Frontier Market Investing: What’s the Value Add?

Abstract

We propose that this chapter will assess the value of frontier markets from an investment perspective. The work we have already completed using a regime switching model in this area will be utilized, showing evidence that the value add of frontier markets is to improve the level of risk-adjusted returns while the extreme correlation of frontier markets in both bear and bull markets also has a positive effect on the overall investment. The growth projections of frontier markets, coupled with the lowering of international regulatory and liquidity constraints, suggest this is an area required for consideration in a client portfolio. We are happy to provide the work that we have already completed in this area as a contribution to the book.

Keywords

1. Introduction

2. Literature Review

2.1. International Markets

2.2. Frontier Markets

In the graph, panel A identifies the behavior of each equity index. The standardized initial value is reported at time 06/07/2002 and reinvested until day 06/17/2015. Panel B instead outlines the annual ln returns for the past 6 years. In the last two columns the means for the past 10 years with the respective 10-year standard deviations are reported. (Bloomberg and recalculations.)

2.3. BRICs’ Lessons for Frontier Market Investing

This graph depicts the level of GDP in the column bar where the darker portion indicates internal consumption, which remains at low levels despite the exponential increase in the real level of GDP. The green line measuring the percentage of internal consumption in GDP highlights a decreasing trend (the level is not available for 2014). The red line shows the decline in annual percentage growth. (World Bank data and recalculation.)

Table 13.1

BRIC Economic Outlook

| GDP growth YoY | Internal consumptiona | Exporta | ||||||

| 2013 (%) | 2014 (%) | 2013 (%) | 2014 (%) | % ∆b | 2013 (%) | 2014 (%) | % ∆b | |

| Brazil | 2.74 |

|

62.06 | 58.95 | 0.9 | 12.02 | 11.52 | −1.1 |

| China | 7.68 |

|

35.98 | — | 7.5b | 23.32 | — | 8.7%b |

| India | 6.90 |

|

59.18 | 59.24 | 7.1 | 25.16 | 23.59 | 0.9 |

| Russia | 1.34 |

|

51.58 | — | 4.7b | 28.61 | — | 4.2b |

Source: World Bank data and recalculations.

The table highlights the structure of the economy, in particular, if GDP is driven by external consumption or internal expenditure. Moreover, it depicts how GDP behaved in the last year, 2014.

a Measured in percentage of total GDP.

b Indicate the annual percent growth; in particular, for China the data concern year 2013.

2.4. Economic Evidence

The graph defines the market capitalization in international dollars. (World Bank data and recalculations.)

2.5. Further Evidence

2.5.1. Technological Development

The charts highlight the number of mobile phone subscriptions per 100 people. In panel A, EU and BRIC are considered as benchmark indexes. The BRIC index is calculated by averaging the specific country values. The bar chart in the background highlights the contribution of each country to the overall value. In this case, Russia carries the highest consumption, followed by Brazil. The two graphs in panel B display the top and bottom five countries. The green points indicate the yearly average percentage change for the past 5 years.

The charts report the number of people with access to the Internet. In panel A, EU and BRIC are considered as benchmark indexes. The BRIC index is calculated by averaging the specific country values. The bar chart in the background reports the contribution of each country to the overall value. In this case, China carries the highest consumption, followed by Russia. The two graphs in panel B display the top and bottom five countries. The green points indicate the yearly average percentage change for the past 5 years. (World Bank data and recalculations.)

2.5.2. Energy Development

The charts report power consumption. In panel A, EU and BRIC are considered as benchmark indexes. The BRIC index is calculated by averaging the specific country values. The bar chart in the background reports the contribution of each country to the overall value. In this case, Russia carries the highest consumption, followed by China. In panel B, the two graphs display the top and bottom five countries. The green points indicate the yearly average percentage change for the past 5 years. (World Bank data and recalculations.)

2.5.3. Health Development

The charts report the number of deaths per 1000 children born. In panel A, EU and BRIC are considered as benchmark indexes. The BRIC index is calculated by averaging the specific country values. The bar chart in the background reports the contribution of each country to the overall value. In this case, India is the strongest contributor, followed by Brazil. Panel B reports the top and bottom five countries. The green points indicate the yearly average percentage change for the past 5 years. (World Bank data and recalculations.)

3. Data and Methodology

Table 13.2

Descriptive Statistics of Raw Data

| Mean (%) | Std. dev. (%) | Minimum (%) | Maximum (%) | Sharpe ratio | |

| MSCI Frontier Markets | 0.158 | 2.252 | −15.22 | 7.15 | 0.0262 |

| MSCI Emerging Markets | 0.217 | 3.376 | −22.51 | 18.67 | 0.0349 |

| MSCI United States | 0.147 | 2.546 | −20.05 | 11.58 | 0.0188 |

| MSCI Europe | 0.153 | 3.274 | −26.54 | 13.94 | 0.0167 |

Source: Matlab.

3.1. Descriptive Statistics

The diagram reports the time-series return. The black lines indicate, respectively, the first and the third percentiles of the series. The bar in the middle represents the median, while the asterisk indicates the mean. The points at the ends of the black lines represent the middle outliers whereas the square points represent the extreme outliers. (Bloomberg and Excel.)

3.2. Normality—Do Markets Behave “Normally”?

Table 13.3

Raw Indexes’ Normality Tests: Jarque–Bera

| p-Value | Resulta | Mean (%) | Std. dev. (%) | Skewness | Kurtosis | |

| MSCI Frontier Markets | 0.0001 | Reject null hypothesis | 0.158 | 2.252 | −1.7371 | 12.8973 |

| MSCI Emerging Markets | 0.0001 | Reject null hypothesis | 0.217 | 3.376 | −1.5084 | 10.8166 |

| MSCI United States | 0.0001 | Reject null hypothesis | 0.147 | 2.546 | −0.9861 | 12.4200 |

| MSCI Europe | 0.0001 | Reject null hypothesis | 0.153 | 3.274 | −1.5084 | 13.4701 |

Source: EViews.

The table summarizes the results for normality, in particular, the Jarque–Bera test’s results and their p-value along with important indicators of skewness and kurtosis.

a Null hypothesis: the data are normally distributed.

The graphs represent the distribution of the weekly returns of the equity under consideration. The histogram in blue represents the frequency distribution of the observed data. The red line instead identifies the normal distribution for the related variable. In the top of the graph, the confidence interval of the normal distribution (in black) is compared with the one of the observed data (in red), the benchmark. (Matlab and Excel.)

3.3. Correlation—Frontier Markets and Diversification

Table 13.4

Equity Indexes Weekly Correlation

| MSCI Frontier Markets | MSCI Emerging Markets | MSCI United States | MSCI Europe | |

| MSCI Frontier Markets | 1.000 | |||

| MSCI Emerging Markets | 0.383 | 1.000 | ||

| MSCI United States | 0.347 | 0.756 | 1.000 | |

| MSCI Europe | 0.397 | 0.844 | 0.846 | 1.000 |

Source: EViews.

The table summarizes the results for the weekly correlations among the MSCI equity indexes. The range of colors highlights the degree of correlation between the time-series.

3.4. The Power of Diversification: Does Correlation Matter?

The graph displays the importance of diversification among global economies. Two portfolios consisting of the same three assets (MSCI Emerging Markets, MSCI Europe, and MSCI United States) are used as a basis. After, in blue, the MSCI Frontier Markets Index was also included in the calculation, while in the green, we included the MSCI Japan Index. (Bloomberg, Matlab, and Excel recalculation.)

3.5. Correlation Extension—True Exposure

(13.1)

(13.1)

The graphs define the bivariate normal distribution between the frontier markets and the emerging markets. Panel A highlights how the time series are correlated with each other. Panel B shows additional visual information on what the “joint probability function” looks like. The axis represents the weekly percentage change calculated as the log return of the prices adjusted to dividends. Second row describes the sample for the correlation in the positive tail. The observations are subjected to the trends θx and θy. (Matlab and Excel regression.)

Table 13.5

Equity Indexes Correlation

| Time series (X) | United States | Emerging markets (EM) | Frontier markets (FM) | ||||||

| Time series (Y) | World | FM | FM | World | US | FM | World | US | EM |

| Unconditional correlation | 0.96 |

0.76 |

0.35 |

0.86 |

0.76 |

0.38 |

0.40 |

0.35 |

0.38 |

| μ– Negative tail correlationa | 0.94 | 0.76 | 0.50 | 0.84 | 0.76 | 0.49 | 0.55 | 0.50 | 0.49 |

| μ+ Positive tail correlationa | 0.92 | 0.70 | 0.07 | 0.77 | 0.70 | 0.17 | 0.06 | 0.07 | 0.17 |

Source: Bloomberg, Matlab, and recalculation.

The table highlights the correlations between the MSCI World Equity Index and the MSCI United States, MSCI Frontier Markets, and MSCI Frontier Markets equity indexes. The arrows visually indicate if correlation is closer to 0 or 1.

a It is measured as the average of the 10 values away from the mean.

The charts depict the extreme correlations between the MSCI World Equity Index and the MSCI United States, MSCI Emerging Markets, and MSCI Frontier Markets equity indexes. The blue line is obtained from the observed data while the red line is obtained from the simulated normalized distribution of the returns. (Bloomberg, Matlab, and recalculation.)

3.6. Frontier Markets and Regime Switching Model

3.6.1. Generalization—Univariate Regime Switching

3.6.2. Hidden Regime Switching—Markov Chain

This diagram represents a randomize scheme for a two-state Markov chain.

(13.4)

(13.4)

(13.5)

(13.5)

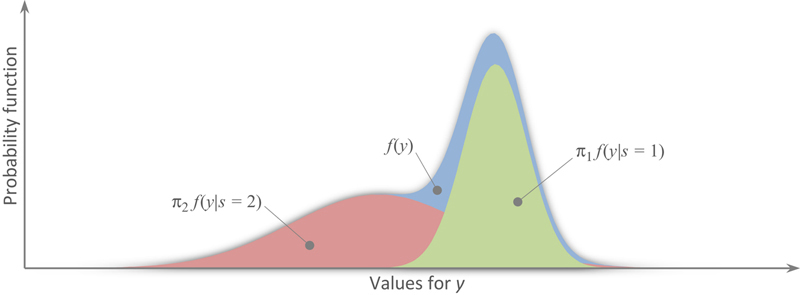

The chart is obtained from a simulated mixed Gaussian distribution with a probability π1,2 equal to 0.5. The blue curve defines the RS distribution with 0.5 probability value for each regime. The red and green curves define the normalized distribution for the two regimes, turbulence (at left) and normal markets. (Matlab and Excel.)

(13.6)

(13.6)

(13.7)

(13.7)3.6.3. Normality—Regime Switching Distribution

The charts represent the distribution of the weekly returns of the equity under consideration. The histogram in blue represents the frequency distribution of the observed data. The red line instead identifies the normal distribution for the related variable. The yellow curve identifies the regime switching distribution with two states and transition probabilities defined by the univariate model. In the top of the graph, the confidence interval of the observed data at the top (in red) is compared with the one of the normal distribution in the middle (in black). In addition, the probability distribution values are given for the regime switching distribution (ie, in frontier markets, the observed values below −3.20% represent 5% of the overall data, whereas the normal distribution indicates 6.8% probability and the regime switching distribution 6.3%). (Matlab and Excel.)

3.6.4. Generalization—Multivariate Regime Switching

(13.9)

(13.9)

(13.10)

(13.10)3.6.5. Additional Evidence of Nonnormality

The charts represent the distribution of the weekly returns of the equity under consideration. The histogram in blue represents the frequency distribution of the observed data. The red line instead identifies the normal distribution for the related variable. The yellow curve identifies the univariate regime switching distribution with two states and transition probabilities defined by the univariate model. The green curve identifies the multivariate regime switching distribution with two states and transition probabilities defined by the multivariate model. In the top of the graph, the confidence interval of the observed data at the top (in red) is compared with the one of the normal distribution in the middle (in black). In addition, the probability distribution values are given for the multivariate regime switching distribution (ie, in frontier markets, the observed values below −3.20% represent the 5% of the overall data, whereas the normal distribution indicates 6.8% probability and the multivariate regime switching distribution 4.9%). (Matlab and Excel.)

3.6.5.1. Correlation—Multivariate Regime Switching

Table 13.6

Multivariate Regime Switching Correlation

| Regime 1—bull markets | ||||

| MSCI Frontier Markets | MSCI Emerging Markets | MSCI United States | MSCI Europe | |

| MSCI Frontier Markets | 1.0000 | |||

| MSCI Emerging Markets | −0.4784 | 1.0000 | ||

| MSCI United States | −0.9170 | 0.6986 | 1.0000 | |

| MSCI Europe | −0.4910 | 0.8755 | 0.7935 | 1.0000 |

| Regime 2—bear markets | ||||

| MSCI Frontier Markets | MSCI Emerging Markets | MSCI United States | MSCI Europe | |

| MSCI Frontier Markets | 1.0000 | |||

| MSCI Emerging Markets | −0.8074 | 1.0000 | ||

| MSCI United States | −0.9799 | 0.7249 | 1.0000 | |

| MSCI Europe | −0.8731 | 0.8184 | 0.9078 | 1.0000 |

Source: Matlab calculations.

This table reports the correlation matrix calculated from the variance–covariance matrix obtained with the multivariate regime switching model. The range of colors highlights the degree of correlation between the time-series.

3.6.5.2. Number of Regimes

4. Frontier Markets—Univariate Regime Switching Application

The charts embody the regime model fitted for each single variable. The red line identifies the natural low return for the equity index, while the gray line represents the probability of switching between the regimes of turbulence and normality, 1 and 0 respectively. The gray areas instead are calculated by setting a 0.5 threshold for the probability calculated before, which more precisely embodies the turbulent periods. The blue line shows the pattern of prices; however, bear in mind that the shape is different among the time series and therefore is not comparable; it is instead included to see if regime switching matches the fluctuation in price.

News reported from the Financial Times:

Global financial markets suffered one of their most turbulent weeks of recent years. Emerging market equities endured their worst losing streak since the 1998 Russian debt crisis. The selling pressure hit its peak on Monday when trading was halted temporarily in India after Mumbai’s benchmark index crashed 10 per cent in a matter of hours.

Table 13.7

Univariate Regime Switching Regressions

| MSCI Frontier Markets | MSCI Emerging Markets | MSCI United States | MSCI Europe | |

| μ1 | 0.23% | 0.26% | 0.32% | 0.32% |

| μ2 | −0.16% | −0.79% | −0.52% | −1.50% |

| σ1 | 1.42% | 2.37% | 1.76% | 2.48% |

| σ2 | 4.55% | 6.83% | 4.87% | 7.24% |

| p11 a | 99.03% | 98.22% | 97.99% | 98.81% |

| p22 a | 96.36% | 92.69% | 93.92% | 93.57% |

| Regime 1 probability | 78.93% | 80.43% | 75.14% | 84.04% |

| Regime 2 probability | 21.07% | 19.57% | 24.86% | 15.16% |

| Regime 1 persistencyb | 102.91 weeks | 56.21 weeks | 49.68 weeks | 84.31 weeks |

| Regime 2 persistencyb | 27.46 weeks | 13.68 weeks | 16.44 weeks | 15.58 weeks |

| H0: μ1 = μ2 c | 0.0000 ✓ |

Reject null |

0.0000 ✓ |

Reject null |

0.0000 ✓ |

Reject null |

0.0000 ✓ |

Reject null |

| H0: σ1 = σ2 d | 0.0000 ✓ |

Reject null |

0.0000 ✓ |

Reject null |

0.0000 ✓ |

Reject null |

0.0000 ✓ |

Reject null |

Source: Matlab and PcGive.

The table summarize the results for the weekly correlations among the MSCI equity indexes. The range of colors highlights the degree of correlation between the time-series.

![]()

where St is explained by an unobservable discrete Markov chain that assumes a two-states regime. The constant μSt is IIN(0,1) among all assets. The results are obtained on a weekly basis from a 7-year period, 06/01/2007 to 05/30/2014 included.

a The probabilities p11 and p22 represent the diagonal of the transition matrix. In particular, p11 identifies the probability of being in Regime 1 at time t + 1 if at the current time we are in Regime 1. The same line of reasoning is employed for p22.

b The persistency indicates the average number of weeks each regime lasts.

c The coefficient indicates the p-value for the relative null hypothesis tested against the alternative hypothesis, H1: μ1 ≠ μ2, and ✓ indicates the rejection of the null hypothesis.

d The portmanteau test is executed with 22 lags, which refers to the corrected version of the Box–Pierce test (1970), also called Q statistics. The test is designated as the goodness-of-fit test. The coefficient indicates the p-value of the test; above 0.05 we reject autocorrelation.

4.1. The Importance of Asset Allocation

4.2. Generalization—Investor Optimization Problem

(13.11)

(13.11)

(13.13)

(13.13)

(13.14)

(13.14)4.3. Portfolio Framework

(13.15)

(13.15)

The graph represents the portfolio distribution for the three-asset case, and the constraint of 15% on the risk-free assets. It is evident how portfolios EF and RS lack redistribution among assets. In fact, one asset, the emerging markets, prevails over the others. In portfolio A there is no inclusion of frontier markets, but they are included in portfolio B. EF stands for efficient frontier methodology; RS stands for regime switching methodology; WA stands for weighted average methodology. (Bloomberg, Matlab, and Excel regression.)

4.4. Results

Table 13.8

Historical 7-Year Portfolios Performances Outlook—Monthly Data Jun. 2007 to Jun. 2014

| Portfolio A | Portfolio B | Benchmarks | ||||||

|

Efficient frontier | Regime switching | Weighted average | Efficient frontier | Regime switching | Weighted average | S&P 500 | MSCI World |

|

|

|

|

|

|

|

|

|

|

| Return | 0.10% | 0.10% | 0.07% | 0.10% | 0.09% | 0.06% | 0.07% | 0.07% |

| Std. dev. | 2.47% | 2.47% | 2.77% | 2.42% | 2.23% | 2.36% | 2.89% | 2.97% |

| Alpha [t-stat] | 0.0003 [5.0429] | 0.0003 [5.0429] | 0.0000 [0.0364] | 0.0003 [3.6915] | 0.0002 [0.8746] | −0.0002 [−0.3093] | — | 0.0001 [0.1266] |

| Beta | 0.8531 | 0.8531 | 0.8744 | 0.8365 | 0.7614 | 0.7269 | 1.0000 | 0.9822 |

| Adj. beta | 0.9021 | 0.9021 | 0.9163 | 0.8910 | 0.8409 | 0.8179 | — | 0.9881 |

| Sharpe ratio | 0.0025 | 0.0025 | −0.0099 | 0.0014 | −00041 | −0.0177 | — | — |

| M2a | 0.10% | 0.10% | 0.10% | 0.10% | 0.10% | 0.10% | — | 0.10% |

| T2a,c | 0.05% | 0.05% | 0.01% | 0.05% | 0.04% | 0.00% | — | 0.01% |

| Information ratioa | 0.0897 | 0.0897 | 0.0054 | 0.0746 | 0.0318 | −0.0061 | — | 0.0021 |

| Client utility | 0.0010 | 0.0010 | 0.0007 | 0.0010 | 0.0009 | 0.0006 | 0.0006 | 0.0007 |

Source: Datastream and recalculations.

The table reports the indexes for the past performances of the complete portfolios, obtained via combination of the optimal portfolio and risk-free assets. The benchmarks are relative to the S&P 500 data and the MSCI World Index. The pie chart represents the distribution of each portfolio. Notice that the blue part representing the risk-free assets is assumed constant at 15%. The red circle in the benchmark section indicates a portfolio fully invested in the relative index.

a The coefficient is tested upon the S&P 500 benchmark, with a weekly average of 0.07% and weekly standard deviation of 2.89%.

b The utility function used in the calculation is: ![]() .

.

c The T2 is calculated on the adjusted beta since it will be more reliable in the long run.

Table 13.9

Actual 1-Year Portfolio Performance—Weekly Data Jun. 2014 to Jun. 2015

| Portfolio A | Portfolio B | Benchmarks | ||||||

|

Efficient frontier | Regime switching | Weighted average | Efficient frontier | Regime switching | Weighted average | S&P 500 | MSCI World |

|

|

|

|

|

|

|

|

|

|

| Return | 0.19% | 0.19% | 0.05% | 0.17% | 0.12% | −0.02% | 0.18% | 0.12% |

| Std. dev. | 1.38% | 1.38% | 1.42% | 1.34% | 1.22% | 1.23% | 1.63% | 1.55% |

| Alpha [t-stat] | 0.0002 [2.4134] | 0.0002 [2.4134] | −0.0010 [−1.1057] | 0.0004 [1.0504] | −0.0004 [−1.5254] | −0.0016 [−1.6443] | — | −0.0005 [−0.8488] |

| Beta | 0.8411 | 0.8411 | 0.7662 | 0.8210 | 0.7307 | 0.6162 | 1.0000 | 0.9130 |

| Adj. beta | 0.8940 | 0.8940 | 0.8441 | 0.8807 | 0.8205 | 0.7442 | — | 0.9420 |

| Sharpe ratio | 0.0689 | 0.0689 | −0.0271 | 0.0611 | 0.0204 | −0.0896 | — | 0.0162 |

| M2a | 0.10% | 0.10% | 0.09% | 010% | 0.10% | 0. 09% | — | 0.09% |

| T2a,c | 0.03% | 0.03% | −0.11% | 0.02% | −0.03% | −0.20% | — | −0.05% |

| Information ratioa | 0.0411 | 0.0411 | −0.1597 | −0.0053 | −0.1151 | −0.2058 | — | −0.0378 |

| Client utilityb | 0.0019 | 0.0019 | 0.0005 | 0.0017 | 0.0012 | −0.0002 | 0.0017 | 0.0012 |

Source: Datastream and recalculations.

The table reports the indexes for the past performances of the complete portfolios, obtained via combination of the optimal portfolio and risk-free assets. The benchmarks are relative to the S&P 500 data and the MSCI World Index. The pie chart represents the distribution of each portfolio. Notice that the blue part representing the risk-free assets is assumed constant at 15%. The red circle in the benchmark section indicates a portfolio fully invested in the relative index.

a The coefficient is tested on the S&P 500 benchmark, with a weekly average of 0.18% and weekly standard deviation of 1.63%.

b The utility function used in the calculation is: ![]() .

.

c The T2 is calculated on the adjusted beta since it will be more reliable in the long run.

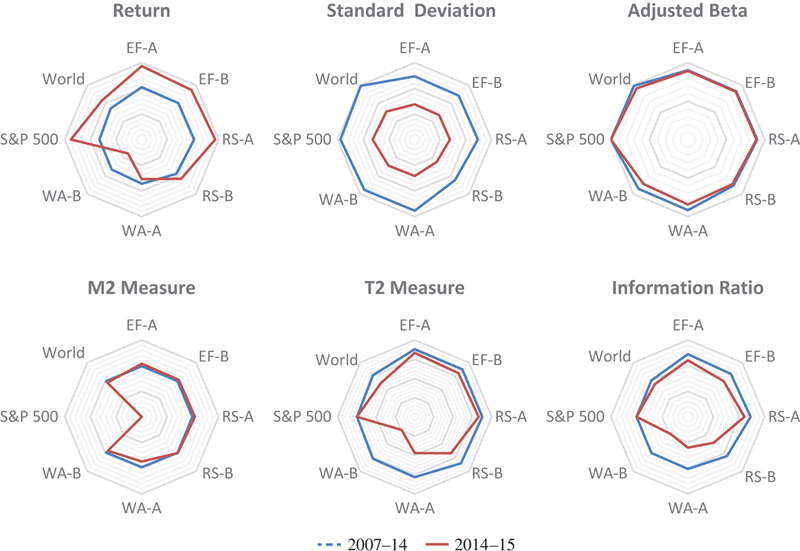

The graphs report the coefficients outlook for the two periods, 2007–14 in blue and 2014–15 in red. The T2 and information ratio are taken from the market benchmark, the S&P 500. In particular, adjusted beta is employed in the T2 measure. (Matlab, Datastream, and recalculations.)

5. Conclusions

Appendix

A.1. Multivariate Regime Switching Model Fit

The graphs represent the regime model fitted for the two single variables. The red line identifies the natural log return for the equity index, while the gray line represents the probability of switching between the regimes of turbulence and normality, 1 and 0 respectively. The gray areas instead are calculated by setting a 0.5 threshold for the probability calculated before; this suggests the turbulence periods more precisely. The yellow area represents the regime switching for the multivariate regime switching method. As a matter of fact, the pattern is the same among all equities. The blue line shows the pattern of prices; however, bear in mind that the scale is different among the time series and therefore not comparable; it is instead included to see if regime switching matches the fluctuation in price. (Matlab and Excel regression.)

A.2. Reliability of Regime Switching Models

The graph represents the RS model fitted for the two single variables. The red line identifies the natural log return for the equity index. The gray areas are calculated by setting a 0.5 threshold for the smooth probability calculated by the RS model and represents the change in regime. The yellow areas identify the coefficient calculated with Eq. A.1.

Due to lack of data availability, the data set is not the same as the one described in Chapter 3. The same weekly frequency in utilized, but a narrower time period is involved (from Sep. 16, 2009, to Jul. 3, 2013). Furthermore, the turbulence coefficient is developed across the 10 industry sectors (energy, telecommunications, health, etc.). To fully explain the frontier markets, 30 companies were chosen from the MSCI Frontier Markets 100 Index in the same proportion to correctly match the behavior of the true index. Furthermore, these companies describe more than 66% of the returns; thus it was decided not to include more variables in the model. (Matlab and Excel regression.)