One of the major objectives of an ERP implementation is to provide clear business insights that can provide support for the organization's top management in the decision-making process. This requires analyzing the numbers, understanding them clearly, and then being able to examine the same numbers from different perspectives. Hence, a detailed structure is required to decide how an organization wants to analyze their numbers.

In this chapter, we will cover the following topics:

- Understanding the concept of financial dimensions

- Understanding the ledger account segmentation

- Posting types in Microsoft Dynamics AX

- Exploring dimension reporting

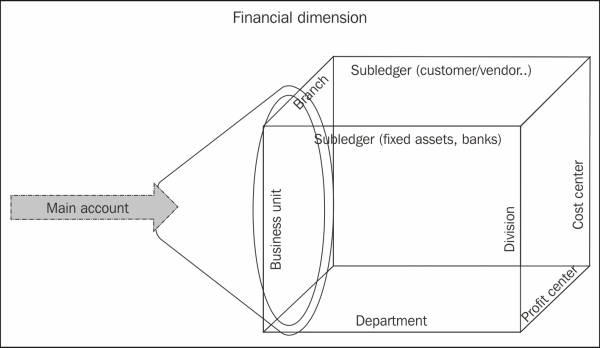

The main source of financial reporting is the main accounts. The components of financial reporting are a balance sheet, income statement, trial balance, cash flow, and so on. The normal scenario is that the main account's balances do not mean much when it comes to analysis. This is because the balance sheet account is a total of the posted transactions' amounts, and it is required to be able to dig into this total breakdown. In other words, it provides us with information on how this amount is allocated, for example, among business units and departments. This allocation gives the lowest level of analysis to break down the same balance for a main account by more than one dimensional perspective.

The following diagram shows the financial dimension allocation for the Main Account:

Financial dimensions provide us with a deeper analysis of the transactions posted on the general ledger accounts, where the financial dimension gives the controller an analytical view of the transactions that occurred on the expenses account. For example, one can analyze the account balance according to the financial dimensions assigned to the main account.

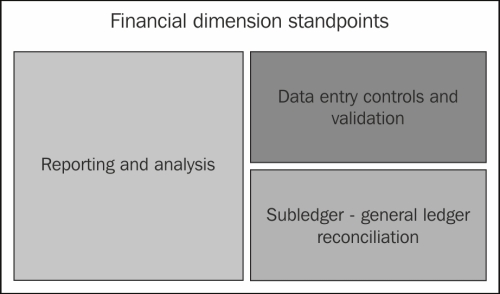

The Microsoft Dynamics AX 2012 financial dimension allows an organization to reach the lowest level of breakdown and analysis. There are three main standpoints to consider while discussing the financial dimension:

- The first standpoint is the required breakdown analysis for each main account in the chart of accounts in order for it to be utilized at the reporting level.

- The second standpoint is the controls and validations while doing the data entry in order to certify that the keyed-in transactions are allocated to the required dimensions before the transaction is posted. This directly affects the accuracy of reporting.

- The third standpoint is the reconciliation between the subledger and the general ledger, and the ability to break down the balance using the subledger (customers, vendors, items, banks, and so on).

These standpoints are shown in the following diagram:

The role of the Microsoft Dynamics AX consultant is to clarify the best usage of financial dimensions to the concerned parties. The key process owners who ascertain the financial dimensions' requirements are the Chief Financial Officer (CFO) and the financial controller. The three main standpoints of financial dimension can be summarized as follows:

The implementation team ascertains the financial dimensions' requirements during the analysis phase to understand what the business needs are at the reporting and analysis stage, and then identifies the required number of financial dimensions and how to utilize these dimensions.

According to the business domain, every business needs to build the structure of their chart of accounts and financial dimensions. They also need to identify which subledger should be tracked at the general ledger level. To build the structure of the chart of accounts and financial dimensions, follow the ensuing steps:

- Classify the required dimensions for each main account, whether it is mandatory or optional.

- Categorize the financial dimensions that are interrelated and are dependent on each other to filter dimensions based on the previously selected value.

- Categorize the intra-related dimensions. These are not dependent on the previously selected dimension.

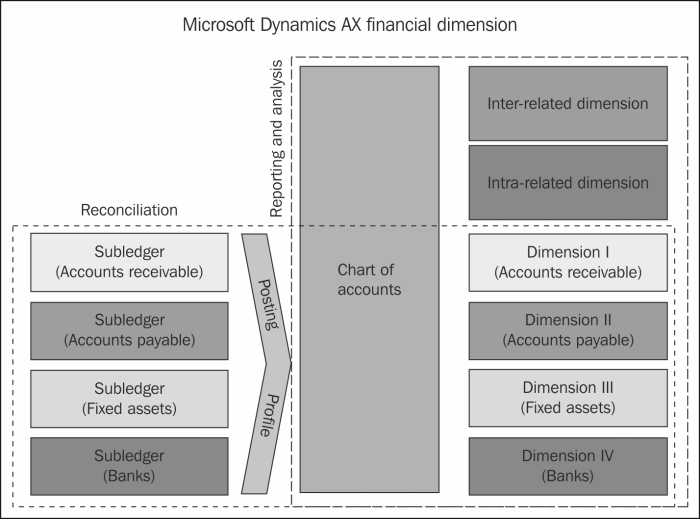

Microsoft Dynamics AX 2012 supports the use of the existing subledger master data to define financial dimensions. The following diagram illustrates the usage of financial dimensions in reporting and analysis, in addition to reconciliation:

The heart of a financial dimension is the chart of accounts, as shown in the previous diagram. It should be carefully structured and set to the required dimension validation of each main account. It is important to consider this structure of the chart of accounts and dimensions' validation in the opening balance upload, as it will affect reporting and analysis in addition to an automatic transaction, such as the exchange rate adjustment.

Note

Changing the financial dimension's structure and validation during operations should be wisely planned, evaluated, and executed as it may affect some historical transactions and some automatic transactions (for example, exchange rate adjustment, inventory adjustment, and settlement). It is recommended that you apply it at the beginning of a month when all historical transactions, along with the old structure and validation, are closed.