to Chapter 6 for further discussion of the sale of accounts receivable.) Exhibit 9-4 illustrates how a company disclosed that it had sold accounts receivable to financial institutions and, as a result, had contingent liabilities in the form of limited recourse obligations for delinquent receivables.

EXHIBIT 9-4 CANADA BREAD COMPANY, LIMITED 2009 ANNUAL REPORT

Note 3 to the Consolidated Financial Statements

INTERNATIONAL PERSPECTIVES

Although, as discussed above, it is considered appropriate in certain circumstances to recognize contingent losses and related contingent liabilities, contingent gains and related contingent assets are not recognized under U.S. GAAP (nor under Canada's Accounting Standards for Private Enterprises). This reflects the principle of conservatism, which suggests that while it may be prudent to anticipate certain losses and liabilities before they are confirmed, gains and assets should not be recognized until they are confirmed. However, International Financial Reporting Standards allow some contingent gains and related contingent assets to be recognized, if it is considered probable that they will be realized.

LEARNING OBJECTIVE 13

Explain what commitments are and how they are handled.

COMMITMENTS

In the course of business, many companies sign agreements committing them to certain future transactions. These are generally described in the notes to the financial statements as commitments.

A common example in many types of businesses is purchase commitments, which are agreements to purchase items in the future for pre-arranged prices. Some purchase commitments are referred to as take-or-pay contracts, which means that the company must pay for a specified quantity at the specified price, whether it actually takes that much from the supplier or not.

As discussed earlier, a purchase commitment is an example of a mutually unexecuted contract and is therefore not recorded as a liability. The company would, however, discuss it in a note to the financial statements if it thought that the commitment could have a material effect on its future operations. Exhibit 9-5 shows an example of this type of disclosure.

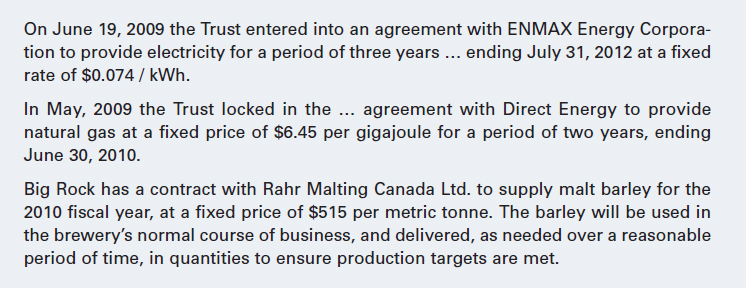

EXHIBIT 9-5 BIG ROCK BREWERY INCOME TRUST 2009 ANNUAL REPORT

Excerpts from Note 13 to the Consolidated Financial Statements

Disclosures regarding purchase commitments such as these are important because they let users know that the company is planning ahead and arranging future contracts at fixed prices for items that it is going to need in its operations. These types of contracts and commitments are often an important part of a company's risk management activities, through which it tries to control the probability and impact of negative events. If prices rise and/or supply shortages occur, the company will benefit from having entered into these commitments in advance. On the other hand, the prices of these items may fall in the marketplace, leaving the company committed to paying prices higher than what would have been paid if no contracts were in place. If this happens, the company will incur losses as a result of having made the purchase commitments. For this reason, any commitments that could have material effects on future operations must be disclosed in the notes to the financial statements.

Also, to enable the users of financial statements to assess risks and estimate future cash flows, companies must disclose any commitments that will require major cash outflows during the next five years. For example, if a company has a long-term loan and a lease contract that commit it to paying significant amounts during the next five years, it must provide schedules of the payments that will be required under these commitments.

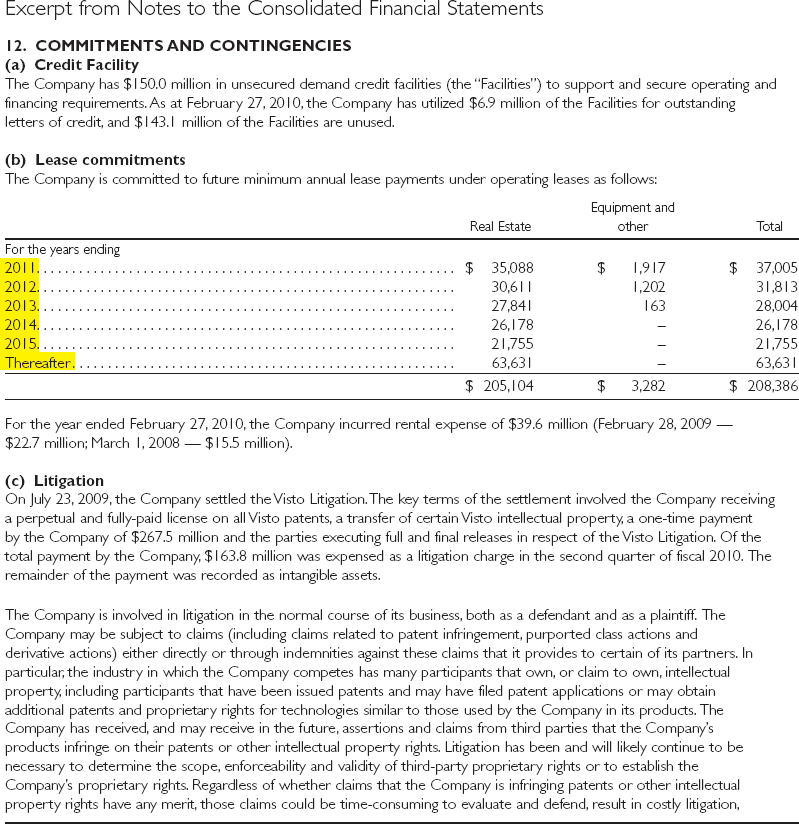

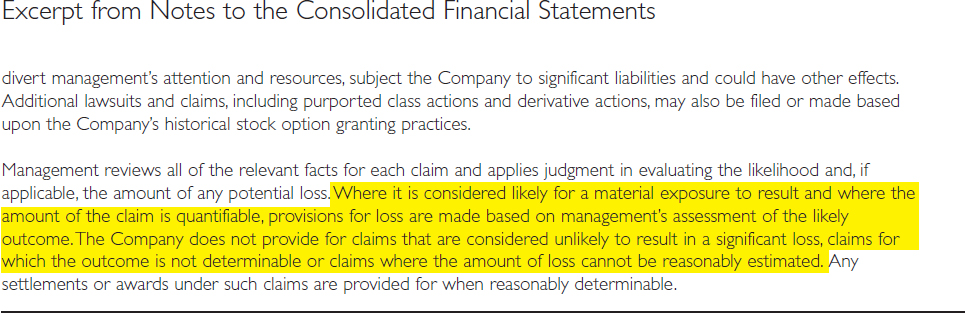

Research in Motion, the Canadian company that manufactures the BlackBerry, has such commitments. Exhibit 9-6 presents Note 12 on commitments and contingencies from RIM's 2010 annual report. Notice that part (b) of this note discloses the amounts that the company is committed to pay in each of the next five years under its lease contracts, while part (c) deals with contingencies and describes how RIM handles the uncertainties surrounding intellectual property disputes and legal actions.

EARNINGS MANAGEMENT

Several of the issues discussed in this chapter—such as estimating the value of future warranty services and customer loyalty rewards, and deciding whether contingencies are probable and the related liabilities should be recorded—require management to make estimates and exercise judgement.

You should by now be realizing the extent to which many issues in accounting are quite subjective or involve “grey areas,” rather than being totally objective or “black and white.” Estimating future bad debts or the expected useful lives of capital assets, deciding whether the value of an asset has been impaired, estimating future costs that will be incurred or the value of future services that will be provided, and deciding whether contingent losses and liabilities are probable and can be reasonably estimated—these all rely on judgement. Management may tend to be biased in exercising such judgement, and the potential impact on the company's earnings and financial position may be significant. Therefore, one of the tasks of auditors is to review the estimates and decisions made by management, to satisfy themselves that the estimates and decisions are fair and reasonable, and that there is no evidence that the financial results are being manipulated.

EXHIBIT 9-6 RESEARCH IN MOTION INC. 2010 ANNUAL REPORT

SUMMARY

This chapter opened with a description of commonly reported current liabilities. It traced the financial statement impact of accounts payable, wages and related payroll liabilities, income taxes, warranty obligations, unearned revenues (including gift certificates and prepaid cards, customer rewards or loyalty programs, and warranty sales), lines of credit, short-term notes, and the current portions of long-term debts. Items significantly affected by International Financial Reporting Standards were highlighted, including the concept of constructive obligations. It also described some items that can affect the decisions made by users, but that may or may not be reflected on the financial statements, such as loss contingencies and commitments.

In Chapter 10, our attention turns to non-current liabilities, particularly long-term notes and bonds payable, mortgages, pension obligations, lease liabilities, and deferred income taxes.

Additional Practice Problems

Answer each of the following questions related to various short-term liabilities.

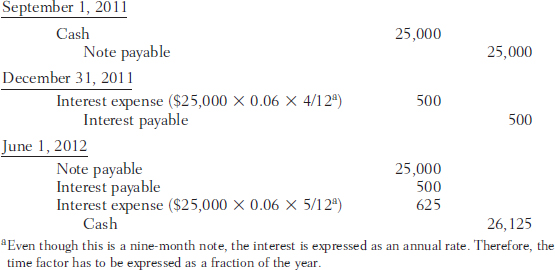

- Valdez Company borrows $25,000 on September 1, 2011, on a nine-month, 6% note. The interest and principal are due at maturity. The company's fiscal year end is December 31. Give the journal entries to record the transaction on September 1, 2011, the adjustment on December 31, 2011, and the payment on June 1, 2012.

- Lilly Limited borrows $5,200 on July 1, 2011, and signs a one-year note payable. No interest was specified, but the note requires that Lilly repay $6,000 on June 30, 2012. What amount should Lilly report as interest expense for the year ended December 31, 2011?

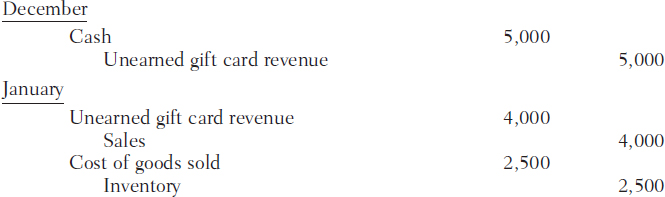

- A clothing store sells $5,000 worth of gift cards in December. In January, cards worth $4,000 are redeemed for merchandise that was purchased by the store in November and carried in its inventory at a cost of $2,500. Make summary journal entries for December and January.

- Minor Manufacturing has a payroll of $7,200 for its employees. Income tax of $1,080 is deducted from the employees, as well as 5% for CPP and 2% for EI. The company's contributions for CPP and EI total $562. Calculate the total payroll expense for the company, the net amount that is payable to the employees, and the total amount that is payable to the government for this payroll.

- Welchor Inc. offers a two-year warranty against failure of its products. The estimated cost of repairs and replacements under the warranty (as a percentage of the initial sales revenue) is 2% in the year of the sale and 4% in the following year. Sales and actual warranty costs for 2010 and 2011 (its first two years of operation) were:

- What amount of warranty expense should be reported on the statement of earnings for the year ended December 31, 2010?

- What amount of warranty obligation should be reported on the December 31, 2010, statement of financial position?

- What amount of warranty obligation should be reported on the December 31, 2011, statement of financial position?

- For each of the following five situations involving a contingency, indicate whether

- the company should recognize it in the accounts, and hence report it as a loss on the statement of earnings and a liability on the statement of financial position;

- the company should not recognize it in the accounts, but should disclose it in a note to the financial statements; or

- the company does not need to do anything with respect to this item at this time:

- The contingency is considered probable; it can be reasonably estimated; it involves a significant amount.

- The contingency is considered probable; it cannot be reasonably estimated; it involves a significant amount.

- The contingency is not considered probable; it can be reasonably estimated; it involves a significant amount.

- The contingency is not considered probable; it can be reasonably estimated; it does not involve a significant amount.

- The contingency is not considered probable; it cannot be reasonably estimated; it does not involve a significant amount.

STRATEGIES FOR SUCCESS:

- If you need guidance with parts “a” or “b,” refer to the examples in the section titled “Short-Term Notes and Interest Payable” (pages 596–599).

- In part “c,” remember that sales revenue is not recorded when gift cards are sold. The amount received for the gift cards is treated as unearned revenue until they are redeemed for merchandise; that is when the real sale occurs.

- If you need help with part “d,” refer to the examples in the section titled “Wages and Other Payroll Liabilities” (pages 586–587).

- In part “e,” you may find that using T accounts is helpful for answering parts “ii” and “iii”.

- If you need guidance with part “f,” refer to the criteria in the section titled “Contingencies” (page 602).

SUGGESTED SOLUTION TO PRACTICE PROBLEM

- The difference between the amount that was received ($5,200) and the amount that is to be repaid ($6,000) represents interest of $800. This covers a one-year period, and half of this occurs during the year ended December 31, 2011. Therefore, half of this amount, $400, should be reported as interest expense in 2011.

-

- The total payroll expense for the company is the gross payroll plus the company's contributions for CPP and EI: $7,200 + $562 = $7,762.

- The employees' net pay is the gross payroll less the payroll deductions withheld from the employees: $7,200 − $1,080 − (0.05 × $7,200) − (0.02 × $7,200) = $7,200 − $1,080 − $360 − $144 = $5,616.

- The total amount to be remitted to the government is the sum of the amounts withheld from the employees and the company's contributions: $1,080 + $360 + $144 + $562 = $2,146.

-

- The expense that should be recognized in 2010 is calculated as follows: (0.02 + 0.04) × $2,300,000 = $138,000. Note that, in accordance with the matching principle, the total expected warranty cost (6% of the sales revenue) should be reported as an expense in the year of the sale.

- The liability that should be reported at the end of 2010 is calculated as follows: $0 beginning balance + $138,000 accrued − $45,000 paid = $93,000 ending balance.

- The liability that should be reported at the end of 2011 is calculated as follows: $93,000 beginning balance + [(0.02 + 0.04) × $2,500,000] accrued − $140,000 paid = $103,000 ending balance.

- Applying the criteria for contingencies that are discussed on page 602 should lead you to the following conclusions:

- The appropriate treatment in these circumstances is alternative (i). Because it satisfies all the criteria, the company should recognize this in the accounts, and report it as a loss on the statement of earnings and a liability on the statement of financial position.

- The company should do everything it reasonably can to estimate the amount (including using the probability-weighted expected value method), so that this can be recognized in the accounts. However, if the amount cannot be reasonably estimated the appropriate treatment is alternative (ii). The company should not recognize it in the accounts, but should disclose it in a note to the financial statements.

- The appropriate treatment in these circumstances is alternative (ii). Because the event is not considered probable, the company should not recognize it in the accounts, but should disclose it in a note to the financial statements.

- The appropriate treatment in these circumstances is alternative (iii). Because the event does not involve a significant amount, the company does not need to do anything at this time.

- The appropriate treatment in these circumstances is alternative (iii). Because the event does not involve a significant amount, the company does not need to do anything at this time.

ABBREVIATIONS USED

| CPP | Canada Pension Plan |

| EI | Employment Insurance |