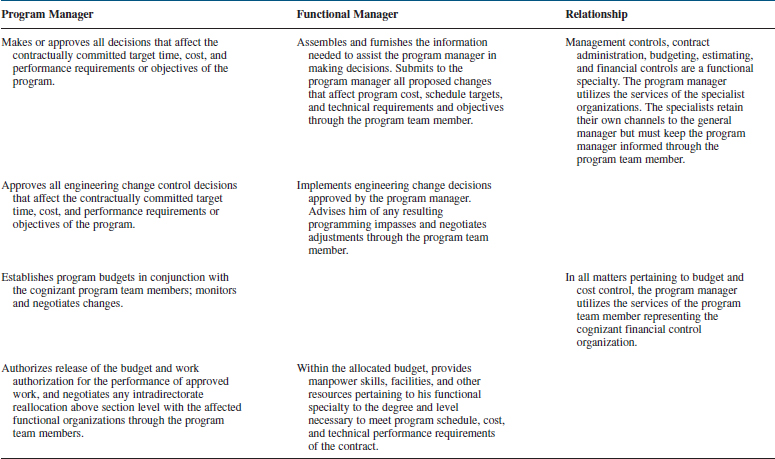

Cost Control

15.0 INTRODUCTION

PMBOK® Guide, 4th Edition

7.3 Cost Control

Cost control is equally important to all companies, regardless of size. Small companies generally have tighter monetary controls because the failure of even one project can put the company at risk, but they have less sophisticated control techniques. Large companies may have the luxury to spread project losses over several projects, whereas the small company may have few projects.

Many people have a poor understanding of cost control. Cost control is not only “monitoring” costs and recording data, but also analyzing the data in order to take corrective action before it is too late. Cost control should be performed by all personnel who incur costs, not merely the project office.

Cost control implies good cost management, which must include:

- Cost estimating

- Cost accounting

- Project cash flow

- Company cash flow

- Direct labor costing

- Overhead rate costing

- Other tactics, such as incentives, penalties, and profit-sharing

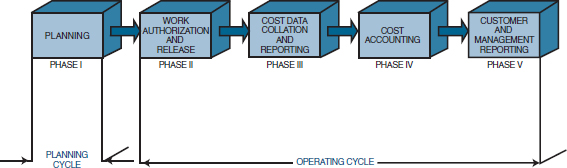

Cost control is actually a subsystem of the management cost and control system (MCCS) rather than a complete system per se. This is shown in Figure 15-1, where the MCCS is represented as a two-cycle process: a planning cycle and an operating cycle. The operating cycle is what is commonly referred to as the cost control system. Failure of a cost control system to accurately describe the true status of a project does not necessarily imply that the cost control system is at fault. Any cost control system is only as good as the original plan against which performance will be measured. Therefore, the designing of a planning system must take into account the cost control system. For this reason, it is common for the planning cycle to be referred to as planning and control, whereas the operating cycle is referred to as cost and control.

The planning and control system must help management project the status toward objective completion. Its purpose is to establish policies, procedures, and techniques that can be used in the day-to-day management and control of projects and programs. It must, therefore, provide information that:

- Gives a picture of true work progress

- Will relate cost and schedule performance

- Identifies potential problems with respect to their sources.

- Provides information to project managers with a practical level of summarization

- Demonstrates that the milestones are valid, timely, and auditable

The planning and control system, in addition to being a tool by which objectives can be defined (i.e., hierarchy of objectives and organization accountability), exists as a tool to develop planning, measure progress, and control change. As a tool for planning, the system must be able to:

- Plan and schedule work

- Identify those indicators that will be used for measurement

FIGURE 15-1. Phases of a management cost and control system.

The project budget that results from the planning cycle of the MCCS must be reasonable, attainable, and based on contractually negotiated costs and the statement of work. The basis for the budget is either historical cost, best estimates, or industrial engineering standards. The budget must identify planned manpower requirements, contract-allocated funds, and management reserve.

Establishing budgets requires that the planner fully understand the meaning of standards. There are two categories of standards. Performance results standards are quantitative measurements and include such items as quality of work, quantity of work, cost of work, and time-to-complete. Process standards are qualitative, including personnel, functional, and physical factors relationships. Standards are advantageous in that they provide a means for unity, a basis for effective control, and an incentive for others. The disadvantage of standards is that performance is often frozen, and employees are quite often unable to adjust to the differences.

As a tool for measuring progress and controlling change, the systems must be able to:

- Measure resources consumed

- Measure status and accomplishments

- Compare measurements to projections and standards

- Provide the basis for diagnosis and replanning

In using the MCCS, the following guidelines usually apply:

- The level of detail is specified by the project manager with approval by top management.

- Centralized authority and control over each project are the responsibility of the project management division.

- For large projects, the project manager may be supported by a project team for utilization of the MCCS.

Almost all project planning and control systems have identifiable design requirements. These include:

- A common framework from which to integrate time, cost, and technical performance

- Ability to track progress of significant parameters

- Quick response

- Capability for end-value prediction

- Accurate and appropriate data for decision-making by each level of management

- Full exception reporting with problem analysis capability

- Immediate quantitative evaluation of alternative solutions

MCCS planning activities include:

- Contract receipt (if applicable)

- Work authorization for project planning

- Work breakdown structure

- Subdivided work description

- Schedules

- Planning charts

- Budgets

MCCS planning charts are worksheets used to create the budget. These charts include planned labor in hours and material dollars.

MCCS planning is accomplished in one of these ways:

- One level below the lowest level of the WBS

- At the lowest management level

- By cost element or cost account

Even with a fully developed planning and control system, there are numerous benefits and costs. The appropriate system must consider a cost-benefit analysis, and include such items as:

- Project benefits

- Planning and control techniques facilitate:

- —Derivation of output specifications (project objectives)

- —Delineation of required activities (work)

- —Coordination and communication between organizational units

- —Determination of type, amount, and timing of necessary resources

- —Recognition of high-risk elements and assessment of uncertainties

- —Suggestions of alternative courses of action

- —Realization of effect of resource level changes on schedule and output performance

- —Measurement and reporting of genuine progress

- —Identification of potential problems

- —Basis for problem-solving, decision-making, and corrective action

- —Assurance of coupling between planning and control

- Planning and control techniques facilitate:

- Project cost

- Planning and control techniques require:

- —New forms (new systems) of information from additional sources and incremental processing (managerial time, computer expense, etc.)

- —Additional personnel or smaller span of control to free managerial time for planning and control tasks (increased overhead)

- —Training in use of techniques (time and materials)

- Planning and control techniques require:

A well-disciplined MCCS will produce the following results:

- Policies and procedures that will minimize the ability to distort reporting

- Strong management emphasis on meeting commitments

- Weekly team meetings with a formalized agenda, action items, and minutes

- Top-management periodic review of the technical and financial status

- Simplified internal audit for checking compliance with procedures

For MCCS to be effective, both the scheduling and budgeting systems must be disciplined and formal in order to prevent inadvertent or arbitrary budget or schedule changes. This does not mean that the baseline budget and schedule, once established, is static or inflexible. Rather, it means that changes must be controlled and result only from deliberate management actions.

Disciplined use of MCCS is designed to put pressure on the project manager to perform exceptionally good project planning so that changes will be minimized. As an example, government subcontractors may not:

- Make retroactive changes to budgets or costs for work that has been completed

- Rebudget work-in-progress activities

- Transfer work or budget independently of each other

- Reopen closed work packages

In some industries, the MCCS must be used on all contracts of $2 million or more, including firm-fixed-price efforts. The fundamental test of whether to use the MCCS is to determine whether the contracts have established end-item deliverables, either hardware or computer software, that must be accomplished through measurable efforts.

Two programs are used by the government and industry in conjunction with the MCCS as an attempt to improve effectiveness in cost control. The zero-base budgeting program provides better estimating techniques for the verification portion of control. The design-to-cost program assists the decision-making part of the control process by identifying a decision-making framework from which replanning can take place.

15.1 UNDERSTANDING CONTROL

PMBOK® Guide, 4th Edition

3.2 Monitoring and Control Process Group

Effective management of a program during the operating cycle requires that a well-organized cost and control system be designed, developed, and implemented so that immediate feedback can be obtained, whereby the up-to-date usage or resources can be compared to target objectives established during the planning cycle. The requirements for an effective control system (for both cost and schedule/performance) should include1:

- Thorough planning of the work to be performed to complete the project

- Good estimating of time, labor, and costs

- Clear communication of the scope of required tasks

- A disciplined budget and authorization of expenditures

- Timely accounting of physical progress and cost expenditures

- Periodic reestimation of time and cost to complete remaining work

- Frequent, periodic comparison of actual progress and expenditures to schedules and budgets, both at the time of comparison and at project completion

Management must compare the time, cost, and performance of the program to the budgeted time, cost, and performance, not independently but in an integrated manner. Being within one's budget at the proper time serves no useful purpose if performance is only 75 percent. Likewise, having a production line turn out exactly 200 items, as planned, loses its significance if a 50 percent cost overrun is incurred. All three resource parameters (time, cost, and performance) must be analyzed as a group, or else we might “win the battle but lose the war.” The use of the expression “management cost and control system” is vague in that the implication is that only costs are controlled. This is not true—an effective control system monitors schedule and performance as well as costs by setting budgets, measuring expenditures against budgets and identifying variances, assuring that the expenditures are proper, and taking corrective action when required.

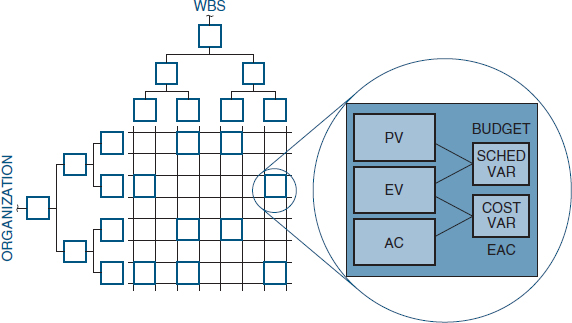

Previously we defined the work breakdown structure as the element that acts as the source from which all costs and controls must emanate. The WBS is the total project broken down into successively lower levels until the desired control levels are established. The work breakdown structure therefore serves as the tool from which performance can be subdivided into objectives and subobjectives. As work progresses, the WBS provides the framework on which costs, time, and schedule/performance can be compared against the budget for each level of the WBS.

The first purpose of control therefore becomes a verification process accomplished by the comparison of actual performance to date with the predetermined plans and standards set forth in the planning phase. The comparison serves to verify that:

- The objectives have been successfully translated into performance standards.

- The performance standards are, in fact, a reliable representation of program activities and events.

- Meaningful budgets have been established such that actual versus planned comparisons can be made.

In other words, the comparison verifies that the correct standards were selected, and that they are properly used.

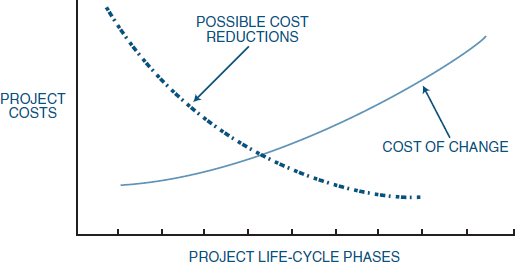

FIGURE 15-2. Cost reduction analysis.

The second purpose of control is decision-making. Three useful reports are required by management in order to make effective and timely decisions:

- The project plan, schedule, and budget prepared during the planning phase

- A detailed comparison between resources expended to date and those predetermined. This includes an estimate of the work remaining and the impact on activity completion.

- A projection of resources to be expended through program completion

These reports, supplied to the managers and the doers, provide three useful results:

- Feedback to management, the planners, and the doers

- Identification of any major deviations from the current program plan, schedule, or budget

- The opportunity to initiate contingency planning early enough that cost, performance, and time requirements can undergo corrected action without loss of resources

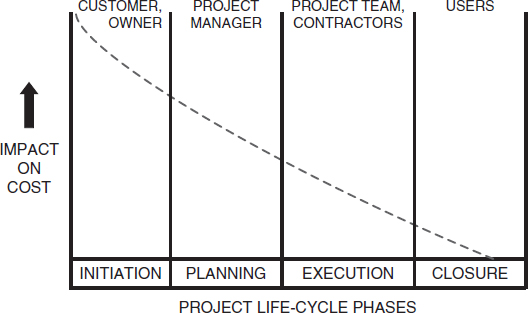

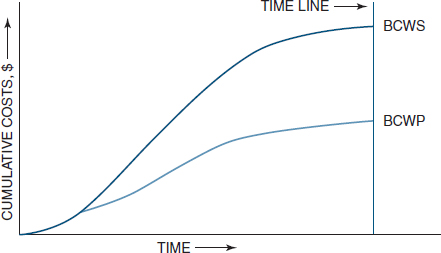

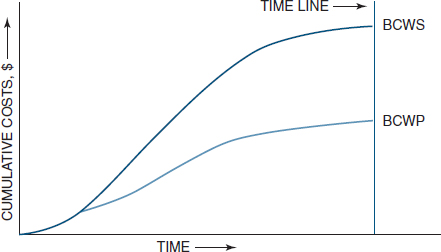

These reports provide management with the opportunity to minimize downstream changes by making proper corrections here and now. As shown in Figures 15-2 and 15-3, cost reductions are more available in the early project phases, but are reduced as we go further into the project life-cycle phases. Figure 15-3 identifies the people that most likely have the greatest influence on possibly initiating changes to a project. Downstream the cost of changes could easily exceed the original cost of the project. This is an example of the “iceberg” syndrome, where problems become evident too late in the project to be solved easily, resulting in a very high cost to correct them.

FIGURE 15-3. People with the ability to influence cost.

15.2 THE OPERATING CYCLE

The management cost and control system (MCCS) takes on paramount importance during the operating cycle of the project. The operating cycle is composed of four phases:

- Work authorization and release (phase II)

- Cost data collection and reporting (phase III)

- Cost analysis (phase IV)

- Reporting: customer and management (phase V)

These four phases, when combined with the planning cycle (phase I), constitute a closed system network that forms the basis for the management cost and control system.

Phase II is considered as work release. After planning is completed and a contract is received, work is authorized via a work description document. The work description, or project work authorization form, is a contract that contains the narrative description, organization, and time frame for each WBS level. This multipurpose form is used to release the contract, authorize planning, record detail description of the work outlined in the work breakdown structure, and release work to the functional departments.

Contract services may require a work description form to release the contract. The contractual work description form sets forth general contractual requirements and authorizes program management to proceed.

Program management may then issue a subdivided work description form to the functional units so that work can begin. The subdivided work description may also be issued through the combined efforts of the project team, and may be revised or amended when either the scope or the time frame changes. The subdivided work description generally is not used for efforts longer than ninety days and must be “tracked” as if a project in itself. This subdivided work description form sets forth contractual requirements and planning guidelines for the applicable performing organizations. The subdivided work description package established during the proposal and updated after negotiations by the program team is incrementally released by program management to the work control centers in manufacturing, engineering, publications, and program management as the authority for release of work orders to the performing organizations. The subdivided work description specifies how contractual requirements are to be accomplished, the functional organizations involved, and their specific responsibilities, and authorizes the expenditure of resources within a particular time frame.

The work control center assigns a work order number to the subdivided work description form, if no additional instructions are required, and releases the document to the performing organizations. If additional instructions are required, the work control center can prepare a more detailed work-release document (shop traveler, tool order, work order release), assign the applicable work order number, and release it to the performing organization.

A work order number is required for all in-house direct and indirect charging. The work order number also serves as a cross-reference number for automatic assignment of the indentured work breakdown structure number to labor and material data records in the computer.

Small companies can avoid this additional paperwork cost by going directly from an awarded contract to a single work order, which may be the only work order needed for the entire contract.

15.3 COST ACCOUNT CODES

PMBOK® Guide, 4th Edition

7.2.2.1 Cost Aggregation

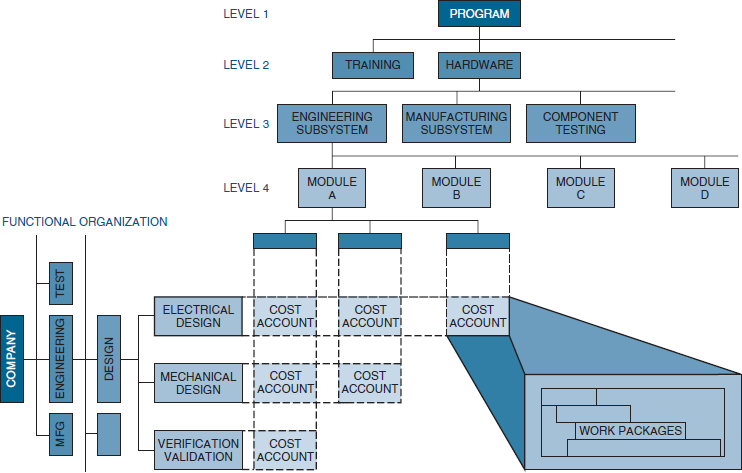

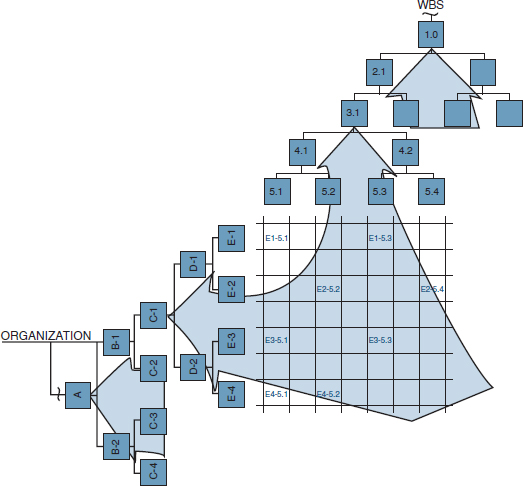

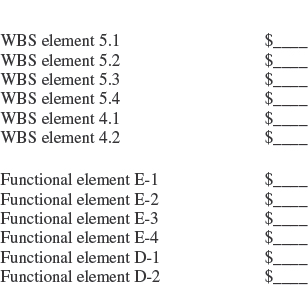

Since project managers control resources through the line managers rather than directly, project managers end up controlling direct labor costs by opening and closing work orders. Work orders define the charge numbers for each cost account. By definition, a cost account is an identified level at a natural intersection point of the work breakdown structure and the organizational breakdown structure (OBS) at which functional responsibility for the work is assigned, and actual direct labor, material, and other direct costs are compared with actual work performed for management control purposes.

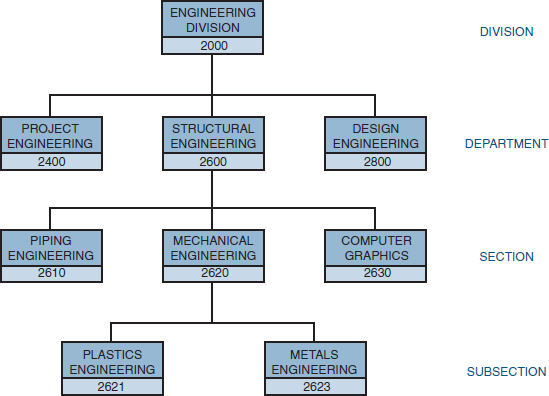

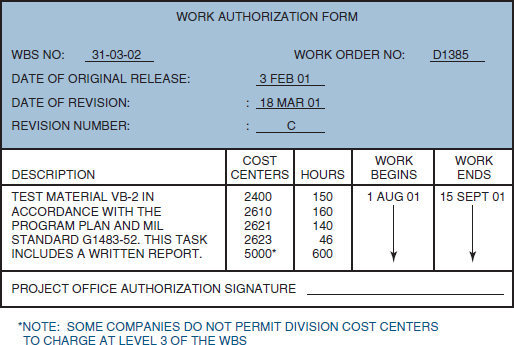

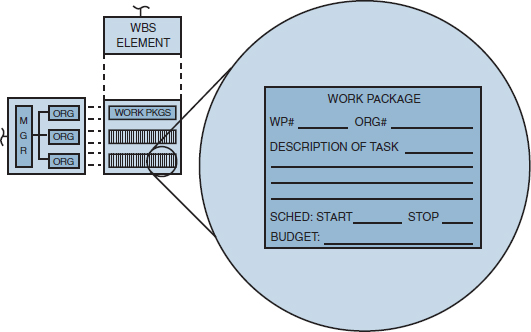

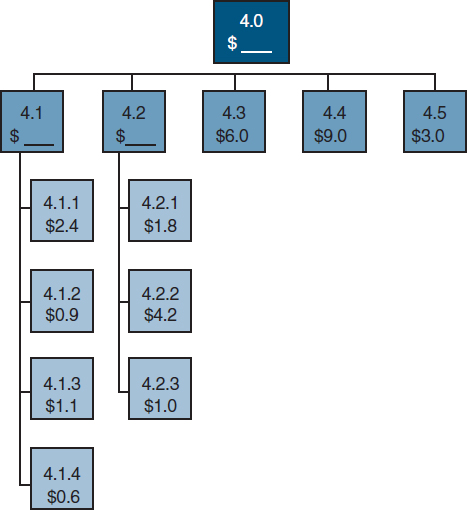

Cost accounts are the focal point of the MCCS and may comprise several work packages, as shown in Figure 15-4. Work packages are detailed short-span job or material items identified for the accomplishment of required work. To illustrate this, consider the cost account code breakdown shown in Figure 15-5 and the work authorization form shown in Figure 15-6. The work authorization form specifically identifies the cost centers that are “open” for this charge number, the man-hours available for each cost center, and the operational time period for the charge number. Because the exact dates of operation are completely defined, the charge number can be assigned perhaps as much as a year in advance of the work-begin date. This can be shown pictorially, as in Figure 15-7.

If the man-hours are assigned to Cost Center 2400, then any 24xx cost center can use this charge number. If the work authorization form specifies Cost Center 2610, then any 261x cost center can use the charge number. However, if Cost Center 2623 is specified, then no lower cost accounts exist, and this is the only cost center that can use this work order charge number. In other words, if a charge number is opened up at the department level, then the department manager has the right to subdivide the assigned man-hours among the various sections and subsections. Company policy usually identifies the permissible cost center levels that can be assigned in the work authorization form. These permissible levels are related to the work breakdown structure level. For example, Cost Center 5000 (i.e., divisional) can be assigned at the project level of the work breakdown structure, but only department, sectional, or subsectional cost accounts can be assigned at the task level of the work breakdown structure.

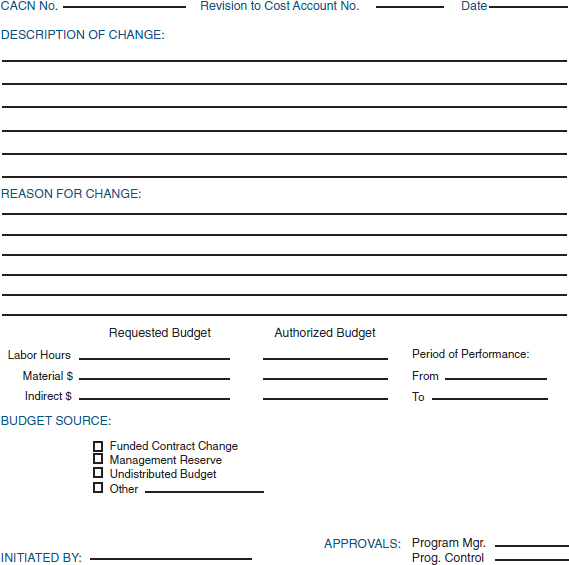

If a cost center needs additional time or additional man-hours, then a cost account change notice form must be initiated, usually by the requesting cost center, and approved by the project office. Figure 15-8 shows a typical cost account change notice form.

Large companies have computerized cost control and reporting systems. Small companies have manual or partially computerized systems. The major difficulty in using the cost account code breakdown and the work authorization form (Figures 15-5 and 15-6) is related to whether the employees fill out time cards, and frequency with which the time cards are filled out. Project-driven organizations fill out time cards at least once a week, and the cards are inputted to a computerized system. Non-project-driven organizations fill out time cards on a monthly basis, with computerization depending on the size of the company.

FIGURE 15-4. The cost account intersection.

PMBOK® Guide, 4th Edition

7.2.2.1 Cost Aggregation

FIGURE 15-5. Cost account code breakdown.

PMBOK® Guide, 4th Edition

4.4 Monitor and Control Project Work

FIGURE 15-6. Work authorization form.

FIGURE 15-7. Planning and budgeting describe, plan, and schedule the work.

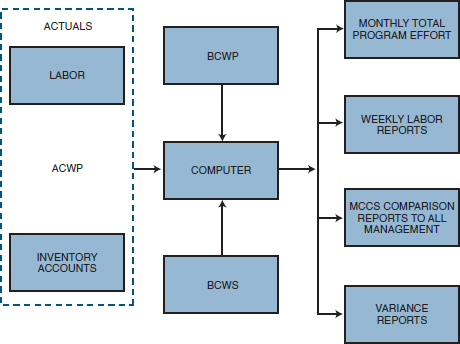

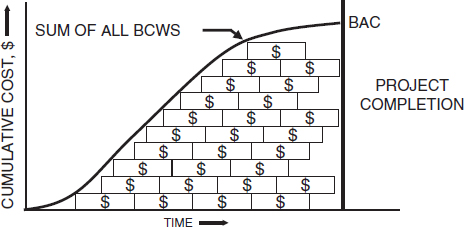

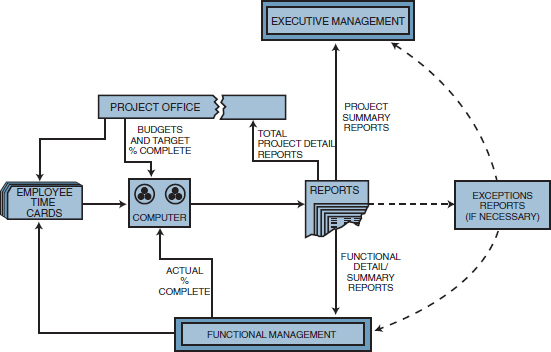

Cost data collection and reporting constitute the second phase of the operating cycle of the MCCS. Actual cost (ACWP) and the budgeted cost for work performed (BCWP) for each contract or in-house project are accumulated in detailed cost accounts by cost center and cost element, and reported in accordance with the flow charts shown in Figure 15-9. These detailed elements, for both actual costs incurred and the budgeted cost for work performed, are usually printed out monthly for all levels of the work breakdown structure. In addition, weekly supplemental direct labor reports can be printed showing the actual labor charge incurred, and can be compared to the predicted efforts.

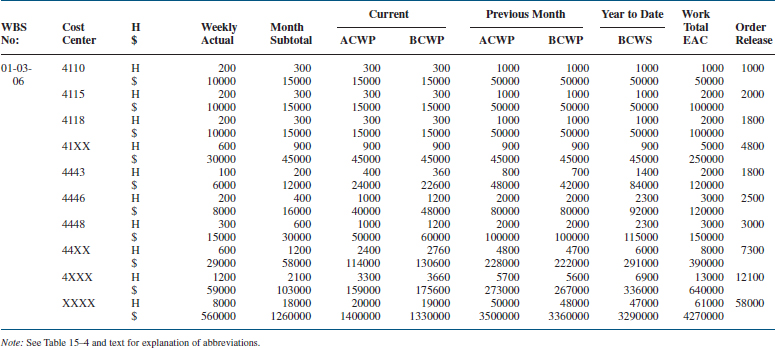

Table 15-1 shows a typical weekly labor report. The first column identifies the WBS number.2 If more than one work order were assigned to this WBS element, then the work order number would appear under the WBS number. This procedure would be repeated for all work orders under the same WBS number. The second column contains the cost centers charging to this WBS element (and possibly work order numbers). Cost Center 41xx represents department 41 and is a rollup of Cost Centers 4110, 4115, and 4118. Cost Center 4xxx represents the entire division and is a rollup of all 4000-level departments. Cost Center xxxx represents the total for all divisions charging to this WBS element. The weekly labor reports must list all cost centers authorized to charge to this WBS element, whether or not they have incurred any costs over the last reporting period.

FIGURE 15-8. Cost account change notice (CACN).

Most weekly labor reports provide current month subtotals and previous month totals. Although these also appear on the detailed monthly report, they are included in the weekly report for a quick-and-dirty comparison. Year-to-date totals are usually not on the weekly report unless the users request them for an immediate comparison to the estimate at completion (EAC) and the work order release.

Weekly labor output is a vital tool for members of the program office in that these reports can indicate trends in cost and performance in sufficient time for contingency plans to be established and implemented. If these reports are not available, then cost and labor overruns would not be apparent until the following month when the detailed monthly labor, cost, and materials output was obtained.

FIGURE 15-9. Cost data collection and reporting flowchart.

In Table 15-1, Cost Center 4110 has spent its entire budget. The work appears to be completed on schedule. The responsible program office team may wish to eliminate this cost center's authority to continue charging to this WBS element by issuing a new subdivided work description or work order canceling this department's efforts. Cost Center 4115 appears to be only halfway through. If time is becoming short, then Cost Center 4115 must add resources in order to meet requirements. Cost Center 4443 appears to be heading for an overrun. This could also indicate a management reserve. In this case the responsible program team member feels that the work can be accomplished in fewer hours.

Work order releases are used to authorize certain cost centers to begin charging their time to a specific cost reporting element. Work orders specify hours, not dollars. The hours indicate the “targets” that the program office would like to have the department shoot for. If the program office wished to be more specific and “compel” the departments to live within these hours, then the budgeted cost for work scheduled (BCWS) should be changed to reflect the reduced hours.

Four categories of cost data are normally accumulated:

- Labor

- Material

- Other direct charges

- Overhead

Project managers can maintain reasonable control over labor, material, and other direct charges. Overhead costs, on the other hand, are calculated yearly or monthly and applied retroactively to all applicable programs. Management reserves are often used to counterbalance the effects of adverse changes in overhead rates.

TABLE 15-1. WEEKLY LABOR REPORT

15.4 BUDGETS

The project budget, which is the final result of the planning cycle of the MCCS, must be reasonable, attainable, and based on contractually negotiated costs and the statement of work. The basis for the budget is either historical cost, best estimates, or industrial engineering standards. The budget must identify planned manpower requirements, contract allocated funds, and management reserve.

All budgets must be traceable through the budget “log,” which includes:

- Distributed budget

- Management reserve

- Undistributed budget

- Contract changes

The distributed or normal performance budget is the time-phased budget that is released through cost accounts and work packages. Management reserve is generally the dollar amount established for categories of unforeseen problems and contingencies resulting in special out-of-scope work to the performers. Sometimes, people interpret the management reserve as their own little kitty of funds for a special purpose. Below are several interpretations on how the control of the management reserve should be used.

- The management reserve is actually excess profits and should not be used at all. It should be booked as additional profits as soon as possible. (Accounting)

- The management reserve should be spent on any activities that add features or additional functionality to the product. Our customers will like that. It will also build up good customer relations for future work. (Marketing)

- The management reserve should be used for those activities that add value to our company, especially our image in the community. (Senior management)

- The management reserve should be use as part of risk management in developing mitigation strategies for risks that occur during the execution of the project. Scope changes not originally agreed to should be billed separately to the customer. (Project manager)

- The management reserve should be used for the additional hours necessary to show that our technical community can exceed specifications rather than merely meeting them. This is our strength. The management reserve should also be used as “seed money” for exploring ideas discovered while working on this project. (Engineering and R&D)

Some people confuse the management reserve with the definition of a “reserve” or “contingency” fund. In the author's opinion, the management reserve is controlled by the project manager of the performing organization and used for escalations in salaries, raw material prices, and overhead rates. The management reserve may also be used for unforeseen problems that may occur. The management reserve should not be used to cover up bad planning estimates or budget overruns.

Also, the management reserve should not be used for scope changes. Scope changes should be paid for out of the customer's reserve or contingency fund. In other words, the management reserve generally applies to the performing organization, whereas the contingency reserve is controlled by the customer for the scope changes that may be requested by the performing organization. There is an exception. If the performing organization is requesting a small scope change, the cost of convening the change control board, paying airfares, meals, and lodgings may be prohibited. In this case, the management reserve may be used and considered as a goodwill activity for the performing organization.

The management reserve should be established based upon the project's risks. Some project may require no management reserve at all, whereas others may necessitate a reserve of 15 percent.

There is always the question of who should get to keep any unused management reserve at the end of the project. If the project is under a firm-fixed price contract, then the management reserve becomes extra profit for the performing organization. If the contract is a cost reimbursable type, all or part of the unused management reserve may have to be returned to the customer.

Although the management reserve may appear as a line item in the work breakdown structure, it is neither part of the distributed budget nor part of the cost baseline. Budgets are established on the assumption that they will be spent, whereas management reserve is money that you try not to spend. It would be inappropriate to consider the management reserve as an undistributed budget.

In addition to the “normal” performance budget and the management reserve budget, there are two other budgets:

- Undistributed budget, which is that budget associated with contract changes where time constraints prevent the necessary planning to incorporate the change into the performance budget. (This effort may be time-constrained.)

- Unallocated budget, which represents a logical grouping of contract tasks that have not yet been identified and/or authorized.

15.5 THE EARNED VALUE MEASUREMENT SYSTEM (EVMS)

In the early years of project management, it became evident that project managers were having difficulty determining project status. Some people believed that status could be determined only by a mystical approach, as shown in Figure 15-10.

The critical question was whether project managers were managing costs or just monitoring costs. The government wanted costs to be managed rather than just monitored, accounted for, or reported. This need resulted in the creation of the EVMS.

The basis for the EVMS, which some consider to be a component of the MCCS, is the determination of earned value. Earned value is a management technique that relates resource planning to schedules and technical performance requirements. Earned value management (EVM) is a systematic process that uses earned value as the primary tool for integrating cost, schedule, technical performance management, and risk management.

FIGURE 15-10. Determining the status.

Without using the EVMS, determining status can be difficult. Consider the following:

- The project

- A total budget of $1.2 million

- A 12-month effort

- Produce 10 deliverables

- Reported status

- Time elapsed: 6 months

- Money spent to date: $700,000

- Deliverables produced: 4 complete, 2 partial

What is the real status of the project? How far along is the project: 40, 50, 60 percent, etc.? Another problem was how to accurately relate cost to performance. If you spent 20 percent of the budget, does that imply that you are 20 percent complete? If you are 30 percent complete, then have you spent 30 percent of the budget?

The EVMS provides the following benefits:

- Accurate display of project status

- Early and accurate identification of trends

- Early and accurate identification of problems

- Basis for course corrections

The EVMS can answer the following questions:

- What is the true status of the project?

- What are the problems?

- What can be done to fix the problems?

- What is the impact of each problem?

- What are the present and future risks?

The EVMS emphasizes prevention over cures by identifying and resolving problems early. The EVMS is an early warning system allowing for early identification of trends and variances from the plan. The EVMS provides an early warning system, thus allowing the project manager sufficient time to make course corrections in small increments. It is usually easier to correct small variances as opposed to large variances. Therefore, the EVMS should be used continuously throughout the project in order to detect the variances while they are small and possibly easy to correct. Large variances are more difficult to correct and run the risk that the cost to correct the large variance may displease management to the point where the project may be canceled.

15.6 VARIANCE AND EARNED VALUE

A variance is defined as any schedule, technical performance, or cost deviation from a specific plan. Variances must be tracked and reported. They should be mitigated through corrective actions and not eliminated through a baseline change unless there is a good reason. Variances are used by all levels of management to verify the budgeting system and the scheduling system. The budgeting and scheduling system variance must be compared because:

- The cost variance compares deviations only from the budget and does not provide a measure of comparison between work scheduled and work accomplished.

- The scheduling variance provides a comparison between planned and actual performance but does not include costs.

There are two primary methods of measurement:

- Measurable efforts: Discrete increments of work with a definable schedule for accomplishment, whose completion produces tangible results.

- Level of effort: Work that does not lend itself to subdivision into discrete scheduled increments of work, such as project support and project control.

Variances are used on both types of measurement.

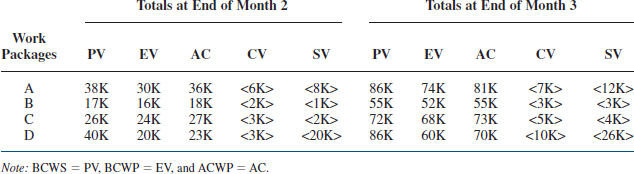

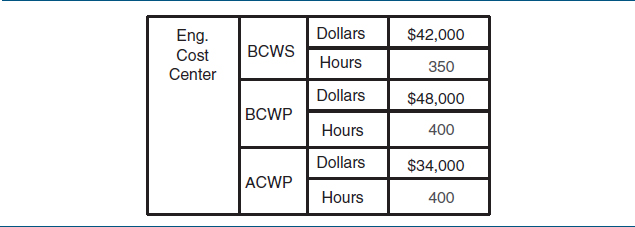

In order to calculate variances, we must define the three basic variances for budgeting and actual costs for work scheduled and performed. Archibald defines these variables3:

- Budgeted cost for work scheduled (BCWS) is the budgeted amount of cost for work scheduled to be accomplished plus the amount or level of effort or apportioned effort scheduled to be accomplished in a given time period.

PMBOK® Guide, 4th Edition

7.3.2 Cost Control Tools and Techniques

7.3.2.4 Performance Measurement Analysis

- Budget cost for work performed (BCWP) is the budgeted amount of cost for completed work, plus budgeted for level of effort or apportioned effort activity completed within a given time period. This is sometimes referred to as “earned value.”

- Actual cost for work performed (ACWP) is the amount reported as actually expended in completing the work accomplished within a given time period.

Note: The Project Management Institute has changed the nomenclature in their new version of the PMBOK® Guide whereby BCWS is now PV, BCWP is now EV, and ACWP is now AC. However, the majority of heavy users of these acronyms, specifically government contractors, still use the old acronyms. Until the PMI acronyms are accepted across all industries, we will continue to focus on the most commonly used acronyms.

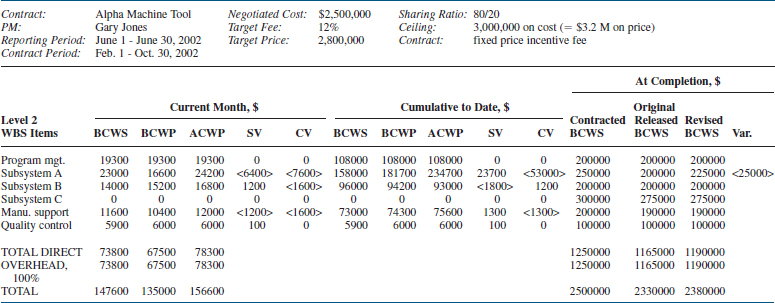

BCWS represents the time-phased budget plan against which performance is measured. For the total contract, BCWS is normally the negotiated contract plus the estimated cost of authorized but unpriced work (less any management reserve). It is time-phased by the assignment of budgets to scheduled increments of work. For any given time period, BCWS is determined at the cost account level by totaling budgets for all work packages, plus the budget for the portion of in-process work (open work packages), plus the budget for level of effort and apportioned effort.

A contractor must utilize anticipated learning when developing the time-phased BCWS. Any recognized method used to apply learning is usually acceptable as long as the BCWS is established to represent as closely as possible the expected actual cost (ACWP) that will be charged to the cost account/work package.

These costs can then be applied to any level of the work breakdown structure (i.e., program, project, task, subtask, work package) for work that is completed, in-program, or anticipated. Using these definitions, the following variance definitions are obtained:

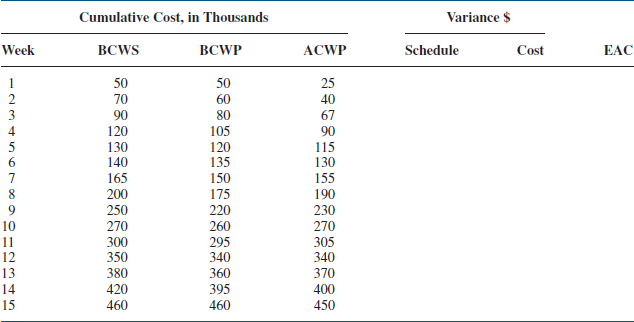

- Cost variance (CV) calculation:

CV = BCWP − ACWP

A negative variance indicates a cost-overrun condition.

- Schedule variance (SV) calculation:

SV = BCWP − BCWS

A negative variance indicates a behind-schedule condition.

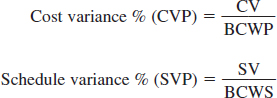

In the analysis of both cost and schedule, costs are used as the lowest common denominator. In other words, the schedule variance is given as a function of cost. To alleviate this problem, the variances are usually converted to percentages:

The schedule variance may be represented by hours, days, weeks, or even dollars.

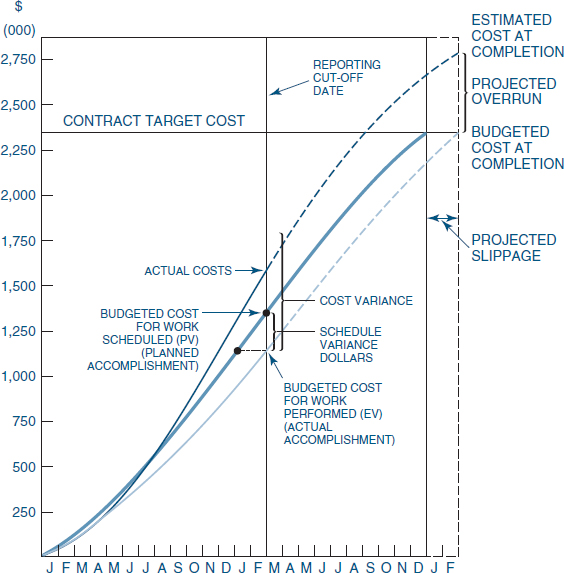

As an example, consider a project that is scheduled to spend $100K for each of the first four weeks of the project. The actual expenditures at the end of week four are $325K. Therefore, BCWS = $400K and ACWP = $325K. From these two parameters alone, there are several possible explanations as to project status. However, if BCWP is now known, say $300K, then the project is behind schedule and overrunning costs.

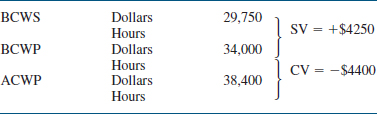

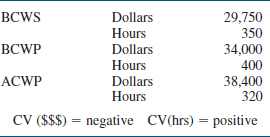

It is important to understand the physical meaning of CV and SV. Consider the following example:

- BCWS = $1000

- BCWP = $800

- ACWP = $700

In this example, the units are dollars. The units could have just as easily been hours, days, or weeks. In this example, CV = $800 − $700 = +$100. Because CV is a positive value, it indicates that physical progress was accomplished at a lower cost than the forecasted cost. This is a favorable situation. Had CV been negative, it would have indicated that physical progress was accomplished at a greater cost than what was forecasted. If CV = 0, then the physical accomplishment was as budgeted.

Although CV is measured in hours or dollars, it is actually a measurement of the efficiency with which physical progress was accomplished compared with the plan. To correct a negative cost variance, emphasis should be placed upon the productivity rate (i.e., burn rate) at which work is being performed.

Returning to the above example, SV = $800 − $1000 = −$200. In this example, the schedule variance is a negative value, indicating that physical progress is being accomplished at a slower rate than planned. This is an unfavorable condition. If the schedule variance were positive, this would indicate physical progress being accomplished at a faster rate than planned. If SV = 0, physical progress is being accomplished as planned.

The schedule variance, SV, measures the timeliness of the physical progress compared to the plan whereas the cost variance, CV, measures the efficiency. To correct a negative schedule variance, emphasis should be placed upon improving the speed by which work is being performed.

The cost variance relates to the real cost. However, the problem with SV is how it relates to the real schedule. The schedule variance is determined from cost account or work package financial numbers and does not necessarily relate to the real schedule. The schedule variance does not distinguish between critical path and non-critical path work packages. The schedule variance by itself does not measure time. A negative schedule variance indicates a behind-schedule condition but does not mean that the critical path has slipped. On the contrary, the real schedule (i.e., precedence networks or the arrow diagramming networks) could indicate that the project will be ahead of schedule. A detailed analysis of the real schedule is still required irrespective of the value for the schedule variance.

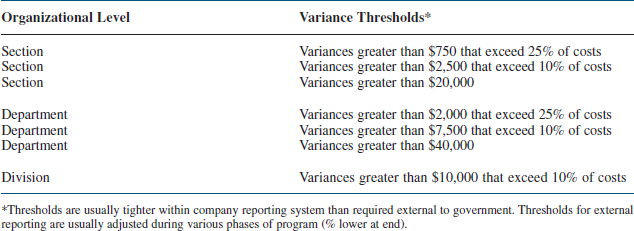

Variances are almost always identified as critical items and are reported to all organizational levels. Critical variances are established for each level of the organization in accordance with management policies.

Not all companies have a uniform methodology for variance thresholds. Permitted variances may be dependent on such factors as:

- Life-cycle phase

- Length of life-cycle phase

- Length of project

- Type of estimate

- Accuracy of estimate

Variance controls may be different from program to program. Table 15-2 identifies sample variance criteria for program X.

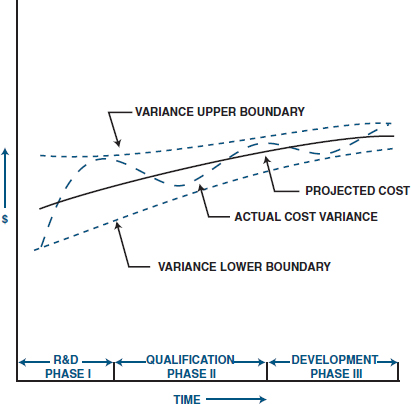

For many programs and projects, variances are permitted to change over the duration of the program. For strict manufacturing programs (product management), variances may be fixed over the program time span using criteria as in Table 15-2. For programs that include research and development, larger deviations may be permitted during the earlier phases than during the later phases. Figure 15-11 shows time-phased cost variances for a program requiring research and development, qualification, and production phases. Since the risk should decrease as time goes on, the variance boundaries are reduced. Figure 15-12 shows that the variance envelope in such a case may be dependent on the type of estimate.

By using both cost and schedule variance, we can develop an integrated cost/schedule reporting system that provides the basis for variance analysis by measuring cost performance in relation to work accomplished. This system ensures that both cost budgeting and performance scheduling are constructed on the same database.

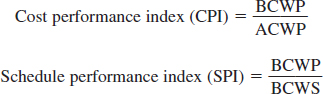

In addition to calculating the cost and schedule variances in terms of dollars or percentages, we also want to know how efficiently the work has been accomplished. The formulas used to calculate the performance efficiency as a percentage of EV are:

TABLE 15-2. VARIANCE CONTROL FOR PROGRAM X

FIGURE 15-11. Project variance projection.

If CPI = 1.0, we have perfect cost performance. If CPI < 1.0, physical progress is being accomplished at a greater cost than forecasted. This is unfavorable. If CPI > 1.0, physical progress is being accomplished at less than the forecasted cost, which is favorable. Similar to CV, CPI measures the efficiency by which the physical progress was accomplished compared to the plan or baseline. For an unfavorable value of CPI, emphasis should be placed upon improving the productivity by which work was being performed.

If SPI = 1.0, we have perfect schedule performance. If SPI < 1.0, physical progress was accomplished at a slower rate than what was planned. This is unfavorable. If SPI > 1.0, physical progress was accomplished at a faster rate than what was planned, which is favorable. For an unfavorable value of SPI, emphasis should be placed upon improving the timeliness of the physical progress.

SPI and CPI are expressed as ratios compared to the performance factor of 1.0 whereas CV and SV are expressed in hours or dollars. One historic reason for this is that SPI and CPI can be used to show performance for a specified time period or trends over a long time horizon without disclosing actual company sensitive numbers. This makes SPI and CPI valuable tools for customer status reporting without disclosing hard numbers.

FIGURE 15-12. Methodology to variance.

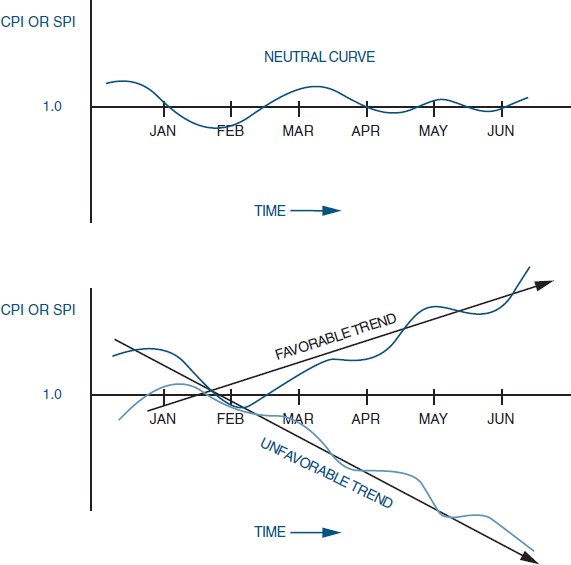

The cost and schedule performance index is most often used for trend analysis as shown in Figure 15-13. Companies use either three-month, four-month, or six-month moving averages to predict trends. Trend analysis provides an early warning system and allows managers to take corrective action. Unfortunately, its use may be restricted to long-term projects because of the time needed to correct the situation.

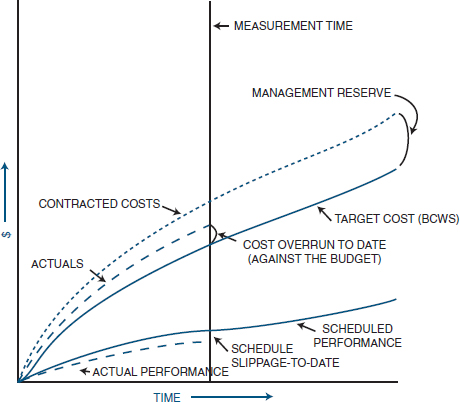

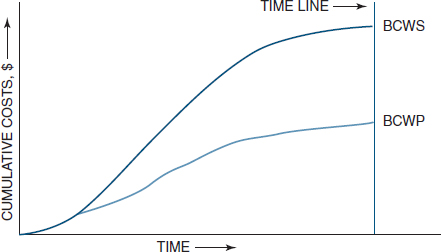

Figure 15-14 shows an integrated cost/schedule system. The figure identifies a performance slippage to date. This might not be a bad situation if the costs are proportionately underrun. However, from the upper portion of Figure 15-14, we find that costs are overrun (in comparison to budget costs), thus adding to the severity of the situation.

Also shown in Figure 15-14 is the management reserve. This is identified as the difference between the contracted cost for projected performance to date and the budgeted cost. Management reserves are the contingency funds established by the program manager to counteract unavoidable delays that can affect the project's critical path. Management reserves cover unforeseen events within a defined project scope, but are not used for unlikely major events or changes in scope. These changes are funded separately, perhaps through management-established contingency funds. Actually, there is a difference between management reserves (which come from project budgets) and contingency funds (which come from external sources) although most people do not differentiate. It is a natural tendency for a functional manager (and some project managers) to substantially inflate estimates to protect the particular organization and provide a certain amount of cushion. Furthermore, if the inflated budget is approved, managers will undoubtedly use all of the allocated funds, including reserves. According to Parkinson4:

FIGURE 15-13. The performance index.

FIGURE 15-14. Integrated cost/schedule system.

- The work at hand expands to fill the time available.

- Expenditures rise to meet budget.

Managers must identify all such reserves for contingency plans, in time, cost, and performance (i.e., PERT slack time).

The line indicated as actual cost in Figure 15-14 shows a cost overrun compared to the budget. However, costs are still within the contractual requirement if we consider the management reserve. Therefore, things may not be as bad as they seem.

Government subcontractors are required to have a government-approved cost/schedule control system. The information requirements that must be demonstrated by such a system include:

- Budgeted cost for work scheduled (BCWS)

- Budgeted cost for work performed (BCWP)

- Actual cost for work performed (ACWP)

- Estimated cost at completion

- Budgeted cost at completion

- Cost and schedule variances/explanations

- Traceability

The last two items imply that standardized policies and procedures should exist for reporting and controlling variances.

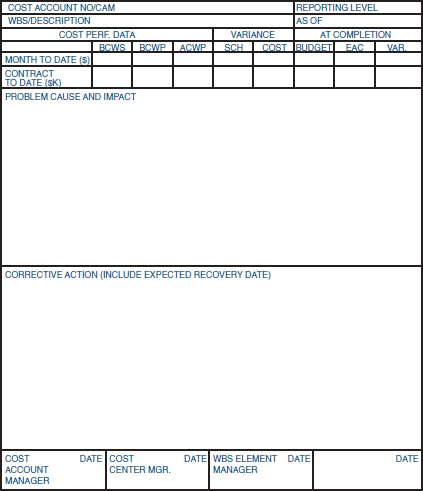

When permitted variances are exceeded, cost account variance analysis reports, as shown in Figure 15-15, are required. Required signatures may include:

- The functional employees responsible for the work

- The functional managers responsible for the work

- The cost accountant and/or the assistant project manager for cost control

- The project manager, work breakdown structure element manager, or someone with signature authority from the project office

For variance analysis, the goal of the cost account manager (whether project officer or functional employee) is to take action that will correct the problem within the original budget or justify a new estimate.

Five questions must be addressed during variance analysis:

- What is the problem causing the variance?

- What is the impact on time, cost, and performance?

- What is the impact on other efforts, if any?

- What corrective action is planned or under way?

- What are the expected results of the corrective action?

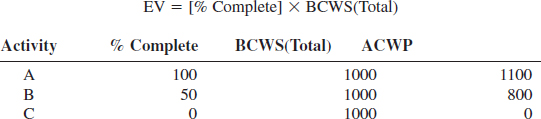

One of the key parameters used in variance analysis is the “earned value” concept, which is the same as BCWP. Earned value is a forecasting variable used to predict whether the project will finish over or under the budget. As an example, on June 1, the budget showed that 800 hours should have been expended for a given task. However, only 600 hours appeared on the labor report. Therefore, the performance is (800/600) × 100, or 133 percent, and the task is underrunning in performance. If the actual hours were 1,000, the performance would be 80 percent, and an overrun would be occurring.

The major difficulty encountered in the determination of BCWP is the evaluation of in-process work (work packages that have been started but have not been completed at the time of cutoff for the report). The use of short-span work packages or establishment of discrete value milestones within work packages will significantly reduce the work-in-process evaluation problem, and procedures used will vary depending on work package length. For example, some contractors prefer to take no BCWP credit for a short-term work package until it is completed, while others take credit for 50 percent of the work package budget when it starts and the remaining 50 percent at completion. Some contractors use formulas that approximate the time-phasing of the effort, others use earned standards, while still others prefer to make physical assessments of the work completed to determine the applicable budget earned. For longer work packages, many contractors use discrete milestones with preestablished budget or progress values to measure work performed.

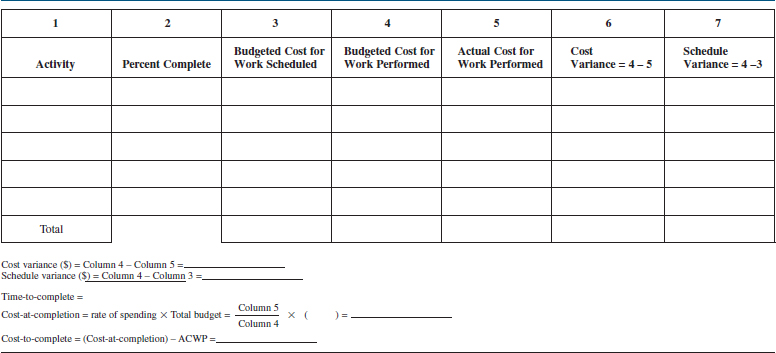

The difficulty in performing variance analysis is the calculation of BCWP because one must predict the percent complete. The simplest formula for calculating BCWP is:

BCWP = (% complete) × BAC

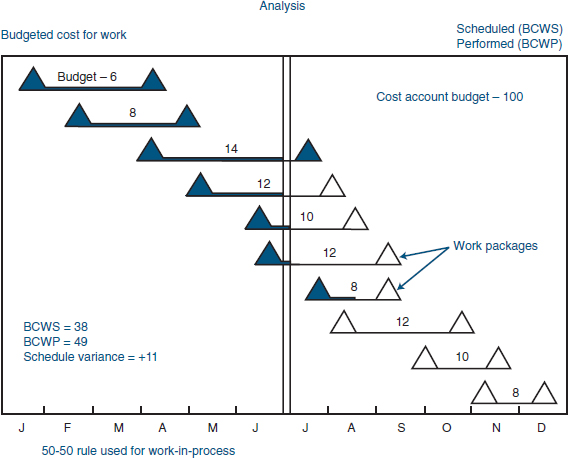

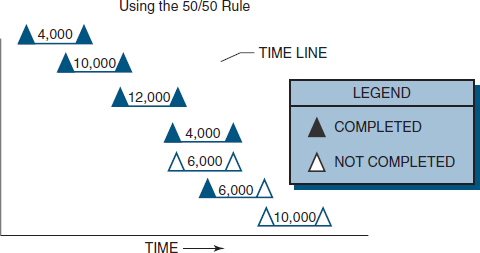

Most people calculate “percent complete” based upon task durations. However, a more accurate representation would be to calculate “percent work complete.” However, this requires a schedule that is resource loaded. To eliminate this problem, many companies use standard dollar expenditures for the project, regardless of percent complete. For example, we could say that 10 percent of the costs are to be “booked” for each 10 percent of the time interval. Another technique, and perhaps the most common, is the 50/50 rule:

FIGURE 15-16. Analysis showing use of 50/50 rule.

Half of the budget for each element is recorded at the time that the work is scheduled to begin, and the other half at the time that the work is scheduled to be completed. For a project with a large number of elements, the amount of distortion from such a procedure is minimal. (Figures 15-16 and 15-17 illustrate this technique.)

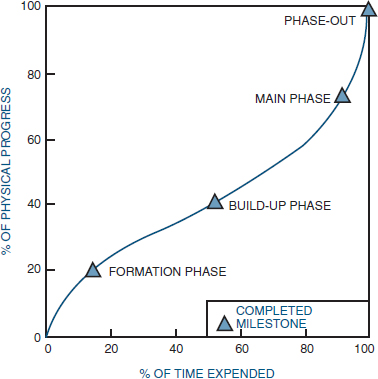

One advantage of using the 50/50 rule is that it eliminates the necessity for the continuous determination of the percent complete. However, if percent complete can be determined, then percent complete can be plotted against time expended, as shown in Figure 15-18.

There are techniques available other than the 50/50 rule5:

- 0/100: Usually limited to work packages (activities) of small duration (i.e., less than one month). No value is earned until the activity is complete.

- Milestone: This is used for long work packages with associated interim milestones, or a functional group of activities with a milestone established at identified control points. Value is earned when the milestone is completed. In these cases, a budget is assigned to the milestone rather than the work packages.

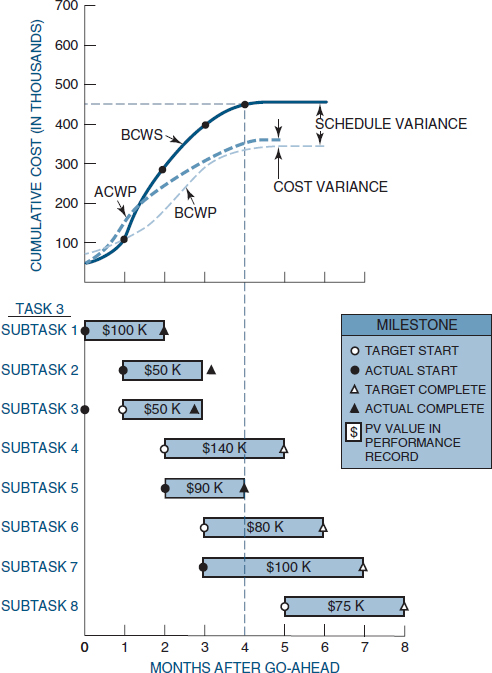

FIGURE 15-17. Project Z, task 3 cost data (contractual).

- Percent complete: Usually invoked for long-duration work packages (i.e., three months or more) where milestones cannot be identified. The value earned would be the reported percent of the budget.

- Equivalent units: Used for multiple similar-unit work packages, where earnings are on completed units, rather than labor.

- Cost formula (80/20): A variation of percent complete for long-duration work packages.

- Level of effort: This method is based on the passage of time, often used for supervision and management work packages. The value earned is based on time expended over total scheduled time. It is measured in terms of resources consumed over a given period of time and does not result in a final product.

- Apportioned effort: A rarely used technique, for special related work packages. As an example, a production work package might have an apportioned inspection work package of 20 percent. There are only a few applications of this technique. Many people will try to use this for supervision, which is not a valid application. This technique is used for effort that is not readily divisible into short-span work packages but that is in proportion to some other measured effort.

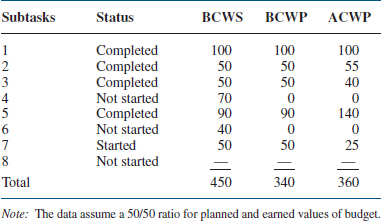

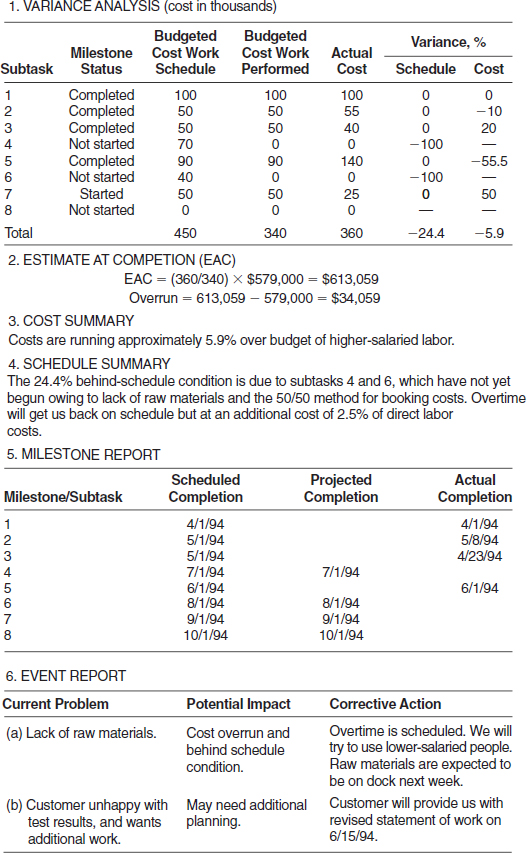

Generally speaking, the concept of earned value may not be an effective control tool if used in the lower levels of the WBS. Task levels and above are normally worth the effort for the calculation of earned value. As an example, consider Figure 15-17, which shows the contractual cost data for task 3 of project Z, and Table 15-3, which shows the cost data status at the end of the fourth month. The following is a brief summary of the cost data for each subtask in task 3 at the end of the fourth month:

- Subtask 1: All contractual funds were budgeted. Cost/performance was on time as indicated by the milestone position. Subtask is complete.

- Subtask 2: All contractual funds were budgeted. A cost overrun of $5,000 was incurred, and milestone was completed later than expected. Subtask is completed.

- Subtask 3: Subtask is completed. Costs were underrun by $10,000, probably because of early start.

TABLE 15-3. PROJECT Z, TASK 3 COST DATA STATUS AT END OF FOURTH MONTH (COST IN THOUSANDS)

- Subtask 4: Work is behind schedule. Actually, work has not yet begun.

- Subtask 5: Work is completed on schedule, but with a $50,000 cost overrun.

- Subtask 6: Work has not yet started. Effort is behind schedule.

- Subtask 7: Work has begun and appears to be 25 percent complete.

- Subtask 8: Work has not yet started.

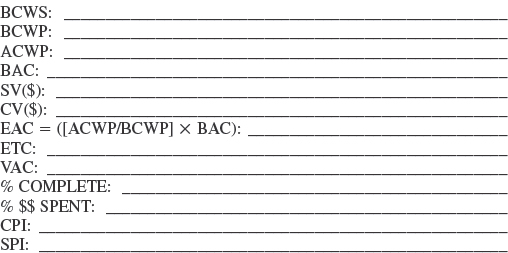

To complete our analysis of the status of a project, we must determine the budget at completion (BAC) and the estimate at completion (EAC). Table 15-4 shows the parameters for variance analysis.

- The budget at completion is the sum of all budgets (BCWS) allocated to the project. This is often synonymous with the project baseline. This is what the total effort should cost.

- The estimate at completion identifies either the dollars or hours that represent a realistic appraisal of the work when performed. It is the sum of all direct and indirect costs to date plus the estimate of all authorized work remaining (EAC = cumulative actuals + the estimate-to-complete).

Using the above definitions, we can calculate the variance at completion (VAC):

VAC = BAC − EAC

TABLE 15-4. THE PARAMETERS FOR VARIANCE ANALYSIS

The estimate at completion (EAC) is the best estimate of the total cost at the completion of the project. The EAC is a periodic evaluation of the project status, usually on a monthly basis or until a significant change has been identified. It is usually the responsibility of the performing organization to prepare the EAC.

The calculation of a new EAC and subsequent revision does not imply that corrective action has been taken. Consider a three-month task that is 99 percent complete and was budgeted to spend $400K (BCWS). The actual costs to date (ACWP) are $395K. Using the 50/50 rule, BCWP is $200K. The estimated cost-to-complete (EAC) ratio is $395K/$200K, which implies that we are heading for a 100 percent cost overrun. Obviously, this is not the case.

Using the data in Table 15-5, we can calculate the estimate at completion (EAC) by the expression

where BAC is the value of BCWS at completion.

The discussion of what value to use for BAC is argumentative. In the above calculation, we used burdened direct labor dollars. Some people prefer to use nonburdened labor with the argument that the project manager controls only direct labor hours and dollars. Also, the calculation for EAC did not include material costs or general and administrative costs.

The above calculation of EAC implies that we are overrunning labor costs by 6.38% and that the final burdened labor cost will exceed the budgeted burdened labor cost by $34,059. For a more precise calculation of EAC we would need to include material cost (assumed at $70,000) and G&A. This would give us a final cost, excluding profit, of $751,365, which is an overrun of $37,365. The resulting profit would be $86,000 less $37,365, or $48,635. The final analysis is that work is being accomplished almost on schedule except for subtask 4 and subtask 6, but costs are being overrun.

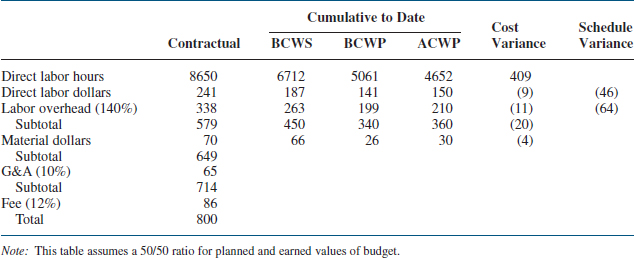

The question that remains is, “Where is the cost overrun occurring?” To answer this question, we must analyze the cost summary sheet for project Z, task 3. Table 15-5 represents a hypothetical case for the cost elements of project Z, task 3. From Table 15-5 we see that negative (overrun) variances exist for labor dollars, overhead dollars, and material costs. Because labor overhead is measured as a percentage of direct labor dollars, the problem appears to be in the direct labor dollars.

From the contractual column in Table 15-5 the project was estimated at $27.86 per hour direct labor ($241,000/8650 hours), but actuals to date are $150,000/4652 hours, or $32.24 per hour. Therefore, higher-salaried people than anticipated are being employed. This salary increase is partially offset by the fact that there exists a positive variance of 409 direct labor hours, indicating that these higher-salaried employees are performing at a more favorable position than expected on the learning curve. Since the milestones (from Figure 15-17) appear to be on target, work is progressing as planned, except for subtask 4.

TABLE 15-5. PROJECT Z, TASK 3 COST SUMMARY FOR WORK COMPLETED OR IN PROGRESS (COST IN THOUSANDS)

The labor overhead rate has not changed. The contractual, BCWS, and BCWP overhead rates were estimated at 140 percent. The actuals, obtained from month-end reports, indicate that the true overhead rate is as predicted.

The following conclusions can be drawn:

- Work is being performed as planned (almost on schedule, although at a more favorable position on the learning curve), except for subtask 4, which is giving us a schedule delay.

- Direct labor costs are increasing through the use of higher-salaried employees.

- Overhead rates are as anticipated.

- Direct labor hours must be reduced even further to compensate for increased costs, or profits will be drastically reduced.

This type of analysis could have been carried out to one more level by identifying exactly which departments were using the more expensive employees. This step should probably be completed anyway to see if lower-paid employees are available and can work at the required position on the learning curve. Had the labor costs been a result of increased labor hours, this step would have definitely been necessary to identify the reason for the overrun in-house. Perhaps poor estimating was the cause.

In Table 15-5, there also appears a positive variance in materials. This likewise should undergo further analysis. The cause may be the result of improperly identified hardware, material escalation costs increasing beyond what was planned, increased scrap factors, or a change in subcontractors.

It should be obvious from the above analysis that a detailed investigation into the cause of variances appears to be the best method for identifying causes. The concept of earned value, although a crude estimate, identifies trends concerning the status of specific WBS elements. Using this concept, the budgeted cost for work scheduled (BCWS) may be called planned earned value (PEV), and the budgeted cost for work performed (BCWP) may be referred to as actual earned value (AEV). Earned values are used to determine whether costs are being incurred faster or slower than planned. However, cost overruns do not necessarily mean that there will be an eventual overrun, because the work may be getting done faster than planned.

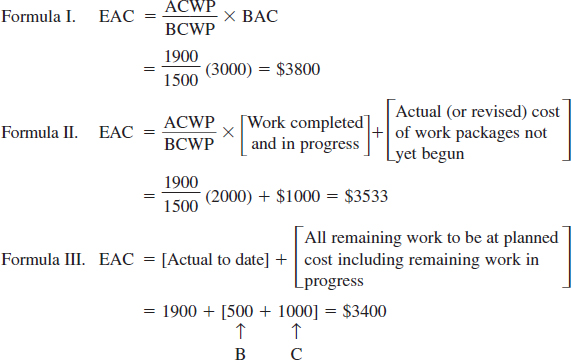

There are several formulas that can be used to calculate EAC. Using the data shown below, we can illustrate how each of three different formulas can give a different result. Assume that your project consists of these three activities only.

Advantages and disadvantages exist for each formula. Formula I assumes that the burn rate (i.e., ACWP/BCWP) will be the same for the remainder of the project. This is the easiest formula to use. The burn rate is updated each reporting period.

Formula II assumes that all work packages not yet opened will be completed at the planned cost. However, it is possible for planned cost to be revised based upon history from completed work packages.

Formula III assumes that all remaining work is independent of the burn rate incurred thus far. This may be unrealistic unless all remaining work can be reestimated if necessary.

TABLE 15-6. VARIANCE ANALYSIS CASE STUDIES

Other techniques are available for determining final completion costs.6 The value of the technique selected is based upon the dollar value of the project, the risk, the quality of the cost accounting system, and the accuracy of the estimates. The estimating techniques here use only labor costs. Material costs can be added into each equation to obtain total cost.

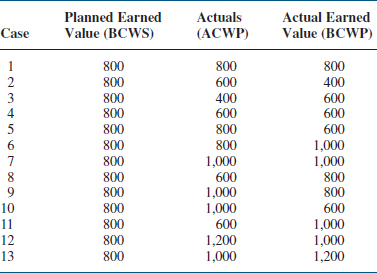

Thirteen cases for comparing planned versus actual performance are shown in Table 15-6. Each case is described below using the relationships:

- Cost variance = actual earned value − actuals

- Schedule/performance variances = actual earned value − planned earned value

Case 1: This is the ideal planning situation where everything goes according to schedule.

Case 2: Costs are behind schedule, and the program appears to be underrunning. Work is being accomplished at less than 100 percent, since actuals exceed AEV (or BCWP). This indicates that a cost overrun can be anticipated. This situation grows even worse when we see that we are also 50 percent behind schedule. This is one of the worst possible cases.

Case 3: In this case there is good news and bad news. The good news is that we are performing the work efficiently (efficiency exceeds 100 percent). The bad news is that we are behind schedule.

Case 4: The work is not being accomplished according to schedule (i.e., is behind schedule), but the costs are being maintained for what has been accomplished.

Case 5: The costs are on target with the schedule, but the work is 25 percent behind schedule because the work is being performed at 75 percent efficiency.

Case 6: Because we are operating at 125 percent efficiency, work is ahead of schedule by 25 percent but within scheduled costs. We are performing at a more favorable position on the learning curve.

Case 7: We are operating at 100 percent efficiency and work is being accomplished ahead of schedule. Costs are being maintained according to budget.

Case 8: Work is being accomplished properly, and costs are being underrun.

Case 9: Work is being accomplished properly, but costs are being overrun.

Case 10: Costs are being overrun while underaccomplishing the plan. Work is being accomplished inefficiently. This situation is very bad.

Case 11: Performance is ahead of schedule, and the costs are lower than planned. This situation results in a big Christmas bonus.

Case 12: Work is being done efficiently, and a possible cost overrun can occur. However, performance is ahead of schedule. The overall result may be either an overrun in cost or an underrun in schedule.

Case 13: Although costs are greater than those budgeted, performance is ahead of schedule, and work is being accomplished very efficiently. This is also a good situation.

In each of these cases, the concept of earned value was used to predict trends in cost and variance analysis. This method has its pros and cons.

Each of the critical variances (or earned values) identified usually requires a formal analysis to determine the cause of the variance, the corrective action to be taken, and the effect on the estimate to completion. These analyses are performed by the organization that was assigned the budget (BCWS) at the level of accumulation directed by program management.

Organization-Level Analysis

Each critical variance identified on the organizational MCCS reports may require the completion of MCCS variance analysis procedures by the supervisor of the cost center involved. Analyzing both the work breakdown and organizational structure, the supervisor systematically concentrates his efforts on cost and schedule problems appearing within his organization.

Analysis begins at the lowest organizational level by the supervisor involved. Critical variances are noted at the cost account on the MCCS report. If a schedule variance is involved and the subtask consists of a number of work packages, the supervisor may refer to a separate report that breaks down each cost account into the various work packages that are ahead or behind schedule. The supervisor can then analyze the variance on the basis of the work package involved and determine with the aid of supporting organizations the cause of the variance, the corrective action that can be taken, or the possible effect on associated or future planned effort.

Cost variances involving labor are analyzed by the supervisor on the basis of the performance of his organization in accomplishing the work assigned, within the budgeted man-hours and planned labor rate. The cause of any variance to this performance is determined, and corrective action is then implemented.

Cost variances on nonlabor efforts are analyzed by the supervisor with the aid of the program team member and other supporting organizations.

All material variance analyses are normally initiated by cost accounting as a service to the using organization. These variance analyses are completed, including cause and corrective action, to the extent that can be explained by cost accounting. They are then sent to the using organization, which reviews the analyses and completes those resulting from schedule performance or usage. If a variance is recognized as a change in the material acquisition price, this information is supplied by cost accounting to the responsible organization and a change to the estimate-to-complete is initiated by the using organization.

The supervisor should forward copies of each completed MCCS variance analysis/EAC change form to his higher-level manager and the program team member.

Program Team Analysis

The program team member may receive a team critical variance report that lists variances in his organization at the lowest level of the work breakdown structure at the division cost center level by cost element. Upon request of the program manager, analyses of variances contributing to the variances on the team critical variance report are summarized by the responsible program team member and reviewed with the program manager.

The preparation of status reports, whether they be for internal management or for the customer, should, at a minimum, answer two fundamental questions:

- Where are we today (with respect to time and cost)?

- Where will we end up (with respect to time and cost)?

The information necessary to answer these questions can be obtained from the following formulas:

- Where are we today?

- Cost variances (in dollars/hours and percent complete)

- Schedule variances (in dollars/hours and percent complete)

- Percent complete

- Percent money spent

- Where will we end up?

- Estimate at completion (EAC)

- The remaining critical path

- SPI (trend analysis)

- CPI (trend analysis)

Since SPI and CPI are used for trend analyses, we can use CPI and SPI to forecast the expected final cost and the expected end date of the project. We can express the cost at completion, EAC, as:

![]()

The time at completion uses SPI for the forecast and can be expressed as:

![]()

Care must be taken with the use of SPI to calculate the new project length because a favorable vale for SPI (i.e., > 1.0) could be the result of work packages that are not on the critical path.

Once EAC and the new project length are calculated, we can calculate the variance at completion (VAC) and the estimated cost to complete (ETC) using the following two formulas:

VAC = BAC − EAC and ETC = EAC − ACWP

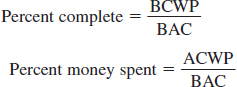

Percent complete and percent money spent can be obtained from the following formulas:

where BAC is the budget at completion.

The program manager uses this information to review the program status with upper-level management. This review is normally on a monthly basis on large projects. In addition, the results of these analyses are used to explain variances in the contractually required reports to the customer.

After the analyses of the variances have been made, reports must be developed for both the customer and in-house (upper-level) management. Customer reporting procedures and specifications can be more detailed than in-house reporting and are often governed by the contract. Contractual requirements specify the reports required, the frequency of submission and distribution, and the customer regulation that specifies the preparation instructions for the report.

The types of reports required by the customer and management depend on the size of the program and the magnitude of the variance. Most reports contain the tracking of the vital technical parameters. These might include:

- The major milestones necessary for project success

- Comparison to specifications

- Types or conditions of testing

- Correlation of technical performance to the activity network and the work breakdown structure

One final note about reports: To save time and money, reports might be only one or two pages or fill-in-the-blank forms.

15.7 THE COST BASELINE

PMBOK® Guide, 4th Edition

7.2.3 Cost Base line

Once the project is initiated, the project team establishes the cost or financial base-line against which status will be reported and variances will be measured. Figure 15-19 represents a cost baseline. Each block represents a cost account or work package element. The summation of all of the cost accounts or work packages would then equal the time-phased budget. Each work package would then be described through the work authorization form for that work package.

FIGURE 15-19. The cost baseline.

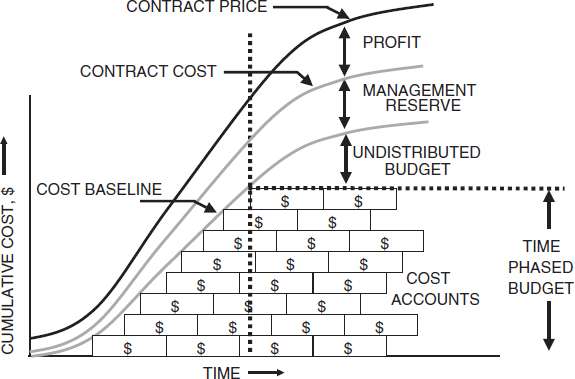

The cost baseline in Figure 15-19 is just part of the cost breakdown. An illustration of a cost breakdown appears in Figure 15-20.

There are certain distinguishing features of Figure 15-20:

- The time-phased budget, which is the released budget, is the summation of all BCWS elements.

- The cost baseline is the summation of the time-phased budget (i.e., the distributed budget) and the undistributed budget. This will equal the released, planned budget at completion (BAC).

- The contractual cost to complete the project is the summation of the cost baseline and the management reserve, assuming that a management reserve exists.

- The contract price is the contract cost plus the profit, if any.

15.8 JUSTIFYING THE COSTS

Project pricing is often based upon best guesses rather than concrete estimates. This is particularly true for companies that survive on competitive bidding and where the preparation cost of a bid may vary between $50,000 and $500,000. If the probability of winning a bid is low, then the company may spend the minimum amount of time and cost during bid preparation.

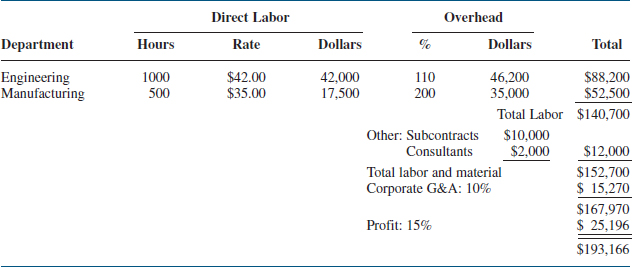

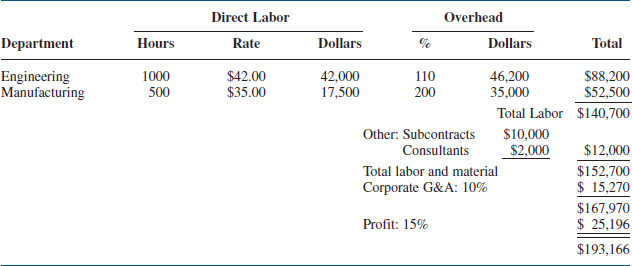

Table 15-7 shows a typical project pricing summary.

In Table 15-7, each functional area or division can have its own overhead rate. In this summary, the overhead rate for engineering is 110 percent, whereas the manufacturing overhead rate is 200 percent. If this company is a subsidiary of a larger company, then a corporate general and administrative (G&A) cost may be included. If the project is for an external customer, then a profit margin will be included.

Once the project pricing summary is completed, the costs must be justified before some executive committee. This is shown in Figure 15-21.

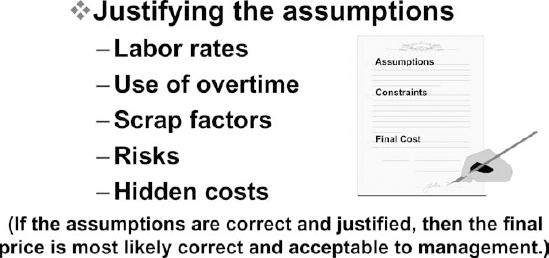

Every company has its own evaluation criteria cost summary approval process. Typical elements that must be justified or supported by hard data include:

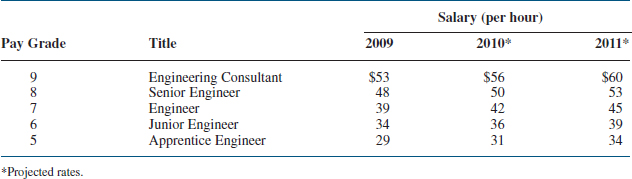

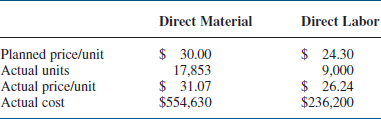

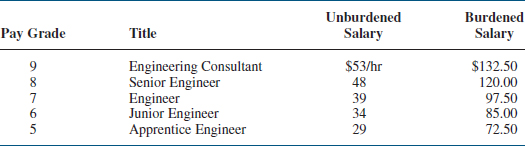

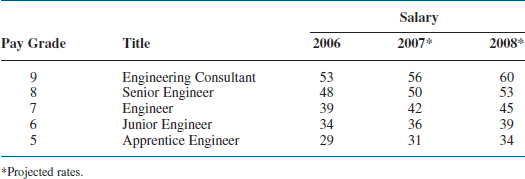

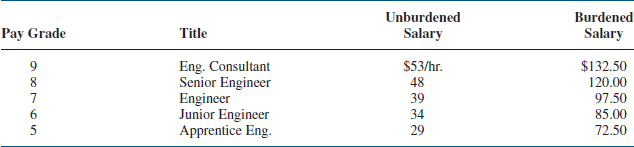

- Labor Rates: For estimating purposes, department averages or skill set weighted averages can be used. This is sometimes called the blended rate. The best-case scenario would be estimating from the actual salary or skill set of the workers to be assigned. This may be impossible during competitive bidding because we do not know who will be available or who will be assigned assuming the contract is received. Also, if the project is a multiyear effort, we may need forward pricing rates, which are the predicted, full burdened salaries anticipated in the next few years. This is illustrated in Table 15-8.

TABLE 15-7. TYPICAL PROJECT PRICING SUMMARY

- Overtime: If resources are scarce and the company has no intention of hiring additional resources, then some of the work must be accomplished on overtime. This could increase the cost of the project and an allowance must be made for possible mistakes made during this period of excessive overtime.

- Scrap Factors: If the project includes procurement of raw materials, then some scrap factor allowance may be necessary. This calculation may be impacted by the skill set of the resources assigned and using the materials, previous experience using these materials, and experience on these types of projects.

TABLE 15-8. FORWARD PRICING RATES: SALARY (Departmental Pay Structure)

- Risks: Risk analysis may be based upon the quality of the estimates and experience of those who made the estimates. Other risks considered include the company's ability to achieve the anticipated benefits or the designated profits and, if a disaster occurs, the company's exposure and liability for lawsuits.

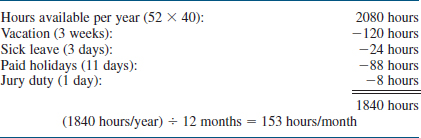

- Hidden Costs: These costs, some of which are illustrated in Figure 15-22, can erode all of the profitability expected on a project. Another potentially hidden cost is the yearly or monthly workload availability. A typical calculation appears in Table 15-9. If we use Table 15-9 and all of the workers are long-term employees, then there may be less than 1840 hours available per year because senior people may have earned more than three weeks of vacation per year.

TABLE 15-9. HOURS AVAILABLE FOR WORK

15.9 THE COST OVERRUN DILEMMA

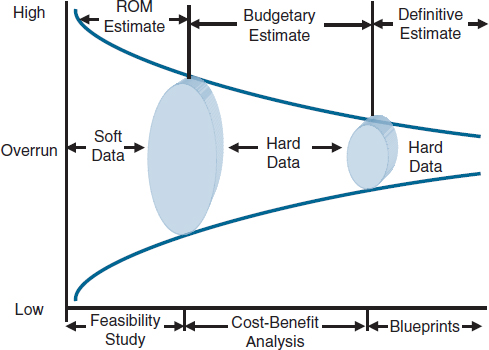

The lifeblood of most organizations is a continuous stream of new products or services. Because of the word “new,” historical data may be at a minimum and cost overruns are expected. Figure 15-23 shows a typical range of overruns.

Rough order-of-magnitude (ROM) estimates are often made from “soft” data, which can result in a wide range of overruns, and are used in the initiation phase of a project. As we go from soft data to hard data and enter the planning phase of a project, the accuracy of the estimates improves and the range of the overruns narrows.

When overruns occur, the project manager looks for ways of reducing costs. The simplest way is to reduce scope. This begins with a search for items that are easy to cut. The items that are easiest to cut are those items that were poorly understood during the estimating process and were therefore underestimated. Typical items that are cut or reduced in magnitude include:

- Project management supervision

- Line management supervision

- Process controls

- Quality assurance

- Testing

FIGURE 15-23. Range of overruns.

If the easy-to-cut items do not provide sufficient cost reductions, then a desperate search begins among the hard-to-cut items. Hard-to-cut items include:

- Direct labor hours

- Materials

- Equipment

- Facilities

- Others

If the cost reductions are unacceptable to management, then management must decide whether or not to pull the plug and cancel the project. Pulling the plug may seem like an easy decision, but it turns out to be one of the most difficult decisions for executives to make. Typical reasons for not pulling the plug include:

- Quantitative reasons

- High exit barriers

- Significant expenditures have been made and are unrecoverable

- Penalty clauses

- Breach-of-contract lawsuits

- Payments to terminated workers

- Low salvage value of goods and property

- High plant closing costs

- Moving people may end up violating seniority and labor agreements

- Qualitative reasons

- Viewing failure as a sign of weakness

- Viewing failure as damage to one's career

- Viewing failure as damage to one's reputation

- Viewing failure as a roadblock to promotion

- Fear of exposing one's mistakes to others

- Viewing bad news as a personal failure

- Refusing to admit defeat or failure

- Seeing what one wants to see rather than seeing reality

15.10 RECORDING MATERIAL COSTS USING EARNED VALUE MEASUREMENT

Using “earned value” measurement, the actual cost for work performed represents those direct and indirect costs identified specifically for the project (contract) at hand. Both the recorded and reported costs must relate specifically to this effort. Recording direct labor costs usually presents no problem since labor costs are normally recorded as the labor is accomplished. Therefore, recorded and reported labor will be the same.

Material costs, on the other hand, may be recorded at various times. Material costs can be recorded as commitments, expenditures, accruals, and applied costs. All provide useful information and are important for control purposes.

Because of the choices available for material cost analysis, material costs should be reported separately from the standard labor hour/labor dollar earned value report. For example, cost variances associated with the procurement of material may be determined at the time that the purchase orders are negotiated and placed with the vendors since this information provides the earliest visibility of potential cost variance problems. Significant variances in the anticipated and actual costs of materials can have a serious effect on the total contract cost and should be reflected promptly in the estimated cost at completion (EAC) and explained in the narrative part of the project status report.

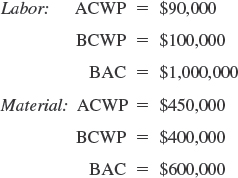

Separating labor from material costs is essential. Consider the following example:

Example 15-1. You are budgeted to spend $1,000,000 in burdened labor and $600,000 in material. At the end of the first month of your project, the following information is made available to you:

For simplicity's sake, let us use the following formula for EAC:

EAC = (ACWP/BCWP) × BAC

Therefore,

EAC(labor) = $900,000

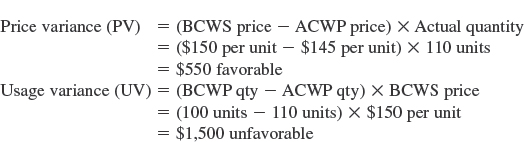

EAC(material) = $675,000