CHAPTER 16 Dilutive Securities and Earnings per Share

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Describe the accounting for the issuance, conversion, and retirement of convertible securities.

- Explain the accounting for convertible preferred stock.

- Contrast the accounting for stock warrants and for stock warrants issued with other securities.

- Describe the accounting for stock compensation plans.

- Discuss the controversy involving stock compensation plans.

- Compute earnings per share in a simple capital structure.

- Compute earnings per share in a complex capital structure.

Kicking the Habit

Some habits die hard. Take stock options—called by some “the crack cocaine of incentives.” Stock options are a form of compensation that gives key employees the choice to purchase shares at a given (usually lower-than-market) price. For many years, companies were hooked on these products. Why? The combination of a hot equity market and favorable accounting treatment made stock options the incentive of choice. They were compensation with no expense to the companies that granted them, and they were popular with key employees, so companies granted them with abandon. However, the accounting rules that took effect in 2005 required expensing the fair value of stock options. This new treatment has made it easier for companies to kick this habit.

As shown in the chart above, a review of option use for the U.S. companies in the S&P 500 indicates a decline in the use of option-based compensation and an increase in restricted-stock plans. Fewer companies are granting stock options, following implementation of stock-option expensing. As a spokesperson at one company commented, “Once you begin expensing options, the attractiveness significantly drops.”

In the 1990s, executives with huge option stockpiles had an almost irresistible incentive to do whatever it took to increase the stock price and cash in their options. By reining in options, many companies are taking the first steps toward curbing both out-of-control executive pay and the era of corporate corruption that it spawned.

![]() CONCEPTUAL FOCUS

CONCEPTUAL FOCUS

- See the Underlying Concepts on pages 890 and 897.

- Read the Evolving Issue on page 890 for a discussion of convertible debt.

![]() INTERNATIONAL FOCUS

INTERNATIONAL FOCUS

- See the International Perspectives on pages 885, 892, 896, 901, and 904.

- Read the IFRS Insights on pages 941–949 for a discussion of:

- Accounting for convertible debt

- Employee share-purchase plans

As indicated earlier, some of the ways that companies are curbing option grants include replacing options with restricted shares. Further analysis of these trends indicates that restricted-stock use is more than 10 times the magnitude of options grants in the financial industry. Even after excluding financial companies from the statistics, restricted shares are now the plan of choice. And in the information technology area (where in the past, share options were heavily favored), the fair value of restricted-share plans exceeds that for share options. In this industry, some companies are simply reducing option grants, without offering a replacement, while others, like Microsoft and Yahoo!, have switched to restricted-stock plans completely. Is this a good trend? Most believe it is; the requirement to expense stock-based compensation similar to other forms of compensation has changed the focus of compensation plans to rewarding talent and performance without breaking the bank. The positive impact on corporate behavior, while hard to measure, should benefit investors in years to come.

Sources: Adapted from: Louis Lavelle, “Kicking the Stock-Options Habit,” BusinessWeek Online (February 16, 2005). Graph from J. Ciesielski, “S&P 500 Executive Pay: The Bread Keeps Rising,” The Analyst's Accounting Observer (June 25, 2012).

PREVIEW OF CHAPTER 16

As the opening story indicates, companies are rethinking the use of various forms of stock-based compensation. The purpose of this chapter is to discuss the proper accounting for stock-based compensation. In addition, the chapter examines issues related to other types of financial instruments, such as convertible securities, warrants, and contingent shares, including their effects on reporting earnings per share. The content and organization of the chapter are as follows.

DILUTIVE SECURITIES

Debt and Equity

LEARNING OBJECTIVE ![]()

Describe the accounting for the issuance, conversion, and retirement of convertible securities.

Many of the controversies related to the accounting for financial instruments such as stock options, convertible securities, and preferred stock relate to whether companies should report these instruments as a liability or as equity. For example, companies should classify nonredeemable common shares as equity because the issuer has no obligation to pay dividends or repurchase the stock. Declaration of dividends is at the issuer's discretion, as is the decision to repurchase the stock. Similarly, preferred stock that is not redeemable does not require the issuer to pay dividends or repurchase the stock. Thus, nonredeemable common or preferred stock lacks an important characteristic of a liability—an obligation to pay the holder of the common or preferred stock at some point in the future.

![]() See the FASB Codification section (page 923).

See the FASB Codification section (page 923).

However the classification is not as clear-cut for other financial instruments. For example, in Chapter 15 we discussed the accounting for mandatorily redeemable preferred stock. Companies originally classified this security as part of equity. The SEC then prohibited equity classification, and most companies classified these securities between debt and equity on the balance sheet in a separate section often referred to as the “mezzanine section.” The FASB now requires companies to report these types of securities as a liability.1 [1]

In this chapter, we discuss securities that have characteristics of both debt and equity. For example, a convertible bond has both debt and equity characteristics. Should a company classify this security as debt, as equity, or as part debt and part equity? In addition, how should a company compute earnings per share if it has convertible bonds and other convertible securities in its capital structure? Convertible securities as well as options, warrants, and other securities are often called dilutive securities because upon exercise they may reduce (dilute) earnings per share.

Accounting for Convertible Debt

Convertible bonds can be changed into other corporate securities during some specified period of time after issuance. A convertible bond combines the benefits of a bond with the privilege of exchanging it for stock at the holder's option. Investors who purchase it desire the security of a bond holding (guaranteed interest and principal) plus the added option of conversion if the value of the stock appreciates significantly.

Corporations issue convertibles for two main reasons. One is to raise equity capital without giving up more ownership control than necessary. To illustrate, assume a company wants to raise $1 million; its common stock is selling at $45 a share. To raise the $1 million, the company would have to sell 22,222 shares (ignoring issue costs). By selling 1,000 bonds at $1,000 par, each convertible into 20 shares of common stock, the company could raise $1 million by committing only 20,000 shares of its common stock.

A second reason to issue convertibles is to obtain debt financing at cheaper rates. Many companies could issue debt only at high interest rates unless they attach a convertible covenant. The conversion privilege entices the investor to accept a lower interest rate than would normally be the case on a straight debt issue. For example, Amazon.com at one time issued convertible bonds that pay interest at an effective yield of 4.75 percent. This rate was much lower than Amazon would have had to pay by issuing straight debt. For this lower interest rate, the investor receives the right to buy Amazon's common stock at a fixed price until the bond's maturity.2

As indicated earlier, the accounting for convertible debt involves reporting issues at the time of (1) issuance, (2) conversion, and (3) retirement.

At Time of Issuance

![]() International Perspective

International Perspective

IFRS requires that the issuer of convertible debt record the liability and equity components separately.

The method for recording convertible bonds at the date of issue follows the method used to record straight debt issues. None of the proceeds are recorded as equity. Companies amortize to the maturity date any discount or premium that results from the issuance of convertible bonds. Why this treatment? Because it is difficult to predict when, if at all, conversion will occur. However, the accounting for convertible debt as a straight debt issue is controversial; we discuss it more fully later in the chapter.

At Time of Conversion

If converting bonds into other securities, a company uses the book value method to record the conversion. The book value method records the securities exchanged for the bond at the carrying amount (book value) of the bond.

To illustrate, assume that Hilton, Inc. has a $1,000 bond that is convertible into 10 shares of common stock (par value $10). At the time of conversion, the unamortized premium is $50. Hilton records the conversion of the bonds as follows.

Support for the book value approach is based on the argument that an agreement was established at the date of the issuance either to pay a stated amount of cash at maturity or to issue a stated number of shares of equity securities. Therefore, when the debtholder converts the debt to equity in accordance with the preexisting contract terms, the issuing company recognizes no gain or loss upon conversion.

Induced Conversions

Sometimes the issuer wishes to encourage prompt conversion of its convertible debt to equity securities in order to reduce interest costs or to improve its debt to equity ratio. Thus, the issuer may offer some form of additional consideration (such as cash or common stock), called a “sweetener,” to induce conversion. The issuing company reports the sweetener as an expense of the current period. Its amount is the fair value of the additional securities or other consideration given.

Assume that Helloid, Inc. has outstanding $1,000,000 par value convertible debentures convertible into 100,000 shares of $1 par value common stock. Helloid wishes to reduce its annual interest cost. To do so, Helloid agrees to pay the holders of its convertible debentures an additional $80,000 if they will convert. Assuming conversion occurs, Helloid makes the following entry.

Helloid records the additional $80,000 as an expense of the current period and not as a reduction of equity.

Some argue that the cost of a conversion inducement is a cost of obtaining equity capital. As a result, they contend, companies should recognize the cost of conversion as a cost of (a reduction of) the equity capital acquired, and not as an expense. However, the FASB indicated that when an issuer makes an additional payment to encourage conversion, the payment is for a service (bondholders converting at a given time) and should be reported as an expense. The issuing company does not report this expense as an extraordinary item. [2]

Retirement of Convertible Debt

As indicated earlier, the method for recording the issuance of convertible bonds follows that used in recording straight debt issues. Specifically this means that issuing companies should not attribute any portion of the proceeds to the conversion feature, nor should it credit a paid-in capital account.

Although some raise theoretical objections to this approach, to be consistent, companies need to recognize a gain or loss on retiring convertible debt in the same way that they recognize a gain or loss on retiring nonconvertible debt. For this reason, companies should report differences between the cash acquisition price of debt and its carrying amount in current income as a gain or loss.

Convertible Preferred Stock

LEARNING OBJECTIVE ![]()

Explain the accounting for convertible preferred stock.

Convertible preferred stock includes an option for the holder to convert preferred shares into a fixed number of common shares. The major difference between accounting for a convertible bond and convertible preferred stock at the date of issue is their classification. Convertible bonds are considered liabilities, whereas convertible preferreds (unless mandatory redemption exists) are considered part of stockholders' equity.

In addition, when stockholders exercise convertible preferred stock, there is no theoretical justification for recognizing a gain or loss. A company does not recognize a gain or loss when it deals with stockholders in their capacity as business owners. Therefore, companies do not recognize a gain or loss when stockholders exercise convertible preferred stock.

In accounting for the exercise of convertible preferred stock, a company uses the book value method. It debits Preferred Stock, along with any related Paid-in Capital in Excess of Par—Preferred Stock, and it credits Common Stock and Paid-in Capital in Excess of Par—Common Stock (if an excess exists). The treatment differs when the par value of the common stock issued exceeds the book value of the preferred stock. In that case, the company usually debits Retained Earnings for the difference.

To illustrate, assume Host Enterprises issued 1,000 shares of common stock (par value $2) upon conversion of 1,000 shares of preferred stock (par value $1) that was originally issued for a $200 premium. The entry would be:

The rationale for the debit to Retained Earnings is that Host has offered the preferred stockholders an additional return to facilitate their conversion to common stock. In this example, Host charges the additional return to retained earnings. Many states, however, require that this charge simply reduce additional paid-in capital from other sources.

What do the numbers mean? HOW LOW CAN YOU GO?

Financial engineers are always looking for the next innovation in security design to meet the needs of both issuers and investors. Consider the convertible bonds issued by STMicroelectronics (STM). STM's 10-year bonds have a zero coupon and are convertible into STM common stock at an exercise price of $33.43. When issued, the bonds sold at an effective yield of −0.05 percent. That's right—a negative yield.

How could this happen? When STM issued the bonds, investors thought the options to convert were so valuable that they were willing to take zero interest payments and invest an amount in excess of the maturity value of the bonds. In essence, the investors are paying interest to STM, and STM records interest revenue. Why would investors do this? If the stock price rises, as many thought it would for STM and many tech companies at this time, these bond investors could convert and get a big gain in the stock.

Investors did get some additional protection in the deal: They can redeem the $1,000 bonds after three years and receive $975 (and after five and seven years, for lower amounts), if it looks like the bonds will never convert. In the end, STM has issued bonds with a significant equity component. And because the entire bond issue is classified as debt, STM records negative interest expense.

Source: STM Financial Reports. See also Floyd Norris, “Legal but Absurd: They Borrow a Billion and Report a Profit,” The New York Times (August 8, 2003), p. C1.

Stock Warrants

LEARNING OBJECTIVE ![]()

Contrast the accounting for stock warrants and for stock warrants issued with other securities.

Warrants are certificates entitling the holder to acquire shares of stock at a certain price within a stated period. This option is similar to the conversion privilege in a convertible bond. Warrants, if exercised, become common stock and usually have a dilutive effect (reduce earnings per share) similar to that of the conversion of convertible securities. However, a substantial difference between convertible securities and stock warrants is that upon exercise of the warrants, the holder has to pay a certain amount of money to obtain the shares.

The issuance of warrants or options to buy additional shares normally arises under three situations:

- When issuing different types of securities, such as bonds or preferred stock, companies often include warrants to make the security more attractive—by providing an “equity kicker.”

- Upon the issuance of additional common stock, existing stockholders have a preemptive right to purchase common stock first. Companies may issue warrants to evidence that right.

- Companies give warrants, often referred to as stock options, to executives and employees as a form of compensation.

The problems in accounting for stock warrants are complex and present many difficulties—some of which remain unresolved. The following sections address the accounting for stock warrants in the three situations listed above.

Stock Warrants Issued with Other Securities

Warrants issued with other securities are basically long-term options to buy common stock at a fixed price. Generally the life of warrants is five years, occasionally 10 years; very occasionally, a company may offer perpetual warrants.

A warrant works like this. Tenneco, Inc. offered a unit comprising one share of stock and one detachable warrant. As its name implies, the detachable stock warrant can be detached (separated) from the stock and traded as a separate security. The Tenneco warrant in this example is exercisable at $24.25 per share and good for five years. The unit (share of stock plus detachable warrant) sold for 22.75 ($22.75). Since the price of the common stock the day before the sale was 19.88 ($19.88), the difference suggests a price of 2.87 ($2.87) for the warrant.

The investor pays for the warrant in order to receive the right to buy the stock, at a fixed price of $24.25, sometime in the future. It would not be profitable at present for the purchaser to exercise the warrant and buy the stock, because the price of the stock was much below the exercise price.3 But if, for example, the price of the stock rises to $30, the investor gains $2.88 ($30 − $24.25 − $2.87) on an investment of $2.87, a 100 percent increase! If the price never rises, the investor loses the full $2.87 per warrant.4

A company should allocate the proceeds from the sale of debt with detachable stock warrants between the two securities.5 The profession takes the position that two separable instruments are involved, that is, (1) a bond and (2) a warrant giving the holder the right to purchase common stock at a certain price. Companies can trade detachable warrants separately from the debt. This allows the determination of a fair value. The two methods of allocation available are:

- The proportional method.

- The incremental method.

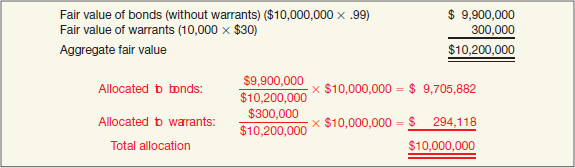

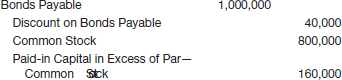

Proportional Method. At one time, AT&T issued bonds with detachable five-year warrants to buy one share of common stock (par value $5) at $25. At the time, a share of AT&T stock was selling for approximately $50. These warrants enabled AT&T to price its bond offering at par with an 8¾ percent yield (quite a bit lower than prevailing rates at that time). To account for the proceeds from this offering, AT&T would place a value on the two securities: (1) the value of the bonds without the warrants, and (2) the value of the warrants. The proportional method then allocates the proceeds using the proportion of the two amounts, based on fair values.

For example, assume that AT&T's bonds (par $1,000) sold for 99 without the warrants soon after their issue. The market price of the warrants at that time was $30. (Prior to sale the warrants will not have a fair value.) The allocation relies on an estimate of fair value, generally as established by an investment banker, or on the relative fair value of the bonds and the warrants soon after the company issues and trades them. The price paid for 10,000, $1,000 bonds with the warrants attached was par, or $10,000,000. Illustration 16-1 shows the proportional allocation of the bond proceeds between the bonds and warrants.

In this situation, the bonds sell at a discount. AT&T records the sale as follows.

![]()

In addition, AT&T sells warrants that it credits to paid-in capital. It makes the following entry.

![]()

AT&T may combine the entries if desired. Here, we show them separately, to indicate that the purchaser of the bond is buying not only a bond but also a possible future claim on common stock in the form of the stock warrant.

Assuming investors exercise all 10,000 warrants (one warrant per one share of stock), AT&T makes the following entry.

What if investors fail to exercise the warrants? In that case, AT&T debits Paid-in Capital—Stock Warrants for $294,118 and credits Paid-in Capital—Expired Stock Warrants for a like amount. The additional paid-in capital reverts to the former stockholders.

Incremental Method. In instances where a company cannot determine the fair value of either the warrants or the bonds, it applies the incremental method used in lump-sum security purchases (as explained in Chapter 15, page 827). That is, the company uses the security for which it can determine the fair value. It allocates the remainder of the purchase price to the security for which it does not know the fair value.

For example, assume that the fair value of the AT&T warrants is $300,000, but the company cannot determine the fair value of the bonds without the warrants. Illustration 16-2 shows the amount allocated to the warrants and the stock in this case.

Conceptual Questions. The question arises whether the allocation of value to the warrants is consistent with the handling of convertible debt, in which companies allocate no value to the conversion privilege. The FASB stated that the features of a convertible security are inseparable in the sense that choices are mutually exclusive. The holder either converts the bonds or redeems them for cash, but cannot do both. No basis, therefore, exists for recognizing the conversion value in the accounts.

![]() Underlying Concepts

Underlying Concepts

Reporting a convertible bond solely as debt is not representationally faithful. However, the cost constraint is used to justify the failure to allocate between debt and equity.

The Board, however, indicated that the issuance of bonds with detachable warrants involves two securities, one a debt security, which will remain outstanding until maturity, and the other a warrant to purchase common stock. At the time of issuance, separable instruments exist. The existence of two instruments therefore justifies separate treatment. Nondetachable warrants, however, do not require an allocation of the proceeds between the bonds and the warrants. Similar to the accounting for convertible bonds, companies record the entire proceeds from nondetachable warrants as debt.6

Evolving Issue IS THAT ALL DEBT?

Evolving Issue IS THAT ALL DEBT?

Many argue that the conversion feature of a convertible bond is not significantly different in nature from the call represented by a warrant. The question is whether, although the legal forms differ, sufficient similarities of substance exist to support the same accounting treatment. Some contend that inseparability per se is an insufficient basis for restricting allocation between identifiable components of a transaction.

Examples of allocation between assets of value in a single transaction do exist, such as allocation of values in basket purchases and separation of principal and interest in capitalizing long-term leases. Critics of the current accounting for convertibles say that to deny recognition of value to the conversion feature merely looks to the form of the instrument and does not deal with the substance of the transaction. In an exposure draft on this subject (project now inactive), the FASB indicates that companies should separate the debt and equity components of securities such as convertible debt or bonds issued with nondetachable warrants (see footnotes 1 and 6).

We agree with this position. In both situations (convertible debt and debt issued with warrants), the investor has made a payment to the company for an equity feature—the right to acquire an equity instrument in the future. The only real distinction between them is that the additional payment made when the equity instrument is formally acquired takes different forms. The warrant holder pays additional cash to the issuing company; the convertible debt holder pays for stock by forgoing the receipt of interest from conversion date until maturity date and by forgoing the receipt of the maturity value itself. Thus, the difference is one of method or form of payment only, rather than one of substance. However, until the profession officially reverses its stand with respect to accounting for convertible debt, companies will continue to report convertible debt and bonds issued with nondetachable warrants solely as debt.

Rights to Subscribe to Additional Shares

If the directors of a corporation decide to issue new shares of stock, the old stockholders generally have the right (preemptive privilege) to purchase newly issued shares in proportion to their holdings. This privilege, referred to as a stock right, saves existing stockholders from suffering a dilution of voting rights without their consent. Also, it may allow them to purchase stock somewhat below its fair value. Unlike the warrants issued with other securities, the warrants issued for stock rights are of short duration.

The certificate representing the stock right states the number of shares the holder of the right may purchase. Each share of stock owned ordinarily gives the owner one stock right. The certificate also states the price at which the new shares may be purchased. The price is normally less than the current market price of such shares, which gives the rights a value in themselves. From the time they are issued until they expire, holders of stock rights may purchase and sell them like any other security.

Companies make only a memorandum entry when they issue rights to existing stockholders. This entry indicates the number of rights issued to existing stockholders in order to ensure that the company has additional unissued stock registered for issuance in case the rights are exercised. Companies make no formal entry at this time because they have not yet issued stock nor received cash.

If holders exercise the stock rights, a cash payment of some type usually is involved. If the company receives cash equal to the par value, it makes an entry crediting Common Stock at par value. If the company receives cash in excess of par value, it credits Paid-in Capital in Excess of Par—Common Stock. If it receives cash less than par value, a debit to Paid-in Capital in Excess of Par—Common Stock is appropriate.

Stock Compensation Plans

The third form of warrant arises in stock compensation plans to pay and motivate employees. This warrant is a stock option, which gives key employees the option to purchase common stock at a given price over an extended period of time.

A consensus of opinion is that effective compensation programs are ones that do the following: (1) base compensation on employee and company performance, (2) motivate employees to high levels of performance, (3) help retain executives and allow for recruitment of new talent, (4) maximize the employee's after-tax benefit and minimize the employer's after-tax cost, and (5) use performance criteria over which the employee has control. Straight cash-compensation plans (salary and perhaps a bonus), though important, are oriented to the short run. Many companies recognize that they need a longer-term compensation plan in addition to the cash component.

Long-term compensation plans attempt to develop company loyalty among key employees by giving them “a piece of the action”—that is, an equity interest. These plans, generally referred to as stock-based compensation plans, come in many forms. Essentially, they provide the employee with the opportunity to receive stock if the performance of the company (by whatever measure) is satisfactory. Typical performance measures focus on long-term improvements that are readily measurable and that benefit the company as a whole, such as increases in earnings per share, revenues, stock price, or market share.

As indicated in our opening story, companies are changing the way they use stock-based compensation. Illustration 16-3 indicates that option expense is a much smaller element of compensation relative to restricted stock at companies such as Ford and Wal-Mart.

The major reasons for this change are two-fold. Critics often cited the indiscriminate use of stock options as a reason why company executives manipulated accounting numbers in an attempt to achieve higher share price. As a result, many responsible companies decided to cut back on the issuance of options, both to avoid such accounting manipulations and to head off investor doubts. In addition, GAAP now results in companies recording a higher expense when stock options are granted.

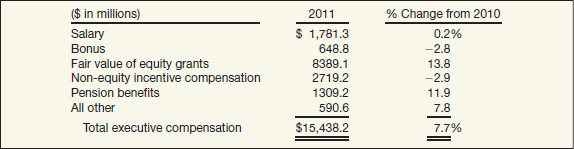

The data reported in Illustration 16-4 (page 892) reinforce the point that the fair value of stock grants is significant and increasing. The study documents that compensation increased 7.7 percent for S&P 500 executives in 2011, with equity grants being the biggest source of growth.

Illustration 16-4 shows that cash compensation is less than 20 percent of total compensation. The fair value of equity grants comprised approximately 54 percent of total compensation.

The Major Reporting Issue. Suppose that as an employee for Hurdle Inc., you receive options to purchase 10,000 shares of the firm's common stock as part of your compensation. The date you receive the options is referred to as the grant date. The options are good for 10 years. The market price and the exercise price for the stock are both $20 at the grant date. What is the value of the compensation you just received?

Some believe that what you have received has no value. They reason that because the difference between the market price and the exercise price is zero, no compensation results. Others argue these options do have value. If the stock price goes above $20 any time in the next 10 years and you exercise the options, you may earn substantial compensation. For example, if at the end of the fourth year, the market price of the stock is $30 and you exercise your options, you earn $100,000 [10,000 options × ($30 − $20)], ignoring income taxes.

![]() International Perspective

International Perspective

IFRS follows the same model as GAAP for recognizing share-based compensation.

The question for Hurdle is how to report the granting of these options. One approach measures compensation cost by the excess of the market price of the stock over its exercise price at the grant date. This approach is referred to as the intrinsic-value method. It measures what the holder would receive today if the option was immediately exercised. That intrinsic value is the difference between the market price of the stock and the exercise price of the options at the grant date. Using the intrinsic-value method, Hurdle would not recognize any compensation expense related to your options because at the grant date the market price equaled the exercise price. (In the preceding paragraph, those who answered that the options had no value were looking at the question from the intrinsic-value approach.)

The second way to look at the question of how to report the granting of these options bases the cost of employee stock options on the fair value of the stock options granted. Under this fair value method, companies use acceptable option-pricing models to value the options at the date of grant. These models take into account the many factors that determine an option's underlying value.7

GAAP requires that companies recognize compensation cost using the fair value method. [5] The FASB position is that companies should base the accounting for the cost of employee services on the fair value of compensation paid. This amount is presumed to be a measure of the value of the services received. We will discuss more about the politics of GAAP in this area later (see “Debate over Stock-Option Accounting,” page 897). Let's first describe the procedures involved.

ACCOUNTING FOR STOCK COMPENSATION

Stock-Option Plans

Stock-option plans involve two main accounting issues:

- How to determine compensation expense.

- Over what periods to allocate compensation expense.

Determining Expense

Under the fair value method, companies compute total compensation expense based on the fair value of the options expected to vest on the date they grant the options to the employee(s) (i.e., the grant date).8 Public companies estimate fair value by using an option-pricing model, with some adjustments for the unique factors of employee stock options. No adjustments occur after the grant date in response to subsequent changes in the stock price—either up or down.

Allocating Compensation Expense

In general, a company recognizes compensation expense in the periods in which its employees perform the service—the service period. Unless otherwise specified, the service period is the vesting period—the time between the grant date and the vesting date. Thus, the company determines total compensation cost at the grant date and allocates it to the periods benefited by its employees' services.

Stock Compensation Example

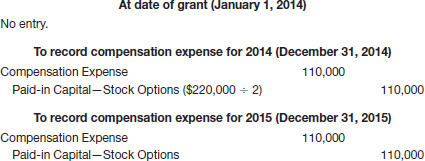

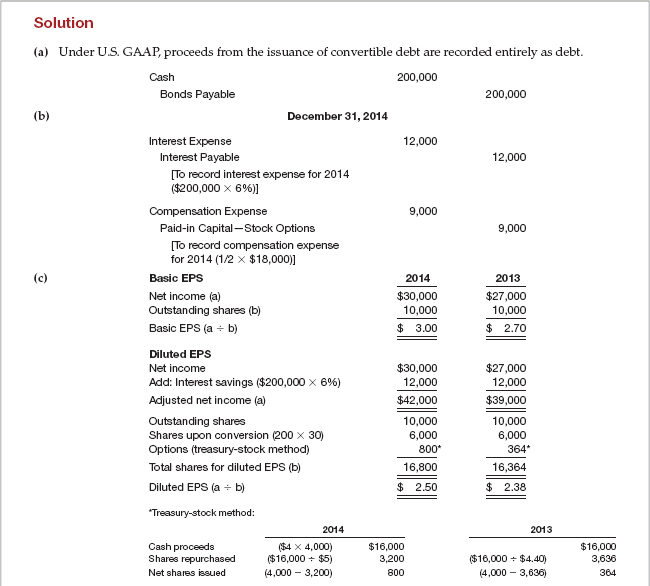

An example will help show the accounting for a stock-option plan. Assume that on November 1, 2013, the stockholders of Chen Company approve a plan that grants the company's five executives options to purchase 2,000 shares each of the company's $1 par value common stock. The company grants the options on January 1, 2014. The executives may exercise the options at any time within the next 10 years. The option price per share is $60, and the market price of the stock at the date of grant is $70 per share.

Under the fair value method, the company computes total compensation expense by applying an acceptable fair value option-pricing model (such as the Black-Scholes option-pricing model). To keep this illustration simple, we assume that the fair value option-pricing model determines Chen's total compensation expense to be $220,000.

Basic Entries. Under the fair value method, a company recognizes the value of the options as an expense in the periods in which the employee performs services. In the case of Chen Company, assume that the expected period of benefit is two years, starting with the grant date. Chen would record the transactions related to this option contract as follows.

As indicated, Chen allocates compensation expense evenly over the two-year service period.

Exercise. If Chen's executives exercise 2,000 of the 10,000 options (20 percent of the options) on June 1, 2017 (three years and five months after date of grant), the company records the following journal entry.

Expiration. If Chen's executives fail to exercise the remaining stock options before their expiration date, the company transfers the balance in the Paid-in Capital—Stock Options account to a more properly titled paid-in capital account, such as Paid-in Capital—Expired Stock Options. Chen records this transaction at the date of expiration as follows.

Adjustment. An unexercised stock option does not nullify the need to record the costs of services received from executives and attributable to the stock option plan. Under GAAP, a company therefore does not adjust compensation expense upon expiration of the options.

However, if an employee forfeits a stock option because the employee fails to satisfy a service requirement (e.g., leaves employment), the company should adjust the estimate of compensation expense recorded in the current period (as a change in estimate). A company records this change in estimate by debiting Paid-in Capital—Stock Options and crediting Compensation Expense for the amount of cumulative compensation expense recorded to date (thus decreasing compensation expense in the period of forfeiture).

Restricted Stock

As indicated earlier, many companies also use restricted stock (in some cases, replacing options altogether) to compensate employees. Restricted-stock plans transfer shares of stock to employees, subject to an agreement that the shares cannot be sold, transferred, or pledged until vesting occurs. Similar to stock options, these shares are subject to forfeiture if the conditions for vesting are not met.9

Major advantages of restricted-stock plans are:

- Restricted stock never becomes completely worthless. In contrast, if the stock price does not exceed the exercise price for a stock option, the options are worthless. The restricted stock, however, still has value.

- Restricted stock generally results in less dilution to existing stockholders. Restricted-stock awards are usually one-half to one-third the size of stock options. For example, if a company issues stock options on 1,000 shares, an equivalent restricted-stock offering might be 333 to 500 shares. The reason for the difference is that at the end of the vesting period, the restricted stock will have value, whereas the stock options may not. As a result, fewer shares are involved in restricted-stock plans, and therefore less dilution results if the stock price rises.

- Restricted stock better aligns the employee incentives with the companies' incentives. The holder of restricted stock is essentially a stockholder and should be more interested in the long-term objectives of the company. In contrast, the recipients of stock options often have a short-run focus which leads to taking risks to hype the stock price for short-term gain to the detriment of the long-term.10

The accounting for restricted stock follows the same general principles as accounting for stock options at the date of grant. That is, the company determines the fair value of the restricted stock at the date of grant (usually the fair value of a share of stock) and then expenses that amount over the service period. Subsequent changes in the fair value of the stock are ignored for purposes of computing compensation expense.

Restricted Stock Example

Assume that on January 1, 2014, Ogden Company issues 1,000 shares of restricted stock to its CEO, Christie DeGeorge. Ogden's stock has a fair value of $20 per share on January 1, 2014. Additional information is as follows.

- The service period related to the restricted stock is five years.

- Vesting occurs if DeGeorge stays with the company for a five-year period.

- The par value of the stock is $1 per share.

Ogden makes the following entry on the grant date (January 1, 2014).

![]()

The credits to Common Stock and Paid-in Capital in Excess of Par—Common Stock indicate that Ogden has issued shares of stock. The debit to Unearned Compensation (often referred to as Deferred Compensation Expense) identifies the total compensation expense the company will recognize over the five-year period. Unearned Compensation represents the cost of services yet to be performed, which is not an asset. Consequently, the company reports Unearned Compensation in stockholders' equity in the balance sheet, as a contra equity account (similar to the reporting of treasury stock at cost).

At December 31, 2014, Ogden records compensation expense of $4,000 (1,000 shares × $20 × 20%) as follows.

![]()

Ogden records compensation expense of $4,000 for each of the next four years (2015, 2016, 2017, and 2018).

What happens if DeGeorge leaves the company before the five years has elapsed? In this situation, DeGeorge forfeits her rights to the stock, and Ogden reverses the compensation expense already recorded.

For example, assume that DeGeorge leaves on February 3, 2016 (before any expense has been recorded during 2016). The entry to record this forfeiture is as follows.

In this situation, Ogden reverses the compensation expense of $8,000 recorded through 2015. In addition, the company debits Common Stock and Paid-in Capital in Excess of Par—Common Stock, reflecting DeGeorge's forfeiture. It credits the balance of Unearned Compensation since none remains when DeGeorge leaves Ogden.

This accounting is similar to accounting for stock options when employees do not fulfill vesting requirements. Recall that once compensation expense is recorded for stock options, it is not reversed. The only exception is if the employee does not fulfill the vesting requirement, by leaving the company before vesting occurs.

In Ogden's restricted-stock plan, vesting never occurred because DeGeorge left the company before she met the service requirement. Because DeGeorge was never vested, she had to forfeit her shares. Therefore, the company must reverse compensation expense recorded to date.11

Employee Stock-Purchase Plans

Employee stock-purchase plans (ESPPs) generally permit all employees to purchase stock at a discounted price for a short period of time. The company often uses such plans to secure equity capital or to induce widespread ownership of its common stock among employees. These plans are considered compensatory unless they satisfy all three conditions presented below.

- Substantially all full-time employees may participate on an equitable basis.

- The discount from market is small. That is, the discount does not exceed the per share amount of costs avoided by not having to raise cash in a public offering. If the amount of the discount is 5 percent or less, no compensation needs to be recorded.

- The plan offers no substantive option feature.

![]() International Perspective

International Perspective

IFRS requires that any discount from the market price in employee stock-purchase plans be recorded as compensation expense.

For example, Masthead Company's stock-purchase plan allowed employees who met minimal employment qualifications to purchase its stock at a 5 percent reduction from market price for a short period of time. The reduction from market price is not considered compensatory. Why? Because the per share amount of the costs avoided by not having to raise the cash in a public offering equals 5 percent.

Companies that offer their employees a compensatory ESPP should record the compensation expense over the service life of the employees. It will be difficult for some companies to claim that their ESPPs are non-compensatory (and therefore not record compensation expense) unless they change their discount policy which in the past often was 15 percent. If they change their discount policy to 5 percent, participation in these plans will undoubtedly be lower. As a result, it is likely that some companies will end up dropping these plans.

Disclosure of Compensation Plans

Companies must fully disclose the status of their compensation plans at the end of the periods presented. To meet these objectives, companies must make extensive disclosures. Specifically, a company with one or more share-based payment arrangements must disclose information that enables users of the financial statements to understand:

- The nature and terms of such arrangements that existed during the period and the potential effects of those arrangements on shareholders.

- The effect on the income statement of compensation cost arising from share-based payment arrangements.

- The method of estimating the fair value of the goods or services received, or the fair value of the equity instruments granted (or offered to grant), during the period.

- The cash flow effects resulting from share-based payment arrangements.

Illustration 16-5 (on page 898) presents the type of information disclosed for compensation plans.

Debate over Stock-Option Accounting

LEARNING OBJECTIVE ![]()

Discuss the controversy involving stock compensation plans.

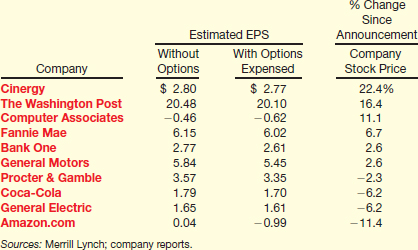

The FASB faced considerable opposition when it proposed the fair value method for accounting for stock options. This is not surprising, given that the fair value method results in greater compensation costs relative to the intrinsic-value model. One study documented that, on average, companies in the Standard & Poor's 500 stock index overstated earnings in a recent year by 10 percent through the use of the intrinsic-value method. (See the “What Do the Numbers Mean” box on page 899.) Nevertheless, some companies, such as Coca-Cola, General Electric, Wachovia, Bank One, and The Washington Post, decided to use the fair value method. As the CFO of Coca-Cola stated, “There is no doubt that stock options are compensation. If they weren't, none of us would want them.”

Yet many in corporate America resisted the fair value method. Many small high-technology companies were especially vocal in their opposition, arguing that only through offering stock options can they attract top professional management. They contended that recognizing large amounts of compensation expense under these plans places them at a competitive disadvantage against larger companies that can withstand higher compensation charges. As one high-tech executive stated, “If your goal is to attack fat-cat executive compensation in multi-billion dollar firms, then please do so! But not at the expense of the people who are ‘running lean and mean,’ trying to build businesses and creating jobs in the process.”

![]() Underlying Concepts

Underlying Concepts

The stock-option controversy involves economic-consequence issues. The FASB believes companies should follow the neutrality concept. Others disagree, noting that factors other than accounting theory should be considered.

The stock-option saga is a classic example of the difficulty the FASB faces in issuing new accounting guidance. Many powerful interests aligned against the Board. Even some who initially appeared to support the Board's actions later reversed themselves. These efforts undermine the authority of the FASB, which in turn damages confidence in our financial reporting system.

Transparent financial reporting—including recognition of stock-based expense—should not be criticized because companies will report lower income. We may not like what the financial statements say, but we are always better off when the statements are representationally faithful to the underlying economic substance of transactions.

By leaving stock-based compensation expense out of income, reported income is biased. Biased reporting not only raises concerns about the credibility of companies' reports, but also of financial reporting in general. Even good companies get tainted by the biased reporting of a few “bad apples.” If we write standards to achieve some social, economic, or public policy goal, financial reporting loses its credibility.

What do the numbers mean? A LITTLE HONESTY GOES A LONG WAY

As you have learned, GAAP requires companies to expense compensation paid in the form of stock options. However, before the change to require expensing, some companies voluntarily expensed options rather than simply disclosing the estimated costs in the notes to the financial statements. You might think investors would punish companies that decided to expense stock options. After all, most of corporate America has been battling for years to avoid having to expense them, worried that accounting for those perks would destroy earnings. And indeed, Merrill Lynch estimated that if all S&P 500 companies were to expense options, reported profits would fall by as much as 10 percent.

Yet, this small band of big-name companies voluntarily made the switch to expensing, and investors for the most part showered them with love. As shown in the following table, with a few exceptions, the stock prices of the “expensers,” from Cinergy to The Washington Post, outpaced the market after they announced the change.

The market's general positive reaction to the expensing of stock options provides a good case study supporting the value that investors place on transparent accounting and reporting. It is puzzling why some companies continued to fight implementation of the expensing rule.

Source: David Stires, “A Little Honesty Goes a Long Way,” Fortune (September 2, 2002), p. 186. Reprinted by permission. See also Troy Wolverton, “Foes of Expensing Welcome FASB Delay,” TheStreet.com (October 15, 2004).

COMPUTING EARNINGS PER SHARE

LEARNING OBJECTIVE ![]()

Compute earnings per share in a simple capital structure.

As indicated earlier, stockholders and potential investors widely use earnings per share in evaluating the profitability of a company. As a result, much attention is given to earnings per share by the financial press. Earnings per share indicates the income earned by each share of common stock. Thus, companies report earnings per share only for common stock. For example, if Oscar Co. has net income of $300,000 and a weighted average of 100,000 shares of common stock outstanding for the year, earnings per share is $3 ($300,000 ÷ 100,000). Because of the importance of earnings per share information, most companies must report this information on the face of the income statement.12 [6] The exception, due to cost-benefit considerations, is nonpublic companies.13 Generally, companies report earnings per share information below net income in the income statement. Illustration 16-6 shows Oscar Co.'s income statement presentation of earnings per share.

When the income statement contains intermediate components of income (such as discontinued operations or extraordinary items), companies should disclose earnings per share for each component. The presentation in Illustration 16-7 is representative.

These disclosures enable the user of the financial statements to recognize the effects on EPS of income from continuing operations, as distinguished from income or loss from irregular items.14

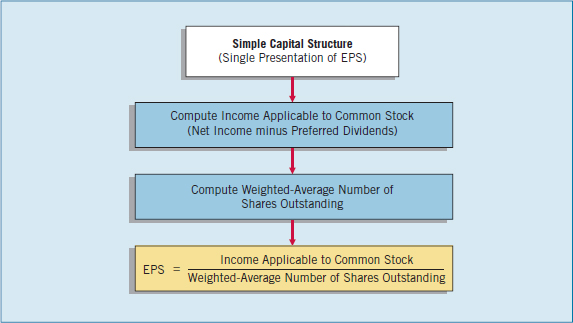

Earnings per Share—Simple Capital Structure

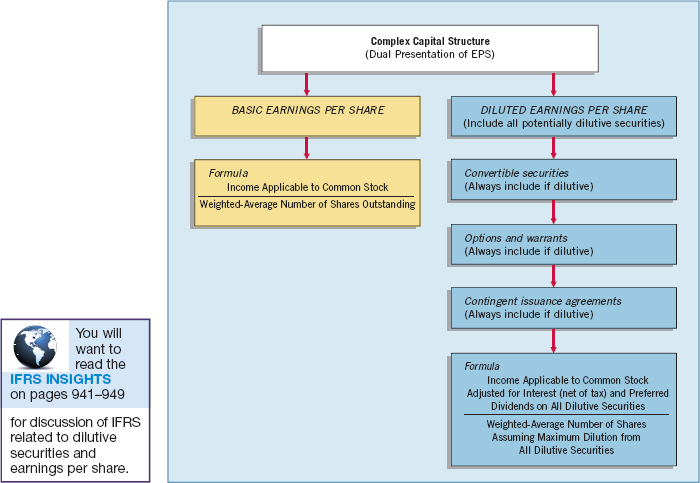

A corporation's capital structure is simple if it consists only of common stock or includes no potential common stock that upon conversion or exercise could dilute earnings per common share. A capital structure is complex if it includes securities that could have a dilutive effect on earnings per common share.

The computation of earnings per share for a simple capital structure involves two items (other than net income)—(1) preferred stock dividends and (2) weighted-average number of shares outstanding.

Preferred Stock Dividends

As we indicated earlier, earnings per share relates to earnings per common share. When a company has both common and preferred stock outstanding, it subtracts the current-year preferred stock dividend from net income to arrive at income available to common stockholders. Illustration 16-8 shows the formula for computing earnings per share.

In reporting earnings per share information, a company must calculate income available to common stockholders. To do so, the company subtracts dividends on preferred stock from each of the intermediate components of income (income from continuing operations and income before extraordinary items) and finally from net income. If a company declares dividends on preferred stock and a net loss occurs, the company adds the preferred dividend to the loss for purposes of computing the loss per share.

![]() International Perspective

International Perspective

The FASB and the IASB are working together on a project to improve EPS accounting by simplifying the computational guidance and thereby increasing the comparability of EPS data on an international basis.

If the preferred stock is cumulative and the company has net income but declares no dividend in the current year, it subtracts an amount equal to the dividend that it should have declared for the current year only. If the stock is cumulative and the company reports a net loss, but declares no dividend in the current year, it adds an amount equal to the dividend to the net loss. The company should have included dividends in arrears for previous years in the previous years' computations.

Weighted-Average Number of Shares Outstanding

In all computations of earnings per share, the weighted-average number of shares outstanding during the period constitutes the basis for the per share amounts reported. Shares issued or purchased during the period affect the amount outstanding. Companies must weight the shares by the fraction of the period they are outstanding. The rationale for this approach is to find the equivalent number of whole shares outstanding for the year.

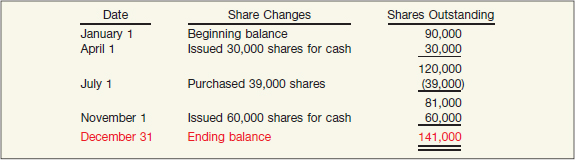

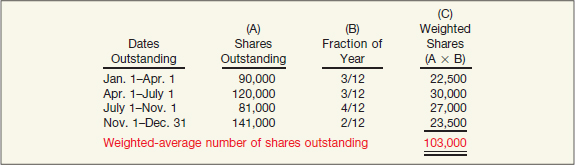

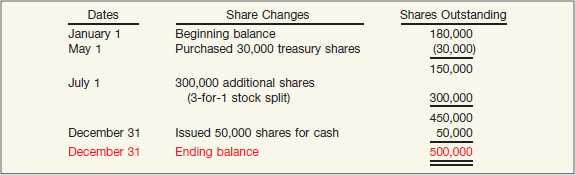

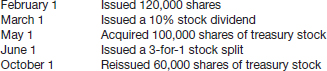

To illustrate, assume that Franks Inc. has changes in its common stock shares outstanding for the period as shown in Illustration 16-9.

Franks computes the weighted-average number of shares outstanding as follows.

As Illustration 16-10 shows, 90,000 shares were outstanding for three months, which is equivalent to 22,500 whole shares for the entire year. Because Franks issued additional shares on April 1, it must weight these shares for the time outstanding. When the company purchased 39,000 shares on July 1, it reduced the shares outstanding. Therefore, from July 1 to November 1, only 81,000 shares were outstanding, which is equivalent to 27,000 shares. The issuance of 60,000 shares increases shares outstanding for the last two months of the year. Franks then makes a new computation to determine the proper weighted shares outstanding.

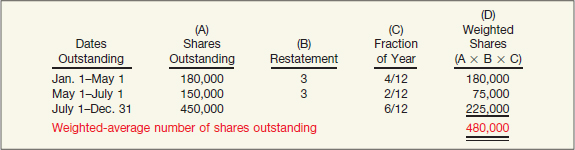

Stock Dividends and Stock Splits. When stock dividends or stock splits occur, companies need to restate the shares outstanding before the stock dividend or split, in order to compute the weighted-average number of shares. For example, assume that Vijay Corporation had 100,000 shares outstanding on January 1 and issued a 25 percent stock dividend on June 30. For purposes of computing a weighted-average for the current year, it assumes the additional 25,000 shares outstanding as a result of the stock dividend to be outstanding since the beginning of the year. Thus, the weighted-average for the year for Vijay is 125,000 shares.

Companies restate the issuance of a stock dividend or stock split, but not the issuance or repurchase of stock for cash. Why? Because stock splits and stock dividends do not increase or decrease the net assets of the company. The company merely issues additional shares of stock. Because of the added shares, it must restate the weighted-average shares. Restating allows valid comparisons of earnings per share between periods before and after the stock split or stock dividend. Conversely, the issuance or purchase of stock for cash changes the amount of net assets. As a result, the company either earns more or less in the future as a result of this change in net assets. Stated another way, a stock dividend or split does not change the shareholders' total investment—it only increases (unless it is a reverse stock split) the number of common shares representing this investment.

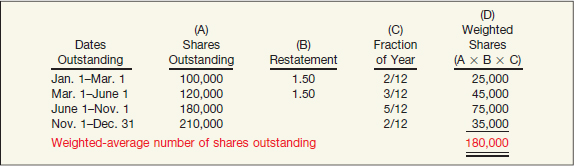

To illustrate how a stock dividend affects the computation of the weighted-average number of shares outstanding, assume that Sabrina Company has the following changes in its common stock shares during the year.

Sabrina computes the weighted-average number of shares outstanding as follows.

Sabrina must restate the shares outstanding prior to the stock dividend. The company adjusts the shares outstanding from January 1 to June 1 for the stock dividend, so that it now states these shares on the same basis as shares issued subsequent to the stock dividend. Sabrina does not restate shares issued after the stock dividend because they are on the new basis. The stock dividend simply restates existing shares. The same type of treatment applies to a stock split.

If a stock dividend or stock split occurs after the end of the year but before issuing the financial statements, a company must restate the weighted-average number of shares outstanding for the year (and any other years presented in comparative form). For example, assume that Hendricks Company computes its weighted-average number of shares as 100,000 for the year ended December 31, 2014. On January 15, 2015, before issuing the financial statements, the company splits its stock 3 for 1. In this case, the weighted-average number of shares used in computing earnings per share for 2014 is now 300,000 shares. If providing earnings per share information for 2013 as comparative information, Hendricks must also adjust it for the stock split.

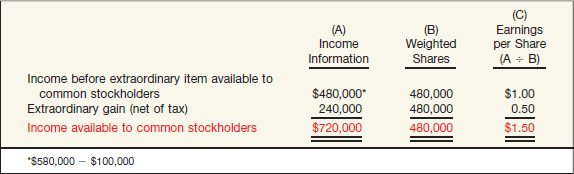

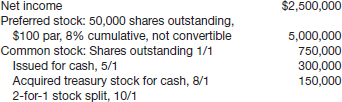

Comprehensive Example

Let's study a comprehensive illustration for a simple capital structure. Darin Corporation has income before extraordinary item of $580,000 and an extraordinary gain, net of tax, of $240,000. In addition, it has declared preferred dividends of $1 per share on 100,000 shares of preferred stock outstanding. Darin also has the following changes in its common stock shares outstanding during 2014.

To compute the earnings per share information, Darin determines the weighted-average number of shares outstanding as follows.

In computing the weighted-average number of shares, the company ignores the shares sold on December 31, 2014, because they have not been outstanding during the year. Darin then divides the weighted-average number of shares into income before extraordinary item and net income to determine earnings per share. It subtracts its preferred dividends of $100,000 from income before extraordinary item ($580,000) to arrive at income before extraordinary item available to common stockholders of $480,000 ($580,000 − $100,000).

Deducting the preferred dividends from the income before extraordinary item also reduces net income without affecting the amount of the extraordinary item. The final amount is referred to as income available to common stockholders, as shown in Illustration 16-15.

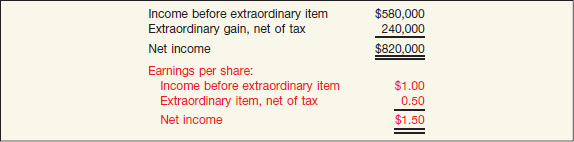

Darin must disclose the per share amount for the extraordinary item (net of tax) either on the face of the income statement or in the notes to the financial statements. Illustration 16-16 shows the income and per share information reported on the face of Darin's income statement.

Earnings per Share—Complex Capital Structure

LEARNING OBJECTIVE ![]()

Compute earnings per share in a complex capital structure.

The EPS discussion to this point applies to basic EPS for a simple capital structure. One problem with a basic EPS computation is that it fails to recognize the potential impact of a corporation's dilutive securities. As discussed at the beginning of the chapter, dilutive securities are securities that can be converted to common stock.15 Upon conversion or exercise by the holder, the dilutive securities reduce (dilute) earnings per share. This adverse effect on EPS can be significant and, more importantly, unexpected unless financial statements call attention to their potential dilutive effect.

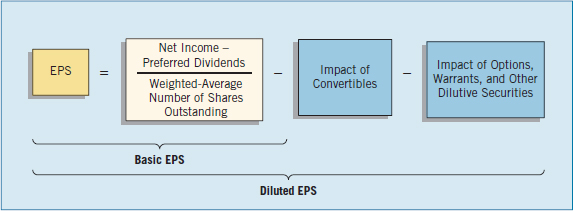

As indicated earlier, a complex capital structure exists when a corporation has convertible securities, options, warrants, or other rights that upon conversion or exercise could dilute earnings per share. When a company has a complex capital structure, it generally reports both basic and diluted earnings per share.

Computing diluted EPS is similar to computing basic EPS. The difference is that diluted EPS includes the effect of all potential dilutive common shares that were outstanding during the period. The formula in Illustration 16-17 shows the relationship between basic EPS and diluted EPS.

![]() International Perspective

International Perspective

The provisions in GAAP are substantially the same as those in International Accounting Standard No. 33, “Earnings per Share,” issued by the IASB.

Some securities are antidilutive. Antidilutive securities are securities that upon conversion or exercise increase earnings per share (or reduce the loss per share). Companies with complex capital structures will not report diluted EPS if the securities in their capital structure are antidilutive. The purpose of presenting both basic and diluted EPS is to inform financial statement users of situations that will likely occur (basic EPS) and also to provide “worst case” dilutive situations (dilutive EPS). If the securities are antidilutive, the likelihood of conversion or exercise is considered remote. Thus, companies that have only antidilutive securities must report only the basic EPS number. We illustrated the computation of basic EPS in the prior section. In the following sections, we address the effects of convertible and other dilutive securities on EPS calculations.

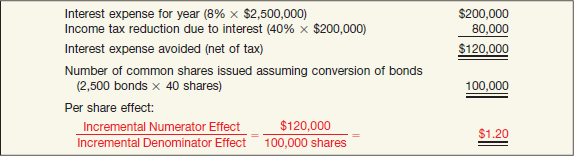

Diluted EPS—Convertible Securities

At conversion, companies exchange convertible securities for common stock. Companies measure the dilutive effects of potential conversion on EPS using the if-converted method. This method for a convertible bond assumes (1) the conversion of the convertible securities at the beginning of the period (or at the time of issuance of the security, if issued during the period), and (2) the elimination of related interest, net of tax. Thus, the additional shares assumed issued increase the denominator—the weighted-average number of shares outstanding. The amount of interest expense, net of tax associated with those potential common shares, increases the numerator—net income.

Comprehensive Example—If-Converted Method. As an example, Mayfield Corporation has net income of $210,000 for the year and a weighted-average number of common shares outstanding during the period of 100,000 shares. The basic earnings per share is therefore $2.10 ($210,000 ÷ 100,000). The company has two convertible debenture bond issues outstanding. One is a 6 percent issue sold at 100 (total $1,000,000) in a prior year and convertible into 20,000 common shares. The other is a 10 percent issue sold at 100 (total $1,000,000) on April 1 of the current year and convertible into 32,000 common shares. The tax rate is 40 percent.

As Illustration 16-18 shows, to determine the numerator for diluted earnings per share, Mayfield adds back the interest on the if-converted securities, less the related tax effect. Because the if-converted method assumes conversion as of the beginning of the year, Mayfield assumes that it pays no interest on the convertibles during the year. The interest on the 6 percent convertibles is $60,000 for the year ($1,000,000 × 6%). The increased tax expense is $24,000 ($60,000 × 0.40). The interest added back net of taxes is $36,000 [$60,000 − $24,000, or simply $60,000 × (1 − 0.40)].

Continuing with the information in Illustration 16-18, because Mayfield issues 10 percent convertibles subsequent to the beginning of the year, it weights the shares. In other words, it considers these shares to have been outstanding from April 1 to the end of the year. As a result, the interest adjustment to the numerator for these bonds reflects the interest for only nine months. Thus, the interest added back on the 10 percent convertible is $45,000 [$1,000,000 × 10% × 9/12 year × (1 − 0.4)]. The final item in Illustration 16-18 shows the adjusted net income. This amount becomes the numerator for Mayfield's computation of diluted earnings per share.

Mayfield then calculates the weighted-average number of shares outstanding, as shown in Illustration 16-19. This number of shares becomes the denominator for Mayfield's computation of diluted earnings per share.

In its income statement, Mayfield reports basic and diluted earnings per share.16 Illustration 16-20 shows this dual presentation.

Other Factors. The example above assumed that Mayfield sold its bonds at the face amount. If it instead sold the bonds at a premium or discount, the company must adjust the interest expense each period to account for this occurrence. Therefore, the interest expense reported on the income statement is the amount of interest expense, net of tax, added back to net income. (It is not the interest paid in cash during the period.)

In addition, the conversion rate on a dilutive security may change during the period in which the security is outstanding. For the diluted EPS computation in such a situation, the company uses the most dilutive conversion rate available. For example, assume that a company issued a convertible bond on January 1, 2013, with a conversion rate of 10 common shares for each bond starting January 1, 2015. Beginning January 1, 2018, the conversion rate is 12 common shares for each bond, and beginning January 1, 2022, it is 15 common shares for each bond. In computing diluted EPS in 2013, the company uses the conversion rate of 15 shares to one bond.

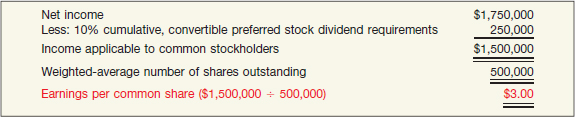

A final issue relates to preferred stock. For example, assume that Mayfield's 6 percent convertible debentures were instead 6 percent convertible preferred stock. In that case, Mayfield considers the convertible preferred as potential common shares. Thus, it includes them in its diluted EPS calculations as shares outstanding. The company does not subtract preferred dividends from net income in computing the numerator. Why not? Because for purposes of computing EPS, it assumes conversion of the convertible preferreds to outstanding common stock. The company uses net income as the numerator—it computes no tax effect because preferred dividends generally are not tax-deductible.

Diluted EPS—Options and Warrants

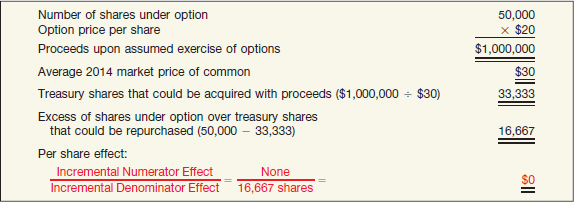

A company includes in diluted earnings per share stock options and warrants outstanding (whether or not presently exercisable), unless they are antidilutive. Companies use the treasury-stock method to include options and warrants and their equivalents in EPS computations.

The treasury-stock method assumes that the options or warrants are exercised at the beginning of the year (or date of issue if later), and that the company uses those proceeds to purchase common stock for the treasury. If the exercise price is lower than the market price of the stock, then the proceeds from exercise are insufficient to buy back all the shares. The company then adds the incremental shares remaining to the weighted-average number of shares outstanding for purposes of computing diluted earnings per share.

For example, if the exercise price of a warrant is $5 and the market price of the stock is $15, the treasury-stock method increases the shares outstanding. Exercise of the warrant results in one additional share outstanding, but the $5 received for the one share issued is insufficient to purchase one share in the market at $15. The company needs to exercise three warrants (and issue three additional shares) to produce enough money ($15) to acquire one share in the market. Thus, a net increase of two shares outstanding results.

To see this computation using larger numbers, assume 1,500 options outstanding at an exercise price of $30 for a common share and a common stock market price per share of $50. Through application of the treasury-stock method, the company would have 600 incremental shares outstanding, computed as shown in Illustration 16-21.17

Thus, if the exercise price of the option or warrant is lower than the market price of the stock, dilution occurs. An exercise price of the option or warrant higher than the market price of the stock reduces common shares. In this case, the options or warrants are antidilutive because their assumed exercise leads to an increase in earnings per share.

For both options and warrants, exercise is assumed only if the average market price of the stock exceeds the exercise price during the reported period.18 As a practical matter, a simple average of the weekly or monthly prices is adequate, so long as the prices do not fluctuate significantly.

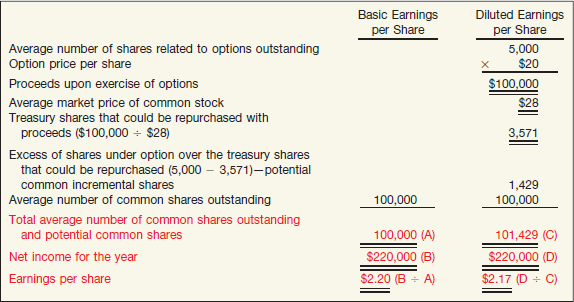

Comprehensive Example—Treasury-Stock Method. To illustrate application of the treasury-stock method, assume that Kubitz Industries, Inc. has net income for the period of $220,000. The average number of shares outstanding for the period was 100,000 shares. Hence, basic EPS—ignoring all dilutive securities—is $2.20. The average number of shares related to options outstanding (although not exercisable at this time), at an option price of $20 per share, is 5,000 shares. The average market price of the common stock during the year was $28. Illustration 16-22 shows the computation of EPS using the treasury-stock method.

Contingent Issue Agreement

In business combinations, the acquirer may promise to issue additional shares—referred to as contingent shares—under certain conditions. Sometimes the company issues these contingent shares as a result of a passage-of-time condition or upon the attainment of a certain earnings or market price level. If this passage-of-time condition occurs during the current year, or if the company meets the earnings or market price by the end of the year, the company considers the contingent shares as outstanding for the computation of diluted earnings per share.19

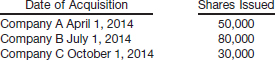

For example, assume that Watts Corporation purchased Cardoza Company and agreed to give Cardoza's stockholders 20,000 additional shares in 2017 if Cardoza's net income in 2016 is $90,000. In 2015, Cardoza's net income is $100,000. Because Cardoza has already attained the 2016 stipulated earnings of $90,000, in computing diluted earnings per share for 2015, Watts would include the 20,000 contingent shares in the shares-outstanding computation.

Antidilution Revisited

In computing diluted EPS, a company must consider the aggregate of all dilutive securities. But first it must determine which potentially dilutive securities are in fact individually dilutive and which are antidilutive. A company should exclude any security that is antidilutive, nor can the company use such a security to offset dilutive securities.

Recall that including antidilutive securities in earnings per share computations increases earnings per share (or reduces net loss per share). With options or warrants, whenever the exercise price exceeds the market price, the security is antidilutive. Convertible debt is antidilutive if the addition to income of the interest (net of tax) causes a greater percentage increase in income (numerator) than conversion of the bonds causes a percentage increase in common and potentially dilutive shares (denominator). In other words, convertible debt is antidilutive if conversion of the security causes common stock earnings to increase by a greater amount per additional common share than earnings per share was before the conversion.

To illustrate, assume that Martin Corporation has a 6 percent, $1,000,000 debt issue that is convertible into 10,000 common shares. Net income for the year is $210,000, the weighted-average number of common shares outstanding is 100,000 shares, and the tax rate is 40 percent. In this case, assumed conversion of the debt into common stock at the beginning of the year requires the following adjustments of net income and the weighted-average number of shares outstanding.

As a shortcut, Martin can also identify the convertible debt as antidilutive by comparing the EPS resulting from conversion, $3.60 ($36,000 additional earnings ÷ 10,000 additional shares), with EPS before inclusion of the convertible debt, $2.10.

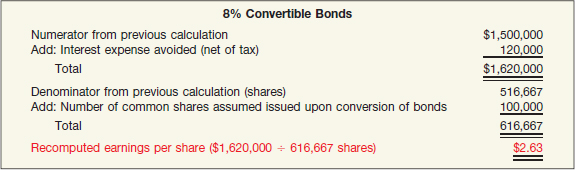

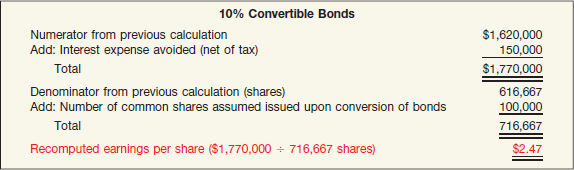

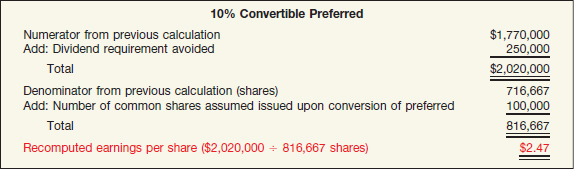

Companies should ignore antidilutive securities in all calculations and in computing diluted earnings per share. This approach is reasonable. The profession's intent was to inform the investor of the possible dilution that might occur in reported earnings per share and not to be concerned with securities that, if converted or exercised, would result in an increase in earnings per share. Appendix 16B to this chapter provides an extended example of how companies consider antidilution in a complex situation with multiple securities.

EPS Presentation and Disclosure

A company with a complex capital structure would present its EPS information as follows.

When the earnings of a period include irregular items, a company should show per share amounts (where applicable) for the following: income from continuing operations, income before extraordinary items, and net income. Companies that report a discontinued operation or an extraordinary item should present per share amounts for those line items either on the face of the income statement or in the notes to the financial statements. Illustration 16-25 (page 910) shows a presentation reporting extraordinary items.

A company must show earnings per share amounts for all periods presented. Also, the company should restate all prior period earnings per share amounts presented for stock dividends and stock splits. If it reports diluted EPS data for at least one period, the company should report such data for all periods presented, even if it is the same as basic EPS. When a company restates results of operations of a prior period as a result of an error or a change in accounting principle, it should also restate the earnings per share data shown for the prior periods. Complex capital structures and dual presentation of earnings per share require the following additional disclosures in note form.

- Description of pertinent rights and privileges of the various securities outstanding.

- A reconciliation of the numerators and denominators of the basic and diluted per share computations, including individual income and share amount effects of all securities that affect EPS.

- The effect given preferred dividends in determining income available to common stockholders in computing basic EPS.

- Securities that could potentially dilute basic EPS in the future that were excluded in the computation because they would be antidilutive.

- Effect of conversions subsequent to year-end, but before issuing statements.

Illustration 16-26 presents the reconciliation and the related disclosure to meet the requirements of this standard.20 [7]

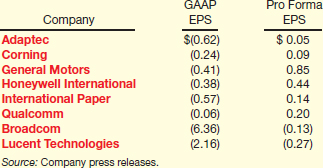

What do the numbers mean? PRO FORMA EPS CONFUSION

Many companies are reporting pro forma EPS numbers along with GAAP-based EPS numbers in the financial information provided to investors. Pro forma earnings generally exceed GAAP earnings because the pro forma numbers exclude such items as restructuring charges, impairments of assets, R&D expenditures, and stock compensation expense. Here are some examples.

Another case of possibly misleading pro forma reporting is the case of social media darlings Facebook, Zynga, and Groupon. For example, social gaming company Zynga recently reported so much stock-compensation expense ($600 million) that it overwhelmed its operating profit; these expenses took operating profit negative to the tune of $406 million. The accounting? Zynga “window dressed” the expense by encouraging Wall Street analysts to use a non-GAAP pro forma accounting figure—“adjusted earnings before interest, taxes, depreciation and amortization”—that ignores the stock compensation. LinkedIn and Groupon also use non-GAAP metrics that exclude stock compensation. LinkedIn's $30 million stock-compensation expense roughly halved its operating profit, while Groupon's $94 million took operating profit $203 million into the red. Wall Street analysts tend to go along with the accounting hocus-pocus, as it allows them to justify higher valuations for stocks. Investors should remember, however, that employee equity awards are real costs.

As discussed in Chapter 4, SEC Regulation G requires companies to provide a clear reconciliation between pro forma and GAAP information. And this applies to EPS measures as well. This reconciliation is especially important, given the spike in pro forma reporting by companies adding back employee stock-option expense.

Sources: See M. Moran, A. J. Cohen, and K. Shaustyuk, “Stock Option Expensing: The Battle Has Been Won; Now Comes the Aftermath,” Portfolio Strategy/Accounting, Goldman Sachs (March 17, 2005); and R. Winkler, “Stock and Awe at Facebook and Zynga,” Wall Street Journal (February 16, 2012).

Summary of EPS Computation

As you can see, computation of earnings per share is a complex issue. It is a controversial area because many securities, although technically not common stock, have many of its basic characteristics. Indeed, some companies have issued these other securities rather than common stock in order to avoid an adverse dilutive effect on earnings per share. Illustrations 16-27 and 16-28 (page 912) display the elementary points of calculating earnings per share in a simple capital structure and in a complex capital structure.

KEY TERMS

antidilutive securities, 904

basic EPS, 904

complex capital structure, 900

convertible bonds, 884

convertible preferred stock, 886

detachable stock warrants, 888

diluted EPS, 904

dilutive securities, 884, 904

earnings per share, 899

fair value method, 892

grant date, 892

if-converted method, 905

income available to common stockholders, 900

incremental method, 889

induced conversion, 885

intrinsic-value method, 892

proportional method, 888

restricted-stock plans, 894

service period, 893

simple capital structure, 900

stock option, 891

stock-based compensation plans, 891

stock right, 890

treasury-stock method, 907

warrants, 887

weighted-average number of shares outstanding, 901

SUMMARY OF LEARNING OBJECTIVES

![]() Describe the accounting for the issuance, conversion, and retirement of convertible securities. The method for recording convertible bonds at the date of issuance follows that used to record straight debt issues. Companies amortize any discount or premium that results from the issuance of convertible bonds, assuming the bonds will be held to maturity. If companies convert bonds into other securities, the principal accounting problem is to determine the amount at which to record the securities exchanged for the bonds. The book value method is considered GAAP. The retirement of convertible debt is considered a debt retirement, and the difference between the carrying amount of the retired convertible debt and the cash paid should result in a gain or loss.