CHAPTER 23 Statement of Cash Flows

LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Describe the purpose of the statement of cash flows.

- Identify the major classifications of cash flows.

- Prepare a statement of cash flows.

- Differentiate between net income and net cash flow from operating activities.

- Determine net cash flows from investing and financing activities.

- Identify sources of information for a statement of cash flows.

- Contrast the direct and indirect methods of calculating net cash flow from operating activities.

- Discuss special problems in preparing a statement of cash flows.

- Explain the use of a worksheet in preparing a statement of cash flows.

Show Me the Money!

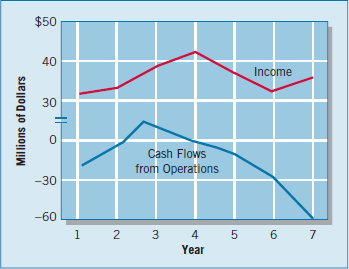

Investors usually look to net income as a key indicator of a company's financial health and future prospects. The following graph shows the net income of one company over a seven-year period.

The company showed a pattern of consistent profitability and even some periods of income growth. Between years 1 and 4, net income for this company grew by 32 percent, from $31 million to $41 million. Would you expect its profitability to continue? The company had consistently paid dividends and interest. Would you expect it to continue to do so? Investors answered these questions by buying the company's stock. Eighteen months later, this company—W. T. Grant—filed for bankruptcy, in what was then the largest bankruptcy filing in the United States.

How could this happen? As indicated by the second line in the graph, the company had experienced several years of negative cash flow from its operations, even though it reported profits. How can a company have negative cash flows while reporting profits? The answer lays partly in the fact that W. T. Grant was having trouble collecting the receivables from its credit sales, causing cash flow to be less than net income. Investors who analyzed the cash flows would have been likely to find an early warning signal of W. T. Grant's operating problems.

![]() CONCEPTUAL FOCUS

CONCEPTUAL FOCUS

- See the Underlying Concepts on pages 1412 and 1437.

- Read the Evolving Issue on page 1433 for a discussion of the direct versus indirect method.

![]() INTERNATIONAL FOCUS

INTERNATIONAL FOCUS

- See the International Perspectives on pages 1413, 1415, and 1434.

- Read the IFRS Insights on pages 1480–1485 for a discussion of:

- Significant non-cash transactions

- Special disclosures

Investors can also look to cash flow information to sniff out companies that can be good buys. As one analyst stated when it comes to valuing stocks: “Show me the money!” Here's the thinking behind that statement. Start with the “cash flows from operations” reported in the statement of cash flows, which (as you will learn in this chapter) consists of net income with non-cash charges (like depreciation and deferred taxes) added back and cash-draining events (like an inventory pile-up) taken out. Now subtract capital expenditures and dividends. What you're left with is free cash flow (as discussed in Chapter 5).

Many analysts like companies trading at low multiples of their free cash flow—low, that is, in relation to rivals today or the same company in past years. Why? They know that reported earnings can be misleading. Case in point: Computer-game firm Activision Blizzard reported net income of $113 million in a recent year. But it did better than that. It took in an additional $300 million, mostly for subscriptions to online multiplayer games. It gets the cash now but records the revenue only over time, as the subscriptions run out. A couple of investment houses put this stock on their buy list on the strength of its cash flows. So watch cash flow—to get an indicator of companies headed for trouble, as well as companies that may be undervalued.

Sources: Adapted from James A. Largay III and Clyde P. Stickney, “Cash Flows, Ratio Analysis, and the W. T. Grant Company Bankruptcy,” Financial Analysts Journal (July–August 1980), p. 51; and D. Fisher, “Cash Doesn't Lie,” Forbes (April 12, 2010), pp. 52–55.

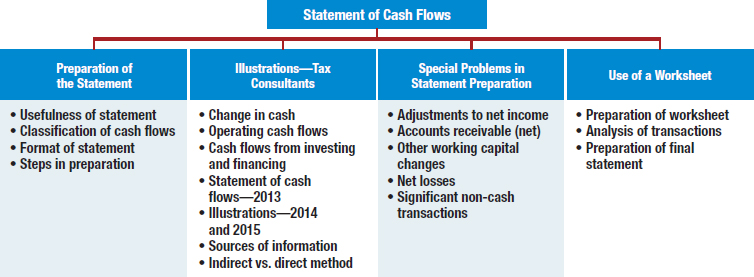

PREVIEW OF CHAPTER 23

As the opening story indicates, examination of W. T. Grant's cash flows from operations would have shown the financial inflexibility that eventually caused the company's bankruptcy. This chapter explains the main components of a statement of cash flows and the types of information it provides. The content and organization of the chapter are as follows.

PREPARATION OF THE STATEMENT OF CASH FLOWS

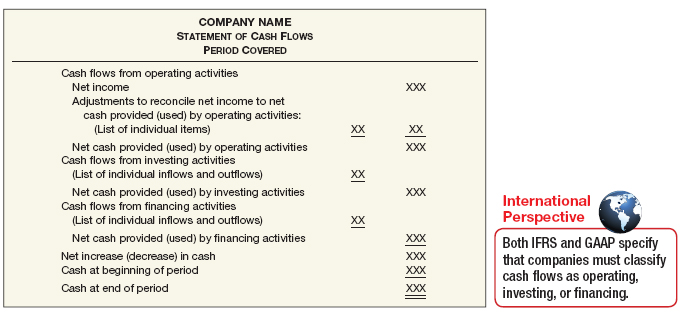

The primary purpose of the statement of cash flows is to provide information about a company's cash receipts and cash payments during a period. A secondary objective is to provide cash-basis information about the company's operating, investing, and financing activities. The statement of cash flows therefore reports cash receipts, cash payments, and net change in cash resulting from a company's operating, investing, and financing activities during a period. Its format reconciles the beginning and ending cash balances for the period.

Usefulness of the Statement of Cash Flows

![]() See the FASB Codification section (page 1454).

See the FASB Codification section (page 1454).

The statement of cash flows provides information to help investors, creditors, and others assess the following [1]:

![]() Underlying Concepts

Underlying Concepts

Reporting information in the statement of cash flows contributes to meeting the objective of financial reporting.

- The entity's ability to generate future cash flows. A primary objective of financial reporting is to provide information with which to predict the amounts, timing, and uncertainty of future cash flows. By examining relationships between items such as sales and net cash flow from operating activities, or net cash flow from operating activities and increases or decreases in cash, it is possible to better predict the future cash flows than is possible using accrual-basis data alone.

- The entity's ability to pay dividends and meet obligations. Simply put, cash is essential. Without adequate cash, a company cannot pay employees, settle debts, pay out dividends, or acquire equipment. A statement of cash flows indicates where the company's cash comes from and how the company uses its cash. Employees, creditors, stockholders, and customers should be particularly interested in this statement, because it alone shows the flows of cash in a business.

- The reasons for the difference between net income and net cash flow from operating activities. The net income number is important: It provides information on the performance of a company from one period to another. But some people are critical of accrual-basis net income because companies must make estimates to arrive at it. Such is not the case with cash. Thus, as the opening story showed, financial statement readers can benefit from knowing why a company's net income and net cash flow from operating activities differ, and can assess for themselves the reliability of the income number.

- The cash and noncash investing and financing transactions during the period. Besides operating activities, companies undertake investing and financing transactions. Investing activities include the purchase and sale of assets other than a company's products or services. Financing activities include borrowings and repayments of borrowings, investments by owners, and distributions to owners. By examining a company's investing and financing activities, a financial statement reader can better understand why assets and liabilities increased or decreased during the period. For example, by reading the statement of cash flows, the reader might find answers to the following questions:

- Why did cash decrease for Home Depot when it reported net income for the period?

- How much did Southwest Airlines spend on property, plant, and equipment last year?

- Did dividends paid by Campbell's Soup increase?

- How much money did Coca-Cola borrow last year?

- How much cash did Hewlett-Packard use to repurchase its common stock?

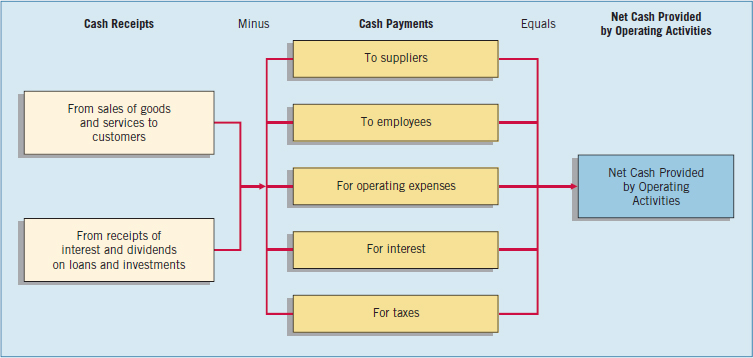

Classification of Cash Flows

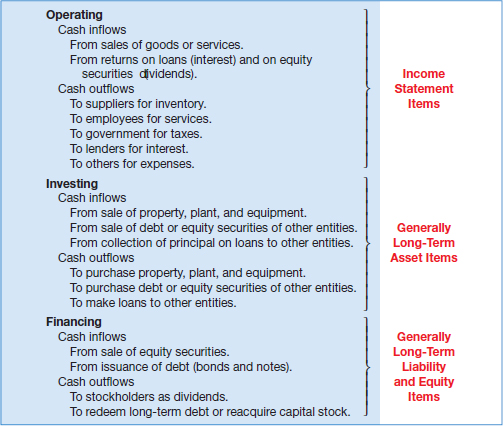

The statement of cash flows classifies cash receipts and cash payments by operating, investing, and financing activities.1 Transactions and other events characteristic of each kind of activity are as follows.

- Operating activities involve the cash effects of transactions that enter into the determination of net income, such as cash receipts from sales of goods and services, and cash payments to suppliers and employees for acquisitions of inventory and expenses.

- Investing activities generally involve long-term assets and include (a) making and collecting loans, and (b) acquiring and disposing of investments and productive long-lived assets.

- Financing activities involve liability and stockholders' equity items and include (a) obtaining cash from creditors and repaying the amounts borrowed, and (b) obtaining capital from owners and providing them with a return on, and a return of, their investment.

Illustration 23-1 classifies the typical cash receipts and payments of a company according to operating, investing, and financing activities. The operating activities category is the most important. It shows the cash provided by company operations. This source of cash is generally considered to be the best measure of a company's ability to generate enough cash to continue as a going concern.

![]() International Perspective

International Perspective

According to IFRS, companies can define “cash and cash equivalents” as “net monetary assets”—that is, as “cash and demand deposits and highly liquid investments less short-term borrowings.”

Note the following general guidelines about the classification of cash flows.

- Operating activities involve income statement items.

- Investing activities involve cash flows resulting from changes in investments and long-term asset items.

- Financing activities involve cash flows resulting from changes in long-term liability and stockholders' equity items.

Companies classify some cash flows relating to investing or financing activities as operating activities.2 For example, companies classify receipts of investment income (interest and dividends) and payments of interest to lenders as operating activities. Why are these considered operating activities? Companies report these items in the income statement, where the results of operations are shown.

Conversely, companies classify some cash flows relating to operating activities as investing or financing activities. For example, a company classifies the cash received from the sale of property, plant, and equipment at a gain, although reported in the income statement, as an investing activity. It excludes the effects of the related gain in net cash flow from operating activities. Likewise, a gain or loss on the payment (extinguishment) of debt is generally part of the cash outflow related to the repayment of the amount borrowed. It therefore is a financing activity.

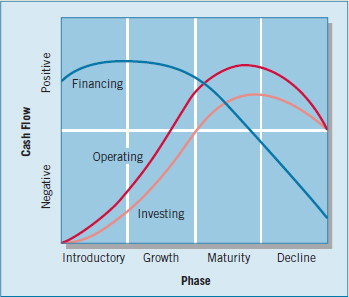

What do the numbers mean? HOW’S MY CASH FLOW?

To evaluate overall cash flow, it is useful to understand where in the product life cycle a company is. Generally, companies move through several stages of development, which have implications for cash flow. As the following graph shows, the pattern of cash flows from operating, financing, and investing activities will vary depending on the stage of the product life cycle.

In the introductory phase, the product is likely not generating much revenue (operating cash flow is negative). Because the company is making heavy investments to get a product off the ground, cash flow from investment is negative, and financing cash flows are positive.

As the product moves to the growth and maturity phases, these cash flow relationships reverse. The product generates more cash flow from operations, which can be used to cover investments needed to support the product, and less cash is needed from financing. So is a negative operating cash flow bad? Not always. It depends on the product life cycle.

Source: Adapted from Paul D. Kimmel, Jerry J. Weygandt, and Donald E. Kieso, Financial Accounting: Tools for Business Decision Making, 6th ed. (New York: John Wiley & Sons, 2011), p. 628.

Format of the Statement of Cash Flows

The three activities we discussed above constitute the general format of the statement of cash flows. The operating activities section always appears first. It is followed by the investing activities section and then the financing activities section.

A company reports the individual inflows and outflows from investing and financing activities separately. That is, a company reports them gross, not netted against one another. Thus, a cash outflow from the purchase of property is reported separately from the cash inflow from the sale of property. Similarly, a cash inflow from the issuance of debt is reported separately from the cash outflow from its retirement.

The net increase or decrease in cash reported during the period should reconcile the beginning and ending cash balances as reported in the comparative balance sheets. The general format of the statement of cash flows presents the results of the three activities discussed previously–operating, investing, and financing. Illustration 23-2 shows a widely used form of the statement of cash flows.

Steps in Preparation

Companies prepare the statement of cash flows differently from the three other basic financial statements. For one thing, it is not prepared from an adjusted trial balance. The cash flow statement requires detailed information concerning the changes in account balances that occurred between two points in time. An adjusted trial balance will not provide the necessary data. Second, the statement of cash flows deals with cash receipts and payments. As a result, the company must adjust the effects of the use of accrual accounting to determine cash flows. The information to prepare this statement usually comes from three sources:

- Comparative balance sheets provide the amount of the changes in assets, liabilities, and equities from the beginning to the end of the period.

- Current income statement data help determine the amount of cash provided by or used by operations during the period.

- Selected transaction data from the general ledger provide additional detailed information needed to determine how the company provided or used cash during the period.

Preparing the statement of cash flows from the data sources above involves three major steps:

Step 1. Determine the change in cash. This procedure is straightforward. A company can easily compute the difference between the beginning and the ending cash balance from examining its comparative balance sheets.

Step 2. Determine the net cash flow from operating activities. This procedure is complex. It involves analyzing not only the current year's income statement but also comparative balance sheets as well as selected transaction data.

Step 3. Determine net cash flows from investing and financing activities. A company must analyze all other changes in the balance sheet accounts to determine their effects on cash.

On the following pages, we work through these three steps in the process of preparing the statement of cash flows for Tax Consultants Inc. over several years.

ILLUSTRATIONS—TAX CONSULTANTS INC.

LEARNING OBJECTIVE ![]()

Prepare a statement of cash flows.

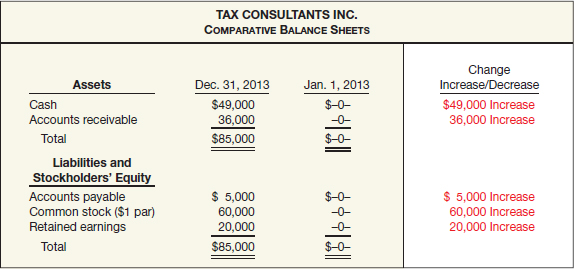

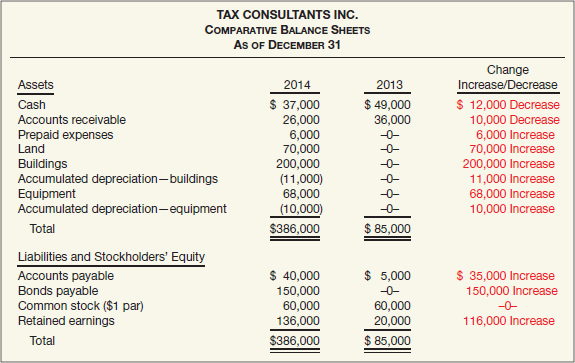

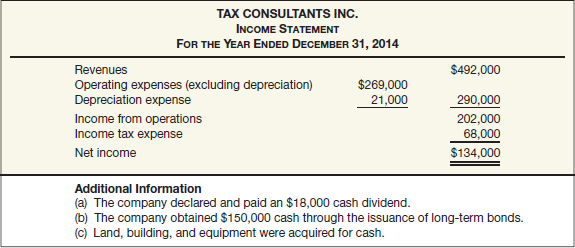

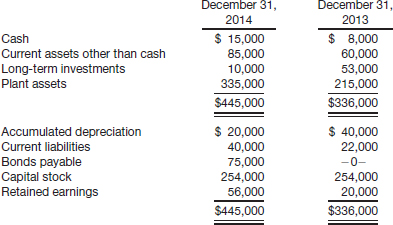

We show the steps in preparing the statement of cash flows using data for Tax Consultants Inc. To begin, we use the first year of operations for Tax Consultants Inc. The company started on January 1, 2013, when it issued 60,000 shares of $1 par value common stock for $60,000 cash. The company rented its office space, furniture, and equipment, and performed tax consulting services throughout the first year. The comparative balance sheets at the beginning and end of the year 2013 appear in Illustration 23-3.

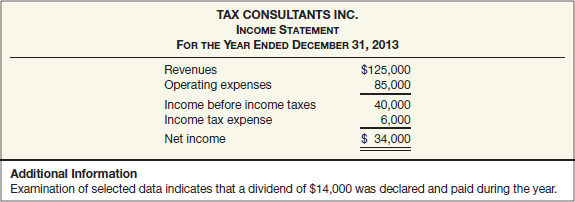

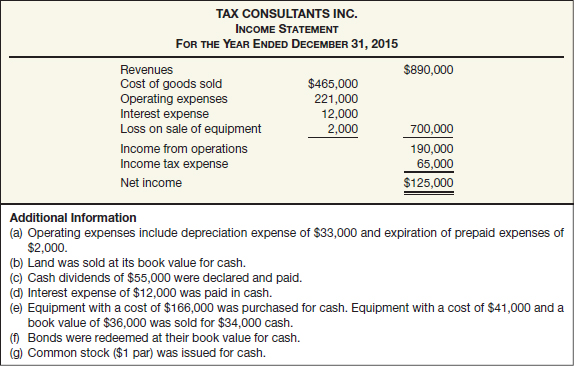

Illustration 23-4 shows the income statement and additional information for Tax Consultants.

Step 1: Determine the Change in Cash

To prepare a statement of cash flows, the first step is to determine the change in cash. This is a simple computation. Tax Consultants had no cash on hand at the beginning of the year 2013. It had $49,000 on hand at the end of 2013. Thus, cash changed (increased) in 2013 by $49,000.

Step 2: Determine Net Cash Flow from Operating Activities

LEARNING OBJECTIVE ![]()

Differentiate between net income and net cash flow from operating activities.

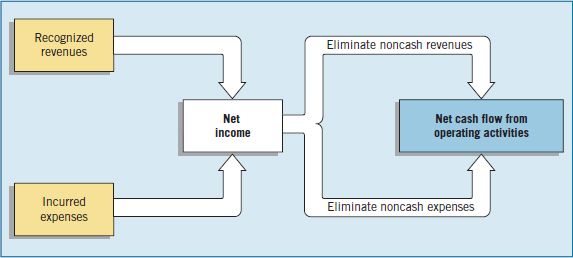

To determine net cash flow from operating activities,3 companies adjust net income in numerous ways. A useful starting point is to understand why net income must be converted to net cash provided by operating activities.

Under generally accepted accounting principles, most companies use the accrual basis of accounting. As you have learned, this basis requires that companies record revenue when a performance obligation is met and record expenses when incurred. Revenues may include credit sales for which the company has not yet collected cash. Expenses incurred may include some items that the company has not yet paid in cash. Thus, under the accrual basis of accounting, net income is not the same as net cash flow from operating activities.

To arrive at net cash flow from operating activities, a company must determine revenues and expenses on a cash basis. It does this by eliminating the effects of income statement transactions that do not result in an increase or decrease in cash. Illustration 23-5 shows the relationship between net income and net cash flow from operating activities.

In this chapter, we use the term net income to refer to accrual-based net income. A company may convert net income to net cash flow from operating activities through either a direct method or an indirect method. Due to its widespread use in practice, in the following sections we illustrate use of the indirect method. Later in the chapter, we describe the direct method and discuss the advantages and disadvantages of the two methods.4

The indirect method (or reconciliation method) starts with net income and converts it to net cash flow from operating activities. In other words, the indirect method adjusts net income for items that affected reported net income but did not affect cash. To compute net cash flow from operating activities, a company adds back noncash charges in the income statement to net income and deducts noncash credits. We explain the two adjustments to net income for Tax Consultants, namely, the increases in accounts receivable and accounts payable, as follows.

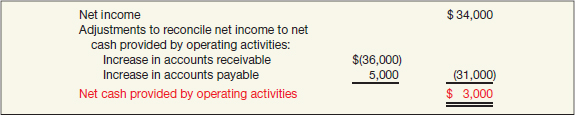

Increase in Accounts Receivable—Indirect Method

Tax Consultants' accounts receivable increased by $36,000 (from $0 to $36,000) during the year. For Tax Consultants, this means that cash receipts were $36,000 lower than revenues. The Accounts Receivable account in Illustration 23-6 shows that Tax Consultants had $125,000 in revenues (as reported on the income statement), but it collected only $89,000 in cash.

As shown in Illustration 23-7, to adjust net income to net cash provided by operating activities, Tax Consultants must deduct the increase of $36,000 in accounts receivable from net income. When the Accounts Receivable balance decreases, cash receipts are higher than revenue recognized under the accrual basis. Therefore, the company adds to net income the amount of the decrease in accounts receivable to arrive at net cash provided by operating activities.

Increase in Accounts Payable—Indirect Method

When accounts payable increase during the year, expenses on an accrual basis exceed those on a cash basis. Why? Because Tax Consultants incurred expenses, but some of the expenses are not yet paid. To convert net income to net cash flow from operating activities, Tax Consultants must add back the increase of $5,000 in accounts payable to net income.

As a result of the accounts receivable and accounts payable adjustments, Tax Consultants determines net cash provided by operating activities is $3,000 for the year 2013. Illustration 23-7 shows this computation.

What do the numbers mean? EARNINGS AND CASH FLOW MANAGEMENT?

Investors must be vigilant in their monitoring of management incentives to manipulate both earnings and cash flows. That is, financial success is dependent not only on a company's ability to generate revenues and earnings, but also cash flow. A company that shows profits but is unable to generate cash will also experience waning investor enthusiasm.

Thus, management has an incentive to make operating cash flow look good because Wall Street has paid a premium for companies that generate a lot of cash from operations, rather than through borrowings. However, similar to earnings, companies have ways to pump up cash flow from operations.

One way that companies can boost their operating cash flow is by “securitizing” receivables. That is, companies can speed up cash collections by selling their receivables. For example, Federated Department Stores reported a $2.2 billion increase in cash flow from operations. This seems impressive until you read the fine print, which indicates that a big part of the increase was due to the sale of receivables. As discussed in this section, decreases in accounts receivable increase cash flow from operations. So while it appeared that Federated's core operations had improved, the company really did little more than accelerate collections of its receivables. In fact, the cash flow from the securitizations represented more than half of Federated's operating cash flow.

Similarly, companies may time the recognition of noncash gains to mask cash flow problems. Take the example of Chesapeake Energy Corp. In a recent quarter, Chesapeake, the second-largest U.S. gas producer, reported a $929 million net profit, nearly double from a year earlier. These results seem pretty good until you take a closer look. Falling commodity prices for natural gas resulted in a 45 percent decrease in Chesapeake's operating cash flow. To plug the hole in its bottom line, the company sold pipeline assets. As a result, all but $3 million of its net income came from these sales and other noncash gains. Thus, in evaluating the quality of accounting, investors must keep an eye on the quality of earnings and cash flows.

Source: Adapted from Ann Tergesen, “Cash Flow Hocus Pocus,” BusinessWeek (July 16, 2002), pp. 130–131. See also C. Mulford and A. Lopez de Mesa, Cash Flow Trends and Their Fundamental Drivers: Comprehensive Industry Review, Georgia Tech Financial Analysis Lab (October 2, 2012); and D. Gilbert, “Chesapeake Plans Increase in Asset Sales as Net Rises,” Wall Street Journal (August 6, 2012).

Step 3: Determine Net Cash Flows from Investing and Financing Activities

LEARNING OBJECTIVE ![]()

Determine net cash flows from investing and financing activities.

After Tax Consultants has computed the net cash provided by operating activities, the next step is to determine whether any other changes in balance sheet accounts caused an increase or decrease in cash.

For example, an examination of the remaining balance sheet accounts for Tax Consultants shows increases in both common stock and retained earnings. The common stock increase of $60,000 resulted from the issuance of common stock for cash. The issuance of common stock is reported in the statement of cash flows as a receipt of cash from a financing activity.

Two items caused the retained earnings increase of $20,000:

- Net income of $34,000 increased retained earnings.

- Declaration of $14,000 of dividends decreased retained earnings.

Tax Consultants has converted net income into net cash flow from operating activities, as explained earlier. The additional data indicate that it paid the dividend. Thus, the company reports the dividend payment as a cash outflow, classified as a financing activity.

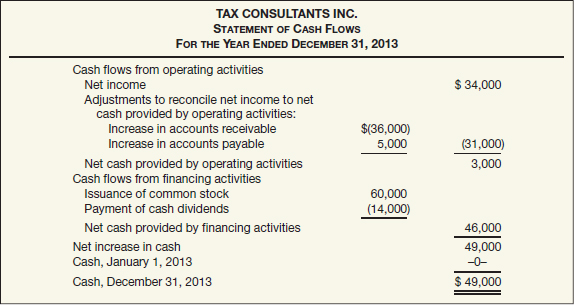

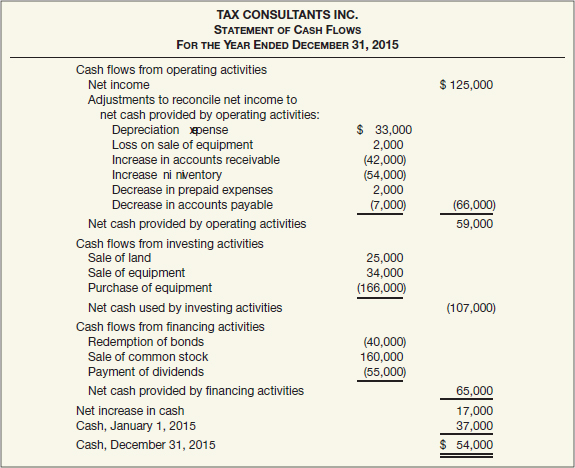

Statement of Cash Flows—2013

We are now ready to prepare the statement of cash flows. The statement starts with the operating activities section. Tax Consultants uses the indirect method to report net cash flow from operating activities.

Illustration 23-8 shows the statement of cash flows for Tax Consultants Inc., for year 1 (2013).

As indicated, the $60,000 increase in common stock results in a financing activity cash inflow. The payment of $14,000 in cash dividends is a financing activity outflow of cash. The $49,000 increase in cash reported in the statement of cash flows agrees with the increase of $49,000 shown in the comparative balance sheets as the change in the Cash account.

Illustration—2014

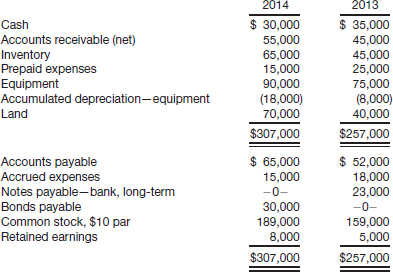

Tax Consultants Inc. continued to grow and prosper in its second year of operations. The company purchased land, building, and equipment, and revenues and net income increased substantially over the first year. Illustrations 23-9 and 23-10 present information related to the second year of operations for Tax Consultants Inc.

Step 1: Determine the Change in Cash

To prepare a statement of cash flows from the available information, the first step is to determine the change in cash. As indicated from the information presented, cash decreased $12,000 ($49,000 − $37,000).

Step 2: Determine Net Cash Flow from Operating Activities—Indirect Method

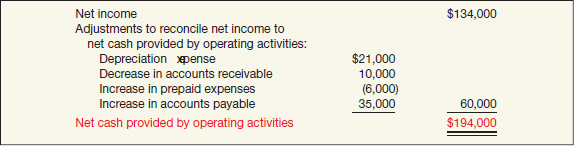

Using the indirect method, we adjust net income of $134,000 on an accrual basis to arrive at net cash flow from operating activities. Explanations for the adjustments to net income follow.

Decrease in Accounts Receivable. Accounts receivable decreased during the period because cash receipts (cash-basis revenues) are higher than revenues reported on an accrual basis. To convert net income to net cash flow from operating activities, the decrease of $10,000 in accounts receivable must be added to net income.

Increase in Prepaid Expenses. When prepaid expenses (assets) increase during a period, expenses on an accrual-basis income statement are lower than they are on a cash-basis income statement. The reason: Tax Consultants has made cash payments in the current period, but expenses (as charges to the income statement) have been deferred to future periods. To convert net income to net cash flow from operating activities, the company must deduct from net income the increase of $6,000 in prepaid expenses. An increase in prepaid expenses results in a decrease in cash during the period.

Increase in Accounts Payable. Like the increase in 2013, Tax Consultants must add the 2014 increase of $35,000 in accounts payable to net income, to convert to net cash flow from operating activities. The company incurred a greater amount of expense than the amount of cash it disbursed.

Depreciation Expense (Increase in Accumulated Depreciation). The purchase of depreciable assets is a use of cash, shown in the investing section in the year of acquisition. Tax Consultants' depreciation expense of $21,000 (also represented by the increase in accumulated depreciation) is a noncash charge; the company adds it back to net income, to arrive at net cash flow from operating activities. The $21,000 is the sum of the $11,000 depreciation on the building plus the $10,000 depreciation on the equipment.

Certain other periodic charges to expense do not require the use of cash. Examples are the amortization of intangible assets and depletion expense. Such charges are treated in the same manner as depreciation. Companies frequently list depreciation and similar noncash charges as the first adjustments to net income in the statement of cash flows.

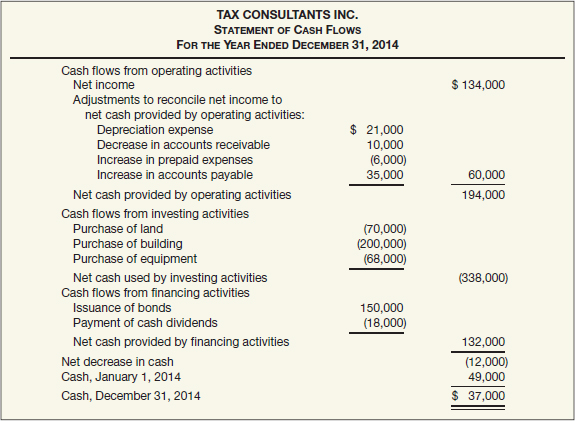

As a result of the foregoing items, net cash provided by operating activities is $194,000 as shown in Illustration 23-11.

Step 3: Determine Net Cash Flows from Investing and Financing Activities

After you have determined the items affecting net cash provided by operating activities, the next step involves analyzing the remaining changes in balance sheet accounts. Tax Consultants Inc. analyzed the following accounts.

Increase in Land. As indicated from the change in the Land account, the company purchased land of $70,000 during the period. This transaction is an investing activity, reported as a use of cash.

Increase in Buildings and Related Accumulated Depreciation. As indicated in the additional data and from the change in the Buildings account, Tax Consultants acquired an office building using $200,000 cash. This transaction is a cash outflow, reported in the investing section. The $11,000 increase in accumulated depreciation results from recording depreciation expense on the building. As indicated earlier, the reported depreciation expense has no effect on the amount of cash.

Increase in Equipment and Related Accumulated Depreciation. An increase in equipment of $68,000 resulted because the company used cash to purchase equipment. This transaction is an outflow of cash from an investing activity. The depreciation expense entry for the period explains the increase in Accumulated Depreciation—Equipment.

Increase in Bonds Payable. The Bonds Payable account increased $150,000. Cash received from the issuance of these bonds represents an inflow of cash from a financing activity.

Increase in Retained Earnings. Retained earnings increased $116,000 during the year. Two factors explain this increase. (1) Net income of $134,000 increased retained earnings, and (2) dividends of $18,000 decreased retained earnings. As indicated earlier, the company adjusts net income to net cash provided by operating activities in the operating activities section. Payment of the dividends is a financing activity that involves a cash outflow.

Statement of Cash Flows—2014

Combining the foregoing items, we get a statement of cash flows for 2014 for Tax Consultants Inc., using the indirect method to compute net cash flow from operating activities.

Illustration—2015

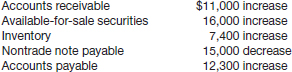

Our third example, covering the 2015 operations of Tax Consultants Inc., is more complex. It again uses the indirect method to compute and present net cash flow from operating activities.

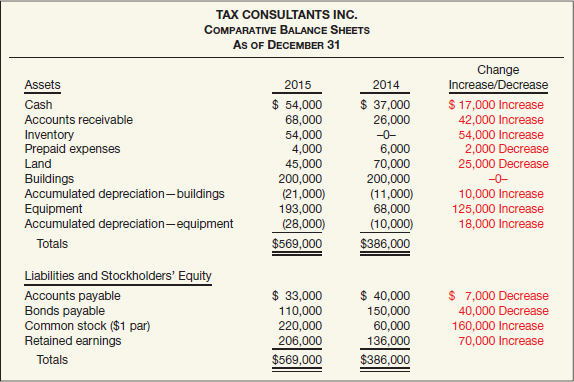

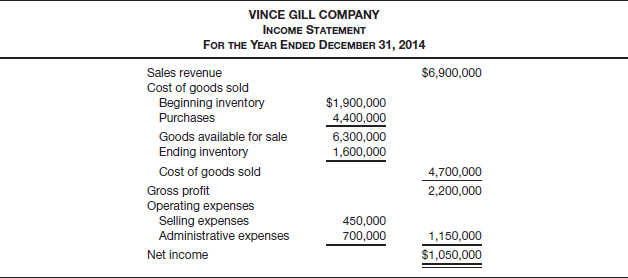

Tax Consultants Inc. experienced continued success in 2015 and expanded its operations to include the sale of computer software used in tax-return preparation and tax planning. Thus, inventory is a new asset appearing in the company's December 31, 2015, balance sheet. Illustrations 23-13 and 23-14 (on page 1424) show the comparative balance sheets, income statements, and selected data for 2015.

Step 1: Determine the Change in Cash

The first step in the preparation of the statement of cash flows is to determine the change in cash. As the comparative balance sheets show, cash increased $17,000 in 2015.

Step 2: Determine Net Cash Flow from Operating Activities—Indirect Method

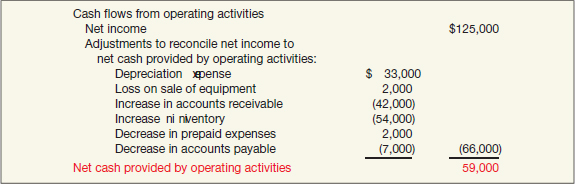

We explain the adjustments to net income of $125,000 as follows.

Increase in Accounts Receivable. The increase in accounts receivable of $42,000 represents recorded accrual-basis revenues in excess of cash collections in 2015. The company deducts this increase from net income to convert from the accrual basis to the cash basis.

Increase in Inventory. The $54,000 increase in inventory represents an operating use of cash, not an expense. Tax Consultants therefore deducts this amount from net income, to arrive at net cash flow from operations. In other words, when inventory purchased exceeds inventory sold during a period, cost of goods sold on an accrual basis is lower than on a cash basis.

Decrease in Prepaid Expenses. The $2,000 decrease in prepaid expenses represents a charge to the income statement for which Tax Consultants made no cash payment in the current period. The company adds back the decrease to net income, to arrive at net cash flow from operating activities.

Decrease in Accounts Payable. When accounts payable decrease during the year, cost of goods sold and expenses on a cash basis are higher than they are on an accrual basis. To convert net income to net cash flow from operating activities, the company must deduct the $7,000 in accounts payable from net income.

Depreciation Expense (Increase in Accumulated Depreciation). Accumulated Depreciation—Buildings increased $10,000 ($21,000 − $11,000). The Buildings account did not change during the period, which means that Tax Consultants recorded depreciation expense of $10,000 in 2015.

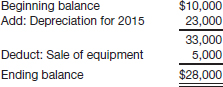

Accumulated Depreciation—Equipment increased by $18,000 ($28,000 − $10,000) during the year. But Accumulated Depreciation—Equipment decreased by $5,000 as a result of the sale during the year. Thus, depreciation for the year was $23,000. The company reconciled Accumulated Depreciation—Equipment as follows.

The company must add back to net income the total depreciation of $33,000 ($10,000 + $23,000) charged to the income statement, to determine net cash flow from operating activities.

Loss on Sale of Equipment. Tax Consultants Inc. sold for $34,000 equipment that cost $41,000 and had a book value of $36,000. As a result, the company reported a loss of $2,000 on its sale. To arrive at net cash flow from operating activities, it must add back to net income the loss on the sale of the equipment. The reason is that the loss is a noncash charge to the income statement. The loss did not reduce cash, but it did reduce net income.5

From the foregoing items, the company prepares the operating activities section of the statement of cash flows, as shown in Illustration 23-15.

Step 3: Determine Net Cash Flows from Investing and Financing Activities

By analyzing the remaining changes in the balance sheet accounts, Tax Consultants identifies cash flows from investing and financing activities.

Land. Land decreased $25,000 during the period. As indicated from the information presented, the company sold land for cash at its book value. This transaction is an investing activity, reported as a $25,000 source of cash.

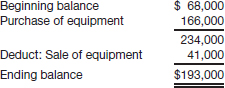

Equipment. An analysis of the Equipment account indicates the following.

The company used cash to purchase equipment with a fair value of $166,000—an investing transaction reported as a cash outflow. The sale of the equipment for $34,000 is also an investing activity, but one that generates a cash inflow.

Bonds Payable. Bonds payable decreased $40,000 during the year. As indicated from the additional information, the company redeemed the bonds at their book value. This financing transaction used $40,000 of cash.

Common Stock. The Common Stock account increased $160,000 during the year. As indicated from the additional information, Tax Consultants issued common stock of $160,000 at par. This financing transaction provided cash of $160,000.

Retained Earnings. Retained earnings changed $70,000 ($206,000 − $136,000) during the year. The $70,000 change in retained earnings results from net income of $125,000 from operations and the financing activity of paying cash dividends of $55,000.

Statement of Cash Flows—2015

Tax Consultants Inc. combines the foregoing items to prepare the statement of cash flows shown in Illustration 23-16.

Sources of Information for the Statement of Cash Flows

LEARNING OBJECTIVE ![]()

Identify sources of information for a statement of cash flows.

Important points to remember in the preparation of the statement of cash flows are these:

- Comparative balance sheets provide the basic information from which to prepare the report. Additional information obtained from analyses of specific accounts is also included.

- An analysis of the Retained Earnings account is necessary. The net increase or decrease in Retained Earnings without any explanation is a meaningless amount in the statement. Without explanation, it might represent the effect of net income, dividends declared, or prior period adjustments.

- The statement includes all changes that have passed through cash or have resulted in an increase or decrease in cash.

- Write-downs, amortization charges, and similar “book” entries, such as depreciation of plant assets, represent neither inflows nor outflows of cash because they have no effect on cash. To the extent that they have entered into the determination of net income, however, the company must add them back to or subtract them from net income, to arrive at net cash provided (used) by operating activities.

Indirect Method—Additional Adjustments

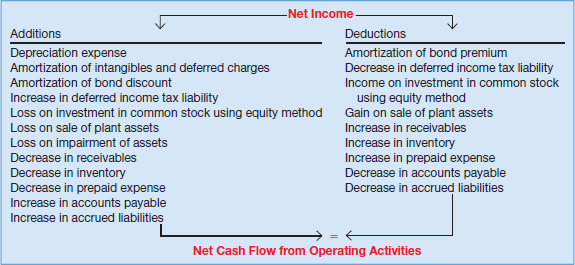

For consistency and comparability and because it is the most widely used method in practice, we used the indirect method in the Tax Consultants' illustrations. We determined net cash flow from operating activities by adding back to or deducting from net income those items that had no effect on cash. Illustration 23-17 presents a more complete set of common adjustments that companies make to net income to arrive at net cash flow from operating activities.

ILLUSTRATION 23-17 Adjustments Needed to Determine Net Cash Flow from Operating Activities—Indirect Method

The additions and deductions in Illustration 23-17 reconcile net income to net cash flow from operating activities, illustrating why the indirect method is also called the reconciliation method.

Net Cash Flow from Operating Activities—Direct Method

LEARNING OBJECTIVE ![]()

Contrast the direct and indirect methods of calculating net cash flow from operating activities.

Two different methods are available to adjust income from operations on an accrual basis to net cash flow from operating activities. We showed the indirect method in the Tax Consultants' illustrations in the prior sections.

The direct method reports cash receipts and cash disbursements from operating activities. The difference between these two amounts is the net cash flow from operating activities. In other words, the direct method deducts operating cash disbursements from operating cash receipts. The direct method results in the presentation of a condensed cash receipts and cash disbursements statement.

As indicated from the accrual-based income statement (see Illustration 23-4 on page 1417), Tax Consultants reported revenues of $125,000. However, because the company's accounts receivable increased during 2013 by $36,000, the company collected only $89,000 ($125,000 − $36,000) in cash from these revenues. Similarly, Tax Consultants reported operating expenses of $85,000. However, accounts payable increased during the period by $5,000. Assuming that these payables relate to operating expenses, cash operating expenses were $80,000 ($85,000 − $5,000). Because no taxes payable exist at the end of the year, the company must have paid $6,000 income tax expense for 2013 in cash during the year. Tax Consultants computes net cash flow from operating activities as shown in Illustration 23-18.

“Net cash provided by operating activities” is the equivalent of cash basis net income. (“Net cash used by operating activities” is equivalent to cash basis net loss.)

The FASB encourages use of the direct method and permits use of the indirect method. Yet, if the direct method is used, the Board requires that companies provide in a separate schedule a reconciliation of net income to net cash flow from operating activities. Therefore, under either method, companies must prepare and report information from the indirect (reconciliation) method.

Direct Method—Expanded Example

Under the direct method, the statement of cash flows reports net cash flow from operating activities as major classes of operating cash receipts (e.g., cash collected from customers and cash received from interest and dividends) and cash disbursements (e.g., cash paid to suppliers for goods, to employees for services, to creditors for interest, and to government authorities for taxes).

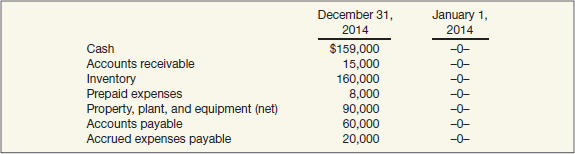

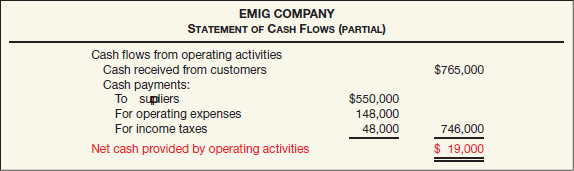

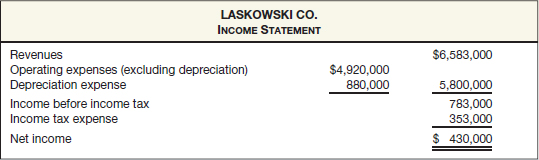

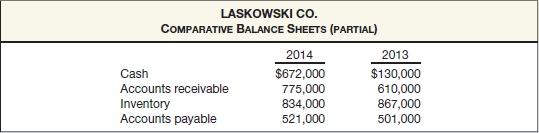

We illustrate the direct method here in more detail to help you understand the difference between accrual-based income and net cash flow from operating activities. This example also illustrates the data needed to apply the direct method. Emig Company, which began business on January 1, 2014, has the following selected balance sheet information.

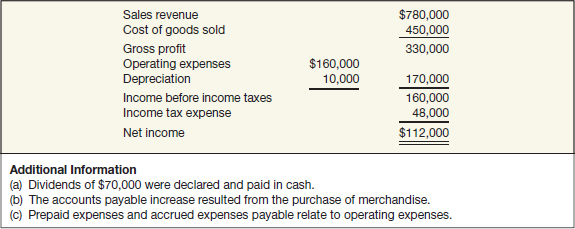

Emig Company's December 31, 2014, income statement and additional information are as follows.

Under the direct method, companies compute net cash provided by operating activities by adjusting each item in the income statement from the accrual basis to the cash basis. To simplify and condense the operating activities section, only major classes of operating cash receipts and cash payments are reported. As Illustration 23-21 shows, the difference between these major classes of cash receipts and cash payments is the net cash provided by operating activities.

An efficient way to apply the direct method is to analyze the revenues and expenses reported in the income statement in the order in which they are listed. The company then determines cash receipts and cash payments related to these revenues and expenses. In the following sections, we present the direct method adjustments for Emig Company in 2014, to determine net cash provided by operating activities.

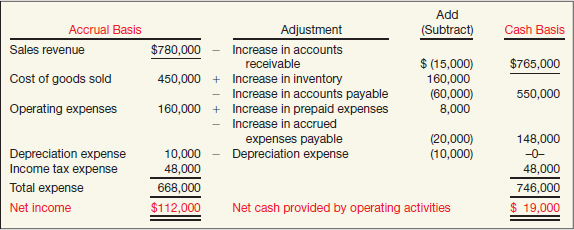

Cash Receipts from Customers. The income statement for Emig Company reported revenues from customers of $780,000. To determine cash receipts from customers, the company considers the change in accounts receivable during the year.

When accounts receivable increase during the year, revenues on an accrual basis are higher than cash receipts from customers. In other words, operations led to increased revenues, but not all of these revenues resulted in cash receipts. To determine the amount of increase in cash receipts, deduct the amount of the increase in accounts receivable from the total sales revenue. Conversely, a decrease in accounts receivable is added to sales revenue because cash receipts from customers then exceed sales revenue.

For Emig Company, accounts receivable increased $15,000. Thus, cash receipts from customers were $765,000, computed as follows.

Emig could also determine cash receipts from customers by analyzing the Accounts Receivable account as shown below.

Illustration 23-22 shows the relationships between cash receipts from customers, sales revenue, and changes in accounts receivable.

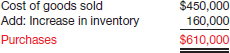

Cash Payments to Suppliers. Emig Company reported cost of goods sold on its income statement of $450,000. To determine cash payments to suppliers, the company first finds purchases for the year, by adjusting cost of goods sold for the change in inventory. When inventory increases during the year, purchases this year exceed cost of goods sold. As a result, the company adds the increase in inventory to cost of goods sold, to arrive at purchases.

In 2014, Emig Company's inventory increased $160,000. The company computes purchases as follows.

After computing purchases, Emig determines cash payments to suppliers by adjusting purchases for the change in accounts payable. When accounts payable increase during the year, purchases on an accrual basis are higher than they are on a cash basis. As a result, the company deducts from purchases the increase in accounts payable to arrive at cash payments to suppliers. Conversely, if cash payments to suppliers exceed purchases, Emig adds to purchases the decrease in accounts payable. Cash payments to suppliers were $550,000, computed as follows.

Emig also can determine cash payments to suppliers by analyzing Accounts Payable, as shown below.

Illustration 23-23 shows the relationships between cash payments to suppliers, cost of goods sold, changes in inventory, and changes in accounts payable.

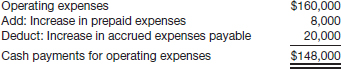

Cash Payments for Operating Expenses. Emig reported operating expenses of $160,000 on its income statement. To determine the cash paid for operating expenses, it must adjust this amount for any changes in prepaid expenses and accrued expenses payable.

For example, when prepaid expenses increased $8,000 during the year, cash paid for operating expenses was $8,000 higher than operating expenses reported on the income statement. To convert operating expenses to cash payments for operating expenses, the company adds to operating expenses the increase of $8,000. Conversely, if prepaid expenses decrease during the year, it deducts from operating expenses the amount of the decrease.

Emig also must adjust operating expenses for changes in accrued expenses payable. When accrued expenses payable increase during the year, operating expenses on an accrual basis are higher than they are on a cash basis. As a result, the company deducts from operating expenses an increase in accrued expenses payable, to arrive at cash payments for operating expenses. Conversely, it adds to operating expenses a decrease in accrued expenses payable, because cash payments exceed operating expenses.

Emig's cash payments for operating expenses were $148,000, computed as follows.

The relationships among cash payments for operating expenses, changes in prepaid expenses, and changes in accrued expenses payable are shown in Illustration 23-24 (page 1432).

Note that the company did not consider depreciation expense because it is a noncash charge.

Cash Payments for Income Taxes. The income statement for Emig shows income tax expense of $48,000. This amount equals the cash paid. How do we know that? Because the comparative balance sheet indicated no income taxes payable at either the beginning or end of the year.

Summary of Net Cash Flow from Operating Activities—Direct Method

The following schedule summarizes the computations illustrated above.

Illustration 23-26 shows the presentation of the direct method for reporting net cash flow from operating activities for the Emig Company illustration.

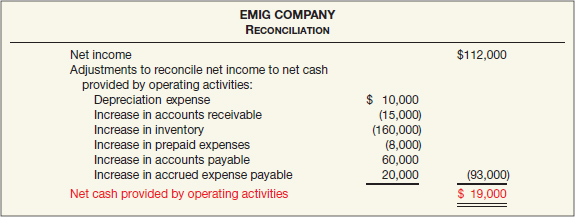

If Emig Company uses the direct method to present the net cash flow from operating activities, it must provide in a separate schedule the reconciliation of net income to net cash provided by operating activities. The reconciliation assumes the identical form and content of the indirect method of presentation, as the following shows.

When the direct method is used, the company may present this reconciliation at the bottom of the statement of cash flows or in a separate schedule.

Evolving Issue DIRECT VERSUS INDIRECT

Evolving Issue DIRECT VERSUS INDIRECT

The most contentious decision that the FASB faced related to cash flow reporting was choosing between the direct method and the indirect method of determining net cash flow from operating activities. Companies lobbied against the direct method, urging adoption of the indirect method. Commercial lending officers expressed to the FASB a strong preference in favor of the direct method. What are the arguments in favor of each of the methods?

In Favor of the Direct Method

The principal advantage of the direct method is that it shows operating cash receipts and payments. Thus, it is more consistent with the objective of a statement of cash flows—to provide information about cash receipts and cash payments—than the indirect method, which does not report operating cash receipts and payments.

Supporters of the direct method contend that knowledge of the specific sources of operating cash receipts and the purposes for which operating cash payments were made in past periods is useful in estimating future operating cash flows. Furthermore, information about amounts of major classes of operating cash receipts and payments is more useful than information only about their arithmetic sum (the net cash flow from operating activities). Such information is more revealing of a company's ability (1) to generate sufficient cash from operating activities to pay its debts, (2) to reinvest in its operations, and (3) to make distributions to its owners. [3]

Many companies indicate that they do not currently collect information in a manner that allows them to determine amounts such as cash received from customers or cash paid to suppliers directly from their accounting systems. But supporters of the direct method contend that the incremental cost of determining operating cash receipts and payments is not significant.

In Favor of the Indirect Method

The principal advantage of the indirect method is that it focuses on the differences between net income and net cash flow from operating activities. That is, it provides a useful link between the statement of cash flows and the income statement and balance sheet.

Many companies contend that it is less costly to adjust net income to net cash flow from operating activities (indirect) than it is to report gross operating cash receipts and payments (direct). Supporters of the indirect method also state that the direct method, which effectively reports income statement information on a cash rather than an accrual basis, may erroneously suggest that net cash flow from operating activities is as good as, or better than, net income as a measure of performance.

In their joint financial statement presentation project, the FASB and the IASB have proposed to allow only the direct method. However, there has been significant pushback on this proposal, which suggests that the choice of either the direct or indirect method will continue to be available.

Source: See http://www.fasb.org; click on Projects and then on Inactive Joint FASB/IASB Projects

Special Reporting Rules Applying to Direct and Indirect Methods

Companies that use the direct method are required, at a minimum, to report separately the following classes of operating cash receipts and payments:

![]() International Perspective

International Perspective

Consolidated statements of cash flows may be of limited use to analysts evaluating multinational companies. Without disaggregation, users of such statements are not able to determine “where in the world” the funds are sourced and used.

Receipts

- Cash collected from customers (including lessees, licensees, etc.).

- Interest and dividends received.

- Other operating cash receipts, if any.

Payments

- Cash paid to employees and suppliers of goods or services (including suppliers of insurance, advertising, etc.).

- Interest paid.

- Income taxes paid.

- Other operating cash payments, if any.

The FASB encourages companies to provide further breakdowns of operating cash receipts and payments that they consider meaningful.

Companies using the indirect method must disclose separately changes in inventory, receivables, and payables in order to reconcile net income to net cash flow from operating activities. In addition, they must disclose, elsewhere in the financial statements or in accompanying notes, interest paid (net of amount capitalized) and income taxes paid.6 The FASB requires these separate and additional disclosures so that users may approximate the direct method. Also, an acceptable alternative presentation of the indirect method is to report net cash flow from operating activities as a single line item in the statement of cash flows and to present the reconciliation details elsewhere in the financial statements.

Finally, the FASB encourages the use of the direct method over the indirect method. If a company uses the direct method of reporting net cash flow from operating activities, the FASB requires that the company provide in a separate schedule a reconciliation of net income to net cash flow from operating activities. If a company uses the indirect method, it can either report the reconciliation within the statement of cash flows or can provide it in a separate schedule, with the statement of cash flows reporting only the net cash flow from operating activities.[4]

SPECIAL PROBLEMS IN STATEMENT PREPARATION

LEARNING OBJECTIVE ![]()

Discuss special problems in preparing a statement of cash flows.

We discussed some of the special problems related to preparing the statement of cash flows in connection with the preceding illustrations. Other problems that arise with some frequency in the preparation of this statement include the following.

- Adjustments to net income.

- Accounts receivable (net).

- Other working capital changes.

- Net losses.

- Significant noncash transactions.

Adjustments to Net Income

Depreciation and Amortization

Depreciation expense is the most common adjustment to net income that companies make to arrive at net cash flow from operating activities. But there are numerous other noncash expense or revenue items. Examples of expense items that companies must add back to net income are the amortization of limited-life intangible assets such as patents, and the amortization of deferred costs such as bond issue costs. These charges to expense involve expenditures made in prior periods that a company amortizes currently. These charges reduce net income without affecting cash in the current period.

Also, amortization of bond discount or premium on long-term bonds payable affects the amount of interest expense. However, neither affects cash. As a result, a company should add back discount amortization and subtract premium amortization from net income to arrive at net cash flow from operating activities.

Postretirement Benefit Costs

If a company has postretirement costs such as an employee pension plan, chances are that the pension expense recorded during a period will either be higher or lower than the cash funded. It will be higher when there is an unfunded liability and will be lower when there is a pension asset. When the expense is higher or lower than the cash paid, the company must adjust net income by the difference between cash paid and the expense reported in computing net cash flow from operating activities.

Changes in Deferred Income Taxes

Changes in deferred income taxes affect net income but have no effect on cash. For example, Delta Airlines reported an increase in its liability for deferred taxes of approximately $1.2 billion. This change in the liability increased tax expense and decreased net income, but did not affect cash. Therefore, Delta added back $1.2 billion to net income on its statement of cash flows.

Equity Method of Accounting

Another common adjustment to net income is a change related to an investment in common stock when recording income or loss under the equity method. Recall that under the equity method, the investor (1) debits the investment account and credits revenue for its share of the investee's net income, and (2) credits dividends received to the investment account. Therefore, the net increase in the investment account does not affect cash flow. A company must deduct the net increase from net income to arrive at net cash flow from operating activities.

Assume that Victor Co. owns 40 percent of Milo Inc. During the year, Milo reports net income of $100,000 and pays a cash dividend of $30,000. Victor reports this in its statement of cash flows as a deduction from net income in the following manner—Equity in earnings of Milo, net of dividends, $28,000 [($100,000 − $30,000) × 40%].

Losses and Gains

Realized Losses and Gains. In the illustration for Tax Consultants, the company experienced a loss of $2,000 from the sale of equipment. The company added this loss to net income to compute net cash flow from operating activities because the loss is a noncash charge in the income statement.

If Tax Consultants experiences a gain from a sale of equipment, it too requires an adjustment to net income. Because a company reports the gain in the statement of cash flows as part of the cash proceeds from the sale of equipment under investing activities, it deducts the gain from net income to avoid double-counting—once as part of net income and again as part of the cash proceeds from the sale.

To illustrate, assume that Tax Consultants had land with a carrying value of $200,000, which was condemned by the state government for a highway project. The condemnation proceeds received were $205,000, resulting in a gain of $5,000. In the statement of cash flows (indirect method), the company would deduct the $5,000 gain from net income in the operating activities section. It would report the $205,000 cash inflow from the condemnation as an investing activity, as follows.

![]()

Unrealized Losses and Gains. Unrealized losses and gains generally occur for debt investments and for equity investments. For example, assume that Target purchases the following two investments on January 10, 2014.

- Debt investment for $1 million that is classified as trading. During 2014, the debt investment has an unrealized holding gain of $110,000 (recorded in net income).

- Equity investment for $600,000 that is classified as available-for-sale. During 2014, the available-for-sale equity investment has an unrealized holding loss of $50,000 (recorded in other comprehensive income).

For Target, the unrealized holding gain of $110,000 on the debt investment increases net income but does not increase net cash flow from operating activities. As a result, the unrealized holding gain of $110,000 is deducted from net income to compute net cash flow from operating activities.

On the other hand, the unrealized holding loss of $50,000 that Target incurs on the available-for-sale equity investment does not affect net income or cash flows—this loss is reported in the other comprehensive income section. As a result, no adjustment to net income is necessary in computing net cash flow from operating activities.

Thus, the general rule is that unrealized holding gains or losses that affect net income must be adjusted to determine net cash flow from operating activities. Conversely, unrealized holding gains or losses that do not affect net income are not adjusted to determine net cash flow from operating activities.

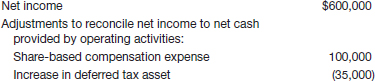

Stock Options

Recall for share-based compensation plans that companies are required to use the fair value method to determine total compensation cost. The compensation cost is then recognized as an expense in the periods in which the employee provides services. When Compensation Expense is debited, Paid-in Capital—Stock Options is often credited. Cash is not affected by recording the expense. Therefore, the company must increase net income by the amount of compensation expense from stock options in computing net cash flow from operating activities.

To illustrate how this information should be reported on a statement of cash flows, assume that First Wave Inc. grants 5,000 options to its CEO, Ann Johnson. Each option entitles Johnson to purchase one share of First Wave's $1 par value common stock at $50 per share at any time in the next two years (the service period). The fair value of the options is $200,000. First Wave records compensation expense in the first year as follows.

![]()

In addition, if we assume that First Wave has a 35 percent tax rate, it would recognize a deferred tax asset of $35,000 ($100,000 × 35%) in the first year as follows.

![]()

Therefore, on the statement of cash flows for the first year, First Wave reports the following (assuming a net income of $600,000).

As shown in First Wave's statement of cash flows, it adds the share-based compensation expense to net income because it is a noncash expense. The increase in the deferred tax asset and the related reduction in income tax expense increase net income. Although the negative income tax expense increases net income, it does not increase cash. Therefore, it should be deducted.

Subsequently, if Ann Johnson exercises her options, First Wave reports “Cash provided by exercise of stock options” in the financing section of the statement of cash flows.7

Extraordinary Items

Companies should report either as investing activities or as financing activities cash flows from extraordinary transactions and other events whose effects are included in net income, but which are not related to operations.

For example, assume that Tax Consultants had land with a carrying value of $200,000, which was condemned by the state of Maine for a highway project. The condemnation proceeds received were $205,000, resulting in an extraordinary gain of $5,000 less $2,000 of taxes. In the statement of cash flows (indirect method), the company would deduct the $5,000 gain from net income in the operating activities section. It would report the $205,000 cash inflow from the condemnation as an investing activity, as follows.

![]()

Note that Tax Consultants handles the gain at its gross amount ($5,000), not net of tax. The company reports the cash received in the condemnation as an investing activity at $205,000, also exclusive of the tax effect.

![]() Underlying Concepts

Underlying Concepts

By rejecting the requirement to allocate taxes to the various activities, the FASB invoked the cost constraint. The information would be beneficial, but the cost of providing such information would exceed the benefits of providing it.

The FASB requires companies to classify all income taxes paid as operating cash outflows. Some suggested that income taxes paid be allocated to investing and financing transactions. But the Board decided that allocation of income taxes paid to operating, investing, and financing activities would be so complex and arbitrary that the benefits, if any, would not justify the costs involved. Under both the direct method and the indirect method, companies must disclose the total amount of income taxes paid.8

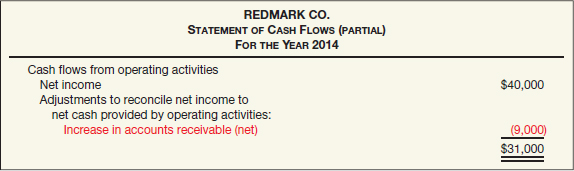

Accounts Receivable (Net)

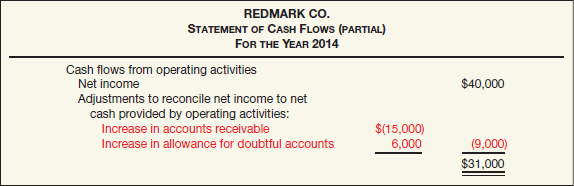

Up to this point, we assumed no allowance for doubtful accounts—a contra account—to offset accounts receivable. However, if a company needs an allowance for doubtful accounts, how does that allowance affect the company's determination of net cash flow from operating activities? For example, assume that Redmark Co. reports net income of $40,000. It has the accounts receivable balances as shown in Illustration 23-28.

Indirect Method

Because an increase in Allowance for Doubtful Accounts results from a charge to bad debt expense, a company should add back an increase in Allowance for Doubtful Accounts to net income to arrive at net cash flow from operating activities. Illustration 23-29 shows one method for presenting this information in a statement of cash flows.

As we indicated, the increase in the Allowance for Doubtful Accounts balance results from a charge to bad debt expense for the year. Because bad debt expense is a noncash charge, a company must add it back to net income in arriving at net cash flow from operating activities.

Instead of separately analyzing the allowance account, a short-cut approach is to net the allowance balance against the receivable balance and compare the change in accounts receivable on a net basis. Illustration 23-30 shows this presentation.

This short-cut procedure works also if the change in the allowance account results from a write-off of accounts receivable. This reduces both Accounts Receivable and Allowance for Doubtful Accounts. No effect on cash flows occurs. Because of its simplicity, use the net approach for your homework assignments.

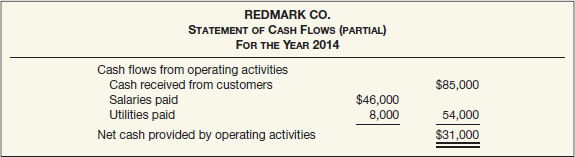

Direct Method

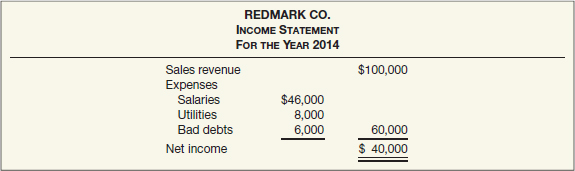

If using the direct method, a company should not net Allowance for Doubtful Accounts against Accounts Receivable. To illustrate, assume that Redmark Co.'s net income of $40,000 consisted of the items shown in Illustration 23-31.

If Redmark deducts the $9,000 increase in accounts receivable (net) from sales for the year, it would report cash sales at $91,000 ($100,000 − $9,000) and cash payments for operating expenses at $60,000. Both items would be misstated: Cash sales should be reported at $85,000 ($100,000 − $15,000), and total cash payments for operating expenses should be reported at $54,000 ($60,000 − $6,000). Illustration 23-32 shows the proper presentation.

An added complication develops when a company writes off accounts receivable. Simply adjusting sales for the change in accounts receivable will not provide the proper amount of cash sales. The reason is that the write-off of the accounts receivable is not a cash collection. Thus, an additional adjustment is necessary.

What do the numbers mean? NOT WHAT IT SEEMS

The controversy over direct and indirect methods highlights the importance that the market attributes to operating cash flow. By showing an improving cash flow, a company can give a favorable impression of its ongoing operations. For example, WorldCom concealed declines in its operations by capitalizing certain operating expenses—to the tune of $3.8 billion! This practice not only “juiced up” income but also made it possible to report the cash payments in the investing section of the cash flow statement rather than as a deduction from operating cash flow.

The SEC recently addressed a similar cash flow classification issue with automakers like Ford, GM, and Chrysler. For years, automakers classified lease receivables and other dealer-financing arrangements as investment cash flows. Thus, they reported an increase in lease or loan receivables from cars sold as a use of cash in the investing section of the statement of cash flows. The SEC objected and now requires automakers to report these receivables as operating cash flows, since the leases and loans are used to facilitate car sales. At GM, these reclassifications reduced its operating cash flows from $7.6 billion to $3 billion in the year before the change.

In the banking industry, how banks classify their investments, deposits, and cash flow from acquisitions results in huge swings in operating cash flows, both downward (Bank of America) and upward (KeyCorp). According to one analyst, “As it stands now, banks can't be reliably compared to each other by their recorded cash flow from operations… operating cash flow for a bank is basically meaningless.” Another questionable cash flow classification for banks is the characterization of increases and decreases in deposits as financing cash flow. Many analysts believe customer-driven deposits should be accounted for under operating cash flow (rather than as a financing cash flow) since “the very health of a bank's operations depends on its deposit base and its ability to attract a growing stream of deposits.” So while the overall cash flow—from operations, investing, and financing—remained the same, operating cash flow at these companies looked better than it really was.

Sources: Peter Elstrom, “How to Hide $3.8 Billion in Expenses,” BusinessWeek Online (July 8, 2002); Judith Burns, “SEC Tells US Automakers to Retool Cash-Flow Accounting,” Wall Street Journal Online (February 28, 2005); and Sarah Johnson, “Cash Flow: A Better Way to Know Your Bank?” CFO.com (July 9, 2009).

Other Working Capital Changes

Up to this point, we showed how companies handled all of the changes in working capital items (current asset and current liability items) as adjustments to net income in determining net cash flow from operating activities. You must be careful, however, because some changes in working capital, although they affect cash, do not affect net income. Generally, these are investing or financing activities of a current nature.

One activity is the purchase of short-term available-for-sale securities. For example, the purchase of short-term available-for-sale securities for $50,000 cash has no effect on net income but it does cause a $50,000 decrease in cash. A company reports this transaction as a cash flow from investing activities as follows. [6]

![]()

What about trading securities? Because companies hold these investments principally for the purpose of selling them in the near term, companies should classify the cash flows from purchases and sales of trading securities as cash flows from operating activities. [7]9

Another example is the issuance of a short-term nontrade note payable for cash. This change in a working capital item has no effect on income from operations but it increases cash by the amount of the note payable. For example, a company reports the issuance of a $10,000 short-term note payable for cash in the statement of cash flows as follows.

![]()

Another change in a working capital item that has no effect on income from operations or on cash is a cash dividend payable. Although a company will report the cash dividends when paid as a financing activity, it does not report the declared but unpaid dividend on the statement of cash flows.

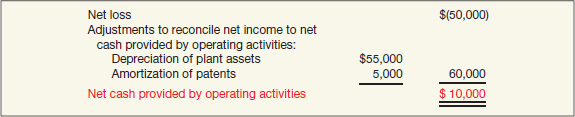

Net Losses

If a company reports a net loss instead of a net income, it must adjust the net loss for those items that do not result in a cash inflow or outflow. The net loss, after adjusting for the charges or credits not affecting cash, may result in a negative or a positive cash flow from operating activities.

For example, if the net loss is $50,000 and the total amount of charges to add back is $60,000, then net cash provided by operating activities is $10,000. Illustration 23-33 shows this computation.

If the company experiences a net loss of $80,000 and the total amount of the charges to add back is $25,000, the presentation appears as follows.

Although not illustrated in this chapter, a negative cash flow may result even if the company reports a net income.

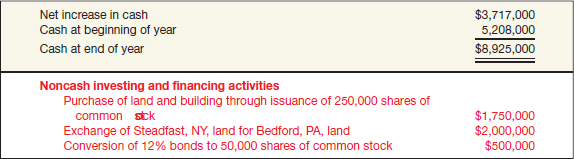

Significant Noncash Transactions

Because the statement of cash flows reports only the effects of operating, investing, and financing activities in terms of cash flows, it omits some significant noncash transactions and other events that are investing or financing activities. Among the more common of these noncash transactions that a company should report or disclose in some manner are the following.

- Acquisition of assets by assuming liabilities (including capital lease obligations) or by issuing equity securities.

- Exchanges of nonmonetary assets.

- Refinancing of long-term debt.

- Conversion of debt or preferred stock to common stock.

- Issuance of equity securities to retire debt.

A company does not incorporate these noncash items in the statement of cash flows. If material in amount, these disclosures may be either narrative or summarized in a separate schedule at the bottom of the statement, or they may appear in a separate note or supplementary schedule to the financial statements.10 Illustration 23-35 (page 1442) shows the presentation of these significant noncash transactions or other events in a separate schedule at the bottom of the statement of cash flows.

Or, companies may present these noncash transactions in a separate note, as shown in Illustration 23-36.

Companies do not generally report certain other significant noncash transactions or other events in conjunction with the statement of cash flows. Examples of these types of transactions are stock dividends, stock splits, and restrictions on retained earnings. Companies generally report these items, neither financing nor investing activities, in conjunction with the statement of stockholders' equity or schedules and notes pertaining to changes in capital accounts.

What do the numbers mean? CASH FLOW TOOL

By understanding the relationship between cash flow and income measures, analysts can gain better insights into company performance. Because earnings altered through creative accounting practices generally do not change operating cash flows, analysts can use the relationship between earnings and operating cash flow to detect suspicious accounting practices. Also, by monitoring the ratio between cash flow from operations and operating income, they can get a clearer picture of developing problems in a company.

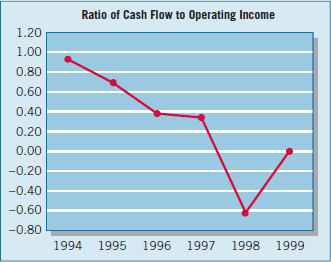

For example, the following chart plots the ratio of operating cash flows to earnings for Xerox Corp. in the years leading up to the SEC singling it out in 2000 for aggressive revenue recognition practices on its leases.

Similar to W. T. Grant in the opening story, Xerox was reporting earnings growth in the years leading up to its financial breakdown in 2000 but teetering near bankruptcy in 2001. However, Xerox's ratio of cash flow to earnings showed a declining trend and became negative well before its revenue recognition practices were revealed. The trend revealed in the graph should have given any analyst reason to investigate Xerox further. As one analyst noted, “Earnings growth that exceeds the growth in operating cash flow cannot continue for extended periods and should be investigated.”

Source: Adapted from Charles Mulford and Eugene Comiskey, The Financial Numbers Game: Detecting Creative Accounting Practices (New York: John Wiley & Sons, 2002), Chapter 11, by permission.

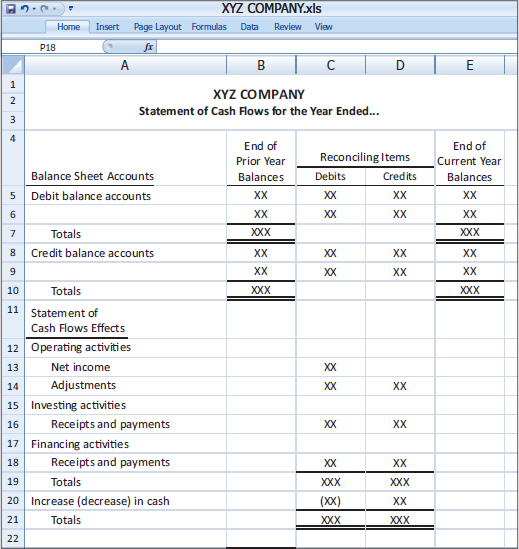

USE OF A WORKSHEET

LEARNING OBJECTIVE ![]()

Explain the use of a worksheet in preparing a statement of cash flows.

When numerous adjustments are necessary or other complicating factors are present, companies often use a worksheet to assemble and classify the data that will appear on the statement of cash flows. The worksheet is merely a device that aids in the preparation of the statement. Its use is optional. Illustration 23-37 shows the skeleton format of the worksheet for preparation of the statement of cash flows using the indirect method.

The following guidelines are important in using a worksheet.

- In the balance sheet accounts section, list accounts with debit balances separately from those with credit balances. This means, for example, that Accumulated Depreciation is listed under credit balances and not as a contra account under debit balances. Enter the beginning and ending balances of each account in the appropriate columns. Then, enter the transactions that caused the change in the account balance during the year as reconciling items in the two middle columns.

After all reconciling items have been entered, each line pertaining to a balance sheet account should foot across. That is, the beginning balance plus or minus the reconciling item(s) must equal the ending balance. When this agreement exists for all balance sheet accounts, all changes in account balances have been reconciled.

- The bottom portion of the worksheet consists of the operating, investing, and financing activities sections. Accordingly, it provides the information necessary to prepare the formal statement of cash flows. Enter inflows of cash as debits in the reconciling columns, and outflows of cash as credits in the reconciling columns. Thus, in this section, a company would enter the sale of equipment for cash at book value as a debit under inflows of cash from investing activities. Similarly, it would enter the purchase of land for cash as a credit under outflows of cash from investing activities.

- Do not enter in any journal or post to any account the reconciling items shown in the worksheet. These items do not represent either adjustments or corrections of the balance sheet accounts. They are used only to facilitate the preparation of the statement of cash flows.

Preparation of the Worksheet

The preparation of a worksheet involves the following steps.

Step 1. Enter the balance sheet accounts and their beginning and ending balances in the balance sheet accounts section.

Step 2. Enter the data that explain the changes in the balance sheet accounts (other than cash) and their effects on the statement of cash flows in the reconciling columns of the worksheet.

Step 3. Enter the increase or decrease in cash on the cash line and at the bottom of the worksheet. This entry should enable the totals of the reconciling columns to be in agreement.

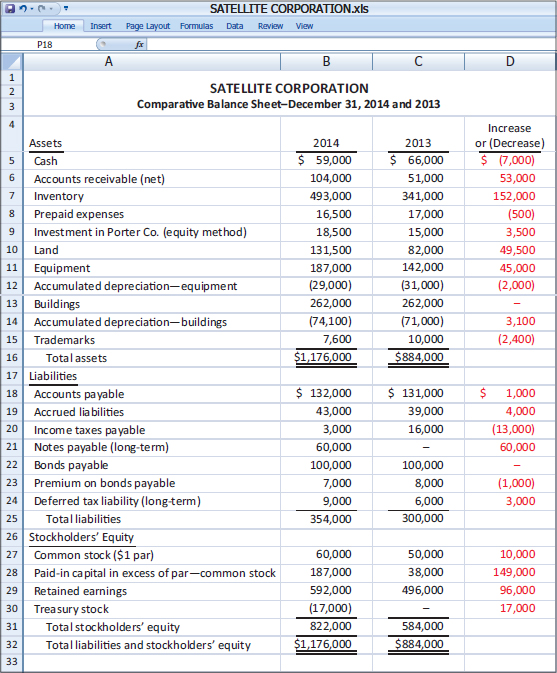

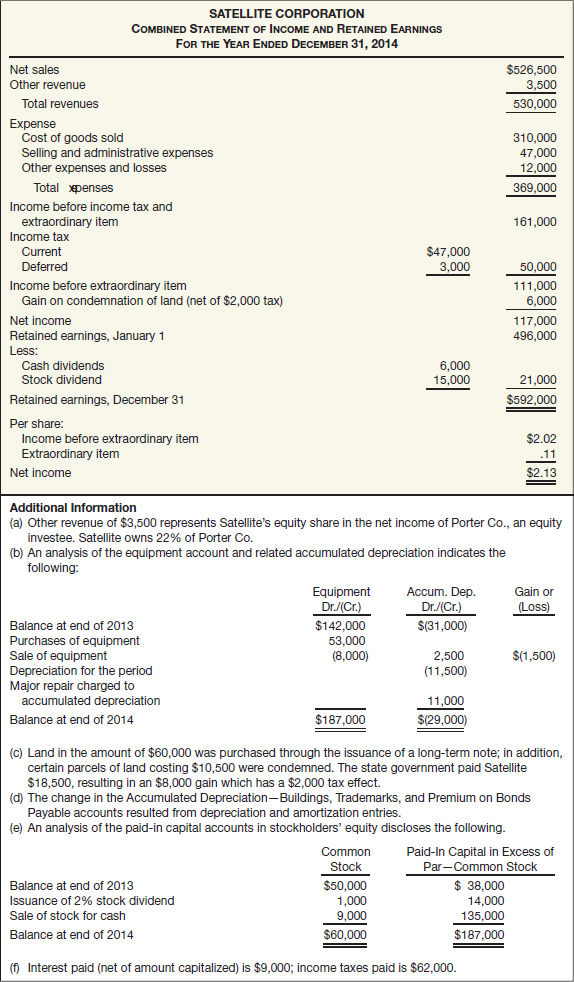

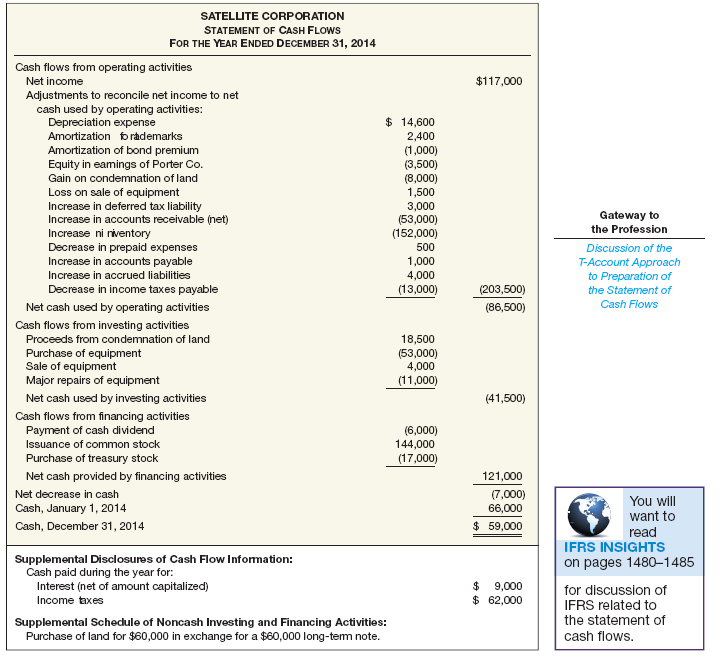

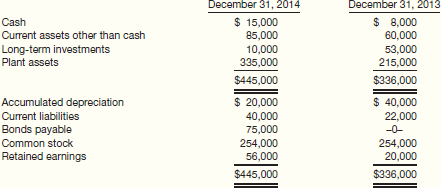

To illustrate the preparation and use of a worksheet and to illustrate the reporting of some of the special problems discussed in the prior section, we present a comprehensive example for Satellite Corporation. Again, the indirect method serves as the basis for the computation of net cash provided by operating activities. Illustrations 23-38 and 23-39 (page 1446) present the balance sheet, combined statement of income and retained earnings, and additional information for Satellite Corporation.

The discussion that follows provides additional explanations related to the preparation of the worksheet.

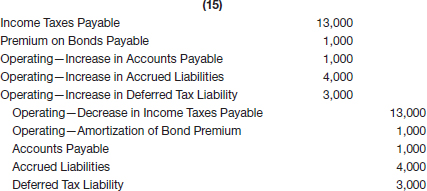

Analysis of Transactions

The following discussion explains the individual adjustments that appear on the worksheet in Illustration 23-40 (page 1450). Because cash is the basis for the analysis, Satellite reconciles the Cash account last. Because income is the first item that appears on the statement of cash flows, it is handled first.

Change in Retained Earnings

Net income for the period is $117,000. The entry for it on the worksheet is as follows.

![]()

Satellite reports net income on the bottom section of the worksheet. This is the starting point for preparation of the statement of cash flows (under the indirect method).

A stock dividend and a cash dividend also affected retained earnings. The retained earnings statement reports a stock dividend of $15,000. The worksheet entry for this transaction is as follows.

The issuance of stock dividends is not a cash operating, investing, or financing item. Therefore, although the company enters this transaction on the worksheet for reconciling purposes, it does not report it in the statement of cash flows.

The $6,000 cash dividend paid represents a financing activity cash outflow. Satellite makes the following worksheet entry:

![]()

The company reconciles the beginning and ending balances of retained earnings by entry of the three items above.

Accounts Receivable (Net)

The increase in accounts receivable (net) of $53,000 represents adjustments that did not result in cash inflows during 2014. As a result, the company would deduct from net income the increase of $53,000. Satellite makes the following worksheet entry.

![]()

Inventory

The increase in inventory of $152,000 represents an operating use of cash. The incremental investment in inventory during the year reduces cash without increasing the cost of goods sold. Satellite makes the following worksheet entry.

![]()

Prepaid Expense

The decrease in prepaid expenses of $500 represents a charge in the income statement for which there was no cash outflow in the current period. Satellite should add that amount back to net income through the following entry.

![]()

Investment in Stock

Satellite's investment in the stock of Porter Co. increased $3,500. This amount reflects Satellite's share of net income earned by Porter (its equity investee) during the current year. Although Satellite's revenue and therefore its net income increased $3,500 by recording Satellite's share of Porter Co.'s net income, no cash (dividend) was provided. Satellite makes the following worksheet entry.

![]()

Land