CHAPTER 6

Portfolio Construction

Markets are constantly in a state of uncertainty and flux and money is made by discounting the obvious and betting on the unexpected.

—George Soros

Portfolio construction is a hot discussion topic that always garners attention, and at times, criticism. I wish it were possible to say that there is only one way to construct a portfolio and the directions are as follows. If followed accurately, you would have on your hands a winning portfolio. Unfortunately, as you might have guessed, there is not one single way to construct a portfolio. Whether the portfolio is conservative in nature or more aggressive, there are numerous opinions on the right way to try to reach the end goal. Some methodology is derived from a very technical or formula-heavy approach, while others subscribe to a more fundamental approach. This is then followed up by connecting these goals to the portfolio's strategy.

In this chapter I will walk you through the different aspects of portfolio construction within the fixed income market. I will outline the three factors I deem most important to portfolio construction and the benefit each factor strives to bring to your portfolio over time.

- Risk defined

- Aligned goals

- Portfolio analysis

The order in which these are transacted in is just as important as the factors themselves. As with almost anything in life, portfolio strategy included, it is important to start by defining what you are looking to accomplish before embarking down the path. The three factors are building blocks that, if not followed properly, may not provide a strong foundation. In this case, a solid portfolio may not be attainable.

It is likely that you are familiar with the concept of the efficient frontier. The Markowitz model outlines the concept that provides the greatest return for the amount of risk that the investor is willing to take. Another way to view this is as you increase the amount of risk you take, you improve the potential for an increase in return.1

With the recent heightened volatility throughout the global markets and economy, it feels as though the balance between risk and return is skewed or unevenly balanced. What I mean is that there is a visible amount of increased downside risk versus the potential for increased reward. This is prevalent within the financial sector. Uncertainty seems to lie behind every corner and headline. This is most evident at the front end of the market. Risk focused on the points at the front end of the curve has always been there, and that is not going to change. Investors are, however, more recently in tune with this notion as the market volatility has increased, creating havoc in fixed income portfolios. The concept of risk versus return should be utilized within the portfolio, within the various asset classes, and for some investors, at each individual security level. At a minimum, the risk should be reviewed at a high level and at the individual security level, which may include monitoring correlations and spread activity.

FACTOR 1: DEFINING YOUR RISK

Just as we defined different types of end investors and portfolio strategies in the previous chapter, we need to take that information and relate it to the preconstruction stage of building the fixed income portfolio. When deciding on the build of a portfolio, a handful of questions need to be answered. These questions include:

- What is the time frame for my investments?

- Is volatility a concern?

- What is the goal for my investments?

These questions will help you shape your portfolio appropriately. Recent years have proven to be difficult for investors for a number of reasons. If your portfolio is constructed with holes and your goals are not aligned properly to your portfolio, a difficult environment will become that much more difficult. For instance, if you are very concerned with volatility, let the equity piece of your portfolio provide the roller-coaster ride. Depending on your risk tolerance, you may not want to introduce added volatility through your fixed income allocation within your portfolio.

FACTOR 2: ALIGNING GOALS

Portfolio construction discussions are usually centered on the allocation between an equity allocation, fixed income, and possibly alternatives. The different allocation or weight between these sectors is usually aligned to the current life stage that the investor may be in. Alignment may also be linked, but not limited, to the portfolio's specific goals. On a cursory level, initial research and common sense tell you that the longer the investment horizon, the more aggressive the investment allocation is likely to be. The reverse occurs as well. In a traditional equity/bond model, the more risk-averse the investor is, the greater the focus on the fixed income allocation. Another way to view this relationship is the closer in reaching the ultimate goal, the greater the fixed income exposure. Simply put, a traditional fixed income asset class is viewed as providing less volatility than the equity markets.

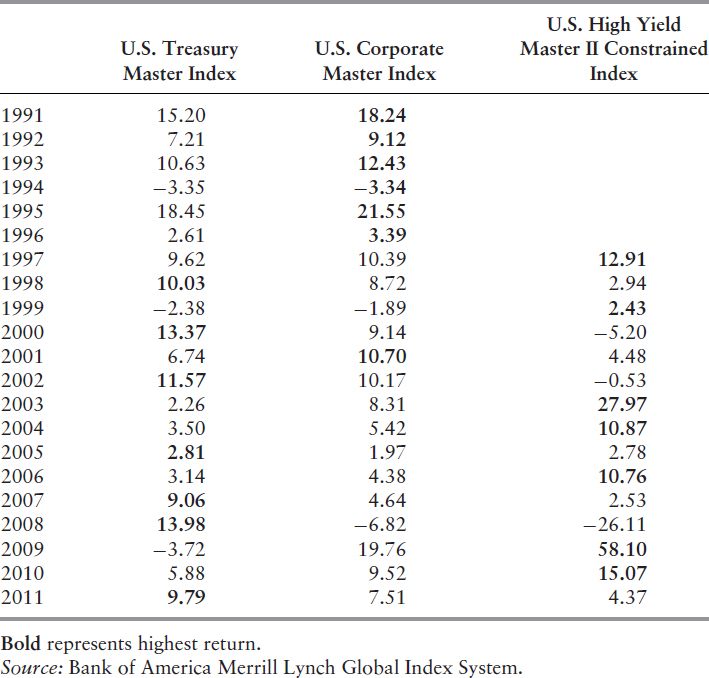

What happens if the portfolio is constructed entirely of fixed income securities? Portfolio goals and strategy should be looked at in similar fashion. Different sectors within the fixed income market carry different characteristics and possible returns. It should not be surprising that over time, the high-yield market (represented by the Bank of America Merrill Lynch U.S. High Yield Master II Constrained index) provides increased returns over the U.S. Treasury sector (represented by the Bank of America Merrill Lynch U.S. Treasury Master index) or even the corporate sector (represented by the Bank of America Merrill Lynch U.S. Corporate Master index), providing greater absolute returns over the Treasury sector. Table 6.1 shows the three sectors discussed. It is clear that the sectors move in and out of favor. This gyration has the potential to make it very difficult to perfectly time a move. Because perfect timing is difficult, there is an increased possibility of falling into the trap of buying high and selling low, in this case rotating in and out of the sector at the most disadvantageous time. There are multiple sectors and subsectors within the fixed income market. I chose the following five sectors represented by an appropriate index for comparison of absolute returns. There is not one sector that predominately outperformed over the time period.

Fixed income sectors are not known to carry high correlations. Table 6.2 shows the correlations to the U.S. Treasury sector. I opted not to run the correlations against all asset classes and just used the Treasury sector as the base. The reason for this is straightforward. The U.S. Treasury market is looked at as the plain vanilla triple-A security, carrying little to no credit risk. Historically, I would have said no credit risk, but due to events over the past couple of years, there needs to be at least the consideration of credit risk when speaking to this sector. As an example, the correlation between the Treasury sector and high-yield is −.714; that is almost 100 percent not correlated.

TABLE 6.1 Index Returns Show that Diversification Matters

This is just one example in favor of diversification. Remember that in the end, if the goal of the portfolio is to achieve consistent returns over the long run, diversification within various sectors is crucial. Later in this chapter, I will stress the importance of diversification and give a few individual security rules on how to remain well diversified.

TABLE 6.2 Correlation to U.S. Treasury market

| Sectors | Treasury |

| Treasury | 1 |

| Agency | 0.897 |

| High-Yield | −0.714 |

| Corporate | 0.367 |

| MBS | 0.868 |

| Time frame: | |

| TSY/Corp 1999–2011 | |

| TSY/HY 1997–2011 | |

| TSY/USD Agency 2000–2011 | |

| TSY/MBS 1999–2011 |

Source: Bank of America Merrill Lynch Global Index System and Bloomberg data.

A sole fixed income portfolio should be addressed the same way as investing within multiple asset classes using portfolio goals or specific characteristics. In addition, aligning a portfolio with particular risk tolerance, possible covenants, and cash flow analysis are used.

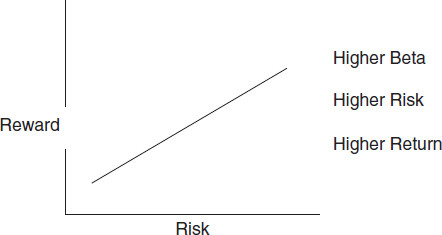

This is where I like to restate the back-to-basics theme. There is no denying that a fixed income portfolio has risk, albeit a different type of risk than your equity or alternative asset classes. A fixed income portfolio should not be the asset class where you are taking the majority of your risk. The trade-off is just not there. There are rewards; however, these rewards usually do not compare to those in other asset classes, such as equities, alternatives, or any other higher-beta asset classes.

Take risk where you get paid for taking risk. Figure 6.1 shows a common basic depiction of the trade-off between risk and reward.

FIGURE 6.1 Trade-off between Risk and Reward

There are different sectors that, at times, are utilized to enhance the portfolio yield or return within the fixed income arena. This may be accomplished through leverage or through higher-beta sectors. In general, when used, an allocation should be minimal. I am not saying to completely abstain from these sectors; just tread lightly. The examples that follow do not include these higher-beta sectors.

Conservative Strategy

The first option all investors have at their disposal is to hide their money under the mattress or in a lockbox in the basement of corporate headquarters. This is the most conservative approach to take, and with money market yields near zero, the mattress may become more appealing. If this option is selected, risks such as fire, theft, and poor sleep due to a lumpy mattress must be mitigated.

Aside from the “bank o' mattress”—which, to be clear, is not really an option—there are varying degrees of conservative strategies. There is always a money market fund, but unfortunately yields are paltry. A more aggressive strategy—the next step or level of risk—is an all-Treasury or government fund. There are positive characteristics with this strategy. To start with, the securities are guaranteed by the U.S. government and carry little to no credit risk. One problem, and potentially a serious one, is that the portfolio is not diversified very well. A secondary concern with this strategy is that it may not keep pace with inflation. It is possible to have a conservative approach while hitting the necessary points to make the portfolio strong and successful. What this strategy won't do is provide you with a government guarantee and a high coupon or yield for the portfolio. Those two characteristics just don't go hand in hand, but they are probably the two most common requests I receive in constructing a portfolio. My answer is always the same. First, I apologize in advance, then I provide the choice to either receive a government guarantee through the Treasury sector or other government products or to receive a more aggressive portfolio attaining a higher yield—just not both at the same time. That is how most of those discussions end.

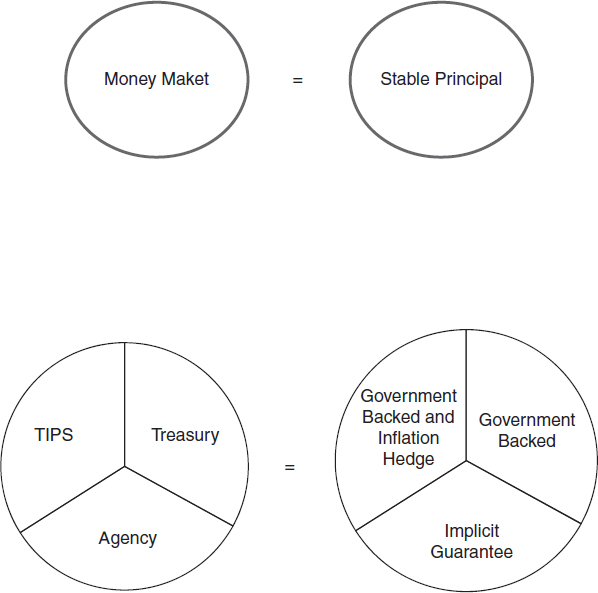

Let's look at a couple of options. Figure 6.2 shows a starting point with a conservative allocation.

This sector allocation represents a conservative allocation with reflection of portfolio goals.

These samples are the starting point or the beginning of the building blocks. The weights can and should be changed to meet risk tolerance, market conditions, and portfolio goals. In the first example, a money market strategy, an investor would expect to have little to no principal volatility and have his or her money available when needed. From the investor's point of view, risk should not be a daily concern. The portfolio manager, on the other hand, should be dissecting and calculating risk on a daily basis, every second of the day. The recent environment created a backdrop where a manager must take nothing for granted. I don't want to say that everything known should be forgotten, but it should be looked at with a new perspective or through a different set of glasses. There are multiple sayings that could be applied here, but the bottom line is that nothing should be taken for granted. At times, the market tests everything that has been learned over a lifetime of investing.

FIGURE 6.2 Money Market Strategy Satisfies a Goal of Stable Principal

A money market or cash strategy could be implemented in a mutual fund or a separate account. Either way, the focus is (in this order): preservation of capital, liquidity, and yield. There are benefits to each vehicle. I will outline the benefits within the separate account section later in this chapter.

The second example is a step to the more aggressive side. A better way to describe it may be a step away from the most conservative side. The portfolio has the ability to be constructed with debt issued by the U.S. government. The greater the percentage of Treasury securities, the more comfort you may gain in that portfolio strategy. Both the Treasury Inflation-Protected Securities (TIPS) and U.S. Treasuries carry the backing of the U.S. government. The agency sector holds a quasi-guarantee from the government. Another way to look at the agency sector with regards to the guarantee is to say that it has implicit guarantee—an implied backstop from the U.S. government. It is important to note that these sectors are just the building blocks. Actual weights can be changed. Through the steps of portfolio construction you, the portfolio manager, will have the ability to make any necessary changes that would provide additional comfort.

If you have trouble coming to terms with the thought of a loss in principal, then you should again go back to basics and invest in the sectors that are closely tied to the government. Investing in a conservative strategy utilizing government sectors helps eliminate many risks. Interest rate risk is a risk that will remain when investing in most fixed income strategies. There are strategies to help mitigate the rise in interest rates, such as implementing a laddered bond strategy. Within construction of that strategy, you will be able to help control the impact of rising rates by investing in securities with shorter-term maturities alongside those across the yield curve. This strategy and others will be discussed in Chapter 11.

Moderate Strategy

Just as an asset manager would work his or her way out on the risk curve within an equity portfolio, the same should happen within the fixed income markets. Higher-beta slices should be increased while reducing the lower-beta sleeves. One way to accomplish this is to reduce your government exposure. As the portfolio increases the overall risk, it makes more sense to diagram the asset class versus goal. Figure 6.3 shows one example of how a portfolio can move out along the risk curve by introducing additional sectors. The introduction of high yield and a core bond fund represented by the Barclays Capital Aggregate index would create a more aggressive strategy. The actual weights will vary depending on risk tolerance and profile.

More Aggressive Strategy

Taking the strategy up another notch in the risk metrics can be accomplished in many ways. Simply changing exposure to the current asset classes will provide opportunity to achieve increased yield and/or return. For example, Figure 6.4 compares the moderate strategy with an aggressive model. It is clear that a more aggressive strategy may be created using the same sectors as the moderate strategy, with greater emphasis on the high yield and less with the TIPS strategy.

FIGURE 6.3 Moderate sector allocation with portfolio goals

We know that these are not the only asset classes in the fixed income market. Keeping it straightforward and clean is important for providing an example, which is why I limited the example to these sectors. Asset-backed securities and mortgage securities are two other asset classes that are usually utilized when investing within the fixed income markets. Both these sectors received a bad reputation and were dragged down through the mud in 2008 and 2009 when both the fixed income and equity markets were imploding. As with any security, there are securities within these asset classes that carry a greater degree of risk than others. If the proper homework is done on all the underlying securities that create the asset-backed security or MBS, you can find securities that offer value. After meticulous attention and analysis, these sectors have the ability to add additional diversification to the portfolio as well as the potential for increased return. These securities are much more difficult to analyze and at times purchase than the typical government or corporate bond. There is a greater number of moving pieces to each bond, which may be affected by a shifting market or a changing economic climate.

FIGURE 6.4 Typical sector allocation compared to a more aggressive allocation

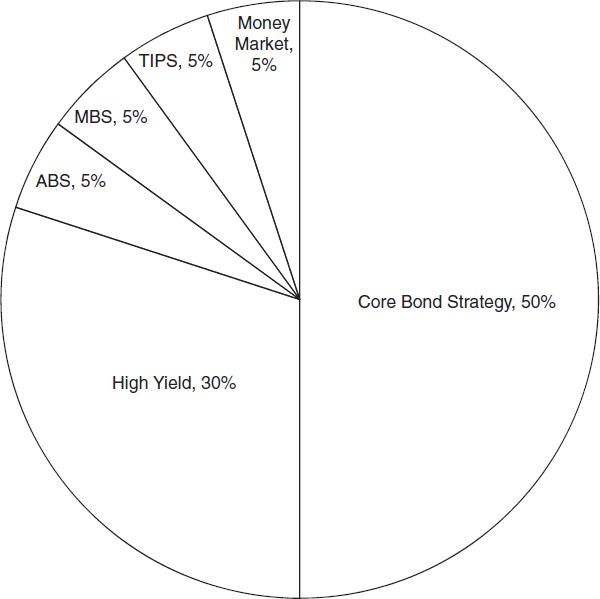

A word of caution: Most core bond strategies have an allocation to these sectors. Because they have an allocation, it is imperative to know the weight if weaving in this strategy with a slice of the specific sector. This is important so that the portfolio isn't unknowingly overexposed to a particular sector. If your target for asset-backed exposure is 5 percent, it is simple enough to go out to the market and add that exposure to your portfolio. However, if the core bond strategy or allocation already has holdings within this sector of 4 percent, in reality your overall exposure is greater than the target weight. Figure 6.5 shows how an aggressive model or strategy snapshot may look.

FIGURE 6.5 Representation of what a more aggressive allocation may look like

The allocation and alignment of strategy is driven from the end client's profile. The strategy is sometimes dictated by other factors; however, whatever the methodology is, it is important to remain disciplined to the strategy that encompasses the necessary goals. It is also worth noting that it is possible to measure risk through various statistical models. There may be a more efficient way to allocate the sectors discussed in Figure 6.4 while achieving a similar expected return. The chosen allocation is to start the discussion and build an efficient risk-adjusted model.

FACTOR 3: PORTFOLIO ANALYSIS

It almost sounds counterintuitive to recommend analyzing a portfolio prior to investing in a new strategy or amending a current strategy. Determining whether it does or doesn't, is the third step to portfolio construction. This is a very crucial step. It is paramount that the portfolio be in alignment with the investor's or investment policy statement's goals. Transitioned portfolios may hold securities that at one time fit the investor's current strategy but are not aligned anymore. Another challenge is that the investment environment is ever-changing and the current environment may not be as favorable for the specific holdings within the portfolio. That is not to say that the same holdings were not in favor at one time.

In a perfect world, a portfolio set for construction would hold only a cash position. Although possible, it is not likely, unless an existing portfolio was liquidated, or perhaps the investor received a windfall of money. I have to admit, anytime I receive a portfolio to manage that is holding a sole cash position, a smile comes to my face. Understandably, in an all-cash transition, there is no need to worry about earmarking which securities to liquidate and which to keep in the portfolio.

The reality is, an investment portfolio usually holds a handful of securities. These are legacy securities and frequently have a story or some history to them. For that reason alone, all factors need to be discussed and flushed out prior to analysis so that the manager knows what he or she truly has to work with. The portfolio may hold a bond that is so far out of the money or in the money that the end investor is not willing to sell because the activity will create additional tax complications. There are also incidents when an investor receives a recommendation from someone of influence or significance and the relationship between the individuals is stronger than the outcome of the security. I am not sure if I would agree with that view, but this information is needed when assessing the portfolio.

When reviewing an existing portfolio there needs to be a similar, if not identical, process that occurs when allocating cash to fund a strategy. A replicable process provides strong and consistent results.

A game plan needs to be utilized when the initial review takes place. Make no mistake that if a process does not exist, one should be created. What I found best and very simple to construct is a document with the pertinent information that is necessary to conduct your analysis, and ultimately a conclusion to either sell or hold an existing portfolio. Notice I didn't say add to a current position. Adding to a position, and there are some exceptions, is at times very difficult to achieve. Supply within the fixed income world is quite different from the world of equities. It is very easy to add exposure of a particular company within the equity space. You go out to the exchange and purchase the shares you are looking to acquire. That luxury doesn't exist in the fixed income world. This holds true specifically within the municipal sector and credit markets. The reason this occurs is that once debt is issued and taken down by investors, there may not be another chance to purchase that specific bond again unless the issuer reopens the deal. What this means is that it may be very difficult to add to existing positions, and that every portfolio may not look identical to one another.

The piece that I am describing above should contain enough information to provide you with comfort. I have always used a variety of different characteristics for review. I don't feel that there should be a set number required to paint a clear picture. The characteristics should be customized, covering the necessary information needed for your analysis to be effective. Different sectors will carry different categories for analysis. For instance, the mortgage sector will require different areas to analyze than the agency or corporate sector.

I feel the following 10 categories provide the necessary information to start your analysis:

- Issuer name

- CUSIP

- Years to maturity

- Duration

- Agency ratings

- Coupon

- Yield information

- Credit view

- Position weight

- Embedded optionality

These data points were chosen because they paint a picture of the security that leads to a recommendation. The basics, such as duration and yields, are noted, as is an opinion on the credit itself. The opinion could be twofold. First, there is a summary from the rating agency on the credit. In addition, and more importantly, there is the view and analysis from the credit team. A credit opinion could resemble the following example, which is for a municipal health care bond:

- The health care sector may come under additional pressure due to proposed legislation.

- There is increased volatility within the issuer as there are signs of softening within funding.

- There is exposure to a significant amount of derivatives.

- Balance sheet is highly levered.

These are just some examples of characteristics that would help shape the view of a particular credit. The third bullet would stand out in particular with me. Because this is a municipal issuer, a health care or hospital bond, I get worried when there is a significant amount of derivative exposure. That is a definite red flag. I would not want to own debt, municipal or taxable, that has any type of indirect exposure within their business that wasn't part of the core business model or the normal course of business. That model is just asking for trouble. Following the summary of data points, a recommendation is made whether to hold or sell the security. Everything discussed thus far is looked at from a fundamental approach. When debt is reviewed, it normally has a binary outcome—you either like it or you don't. At times, there are grey areas that complicate matters. It shouldn't be a surprise that complications come with the territory.

There are other factors that influence the decision to hold or to sell existing debt. From a fundamental perspective, if the credit opinion is negative, the decision is easy and straightforward: sell the debt. It is common that debt in an existing portfolio does not fit the new investment strategy. If anything is straightforward, this concept is. All bonds that are to be held in the portfolio must fit the new investment strategy and guidelines. Strategy guidelines that state all bonds must have a final stated maturity no longer than ten years are easy to understand. Any bond that has a final stated maturity longer than ten years should automatically be rejected. A bond holding a final stated maturity of twenty years should never make it into the portfolio. The same would hold true for a bond that doesn't meet other criteria such as credit quality.

Diversification needs to be assessed as well at this point. If you have listened to me present on this topic or spoken to me directly this example should resonate with you. It is difficult to begin to try to quantify how many times poor diversification occurs. It happens time and time again, and once you think the environment has changed, it becomes clear that it really hasn't changed at all. That is the search for yield. I am not referring to the search for yield through the typical diversification within a strategy. What I am about to describe is looking at an offering sheet, sorting it from highest yield to lowest, and picking the top ten bonds. These bonds are picked on what seems to be only yield, neglecting fundamentals or other characteristics.

Once again, I will refer to the fall of 2008. It was very common to see accounts with minimal holdings and a very highly concentrated sector. The most outrageous example that came across my desk was a portfolio with only six holdings, all within the financial sector. To make matters worse, those six holdings all in the financial sector comprised just a few names, specifically the four large investment banks that, unfortunately, were in the daily headlines. The noise around these banks set the backdrop and the landscape for higher yields. It seems that these yields are what drove the investment decision. Whoever constructed this portfolio was seeking out yield and only yield. The risk-reward trade off was overlooked. As the market imploded, the common scenario unfolded. The portfolio value decreased rapidly because it was not well diversified across many measures.

Reduction of Credit Risk

If you are looking for consistent long-term results, once again, there needs to be a focus around a disciplined investment approach. Through this approach risk will be mitigated. Diversification is a key contributor within the process to reduce risk. The essentials within portfolio construction focus around a credit review approach that provides the groundwork for proper diversification. When success is found through diversification, you will realize a sense of control. In a nutshell, diversification is looked at by some at the security level. That is an accurate assessment, although lacking. Diversification should be taken a few steps further. A solid philosophy for diversification and portfolio construction encompasses not only credit-specific, but sector and regional analysis driving diversification. Diversification should encompass multiple levels and can be accomplished through five categories:

- Product diversification

- Issuer diversification

- Sector diversification

- Geographic diversification

- Quality diversification

This approach thoroughly covers multiple fronts on diversification. This multilayer approach will help provide success within the portfolio toward the generation of consistent results. Relate this view back to the example of the investment banks that were held in a portfolio. All five of the diversification measures were not met. All securities were fixed-rate corporate notes; therefore, product diversification was not met. The fact that there were only six bonds and all were financial institutions from the U.S. negates issuer, sector, and geographic diversification rules. Finally, the quality measure may be interpreted different ways. I look at both the actual rating of the security and where it stands within the capital structure. Depending on the timing, this measure may have been adhered to at the time of purchase. There is the possibility that it was not, particularly if the positions were acquired in or around the time of the financial crisis when the entire sector was under attack from rating agencies with downgrades.

Outlined next is a representation of diversification and limits. The first section represents the taxable market, followed by an example from the municipal sector.

These position limits may be viewed either as soft limits or hard and fast rules. I subscribe to the notion of implementing them as a soft rule, with a hard rule slightly above. What I mean is that a 3 percent single-A limit is a soft rule; however, if due to market value swings or cash flows, the position creeps up to 4 percent, the hard rule would be to reduce the position by at least 1 percent. The move higher would trigger action, which may be to pare back exposure or, depending on the circumstances, hold firm.

Securities represented within the corporate sector should have a rating from at least one nationally recognized rating agency, if not two. This is driven by the internal credit review process. If the credit process is strong, one rating may be sufficient. The individual security limits should be thought of and structured in a tiered fashion. For instance, a triple-A security, the highest possible credit rating, would have a 7 percent allowable maximum limit. This weight is established at the time of purchase. The limit needs to be calculated at the issuer level. That is, the individual issues must be rolled up to the parent company. A company's finance arm needs to be looked at just as the parent is, as well any commercial paper that is issued by the company. It doesn't stop with commercial paper. Any security that is backed or supported by the parent needs to be counted as well.

As you work your way down the credit curve, the weight of each position is reduced. An example would be for double-A to have an allowable 3 to 5 percent weight; single-A, 1 to 2 percent; and triple-B, 0.5 to 1 percent.

Government Securities

A similar concept should be utilized when allocating government securities. It is slightly different, because these securities are associated with the government and have the backstop and pockets of the same entity. Individual U.S. Treasury securities have no limit at the security level. Best judgment should be used to avoid curve risk through too much exposure in one issue and point on the curve. Explicit government guaranteed corporate debt may have a 10 percent allowable limit. If you remember, this is the debt that was issued back in 2008 and 2009 when the market was imploding and liquidity was scarce. In some cases, corporate issuers would not have been able to issue debt and receive funding without the help of the U.S. government. Since the downturn, corporate issuance with government backing has been nonexistent. This is to be expected moving forward, unless there is another global disruption where the government needs to step in. Hopefully the likelihood of that occurring is minimal.

Agency securities that carry the implicit guarantee by the government could be held to 5 to 10 percent per issue unless otherwise stated in the investment policy statement or portfolio guideline.

When it comes to setting limits for sub debt, the equation becomes a little more difficult. Some individuals group the sub debt in under the agency guidelines. I feel more comfortable adhering to the credit guidelines. One reason for the disparity is because sub debt does not have the same type of liquidity as senior debt. Also, if push comes to shove, there is the possibility that the government may decide to lift the implicit guarantee from the sub debt while continuing to support the senior debt. If this were to happen, the market would not look favorably on this activity.

Similar criteria and actions should be upheld within the municipal market as well. Again, these position limits may be viewed as soft limits or hard rule. The municipal sector is inherently less liquid. As a result, careful consideration needs to be taken when assessing any actions that may occur due to a downgrade. Due to the nature of the sector, specifically within a separate account structure, I would hold true to the percentage owned at the time of purchase.

There are two different times these percentages could be calculated for qualification. I find that the when implementing diversification requirements, they act as a reflection and help paint an accurate picture when they are calculated at the time of purchase. Some professionals may use the weight at the time of purchase, converting this methodology to market value subsequent to the purchase. The combination of the two, including a tiered approach as described earlier, works the best. If the diversification limits are breached, this does not mean that an automatic sell is required. If the percentage increases due to cash flows, it should be at the discretion of the management team to decide whether to reduce the position or continue to hold. Cash flows are sometimes replenished quickly, resulting automatically in the reduction of the percentage owned. Each portfolio is likely different and only the history of the account will provide guidance. Usually, flows within a mutual fund are replenished at a quicker pace than in a separate account, because there are multiple investors within the product rather than a single investor in a separate account.

Once a security is purchased, what is the process to follow if a downgrade happens? It is unrealistic to think that a downgrade will not happen. In recent years, with the volatile environment we have lived and invested through, downgrades seem to occur more frequently and with greater magnitude. The simple one-notch downgrade at times seems like a thing of the past. Two- and three-notch downgrades, and sometimes even more, feel as if they occur on a more frequent basis than ever before.

In the event of a downgrade, a formal review from the credit analyst covering the issuer and portfolio manager should commence. The analysis should start within 24 to 48 hours, with a formal decision and documentation within a reasonable time frame. A logical time frame may be determined by current market conditions and the degree of the downgrade. The findings should determine if any action needs to be taken due to change in the outright credit quality or specific portfolio guidelines.

The idea is that by adhering to the aforementioned weights prior to any purchases and frequently monitoring positions, the portfolio will automatically maintain a balance and remain well diversified. The positions should be reviewed daily by the portfolio manager, and formally at a weekly investment policy committee meeting. These two actions will help reduce volatility and mitigate overall risk.

The recipe for a solidly constructed portfolio is to efficiently and successfully piece together securities that hold characteristics that are allowable within the portfolio's guidelines. These credits need to be filtered minding the five levels of diversification. Once filtered, they next need to be most advantageously utilized in a way that constructs a solid portfolio. The strength of the portfolio will help mitigate risk while providing the necessary characteristics to effectively reach all stipulated goals.

Risks to Consider

Throughout the course of investing, you will no doubt encounter different interest rate environments. No matter what the environment is, the current rate environment should help shape the portfolio you are constructing.

Interest Rate Environment Interest rates are always shifting, many times driven by investor demand and the economic landscape. The rise and fall of interest rates doesn't necessarily stop there. Many times an exogenous event occurs, changing investor sentiment and possibly long-term outlooks, which will impact the environment. The yield curve can shift and twist in parallel fashion either up or down, or flatten or steepen. Whichever path is taken, the effects on a portfolio may be drastically different. As explained earlier, this is why, within the construction phase, the current and expectation for future interest rates must be taken into consideration.

I am not going to spend a lot of time describing a falling interest rate environment. As interest rates fall, prices rise, usually benefiting the portfolio. A rising interest rate environment, normally associated with a bear market, is much more challenging to navigate through.

A rising rate environment has the ability to play havoc with a fixed income portfolio. There are ways to combat this move. Let's be real here for a moment. If interest rates rise, almost any fixed income portfolio will be negatively impacted in some way. By introducing different asset classes, the manager has the ability to mitigate the risks.

Floating Rate Notes Adding floating rate note securities is one way to tie the portfolio to different indexes that move with interest rates. Floaters are issued in a variety of asset classes from corporate securities to agency debt. The U.S. Treasury is even considering the possible launch of a floating rate Treasury note. The addition of a floating rate note will benefit the portfolio predominantly in an environment where short-term rates are moving higher. If the yield curve steepens where the long end moves higher with little to no effect on the front end, floating rate notes may still outperform longer-dated bonds; however, the coupons tied to these notes will not be adjusted.

My belief is that a separate account is the optimal vehicle to use in a bear market or rising interest rate environment. There are different opinions around this topic with some probably strongly disagreeing with my view. There are benefits as well as drawbacks to a separate account. In the end, the deciding factor will be driven by the investment goals.

A mutual fund is the common alternative to a separate account. The primary difference between a separate account and a mutual fund is the number of investors within each vehicle. A separate account is unique to the owner of the account. This singular ownership provides different benefits to the investor, institutional or otherwise. What that means is that the investor has full transparency into the account. They are able to see each individual holding. These holdings that are used to complete the strategy are also customized to the investor's goals. Due to the nature of the account, if the investor's goals change over time, it is fairly simple to adjust or realign the objective of the strategy to their goals. This is the customization feature that coincides with a separate account. Lastly, your assets are yours and are only affected by the actions you take. The securities you are invested in are not subject to other investor's activity. For example, if a group of investors are becoming jittery and start to redeem their shares from the mutual fund, there is a chance that the fund managers may need to liquidate or raise cash at unopportunistic times. That type of activity may negatively affect the fund, as the net asset value (NAV) may drop, lowering the value of your holding. In a separate account, the only assets that are held are your assets. If you want to liquidate you may, but more importantly, if you want to hold firm to your positions and ride out the volatility, that is your choice and is easily accomplished.

In addition to a rising rate environment, there are other risks that need to be considered in fixed income portfolio construction:

- Lack of liquidity or a frozen market

- An inflationary environment

- Credit risk

A market characterized by little liquidity, or even frozen, is a nightmare for managers to navigate. It has happened time and time again, particularly when a crisis—or what is perceived to be a crisis—materializes. It is possible to track back to almost any major correction and watch how quickly liquidity evaporates from the system. The occurrence could be driven by instances at a macro level or caused by a systemic event, but there are also times when an event is centered on just one security or a particular sector—more of an idiosyncratic risk. Impact on one security, if that was to happen, may initially be minimal at the portfolio level. If the occurrences grow and the ripple effect takes hold, it might become more problematic.

Think about what happens if the singular event starts to snowball. The snowball effect moves from the initial company to others in the sector. What if there is fear that those names in the sector will negatively impact other names in a completely different sector? There are a lot of what-ifs involved in this example. Unfortunately, that is the way these situations develop and need to be looked at. A single instance can easily develop into a larger problem that will affect the liquidity of the portfolio. The absence of liquidity will drive prices lower, if you are lucky enough to receive a price at all.

Inflation Inflation is damaging to a fixed income portfolio, just as it is to the consumer. Inflation erodes the dollar and the markets. If your dollar is worth less tomorrow than it is today, you will be unhappy. The same concept applies to fixed income securities. The value of a bond held today does not hold the same value tomorrow if inflation is running higher. If the inflation rate is moving higher, interest rates are going to follow the same path. As interest rates move up, bond prices move down, and your portfolio becomes worth less. A different way to look at this is that a bond with a 2 percent coupon is not going to be as attractive to someone if inflation is present; the 2 percent coupon you are receiving is not going to have the same purchasing power now as it did when inflation was nonexistent. The investor is now going to demand a higher coupon and yield if inflation is picking up and eroding his investment.

Credit Risk Credit risk is probably one of the most straightforward risks the bond market faces. Although it is straightforward at times, it may be masked by other elements within the market. Investors grasping for hope and speculation are sometimes the biggest culprits behind present or hidden credit risk. Credit risks may materialize from either fundamental or event-driven characteristics. Fundamental risk, I believe, is easier to uncover than technical risk. Balance sheet analysis together with earnings calls usually provides enough information to develop a solid view and opinion. As with anything, the goal is to spot an early-developing trend. In a perfect world, the trend would be uncovered in its infancy stage so you have ample time to take action if needed. For example, take the pharmaceutical sector. If a company's pipeline is slowing and a prominent drug is coming off patent (meaning generics will be developed and soon be competing) there is a pretty good chance that earnings may start to slow or at least show signs of slowing. The slowdown in earnings may drive the company to start or increase the burn rate of its available cash, applying more toward research and development or even a possible acquisition with the hopes of building a new pipeline through acquisition.

In some instances, activity happens at a rapid pace, too fast for fundamentals to provide a downward or even a sideways trend. Unfortunately, there is a lag between an event and the materialization of facts laying the groundwork for the fundamentals to develop. Too common an example is when a company has an accident that will immediately impact its earnings and ultimately its cash on hand. Oil spills or automotive recalls certainly fall into this category. Instantaneously when the headline is reported over the tape or news wire, the company's outstanding debt begins to be repriced. There is usually an initial gap lower while investors analyze the headlines and use their best judgment to calculate what price they feel the bond should trade at. A different approach to get to the same answer is to attempt to calculate what price the company is worth after the accident. Assumptions will need to be made on different outcomes. Always remember to include the high-probability and low-probability events. It doesn't hurt to prepare for the worst-case scenario, even if it the odds of it materializing are very low. Because additional credit risk is created from an unfortunate event, it may at times seem very difficult or nearly impossible to accurately calculate and make a decision as the data are just being reported. You are not cutting diamonds; you just need to be in the ballpark.

As with anything, there are varying degrees of risk depending on the security. Risk takes on many shapes and varieties, and when constructing a portfolio they all need to be calculated. Daily investors wrestle with minimal risk that usually only impacts the price of the security and should be viewed as temporary. From time to time, events arise that create substantial risk to a company, bringing into question the company's ability to remain a going concern. In the end, whether you are uncovering minimal risk or substantial risk, what it really comes down to is that one question: Is the company solvent or not?

BOTTOM LINE

In an environment that poses multiple challenges, fixed income investing needs to be examined differently than in previous years. Asset managers are not only responsible for generating alpha; they must also take an active approach to bring risks down. These two goals do go hand in hand, though the reduction of risk is at times overlooked.

In an environment that is conducive to investing, there is never much question about risk or positioning. When the markets are good, everyone is usually happy and questions are kept to a minimum. Unfortunately, this can change on a dime. Risk and positioning are two concepts that always rear their ugly heads when markets are stressed. Think about how many more questions arise or the number of times a portfolio is analyzed when the markets are moving lower. A global disruption or a disruption that materializes on local soil creates a similar effect. At any point when either of these circumstance or others similar in nature arise, the first thought that should cross your mind is to reduce risk. When these circumstances materialize, the rule of thumb is to reduce the size of your bets. As you reduce the bets, the overall risk to a fixed income portfolio should naturally decline.

Make no mistake—outpacing markets is difficult to do on a consistent basis. The low interest rate environment that has impacted everyone has created an even more difficult environment to construct a portfolio. New headaches were created as financial institutions needed additional capital to survive. Unfortunately, there is not a quick cure on the horizon. Investors need to prepare themselves and their portfolios to accommodate the new environment. The bottom line is that you need to construct a strategy to fit your needs and weather the events that the market and economy may throw your way.