This chapter focuses on project cost management. Project cost management, like the other knowledge areas, begins with a process of planning that produces a cost management plan. Then there is an iterative process that produces and updates the cost estimates and cost baseline. After these have been developed, a monitoring and controlling process is used to measure actual versus planned cost performance and to manage any change requests.

You may need to pay particular attention in this chapter to the activities involved in calculating earned value management, because there is quite a bit of technical information you need to learn.

The PMBOK

®

Guide Processes

Project Cost Management Knowledge Area

The four processes

in the Project Cost Management knowledge area are as follows:

- Plan Cost Management (planning process)

- Estimate Costs (planning process)

- Determine Budget (planning process)

- Control Costs (monitoring and controlling process)

What Is Project Cost Management?

Project cost

management is focused on the processes of developing a cost management plan, the processes of estimating costs for activities and the overall project, preparing your project budget or cost baseline, recording performance, and influencing and assessing any changes to the project budget.

Exam Tip

Although presented as discrete processes, the two processes of estimating costs and determining budget are usually done concurrently.

The processes contained in this knowledge area present a logical and sequential flow of information from estimating costs through controlling changes to your project budget. Figure 5-1 shows the general flow through this linear process without the general initial Plan Cost Management process.

Figure 5-1.

The project cost baseline development process flow

REAL WORLD

I have always found that developing the project cost estimates and the approved cost budget is one of the most iterative parts of project management. You start out with high-level estimates based on incomplete information and constantly revise and refine both the information you have and the estimates based on the information. When you check how progress is going, you may need to revisit your estimates and revise individual cost estimates. Because of this iterative nature and the high expectations of stakeholders regarding project costs, I pay extra attention to the cost management processes.

Plan Cost Management

More Info

Plan Cost Management

You can read more about the Plan Cost Management process in the PMBOK Guide, 5th edition, in Chapter 7, section 7.1. Table 5-1 identifies the process inputs, tools and techniques, and outputs.

Table 5-1.

Plan Cost Management Process

Inputs ➪ | Tools and Techniques ➪ | Outputs |

|---|---|---|

• Project management plan • Project charter • Enterprise environmental factors • Organizational process assets | • Expert judgment • Analytical techniques • Meetings | • Cost management plan |

Exam Tip

Did you notice that the inputs, tools, and techniques for the Plan Cost Management process are identical to the inputs, tools, and techniques for the Plan Schedule Management process? The only difference between the two processes is the single output.

The Plan Cost Management process is a planning process with a single output: the cost management plan. Like all other planning documents, the cost management plan guides your efforts in defining and controlling the project budget. It forms a subsidiary plan to the overall project management plan.

The Plan Cost Management process covers the following planning domain task

:

- Task 3: Develop the cost management plan based on the project scope, schedule, resources, approved project charter and other information, using estimating techniques, in order to manage project costs.

Inputs

The Plan Cost Management process uses some or all of the following inputs as part of the development of the cost management plan for the project.

Project Management Plan

The distinct elements of the project management plan that are useful in developing your own cost management plan are the scope and schedule information contained in the scope baseline and schedule baseline, respectively. After it is created, the cost management plan becomes part of the project management plan. The project management plan is an output from the Develop Project Management Plan process.

Project Charter

The project charter

contains the approved initial budget for the project at the time of project initiation. It also contains known constraints, assumptions, and risks that may affect project costs and their management. The project charter is an output from the Develop Project Charter process.

Enterprise Environmental Factors

Particular enterprise environmental factors

that may assist with development of your cost management plan include the particular organizational culture and structure, any external market conditions that may affect project costs, and any published commercially available cost information that you may use to develop and check your cost estimates.

Organizational Process Assets

Organizational process assets

that may play an important part in the development of your cost management plan include any historical information and any established financial control procedures, policies, and templates for defining and controlling project costs and budget.

Exam Tip

It is important to note that in your day-to-day work you may use the terms cost and budget interchangeably. However, for the purposes of this exam, you must understand that the two words have separate meanings. Cost refers to the actual costs of each activity or work package, which, when aggregated, form a total project cost. Budget, on the other hand, refers to costs over time.

REAL WORLD

One way to keep your accounts people very happy is to be proactive with the development of your project budget. If you are able to tell them clearly when you expect to spend money and when you expect to have money come in, they can better plan the organization’s cash flow requirements. It is important to realize that as a project manager, your project may impose serious cash flow problems on the wider organization, and the accounts people have to figure out how to make sure money is available when you need it. I have always found that giving the accounts people information early and often about when I plan to use money is a great way to manage this particular group of stakeholders.

Tools and Techniques

The following tools and techniques are available to be used to develop the inputs into this process in order to produce the cost management plan.

Expert Judgment

Expert judgment

is used as a tool and technique in the Plan Cost Management process as again you rely on the experience, opinion, and expertise of individuals to assist with the development of a cost management plan. The experts you consult may be members of your project team, other employees in your organization, or people from outside your organization with particular experience in putting together an appropriate cost management plan.

Analytical Techniques

Analytical techniques

are an important tool in the development of your cost management plan because you or your financial department must analyze options and make decisions about how the project will be funded. You may be able to fund the project with cash reserves, bank loans, funding with equity from shareholders, or funding with debt from other sources. Each of these options has its own benefits and drawbacks. In making the decision, you can use a number of techniques such as payback period, return on investment, internal rate of return, discounted cash flow, and net present value. Each of these terms was discussed in more detail in the Develop Project Charter process as part of the project selection process.

REAL WORLD

I have found that many project managers are completely oblivious to how the project is going to be funded. I believe an important skill that any project manager should have is an understanding of project financing methods and the implications of different finance sources for project costs. One of the first places to look for guidance about funding criteria and sources of potential funding is the project charter.

Meetings

Meetings

are a great way to bring together members of the project team who have expertise and skill in development of the cost management plan, because they are the people completing the work. You may also choose to invite selected stakeholders from outside the project team who have specialist knowledge and skills in this particular area. An example would be inviting members of your organization’s financial or accounts department to contribute to the development of the cost management plan.

Outputs

After the appropriate tools and techniques have been applied to the selected inputs, the Plan Cost Management process has the following output.

Cost Management Plan

The Plan Cost Management process has only a single output: the cost management plan. The cost management plan is a subsidiary plan of the project management plan and is used as a guide for the other cost management processes. The purpose of the cost management plan is to provide guidance to the project manager and the project team on how the organization expects costs to be estimated, budgets to be determined, cost performance to be assessed, and any potential changes assessed, documented, and reported on. It also outlines the process of reporting progress in relation to forecast cost versus actual cost for the project and prescribes acceptable tools, techniques, processes, and any other relevant information relating to how costs will be managed on the project.

The cost management plan is then a key input into the Estimate Costs and Determine Budget processes

, both of which are planning processes.

Quick

Check

1.

What is the main purpose of the cost management plan?

2.

What is the main reason for using analytical techniques during the Plan Cost Management process?

3.

What sort of organizational process assets would be useful as inputs into the Plan Cost Management process?

Quick Check Answers

1.

The main purpose of the cost management plan is to provide guidance on further planning of project costs, estimating costs, developing a project budget, checking planned cost performance against actual cost performance, and managing any potential changes to the cost baseline.

2.

Analytical techniques are used as a tool to help assess the different options, and the pros and cons of each, for funding or financing the project.

3.

The types of organizational process assets that are useful as inputs into the Plan Cost Management process include any existing organizational financial control procedures, blank templates, established processes, gathered historical cost information, and any internal financial databases.

Estimate Costs

More Info

Estimate Costs

You can read more about the

Estimate Costs process in the PMBOK Guide, 5th edition, in Chapter 7, section 7.2. Table 5-2 identifies the process inputs, tools and techniques, and outputs.

Table 5-2.

Estimate Costs Process

Inputs ➪ | Tools and Techniques ➪ | Outputs |

|---|---|---|

• Cost management plan • Human resource management plan • Scope baseline • Project schedule • Risk register • Enterprise environmental factors • Organizational process assets | • Expert judgment • Analogous estimating • Parametric estimating • Bottom-up estimating • Three-point estimating • Reserve analysis • Cost of quality • Project management software • Vendor bid analysis • Group decision-making techniques | • Activity cost estimates • Basis of estimates • Project document updates |

The Estimate Costs process is a planning process that uses the cost management plan for guidance, takes the defined activities and work packages, and assigns a cost estimate for each one using a variety of tools and techniques. In order to easily track which estimates are for which particular work package, you can use the numbering systems from the work breakdown structure (WBS). This is a highly iterative process that is repeated throughout the life of the project.

The Estimate Costs process covers the following planning domain task

:

- Task 3: Develop the cost management plan based on the project scope, schedule, resources, approved project charter and other information, using estimating techniques, in order to manage project costs.

In assessing the estimate for each activity, it is important to have a basic understanding of different types of costs that may be estimated.

Variable costs

are costs that change with the amount of production. The more you produce, the more costs you incur. For example, if you increase the number of homes you are building, you will use more home-building materials. If you use more electricity as a result of greater amounts of work, then your costs will increase.

Fixed costs

are costs that are fixed no matter how much you produce. For example, the rental you pay for your warehouse storage space is constant whether the warehouse is full or empty. Also, the costs you pay for any consents you require or equipment needed to complete the job are fixed costs.

Direct costs

are costs attributable directly to the actions of the project. For example, the materials you use on your project are direct costs.

Indirect costs

are costs that are not incurred directly by the project but that the project may have to account for. For example, the project may have to make provision for paying a share of corporate overheads such as office rental space and shared services. Your cost management plan may contain guidelines on what portion, if any, of indirect costs you must account for in your cost estimates. These are often referred to as overheads.

REAL WORLD

Indirect costs, or overheads, are often overlooked by project managers when preparing their cost estimates. Unless there are clear guidelines from the organization about what portion, if any, of indirect costs the project must account for, many project managers simply do not think about this. Many organizations account for indirect costs in required margins or profits. Hopefully, your organizational process assets include guidance on how you are expected to manage this issue.

Sunk costs are costs spent on the project to date that cannot be recovered if the project were to stop. For example, the money you have spent developing code for a new piece of software is a sunk cost if you stop halfway through, because it has no recoverable value. Your cost management plan may contain guidelines on how sunk costs are treated in determining whether to continue on a troubled project.

All estimates are simply your best guess at the future, based on the information available to you. The better the information you have, the better the estimates will be. Thus, there is nearly always an element of uncertainty inherent in any estimate. It is often important to express this range of uncertainty inherent in any estimate. As a rule, the accuracy of cost estimates improves as the project progresses, and your organization may have, as part of its organizational process assets, guidelines on the necessary level of accuracy required before proceeding. Table 5-3 shows the typical description of a variety of estimate ranges

.

Table 5-3.

Range of Estimates

Estimate Type | Estimate Range |

|---|---|

Order of magnitude estimate | -50% to +100% |

Rough order of magnitude estimate | -25% to +75% |

Conceptual estimate | -30% to +50% |

Preliminary estimate | -20% to +30% |

Definitive estimate | -15% to +20% |

Control estimate | -10% to +15% |

Inputs

The Estimate Costs process uses some or all of the following seven inputs.

Cost Management Plan

The cost management plan

is obviously a key input into the Estimate Costs process, because it provides the guidance for how you are going to complete this process. Without it, you would not be able to complete the process. The cost management plan is an output from the Develop Cost Management Plan process.

Human Resource Management Plan

The

human resource management plan

is used as an input into the Estimate Costs process because it contains information about the project staff who will be working on the project and the charge-out rates, remuneration packages, and any other financial rewards to be paid to them. In order to develop the project cost, you need to know this information. The human resource management plan is an output from the Plan Human Resource Management process.

Scope Baseline

The scope baseline

is composed of the project scope statement, the work breakdown structure (WBS), and the WBS dictionary, and it contains a full and detailed description of all the work to be done on the project. By using this information, you can attribute costs to each of the work packages and also the activities taken from the project schedule, and aggregate these costs into a total project cost estimate. The scope baseline is an output from the Create WBS process.

Project Schedule

The project schedule

is an important input into the Estimate Costs process because it gives an indication of when the work packages and activities are to be completed. The sequencing, timing, and duration of distinct project work packages and activities affect the costs. The project schedule is an output from the Develop Project Schedule process, which in itself is the culmination of the other schedule management planning processes.

Risk Register

The risk register

is used as an input into the Estimate Costs process because it contains information around defined and documented uncertainty relating to specific work packages. This uncertainty is captured in the contingency reserve for each activity work package and needs to be taken into account in developing the project cost estimates. The risk register is an output from the Identify Risks process.

Enterprise Environmental Factors

The specific types of enterprise environmental factors

that are useful as inputs into the Estimate Costs process are external market conditions that will affect the prices of products and services being procured for the project, and any published commercially available estimating data.

REAL WORLD

It is worthwhile to carefully subscribe to, and pay for access to, reputable published estimating databases. These databases are usually very accurate sources of information about the costs of particular materials and resources, and they are often separated into regional areas to determine variances at a local level. Many organizations, industry associations, and professional bodies compile these databases and allow access for a fee.

Organizational Process Assets

The specific types of organizational process assets

that are useful as inputs into the Estimate Costs process are any relevant templates and processes useful in the development of project cost estimates, including any historical information and lessons learned owned by the organization.

Tools and Techniques

The following ten tools and techniques are used on the inputs to deliver the process outputs.

Expert Judgment

The use of experts is an acknowledged tool in the preparation of project cost estimates. The experts, or people working on the project, have intimate knowledge of the work to be done and the likely cost of that work. In addition to project team members with expert judgment on the work to be done, you may also choose to consult external experts, such as those involved in the quantity surveying profession, who can provide expert advice on the expected costs of materials and resources to be used.

Analogous Estimating

Analogous estimating

is a quick means of estimating a likely cost for a particular material or resource by comparing your current requirements with the requirements of a previous project you have information on, and then looking at the similarities between the two instances to determine your current estimate. For example, if on a previous project you used a particular amount of concrete and it cost $1,500, and on this project you expect to use twice as much, you would assume that your cost estimate is $3,000, by using analogous estimating. Because you are using an analogy from previous experience, there is a certain degree of expected inaccuracy in this form of estimating.

Parametric Estimating

Parametric estimating

is generally considered to be more accurate than analogous estimating because it uses known quantities of materials for resources and multiplies them by known financial rates. For example, you may know that you require 50 hours of work to be done by a business analyst, and that a business analyst costs $80 an hour; therefore, multiplying 50 hours by $80 an hour, you will arrive at a cost estimate of $4,000 by using parametric estimating.

Bottom-Up Estimating

Bottom-up estimating

is generally considered to be quite an accurate form of estimating. You take cost estimates from lower-level information—for example, the bottom level of the WBS—and then add up, or roll up, to higher levels and aggregate those costs to report a total cost.

Three-Point Estimating

You saw the use of three-point estimating

in the Estimate Activity Durations process from the Schedule Management knowledge area. Here it is used again as a method of determining an estimate where there is a most likely (cM), an optimistic (cO), and a pessimistic (cP) cost estimate for an activity.

Exam Tip

Although the correct name for the formula is the three-point estimate, and it is part of the Program Evaluation and Review Technique (PERT), it is often simply called the PERT formula.

To get a simple average, which is used with a triangular distribution, you take these three figures and add them together and divide by 3. The formula is

However, if you want to get a weighted average that gives greater weight to the most likely (cM) figure and is typical of a beta distribution, the formula to use is

For example, if you have an optimistic cost estimate of $10, a most likely cost estimate of $16, and a pessimistic cost estimate of $25, the weighted average using three-point estimating is $16.50.

You can also calculate the standard deviation, which indicates how far from the average the optimistic and pessimistic figures are. A smaller standard deviation means they are closer to the average than a larger standard deviation. The formula for standard deviation is

For example, using the numbers from the previous example, the standard deviation is $2.50.

After you have determined the standard deviation, you can then express your certainty about a cost estimate range. You express this certainty as a confidence interval, where one standard deviation either side of the mean represents a confidence interval of 68%, two standard deviations either side of the mean gives a confidence interval of 95%, and three standard deviations either side of the mean gives a confidence interval of 99.7%.

For example, using the numbers from the previous example, you could say that you have a 95% certainty that the cost for the activity will be between $11.50 and $21.50.

REAL WORLD

In reality, when you are completing any sort of estimating process in the project, you will use a variety of estimating techniques. The type of estimating technique you choose to use will depend on how much information you have. At the beginning of a project, when information is generally less available, you may choose to use less accurate forms of estimating. As the project progresses and you have more information available, you may choose to use more accurate and time-consuming forms of estimating for work you have greater information about. In relation to rolling-wave planning, you will most likely use more accurate forms of estimating on the work to be done in the immediate future and less accurate forms of estimating on work to be done further off in the future.

Reserve Analysis

Reserve analysis

looks at the contingency reserves, or contingency allowances, provided for in the project cost estimates. The contingency reserve is an amount that reflects and allows for identified uncertainty in estimating particular costs. It is commonly known as “accounting for the known unknowns” in any project and is usually calculated during quantitative risk analysis performed as part of the Risk Management knowledge area. For example, you may determine that a particular activity has a 10% chance of experiencing a $1,750 cost overrun, and therefore you allow $175 ($1,750 × 10%) in the contingency reserve. By aggregating, or adding up, all the individual amounts allowed for in the contingency reserve analysis, you arrive at a total contingency reserve for the entire project.

The management reserve for unknown unknowns can also be calculated during risk assessment or by expressing the range of uncertainty in your estimates as a total amount. The management reserve is controlled by senior managers, and the project manager must apply to use it; it is not part of the approved budget.

REAL WORLD

In theory, the contingency reserve should be part of the approved project budget and under the control of the project manager, and the management reserve should be under the control of senior management or members of the steering group. In reality, you may find that your approved budget is just for known costs and that sponsors can sometimes be reluctant to approve reserve budgets, because they view it as endorsing inaccuracy and sloppy estimating practices. My argument is that I prefer to go forward on a “no surprises” basis and release the reserves once the identified uncertainty has been defined or passed.

Cost of Quality

As part of the preparation of your quality management plan, you need to consider the issue of cost of quality. Any decisions made about what this means to you will affect cost on the project immediately and for the organization after the project is handed over. Cost of quality refers to the quality attributes of the project and the product over the life of the product. For example, you may need to take into account the cost of future product returns or warranty claims because of decisions made to manufacture lower quality to lower the project costs.

Project Management Software

Project management software

should be considered essential for any large and complex projects, because trying to collect and aggregate many cost estimates manually is simply not possible.

Vendor Bid Analysis

The

vendor bid analysis

process is a way of double-checking the bids received from vendors to make sure they are neither overinflated nor underinflated. You can think of vendor bid analysis as your quality check on the prices people are submitting to you.

Group Decision-Making Techniques

Good cost estimates are prepared by people familiar with the activities being estimated, and when you get a group of these people together, you need effective group decision-making techniques to make sense of the expert opinions supplied. These techniques are also used when estimating elements of the project schedule and include brainstorming, nominal group techniques, and the Delphi technique.

Outputs

The Estimate Costs process produces some or all of the following outputs.

Activity Cost Estimates

The

activity cost estimates

are the individual estimates for each activity identified. They are the entire focus of this process and are used to put together your cost baseline. The activity cost estimates are used as an input into the Determine Budget process.

Basis of Estimates

The

basis of estimates

is a useful document because it outlines the assumptions made, the type of estimating technique used, any known constraints, and an indication of the range of uncertainty and of the confidence level of the final estimates for each activity and, indeed, the entire project. The basis of estimates is used as an input into the Determine Budget process.

Exam Tip

Several supporting documents provide additional information to summary documents. For the requirements documentation, you have the requirements traceability matrix. For the WBS, you have the WBS dictionary. For the activity list, you have the activity attributes. For the activity cost estimates, you have the basis of estimates. The summary document and the document containing greater detail are both important to provide a full picture.

Project Document Updates

The specific project documents

that may be updated as a result of estimating costs include such things as the statement of work, which may be updated as a result of the cost estimates, and elements of the risk register that are refined and updated as a result of specific cost estimates.

Quick Check

1.

What is the difference between a simple average and a weighted average?

2.

What is the difference between a contingency reserve and a management reserve?

3.

What information does the basis of estimates contain?

Quick Check Answers

1.

A simple average divides the most likely (cM), the optimistic (cO), and the pessimistic (cP) cost estimates by 3, whereas a weighted average gives a higher weighting of 4 to the most likely cost estimate and then divides by 6.

2.

A contingency reserve is prepared for the known uncertainty, or known unknowns, on a project and should be under the control of the project manager. A management reserve is prepared for the unknown uncertainty, for unknown unknowns, and is generally under the control of senior management.

3.

The basis of estimates contains information about the assumptions made in preparing cost estimates, the types of estimating techniques used, and the amount of uncertainty in the final activity cost estimates.

Determine Budget

More Info

Determine Budget

You can read more about the Determine Budget process in the PMBOK Guide, 5th edition, in Chapter 7, section 7.3. Table 5-4 identifies the process inputs, tools and techniques, and outputs.

Table 5-4.

Determine Budget Process

Inputs ➪ | Tools and Techniques ➪ | Outputs |

|---|---|---|

• Cost management plan • Scope baseline • Activity cost estimates • Basis of estimates • Project schedules • Resource calendars • Risk register • Agreements • Organizational process assets | • Cost aggregation • Reserve analysis • Expert judgment • Historical relationships • Funding limit reconciliation | • Cost baseline • Project funding requirements • Project document updates |

The Determine Budget process is a planning process that takes the individual activity cost estimates, aggregates them into a total project cost, and then applies the project schedule to determine the timing of when costs will be incurred in order to develop the project budget, or cost baseline.

The Determine Budget process covers the following planning domain task

:

- Task 3: Develop the cost management plan based on the project scope, schedule, resources, approved project charter and other information, using estimating techniques, in order to manage project costs.

Inputs

The inputs used in this process take the individual cost estimates and aggregate them into the project budget.

Cost Management Plan

The cost management plan

is used as a key input into the Determine Budget process because the cost management plan sets out the processes, policies, rules, and regulations that you will apply in order to determine a project budget. The cost management plan is an output from the Plan Cost Management process.

Scope Baseline

The scope baseline

is a very important input into this process because it outlines all the work to be done, and the work not to be done, as part of the project. By breaking down the scope baseline into its component parts via the WBS and subsequently down to activity level with the schedule of work, you can estimate individual activity costs. The scope baseline consists of the project scope statement, the WBS, and the WBS dictionary, and it is an output from the Create WBS process.

Activity Cost Estimates

The activity cost estimates

provide you with individual estimates of cost for identified activities by using a variety of tools and techniques from the Estimate Costs process. In order to put together your project budget, you take these individual activity estimates, aggregate them, and determine the time period in which those costs will be incurred. The activity cost estimates are an output from the Estimate Costs process.

Basis of Estimates

The basis of estimates

is an important input because it provides further information about each of the estimates you have determined for the individual activities. The basis of estimates is an output from the Estimate Costs process.

Project Schedule

The project schedule

is used as an input into the Determine Budget process because you need to know when each activity will be performed so that you can determine when the costs of activity will be incurred. This is the essence of developing a project budget: taking the project costs and applying them over time. The project schedule is an output from the Develop Schedule process.

Resource Calendars

Resource calendars

are used as an input into the Determine Budget process because they provide additional and more detailed information about when specific resources are available to work on the project. They are an output from the Acquire Project Team process.

Risk Register

The risk register

is used as an input into this process because it identifies risks associated with both individual activity cost estimates and elements of the project schedule that need to be taken into account when developing the project budget. It is an output from the Identify Risks process.

Agreements

Any existing agreements

are used by the project manager as an input into this process because they outline any agreement between parties to the project about costs, payments, and any other matters, such as retention payments, that need to be included in the project budget. For example, you may have an agreement for paying suppliers that requires payment regularly each month, or one that requires progress payments at certain project milestones. These agreements are an output from the Conduct Procurements process.

Organizational Process Assets

The specific organizational process assets

that can assist in the development of the project budget include any organizational policies and procedures relating to the development and presentation of the project budget, and any blank templates for preparing budgets and for reporting the budget.

Tools and Techniques

The five tools and techniques of this process are all used on the separate inputs to deliver the process outputs.

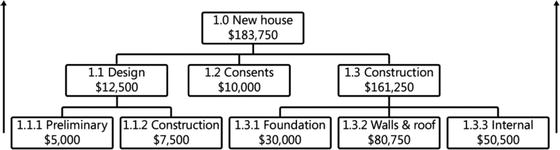

Cost Aggregation

Cost aggregation

is the process of taking the individual estimates for each of the activities, aggregating upward to the work package level, and then rolling these estimates up to high-level, sub-deliverable level, and deliverable level to arrive at a bottom-up estimate for portions of the project or the entire project. Figure 5-2 shows how individual activities are added up, or aggregated.

Figure 5-2.

An example of bottom-up cost aggregation

Reserve Analysis

Reserve analysis

is a method of looking at both the contingency reserve and the management reserve required for the project and the timing of access to those reserves. Contingency reserves are identified for specific uncertain activities, or known unknowns; access to the contingency reserve will be when the activity is being performed. The contingency reserve is approved as part of the project budget and is under the control of the project manager.

Access to the management reserve, which is for unknown unknowns, could be required at any time in the project. Use of the management reserve requires approval from management; once approved, it is added to the cost baseline.

Expert Judgment

Again, expert judgment

is a key tool and technique in determining the budget. The experts should be from the project team and also from outside the project team: for example, from the organization’s finance or accounts department.

Historical Relationships

If the organization is mature enough to have been recording information about historical relationships

and the reliability and range of uncertainty in its cost estimating process, it can use this information to further refine its current cost estimates or to acknowledge a quantifiable amount of uncertainty in those estimates.

Funding Limit Reconciliation

As part of the Determine Budget process, you may find that there are

funding limit reconciliation

issues that need to be considered. For example, you may want to do more work but simply will not have the funds until a later time; therefore, you have to limit the activity on the project until funds to complete the work become available.

REAL WORLD

It is important that you are able to determine how the project will be funded early on, and whether this funding process imposes any constraints on your project schedule. I have often found that there are constraints on when funds will be available, which is generally related to the financial years into which the funds are allocated. This is why the finance department of an organization is so interested in how much of your project budget you are spending, how much you are carrying over to the next financial year, and how much you want to bring forward into this financial year. You may not realize that someone has to find the finances to complete not only your project but all other projects the organization is completing.

Outputs

The major outputs from the Determine Budget process are the following.

Cost Baseline

The

cost baseline

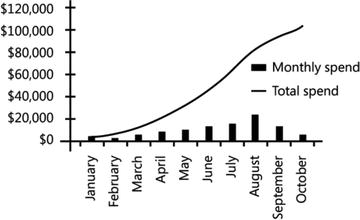

is one of four baselines you will use to measure progress on the project. The other three are the scope baseline, the time baseline, and the quality baseline. The key element of the cost baseline is that it takes the aggregated individual estimates of cost for each activity and applies them to the time periods in which the costs will be accrued. This is the baseline against which you will measure project cost performance. Figure 5-3 shows an example of a cost baseline represented graphically. It shows the total amount of spend for each time period, in this case in months. Additionally, it shows the cumulative spend over the life of the project. This is represented by the line, which is often referred to as the S-curve because it is in the shape of the letter S. There is little spend at the beginning of a project, a lot of spend in the middle section of the project, and a decrease in spending toward the end of the project.

Figure 5-3.

An example of a cost baseline

Exam Tip

Individual contingency reserve figures are added to the individual activity cost estimates. These are then aggregated and rolled up to work-package level, with the aggregated contingency reserve applied against individual work packages. The management reserve is added to the total cost baseline once management has approved its use. The only way you can use funds from the management reserve is to obtain approval by the documented and approved change-control process.

Project Funding Requirements

The

project funding requirements

acknowledge when the funding for the project will be available: for example, annually, quarterly, or monthly. This recognizes that funding for a project often occurs in incremental amounts, whereas expenditure on a project may be continuous.

REAL WORLD

Matching when funds will be available against when money will be spent is an important aspect of sound and prudent financial management for the project. You do not want to be in a situation where you have spent more than your ability to pay, because this may mean delays in paying creditors and ultimately delays to the project.

Project Document Updates

The types of project documents

that may be updated as a result of the Determine Budget process are the individual cost estimates, project schedule, and risk register.

Quick Check

1.

Why is the project schedule an important input into the Determine Budget process?

2.

How would you describe cost aggregation?

3.

Why are funding limit reconciliations and the project funding requirements important aspects of any project cost baseline?

Quick Check Answers

1.

The project schedule allows you to view the time period in which the project activities will be performed and their costs incurred.

2.

Cost aggregation is the process of adding up individual activity cost estimates up to the work-package level, then the sub-deliverable level, and then the deliverable level.

3.

Both the technique of funding limit reconciliation and the output of project funding requirements recognize that funds for the project may be incremental, whereas spending may be continuous, and therefore sometimes there are not enough funds to pay accrued expenses.

Control Costs

More Info

Control Costs

You can read more about the

Control Costs process in the PMBOK Guide, 5th edition, in Chapter 7, section 7.4. Table 5-5 identifies the process inputs, tools and techniques, and outputs.

Table 5-5.

Control Costs Process

Inputs ➪ | Tools and Techniques ➪ | Outputs |

|---|---|---|

• Project management plan • Project funding requirements • Work performance data • Organizational process assets | • Earned value management • Forecasting • To-complete performance index (TCPI) • Performance reviews • Project management software • Reserve analysis | • Work performance information • Cost forecasts • Change requests • Project management plan updates • Project document updates • Organizational process asset updates |

Exam Tip

Did you notice that the outputs from the Control Costs process are the same as the outputs from the Control Schedule process, with the exception of the cost forecasts instead of schedule forecasts?

The Control Costs

process is focused mainly on measuring actual against planned cost performance, forecasting likely future cost performance, and managing any changes to the cost baseline. The Control Costs process covers the following monitoring and controlling domain task

:

- Task 1: Measure project performance using appropriate tools and techniques, in order to identify and quantify any variances and corrective actions.

Inputs

The Control Costs process uses the following inputs.

Project Management Plan

The project management plan

and its subsidiary plans guide you in the process of controlling any potential changes to your cost baseline or any of the individual estimates that were prepared. As such, it is an important input into the Control Costs process. The project management plan is an output from the Develop Project Management Plan process.

Project Funding Requirements

The project funding requirements

are an important input into the Control Costs process because they enable you to determine when expenditures will be incurred and when funding for the project will be available, and to therefore assess actual versus planned project funding requirements and control any changes to these elements. The project funding requirements are an output from the Determine Budget process.

Work Performance Data

By now you should have picked up that work performance data

is an important input into several controlling processes. Work performance data is the information you gather about what is actually occurring on the project down to the level of which activities have started, the costs associated with completing those activities, and any estimates for completing the remainder of the work to be done. Work performance data is an output from the Direct and Manage Project Work process.

Organizational Process Assets

The types of organizational process assets

that are useful as inputs into the Control Costs process are any existing organizational policies, procedures, templates, or other elements relating to how costs will be monitored and reported on in your project.

Tools and Techniques

The following tools and techniques can be used on the inputs into the Control Costs process.

Earned Value Management

The earned value management

(EVM)

system provides an effective and efficient way of to establish what has occurred in the past and to use this information to forecast likely future scenarios by using a range of mathematical equations. It is better than simply taking one or two elements of past performance and expecting that performance to continue. For example, imagine that you are a project sponsor, and your project manager tells you that the project is 50% of the way through and has spent only 40% of the budget. Is this a good situation? It may be, but without knowing how much of the actual work has been completed and how much value has been earned, you don’t really know if this is a positive statement. This is exactly the scenario that EVM can get around.

EVM takes the original project cost baseline

, the planned value of the work you had expected to have completed by now, the earned value of the work you have completed, and the actual cost of delivering that value, to determine the project cost and schedule performance to date and then forecast the likely costs at completion. It does this by using the following formulas:

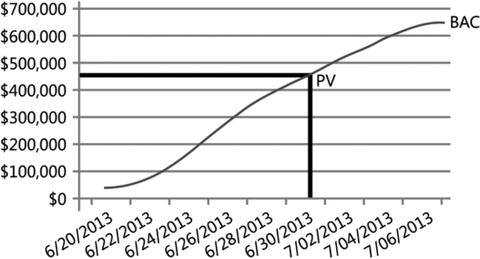

- Budget at completion (BAC) : The original forecast budget for the project. The BAC is also the total planned value (PV) for the project.

- Planned value (PV) : The amount of value you should have earned by this time in the project. Because the total PV for a project equals the BAC, you can determine the PV by simply determining how far through the project you are in relation to time, and mapping this back to the approved cost baseline. Figure 5-4 demonstrates how to determine the PV from the BAC.

Figure 5-4.The project cost baseline showing PV and BACIf you do not have a cost baseline from which to read PV, the easiest way to determine PV is to calculate the percentage of time that has been completed and multiply the BAC by this. If you have completed 7 months of a 10-month project and the BAC is $50,000, then your PV is 70% of $50,000, which equals $35,000. Obviously this method assumes a linear spend on the project instead of the S-curve you normally see.

Figure 5-4.The project cost baseline showing PV and BACIf you do not have a cost baseline from which to read PV, the easiest way to determine PV is to calculate the percentage of time that has been completed and multiply the BAC by this. If you have completed 7 months of a 10-month project and the BAC is $50,000, then your PV is 70% of $50,000, which equals $35,000. Obviously this method assumes a linear spend on the project instead of the S-curve you normally see. - Earned value (EV) : The value of the work that has been completed. This is not the actual cost of the work that has been completed but rather the original ascribed value from your approved cost baseline for the value of the work.

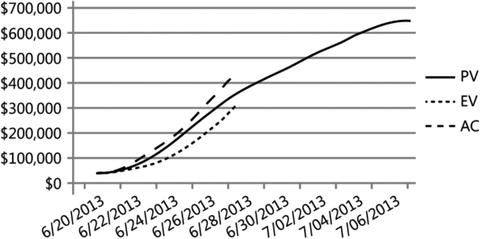

- Actual cost (AC) : The actual realized cost incurred for the work done to date. You can get a record of this from your accounts system.Figure 5-5 shows the BAC, PV, EV, and AC on a single graph. Incidentally, it shows a project in trouble in terms of both time and cost: the AC is above the PV, and the EV is less than the PV.

Figure 5-5.A record of project planned value, earned value, and actual cost

Figure 5-5.A record of project planned value, earned value, and actual cost

Exam Tip

On most questions, you will be challenged to extract the BAC, PV, EV, and AC from the scenario given. Take your time to ensure that you are extracting the correct figures.

REAL WORLD

I’ve often found that when calculating the actual cost, it is important to remove from this calculation the value of any material held in stock. On some projects, you may decide to procure a lot of required materials early to avoid potential cost increases over time. Therefore, you will have paid for these materials, and this shows up in your accounts. However, incorporating this amount into your actual cost figure for the purposes of EVM will skew the results negatively. Therefore, I recommend that you do regular stock takes and remove the value of material held in stock from the actual cost figure you use for the EVM calculations.

- Cost variance (CV) : The difference between the value of what you expected to have earned (EV) at this point and the AC at this point. A positive CV is good and shows that the project is under budget. A negative CV is bad and shows that the project is over budget. The formula isCV = EV – AC

- Cost performance index (CPI) : One limitation of the CV equation is that it gives you a simple gross figure. You can’t tell whether a $10,000 CV is significant on your project. If you are working on a $50,000 project, it is significant; if you are working on a $10 million contract, it may not be as significant. The CPI calculation tells you the magnitude of the variance. A CPI of more than 1 is good, because it means the project is under budget; a CPI of less than 1 is bad, because it means the project is over budget. For example, if you have a CPI of 1.1, it means for every dollar you spend on the project, you are getting a $1.10 return. The formula isCPI = EV/AC

- Schedule variance (SV) : Tells you whether you are ahead or behind your planned schedule. It is the difference between the EV and the PV. A positive SV is good and means you are ahead of schedule; a negative SV is bad and means you are behind schedule. The formula isSV = EV – PV

- Schedule performance index (SPI) : A ratio of the EV and PV that allows you to better determine the magnitude of any variance. An SPI of more than 1 is good, because it means the project is ahead of time; an SPI of less than 1 is bad, because it means the project is behind schedule. For example, if you have an SPI of 0.95, it means every day you spend working on the project, you are getting a 0.95 day return. The formula isSPI = EV/PV

Exam Tip

A quick and easy way to remember the formula for CV, CPI, SP, and SPI is that each of the formula starts with EV. If it is a formula relating to variance (CV or SV), then the next symbol is a minus sign. If it is a formula relating to a performance index (CPI or SPI), then the next symbol is a division sign. If the formula is in relation to cost (CV or CPI), then the final part of the formula is AC. If the formula is in relation to schedule (SV or SPI), then the final part of the formula is PV.

Forecasting

Forecasting

is the process of taking time and cost performance to date and using this information to forecast a likely future scenario. The time and cost performance measurements are the cost variance (CV), schedule variance (SV), cost performance index (CPI), and schedule performance index (SPI). You can use these measurements and the following formulas to forecast a likely project cost at completion, the amount of money required to complete the project, and the difference between what you originally thought it would cost and what you now think it will cost:

- Estimate at completion (EAC): There are many ways to calculate a forecast EAC. Keep in mind that in order to forecast a likely future cost or time frame for the project, you will be using historical information. Therefore, the quality of your EAC calculation depends entirely on the quality of the historical information you use. The following four formulas use different inputs to calculate the EAC. Each one gives a different answer for the same project.EAC = BAC/CPI: This is perhaps the simplest of the EAC calculations because it takes your original BAC and divides that by your CPI. Obviously, this is a useful calculation if your cost performance to date is indicative of your likely cost performance going forward; by the same measure, it will not be a great calculation to use if your cost performance to date is not indicative of your cost performance in the future.EAC = AC+ ETC: Simply adding your ETC to your AC spent to date is an effective way to determine your EAC. However, the method by which you determine your EAC calculation has a significant effect on whether this formula is accurate.EAC = AC + (BAC – EV): This formula takes the AC spent to date and adds to them the total BAC, subtracting the current EV.EAC = AC + ((BAC – EV)/(CPI × SPI)): This formula takes into account both your cost performance and your schedule performance and applies them to the value of the work you have left to complete.

Exam Tip

Memorize all these formulas, and as soon as you are allowed to start the exam, write them down.

Note

Cumulative vs. Non-Cumulative

When using either the CPI or SPI formula, you can choose whether to use cumulative or non-cumulative variations. The cumulative calculation calculates from the start of the project to where you are now in the project; obviously, if you use this, you are assuming that particular range is indicative and typical of your cost or schedule performance going forward. However, if for some reason you have experienced atypical variances in either time or cost on your project in the past, you may want to avoid using these when you use either CPI or SPI for forecasts. In this case, you should use non-cumulative CPI or SPI calculations taken from a specific period of time you feel is a more accurate representation of likely future performance.

REAL WORLD

When using an EAC formula, as a general rule of thumb, I use the BAC divided by CPI calculation for the first third of the project because the information coming out at this point tends to be less accurate. After I get past the halfway point on a project, I use the AC + ((BAC-EV)/(CPI × SPI)) formula, because it takes into account all parameters and is generally more accurate.

- Estimate to complete (ETC): Your forecast of the remaining costs to be incurred on the project. The easiest way to calculate this is to subtract AC spent to date from your EAC. The formula isETC = EAC – AC

- Variance at completion (VAC): The difference between what you originally thought the project was going to cost (BAC) and what you now think it will cost (EAC). A negative variance is bad, and a positive variance is good. The formula isVAC = BAC – EAC

Exam Tip

There may be occasions when the acronyms used here to outline the EVM system are represented by an older set of four-letter acronyms, as follows:

Planned value (PV) = Budgeted cost of work scheduled (BCWS)

Actual cost (AC) = Actual cost of work performed (ACWP)

Earned value (EV) = Budgeted cost of work performed (BCWP)

Exam Tip

On the exam, you will often be presented with a scenario that requires you to work out one set of figures before you can work out another set of figures. For example, you may be required to work out the EAC by using either CPI or SPI but will not be given the CPI figures or SPI figures. You will instead be given figures for EC, AC, and PV, and be expected to work out either the CPI or the SPI first. Also, when looking at a question that requires you to calculate any formula, be on the lookout for irrelevant information, because sometimes not all the information presented in the scenario is relevant.

To-Complete Performance Index (TCPI )

The to-complete performance index (TCPI) tells you the rate at which you have to work to achieve either your EAC or your BAC, depending on which one you are targeting. A TCPI of less than 1 is good, whereas a TCPI of more than 1 is bad. If you are using the original BAC as your target, the formula is

If you are using the EAC as the target, the formula for TCPI is

Exam Tip

When doing any calculations on the exam, round your answer to two decimals places, but be prepared for an answer that is slightly different due to minor differences in the approach to rounding of decimal places.

Performance Reviews

Performance reviews

are conducted via a variety of means, including EVM variances and trend analysis. You already have seen the use of EVM variances for the calculation of both the cost variance (CV) and schedule variance (SV) using EVM. These are the most frequently used methods of determining variance and performance.

In addition to EVM variances as a performance review tool, you can use trend analysis, which looks at past performance and extrapolates from that a likely future performance, usually by using graphs and linear regression.

Project Management Software

Project management software

is very useful in monitoring the performance of cost on a project because it can quickly do what would take a lot of time if done manually. Additionally, it can take both the original data and any data from calculations and display it graphically for easy interpretation and communication.

Reserve Analysis

Reserve analysis

in this monitoring and controlling process is the process of re-examining the original reserves calculated—both the contingency and management reserves—and checking whether the assumptions made when calculating them are still valid, and also releasing any unused portions of contingency reserves from the approved project budget in order to enable other projects to access the pool of funds.

Outputs

The Control Costs process produces the following outputs.

Work Performance Information

The easiest way to display work performance information

based on the work performance data is by using the earned value calculations for CV, SV, CPI, SPI, and the TCPI. The work performance information goes on to be used as an input into the Monitor and Control Project Work process.

Cost Forecasts

Cost forecasts

are obtained from the EAC values. Cost forecasts go on to be used as an input into the Monitor and Control Project Work process.

REAL WORLD

It is important to emphasize to project stakeholders that any EAC calculation is just that: your estimate about what it will cost to complete the project. When calculating the EAC, you are using historical information to try to forecast a likely future outcome. If project stakeholders consider your EAC figure an absolute amount that you will definitely achieve, this will create unrealistic expectations.

Change Requests

One of the key outputs from any controlling process is change requests that arise as a result of either variances detected or additional information provided. Change requests may include preventive or corrective actions. All change requests are processed as per your documented and approved change-control process.

Change requests

go on to be used as an input into the Perform Integrated Change Control process from the Integration Management knowledge area.

Project Management Plan Updates

Specific parts of the project management plan

that may be updated as a result of the Control Costs process include the cost baseline and the cost management plan. Project management plan updates are used in turn as an input into the Develop Project Plan process.

Project Document Updates

Specific project documents

that may be updated as a result of the Control Costs process include any documentation relating to how you build up your cost estimates, such as the cost baseline and the basis of estimates document.

Organizational Process Asset Updates

Specific organizational process assets

that may be updated as a result of the Control Cost process are historical information, records of financial information kept, lessons learned, records of corrective actions, and updates to any organizational financial templates and policies in order to ensure that they are still relevant.

Quick Check

1.

What is the difference between work performance data and work performance information?

2.

If a project has a CPI of 1.1 and an SPI of .90, how is it performing in relation to time and cost?

3.

What is the key difference between each of the four formulas for estimate at completion?

Quick Check Answers

1.

Work performance data is the raw information collected by checking on cost and time performance. Work performance information applies filters to this data to make it useful information.

2.

This project is under budget because the CPI is greater than 1, but behind schedule because the SPI is less than 1.

3.

Each of the four formulas uses different historical information about the project to forecast a likely future outcome.

Chapter Summary

- The Cost Management knowledge area is focused on the development and checking of project costs and begins with a planning process that produces the cost management plan, which then guides the individual cost estimating process and development of the cost baseline. It also provides guidance on monitoring actual versus planned cost performance and managing any changes to the cost baseline.

- The Plan Cost Management process focuses on the production of the cost management plan, which is a subsidiary plan of the project management plan.

- The Estimate Costs process is a highly iterative process repeated throughout the project that uses a variety of estimating techniques to developed individual activity cost estimates.

- The Determine Budget process aggregates the individual activity cost estimates and determines exactly when the costs will be incurred to produce a time-phased project budget, or cost baseline.

- The Control Costs process assesses planned cost performance against actual cost performance and forecasts a likely future state by using the earned value management systems. Any changes to the project cost baseline or individual activity cost estimates are managed through the approved change-control process.

Exercises

The answers for these exercises are located in the “Answers” section at the end of this chapter.

1.

You are the project manager on a project to build ten identical offices. You expect to spend $50,000 per office to complete the work and take 20 months to finish. You are 12 months into the work and have completed five offices and spent $310,000 in total. Use this information to calculate the following:

i.

Budget at completion (BAC)

ii.

Actual cost (AC)

iii.

Planned value (PV)

iv.

Earned value (EV)

v.

Cost variance (CV)

vi.

Cost performance index (CPI)

vii.

Schedule variance (SV)

viii.

Schedule performance index (SPI)

ix.

Estimate at completion (EAC)

x.

Estimate to complete (ETC)

xi.

Variance at completion (VAC)

xii.

To-complete performance index (TCPI)

(b) Based on the information gained from the calculations you have performed, how is the project performing in terms of both cost and time?

2.

You are the project manager on a project to complete 15 miles of road. Your approved budget for the project is $930,000, and you have forecast that the project will take 35 weeks to complete. You are 13 weeks into the project and have constructed 7 miles of road at a cost of $58,000 per mile. Use this information to calculate the following:

i.

Budget at completion (BAC)

ii.

Actual cost (AC)

iii.

Planned value (PV)

iv.

Earned value (EV)

v.

Cost variance (CV)

vi.

Cost performance index (CPI)

vii.

Schedule variance (SV)

viii.

Schedule performance index (SPI)

ix.

Estimate at completion (EAC)

x.

Estimate to complete (ETC)

xi.

Variance at completion (VAC)

xii.

To-complete performance index (TCPI)

(b) Based on the information gained from the calculations you have performed, how is the project performing in terms of both cost and time?

Review Questions

Test your knowledge of the information in Chapter 5 by answering these questions. The answers to these questions, and the explanation of why each answer choice is correct or incorrect, are located in the “Answers” section at the end of this chapter.

1.

What is the correct order of processes in the Cost Management knowledge area?

A.

Plan Cost Management, Estimate Costs, Determine Budget, Control Costs

B.

Plan Cost Management, Determine Budget, Estimate Costs, Control Costs

C.

Plan Cost Management, Control Costs, Estimate Costs, Determine Budget

D.

Plan Cost Management, Estimate Costs, Control Costs, Determine Budget

2.

What is the single output from the Plan Cost Management process?

A.

Activity cost estimates

B.

Cost baseline

C.

Cost management plan

D.

Cost forecasts

3.

All of the following could be included in the cost management plan except?

A.

A description of the accuracy of estimating

B.

The cost reporting formats to be used

C.

A description of the units of measure used to estimate costs

D.

The dates each activity will occur

4.

If you are estimating the cost for an activity by comparing the current activity with similar ones you have completed in the past, what sort of estimating technique are you using?

A.

Analogous estimating

B.

Parametric estimating

C.

Three-point estimating

D.

Bottom-up estimating

5.

If you are aggregating the individual activity cost estimates up to the work-package level, then the sub-deliverable level, and then the deliverable level to arrive at a total project cost estimate, what sort of estimating technique are you using?

A.

Analogous estimating

B.

Parametric estimating

C.

Three-point estimating

D.

Bottom-up estimating

6.

If you are applying to senior management to obtain extra funds for unforeseen costs on your project, what are you using?

A.

Contingency reserve

B.

Funding limit reconciliation

C.

Management reserve

D.

Cost aggregation

7.

If you have a project with a schedule performance index (SPI) of 1.05 and a cost performance index (CPI) of 0.92, how is your project performing?

A.

The project is over budget and behind schedule.

B.

The project is over budget and ahead of schedule.

C.

The project is under budget and behind schedule.

D.

The project is under budget and ahead of schedule.

8.

If the budget at completion for your project is $70,000, the earned value is $30,000, and the actual cost is $32,000, what is your estimate at completion?

A.

$70,000.00

B.

$65,625.00

C.

$74,468.08

D.

$62,000.00

9.

If the budget at completion for your project is $70,000, the earned value is $30,000, and the actual cost is $32,000, what is your variance at completion?

A.

$0.00

B.

$7,375.00

C.

–$4 468.08

D.

$8 000.00

10.

If the to-complete performance index calculated for the budget at completion for your project is 1.1, what does this mean?

A.

Your project is doing well, and you can slow down and still achieve the budget at completion.

B.

Your project is right on track to achieve the budget at completion.

C.

You need to produce $1.10 worth of effort for every $1.00 spent to achieve the budget at completion.

D.

You need to speed up the schedule but slow down spending.

11.

Which of the following is an example of work performance information?

A.

Reserve analysis

B.

Activity cost estimates

C.

Project funding requirements

D.

Schedule variance

Answers

This section contains the answers to the questions for the Exercises and Review Questions in this chapter.

Exercises

1.

You are the project manager on a project to build ten identical offices. You expect to spend $50,000 per office to complete the work and take 20 months to finish. You are 12 months into the work and have completed five offices and spent $310,000 in total. Use this information to calculate the following:

i.

Budget at completion (BAC): 10 offices × $50,000 each = $500,000

ii.

Actual cost (AC): You have spent $310,000 in total, so this is your actual cost.

iii.

Planned value (PV): You are 12 months into a 20-month work program, so you planned to have created value equivalent to 12/20, or 60%, of your total planned value, or budget at completion. Therefore, your planned value (PV) is $500,000 × 60% = $300,000.

iv.

Earned value (EV): You have built five offices, each with a value to you of $50,000, so your earned value is 5 × $50,000 = $250,000.

v.

Cost variance (CV): CV = EV – AC: $250,000 – $310,000 = –$60,000.

vi.

Cost performance index (CPI): CPI = EV/AC: $250,000/$310,000 = 0.81.

vii.

Schedule variance (SV): SV = EV – PV: $250,000 – $300,000 = –$50,000.

viii.

Schedule performance index (SPI): SPI = EV/PV: $250,000/$300,000 = 0.83.

ix.

Estimate at completion (EAC)

a.

EAC= BAC/CPI: $500,000/0.81 = $617,283.95

b.

EAC = AC + ETC: $310,000 + $307,283.95 = $617,283.95

c.

EAC = AC + (BAC – EV): $310,000 + ($500,000 – $250,000) = $560,000

d.

EAC = AC + ((BAC–EV)/(CPI × SPI)): $310,000 + (($500,000 – $250,000)/(0.81 × 0.83)) = $681,857.80

x.

Estimate to complete (ETC): This answer depends on which EAC figure you choose to use in the formula ETC = EAC – AC. If you use the EAC from the BAC/CPI formula, the answer is $307,283.95.

xi.

Variance at completion (VAC): This answer depends on which EAC you choose to use in the formula VAC = BAC – EAC. If you use the EAC from the BAC/CPI formula, the answer is –$117,283.95.

xii.

To-complete performance index (TCPI): This answer depends on whether your target is your BAC or the EAC. If it is the EAC, the answer depends on which formula you use to calculate that. The following example uses BAC/CPI to calculate EAC:

a.

TCPI for EAC = (BAC – EV)/(EAC – AC) = 0.81

b.

TCPI for BAC = (BAC – EV)/(BAC – AC) = 1.31

(b) Based on the information gained from the calculations you have performed, how is the project performing in terms of both cost and time?

Based on the information calculated, the project is over budget because the cost variance (CV) is negative and the cost performance index (CPI) is less than 1. The project is behind schedule, because the schedule variance (SV) is negative and the schedule performance index (SPI) is less than 1.

2.

You are the project manager on a project to complete 15 miles of road. Your approved budget for the project is $930,000, and you have forecast that the project will take 35 weeks to complete. You are 13 weeks into the project and have constructed seven miles of road at a cost of $58,000 per mile. Use this information to calculate the following:

i.

Budget at completion (BAC): $930,000

ii.

Actual cost (AC): You have built seven miles of road at a cost of $58,000, so your AC is 7 × $58,000 = $406,000.

iii.

Planned value (PV): You are 13 weeks into a 35-week work program, so you planned to have created value of 13/35, or 37%, of your total planned value, or budget at completion. Therefore, your PV is $930,000 × 37% = $344,100.

iv.

Earned value (EV): You are building 15 miles of road for $930,000, so each mile of road has a value of $930,000/15 = $62,000. You have built seven miles of road each with a value to you of $62,000, so your earned value is 7 × $62,000 = $434,000.

v.

Cost variance (CV): CV = EV – AC: $434,000 – $406,000 = $28,000.

vi.

Cost performance index (CPI): CPI = EV/AC: $434,000/$406,000 = 1.07.

vii.

Schedule variance (SV): SV = EV – PV: $434,000 – $344,100 = $89,900.

viii.

Schedule performance index (SPI): SPI = EV/PV: $434,000/$344,100 = 1.26.

ix.

Estimate at completion (EAC)

a.

EAC= BAC/CPI: $930,000 / 1.07 = $869,158.88

b.

EAC = AC + ETC: $406,000 + $464, 158.88 = $870,158.88

c.

EAC = AC + (BAC – EV): $406,000 + ($930,000 – $434,000) = $902,000

d.

EAC = AC + ((BAC – EV)/(CPI × SPI)): $406,000 + (($930,000 – $434,000)/(1.07 × 1.26)) = $773,407.41

x.

Estimate to complete (ETC): This answer depends on which EAC figure you choose to use in the formula ETC = EAC – AC. If you use the EAC from the BAC/CPI formula, the answer is $463,158.88.

xi.

Variance at completion (VAC): This answer depends on which EAC you choose to use in the formula VAC = BAC – EAC. If you use the EAC from the BAC/CPI formula, the answer is $60,841.12.

xii.

To-complete performance index (TCPI): This answer depends on whether your target is your BAC or the EAC. If it is the EAC, the answer depends on which formula you use to calculate that. The following example uses BAC/CPI to calculate EAC:

a.

TCPI for EAC = (BAC – EV)/(EAC – AC) = 1.07

b.

TCPI for BAC = (BAC – EV)/(BAC – AC) = 0.95

(b) Based on the information gained from the calculations you have performed, how is the project performing in terms of both cost and time?

Based on the information from the earned value calculations, the project is ahead of schedule because the schedule variance (SV) is positive and the schedule performance index (SPI) is greater than 1. The project is also under budget, because the cost variance (CV) is positive and the cost performance index (CPI) is greater than 1.

Chapter Review

1.

Correct Answer: A

A.

Correct: First plan your approach to cost management, then estimate costs, then determine your budget, then control the costs.

B.

Incorrect: Estimate Costs occurs before Determine Budget.

C.

Incorrect: Control Costs occurs after Determine Budget.

D.

Incorrect: Control Costs occurs after Determine Budget.

2.

Correct Answer: C

A.

Incorrect: Activity cost estimates are an output from the Estimate Costs process.

B.

Incorrect: The cost baseline is an output from the Determine Budget process.

C.

Correct: The cost management plan is the sole output from the Plan Cost Management process.

D.

Incorrect: Cost forecasts are an output from the Control Costs process.

3.

Correct Answer: D

A.

Incorrect: A description of the accuracy of estimating would be included in the cost management plan.

B.

Incorrect: A description of the cost reporting formats to be used would be included in the cost management plan.

C.

Incorrect: A description of the units of measure used to estimate costs would be included in the cost management plan.

D.

Correct: The dates each activity will occur would be included as part of your project schedule, not the cost management plan.

4.

Correct Answer: A

A.

Correct: Analogous estimating uses similar activities from the past and extrapolates from them a likely current cost estimate.

B.

Incorrect: Parametric estimating multiplies a known quality by a known dollar amount to arrive at a cost estimate.

C.

Incorrect: Three-point estimating takes the weighted average of most likely, optimistic, and pessimistic cost estimates.

D.

Incorrect: Bottom-up estimating aggregates lower-level cost estimates.

5.

Correct Answer: D

A.

Incorrect: Analogous estimating uses similar activities from the past and extrapolates from them a likely current cost estimate.

B.

Incorrect: Parametric estimating multiplies a known quality by a known dollar amount to arrive at a cost estimate.

C.

Incorrect: Three-point estimating takes the weighted average of most likely, optimistic, and pessimistic cost estimates.

D.

Correct: Bottom-up estimating aggregates lower-level cost estimates up to higher levels to arrive at a total project cost estimate.

6.

Correct Answer: C

A.

Incorrect: The contingency reserve is for known unknowns on the project.

B.

Incorrect: The funding limit reconciliation is an output from the Determine Budget process.

C.

Correct: The management reserve is available for truly unforeseen costs that arise on a project and is controlled by senior management.

D.

Incorrect: Cost aggregation is the technique of adding up lower-level costs to obtain higher-level cost estimates.

7.

Correct Answer: B

A.

Incorrect: The project would need a CPI less than 1 and an SPI less than 1 to be over budget and behind schedule.

B.

Correct: A CPI less than 1 and an SPI greater than 1 indicate that the project is over budget and ahead of schedule.

C.

Incorrect: The project would need a CPI greater than 1 and an SPI less than 1 to be under budget and behind schedule.

D.

Incorrect: The project would need a CPI greater than 1 and an SPI greater than 1 to be under budget and ahead of schedule.

8.

Correct Answer: C

A.

Incorrect: $70,000 is the budget at completion.

B.

Incorrect: You would arrive at this figure if you reversed the calculation for cost performance index (CPI).

C.

Correct: If you calculate the cost performance index (CPI) first by dividing the earned value (EV) by the actual cost (AC), then divide the budget at completion (BAC) by the cost performance index (CPI), this is the answer you get.

D.