Chapter 15

Financing Mediterranean Electricity Infrastructure: Challenges and Opportunities for an Interconnected Mediterranean Grid

Houda Ben Jannet Allal*

Abstract

The chapter offers a brief overview of the Mediterranean energy context, situation, and prospects based on OME findings. In addition, the issue of financing electricity infrastructures in the southern and eastern Mediterranean (SEM) is examined, highlighting regulatory and market challenges as well as socioeconomic opportunities, in an attempt to promote the investment urgently required to deal with the expected increase in energy needs. In this regard, the main regulatory issues that a more interconnected Mediterranean grid entails are discussed as one of the most important factors related to financing features. Finally, some pragmatic recommendations are proposed to feed the debate and draw attention to the main policy implications.

Keywords

energy policy

electricity markets

regulation

electricity infrastructure

crossborder investments

transmission system operator (TSO)

national regulatory authority (NRA)

financial markets

public–private partnership

institutional investors

multilateral financing

1. Introduction: regional energy context and OME vision

Before addressing the question of financing electricity infrastructure in the Mediterranean, it seems appropriate to present an overview of the regional energy context in terms of energy policy and perspectives. Energy is not in itself a final good, but energy services are a key component of economic development, contributing to improving overall social welfare. In this respect, energy should be secure and sustainable, safe and affordable, efficient and competitive; it should take into account resource availability and environmental challenges. Thus, the question is how to cope with increasing energy needs, in particular electricity demand, both in the short and the long run. To that end, a sound analysis of the investment needed in the future seems to be crucial. This exercise requires a shared vision of energy system development in the region, within a cooperative approach.

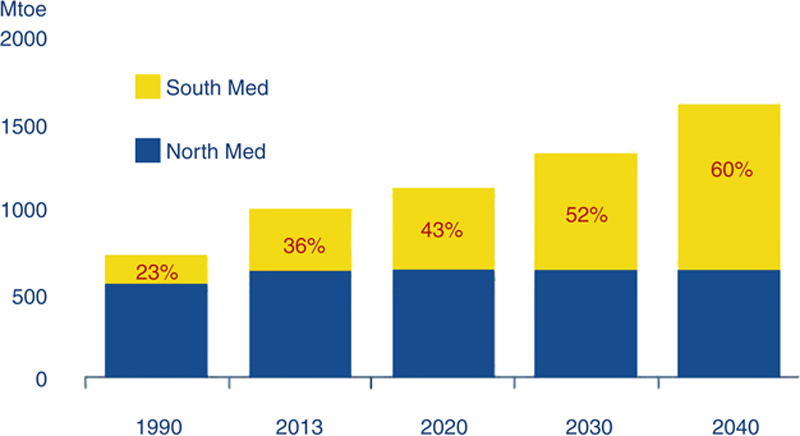

According to the OME scenarios (OME, 2015), the demand in the Mediterranean region is growing rapidly as a result of population and economic growth. Most of the increase in Mediterranean energy demand is expected to be concentrated in the southern and eastern Mediterranean countries (SEMCs). Indeed, the OME Conservative Scenario1 shows almost a doubling of energy demand from 2013 to 2030 (362–687 Mtoe), and something close to a tripling a decade later (up to 958 Mtoe in 2040). Turkey and Egypt alone are expected to reach 566 Mtoe in 2040, which is more than half of the total energy demand in the south. These two countries represent more than half of the total increase of energy demand in the entire region with some 367 Mtoe of additional energy consumption (Fig. 15.1).

Figure 15.1 Energy demand by region.

As for electricity perspectives, demand is expected to remain almost stable in the north Mediterranean over the next two decades, while it would more than triple in the south and in the east during the same period (from 47 Mtoe in 2013 to about 146 Mtoe in 2040). In terms of electricity demand per capita, steady growth is expected in the south, even though this increase will remain far below levels in the north over the next two decades (Fig. 15.2).

Figure 15.2 Electricity demand per capita.

From the supply side, energy dependency in the Mediterranean region is presently about 44%, and reaches 66% for fossil fuels, although regional production is still considerable. By 2040, dependency may increase despite recent discoveries and promising available resources, mainly because of sustained growth in demand in the region.

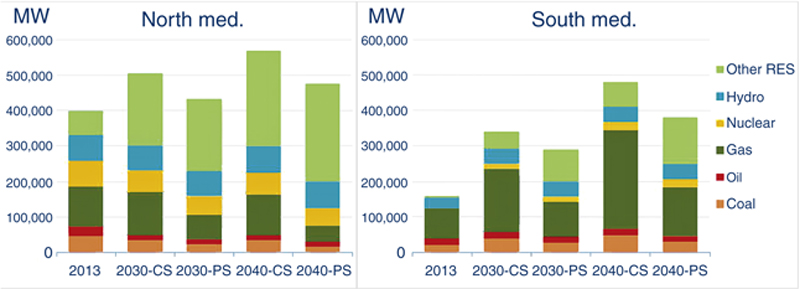

In all scenarios, both Conservative and Proactive, hydrocarbons will play a major role in the electricity generation mix at the regional level. According to the Conservative Scenario, 446 GW of natural gas-fired power plants are expected in 2040 (from 202 GW in 2013), of which 280 GW are in the south and east Mediterranean (SEM) (from 86 GW in 2013). Renewables will also play an important role and are expected to reach around 449 GW of installed capacity in 2040 (105 GW in the SEM), of which 331 GW are from nonhydro (61 GW in the SEM). Most global additions in terms of installed capacity are expected to take place in the south and east (313 GW, including nuclear), whereas 218 GW are expected in the north, where most additions will be from renewable energy sources (RES) (Fig. 15.3).

Figure 15.3 Installed capacity by region.

To achieve resilience at the regional level in this respect, taking into account current and future energy challenges, social concerns, and environmental risks, we consider the following five axes essential to making energy development more sustainable:

• energy efficiency and demand-side management;

• optimal use of all resources and technologies at the regional level;

• infrastructure investment;

• well-designed public policies;

• capacity building.

There is a clear need for long-term investment, both for development and for transformation of the Euro-Mediterranean energy sector. The International Energy Agency (IEA, 2014) estimates total amount of investment required in Europe up to 2035 in just the power sector at more than US$2 trillion (OECD/IEA, 2014). In SEMCs, OME estimates investment in additional generation capacity will amount to €715 billion by 2030.

In its recent report, the IEA argues that: “decisions to commit capital to the energy sector are increasingly shaped by government policy measures and incentives, rather than by signals coming from competitive markets (…). Private sector participation is essential to meet energy investment needs in full, but mobilizing private investors and capital will require a concerted effort to reduce political and regulatory uncertainties (…). New types of investors in the energy sector (smaller market players and new entrants) are emerging, but the supply of long-term finance on suitable terms is still far from being guaranteed (…). The increase of small and distributed renewables reduces the share of utilities, and will rely more on debt financing.”(OECD/IEA, 2014, p. 12).

All this fully applies to the Euro-Mediterranean region, where major efforts are needed to attract investment. As recognized by every international institution and actor alike, it requires: a stable political and economic system; transparent, consistent, and credible policies; an adapted institutional and legal framework; satisfactory market regulation based on competitive neutrality; and independent national regulatory authorities for the energy system and market competition. The latter includes budget independence and a management commissioning process. In this regard, regional cooperation between national regulatory authorities is essential, and the role of the Association of Mediterranean Energy Regulators (MEDREG) is crucial to promoting a clear, stable, transparent, and harmonized regulatory framework in the Mediterranean area.

In addition to this, reforming energy subsidy policies are also fundamental to creating a favorable and pertinent framework for investments. This has already started in several countries in the region and should proceed in a progressive and consistent manner. Such reform should be further complemented by significant and targeted social policies for access to modern energy.

As already highlighted, a shared view of the transition toward energy demand in light of technology innovation and deployment as well as understanding the new role of economic actors in a changing environment are of crucial importance. In such a situation, investment in infrastructure (particularly in electricity transmission and generation) should leverage all sources available – public and private, local and international – taking into account the specificity of every actor to tackle the main financing challenges.

The first of the remaining sections in this chapter (Section 15.2) presents and analyzes the challenges involved in financing infrastructure in the SEM, focusing on the role of public–private partnerships and multilateral financing. Section 15.3 deals with the important issue of setting a common regulatory and institutional framework. Some recommendations are proposed in order to establish a concrete pathway for progressive integration of electricity systems in the region. Section 15.4 concludes by identifying policy implications at both the institutional and regulatory level, which suggest proceeding by taking a gradual and more pragmatic bottom-up approach.

2. The challenge of financing infrastructure in SEMCs

The financing infrastructure in most SEMCs is strictly linked to ongoing transformations in the global electricity industry, the weakness of local capital markets, and the fragmentary reform process.

There is a need for a more balanced public–private approach and for innovative risk-sharing mechanisms to facilitate mobilization of the private sector. Financing infrastructure development in the electricity sector is not only a question of efficient allocation of resources, but also concerns the economic characteristics of infrastructure – high capital intensity, elements of natural monopoly, and location-specific investments – all of which affect private sector incentives to commit long-term capital.

Economic and financial expansion of the power sector in the SEM requires a larger share of private capital and governments to increase their focus on creating the necessary conditions to attract domestic and foreign capital. Creating appropriate economic signals is necessary for providing incentives for investments that not only can be financed, but also reward the ownership of assets.

As the IEA underlines, “Even where states and state-owned companies take direct responsibility for energy investment, pressures on public funds and the need for new technology and expertise create room for greater private involvement.”(OECD/IEA, 2014, p. 12). There is a clear role here for institutional actors – multilateral and bilateral financing institutions, such as the European Investment Bank (EIB) and the European Bank for Reconstruction and Development (EBRD), and selected institutional investors such as sovereign wealth funds and pension funds – to act as intermediaries in the market and leverage additional funding notably for renewable energy projects and network investments, while reducing transaction costs and capital risks.

To foster such a process, regional cooperation would help to pool resources and mobilize private funding. With this end in mind governments should ensure there is no discrimination between actors regarding access to finance. In addition, it would be appropriate to strengthen domestic financial markets, increase the range of financial products available, and derisking policy schemes that reduce the interest rate on capital lending.

The bottlenecks to ensure a healthy flow of capital from international markets to SEM infrastructure projects subsist at the political, institutional, and regulatory level. There is a real need to unlock new sources of finance, via growth of bonds, securitization, and equity markets, and, potentially, by tapping into the large funds held by institutional investors. Multilateral financing can play a crucial role in providing risk mitigation instruments (including guarantees and political risk insurance) and promoting the development of local capital markets (OECD/IEA, 2014).

Foreign direct investment is important to finance new infrastructure, especially in markets where privatization reforms are implemented. Multilateral development banks, regional development banks, and import/export agencies have a variety of mechanisms and instruments available to facilitate foreign investor activity. However, governments will continue to have a key role to play in mitigating risks by creating a legal system capable of giving assured legal protection, planning for the establishment of financial sectors, and providing multilateral agreements on investments. The long lifetime of power infrastructure and long amortization periods inflate the risk of political change over the lifetime of a project (Cambini and Rubino, 2014).

At present, no single solution fits all countries. Public entities will remain major players in the financing, development, and delivery of infrastructure services in many SEMCs. Fundamental improvements in their creditworthiness will be essential to facilitate access to global and domestic capital markets, as well as to bring in private equity investments to a range of public–private partnerships. Corporate-level and sector-specific reforms will have to be pursued. At the corporate level, investment planning, financial reporting, and corporate governance should have to meet commercial standards, and public listing of companies may reduce the transaction costs of capital flows. This would allow them to tap capital markets more easily to raise money. With this end in mind, reforms in the regulatory environment will be essential to minimize regulatory risk. Furthermore, transparency and corporate standards may stimulate more efficient management.

Substantial investments in SEM infrastructure are unlikely to materialize unless there is a strong institutional framework that protects creditor rights and has effective covenants and reliable avenues of legal enforcement and remedy. Over the longer term, enhancing SEMC infrastructure access to international capital markets will also require developing an international mechanism to deal with crossborder investment regulation, competition rules, and consistency between national regulatory regimes. As technology increasingly interacts with economic pressures to regionalize infrastructure industries and open them up to international competition, the consistency and compatibility of national competition laws and policies will become more important for achieving gains. Where elements of competition and natural monopoly coexist and are complementary, the regulation of third-party access to essential facilities is essential.

The challenge involved in financing infrastructure requires a cooperative regional approach to foster investment and exploit energy complementarities between countries across the region. This can be done by progressive reform of market design and the regulatory framework in SEMCs, and by developing new interconnectors and supporting power exchanges, particularly from renewables, whose potential is huge.

The OME is trying to adapt such a regional integration process to the electricity sector by helping to identify the main issues to be tackled and proposing some recommendations expected to offer improvements in terms of policies and measures to implement. In OME and Medgrid (2013), a number of actions and recommendations have been identified that should deliver a more interconnected power system across the region.

3. Toward an interconnected Mediterranean grid: some regulatory perspectives

The idea of integrating electricity systems in the region is based on the assumption that regional integrated markets are more effective than fragmented national ones at delivering benefits in terms of a more secure, more stable, and more affordable power supply. In addition, the integration of power systems in the Mediterranean region will contribute to orient cooperation between Mediterranean systems toward open electricity markets characterized by transparency, reciprocity, and nondiscrimination in all countries.

The potential for regional electricity trade in the Mediterranean (and its “corridors”) is particularly significant, given the great complementarity between supply and demand profiles across the region. However, despite this crossborder trade potential, the volume of electricity exchanged among Euro-Mediterranean countries is presently very low. This is evident in the south, where physical interconnections between North African countries exist. However, the utilization rate of these infrastructures is often very low. As for north–south exchanges, they are even lower and are limited to just the trans-Mediterranean interconnection between Spain and Morocco, through the Strait of Gibraltar.

Suboptimal exploitation of regional complementarities in terms of power exchanges is mainly due to lack of cooperation between countries, lack of transmission networks (both domestic and crossborder), lack of technical coordination in terms of system operations and measures (when the infrastructure exists but is not adequately exploited), and unsatisfactory regulatory harmonization. All these deficiencies represent a set of drawbacks that jeopardize the development of a more integrated regional electricity system by discouraging investment to the detriment of wider social welfare.

As a general rule, clear separation between politics, regulation, and system exploitation at the institutional level seems necessary to create a more attractive environment to foster investment in infrastructure. In countries where monopolies exist, there is often confusion between these roles. Introducing clear separation between political authorities (that remain responsible for defining the energy policy), regulation (preferably entrusted to a specialized authority independent from politics and participants of the electricity sector), and exploitation (entrusted to companies, either public or private, which take part in the national electricity market) is a fundamental precondition of the reform process.

As for market organization, in countries where national or regional monopolies exist, vertical splitting between different sectors (unbundling) may be necessary to allow the development of competition. In particular, effective dissociation of accounts and operations between “contestable” sectors and those that are regulated (as natural monopolies) is fundamental to guaranteeing effective regulation and adequate control by an independent authority, to eliminating general, indirect, and crossed subsidies, and to establishing tariffs that reflect costs and allow transparent financing of the sector.

The most important objectives of vertical unbundling refer to equitable access to the network for new entrants to ensure market transparency and promote in a nondiscriminatory way infrastructure investment. Moreover, unbundling is essential to avoid cross-subsidies between “contestable” and regulated activities, which affect fair competition negatively and prevent integrated companies from granting, to other branches of the same firm, preferential treatment compared to third competitors. These conditions are also necessary to implement other objectives of the energy policy (in particular, the development of renewable energies and energy efficiency measures).

Today, the process used to integrate Mediterranean electricity systems is based on three pillars: (1) technical coordination allows crossborder networks to be integrated; (2) regulatory harmonization of national regulations; and (3) political cooperation between Mediterranean countries. These three approaches are rooted in the national will of all Mediterranean countries wanting to autonomously implement reforms. This can be done by getting support from the Association of Mediterranean Transmission System Operators (Med-TSO) to promote closer and stronger coordination between Transmission System Operators (TSOs); MEDREG to promote better and institutionalized cooperation among national regulators; and the Union for the Mediterranean (UfM) to enhance political consensus.

Convergence between different institutional and regulatory frameworks across the Mediterranean is essential to move forward, but does not mean reproducing the European model. This is because grid maturity has yet to be achieved in SEMCs, the electricity industrial background is not the same, and energy policy targets are different, as are economic needs and energy priorities.

There is an urgent need for new infrastructure investment such that power systems can be regionally integrated. This requires the establishment of common rules for network operations and electricity trade, a conditio sine qua non for the achievement of this objective. In the aforementioned study (OME and Medgrid, 2013) some recommendations are presented for better identification and implementation of Mediterranean projects of common interest, as well as for establishment of a common regulatory and legal framework enabling mutually beneficial electricity exchanges. However, these recommendations do not aim to apply existing European regulations to all Mediterranean countries. In particular, a fully open and competitive electricity market in the Mediterranean region is both unrealistic in the short to medium term and not adapted to the strong load growth of SEMCs. A more pragmatic approach would allow regulations existing in each country/subregion to evolve progressively and allow north–south and south–south electricity exchanges to the benefit of all Mediterranean countries.

The following recommendations aim at establishing a concrete pathway for such an evolution and should be considered as interim steps toward market integration characterized by transparent, nondiscriminatory conditions and total reciprocity. The main actions to be undertaken are summarized in the remainder of this section.

1. An unbundled TSO and an independent NRA should be established in each Mediterranean country.

In most SEMCs, electricity supply is still the responsibility of an integrated utility, covering generation, transmission, and distribution. To achieve the benefits of Mediterranean integration, new entrants are necessary (in particular, independent power producers) to diversify generation technologies and funding sources. A prerequisite to ensure that independent producers are treated in a nondiscriminatory way is to “unbundle” the TSO from the rest of the incumbent utility and to check the independence of the TSO at least in terms of management and accounting.

An independent NRA should also be created in each Mediterranean country to ensure that all players in the electricity market are treated by the TSO in a nondiscriminatory way. In particular, the regulator will be responsible for checking that independent producers are subject to the same conditions as the generation department of the incumbent utility when it comes to access to the grid.

The unbundled TSO and the independent regulator will have all the necessary capacities to work out a fair and transparent network tariff, ensuring nondiscriminatory grid access for all market players.

The creation of an NRA in each SEMC should follow the principles set out by the MEDREG Institutional Ad Hoc Group, including clear legal status and real independence.

2. Incumbent utilities in SEMCs should take advantage of participating in the European market (being interconnected and within a framework gives rise to fair sharing of costs and benefits for all interconnected countries). They should optimize their participation by establishing a mechanism that coordinates countries in the south.

A fully competitive market, such as the one that exists in the European Union, with open access for all generators and all customers to the grid can only be a long-term target for other Mediterranean countries. In the short term, such a competitive market is not considered a practical approach, especially when taking into account the need to cope with the rapid growth in electricity demand in SEMCs. Regulations in these countries should evolve step by step toward open access to the grid (with an unbundled TSO) for an increasing number of new players.

When an SEMC is first interconnected to an EU member state, the incumbent utility in the SEMC should become an active player in the European market. In this way the incumbent utility could submit demand and offer bids, based on the costs of its own generation units, thus allowing short-term north–south exchanges. As a result of proper sharing of congestion rents, benefits may appear on both sides. This step has already been completed in the Spain–Morocco interconnection with the Moroccan utility ONEE participating in the Iberian market, although balanced sharing of congestion rents on this interconnector remains pending.

Furthermore, incumbent utilities in other SEMCs that are not directly connected to Europe but only via a first SEMC should also be players in the European market (by transiting across the first SEMC). The possibility of setting up a coordination mechanism in the south by which incumbent utilities in several interconnected SEMCs participating in the same EU market could merge their bids prior to submission to the market should be explored. A coordination mechanism covering several SEMC utilities participating together in the same European market could allow them short-term exchanges, not only bilaterally between each of them and the EU market, but also directly between them. Pricing of south–south exchanges could follow the same rules as that of north–south exchanges (i.e., based on the same bid prices covering the extent of north–south interconnector capacity).

Further steps toward market integration will progressively lead to balanced sharing of congestion rents in north–south interconnectors, north–south reciprocity of conditions for access to the grid and to the market, and transparency of electricity prices in southern countries.

3. Regulation in SEMCs should allow independent producers access to the grid and to north–south interconnectors under fair and transparent conditions.

In the short term, independent producers in SEMCs should not be limited to power purchase agreements (PPA) with the incumbent national monopoly. Access conditions should be published by the TSO for the internal grid of the SEMC and for interconnection with the EU. Access conditions – which must be fair, transparent, and nondiscriminatory – should cover:

a. First connection to the national grid in the SEMC (cost, delay).

b. Congestion management (guarantee of access).

c. Pricing of access (e.g., through regulated tariffs, capacity auctioning, or other nondiscriminatory mechanisms).

d. Settlement of imbalances (preferably with reference to actual system conditions, instead of a fixed tariff).

More precisely, the access tariff for a north–south interconnector should separately show the price for accessing the interconnector itself, the price for accessing the adjacent main transmission grid, and the price for the inter-TSO compensation mechanism (if any). Once the costs and congestion rents have been shared in the case of a regulated interconnector, it is recommended that the national regulator in each country consider various possibilities for cost recovery by the TSO, namely:

a. Fee for actual use of the infrastructure.

b. Socialization of costs through a national grid tariff (this solution would remove barriers to crossborder trade).

More generally, the TSO in each SEMC should develop a grid code stipulating technical access rules in detail subject to approval by the NRA. Eventually, national grid codes should be harmonized, under supervision of MEDREG and Med-TSO, and coordinated by the European Network of Transmission System Operators for Electricity (ENTSO-E).

4. A compensation mechanism should be developed for Mediterranean TSOs to cover the costs in their existing grids as a result of hosting crossborder transits (originating/ending in other countries).

Crossborder trade in energy between Mediterranean countries can induce transit flows into national grids that are neither the origin nor destination of the energy. The TSOs in transited grids need to be compensated for the costs incurred, including additional losses. For EU member states, an inter-TSO compensation (ITC) mechanism has been set up to resolve this issue, based on European Regulation (EU) No. 838/2010.

It is recommended that a similar mechanism (separate from the European one) be set up to cover compensation for all Mediterranean countries once they are interconnected (with a possible contribution from Med-TSO and supervision by MEDREG). In the longer term, consideration could be given to merging the Mediterranean compensation mechanism with the European one.

5. National legislations and regulations should specifically address north–south interconnector issues in all Mediterranean countries.

It must be emphasized that north–south interconnectors are not subject to EU legislation, but to national legislations in northern and southern countries. Depending on the country interconnected, the transmission infrastructure can be “regulated” (i.e., subject to national regulations concerning ownership and/or access rules) or (less often) “merchant” (i.e., partially or totally exempted from observing regulatory obligations in terms of third-party access, congestion rent, assets remuneration, etc.). However, in almost all cases national legislations concerning north–south interconnectors are rather vague. It is therefore recommended that it be made more precise.

a. National legislation that only allows regulated north–south interconnectors could authorize TSOs to sell very long–term transmission rights to such interconnectors to satisfy the needs of producers (in coherence with the prescriptions of European grid codes).

b. National legislation could also allow merchant north–south interconnectors that are exempted from regulations. The conditions for exemption could be defined in each country based on those already existing in the EU regulations.

Above all, it is recommended that SEMCs consider signing the Energy Charter Treaty, which provides more security to foreign investors.

6. North–south interconnector projects should be considered relevant candidates in the selection process for “Projects of Common Interest” without encountering any form of discrimination.

The Regulation on Guidelines for Trans-European Infrastructure (EU) No. 347/2013 introduces the possibility of selecting some transmission infrastructure as “Projects of Common Interest” (PCI), which benefit from several advantages: faster authorization procedures, access to special sources of funding, and possibly cost sharing between several beneficiary countries. These advantages would be highly beneficial to north–south interconnector projects; their promoters should apply to the PCI selection process and participate actively, together with the TSO of the third country concerned, in the corresponding regional group led by the EC. Two regional groups are relevant for north–south interconnector projects, corresponding to two priority corridors: “north–south electricity interconnections in western Europe” and “north–south electricity interconnections in central eastern and southeastern Europe.”

Particular attention should be paid to showing that a north–south interconnector project involves at least two member states (a condition required for a project to be considered a PCI): it allows for delivery of energy from renewable sources in a third country not only to one member state, but to several EU countries. This can be checked, as required by the European regulation, by showing the capacity increase brought by the interconnector at an essential cross-section of a north–south priority corridor.

As required by the European Regulation on Energy Infrastructure, ENTSO-E has developed a methodology for cost–benefit analysis (CBA) of PCI candidates. It is recommended that some improvements to this methodology be investigated, to better show the contribution of north–south interconnector projects to electricity exchanges between countries in the priority corridor. Once an interconnector project is regulated, the results of CBA could be used to share interconnector project costs between the third country and the member states concerned according to their respective benefits.

7. A first-ever Mediterranean-wide Ten-Year Network Development Plan should be drawn up by Mediterranean TSOs.

To progress toward a more integrated grid between all Mediterranean countries, it is absolutely necessary to identify the need for new infrastructure, not only for new north–south interconnectors, but also for new south–south and north–north interconnectors. A common approach is required between all Mediterranean TSOs and their regulators.

It is recommended that Mediterranean TSOs, in close cooperation with ENTSO-E draw up a Mediterranean-wide Ten-Year Network Development Plan (TYNDP), with the participation of all interested stakeholders, possibly following the same principles as its EU equivalent. The Mediterranean TYNDP, possibly updated every 3 years, should reflect the long-term needs of transmission grids around the Mediterranean Sea and identify bottlenecks, mainly in interconnectors (north–north, north–south, and south–south), but also possibly in internal grids.

Furthermore, CBA should be made possible for new infrastructure in the Mediterranean grid. Therefore, it is recommended to set up a model of the Mediterranean power system (north and south), including data over the years n + 5 to n + 20, for all Mediterranean countries concerned. This model could be based on that under construction for the European grid and then extended to all other Mediterranean countries. This task should be given to Med-TSO in close cooperation with ENTSO-E.

8. A cost-sharing mechanism should be developed to cover the cost of grid reinforcement needed by Mediterranean countries to accommodate crossborder transits (based on a CBA approach).

Grid reinforcement may be necessary in Mediterranean countries purely to accommodate larger numbers of crossborder transits. In such a case, corresponding costs should not be covered by national consumers, but by the final beneficiaries of crossborder transits in the countries of origin and/or destination. If grid reinforcement is located in an EU member state, it can be considered a PCI, and the cost issue can be resolved by Regulation on Energy Infrastructure (EU) No. 347/2013, since this introduces a regulatory procedure for cost sharing, based on Europe-wide CBA.

If grid reinforcement is located in an SEMC, or in an EU member state but has not been selected as a PCI,’ the cost-sharing mechanism described in the regulation is not applicable and another similar mechanism has to be introduced. This mechanism must be agreed ex ante and remain stable in the long term, so as to minimize uncertainties for the investor in the new grid infrastructure as well as for those making use of it. Med-TSO and MEDREG could investigate the issue.

9. For a new north–south interconnector project, governments, TSOs, and investors should commit themselves by getting together within an adequate contractual framework.

The contractual framework for a new north–south interconnector project must be adapted to the diverse situations found in the north and in the south as well as to the diverse responsibilities of governments and TSOs on both sides. Therefore, governments, TSOs, and investors involved in a new north–south interconnector project (TSOs can be investors themselves in the case of a regulated interconnector) should adopt a contractual framework including the following agreements:

a. An intergovernmental agreement to ensure international cooperation in the project and, in particular, the provision of land rights and permission for electricity transmission in the interconnector.

b. For each part (north and south) of the project, an agreement between the local government (north and south, respectively) and investors. The purpose of the agreement is to expand on issues dealt with by the intergovernmental agreement.

c. An interoperability agreement between TSOs and investors (submitted for regulatory approval), covering all issues related to system operation and market operation (including access conditions by third parties).

In the absence of an interoperability agreement for a regulated north–south interconnector, the two TSOs would have to compete against each other during the operational life of the infrastructure, each TSO trying to keep a larger part of the revenue from access by users of the interconnector, ultimately to the detriment of the latter. Furthermore, the interconnector project could be articulated in several “vehicles” (companies) should this be deemed necessary for a particular regulatory situation (in the north and in the south) or for a particular task (construction, asset ownership, and management operation).

10. Long-term transmission rights should be available to mitigate the risks of congestion incurred by producers of electricity from renewable sources in SEMCs willing to export.

The standard duration of long-term transmission rights given to interconnectors in the EU is presently 1 year (expected to be pluriannual with the new grid code “forward capacity allocation”). It is therefore recommended to offer at least the same duration to the whole Mediterranean region.

Furthermore, electricity producers from renewable sources in an SEMC may need transmission rights with longer durations, since their installations are characterized by high upfront investment costs. This makes them much more risky investments than conventional installations, which have lower investment costs. Therefore, investors in renewable installations need long-term visibility for their market arrangements to secure their investment. They should have the possibility to buy (very) long-term transmission rights (on timescales longer than 1 year, possibly 10 years or more).

Should very long-term transmission rights for all market players not be considered compatible with competition policy, the availability of such rights could be studied at least for those producers of renewable energy (in EU member states or in SEMCs) who do not receive support for their energy in their own country. Transmission rights over very long periods (10 years or more) would also be beneficial for investors in the interconnector. This is a way to secure long-term revenues, thus facilitating the financing of investment. Such an approach is already used for the gas infrastructure (open season) and should be considered for a new Mediterranean interconnector.

4. Policy implications and conclusions

Linking Mediterranean countries together through electricity highways is a long-standing idea introduced as far back as the 1930s as a promise of peace in the region.

Today, technological advances put this possibility within our reach: continuous current links can transport impressive amounts of energy under the sea and on land; converter stations for switching from AC to DC are able to interconnect different-sized networks; and sophisticated control means and new “smart” devices allow for responsive demand and supply. Technology is no longer an obstacle and should even continue to improve. However, many obstacles still exist; they are not technological but regulatory entailing consequences in terms of finance availability.

North Mediterranean EU countries needed over 20 years to define common rules of power exchange as part of an integrated electricity market. This work is still in progress, notably to develop a European “network code” and a long-term network development plan. In addition to this, there still exist insufficiently interconnected European countries such as Italy and Spain. However, large amounts of electricity are traded every day, every hour, between European countries in a transparent and nondiscriminatory way. These exchanges allow the provision of mutual aid between countries and contribute to the most efficient use of generation facilities in Europe, enabling lower power supply costs.

On the other hand, there is no general framework today for electricity trading in the SEM. There exist agreements between countries allowing for “technical” exchanges, specifically dedicated to mutual aid, and a few “commercial” exchanges entailing real benefits in terms of cost reduction and efficiency improvements.

Despite these two different systems and related regulatory frameworks, it is remarkable that north–south trade is regularly practiced in two precursor systems set up for it by Spain and Morocco through the submarine interconnection crossing the Strait of Gibraltar.

Both countries have succeeded in building a pragmatic and operational system that allows them both to share real trade benefits. In the present context, Spain could sell its excess power generation and Morocco can sometimes benefit from cheaper electricity than that produced by its own production facilities. According to our scenarios, energy transfer in the future could occur in both directions using the capacity of existing lines and even requiring creation of new interconnection links.

The recommendations we have made stem from propositions derived from our analysis. They are also based on a case study of the electricity trade between Morocco and Spain. These two countries, placed as they are in very different regulatory systems (an open and competitive market in Spain; a single-buyer, integrated business in Morocco), decided to proceed following a successful pragmatic approach which represents a good example to take into consideration.

In this respect, our recommendations aim to offer a pragmatic perspective without transferring the European model to the SEM. However, they highlight some fundamental issues that need to be dealt with in order to proceed toward a more interconnected regional grid in a more comprehensive and coordinated way.

A bottom-up approach has been considered a better way to proceed than the more traditional top-down method, which has proved inefficient and scarcely attractive to SEMCs. Regional institutions such as Med-TSO, MEDREG, and the UfM Secretariat are the expression of a common objective that domestic TSOs, national regulators, and governments share toward integration of electricity systems across the Mediterranean. This approach helps to identify common needs and draw regional perspectives in areas of action such as sector regulation and governance, regional TSO commitment, and legal frameworks. Such action might be framed in the newly established “Euro-Mediterranean Platform on Regional Electricity Market” (Box 15.1), with the aim of becoming a new catalyst for development of a more integrated regional electricity system on the basis of an inclusive, pragmatic, and bottom-up approach (MEDREG, 2014).

It is here that sector-based organizations, industrial associations, financing institutions, and scientific cooperation projects, at national and supranational level, will play a central role in undertaking actions and implementing measures. This will also contribute to enhancing capacity building and transfer of know-how to SEMCs, which are fundamental aspects for a coherent and harmonized development process. Associations and organizations with a regional remit are particularly functional for catalyzing the fundamental interests of private stakeholders, and represent an important link between the industry, the financing milieu, and the scientific community operating in the Mediterranean area. Furthermore, they work in cooperation with institutions such as the UfM Secretariat, MEDREG, and Med-TSO, which is essential to addressing issues and providing specific analysis on different topics.

Financing the energy infrastructure in the Mediterranean is a complex and articulated undertaking, where financial aspects are interrelated not only with economic ones but also with political, institutional, technical, and regulatory features, in a context that is geopolitically unstable and uncertain, implying more risks for investors. To build a more interconnected Mediterranean grid and proceed toward gradual market integration, it is imperative that nondiscriminatory conditions be applied, with transparency and total reciprocity between countries as the basis of a common regional will that needs to be translated into reality.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.