Financial

reporting

$50

billion

the amount hidden via

loans diguised as sales by

Lehman Brothers in 2008

Financial reports are everywhere: a bill at a restaurant is a financial report, as

are sales receipts and bank statements. In business, however, financial reporting

refers to the financial statements that make up a company’s annual report and

accounts. Compiled by accountants, they provide investors and lenders with

information to assess a company’s profitability, and enable company managers,

government, tax authorities, and other stakeholders to evaluate the business.

Types of financial reports

Financial reports take many forms and can

contain a vast amount of information about a

company’s finances, work, core business values,

performance, employees, and its compliance

with local, logistical, domestic, and international

laws. The most important financial report,

or statement, is usually the annual report—

essentially a collection of many other, smaller

reports—which sums up how the business has

performed in the last year. There is a multitude

of laws, regulations, and guidelines governing

what should be put into this report.

The annual report

Financial statements usually appear in a company’s

annual report and sum up its financial activities in a

standardized way for different audiences to interpret

quickly and clearly. These statements take diverse forms,

and being able to deconstruct them is a vital skill for

accountants and businesspeople, making it simple

to see how well a business is performing and why.

The eight steps of the accounting cycle are

used by nearly all accountants. The cycle

helps by standardizing processes and makes

sure that accounting jobs are

performed correctly and in

the same way and order

for every activity.

See pp.102–103.

THE ACCOUNTING CYCLE

$

$

$

US_100-101_Financial_Reporting_overview.indd 100 21/11/2014 16:23

100 101

HOW FINANCE WORKS

Financial reporting

There are seven widely recognized types of accounting:

Types of accounTing

F

i

n

a

n

c

i

a

l

s

t

a

t

e

m

e

n

t

s

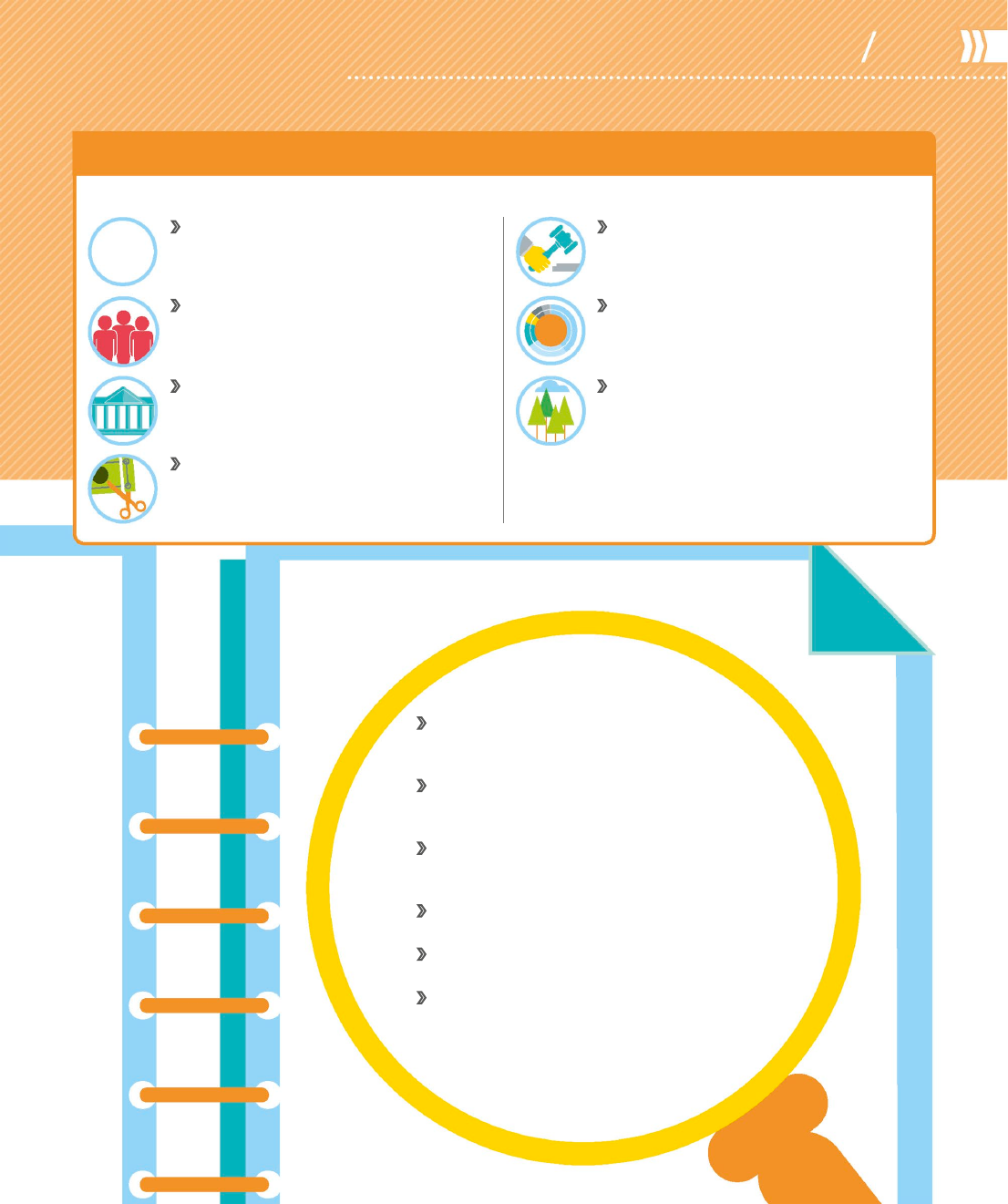

What’s in an annual report? A full record

of company performance according to various

criteria, as well as accounts. See pp.104–105.

What are the statements? The main one is

financial; others include sustainability, directors’

pay, and charitable donations. See pp.106–107.

Who reads which statements? Sections are

relevant to banks, shareholders, government,

auditors, staff, and media. See pp.108–109.

What do the notes mean? Main statements

are annotated in detail. See pp.104–109.

What are the rules? Accounting principles

regulate financial reports. See pp.112–113.

Which are the most important financial

statements? Profit-and-loss statements,

balance sheets, and cash-flow statements

contain key facts. See pp.114–121.

Financial Drawn up by accountants;

used by investors, creditors, and

management. See pp.110–129.

Management Used by managers

to control cash flow and budgets, and

forecast sales. See pp.130–143.

Governmental Also called public

finance accounting; used by public

sector for noncommercial accounting.

Tax Dictates exact rules that companies

and individuals must follow when

preparing and submitting tax returns.

Forensic Engages in disputes and

litigation, and in criminal investigations

of fraud. See pp.152–153.

Project Deals with a particular project;

a useful aid for project management.

Social and environmental Shows how

a company makes a positive difference

to the community and environment.

$

$

$

US_100-101_Financial_Reporting_overview.indd 101 15/12/2014 12:56

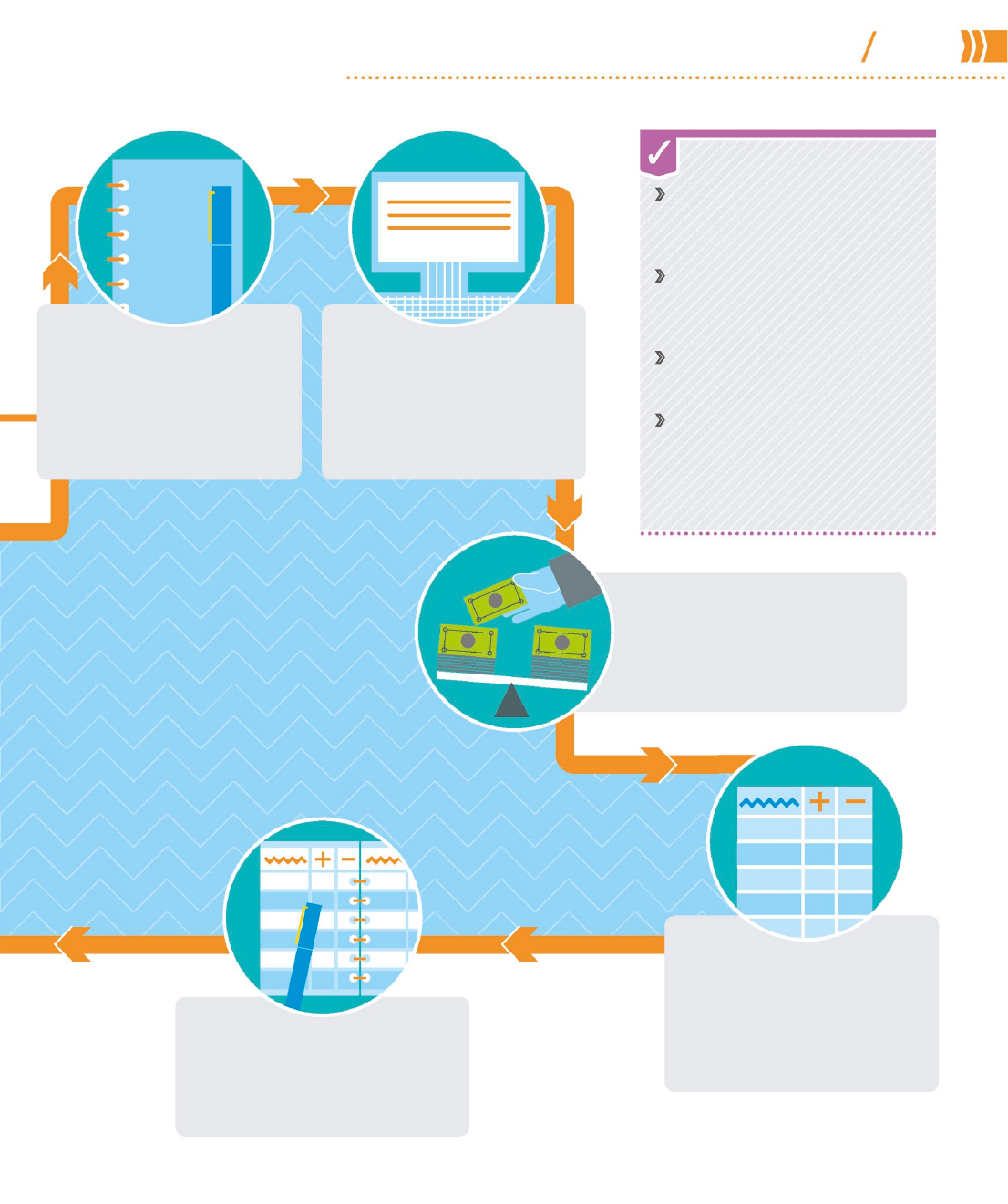

How it works

The cycle works as an aid to organize workflow into a

cyclical chain of steps that are designed to reflect the

way assets, money, and debts have moved in and out

of a business. It progresses through eight different

steps, in the same order each time, and restarts as

soon as it has finished. The cycle can be based on

any length of time—this is known as an accounting

period—and usually lasts a month, a quarter, or a year.

Accounts which deal with revenues and expenses

return to zero at the end of each financial year, while

accounts showing assets, liabilities, and capital carry

over from year to year.

The accounting cycle

The eight-step cycle

The processes shown here are

repeated in the same way for every

accounting period. All businesses

go through different phases, and the

accounting cycle works by reflecting

that. The financial statement, which

is prepared toward the end of each

cycle, is helpful in showing how

strongly the business has performed

during each period of time.

The accounting cycle is a step-by-step process bookkeepers use to

record, organize, and classify a company’s financial transactions.

It helps to keep all accounting uniform and eliminate mistakes.

Internal controls A method

of deploying, measuring, and

monitoring a business’s resources.

This helps prevent fraud and keep

track of the value of assets.

Double-entry bookkeeping

The process of recording all

transactions twice—as a debit

and as a credit. If a company buys

a chair for $100, its debit account

increases by $100 and its credit

account decreases by $100.

Bad debts Debts that cannot be

or are unlikely to be recovered, so

are useless to the creditor (lender),

who writes them off as an expense.

Financial statements

The corrected balances are then

used to prepare the company’s

financial statements.

Closing the books

A closing entry based on adjusted

journal entries is taken, the books

are closed, and the cycle restarts.

Transactions

Any type of financial transaction,

from buying or selling an asset to

paying off a debt, can start the

accounting cycle.

BOOKKEEPING AND

ACCOUNTING

new cycle

6,000

15,000

21,000

US_102-103_The_Accounting_Cycle.indd 102 21/11/2014 16:23

102 103

HOW FINANCE WORKS

Financial reporting

13%

more accountants

will be required

in the US by 2022

Debits An entry where assets and

expenses increase. In double-entry

accounting, debits appear on the

left-hand side of the account

Credits An entry where revenue,

owners’ equity, and liabilities increase.

In double-entry accounting, credits

appear on the right-hand side

Chart of accounts List giving

the names of all of a company’s

accounts, used to organize records

Audit trail Full history of a

transaction, allowing auditors to

trace it from its source, through

the general ledger, and note any

adjustments made

NEED TO KNOW

Journal entries

Accountants then analyze the

transaction and note it in the

relevant journal—a book or an

electronic record.

Posting

Journal entries are then

transferred to thegeneral

ledger—a large book or

electronic record logging

all the company’s accounts.

Worksheet

Often, trial balance calculations

don’t accurately balance the

books (see pp.116–117). In such

cases, changes are made on

a worksheet.

Adjusting journal entries

Once the accounts are balanced, any

adjustments are noted in journals at

the end of the accounting period.

Trial balance

A list of all the company’s accounts

is prepared at the end of the

accounting period, usually a year,

quarter, or month.

10,000

21,000

23055

$

$

$

US_102-103_The_Accounting_Cycle.indd 103 09/11/2016 11:01

102 103

HOW FINANCE WORKS

Financial reporting

13%

more accountants

will be required

in the US by 2022

Debits An entry where assets and

expenses increase. In double-entry

accounting, debits appear on the

left-hand side of the account

Credits An entry where revenue,

owners’ equity, and liabilities increase.

In double-entry accounting, credits

appear on the right-hand side

Chart of accounts List giving

the names of all of a company’s

accounts, used to organize records

Audit trail Full history of a

transaction, allowing auditors to

trace it from its source, through

the general ledger, and note any

adjustments made

NEED TO KNOW

Journal entries

Accountants then analyze the

transaction and note it in the

relevant journal—a book or an

electronic record.

Posting

Journal entries are then

transferred to thegeneral

ledger—a large book or

electronic record logging

all the company’s accounts.

Worksheet

Often, trial balance calculations

don’t accurately balance the

books (see pp.116–117). In such

cases, changes are made on

a worksheet.

Adjusting journal entries

Once the accounts are balanced, any

adjustments are noted in journals at

the end of the accounting period.

Trial balance

A list of all the company’s accounts

is prepared at the end of the

accounting period, usually a year,

quarter, or month.

10,000

21,000

23055

$

$

$

US_102-103_The_Accounting_Cycle.indd 103 09/11/2016 11:01

How it works

Financial statements summarize a company’s

commercial activities clearly and succinctly, with

details of the business’s performance and changes to

its financial position. They are aimed at several parties,

so they need to be detailed but also comprehensible

to the general public. The statements are usually

presented together in the form of an annual report,

with in-depth accounts and footnotes to give detail.

Legal requirements vary, but accounts must be exact.

Financial statements

The formal records of a business’s financial activities are presented as

financial statements. Most jurisdictions require accurate information

by law, and financial directors and auditors are liable for its contents.

What’s in an annual report

The contents page shows where to find the big three statements—the balance sheet, cash-flow

statement, and profit-and-loss statement—and softer information such as stories about staff and

opinions of other stakeholders. The annual report provides an opportunity to impress shareholders

and lenders as well as fulfill legal reporting obligations. It will contain all, or most, of the following.

It is common for the chairman

to write an introduction

focusing on the positives and

explaining any negative parts

of an annual report for the

benefit of shareholders.

C

h

a

i

r

’

s

i

n

t

r

o

d

u

c

t

i

o

n

This section underlines a

company’s social ethos, in

particular its community

involvement. Different types

of companies may focus on

different values.

O

u

r

c

u

s

t

o

m

e

r

s

a

n

d

c

o

m

m

u

n

i

t

y

A brief overview summarizes

the key areas of finance

for the company, including

overall performance,

turnover, operating

costs, capital investment,

depreciation, interest charges,

taxation, and dividends.

(See also pp.114–121.)

O

u

r

fi

n

a

n

c

e

s

These pages contain much of

the company’s information on

its environmental protocols,

most of which are industry-

specific. See also pp.122–123.

O

u

r

e

n

v

i

r

o

n

m

e

n

t

A section on employees

details areas such as staff

development and training,

health and safety, and key

statistics on staff satisfaction.

O

u

r

e

m

p

l

o

y

e

e

s

The infrastructure pages of

an annual report are a good

place to supply more detail

about the company’s fixed

assets and explain why the

company is an attractive

investment for investors

O

u

r

i

n

f

r

a

s

t

r

u

c

t

u

r

e

$

US_104-109_Financial_Statements.indd 104 21/11/2014 17:27

104 105

How finance works

Financial reporting

Performance indicators are

common across all industries.

They measure areas such as

customer satisfaction and the

quality of goods or services

provided by the company.

O

u

r

p

e

r

f

o

r

m

a

n

c

e

i

n

d

i

c

a

t

o

r

s

The environmental

accounting section contains

figures that pertain to the

environment, often those

stipulated by law—for

example, greenhouse

gas emissions.

E

n

v

i

r

o

n

m

e

n

t

a

l

a

c

c

o

u

n

t

i

n

g

The board of directors,

governance report, and

statement of directors’

responsibilities sections

indicate who is leading the

company, showcases their

credentials and roles, and

reveals their pay.

B

o

a

r

d

o

f

d

i

r

e

c

t

o

r

s

In the directors’ report,

members of the board

of directors give their

professional opinions

on how the business

has performed over

the last year.

D

i

r

e

c

t

o

r

s

’

r

e

p

o

r

t

Auditors are independent

and check the accuracy of

companies’ accounts. This

helps to eliminate mistakes

and track fraud.

I

n

d

e

p

e

n

d

e

n

t

a

u

d

i

t

o

r

’

s

r

e

p

o

r

t

Notes to the accounts

are a key part of financial

statements. They provide

extra detail, insight, and

explanation of the bare-

bones figures supplied in

earlier pages of the report.

N

o

t

e

s

t

o

t

h

e

a

c

c

o

u

n

t

s

CO

2

In an era of globalization, large corporations are now commonly made up of

multiple companies. Companies owned by a parent company are known as

subsidiaries, and continue to maintain their own accounting records, but the

parent company produces a consolidated financial statement, which shows

the financial operations of both companies. Depending on the jurisdiction’s

reporting requirements, however, if a company owns a minority stake in a

second company, then the latter will not be included in the former’s

consolidated financial statement.

COnsOlidated finanCial statements

need tO knOw

Subsidiary One company that

is controlled by another, usually

a holding company

Holding company A company

set up to buy shares of other

companies, then control them

Globalization The process of

businesses developing such large

multinational presences that they

transcend international borders

$

US_104-109_Financial_Statements.indd 105 21/11/2014 17:27

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.