Chapter 10

Stock Index Return Predictability in Frontier Markets: Is It There?

A. Vivian School of Business and Economics, Loughborough University, Loughborough, United Kingdom

Abstract

This chapter builds upon the extensive prior literature on return predictability by studying 10 frontier market indices. In general there is modest evidence of return predictability in frontier markets. More evidence is found in favor of predictability than would be expected under the null of no predictability. However, there is not widespread evidence in favor of any one predictor across countries; rather, return predictability is clustered in specific countries. In terms of economic value we find that in general, modest economic value can be generated. The difference between our predictability and economic value results are likely due to differences in weighting of observations; for example, in the economic value models the extreme forecasts are winsorized when portfolio weights are determined. The cross-country relationship between market characteristics and predictability/economic value is also examined. Predictability is stronger in countries with more liquid markets and higher GDP per capita.

Keywords

return forecasting

fundamental ratios

frontier markets

market liquidity

economic value

market development

1. Introduction

Return predictability is a fiercely debated topic. The literature finds that in-sample (INS) aggregate return predictability is primarily found in the United Kingdom and United States (Rapach and Wohar, 2009; Engsted and Pedersen, 2010), in developed countries (Hjalmarsson, 2010), and in the largest countries (Rangvid et al., 2014). However, only Rangvid et al. (2014) formally test the link between country characteristics and INS predictability.

This chapter investigates whether aggregate (market index) returns can be forecast out-of-sample (OOS) for 10 frontier markets for which there is very little prior evidence. This sample includes markets of varying size, liquidity, and development. We provide empirical evidence on the link between country characteristics and OOS forecast performance. Many variables have been used to predict stock returns; however, fundamental ratios (such as dividend-price) are amongst the most frequently examined predictors of stock returns in developed markets; the economic foundation of these variables are well known and well established.a Using US data, Goyal and Welch (2008, hereafter GW), test the robustness of OOS predictability compared to a simple historical average benchmark and conclude such models would not have been useful to investors in timing the market. There are relatively few papers that examine return forecasting in an international context. Those that do in general focus on a similar set of large economies that includes the major developed countries,b although notable exceptions include Jordan et al. (2014b, 2015b), who investigate Asian markets and emerging European markets, respectively. Nonetheless there is very little forecasting evidence for frontier markets. The international literature provides mixed evidence on the extent of OOS predictability, if it exists at all, and on whether it cannot generate substantial utility gains for investors.

This chapter studies 10 markets from the MSCI Frontier Emerging Markets Index and provides extensive OOS forecasting tests for countries which have not been previously studied. This includes frontier and emerging markets, countries from several different continents (Africa, Europe, South America, and Asia), and countries with small, medium, and large populations. The focus is on fundamental ratios, and we consider five established variables that were covered in Goyal and Welch’s (2008) US study: dividend:price, dividend yield, earnings:price, book:market and dividend:payout. This chapter provides evidence on two main questions that are summarized next.

First, can any fundamental ratio predictor beat the historical average? We compare performance in terms of both statistical and economic significance. In particular, we provide portfolio allocation evidence as well as INS predictability and OOS forecast accuracy tests for 10 countries. The portfolio allocation evidence is particularly useful because it investigates whether in practice return forecasts can help to improve the asset allocation decision, and because it provides an estimate of the magnitude of possible real-time gains. We investigate the economic value of predictability under mean-variance optimization and under the manipulation proof methodology of Goetzmann et al. (2007, hereafter GISW).

Second, is there a link between country characteristics and the degree of forecastability? We study frontier markets which have decidedly different characteristics. There is substantial variation in the income per head, the extent of financial market development, and also levels of liquidity in the equity markets examined. Is forecast performance dependent upon these characteristics, or is its presence (or absence) unrelated to these factors? We provide empirical evidence on the link between market characteristics and OOS forecast performance.

We find some support for INS and OOS predictability, as well as reporting that OOS economic gains can be made. From a practical perspective, our results suggest that implementing these averaging strategies in frontier markets could help investors to time-vary their portfolio allocations between debt and equity. We find evidence that the economic value of fundamental ratio forecasts is related to economic development in both sets of tests we conduct. There is also some evidence that (1) predictability performance of fundamentals is related to liquidity and market development, and (2) technical variables provide larger economic gains in both larger and more developed markets. Overall, our results suggest that the value of OOS forecasts can differ depending upon a country’s liquidity and development.

2. Data Description

Our sample covers monthly data for 10 frontier markets listed on the MSCI Frontier Emerging Markets Index. The sample comprises a substantial geographical mix: two European countries (Romania and Slovenia), three South American countries (Argentina, Colombia, and Peru), two African countries (Egypt and Morocco), and three Asian countries (Pakistan, the Philippines, and Sri Lanka) over a balanced sample period, Jan. 2000 to Dec. 2014. We chose Jan. 2000 as the start date so that we would have 60 monthly observations before the OOS forecasting period began in 2005, which allowed for about 120 forecasts, providing more than sufficient observations for OOS tests to be appropriately conducted.

The data is monthly and primarily from Thomson Datastream. Returns are based on domestic currency denominated indices, which have been adjusted for dividends and stock splits.c We include five of the fundamental variables used by GW. The appendix provides further detail on each variable and how these variables are constructed, as well as an explanation of abbreviations. We include five fundamental variables from GW:

1. Dividend–price ratio (log), (DP): The difference between the log of dividends paid on the market index and the log of stock prices, where dividends are measured using a 1-year moving sum.

2. Dividend yield (log), (DY): The difference between the log of dividends and the log of 1-month lagged stock prices.

3. Earnings–price ratio (log), (EP): The difference between the log of earnings on the market index and the log of stock prices, where earnings are measured using a 1-year moving sum.

4. Dividend–payout ratio (log), (DE2): The difference between the log of dividends and the log of earnings.

5. Book–market ratio (log), (BM): The difference between the log of book value and the log of market value.

Table 10.1 provides a summary of descriptive statistics for our sample of countries. Panel A provides country characteristics for each of the 10 markets examined (an average for these countries over the 2005–14 OOS period) and information on the United States as a comparator. There is wide variation across countries for almost all of the national-level characteristics we report. In terms of population Slovenia is the smallest country, with just 2 million inhabitants, whereas Pakistan is the largest with 170 million, although most countries are in the 20–50 million range. In terms of GDP per capita Slovenia is the highest at about $19,154, while Pakistan is the lowest at $736.83, with most countries being between $1000 and $4000. Thus the typical frontier country has a population less than one-fifth of that of the United States and an income per head of about one-tenth of that of the United States. In terms of trade openness (trade/GDP), all countries in our sample are above the US level, with half of the countries being more than double the US level. For equity market development and total financial sector development, we see that the United States is greatly more developed than any of the frontier markets. The US equity market-GDP ratio (MKT DEV) is 115%, while five frontier countries have a value below 30%. In terms of total financial sector development [(equity market cap. + private credit)/GDP] the United States dwarfs the other countries with a ratio of 300%, compared to an average of 80% across frontier markets. The United States also dwarfs the frontier markets in terms of equity market liquidity (MOVERS). In the United States 95% of stocks move (have a nonzero return) each day, whereas for the average frontier market only 61% of stock move, so in the United States 5% of stocks have a zero return whereas in frontier markets on average 39% have a zero return! In terms of stock turnover/market capitalization, for the United States the ratio is 223%, while it averages 31% for frontier markets. Internet usage in the United States is also much more prevalent than the other countries, which suggests that individual investors outside the United States might have a harder time collecting relevant information about stocks or making trades rapidly in response to news about stocks they hold. Overall, frontier countries are substantially smaller and poorer than the United States, but they trade more compared to their incomes. Frontier market financial sectors are much smaller compared to GDP than those in the United States, and they are substantially less liquid than the United States.

Table 10.1

Descriptive Statistics—Country Characteristics, Mean, and Standard Deviations of Variables

| Panel A: country characteristics (average 2005–2014) | ||||||||||||

| ARG | COL | PER | EGY | MOR | PAK | PHI | SRL | ROM | SLOV | AV. FRONT | US | |

| POP(m) | 40.03 | 45.78 | 28.99 | 76.83 | 31.41 | 170.06 | 91.99 | 20.28 | 20.53 | 2.03 | 52.79 | 306.32 |

| GDP(pc) | 5763.87 | 3840.27 | 3329.17 | 1434.41 | 2233.37 | 736.83 | 1348.62 | 1534.63 | 5466.50 | 19153.65 | 4484.13 | 44659.58 |

| TRADE OPEN | 33.57 | 36.78 | 51.09 | 55.12 | 78.75 | 33.71 | 76.11 | 61.50 | 77.58 | 131.54 | 63.58 | 28.31 |

| MKTDEV | 17.14 | 51.40 | 60.85 | 57.91 | 69.51 | 26.40 | 62.48 | 25.75 | 17.83 | 26.36 | 41.56 | 115.34 |

| TOTDEV | 29.24 | 92.00 | 85.54 | 96.36 | 132.31 | 49.43 | 93.09 | 55.87 | 56.49 | 105.16 | 79.55 | 307.32 |

| MOVERS | 0.64 | 0.81 | 0.38 | 0.49 | 0.57 | 0.83 | 0.66 | 0.59 | 0.61 | 0.47 | 0.61 | 0.95 |

| TURN | 10.57 | 14.50 | 6.51 | 47.46 | 25.28 | 140.20 | 22.77 | 17.60 | 13.18 | 7.62 | 30.57 | 222.80 |

| INT USE | 37.60 | 31.25 | 30.35 | 27.88 | 37.81 | 8.00 | 17.73 | 10.00 | 35.45 | 61.99 | 29.81 | 73.54 |

| Panel B: mean and standard deviation of variables (Jan. 2000 – Dec. 2014) | ||||||||||

| ARG | COL | PER | EGY | MOR | PAK | PHI | SRL | ROM | SLOV | |

| R | 0.014 | 0.014 | 0.010 | 0.011 | 0.007 | 0.016 | 0.008 | 0.015 | 0.014 | 0.004 |

| 0.094 | 0.056 | 0.055 | 0.080 | 0.046 | 0.085 | 0.057 | 0.070 | 0.107 | 0.052 | |

| DP | −3.838 | −3.408 | −3.267 | −3.167 | −3.291 | −2.895 | −3.936 | −3.400 | −3.415 | −4.291 |

| 1.085 | 0.282 | 0.440 | 0.380 | 0.219 | 0.238 | 0.313 | 0.569 | 0.750 | 0.908 | |

| DY | −3.849 | −3.419 | −3.274 | −3.174 | −3.295 | −2.906 | −3.943 | −3.412 | −3.425 | −4.294 |

| 1.100 | 0.283 | 0.443 | 0.395 | 0.223 | 0.235 | 0.305 | 0.577 | 0.763 | 0.904 | |

| EP | −2.360 | −2.677 | −2.726 | −2.467 | −2.842 | −2.296 | −2.774 | −2.499 | −2.327 | −2.725 |

| 0.480 | 0.459 | 0.867 | 0.460 | 0.224 | 0.269 | 0.220 | 0.481 | 0.621 | 0.342 | |

| DE2 | −1.478 | −0.731 | −0.541 | −0.700 | −0.449 | −0.599 | −1.162 | −0.901 | −1.087 | −1.566 |

| 1.236 | 0.565 | 0.860 | 0.325 | 0.200 | 0.209 | 0.303 | 0.355 | 0.378 | 0.872 | |

| BM | −0.385 | −0.189 | −0.570 | −0.625 | −1.066 | −0.711 | −0.496 | −0.273 | 0.000 | −0.077 |

| 0.345 | 0.545 | 0.484 | 0.406 | 0.314 | 0.301 | 0.303 | 0.600 | 0.000 | 0.358 | |

Notes: Table 10.1 Panel A reports country characteristics for each country sampled, averaged over the 2005–14 OOS period. POP(m) is the population in millions, GDP(pc) is GDP per capita in US dollars, and TRADE OPEN is the ratio of total trade (imports and exports) to aggregate GDP. MKT DEV is equity market development, which is calculated as equity market capitalization to GDP. TOTDEV is total financial sector development, calculated as equity market capitalization plus private credit, all divided by GDP. MOVERS is the proportion of nonzero returns and TURN is the total market volume divided by GDP. INT USE is the percentage of internet users.

Table 10.1 Panel B reports the mean (upper value) and standard deviation (lower value). For example, for nominal return R, Argentina has a monthly return of 0.014 and a standard deviation of 0.094. ARG, Argentina; COL, Colombia; PER, Peru; EGY, Egypt; MOR, Morocco; PAK, Pakistan; PH, Philippines; SRL, Sri Lanka; ROM, Romania; SLOV, Slovenia; DP, log dividend-price ratio; DY, log dividend-yield; EP, log earnings-price ratio; DE2, log payout ratio; BM; book-market ratio.

Each variable in Table 10.1 of Panel B has two entries in each row. The upper value is the mean of each variable and the lower value is the standard deviation. There are several notable points. First, the average nominal returns (R) are typically around 0.01–0.015 (1–1.5% per month or 12–18% per year compounded), the only country substantially outside this is Slovenia, where the return is 0.004 (about 5% per year). The standard deviation (SD) of returns is also typically in a similar band across countries—about 0.06–0.08 (an annualized SDd of about 20.8–27.7%)—although it is as high as 0.107 in Romania (annualized SD of 37.1%) and 0.094 in Argentina (annualized SD of 32.6%). There is substantial variation across countries in terms of the payout ratio and the book:market ratio. The average book–market ratio varies from −0.077 (92.6%) in Slovenia to −1.066 (34.4%) in Morocco; typically the book–market ratio is around −0.3 to −0.6 (74–55%).

3. Empirical Methodologye

3.1. Predictive Regressions and Individual Forecasts

Eq. 10.1 is used to measure INS predictive power. The variable rt + 1 is the nominal continuously compounded log stock returnf from t to t + 1.The variable zt is the predictor variable for t. The following regression is utilized:

Eq. 10.1 is estimated for a 1-month horizon and bootstrapped t-statistics similar to Mark (1995) and Nelson and Kim (1993) are calculated. This simulation approach helps mitigate concerns over the impact of autocorrelation and small-sample bias (Nelson and Kim, 1993; Ang and Bekaert, 2007), as well as concerns over data mining (Rapach and Wohar, 2006).g

Out-of-sample our procedure only uses information available to investors in real time, and hence regression model forecasts are generated using only information available at period t. Time-varying coefficients of each model are estimated using a recursive (expanding window) regression technique given by Eq. 10.2, and then forecasts are produced using Eq. 10.3. We implement an initial window length covering 5 years of monthly data (60 observations). We add one observation for each subsequent time we repeat the parameter estimation. Our initial estimate utilizes 60 observations due to concerns about parameter estimation error. We use an expanding estimation window because parameter estimation error is reduced with sample size (Clark and McCracken, 2009).h Thus the Feb. 2000 to Jan. 2005 period provides the first coefficient estimates, and the first monthly forecast is for the Feb. 2005 return. This regression is followed for each predictor variable.

The historical average, which is calculated over all prior observations, simply expects that next period’s return is equal to the mean of all previous returns:  . This is equivalent to restricting β = 0, and thus the historical average is equivalent to the prediction of a random-walk model with drift and nested within the regression forecasts.

. This is equivalent to restricting β = 0, and thus the historical average is equivalent to the prediction of a random-walk model with drift and nested within the regression forecasts.

3.2. Forecast Evaluation and Application

We follow GW and Campbell and Thompson (2008) in calculating forecast evaluation measures. Campbell and Thompson (2008) propose an OOS R2 to assess the forecasting performance of each model, which is closely related to the well-known Theil’s U.i The OOS R2 measure compares the performance of a specific model relative to a benchmark. The benchmark used in the literature is the historical average return (a random-walk with drift model).

(10.4)

(10.4)Eq. 10.4 computes the ratio of cumulative squared error (CSE) of the regression model (zt) from period 1 to period t as a proportion of the CSE of the historical average (HA) over the same period. The summation is over all forecasts made. Thus, if we make N forecasts, then we sum from n = 1–N in Eq. 10.4, where n = 1 is the first forecast made and n = N is the final forecast made. The OOS R2 is then defined as one minus the ratio of CSEs. Clearly, if the OOS R2 is positive then this indicates the regression model on average beats the HA benchmark over the sample period. This metric also has the useful property that its value represents the proportion by which the benchmark is outperformed or underperformed. For instance, a value of 0.10 indicates the cumulative mean-squared errorj of the regression model is 10% lower than that of the HA prediction and translates to an outperformance of 10% over the sample period considered.

To statistically assess the performance of the models, we report results from the MSE-F test developed by McCracken (2007).k The MSE-F statistic is a one-sided test for equal forecast accuracy. More specifically, it is formulated under the null that the forecast error from the regression model is equal to or larger than (inferior to) that from the HA regression. A rejection of the null hypothesis indicates that the regression model has superior forecast performance over the benchmark.

(10.5)

(10.5)h measures the degree of overlap, where h is equal to 1 for no overlap. Clark and McCracken (2005) have shown that MSE-F statistics have nonstandard statistical distributions. Hence, critical values for MSE-F (as well as INS t-statistics) are produced via a bootstrap procedure following Mark (1995) and implemented in a similar manner to Goyal and Welch (2008) and Rapach and Wohar (2006).

(10.6)

(10.6)Parameters are estimated using the full sample and error terms are saved to generate pseudo series for r and z. The pseudo series for r and z have identical length to our sample and are formed by drawing from the time series of residuals with replacement. We create pseudo series for r and z, dropping the first 100 start-up series and then saving the next 1000 simulated series of r and z. Bootstrapped critical values for each test are created by running the INS and OOS procedures for each set of simulated series.

Our final set of empirical tests deal with the economic value of forecasts. We analyze whether portfolio allocations could have been improved by following the regression model rather than the HA. First, we consider a mean-variance optimizing investor in the spirit of Campbell and Viceira (2002) and Campbell and Thompson (2008). Our analysis is for log returns, while Campbell and Thompson (2008) expound the model for simple excess returns. We take the predictive regression:

where rt + 1 is the log stock return. A mean-variance optimizing investor has the objective function:

(10.8)

(10.8)where O is the objective, rp is the portfolio return, and γ is the coefficient of relative risk aversion.

Such an investor will choose a portfolio weight (ω) of the risky asset under the prediction from the HA and the regression model (Eq. 10.7):l

(10.9)

(10.9)

(10.10)

(10.10)We use 5-years of rolling monthly data to estimate volatilities; however, alternative window lengths for estimating volatility have little impact on the change in utility, since  is common to both ωt, HA and ωt, z. The weight of the HA is determined as in Campbell and Viceira (2002, p. 29),m while the weight in the regression model takes into account the prediction of zt.

is common to both ωt, HA and ωt, z. The weight of the HA is determined as in Campbell and Viceira (2002, p. 29),m while the weight in the regression model takes into account the prediction of zt.

The utility gain (∆O) from using the regression model rather than the HA is shown by Eq. 10.11:

(10.11)

(10.11)Second, we implement the GISW test of abnormal performance:

(10.12)

(10.12)The GISW certainty equivalent measure looks at the average performance of a portfolio relative to the risk-free rate. An advantage of the GISW measure is that it can be difficult to manipulate. The parameter  is set to reflect the overall reward (return) to risk (variance) ratio for each country based upon the actual OOS period data. This reduces the possibility of manipulation and incorrect inference.

is set to reflect the overall reward (return) to risk (variance) ratio for each country based upon the actual OOS period data. This reduces the possibility of manipulation and incorrect inference.

4. In-Sample Return Predictability

In this section we consider 1-month ahead INS return predictability. We explore the robustness of INS aggregate predictability results reported for the United States and many developed countries compared to new frontier markets. Our analysis covers the 2000–14 period, and hence examines a time period different from that of much of the prior literature. In general, statistical evidence of INS predictability is found more frequently than evidence of OOS forecast accuracy in the aggregate stock return literature and in the empirical finance literature more generally. Given these empirical results, many researchers have placed greater emphasis on OOS tests than INS tests. It has also been suggested that INS tests are more susceptible to data mining or dynamic misspecification. In an important and influential article, Inoue and Kilian (2005) provide theoretical analysis that questions these conjectures about the superiority of OOS tests. Nevertheless, INS and OOS tests can complement each other and one test can be viewed as a robustness test for the other.

Table 10.2 provides the magnitude of predictability for each pair of country fundamental ratios. Our INS predictability tests consist of regressions of one-period ahead stock returns on current predictor variables. The coefficient for all fundamental price ratios is expected to be positive, as implied by the Campbell–Shiller present-value model, while for the payout ratio (DE) there is not a clear coefficient sign the ratio should take. Several observations are relevant to the predictability literature. First, there is some evidence of predictability INS; there are 9 out of 49 cases (18.3%) in which significance is reported at the 5% level—hence there is more predictability discovered than one would anticipate under the null (5%). Second, the predictability is somewhat clustered in Pakistan, the Philippines, and to a lesser extent, Argentina, while there is no statistical evidence of predictability in Colombia, Peru, or Romania. Third, the EP is the poorest performing predictor. Fourth, while most coefficients have the correct sign, in a minority of cases they have the wrong sign (11 out of 39), and in two cases this is significant at the 10% level (EGY-DY and MOR-BM). Finally, the explanatory power of the regressions is modest at best. None of the regressions can explain more than 10% of variation in returns, while only 7 out of 49 have an R-squared above 2.5%. Nevertheless, this seems somewhat larger than that reported for European markets by Jordan et al. (2014a).

Table 10.2

In-Sample Predictability of Stock Returns—1 Month Ahead, Feb. 2000 to Dec. 2014

| ARG | COL | PER | EGY | MOR | PAK | PHI | SRL | ROM | SLOV | |

| DP | −0.080 | 0.066 | 0.051 | −0.045 | 0.100 | 0.264 *** | 0.210*** | 0.021 | 0.011 | 0.137* |

| {0.006} | {0.004} | {0.003} | {0.002} | {0.010} | {0.072} | {0.044} | {0.000} | {0.000} | {0.019} | |

| DY | −0.094 | 0.034 | 0.044 | −0.087* | 0.085 | 0.246*** | 0.190** | 0.005 | −0.009 | 0.116 |

| {0.009} | {0.001} | {0.002} | {0.007} | {0.007} | {0.063} | {0.036} | {0.000} | {0.000} | {0.013} | |

| EP | 0.155** | −0.105 | −0.022 | −0.062 | −0.036 | 0.100 | 0.067 | 0.035 | −0.005 | 0.024 |

| {0.024} | {0.011} | {0.001} | {0.004} | {0.001} | {0.010} | {0.005} | {0.001} | {0.000} | {0.001} | |

| DE2 | −0.143** | 0.103 | 0.045 | −0.019 | 0.142* | 0.166** | 0.149** | −0.039 | −0.010 | 0.112 |

| {0.020} | {0.011} | {0.002} | {0.000} | {0.020} | {0.029} | {0.023} | {0.002} | {0.000} | {0.012} | |

| BM | 0.147 | 0.082 | 0.035 | 0.020 | −0.085* | 0.163* | 0.034 | 0.190*** | 0.025 | |

| {0.022} | {0.007} | {0.001} | {0.000} | {0.007} | {0.027} | {0.001} | {0.036} | {0.001} |

Notes: Table 10.2 reports the in-sample predictability of stock returns at the 1-month horizon. Our in-sample predictability tests consist of regressions of one period ahead stock returns on current predictor variables. For each country-fundamental pairing, the top value is the slope coefficient and the adjusted R2 is given in curly brackets. The symbols ***, **, and * denote statistical significance for the slope coefficient at the 1, 5, and 10% levels, respectively, for a two-sided test; critical values are bootstrapped from the empirical distribution.

ARG, Argentina; COL, Colombia; PER, Peru; EGY, Egypt; MOR, Morocco; PAK, Pakistan; PH, Philippines; SRL, Sri Lanka; ROM, Romania; SLOV, Slovenia. DP, log dividend-price ratio; DY, log dividend-yield; EP, log earnings-price ratio; DE2, log payout ratio; BM, book–market ratio.

Lettau and Van Nieuwerburgh (2008) and Paye and Timmermann (2006) note the US dividend–price ratio predictive ability deteriorates during the 1990s; they suggest this could be due to model instability.n Our results verify that dividend-price predictability at the 1-month horizon is not a universal feature across global markets (especially frontier markets) and that evidence of weak dividend:price predictability in recent years is not confined to the United States, consistent with the broader study of Rangvid et al. (2014). Jordan et al. (2014a) extended this analysis to demonstrate that this is not unique to just the dividend-price ratio but also apparent for other fundamental ratios. In frontier markets, overall, the results presented in Table 10.2 suggest that there are cases of 1-month stock-return predictability. However, this evidence is not widespread across countries, in the sense that no one individual variable is found to predict returns for a majority of our sample markets.

5. Out-of-Sample Stock Return Forecasts

Could investors actually utilize regression models based on fundamental ratios in order to benefit from more accurate predictions of future stock returns? This issue is of importance to both practitioners and academics alike. Asset managers and economic policymakers, as well as pension providers and contributors, all need accurate estimates of future market returns.

5.1. OOS Forecast Accuracy

Table 10.3 reports the OOS R2 in percentage points. We use the HA return as our benchmark. Perhaps the clearest finding from Table 10.3 is that the benchmark is only beaten in a small minority of cases; in a large majority of cases (42 out of 49) the OOS R2 is negative, indicating underperformance of the benchmark. In fact for only four of our ten countries do we find a positive R2 for any of the fundamental ratios studied. We also examined statistical outperformance of the benchmark in using the McCracken’s (2007) MSE-F test under the null that the regression forecast is not better than the benchmark (see Section 3.2 for a fuller explanation). The MSE-F test does nonetheless detect statistical outperformance at the 10% level or better in each of the seven cases in which a positive OOS R2 is reported. This is statistically significant at the 1% (5%) level for PAK-DP, PAK-DY and SRL-BM (ARG-DE2, PHI-DE2), which indicates the regression forecast mean-squared error is statistically smaller than the benchmark.

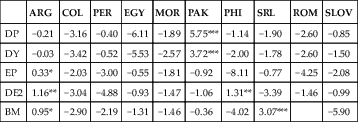

Table 10.3

Out-of-Sample Forecasts of Stock Returns—1 Month Ahead, Feb. 2005 to Dec. 2014

| ARG | COL | PER | EGY | MOR | PAK | PHI | SRL | ROM | SLOV | |

| DP | −0.21 | −3.16 | −0.40 | −6.11 | −1.89 | 5.75*** | −1.14 | −1.90 | −2.60 | −0.85 |

| DY | −0.03 | −3.42 | −0.52 | −5.53 | −2.57 | 3.72*** | −2.00 | −1.78 | −2.60 | −1.50 |

| EP | 0.33* | −2.03 | −3.00 | −0.55 | −1.81 | −0.92 | −8.11 | −0.77 | −4.25 | −2.08 |

| DE2 | 1.16** | −3.04 | −4.88 | −0.93 | −1.47 | −1.06 | 1.31** | −3.39 | −1.46 | −0.99 |

| BM | 0.95* | −2.90 | −2.19 | −1.31 | −1.46 | −0.36 | −4.02 | 3.07*** | −5.90 |

Notes: Table 10.3 reports the OOS R2 in percentage points. The OOS R2 gives the percentage by which the regression model beats the HA benchmark. Note that the link between OOS R2 and Theil’s U is OOS R2 = 1 − U2. Statistical inference is based on the McCracken’s (2007) MSE-F test, which assesses if the forecast error from the regression model is smaller than the forecast error from the HA regression. Critical values are based on a bootstrap procedure under the null hypothesis of equal forecast accuracy. The symbols ***, **, and * denote statistical significance at the 1, 5, and 10% levels, respectively, for a one-sided test.

ARG, Argentina; COL, Colombia; PER, Peru; EGY, Egypt; MOR, Morocco; PAK, Pakistan; PH, Philippines; SRL, Sri Lanka; ROM, Romania; SLOV, Slovenia. DP, log dividend-price ratio; DY, log dividend-yield; EP, log earnings-price ratio; DE2, log payout ratio, BM, book–market ratio.

Overall, we find pockets of forecastability OOS, but in a majority of cases for each fundamental ratio there is little evidence that the null of no OOS predictability can be rejected. These results are broadly consistent with our INS predictability findings. Inoue and Kilian (2005) conclude that if INS and OOS tests give similar conclusions, then it is both tests that provide relevance. Since our INS and OOS results are broadly consistent, both results can be viewed as providing corroborating evidence on the nature of the predictability that exists.

6. Economic Significance of Stock Return Forecasts

This section examines whether regression forecasts could be used in real time to enhance the risk-return trade-off. First, we follow Campbell and Thompson (2008), where portfolios comprise a mix of equity and the risk-free asset under the assumption of a mean-variance optimizing investor with the restriction that the equity weight is between 0 and 1.5 of the total portfolio. We apply a utility gain measure and the manipulation proof measure of performance from GISW. The reported significance levels in Tables 10.4 and 10.5 are bootstrapped to account for finite sample and data mining biases. The utility gain measure has a stronger foundation in economic theory, while GISW is a better measure of market-timing ability.

Table 10.4

Portfolio Allocation Gains to a Mean-Variance Optimizing Investor—1 Month Ahead, Feb. 2005 to Dec. 2014

| ARG | COL | PER | EGY | MOR | PAK | PHI | SRL | ROM | SLOV | |

| DP | 1.26 | 0.92** | −1.33 | −2.30 | 0.08 | 3.52* | 1.66** | −1.56 | −4.49 | 2.14 |

| DY | 1.57 | −1.28 | −1.45 | −0.33 | −0.75 | 0.60 | 0.90* | −1.46 | −4.22 | 0.56 |

| EP | −2.02 | −0.82 | −1.95 | 0.39 | 0.87 | −8.86 | −8.65 | −1.13 | −4.84 | −1.32 |

| DE2 | 4.04** | 0.30* | −7.39 | −1.83 | 2.12 | 5.80** | 2.06** | −1.38 | −3.96 | 2.39** |

| BM | 2.49 | −2.62 | −1.16 | −2.03 | 2.21 | 2.07 | −2.90 | 2.23 | 1.07 |

Notes: Table 10.4 reports the economic significance of regression forecasts. It reports bootstrap significance levels that have been adjusted for data mining. The symbols ***, **, and * denote statistical significance at the 1, 5, and 10% levels, respectively. Utility gains are reported as percentage points and are annualized by multiplying monthly values by 12. Utility gains are calculated for an investor with mean-variance preferences under assumptions of a relative risk aversion coefficient of 3 and a weight limit for the risky asset of no less than 0 and no more than 1.5 (as in Campbell and Thompson, 2008). We forecast the return and use the current market risk-free rate to calculate the excess return. AVall combines forecasts using the average of all individual forecasts. AVall takes the average (unsmoothed) portfolio weight of each portfolio and then applies the weight limits on the risky asset.

ARG, Argentina; COL, Colombia; PER, Peru; EGY, Egypt; MOR, Morocco; PAK, Pakistan; PH, Philippines; SRL, Sri Lanka; ROM, Romania; SLOV, Slovenia; DP, log dividend-price ratio; DY, log dividend-yield; EP, log earnings-price ratio; DE2, log payout ratio; BM, book–market ratio.

Table 10.5

Portfolio Allocation Gains Using GISW Manipulation Proof Measure—1 Month Ahead, Feb. 2005 to Dec. 2014

| ARG | COL | PER | EGY | MOR | PAK | PHI | SRL | ROM | SLOV | |

| DP | 1.25 | 0.91 | 0.91 | 5.23** | −0.14 | 4.12 | 3.07** | −1.21 | 0.13 | 4.13** |

| DY | 1.64 | −1.35 | −1.35 | 6.82** | −0.94 | 1.58 | 2.14* | −0.60 | 0.52 | 2.64* |

| EP | 2.12 | 0.36 | 0.36 | 4.73** | 1.36 | −3.61 | −8.17 | −0.99 | 2.02 | −0.85 |

| DE2 | 4.40* | 1.35* | −6.68 | −1.54 | 3.15* | 7.10** | 3.07** | −1.09 | −3.14 | 2.86* |

| BM | 3.11 | −2.83 | −0.88 | 0.96 | 2.91 | 2.06 | −2.84 | 3.26 | −0.79 |

Notes: Table 10.5 reports the economic significance of regression forecasts. The table reports bootstrap significance levels that have been adjusted for data mining. The symbols ***, **, and * denote statistical significance at the 1, 5, and 10% levels, respectively. We limit the weight in the risky asset to be no less than 0 and no more than 1.5 (as in Campbell and Thompson, 2008). This test utilizes the certainty equivalent measure of Goetzmann et al. (2007). The values reported are in percentage points and are annualized. Gains are measured using a certainty equivalent measure of abnormal performance, which is more robust to manipulation motives of agents.

ARG, Argentina; COL, Colombia; PER, Peru; EGY, Egypt; MOR, Morocco; PAK, Pakistan; PH, Philippines; SRL, Sri Lanka; ROM, Romania; SLOV, Slovenia. DP, log dividend-price ratio; DY, log dividend-yield; EP, log earnings-price ratio; DE2, log payout ratio; BM, book–market ratio.

6.1. Utility Gains

The first method we implement to estimate economic value is the utility gains approach outlined in Section 3.2. We find some evidence that regression forecasts can be utility enhancing. The utility gains are above zero in 9 out of 49 cases at the 10% significance level and the estimated gains appear in general to be fairly modest. Positive significant gains are reported at the 5% level for ARG-DE2, COL-DP, PAK-DE2, PHI-DP, PHI-DE2 and SLOV-DE2. Hence these results are concentrated in the payout ratio and the dividend:price ratio. The magnitude of the gains however is rarely more than 4% p.a. except in Argentina and Pakistan. However, there are more positive signed utility gains in this exercise than the forecast accuracy exercise, with 16 out of 49 having positive gains. Table 10.4 reports the results of the economic significance of regression forecasts when sign and slope restrictions are not applied.

6.2. Manipulation Proof Utility Gains

We also apply the GISW manipulation proof measure of portfolio performance, which is outlined in Section 3.2. The GISW measure is an estimate of the certainty equivalent gain from utilizing the regression forecast rather than the benchmark forecast. It should be noted that the manipulation proof adjustment is made to provide a measure that purely captures an investors’ ability to time the market. However, the manipulation proof measure also implies there are differences across countries in the investor risk parameters.o

Table 10.5 contains the results. The results from the GISW measure provide more evidence that return forecasts can generate economic value. In 31 of 49 cases, the GISW measure is positive. Moreover, there are 7 (13) cases in which results are significant at the 5% (10%) level according to bootstrap simulations. Finally, the point estimates of the magnitude of gains are substantially somewhat higher. There are now estimated gains of 4% p.a. or more (by at least one fundamental ratio) in four of the ten countries analyzed (ARG, EGY, PAK, SLOV) as opposed to just two (ARG and PAK) under the utility gain measure. Overall, the results from the GISW measure are somewhat stronger than the utility gain measure. This probably reflects the fact that the actual capital market line differs from that implied by the risk aversion estimates imposed by the utility gain measure, whereas the GISW model explicitly accounts for this in the Γ discount parameter (which varies across countries).

Our empirical results suggest there is some economic value from forecasting returns with fundamental variables in the subset of the frontier markets we study. This could potentially be exploited by practitioners. There are cases in which regression forecasts would enable investors to tilt their portfolio so that utility could be increased and the risk-return trade-off enhanced. Simply, when the regression model predicts high (low) returns the portfolio is tilted towards equities (T-bills). The economic value results in general are somewhat stronger than the OOS forecast accuracy results, which may reflect the different weighting across the different methods and the fact that extreme forecasts are winsorized under the portfolio allocation method (as noted by Jordan et al., 2015b). Nevertheless, the actual economic value that could be achieved in frontier markets is not as large as reported for some established emerging or developed European countries (Jordan et al. (2014a), or some Asian countries (Jordan et al., 2014b, 2015b).

7. Country Characteristics and Forecast Performance

In this section we provide evidence on whether country characteristics are linked to OOS forecast performance. Prior literature has reported that INS predictability evidence primarily exists in countries with characteristics such as large financial markets or developed markets. However, the link between characteristics and INS predictability is tested by Rangvid et al. (2014) for the dividend–price ratio, while Jordan et al. (2014a, 2015b) examine the correlationp between country characteristics and OOS forecast performance (ie, forecast accuracy and economic value). This section provides further evidence on the link between various OOS forecast performance measures and country characteristics for a range of different fundamental ratios.

The country characteristics examine proxies for development and liquidity. These characteristics could be linked to the degree of market efficiency, since one would anticipate equity prices to adjust slowly in less developed or illiquid markets. Prior empirical literature suggests that INS predictability is connected to market development (Hjalmarsson, 2010) and market size (Rangvid et al., 2011). We use three proxies for development: GDP per capita [GDP(pc)], the ratio of stock market capitalization to total GDP (MKT DEV), and the ratio of total financial development to GDP (TOT DEV). We use two proxies for liquidity: turnover ratio (TURN, which equals total volume to stock market capitalization) and movers (MOVE, which is the proportion of firms which have nonzero daily returns). These proxies are calculated as averages over the OOS period of 2005–14.

Table 10.6 Panel A reports the results for the correlation between country characteristics and INS R2 or OOS R2, respectively. Interestingly, there are some slightly mixed results for the development measures. GDP(pc) is generally positively associated with predictability for both INS and OOS, whereas MKT DEV and TOT DEV are negatively associated with predictability. There is typically a positive relationship between our liquidity measures and forecast performance. This is consistent with the findings of Jordan et al. (2014a) for European markets. The more liquid a market, the better performance one can expect from the traditional fundamental variables.q This may be an important factor in explaining the different results we find in our less liquid sample of countries compared to results reported for highly liquid countries like the United States and United Kingdom.

Table 10.6

Forecast Performance and Country Characteristics

| Panel A: correlation between in-sample and OOS R2 and country characteristics | ||||||||||

| INS R-SQ | OOS R-SQ | |||||||||

| GDP (pc) | MKTDEV | TOTDEV | TURN | MOVE | GDP (pc) | MKTDEV | TOTDEV | TURN | MOVE | |

| DP | 0.31 | −0.05 | −0.12 | 0.80*** | 0.53 | 0.56* | −0.35 | −0.41 | 0.70** | 0.40 |

| DY | 0.32 | −0.06 | −0.17 | 0.82*** | 0.51 | 0.57* | −0.43 | −0.52 | 0.64** | 0.34 |

| EP | 0.36 | −0.33 | −0.57* | 0.25 | 0.52 | 0.40 | −0.35 | −0.27 | 0.19 | 0.01 |

| DE2 | 0.21 | 0.02 | −0.04 | 0.54 | 0.56* | −0.19 | −0.17 | −0.15 | 0.07 | 0.27 |

| BM | 0.67** | −0.68** | −0.74** | 0.38 | 0.45 | 0.51 | −0.37 | −0.64** | 0.13 | 0.17 |

| AVI. | 0.40 | −0.19 | −0.32 | 0.81*** | 0.64** | 0.69** | −0.52 | −0.64** | 0.61* | 0.40 |

| Panel B: correlation between economic gains and country characteristics | ||||||||||

| UG | GISW | |||||||||

| GDP (pc) | MKTDEV | TOTDEV | TURN | MOVE | GDP (pc) | MKTDEV | TOTDEV | TURN | MOVE | |

| DP | 0.01 | −0.01 | 0.03 | 0.52 | 0.46 | −0.20 | 0.08 | 0.14 | 0.40 | 0.00 |

| DY | −0.35 | 0.06 | −0.02 | 0.23 | 0.14 | −0.30 | −0.03 | 0.01 | 0.09 | −0.16 |

| EP | −0.28 | 0.22 | 0.40 | −0.57* | −0.48 | 0.13 | −0.09 | 0.00 | −0.31 | −0.36 |

| DE2 | 0.22 | −0.24 | −0.11 | 0.51 | 0.62* | 0.25 | −0.21 | −0.09 | 0.55* | 0.65** |

| BM | 0.57* | −0.62* | −0.37 | 0.15 | 0.02 | 0.53 | −0.42 | −0.38 | 0.11 | −0.05 |

| AVI. | −0.27 | −0.02 | 0.11 | −0.02 | 0.08 | 0.17 | −0.24 | −0.11 | 0.32 | 0.11 |

Notes: Table 10.6 reports the correlations between measures of forecast performance and country characteristics. Panel A reports results for the correlation between country characteristics and OOS R2 for the unrestricted (restricted) model. Panel B reports results for the correlation between country characteristics and economic value, where we examine the unrestricted (restricted) model GISW measure for the unrestricted (restricted) model. The country characteristics are GDP per capita [GDP(pc)], stock market development (MV/GDP), total financial sector development (MV + PC/GDP), turnover (calculated as Vol/MV), and move (calculated as proportion of stocks that move each day divided by the total number of stocks). Country characteristics are measured over the 2005–14 OOS period. The symbols ***, **, and * denote statistical significance at the 1, 5, and 10% levels, respectively.

DP, log dividend-price ratio; DY, log dividend-yield; EP, log earnings-price ratio; DE2, log payout ratio; BM, book–market ratio. AV1 is the correlation between the country characteristic and the average of each measure (eg, average INS R2 across the five predictors).

Table 10.6 Panel B reports the results for the correlation between country characteristics and utility gain or GISW, respectively. Interestingly the results differ from those reported for the R-squared measures in Panels A and B. The correlations are typically substantially smaller for the economic value measures than for the predictability measures. There is a generally negative relationship between financial sector development and economic value, especially for utility gains. However, the link between economic value measures and liquidity is very weak and typically has the opposite sign to the predictability measures. In general, these results suggest the link between country characteristics and economic value is moderate; thus it is consistent with the view that economic value could be generated in most countries regardless of their characteristics.

To summarize, there is a clearer link between country characteristics and predictability than there is between country characteristics and economic value. Predictability is positively related to liquidity and GDP per capita, but negatively related to financial sector development. These relationships are much weaker when economic value is considered, and for liquidity and financial sector development measures they often switch sign as well. Hence, while the degree of predictability may depend upon country characteristics, this is much less prevalent for economic value. The most plausible reason for the difference is the weighting schemes involved in calculating these different measures; the predictability measures emphasize mean-squared deviations, whereas the economic value measures are generated under a scheme which winsorizes extreme observations.

8. Conclusions

This paper examines the central issue of stock return predictability of aggregate equity indices. This study examines INS predictability but focuses on OOS forecasting of stock returns using a sample of 10 frontier markets with differing characteristics. These countries have very little prior OOS forecasting evidence. We consider if fundamental ratios can forecast stock returns.

The fundamental contributions of this chapter are to provide evidence on the questions (1) Can returns be forecast in less developed countries and less liquid financial markets than those previously studied? Can they generate economic benefits? and (2) Is there a link between country characteristics and the extent of predictability, and/or the economic value, that can be derived from OOS forecasts?

First, the statistical and economic value of predictability varies across countries. Specifically, we find that fundamental ratios provide modest evidence of predictability and that this is concentrated in specific countries, such as Pakistan, the Philippines, and Argentina. The economic value is also generally modest, but positive gains are somewhat more widespread than those from the predictability tests.

Second, we provide some new evidence on the relationship between country-level characteristics and predictability/economic value using correlation tests. We provide evidence that predictability is linked to some country characteristics, such as liquidity and development. We find evidence that fundamental ratios generate large R2s in more liquid markets and in wealthier countries. Finally, we find that the links between economic value and country characteristics are typically weak. Modest economic value can be earned in many countries regardless of country characteristics. The differences between the predictability and economic value test results are likely to be due to the different weightings applied to extreme forecasts in generating these measures. Criteria based on mean-squared error, such as R2, heavily weight extreme forecast errors, in contrast to our economic value measures.

In summary, the statistical and economic value of forecasts from individual predictors tends to vary across frontier countries. There are some instances in which fundamental ratios would have generated substantial benefits to investors. However, the gains to investors in terms of improved forecast accuracy and economic value are generally more modest than has been reported for emerging (or developed) markets in Europe (Jordan et al., 2014a) or Asia (Jordan et al., 2015b), but they could still be of use to an investor. Investors could use fundamental ratios to generate benefits in frontier markets by time-varying portfolio allocations between debt and equity.

Appendix: Data Definitions

Equity and financial market data in this chapter are monthly time series and come from two main sources, both of which are extracted from Datastream: (1) for equity market data, Datastream-compiled stock indices, and (2)for interest rates, data from the International Monetary Fund’s International Financial Statistics publication. The following 10 countries are analyzed: Argentina (ARG), Colombia (COL), Peru (PER), Egypt (EGY), Morocco (MOR), Pakistan (PAK), the Philippines (PH), Sri Lanka (SRL), Romania (ROM), and Slovenia (SLOV).

The Datastream stock market index for each country generally includes up to 50 equities, and the codes for the countries being studied are: TOTMKAR, TOTMKCB, TOTMKPE, TOTMKEY, TOTMKMC, TOTMKPK, TOTMKPH, TOTMKCY, TOTMKTM and TOTMKSJ.

Other notes:

• Stock returns (R) are calculated as the log change in the stock return index (RI). Thus Rt = ln[RIt/RIt − 1].

• Dividend-price ratio. In the empirical analysis we take the log of this ratio. This is the sum of dividends paid over the last 12 months by firms in the stock index divided by the current price of the stock index. Datastream reports this value as a percentage, and so we convert it to a decimal by dividing by 100. Then the natural logarithm is taken.

• Dividend-yield ratio. This is the sum of dividends paid over the last 12 months by firms in the stock index divided by the previous month’s stock index price. It is calculated by taking the Datastream dividend-price ratio (DY), multiplying it by its current price index (PI), and dividing by the previous month’s price index. The natural logarithm of this ratio is then taken.

• Earnings-price ratio. This is derived in a manner similar to the dividend-price ratio. Datastream provides the price-earnings ratio (PE). The current stock index price is divided by the sum of earnings generated by firms in the index over the last 12 months. We take the log of 100 multiplied by the reciprocal to generate the log earnings-price ratio: ln (100/PE). Payout ratio is abbreviated DE and is the log dividend-price ratio minus the log earnings-price ratio.

• Risk-free rate proxy. This is taken from the IMF’s international financial statistics. We use the money market rate if available (I60..) or if this is not available the T-bill rate.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.