Measuring Market Risk in the Light of Basel III: New Evidence From Frontier Markets

Abstract

The recent 2008–09 financial crisis has led international financial authorities to review the existing regulations in order to strengthen the risk coverage of the capital framework. These reforms will help to raise capital requirements for the trading book, which represents a major source of losses for international financial institutions, especially during crisis periods. In particular, the Basel Committee on Banking Supervision has introduced a stressed value at risk (SVaR) capital requirement as a new methodology to evaluate market risk. This chapter focuses on frontier markets and aims to compare five different models evaluating market risk, highighting potential issues that banks have to face while calculating the amount of SVaR for their investments. It emerges that frontier markets, showing an interesting risk–return profile and presenting a low correlation level with the European and the US markets, allow international investors to improve their asset allocation while simultaneously containing the cost of capital requirements.

Keywords

1. Introduction

2. Literature Review

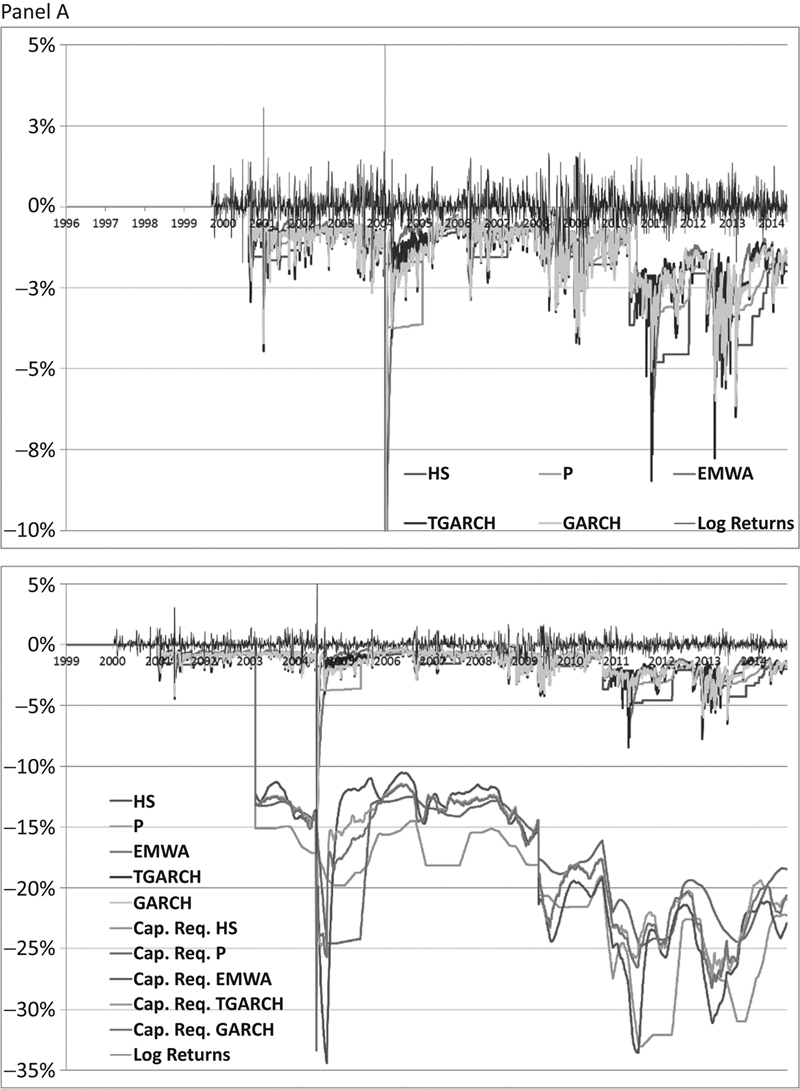

3. Value at Risk and the Capital Requirement for Market Risks

3.1. Defining Value at Risk

(7.1)

(7.1)

3.2. VaR Estimation in the Banking Regulation

(7.5)

(7.5) is the average VaR of the past 60 trading days.

is the average VaR of the past 60 trading days.

(7.6)

(7.6)3.3. The Estimation Models

3.3.1. Historical Simulation Models

3.3.2. Parametric Models

3.3.3. GARCH Models

(7.8)

(7.8)

(7.10)

(7.10)

(7.11)

(7.11)3.3.4. EWMA Models

3.3.5. TGARCH Models

(7.13)

(7.13)3.4. The Opportunity Cost of Regulation

(7.15)

(7.15)

4. The Results of the Empirical Analysis

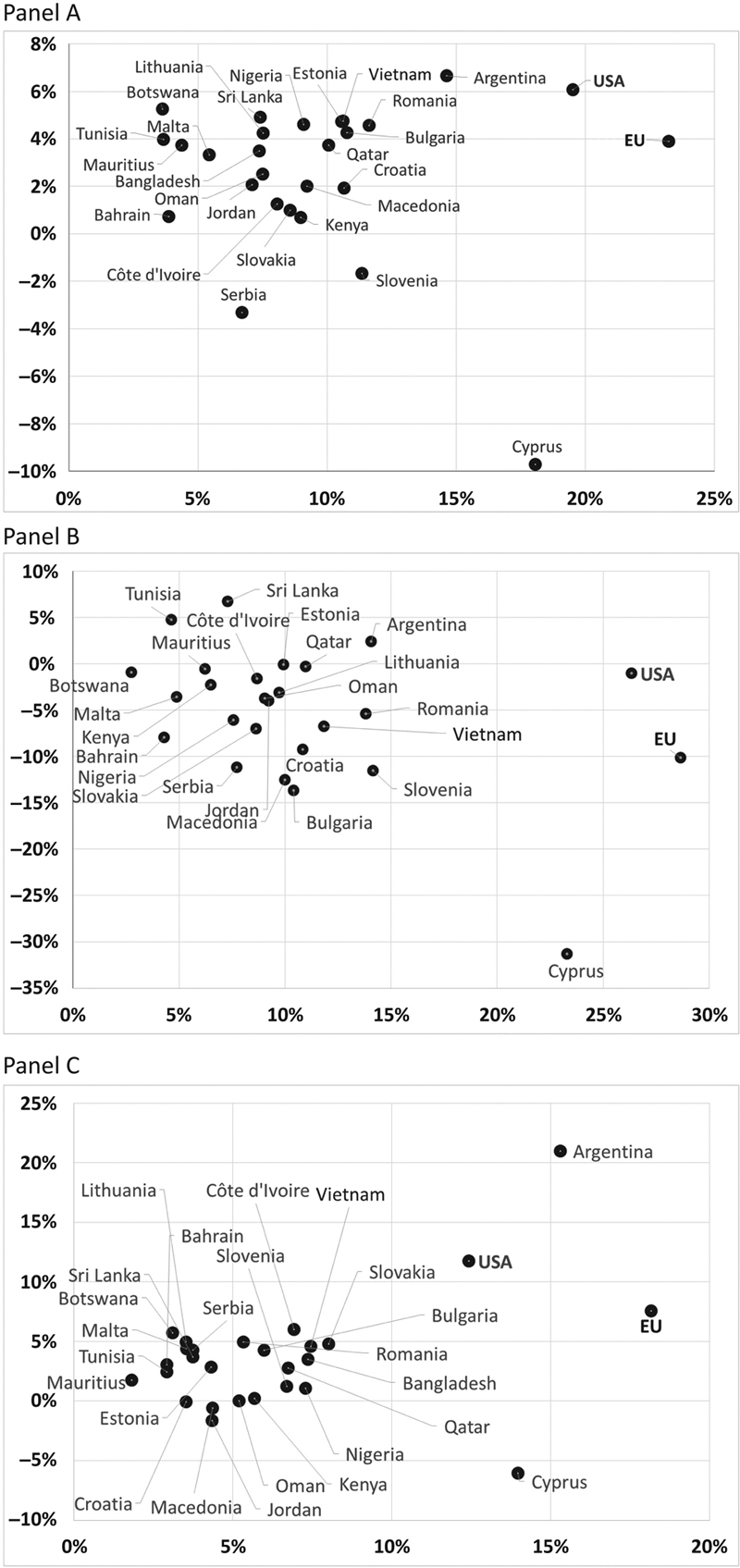

4.1. Investment Opportunity in Frontier Markets

Table 7.1

Emerging Countries Considered in the Analysis Sample, Benchmark Index of the Stock Markets and Starting Date of the Observations

| Country | Index | Start date |

| Argentina | Argentina Merval | 09/07/1995 |

| Bahrain | Bahrain All Share | 01/02/2003 |

| Bangladesh | Bangladesh DSE 30 | 01/28/2013 |

| Botswana | Botswana SE DMS Cos. Idx. | 05/01/2001 |

| Bulgaria | Bulgaria SE SOFIX | 10/20/2000 |

| Côte d’Ivoire | S&P Côte d’Ivoire BMI | 07/30/2008 |

| Croatia | Croatia CROBEX | 01/02/1997 |

| Cyprus | Cyprus General | 09/03/2004 |

| Estonia | OMX Tallinn (OMXT) | 06/03/1996 |

| Jordan | Amman SE Financial Market | 09/07/1995 |

| Kenya | Kenya Nairobi SE (NSE20) | 09/07/1995 |

| Lithuania | OMX Vilnius (OMXV) | 01/03/2000 |

| Macedonia | Macedonian SE MBI 10 | 01/03/2005 |

| Malta | Malta SE MSE | 05/14/1998 |

| Mauritius | Mauritius SE SEMDEX | 09/07/1995 |

| Nigeria | Nigeria All Share | 01/14/2000 |

| Oman | Oman Muscat Securities Mkt. | 10/22/1996 |

| Qatar | Qatar-DS | 01/01/2004 |

| Romania | Romania BET | 09/19/1997 |

| Serbia | Belgrade BELEX Line | 12/25/2006 |

| Slovakia | Slovakia SAX 16 | 09/07/1995 |

| Slovenia | Slovenian Blue Chip (SBI Top) | 03/31/2006 |

| Sri Lanka | Colombo SE All Share | 09/07/1995 |

| Tunisia | Tunisia TUNINDEX | 01/01/1998 |

| Vietnam | Ho Chi Minh SE Vietnam Index | 0728//2000 |

| EU | Euro Stoxx 50 | 09/07/1995 |

| USA | S&P 500 | 09/07/1995 |

Panel A, complete sample; panel B, crisis period 2008–12; panel C, Post-Crisis Era.

Table 7.2

Correlation Matrix of the Returns of Emerging Markets Analyzed

In dark gray high correlation, in white low or negative correlation.

4.2. The Capital Requirement and VaR Models within the Context of Frontier Markets

Panel A, Nigeria; panel B, Argentina; panel C, Qatar; panel D, Romania.

Table 7.3

Average Value of Capital Requirements, Broken Down by Country and by Model Estimation

| Country | HS (%) | p (%) | GARCH (%) | EMWA (%) | TGARCH (%) |

| Argentina | −74.1 | −58.1 | −60.9 | −59.1 | −60.3 |

| Bahrain | −16.2 | −10.1 | −10.4 | −11.3 | — |

| Bangladesh | — | — | — | — | — |

| Botswana | −16.8 | −9.4 | −8.0 | −7.5 | — |

| Bulgaria | 42.5 | −29.9 | −29.3 | −28.6 | — |

| Côte d’Ivoire | — | — | — | — | — |

| Croatia | 44.7 | −30.0 | −30.0 | −31.0 | — |

| Cyprus | −53.3 | −41.3 | −45.1 | 45.9 | 46.0 |

| Estonia | −79.6 | 47.9 | 47.7 | 47.8 | 46.9 |

| Jordan | −22.6 | −17.8 | −18.7 | −18.7 | — |

| Kenya | −20.7 | −15.7 | −15.3 | −15.2 | −14.5 |

| Lithuania | −26.0 | −17.6 | −16.4 | −18.3 | −16.8 |

| Macedonia | 42.4 | −27.6 | −24.5 | −26.6 | −25.5 |

| Malta | −14.7 | −9.7 | −9.9 | −10.6 | −10.3 |

| Mauritius | −14.3 | −10.7 | −10.7 | −10.9 | — |

| Nigeria | −21.0 | −17.9 | −18.2 | −18.8 | −18.0 |

| Oman | −26.2 | −19.2 | −19.9 | −20.7 | −20.1 |

| Qatar | −36.1 | −26.4 | −30.8 | −30.5 | −31.5 |

| Romania | −35.0 | −28.4 | −29.4 | −30.9 | −29.2 |

| Serbia | −27.5 | −19.4 | −18.6 | −21.5 | −18.5 |

| Slovakia | −26.3 | −20.1 | −20.6 | −21.3 | — |

| Slovenia | −36.5 | −27.0 | −26.0 | −27.5 | −26.0 |

| Sri Lanka | −22.0 | −18.2 | −17.9 | −17.0 | −17.2 |

| Tunisia | −11.3 | −9.1 | −8.7 | −9.2 | −8.8 |

| Vietnam | −32.1 | −28.4 | −23.2 | −22.9 | −23.0 |

| EU | −82.6 | −59.6 | −61.4 | −58.8 | −62.3 |

| USA | −61.0 | −53.0 | −54.6 | −56.3 | −52.5 |

4.3. The Effects of Stressed VaR in Capital Requirements for Market Risk in Frontier Markets

Table 7.4

Average Value of Capital Requirements Without the SVaR Provision, Broken Down by Country and by Model Estimation

| Country | HS (%) | p (%) | GARCH (%) | EMWA (%) | TGARCH (%) |

| Argentina | −14.5 | −12.5 | −12.2 | −11.8 | −12.1 |

| Bahrain | −3.0 | −2.2 | −2.2 | −2.1 | — |

| Bangladesh | −4.9 | 4.1 | −3.8 | −3.6 | −3.8 |

| Botswana | −2.7 | −1.9 | −1.7 | −1.7 | — |

| Bulgaria | −7.4 | −5.4 | 4.9 | 4.7 | — |

| Côte d’Ivoire | −5.8 | 4.5 | 4.4 | 4.2 | 4.4 |

| Croatia | −7.4 | −5.6 | −5.2 | −5.2 | — |

| Cyprus | −11.1 | −9.1 | −9.1 | −9.0 | −9.1 |

| Estonia | −11.9 | −8.8 | −8.2 | −7.9 | −8.1 |

| Jordan | −7.0 | −5.7 | −5.4 | −5.4 | — |

| Kenya | −4.5 | 4.1 | −3.7 | −3.5 | −3.8 |

| Lithuania | −5.3 | 4.1 | −3.8 | −3.8 | −3.8 |

| Macedonia | −6.6 | 4.9 | 4.4 | 4.4 | 4.4 |

| Malta | −3.9 | −3.0 | −2.8 | −2.8 | −2.7 |

| Mauritius | −2.9 | −2.2 | −2.1 | −2.1 | — |

| Nigeria | −7.5 | −6.5 | −5.8 | −5.9 | −5.7 |

| Oman | −5.2 | −3.9 | −3.5 | −3.5 | −3.6 |

| Qatar | −6.6 | −5.4 | −5.5 | −5.1 | −5.4 |

| Romania | −8.4 | −6.4 | −6.0 | −5.9 | −6.0 |

| Serbia | −4.8 | −3.6 | −3.4 | −3.4 | −3.2 |

| Slovakia | −7.3 | 4.9 | 4.8 | 4.7 | — |

| Slovenia | −6.3 | −5.8 | −5.4 | −5.1 | −5.4 |

| Sri Lanka | −5.9 | 4.2 | −3.9 | −3.8 | 4.0 |

| Tunisia | −2.5 | −2.1 | −1.9 | −2.0 | −2.0 |

| Vietnam | −6.9 | −5.9 | −5.7 | −5.6 | −5.5 |

| EU | −15.7 | −12.6 | −12.3 | −11.8 | −12.5 |

| USA | −12.7 | −10.7 | −9.9 | −10.0 | −9.4 |

Table 7.5

Average Value of the Cost of Capital Requirements, Broken Down by Country and by Model Estimation

| Country | HS (%) | p (%) | GARCH (%) | EMWA (%) | TGARCH (%) |

| Argentina | −89.0 | −61.7 | −64.9 | −63.5 | −62.8 |

| Bahrain | −16.2 | −10.1 | −10.4 | −11.3 | — |

| Bangladesh | — | — | — | — | — |

| Botswana | −15.4 | −8.2 | −7.7 | −7.5 | — |

| Bulgaria | −41.4 | −28.2 | −28.5 | −30.2 | — |

| Côte d’Ivoire | — | — | — | — | — |

| Croatia | −39.0 | −27.5 | −28.0 | −31.2 | — |

| Cyprus | −53.3 | 41.3 | 45.1 | 45.9 | 46.0 |

| Estonia | −93.7 | −59.5 | −62.5 | −61.6 | −60.4 |

| Jordan | −29.7 | −24.6 | −27.3 | −27.6 | — |

| Kenya | −25.4 | −17.9 | −17.8 | −18.0 | −16.6 |

| Lithuania | −34.0 | −20.7 | −18.9 | −22.9 | −19.6 |

| Macedonia | −42.4 | −27.6 | −24.5 | −26.6 | −25.5 |

| Malta | −14.9 | −9.8 | −9.8 | −10.8 | −10.4 |

| Mauritius | −22.5 | −16.0 | −16.1 | −17.1 | — |

| Nigeria | −24.3 | −19.9 | −21.3 | −22.8 | −21.1 |

| Oman | −31.9 | −22.4 | −23.8 | −27.1 | −25.8 |

| Qatar | −36.1 | −26.4 | −30.8 | −30.5 | −31.5 |

| Romania | −12.8 | −31.7 | −33.3 | −36.2 | −33.2 |

| Serbia | −27.5 | −19.4 | −18.6 | −21.5 | −18.5 |

| Slovakia | −23.4 | −14.7 | −15.7 | −17.1 | — |

| Slovenia | −36.5 | −27.0 | −26.0 | −27.5 | −26.0 |

| Sri Lanka | −21.0 | −14.9 | −16.7 | −17.1 | −15.9 |

| Tunisia | −13.5 | −10.2 | −9.8 | −10.9 | −9.6 |

| Vietnam | −31.3 | −29.2 | −28.0 | −28.8 | −27.9 |

| EU | −97.6 | −61.9 | −64.9 | −63.4 | −62.9 |

| USA | −79.7 | −59.6 | −65.8 | −72.3 | −69.2 |