Chapter 3

Fringe Benefits

Employer-furnished fringe benefits are exempt from tax if the tests discussed in this chapter are met.

The most common tax-free benefits are accident and health plan coverage, including employer contributions to health savings accounts (HSAs), group-term life insurance plans, dependent care plans, education assistance plans, tuition reduction plans, adoption benefit plans, cafeteria plans, and plans providing employees with discounts, no-additional-cost services, or employer-subsidized meal facilities.

Highly compensated individuals may be taxed on certain benefits from such plans if nondiscrimination rules are not met.

Table 3-1 Are Your Fringe Benefits Tax Free?

| Fringe benefit— | Tax Pointer— |

| Adoption benefits | Employer payments to a third party or reimbursements to you in 2017 for qualified adoption expenses are generally tax free up to a limit of $13,570. The exclusion for 2017 starts to phase out if modified adjusted gross income (MAGI) exceeds $203,540 and is completely phased out if MAGI is $243,540 or more (3.6). |

| Athletic facilities | The fair market value of athletic facilities, such as gyms, swimming pools, golf courses, and tennis courts, is tax free if the facilities are on property owned or leased by the employer (not necessarily the main business premises) and substantially all of the use of the facilities is by employees, their spouses, and dependent children. Such facilities must be open to all employees on a nondiscriminatory basis in order for the company to deduct related expenses. |

| Child or dependent care plans | The value of day-care services provided or reimbursed by an employer under a written, nondiscriminatory plan is tax free up to a limit of $5,000, or $2,500 for married persons filing separately. Expenses are excludable if they would qualify for the dependent care credit; see Chapter 25. On your tax return, you must report employer-provided benefits to figure the tax-free exclusion. Tax-free employer benefits reduce eligibility for the dependent care tax credit (3.5). |

| De minimis (minor) fringe benefits | These are small benefits that are administratively impractical to tax, such as occasional supper money and taxi fares for overtime work, company parties or picnics, and occasional theater or sporting event tickets (3.10). |

| Discounts on company products and services | Services from your employer that are usually sold to customers are tax free if your employer does not incur additional costs in providing them to you (3.16). Merchandise discounts and other discounted services are also eligible for a tax-free exclusion (3.17). |

| Education plans | An up-to-$5,250 exclusion applies to employer-financed undergraduate and graduate courses (3.7). |

| Employee achievement awards | Achievement awards are taxable unless they qualify under special rules for length of service or safety achievement (3.12). |

| Group-term life insurance | Premiums paid by employers are not taxed if policy coverage is $50,000 or less (3.4). |

| Health and accident plans including HSAs | Premiums paid by an employer are tax free. For 2017, employer contributions to a health savings account, or HSA, on behalf of an eligible employee are generally not taxed up to $3,400 for self-only coverage or $6,750 for family coverage (3.2). Health benefits paid from an employer plan are also generally tax free (3.1–3.4). |

| Interest-free or low-interest loans | Interest-free loans received from your employer may be taxed (4.31). |

| Retirement planning advice | Employer-provided retirement income planning advice and information are tax free to employees (and their spouses) so long as the employer maintains a qualified retirement plan. The exclusion does not apply to tax preparation, accounting, legal, or brokerage services. |

| Transportation benefits | Within limits, employer-provided parking benefits, transit passes, and bicycle commuting reimbursements are tax free; see 3.8. |

| Tuition reductions | Tuition reductions for courses below the graduate level are generally tax free. Graduate students who are teaching or research assistants are not taxed on tuition reduction unless the reduction is compensation for teaching services (3.7). |

| Working condition benefits | Benefits provided by your employer that would be deductible if you paid the expenses yourself are a tax-free working condition fringe benefit. These include business use of a company car or employer-provided cell phone (3.9). |

3.1 Tax-Free Health and Accident Coverage Under Employer Plans

You are not taxed on contributions or insurance premiums your employer makes to a health, hospitalization, or accident plan to cover you, your spouse, your dependents, and your children under age 27 (as of the end of the year) whether or not they can be claimed as your dependents. Tax-free treatment for a spouse applies to same-sex as well as opposite sex spouses. A domestic partner is not a spouse; you must pay tax on employer-paid coverage for a domestic partner.

If you obtain coverage by making pre-tax salary-reduction contributions under your employer’s cafeteria plan (3.15), the salary reductions are treated as employer contributions that are tax free to you. If you are temporarily laid off and continue to receive health coverage, the employer’s contributions during this layoff period are tax free. If you are retired, you do not pay tax on insurance paid by your former employer. Medical coverage provided to the family of a deceased employee is tax free since it is treated as a continuation of the employee’s fringe-benefit package. If you are age 65 or older, Medicare premiums paid by your employer are not taxed. If you retire and have the option of receiving continued coverage under the medical plan or a lump-sum payment covering unused accumulated sick leave instead of coverage, the lump-sum amount is reported as income at the time you have the option to receive it. If you elect continued coverage, the amount reported as income may be deductible as medical insurance if you itemize deductions (17.5).

Disability coverage. If your employer pays the premiums for your disability coverage (short term or long term) and does not report the payment as compensation income on your Form W-2, or if you pay the premiums with pre-tax salary-reduction contributions, your coverage is tax free but any benefits you subsequently receive from the plan upon becoming disabled will be includible in your gross income (3.3). If you pay the premiums with after-tax contributions or your employer makes contributions that are included on your Form W-2, any disability benefits you receive from the plan will not be taxable to you.

Health Reimbursement Arrangements (HRAs). Employer contributions to health reimbursement arrangements (HRAs) are not taxed to the employees. The contributions must be paid by the employer and not provided by salary reduction. HRA contributions can be used to reimburse the medical costs of employees, their spouses, and their dependents, and unused expenses may be carried forward to later years (3.3).

Long-term care coverage. You are not taxed on contributions your employer makes for long-term care coverage that would pay you benefits in the event you become chronically ill (17.15). However, long-term care coverage may not be offered to you through a cafeteria plan (3.15) and reimbursements of long-term care expenses may not be made through a flexible spending arrangement (3.16).

Continuing coverage for group health plans (COBRA coverage). Employers are subject to daily penalties unless they offer continuing group health and accident coverage to employees who leave the company voluntarily or involuntarily (unless for gross misconduct) and to spouses and dependent children who would lose coverage in the case of divorce or the death of the employee. Federal COBRA continuing coverage rules apply to employers with 20 or more employees but smaller employers may be required under state law to provide comparable continuing coverage under “mini-COBRA” laws.

Generally, an employer may charge you premiums for continuing coverage that are as much as 102% of the regular plan premium for the applicable (family or individual) coverage.

3.2 Health Savings Accounts (HSAs) and Archer MSAs

If you are covered by a qualifying high-deductible health plan (HDHP), your employer may make tax-free contributions to a health savings account (HSA) on your behalf. Earnings accumulate tax free within an HSA and distributions are tax free if used to pay your qualified medical expenses, or those of your spouse or dependents. If your employer does not make the maximum tax-free contribution to your HSA, you can make a deductible contribution, so long as the total does not exceed the annual contribution limit (see below).

Archer MSAs are an older type of medical savings plan that HSAs are intended to replace. If your employer set up an Archer MSA on your behalf before 2008, or you became eligible to participate after 2007 in a pre-2008 plan, your employer may continue to contribute to the account. If you ork for an eligible small employer with a high-deductible plan, your employer may make tax-free contributions to an Archer MSA on your behalf. A rollover can be made from an Archer MSA to a new health savings account (HSA) that accepts rollovers. If the Archer MSA is retained, withdrawals will be tax free if used to pay qualified medical expenses for you, your spouse, or your dependents.

Health Savings Account (HSA)

You may set up an HSA only if you are covered by a qualifying high-deductible health plan (HDHP, see details below), you are not enrolled in Medicare, and you are not the dependent of another taxpayer. Generally, you must have no coverage other than HDHP coverage, but there are exceptions. You are allowed to have separate coverage for vision, dental, or long-term care, accidents, disability, per diem insurance while hospitalized, insurance for a specific disease or illness, car insurance (or similar insurance for owning or using property), or insurance for workers’ compensation or tort liabilities. Preventive care is also exempt from the deductible requirement.

As an eligible employee, you, your employer, or both may contribute to your HSA. The same maximum annual contribution limit applies (see below) regardless of the number of contributors. Your employer may allow you to make pre-tax salary-reduction contributions to an HDHP and HSA as an option under a “cafeteria” plan (3.13).

High-deductible health plan (HDHP). An HDHP must have a minimum annual deductible and an annual out-of-pocket maximum. For 2017, the minimum plan deductible was $1,300 for self-only coverage and $2,600 for family coverage. Out-of-pocket costs for 2017 were limited to $6,550 for self-only coverage and $13,100 for family coverage. For 2018, the minimum plan deductible increases slightly to $1,350 for self-only coverage and $2,700 for family coverage, and the cap on out-of- pocket costs increases to $6,650 for self-only coverage and $13,300 for family coverage. The limit for out-of- pocket costs covers plan deductibles, co-payments and other out-of-pocket expenses, but not premiums.

In the case of family coverage, the terms of the HDHP must deny payments to all family members until the family as a unit incurs annual covered expenses in excess of the minimum annual deductible ($2,600 for 2017). Thus, a plan is not a qualified HDHP for 2017 if it allows payment of an individual family member’s medical expenses exceeding $1,300 (the minimum deductible for self-only coverage) but the family as a whole does not have expenses over $2,600.

However, the minimum annual HDHP deductible does not apply to preventive care benefits. The plan can qualify as an HDHP even if it pays for preventive care without a deductible or after a small deductible (below the regular HDHP minimum). The IRS has provided a safe harbor list of preventive care benefits, including annual physicals, routine prenatal and well-child care, immunizations, tobacco cessation and obesity programs, and screening services for a broad range of conditions including cancer (such as breast, cervical, prostate, ovarian, and colorectal cancer) and cardiovascular disease. Prescription drugs qualify for the preventive care safe harbor if taken by asymptomatic patients with risk factors for a disease, or by recovering patients to prevent the recurrence of a disease.

By law, prescription drug coverage, other than coverage meeting the preventive care safe harbor, is not a permitted exception to the high-deductible requirement. This is a problem for employees whose employers offer separate prescription drug plans that provide first-dollar drug coverage with either a flat dollar or percentage co-payment. HSA contributions cannot be made for individuals with an HDHP and such a prescription drug plan because the prescription drug benefits are not subject to the HDHP minimum annual deductible.

Maximum annual HSA contribution for employees. For 2017, the maximum HSA contribution for an employee with self-only coverage is $3,400, and for an employee with family coverage, the maximum contribution for 2017 is $6,750. For employees who are age 55 or older by the end of 2017 but not enrolled in Medicare, an additional “catch-up” contribution of $1,000 may be made. The applicable limit must be reduced by any contributions to an Archer MSA.

For 2018, the self-only contribution limit increases slightly to $3,450, and the limit for family coverage increases to $6,900, plus the additional $1,000 catch-up for those age 55 or older; the $1,000 catch-up is fixed by statute.

If you become eligible under an HDHP, contributions are allowed for the months prior to your enrollment in the HDHP, provided you are eligible in December of that year. However, the contributions for the months prior to your enrollment will be included in your income and subject o a 10% penalty if you do not remain eligible for the 12 months following the end of the first eligibility year, unless you are disabled (or die).

All employer contributions must be reported on Form 8889, which you attach to your Form 1040. Contributions by your employer up to the above limit are tax free and are not subject to withholding for income tax or FICA (Social Security and Medicare) purposes. All employer contributions to an HSA are reported in Box 12 of Form W-2 with Code W. Contributions exceeding the excludable limit are also reported in Box 1 of Form W-2 as taxable wages. If you do not remove an excess contribution (and any net income) by the due date for your return (including extensions), the excess is subject to a 6% penalty; see the instructions to Forms 8889 and 5329.

If your employer contributes less than the limit, you may contribute to your HSA but the same overall limit applies to the aggregate contributions. Contributions you make are reported on Form 8889 and deductible “above the line” from gross income on Line 25 of Form 1040. You must attach Form 8889 to your Form 1040.

Archer MSAs

Most employers have replaced Archer MSAs (medical savings accounts) with HSAs. However, an Archer MSA that is not rolled over to a new HSA may continue to be funded.

To contribute, you must have coverage under a high-deductible health plan and must work for a “small employer,” one that had an average of 50 or fewer employees during either of the two preceding years. For 2017, self-only coverage under a high-deductible health plan, the minimum deductible was $2,250, the maximum deductible was $3,350, and the plan limit on out-of-pocket expenses (other than premiums) was $4,500. For 2017 family coverage, the deductible had to be at least $4,500 and no more than $6,750, and the limit on out-of-pocket expenses (other than premiums) was $8,250. All of these limits are subject to an inflation adjustment for 2018; see the e-Supplement at jklasser.com.

Generally, you are not eligible for an Archer MSA if you have any other health insurance in addition to the high-deductible plan coverage, except for policies covering only disability, vision or dental care, long-term care, or accidental injuries, or plans that pay a flat amount during hospitalization.

Employer contribution limits. Your employer’s contributions to your Archer MSA are tax free up to an annual limit of 65% of the plan deductible if you have individual coverage and 75% of the deductible for family coverage. The limit is reduced on a monthly basis if you are not covered for the entire year. For example, if for all of 2017 you were covered by a qualifying family coverage high-deductible plan with a $6,750 annual deductible (this is the maximum deductible for 2017), the maximum tax-free contribution is $5,063 (75% of $6,750). If you had coverage for only 10 months, the limit would be $4,219 (10/12 × $5,063). All employer contributions to your Archer MSA are reported in Box 12 of Form W-2 (Code R). If the contributions exceed the tax-free limit, the excess is reported in Box 1 of Form W-2 as taxable wages. You must report all employer contributions on Form 8853, which you attach to your Form 1040.

If your employer makes any contributions to your account, you may not make any contributions for that year. In addition, if you and your spouse have family coverage under a high-deductible plan and your spouse’s employer contributes to his or her Archer MSA, you cannot contribute to your Archer MSA. If your employer (or spouse’s employer) does not contribute, you may make deductible contributions up to the above employer contribution limits. You report your contributions on Form 8853 and claim your deduction on Line 36 of Form 1040; label it “MSA.” Contributions exceeding the annual limit are subject to a 6% penalty.

3.3 Reimbursements and Other Tax-Free Payments From Employer Health and Accident Plans

Several types of payments from a health or accident plan are tax free to you even if your employer paid the entire cost of your coverage:

- Reimbursements of your medical expenses; see below.

- Payments for permanent physical injuries; see below.

- Distributions from a health savings account (HSA) or Archer MSA if they are used to pay for qualified medical expenses; see below.

- Payments you receive when you are chronically ill from a qualifying long-term-care insurance contract; but if payments are made on a per diem or other periodic basis, the exclusion may be limited. For 2017, payments of up to $360 per day are tax free regardless of actual expenses. If the payments exceed $360 per day, you are only taxed to the extent that the payments exceed your qualifying long-term-care expenses. See 17.15 for further details.

Payments that are not within the above tax-free categories, such as disability benefits, are not taxable to you if you paid all of the premiums with after-tax contributions. If your contributions were made on a pre-tax basis, benefits received from the plan are taxable. For example, disability benefits are taxable if you paid premiums paid under a cafeteria plan (3.14) with pre-tax contributions that were excluded from your income. If your employer paid all the premiums and you were not taxed on your employer’s payment, any benefits you receive from the plan are fully taxable. If both you (with after-tax contributions) and your employer contributed to the plan, only the amount received that is attributable to your employer’s payments is taxable.

Tax-Free Reimbursements for Medical Expenses

Reimbursements of medical expenses (17.2) that you paid for yourself, your spouse, or any dependents and your children under age 27 are tax free, provided you incurred the expenses after the plan was established. Payment does not have to come directly to you to be tax free; it may go directly to your medical care providers.

Tax-free reimbursements may be from a health-care flexible spending arrangement (FSA) (3.16). Reimbursements made under a qualifying health reimbursement arrangement (HRA) also qualify for tax-free treatment; see below.

Tax-free treatment applies only for reimbursed expenses, not amounts you would have received anyway, such as sick leave that is not dependent on actual medical expenses. If your employer reimburses you for premiums you paid, the reimbursement is tax free so long as your payment was from after-tax funds. If you paid premiums with pre-tax salary reductions, a “reimbursement” from the employer will be taxable to you because the salary reductions are treated as your employer’s payment, not yours.

Reimbursements for cosmetic surgery do not qualify for tax-free treatment, unless the surgery is for disfigurement related to congenital deformity, disease, or accidental injury.

Reimbursements for your dependents’ medical expenses are tax free. This exclusion applies not only to reimbursed expenses of persons claimed as dependents (21.1) on your return, but also to expenses of qualifying children or relatives who cannot be claimed as your dependents because: (1) they are claimed by the other parent under the special rules for divorced/separated parents (21.7), (2) their gross income exceeds the limit for qualifying relatives ($4,050 for 2017), (3) they file a joint return with their spouse, or (4) you are the dependent of another taxpayer and thus are barred from claiming any dependents on your return.

A qualifying dependent does not include a live-in mate where the relationship violates local law.

If the reimbursement is for medical expenses you deducted in a previous year, the reimbursement may be taxable. See 17.4 for the rules on reimbursements of deducted medical expenses.

If you receive payments from more than one policy and the total exceeds your actual medical expenses, the excess is taxable if your employer paid the entire premium; see the Examples in 17.4.

Health Reimbursement Arrangements (HRAs). Employers can set up health reimbursement arrangements (HRAs) that are integrated with a group health plan. The HRA reimburses out-of-pocket medical expenses of employees, their spouses, children under age 27 and their dependents. Former employees including retired employees, and spouses and dependents of deceased employees can be covered. Self-employed individuals are not eligible. An HRA must be funded solely by employer contributions and not by salary reductions or after-tax contributions from employees.

Employees are not taxed on HRA reimbursements for medical expenses that may be claimed as itemized deductions (17.2), including premiums. Over-the-counter medicines or drugs other than insulin do not qualify for tax-free reimbursement from an HRA unless they are prescribed by a physician. For contributions and reimbursements (3.1) to be tax free, employees must not receive cash or any benefit (taxable or nontaxable) from an HRA other than reimbursement for medical expenses. If the reimbursement limit is not fully used up by the end of a coverage year, the unused limit can be carried forward to a subsequent year. Nondiscrimination rules apply to self-insured HRAs.

Qualified Small Employer Health Reimbursement Arrangements (QSEHRAs). If your employer is a “small employer” (no more than 49 full-time and full-time-equivalent employees) that does not offer a group health plan, you may be offered reimbursements of your premiums for personally obtained health coverage and other out-of-pocket medical expenses (that may be claimed as itemized deductions (17.2)) through a qualified small employer health reimbursement arrangement (QSEHRA). A QSEHRA is funded solely by the employer (no salary reductions permitted) and must meet certain nondiscrimination requirements. Reimbursements are tax-free up to an annual limit. For 2017, the maximum amount of excludable reimbursements under a QSEHRA is $4,950 for self-only coverage, or $10,050 for family coverage; these amounts may get an inflation increase for 2018; see the e-Supplement at jklasser.com. The dollar limit is prorated for your period of coverage. Thus, if you obtained family coverage starting July 1, 2017, your excludable reimbursement for 2017 is limited to $5,025 (6/12th of $10,050). You must provide proof of coverage to your employer.

A QSEHRA is not treated as a group health plan. If you obtain health coverage through a government marketplace and are eligible for the premium tax credit (25.12), the credit amount is reduced by reimbursements through a QSEHRA; you must disclose to the marketplace the amount that you could be reimbursed for under a QSEHRA if you are applying for advance payment of the credit.

Your employer must provide you with a written notice about your eligibility for reimbursement and the terms of your employer’s QSEHRA. The notice generally must be provided at least 90 days before the start of the year for which the QSEHRA is provided, or 90 days before the first eligibility date for employees not eligible at the beginning of the year. The notice must state that you may be liable for the individual responsibility penalty, and that your reimbursements under the QSEHRA may become taxable, if you do not have minimum essential health coverage (38.5). In addition, the notice must include the requirement (noted above) that you disclose your QSEHRA coverage to a government marketplace when applying for advance payment of the premium tax credit.

Self-employed health plan that includes spouse. If a self-employed person hires his or her spouse and provides family coverage under a health plan purchased in the name of the business, the employee-spouse may be reimbursed tax free for medical expenses incurred by both spouses and their dependent children.

Executives taxed in discriminatory self-insured medical reimbursement plans. Although reimbursements from an employer plan for medical expenses of an employee and his or her spouse and dependents are generally tax free, this exclusion does not apply to certain highly compensated employees and stockholders if the plan is self-insured and it discriminates on their behalf. A plan is self-insured if reimbursement is not provided by an unrelated insurance company. If coverage is provided by an unrelated insurer, these discrimination rules do not apply. If a self-insured plan is deemed discriminatory, rank-and-file employees are not affected; only highly compensated employees are subject to tax.

Highly compensated participants subject to these rules include employees owning more than 10% of the employer’s stock, the highest paid 25% of all employees (other than employees who do not have to be covered under the law), and the five highest paid officers.

If highly compensated employees are entitled to reimbursement for expenses not available to other plan participants, any such reimbursements are taxable to them. For example, if only the five highest paid officers are entitled to dental benefits, any dental reimbursements they receive are taxable. However, routine physical exams may be provided to highly compensated employees (but not their dependents) on a discriminatory basis. This exception does not apply to testing for, or treatment of, a specific complaint.

If highly compensated participants are entitled to a higher reimbursement limit than other participants, any excess reimbursement over the lower limit is taxable to the highly compensated participant. For example, if highly compensated employees are entitled to reimbursements up to $5,000 while all others have a $1,000 limit, a highly compensated employee who receives a $4,000 reimbursement must report $3,000 ($4,000 received minus the $1,000 lower limit) as income.

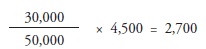

A separate nondiscrimination test applies to plan eligibility. The eligibility test requires that the plan benefit: (1) 70% or more of all employees or (2) 80% or more of employees eligible to participate, provided that at least 70% of all employees are eligible. A plan not meeting either test is considered discriminatory unless proven otherwise. In applying these tests, employees may be excluded if they have less than three years of service, are under age 25, do part-time or seasonal work, or are covered by a union collective bargaining agreement. A fraction of the benefits received y a highly compensated individual from a nonqualifying plan is taxable. The fraction equals the total reimbursements to highly compensated participants divided by total plan reimbursements; benefits available only to highly compensated employees are disregarded. For example, assume that a plan failing the eligibility tests pays total reimbursements of $50,000, of which $30,000 is to highly compensated participants. A highly compensated executive who is reimbursed $4,500 for medical expenses must include $2,700 in income:

Taxable reimbursements are reported in the year during which the applicable plan year ends. For example, in early 2017 you are reimbursed for a 2016 expense from a calendar-year plan. If under plan provisions the expenses are allocated to the 2016 plan year, the taxable amount should be reported as 2016 income. If the plan does not specify the plan year to which the reimbursement relates, the reimbursement is attributed to the plan year in which payment is made.

Tax-Free Payments for Permanent Physical Injuries

Payments from an employer plan are tax free if they are for the permanent loss of part of the body, permanent loss of use of part of the body, or for permanent disfigurement of yourself, your spouse, your children under age 27 (as of the end of the year), or your dependent. An appeals court held that severe hypertension does not involve loss of a bodily part or function and thus does not qualify for the exclusion.

To be tax free, the payments must be based on the kind of injury and have no relation to the length of time you are out of work or prior years of service. If the employer’s plan does not specifically allocate benefits according to the nature of the injury, the benefits are taxable even if an employee is in fact permanently disabled.

Disability payments from profit-sharing plan. The Tax Court has held that a profit-sharing plan may provide benefits that qualify for the exclusion for permanent disfigurement or permanent loss of bodily function. The plan must clearly state that its purpose is to provide qualifying tax-free benefits, and a specific payment schedule must be provided for different types of injuries. Without such provisions, payments from the plan are treated as taxable retirement distributions.

HSA or Archer MSA Payments

Tax-free distributions from a health savings account (HSA). Distributions from an HSA (3.2) are tax free if used to pay qualified medical expenses for you, your spouse, or your dependents. Qualified medical expenses are unreimbursed costs eligible for the itemized deduction (17.2) on Schedule A of Form 1040. Over-the-counter medicines other than insulin that do not require a prescription qualify for HSA purposes if they are actually prescribed by a physician. Medical expenses are “qualified” only if incurred after the HSA has been established. A distribution is taxable to the extent it is not used to pay qualified medical expenses. A taxable distribution is also subject to a 20% penalty unless you are disabled or are age 65 or older. Distributions will be reported to you on Form 1099-SA and you must report them on Form 8889, which you attach to Form 1040. On Form 8889, you determine if any part of the distribution is taxable and, if it is, that amount must be included as “Other income” on Line 21 of Form 1040. The 20% penalty from Form 8889, if any, is entered on Form 1040, Line 62.

A non-spouse beneficiary who inherits an HSA after the death of the account owner generally must include in income the fair market value of the assets as of the date of death. However, the beneficiary is not subject to the 20% penalty for taxable distributions. If the beneficiary is the account owner’s spouse, he or she becomes the owner of the HSA and will be taxed only on distributions that are not used for qualified medical expenses.

Tax-free distributions from Archer MSA. If you work for a small-business employer and have a qualifying Archer MSA (3.2), earnings accumulate in the account tax free. Withdrawals are tax free if used to pay deductible medical costs for you, your spouse, or dependents. Withdrawals used for a non-qualifying purpose are taxable and a taxable distribution before age 65 or becoming disabled is also subject to a 20% penalty. See 41.13 for further details.

3.4 Group-Term Life Insurance Premiums

You are not taxed on your employer’s payments of premiums of up to $50,000 on your life under a group-term insurance policy. You are taxed only on the cost of premiums for coverage of over $50,000 as determined by the IRS rates shown in the table below. On Form W-2 your employer should include the taxable amount as wages in Box 1 and separately label the amount in Box 12 with Code C. You may not avoid tax by assigning the policy to another person.

If two or more employers provide you with group-term insurance coverage, you get only one $50,000 exclusion. You must figure the taxable cost for coverage over $50,000 by using the IRS rates below.

Regardless of the amount of the policy, you are not taxed if, for your entire tax year, the beneficiary of the policy is a tax-exempt charitable organization or your employer.

Your payments reduce taxable amount. If you pay part of the cost of the insurance, your payment reduces dollar for dollar the amount includible as pay on Form W-2.

Retirees. If your former employer provides you with over $50,000 of group-term life insurance coverage, the cost of the coverage over $50,000 is generally taxable to you as if you were an employee. However, if you retired because of a total and permanent disability and remain covered by your company’s plan, you are not taxed even if coverage exceeds $50,000.

There are also exceptions for coverage under plans in existence on January 1, 1984. If you retired on or before that date (normal retirement or disability), were covered by the plan when you retired, and are still covered by it, your current coverage is tax free even if coverage is over $50,000. If you were age 55 or older on January 1, 1984, and retired after that date, and were employed during 1983 by the employer providing the current coverage or a predecessor employer, you are not taxed on the cost of your current coverage.

However, even if the above tests for tax-free coverage are met, you may be taxed under the rule below for discriminatory plans if you retired after 1986 and were a key employee.

Key employees taxed under discriminatory plans. The $50,000 exclusion is not available to key employees unless the group plan meets nondiscrimination tests for eligibility and benefits. For 2017, key employees include those who during the year were: (1) more-than-5% owners; (2) more-than-1% owners earning over $150,000; and (3) officers with compensation over $175,000. If the plan discriminates, a key employee’s taxable benefit is based on the larger of (1) the actual cost of coverage or (2) the amount for coverage using the IRS rate table below.

The nondiscrimination rules also apply to former employees who were key employees when they separated from service. The discrimination tests are applied separately with respect to active and former employees.

Group-term life insurance for dependents. Employer-paid coverage for your spouse or dependents is a tax-free de minimis fringe benefit (3.10) if the policy is $2,000 or less. For coverage over $2,000, you are taxed on the excess of the cost (determined under the IRS table below) over your after-tax payments for the insurance, if any.

Permanent life insurance. If your employer pays premiums on your behalf for permanent nonforfeitable life insurance, you report as taxable wages the cost of the benefit, less any amount you paid. A permanent benefit is an economic value that extends beyond one year and includes paid-up insurance or cash surrender value, but does not include, for example, the right to convert or continue life insurance coverage after group coverage is terminated. Where permanent benefits are combined with term insurance, the permanent benefits are taxed under formulas found in IRS regulations.

Table 3-2 Taxable Premiums for Group-Term Insurance Coverage Over $50,000

Age—* |

Monthly cost for each $1,000 |

Under 25 |

$0.05 |

25–29 |

0.06 |

30–34 |

0.08 |

35–39 |

0.09 |

40–44 |

0.10 |

45–49 |

0.15 |

50–54 |

0.23 |

55–59 |

0.43 |

60–64 |

0.66 |

65–69 |

1.27 |

70 and over |

2.06 |

*Age is determined at end of year.

3.5 Dependent Care Assistance

The value of qualifying day-care services provided by your employer under a written, nondiscriminatory plan is generally not taxable up to a limit of $5,000, or $2,500 if you are filing separately. The same tax-free limits apply if you make pre-tax salary deferrals to a flexible spending account for reimbursing dependent care expenses (3.15). However, you may not exclude from income more than your earned income. If you are married and your spouse earns less than you do, your tax-free benefit is limited to his or her earned income. If your spouse does not work, all of your benefits are taxable unless he or she is a full-time student or is disabled. If a full-time student or disabled, your spouse is treated as earning $250 a month if your dependent care expenses are for one dependent, or $500 a month if the expenses are for two or more dependents.

Expenses are excludable from income only if they would qualify for the dependent care credit; see Chapter 25. If you are being reimbursed by your employer, the exclusion is not allowed if dependent care is provided by a relative who is your dependent (or your spouse’s dependent) or by your child under the age of 19. You must give your employer a record of the care provider’s name, address, and tax identification number. The identifying information also must be listed on your return.

If the plan does not meet nondiscriminatory tests, benefits provided for highly-compensated employees are not excludable from their income.

Reporting employer benefits on your return. Your employer will show the total amount of your dependent care benefits in Box 10 of your Form W-2. Any benefits over $5,000 will also be included as taxable wages in Box 1 of Form W-2 and as Social Security wages (Box 3) and Medicare wages (Box 5).

You must report the benefits on Part III of Form 2441, where you determine both the tax-free and taxable (if any) portions of the employer-provided benefits. If any part is taxable, that amount must be included on Line 7 of your return as wages and labeled “DCB.”

Follow IRS instructions for identifying the care provider (employer, babysitter, etc.) on Part I of Form 2441.

The tax-free portion of employer benefits reduces expenses eligible for the dependent care credit (Chapter 25).

3.6 Adoption Benefits

If your employer pays or reimburses you in 2017 for qualifying adoption expenses under a written, nondiscriminatory plan, up to $13,570 per qualifying child may be tax free. Employer-provided adoption assistance may be for any child under age 18, or a person physically or mentally incapable of self-care. The exclusion applies to adoption fees, attorney fees, court costs, travel expenses, and other expenses directly related to a legal adoption. Expenses for adopting your spouse’s child and the costs of a surrogate-parenting arrangement do not qualify. If you have other qualifying adoption expenses, you may also be able to claim a tax credit up to a separate $13,570 limit; both the exclusion and the credit may be claimed for the same adoption if they are not for the same expenses. The exclusion and the credit are subject to similar limitations, including a phaseout based on income. See Chapter 25 for a full discussion of the credit.

The full $13,570 exclusion limit is available for the adoption of a “special needs” child even if actual adoption expenses are less than $13,570. A “special needs” designation is made when a state determines that adoption assistance is required to place a child (U.S. citizen or resident) with adoptive parents because of special factors, such as the child’s physical condition or ethnicity.

If you are adopting a child who is not a U.S. citizen or resident when the adoption effort begins, the exclusion is available only in the year the adoption becomes final. For example, if in 2017 your employer pays for expenses of adopting a foreign child but the adoption has not become final by the end of the year, you must report the employer’s payment as wage income for 2017. You will claim the exclusion on Form 8839 in the year the adoption is final.

Reporting employer benefits and claiming the exclusion on your return. You must file Form 8839 to report your employer’s payments and to figure the tax-free and taxable portions of the benefits. The employer’s payments will be included in Box 12 of Form W-2 (Code T). This total includes pre-tax salary reduction contributions that you made to a cafeteria plan (3.14) to cover such expenses.

If you are married, you generally must file a joint return to exclude the benefits as income. However, if you are legally separated or if you lived apart from your spouse for the last six months of the year, the exclusion may be available on a separate return; see Form 8839 for details.

On 2017 tax returns, the allowable exclusion begins to phase out if your modified adjusted gross income (MAGI) exceeds $203,540. If MAGI is $243,540 or more (including the employer’s adoption assistance and adding back certain tax-free income from foreign sources), the phaseout is complete and all of the employer-paid adoption assistance is taxable. Figure the tax-free amount on Form 8839.

3.7 Education Assistance Plans

If your employer pays for job-related courses, the payment is tax free to you provided that the courses do not satisfy the employer’s minimum education standards and do not qualify you for a new profession. If these tests are met, the employer’s education assistance is a tax-free working condition fringe benefit (3.9).

Even if not job related, your employer’s payment for courses is tax free up to $5,250, provided the assistance is under a qualifying Section 127 plan meeting nondiscriminatory tests. Graduate courses qualify for the exclusion as well as undergraduate courses. The Section 127 exclusion covers tuition, fees, books, and equipment, plus supplies that you cannot keep at the end of the course. Lodging, meals, and transportation are not covered by the exclusion. Sports or hobby-type courses qualify only if the courses are related to your business or are required as part of a degree program.

Tuition reductions. Employees and retired employees of educational institutions, their spouses, and their dependent children are not taxed on tuition reductions for undergraduate courses provided the reduction is not payment for teaching or other services. However, an exclusion is allowed for tuition reductions under the National Health Services Corps Scholarship Program and the Armed Forces Health Professions Scholarship Program despite the recipient’s service obligation. Widows or widowers of deceased employees or of former employees also qualify. Officers and highly paid employees may claim the exclusion only if the employer plan does not discriminate on their behalf. The exclusion applies to tuition for undergraduate education at any educational institution, not only the employer’s school.

Graduate students who are teaching or research assistants at an educational institution are not taxed on tuition reductions for courses at that school if the tuition reduction is in addition to regular pay for the teaching or research services or the reduction is provided under the National Health Services Corps Scholarship Program or the Armed Forces Health Professions Scholarship Program. The graduate student exclusion for tuition reductions applies only to teaching and research assistants, and not to faculty or other staff members (or their spouses and dependents) who take graduate courses and also do research for or teach at the school. However, if the graduate courses are work related, a tuition reduction for faculty and staff may qualify as a tax-free working condition fringe benefit (3.9).

3.8 Company Cars, Parking, and Transit Passes

The costs of commuting to a regular job site are not deductible (20.2), but employees who receive transit passes or travel to work on an employer-financed van get a tax break by not having to pay tax on some or all of such benefits. Where a company car is provided, the value of personal use is generally taxable, as discussed below.

Company cars. The use of a company car is tax free under the working condition fringe benefit rule (3.9) to the extent you use the car for business. If you use the car for personal driving, your company has the responsibility of calculating taxable income, which generally is based on IRS tables that specify the annual lease value of various priced cars. You are also required to keep for your employer a mileage log or similar record to substantiate your business use. Your employer should tell you what type of records are required.

Regardless of personal use, you are not subject to tax for a company vehicle that the IRS considers to be of limited personal value. These are ambulances or hearses; flatbed trucks; dump, garbage, or refrigerated trucks; one-passenger delivery trucks (including trucks with folding jump seats); tractors, combines, and other farm equipment; or forklifts. Also not taxable is personal use of school buses, passenger buses (seating at least 20), and moving vans where such personal use is restricted. Exclusions are also allowed for commuting use of a clearly marked police, fire, or public safety officer vehicle by officers required to be on call at all times, and for officially authorized uses of unmarked vehicles by law enforcement officers.

Demonstration cars. The value of a demonstration car used by a full-time auto salesperson is tax free as a working condition fringe benefit if the use of the car facilitates job performance and if there are substantial personal-use restrictions, including a prohibition on use by family members and for vacation trips. Furthermore, mileage outside of normal working hours must be limited and personal driving must generally be restricted to a 75-mile radius around the dealer’s sales office.

Chauffeur services. If chauffeur services are provided for both business and personal purposes, you must report as income the value of the personal services. For example, if the full value of the chauffeur services is $30,000 and 30% of the chauffeur’s workday is spent driving on personal trips, then $9,000 is taxable (30% of $30,000) and $21,000 is tax free.

If an employer provides a bodyguard-chauffeur for business security reasons, the entire value of the chauffeur services is considered a tax-free working condition fringe benefit if: (1) the automobile is specially equipped for security and (2) the bodyguard is trained in evasive driving techniques and is provided as part of an overall 24-hour-a-day security program. If the value of the bodyguard-chauffeur services is tax free, the employee is still taxable on the value of using the vehicle for commuting or other personal travel.

How your employer reports taxable automobile benefits. Social Security and Medicare tax must be withheld. Income tax withholding is not required, but your employer may choose to withhold income tax. If income tax is not withheld, you must be notified of this fact so that you may consider the taxable benefits when determining whether to make estimated tax installments; see Chapter 27. Whether or not withholdings are taken, the taxable value of the benefits is entered on your Form W-2 in Box 14 or on a separate Form W-2 for fringe benefits.

A special IRS rule allows your employer to include 100% of the lease value of using the car on Form W-2, even if you used the car primarily for business. Your employer must specifically indicate on Form W-2 (Box 14) or on a separate statement if 100% of the lease value has been included as income on your Form W-2. If it has, you should compute a deduction on Form 2106 for the business-use value of the car. However, this deduction, plus any unreimbursed car operating expenses, may be claimed only as a miscellaneous itemized deduction on Schedule A subject to the 2% of AGI floor (19.1).

Company planes. Under rules similar to those for company cars, employees who use a company airplane for personal trips are taxable on the value of the flights, as determined by the employer using IRS tables.

Qualified Transportation Benefits

Your employer may provide you with transportation benefits that are tax free within certain limits. There are three categories of qualified benefits: (1) transit passes and commuter transportation in a van, bus, or similar highway vehicle are considered together, (2) parking, and (3) bicycle commuting reimbursements.

You may receive benefits from each category so long as the applicable monthly limit (see below) is not exceeded. If the benefits exceed the monthly limit, the excess is treated as wages subject to income tax, Social Security, and Medicare tax.

Transit pass/commuter transportation benefits and parking benefits may be provided through a salary-reduction arrangement. An irrevocable salary-reduction election may be made prospectively for a monthly amount of benefits. The salary reduction for any month may not exceed the total limit for both categories. Unused salary reductions may be carried over to later months and from year to year. However, if you leave the company before using the carryover, the unused amount is forfeited; you cannot get a refund.

Exclusion limit. The same monthly exclusion limit applies to (1) the combined value of qualified employer-provided transit passes plus commuting in an employer’s van or bus, and (2) qualified parking benefits. For 2017, the maximum monthly exclusion for each of these categories is $255 per month. If the value of benefits for any month does not equal the exclusion limit, the unused amount is lost and may not be carried over to other months. For 2018, the monthly cap for each benefit may be increased above $255 by an inflation adjustment; see the e-Supplement at jklasser.com.

The maximum exclusion for qualified bicycle commuting costs is $20 per qualifying month.

Details on what constitutes qualified transit pass/van pool, parking, and bicycle commuting benefits are in the following paragraphs.

Qualified transit passes and van/bus transportation. For purposes of the exclusion, qualifying transit passes include tokens, fare cards, or vouchers for mass transit or private transportation businesses using highway vehicles seating at least six passengers. A cash reimbursement for a transit pass is taxable if vouchers (or similar items) are readily available to the employer for distribution to employees. “Ready availability” is determined under tests in IRS regulations. Cash advances are taxable.

Qualifying van or bus pool vehicles must seat at least six passengers and be used at least 80% of the time for employee commuting; on average, the number of employees must be at least half the seating capacity.

The exclusion applies only to regular employees. For partners, more than 2% S corporation shareholders, and independent contractors who are provided transit passes, the IRS allows up to $21 per month as a tax-free de minimis benefit. If the monthly value exceeds $21, the full value is taxable and not just the excess over $21.

Qualified parking benefits. The value of employer-provided parking spots or subsidized parking qualifies for the exclusion (up to the monthly limit) if the parking is on or near the employer’s premises, or at a mass transit facility such as a train station or car pooling center. For purposes of determining if the value of the parking exceeds the monthly limit ($255 per month in 2017), the IRS tells employers to value parking benefits according to the regular commercial price for parking at the same or nearby locations. For example, if an employer in a rural or suburban location provides free parking for employees and there are no commercial parking lots in the area, the employee parking is tax free. Where free parking is available to both business customers and employees, the employee parking is considered to have “zero” value unless the employee has a reserved parking space that is closer to the business entrance than the spaces allotted to customers.

If the value of the right of access to a parking space for a month exceeds the monthly exclusion limit ($255 per month in 2017), an employee will be taxed on the excess even if he or she actually uses the space for only a few days during the month.

If the employee pays a reduced monthly price for parking, there is a taxable benefit for that month only if the price paid plus the monthly exclusion amount is less than the value of the parking.

Commuter parking benefits for self-employed partners, independent contractors, or more-than-2% S corporation shareholders do not qualify for the monthly exclusion but may qualify as a tax-free de minimis benefit (3.10).

Qualified bicycle commuting reimbursements. Reimbursements for the cost of a bicycle used for commuting, and for storing, repairing and improving the bicycle, are tax free up to $20 per qualifying month. A qualifying reimbursement may be made until March 31 of the following year.

However, the restrictive definition of “a qualifying month” may block the benefit of the excluion for many employees. The exclusion is allowed only for months in which the employee (1) regularly uses the bicycle for a substantial portion of the commute from home to the place of employment, and (2) does not receive either transit pass/commuter vehicle benefits or parking benefits.

Because of the second condition, an employee who bicycles from home to a train or bus station and continues his or her commute from there cannot get the bicycle exclusion for any month for which he or she takes advantage of the transit pass/commuter vehicle benefit.

3.9 Working Condition Fringe Benefits

An employer-provided benefit that would be deductible by you if you paid for it yourself (19.3) is a tax-free working condition fringe benefit. These benefits include:

Company car or plane. The value of a company car or plane is tax free to the extent that you use it for business; see 3.8 for more on company cars.

Employer-provided cell phone. The cost of an employer-provided cell phone is a tax-free working condition benefit if your employer has substantial business reasons for giving you the phone. The phone qualifies if the employer needs to reach you at all times for work-related emergencies or you need to call clients when away from the office or outside of normal business hours. On the other hand, the value of the phone is taxable if it is a goodwill gesture or intended as additional compensation; these are not considered substantial business reasons.

Employer-paid subscriptions or memberships. For example, if your employer pays for your subscriptions to business-related publications, or reimburses you for membership dues in professional associations, these are tax-free working condition benefits.

Product testing. This is a limited exclusion for employees who test and evaluate company manufactured goods away from company premises.

Employer-provided education assistance. Employer-paid undergraduate and graduate courses may be a tax-free working condition fringe benefit if the courses maintain or improve your job skills but are not needed to meet your employer’s minimum educational requirements and do not prepare you for a new profession.

Job-placement assistance. According to the IRS, job placement services are tax free so long as they are geared to helping you find a job in the same line of work and you do not have an option to take cash instead of the benefits. The employer must also have a business purpose for providing such assistance, such as maintaining employee morale or promoting a positive business image.

For tax-free treatment, there is no nondiscrimination requirement; different types of job placement assistance may be offered, or no assistance at all, in the case of discharged employees with readily transferable skills. Tax-free benefits include the value of counseling on interviewing skills and resume preparation. Executives may be given secretarial support and the use of a private office during the job search.

Job placement benefits that you receive as part of a severance pay arrangement are taxable to the extent that you could have elected to receive cash. If your severance benefits are reduced because you get job placement assistance, you are taxed on the difference between the reduced and unreduced severance amounts. Taxable benefits, if any, can be offset with a deduction only if you itemize and are able to claim the amount as a miscellaneous deduction subject to the 2% of adjusted gross income floor (19.3).

3.10 De Minimis Fringe Benefits

Small benefits that would be administratively impractical to tax are considered tax-free de minimis (minor) fringe benefits. Examples are personal use of an employer-provided cell phone (see below), occasional meal money or local transportation fares given to employees working overtime, employer-provided coffee, tea, doughnuts, or soft drinks, personal use of company copying machines, company parties, or tickets for the theater or sporting events.

Personal use of employer-provided cell phone. If your employer gives you a phone for substantial business reasons, the value of the phone is a tax-free working condition fringe benefit (3.9). In such a case, your personal use of the phone is tax free as a de minimis benefit.

Company eating facility. The value of meals provided to employees on workdays at a subsidized eating facility is a tax-free de minimis fringe benefit if the facility is located on or near the business premises and the annual revenue from meal charges equals or exceeds the facility’s direct operating costs. Revenue is treated as equal to operating costs for meals that are tax-free to employees under the employer convenience test (3.13).

Highly compensated employees or owners with special access to executive dining rooms may not exclude the value of their meals as a de minimis fringe benefit; however, the meals may be tax free if meals must be taken on company premises for business reasons (3.13).

Commuting under unsafe circumstances. If you are asked to work outside your normal working hours and due to unsafe conditions your employer provides transportation such as taxi fare, the first $1.50 per one-way commute is taxable but the excess over $1.50 is a tax-free de minimis benefit. This exclusion is not available to certain highly compensated employees and officers, corporate directors, or owners of 1% or more of the company.

Even when working their regular shift, hourly employees eligible for overtime who are not considered highly compensated are taxed on only $1.50 per one-way commute if their employer pays for car service or taxi fare because walking or taking public transportation to or from work would be unsafe. The excess value of the transportation over $1.50 is tax free. These rules can apply to day-shift employees who work overtime as well as night-shift employees working regular hours so long as transportation is provided because of unsafe conditions.

3.11 Employer-Provided Retirement Advice

If your employer maintains a qualified retirement plan, the value of retirement planning information and advice provided to you by the employer is not taxable. The exclusion is not limited to information pertaining to the employer’s particular retirement plan. It applies to information for you and your spouse on general retirement income planning, as well as information on how the employer’s plan fits within your overall plan.

Highly compensated employees qualify for the exclusion if similar services are provided to all employees who normally receive information updates on the employer’s retirement plan.

The exclusion does not apply to related services that may be provided by the employer, such as brokerage services, tax preparation, accounting, or legal services; the value of such services is taxable.

3.12 Employee Achievement Awards

Achievement awards are taxable unless they meet special rules for awards of tangible personal property (such as a watch, television, or golf clubs) given to you in recognition of length of service or safety achievement. Cash awards, gift certificates, and similar items are taxable.

As a general rule, if your employer is allowed to deduct the cost of a tangible personal property award, you are not taxed. The employer’s deduction limit, and therefore the excludable limit for you, is $400 for awards from nonqualified plans and $1,600 for awards from qualified plans or from a combination of qualified and nonqualified plans. If your employer’s deduction is less than the item’s cost, you are taxed on the greater of: (1) the difference between the cost and your employer’s deduction, but no more than the award’s fair market value; or (2) the excess of the item’s fair market value over your employer’s deduction. Deduction tests for achievement awards are discussed in 20.26. Your employer must tell you if the award qualifies for full or partial tax-free treatment.

An award will not be treated as a tax-free safety achievement award if employee safety achievement awards (other than those of de minimis value) during the year have already been granted to more than 10% of employees (not counting managers, administrators, clerical employees, or other professional employees). An award made to a manager, administrator, clerical employee, or other professional employee for safety achievement does not qualify for tax-free treatment.

Tax-free treatment also does not apply when you receive an award for length of service during your first five years of employment or when you previously received such an award during the current year or in the four preceding years, unless the prior award qualified as a de minimis fringe benefit.

3.13 Employer-Furnished Meals or Lodging

The value of employer-furnished meals is not taxable if furnished on your employer’s business premises for the employer’s convenience. The value of lodging is not taxable if, as a condition of your employment, you must accept the lodging on the employer’s business premises for the employer’s convenience.

Business premises test. The IRS generally defines business premises as the place of employment, such as a company cafeteria in a factory for a cook or an employer’s home for a household employee. The Tax Court has a more liberal view, extending the area of business premises beyond the actual place of business in such cases as these:

- A house provided a hotel manager, although located across the street from the hotel. The IRS has agreed to the decision.

- A house provided a motel manager, two blocks from the motel. However, a court of appeals reversed the decision and held in the IRS’ favor.

- A rented hotel suite that is used daily by executives for a luncheon conference.

Remote camp in foreign country. Lodging in certain foreign “camps” is considered to be furnished on the business premises of the employer. To qualify, lodging must be provided to employees working in remote foreign areas where satisfactory housing is not available on the open market, it must be located as near as practicable to where they work, and it must be in a common area or enclave that is not available to the public and which normally accommodates at least 10 employees.

Convenience of employer test. The employer convenience test requires proof that an employer provides the free meals or lodging for a business purpose other than providing extra pay. In the case of meals, the employer convenience test is deemed to be satisfied for all meals provided on employer premises if a qualifying business purpose is shown for more than 50% of the meals. If meals and lodging are described in a contract or state statute as extra pay, this does not bar tax-free treatment provided they are also furnished for other substantial, noncompensatory business reasons; for example, you are required to be on call 24 hours a day, or there are inadequate eating facilities near the business premises.

Meal charges. Your company may charge for meals on company premises and give you an option to accept or decline the meals. However, by law, the IRS must disregard the charge and option factors in determining whether meals that you buy are furnished for noncompensatory business reasons. If such business reasons exist, the convenience-of-employer test is satisfied. If such reasons do not exist, the value of the meals may be tax free as a de minimis benefit (3.10); otherwise, the value of the meal subsidy provided by the employer is taxable.

Where your employer provides meals on business premises at a fixed charge that is subtracted from your pay whether you accept the meals or not, the amount of the charge is excluded from your taxable pay. If the meal is provided for the employer’s convenience, as in the previous Examples, the value of the meals received is also tax free. If it is not provided for the employer’s convenience, the value is taxable whether it exceeds or is less than the amount charged.

Lodging must be condition of employment. This test requires evidence that the lodging is necessary for you to perform your job properly, as where you are required to be available for duty at all times. The IRS may question the claim that you are required to be on 24-hour duty. For example, at one college, rent-free lodgings were provided to teaching and administrative staff members, maintenance workers, dormitory parents who supervised and resided with students, and an evening nurse. The IRS ruled that only the lodgings provided to the dorm parents and the nurse met the tax-free lodging tests because, for the convenience of the college, they had to be available after regular school hours to respond to emergencies.

If you are given the choice of free lodging at your place of employment or a cash allowance, the lodging is not considered to be a condition of employment, and its value is taxable.

If the lodging qualifies as tax free, so does the value of employer-paid utilities such as heat, electricity, gas, water, sewerage, and other utilities. Where these services are furnished by the employer and their value is deducted from your salary, the amount deducted is excluded from taxable wages on Form W-2. But if you pay for the utilities yourself, you may not exclude their cost from your income.

Groceries. An employer may furnish unprepared food, such as groceries, rather than prepared meals. Courts are divided on whether the value of the groceries is excludable from income. One court allowed an exclusion for the value of nonfood items, such as napkins and soap—as well as for groceries—furnished to a doctor who ate at his home on the hospital grounds so that he would be available for emergencies.

Table 3-3 Are Your Meals and Lodging Tax Free?

|

Yes— |

No— |

Hotel executives, managers, housekeepers, and auditors who are required to live at the hotel. Domestics, farm laborers, fishermen, canners, seamen, servicemen, building superintendents, and hospital and sanitarium employees who are required to have meals and lodging on employer premises. Restaurant and other food service employees who have meals furnished during or immediately before or after working hours. Employees who must be available during meal periods for emergencies. Employees who, because of the nature of the business, must be given short meal periods. Workers who must use company-supplied facilities in remote areas. Park employees who voluntarily live in rent-free apartments provided by a park department in order to protect the park from vandalism. |

Your employer gives you a cash allowance for your meals or lodgings. You have a choice of accepting cash or getting the meals or lodging. For example, under a union contract you get meals, but you may refuse to take them and get an automatic pay increase. A state hospital employee is given a choice. He or she may live at the institution rent free or live elsewhere and get extra pay each month. Whether he or she stays at the institution or lives outside, the extra pay is included in his or her income. A waitress, on her days off, is allowed to eat free meals at the restaurant where she works. |

Cash allowances. A cash allowance for meals and lodging is taxable.

Faculty lodging. Teachers and other employees (and their spouses and dependents) of an educational institution, including a state university system or academic health center, do not have to pay tax on the value of school-provided lodging if they pay a minimal rent. The lodging must be on or near the campus. The minimal required rent is the smaller of: (1) 5% of the appraised value of the lodging; or (2) the average rental paid for comparable school housing by persons who are neither employees nor students. Appraised value must be determined by an independent appraiser and the appraisal must be reviewed annually.

For purposes of the 5% minimum rent rule, academic health centers include medical teaching hospitals and medical research organizations with regular faculties and curricula in basic and clinical medical science and research.

Peace Corps and VISTA volunteers. Peace Corps volunteers working overseas may exclude subsistence allowances from income under a specific code provision. The law does not provide a similar exclusion for the small living expense allowances received by VISTA volunteers.

3.14 Minister’s Housing or Housing Allowance

By statute, a duly ordained minister pays no tax on the rental value of a home provided as part of his or her pay. If a minister is provided with a cash allowance rather than a home itself, the allowance is generally tax free if used to pay rent, to make a down payment to buy a house, to pay mortgage installments, or for utilities, interest, tax, and repair expenses of the house. However, the exclusion for a cash allowance is limited to the fair rental value of the home, including furnishings and appurtenances such as a garage, plus the cost of utilities. A rabbi or cantor is treated the same as a minister for purposes of the allowance or in-kind housing exclusion.

The Tax Court has held that the parsonage exclusion is allowed for expenses of a second home as well as for a principal residence. However, the Eleventh Circuit appeals court reversed the Tax Court, concluding that the exclusion can apply only to one home.

The church or local congregation must officially designate the part of the minister’s compensation that is a rental or housing allowance. To qualify for tax-free treatment, the designation must be made in advance of the payments. Official action may be shown by an employment contract, minutes, a resolution, or a budget allowance.

Who qualifies for the exclusion? Tax-free treatment is allowed to ordained ministers, rabbis, and cantors who receive in-kind housing or housing allowances as part of their compensation for ministerial duties. Retired ministers qualify if the housing or allowance is furnished in recognition of past services.

The IRS has allowed the exclusion to ministers working as teachers or administrators for a parochial school, college, or theological seminary which is an integral part of a church organization. A traveling evangelist was allowed to exclude rental allowances from out-of-town churches to maintain his permanent home. Church officers who are not ordained, such as a “minister” of music (music director) or “minister” of education (Sunday School director), do not qualify.

The IRS has generally barred an exclusion to ordained ministers working as executives of nonreligious organizations even where services or religious functions are performed as part of the job. The Tax Court has focused on the duties performed. A minister employed as a chaplain by a municipal police department under church supervision was allowed a housing exclusion, but the exclusion was denied to a minister-administrator of an old-age home that was not under the authority of a church and a rabbi who worked for a religious organization as director of inter-religious affairs.

Allowance subject to self-employment tax. Although a qualifying housing allowance is not treated as taxable income, the exempt amount is included as self-employment income for Social Security and Medicare purposes; see Chapter 45. If you do not receive a cash allowance, report the rental value of the parsonage as self-employment income. Rental value is usually equal to what you would pay for similar quarters in your locality. Also include as self-employment income the value of house furnishings, utilities, appurtenances supplied—such as a garage—and the value of meals furnished that meet the rules in 3.13.

Business expenses allocable to tax-free housing not deductible. A minister may deduct business expenses allocable to taxable compensation, but not expenses allocable to a tax-free housing allowance or in-kind housing. If part of a minister’s salary is designated as a housing allowance, and the minister also has self-employment earnings from the exercise of his ministry, a double allocation is required, first between salary income and self-employment income, and then between the taxable and tax free parts of salary.

For example, in one case a minister had self-employment income comprising 21.56% of his annual income. Of the rest, 53.85% was a tax-free housing allowance and 46.15% was taxable salary. The Tax Court agreed with the double allocation required by the IRS. Since the minister did not provide evidence as to which expenses were generated by which type of income, the Court allocated expenses on a pro rata basis, applying the ratio of salary and self-employment income to total income. Since the self-employment income was 21.56% of total income (including the allowance), 21.56% of the expenses were deductible on Schedule C. The remaining expenses were treated as job-related costs deductible, if at all, as miscellaneous itemized expenses on Schedule A. However, because 53.85% of the minister’s salary was a tax-free housing allowance, 53.85% of the expenses were nondeductible. The balance (46.15% of the expenses) could be claimed on Schedule A as a miscellaneous itemized deduction subject to the 2% of adjusted gross income floor (19.3).

3.15 Cafeteria Plans Provide Choice of Benefits

“Cafeteria plans” is a nickname for plans that give an employee a choice of selecting either cash or at least one qualifying nontaxable benefit. You are not taxed when you elect qualifying nontaxable benefits, although cash could have been chosen instead. A cafeteria plan may offer tax-free benefits such as group health insurance or life insurance coverage, long-term disability coverage, dependent care or adoption assistance, medical expense reimbursements, or group legal services. Long-term care insurance may not be offered through a cafeteria plan under current law.

Employees may be offered a premium-only plan (POP), which allows them to purchase group health insurance coverage or life insurance on a pre-tax basis using salary-reduction contributions.

Health savings accounts (HSAs) and their related high-deductible health plans (HDHPs) may be offered as options by a cafeteria plan (3.2). If so, employees may elect to have contributions made to an HSA and an HDHP on a pre-tax salary-reduction basis.

A cafeteria plan may also offer benefits that are nontaxable because they are attributable to after-tax employee contributions. For example, employees may be offered the opportunity to purchase disability benefits (short term or long term) with after-tax contributions. If a covered employee subsequently receives disability benefits that are attributable to after-tax contributions, the benefits will be tax free. On the other hand, the plan may allow employees to elect paying for disability coverage on a pre-tax basis and, in this case, any benefits from the plan attributable to the pre-tax contributions will be taxable when received.

Under a flexible spending arrangement (FSA), employees may be allowed to make tax-free salary-reduction contributions to a medical or dependent care reimbursement plan (3.16).

A qualified cafeteria plan must be written and not discriminate in favor of highly compensated employees and stockholders. If the plan provides for health benefits, a special rule applies to determine whether the plan is discriminatory. If a plan is held to be discriminatory, the highly compensated participants are taxed to the extent they could have elected cash. Furthermore, if key employees (3.4) receive more than 25% of the “tax-free” benefits under the plan, they are taxed on the benefits. Employers averaging 100 or fewer employees who agree to contribute a fixed amount towards benefits are treated as meeting the nondiscrimination tests under special rules for “simple” cafeteria plans.