Chapter 19

COST-VOLUME-PROFIT ANALYSIS: ADDITIONAL ISSUES

After studying this chapter, you should be able to:

1. Describe the essential features of a cost-volume-profit income statement.

2. Apply basic CVP concepts.

3. Explain the term sales mix and its effects on break-even sales.

4. Determine sales mix when a company has limited resources.

5. Understand how operating leverage affects profitability.

*6. Explain the difference between absorption costing and variable costing.

*7. Discuss net income effects under absorption costing versus variable costing.

*8. Discuss the merits of absorption versus variable costing for management decision making.

*Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

PREVIEW OF CHAPTER 19

The relationship between a company's fixed and variable costs can have a huge impact on its profitability. In particular, the trend toward cost structures dominated by fixed costs has significantly increased the volatility of many companies' net income. The purpose of this chapter is to demonstrate additional uses of cost-volume-profit analysis in making sound business decisions. The content and organization of this chapter are as follows:

Cost-Volume-Profit Income Statement

1. (L.O. 1) The Cost-Volume-Profit (CVP) income statement classifies costs as variable or fixed and computes a contribution margin. Contribution margin is the amount of revenue remaining after deducting variable costs. It is often stated both as a total amount and on a per unit basis.

Basic Computations

2. (L.O. 2) Desossa Music Players' CVP income statement shows that total contribution margin (sales minus variable expenses) is $175,000, and the company's contribution margin per unit is $50. The contribution margin ratio (contribution margin divided by sales) is 41.67% ($50 ÷ $120). Desossas' break-even point in units (using contribution margin per unit) or in dollars (using contribution margin ratio) are calculated as follows:

3. Assuming Desossa's management has a target net income of $100,000, the required sales in units and dollars to achieve its target net income are calculated as follows:

4. Desossas' margin of safety in dollars or as a ratio are calculated as follows:

CVP and Changes in the Business Environment

5. To better understand how CVP analysis works, let's assume that shipping costs have increased significantly causing the unit variable cost to increase by 10%, what effect will this have on Desossas' break-even point?

Answer: A 10% increase in variable costs increases the per unit variable cost to $77 [$70 + ($70 × 10%)]. The new contribution margin per unit is therefore $43 ($120 − $77). Thus the new break even point in units is calculated as follows:

![]()

Sales Mix

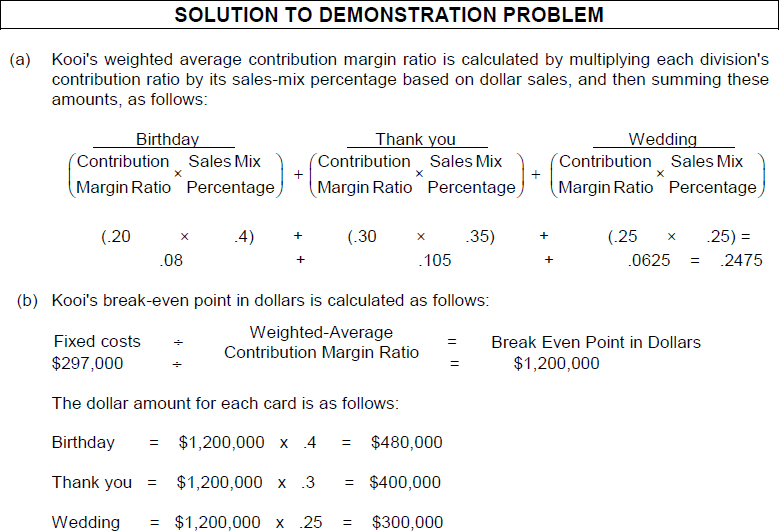

6. (L.O. 3) Sales mix is the relative percentage in which a company sells its multiple products. For example, if 60% of product A is sold for every 40% of product B, the sales mix of the product is 60% to 40%.

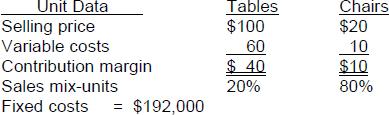

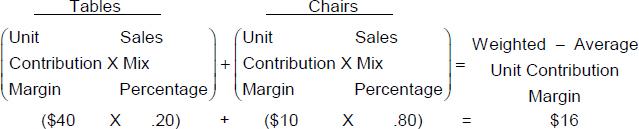

7. Break-even sales can be computed for a mix of two or more products by determining the weighted average unit contribution margin of all the products. Assume that Seth Inc. sells tables and chairs in a ratio of four chairs for every one table. The sales mix in percentages is 20% (1/5) for tables and 80% (4/5) for chairs. The following is the per unit data for Seth Inc.:

To compute break-even for Seth Inc., we use the weighted average contribution margin as follows:

To break even, Seth must sell 2,400 (12,000 × 20%) tables and 9,600 (12,000 × 80%) chairs.

8. At any level of units sold, net income will be greater if more high contribution margin units are sold than low contribution margin units. An analysis of these relationships generally shows that a shift from low-margin sales to high margin sales may increase net income, even though there is a decline in total units sold.

9. The formula for computing the break-even point in dollars is fixed costs divided by the weighted-average contribution margin ratio. To compute a company's weighted-average contribution ratio, multiply each division's contribution margin ratio by its percentage of total sales and then sum these amounts.

Seth Inc's contribution margin ratio for sales of tables is .40 ($40/$100) and for chairs is .50 ($10/$20). The weighted-average contribution margin ratio is calculated as follows:

The break-even point in dollars is calculated as follows:

Sales Mix with Limited Resources

10. (L.O. 4) When a company has limited resources (e.g., floor space, raw materials, direct labor hours), management must decide which products to make and sell in order to maximize net income. Assume that Seth Inc. has limited machine capacity which is 2,600 hours per month. Relevant data consist of the following:

The contribution margin per unit of limited resource is calculated as follows:

If Seth Inc. increases machine capacity hours by 400 hours per month, it would be better to use the hours to produce more chairs.

Cost Structure and Operating Leverage

11. (L.O. 5) Cost structure refers to the relative proportion of fixed versus variable costs that a company incurs. In most cases, increased reliance on fixed costs increases a company's risk. When sales are increasing, profits can increase at a high rate, but when sales decline, losses can also increase at a high rate. Companies can change their cost structure by using more sophisticated robotic equipment and reducing it later, or vice versa. The equipment would increase the fixed costs whereas labor increases variable costs.

Variable Costing vs. Absorption Costing

*12. (L.O. 6) There are two approaches to product costing.

a. Under full or absorption costing all manufacturing costs are charged to the product. This is also the approach required under generally accepted accounting principles.

b. Under variable costing only direct materials, direct labor, and variable manufacturing overhead costs are treated as product costs; fixed manufacturing overhead costs are recognized as period costs (expenses) when incurred.

*13. The primary difference between variable and absorption costing is that under variable costing the fixed manufacturing overhead is charged as an expense in the current period. The result is that absorption costing will show a higher net income number than variable costing whenever units produced exceed units sold. The reason: the cost of the ending inventory is higher under absorption costing than under variable costing.

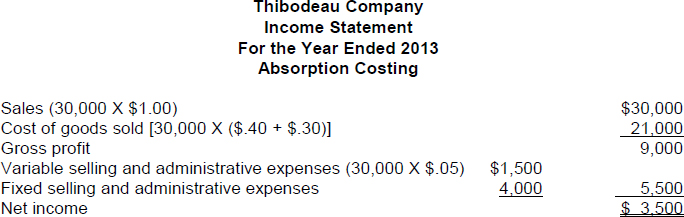

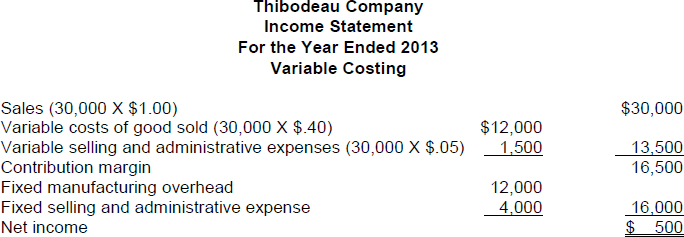

*14. Assume Thibodeau Company manufactures candy bars and has the following information:

The absorption costing income statement and variable costing income statement are shown below:

*15. (L.O. 7) The effects of the alternative costing methods on income from operations are:

| Circumstance | Effects on Income From Operations |

| Units produced exceed units sold | Income under absorption costing is higher than under variable costing |

| Units produced are less than units sold | Income under absorption costing is lower than under variable costing |

| Units produced equal units sold | Income will be equal under both approaches |

*16. (L.O. 8) One of the problems with absorption costing is that management may be tempted to overproduce in a given period in order to increase net income. Therefore, to avoid this overproduction, variable costing is often used internally to evaluate management decisionmaking.

*17. The following are potential advantages of variable costing:

a. Net income computed under variable costing is unaffected by changes in production levels.

b. The use of variable costing is consistent with cost-volume-profit and incremental analysis.

c. Net income computed under variable costing is closely tied to changes in sales levels giving a more realistic assessment of a company's success or failure.

d. The presentation of fixed and variable cost components on the face of the variable costing income statement makes it easier to identify these costs and understand their effect on the business.

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

Circle the letter that best answers each of the following statements.

- (L.O. 1) Carlson Inc. manufactures baby cribs and currently has fixed costs of $50,000 and a sales price per unit of $315. Carlson's major raw materials supplier announced it will be increasing its prices, therefore Carlson is expecting the variable costs of its baby cribs to increase from $90 to $115. Carlson is going to hold the line on the selling price of its cribs but plans to cut fixed costs by $5,000. If Carlson currently has monthly net income of $40,000 on sales of 400 cribs, what increase in units sold will Carlson need to maintain the same level of income?

- 10

- 15

- 25

- 35

- (L.O. 3) Break-even sales can be computed for a mix of two or more products by determining the:

- sales revenue of the two products divided by the number of products sold.

- weighted average unit contribution margin of all the products.

- cost of goods sold less the variable costs.

- weighted average unit gross profit margin of all the products.

The following information pertains to questions 3 and 4.

Jennifer Company sells both chairs and tables at the following per unit data:

3. (L.O. 3) Assuming $210,000 fixed costs, how many tables and chairs should Jennifer Company sell to break even?

4. (L.O. 3) Assuming $118,580 fixed costs, what is the total revenues in chairs Jennifer Company needs to break even?

a. $154,800

b. $169,400

c. $175,200

d. $188,600

The following information pertains to questions 5 and 6.

Sheltie Company sells both lamps and clocks at the following per unit data:

5. (L.O. 3) Assuming $312,000 fixed costs, how many lamps and clocks should Sheltie Company sell to break even?

6. (L.O. 3) Assuming $149,952 fixed costs, what is the total revenues in lamps Sheltie Company needs to break even?

a. $289,800

b. $333,720

c. $351,450

d. $377,600

7. (L.O. 3) At any level of units sold, net income will be greater if:

a. more low contribution margin units are sold than high contribution margin units.

b. more high contribution margin units are sold than low contribution margin units.

c. fixed costs equal the dollar amount of sales.

d. variable costs equal fixed costs.

8. (L.O. 4) The contribution margin per unit of limited resource is calculated as:

a. Limited resource per unit to produce ÷ Contribution margin per unit

b. Limited resource per unit to produce ÷ Sales price per unit

c. Contribution margin per unit ÷ Limited resource per unit to produce

d. Sales price per unit ÷ Limited resource per unit to produce

9. (L.O. 4) Handy Andy Company has limited direct labor hours of 4,000 hours per month for its employees. Handy Andy manufactures a standard entertainment center and a deluxe entertainment center. The standard and deluxe units have the following information:

The contribution margin per unit of limited resource is:

10. (L.O. 5) Operating leverage refers to:

a. the operating expense in comparison to advertising expenses.

b. the change that a company experiences in net income when there is a change in its production levels.

c. the change that a company experiences in net income when there is a change in its variable costs.

d. the change that a company experiences in net income when there is a change in its sales revenue.

11. (L.O. 5) Because of operating leverage, the more a company relies on fixed costs,

a. the greater a company's risk.

b. the less a company's risk.

c. the less net profit it will experience when sales increase.

d. the less net loss it will experience when sales decrease.

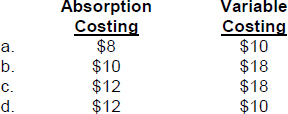

*12. (L.O. 6) Klotz Co. manufactures a dog shampoo called Cleanfur. Relevant data for Cleanfur in January 2013, the first month of production, are as follows:

| Selling price | $26 per unit |

| Units | Produced 20,000; sold 15,000; beginning inventory zero |

| Variable manufacturing unit costs | $10 |

| Fixed costs | Manufacturing overhead $140,000 Selling and administrative expenses $30,000 |

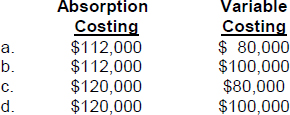

The per unit costs under both absorption and variable costing are:

*13. (L.O. 6) Ebbinghaus Company produces basketballs. In 2013, 100,000 units are produced and 80,000 units sold. Variable costs per unit are $10 and fixed manufacturing costs are $200,000. The per unit cost for both absorption and variable costing are as follows:

*14. (L.O. 6) In the Klein Company, 50,000 units are produced and 40,000 units are sold. Variable manufacturing costs per unit are $8 and fixed manufacturing costs are $160,000. The cost of the ending finished goods inventory under each costing approach is:

*15. (L.O. 7) When units produced are less than units sold, income under absorption costing will be:

a. higher than under variable costing.

b. the same as under variable costing.

c. lower than under variable costing.

d. indeterminate compared to variable costing.

*16. (L.O. 7) When units produced and sold are the same, income under variable costing will be:

a. higher than under absorption costing.

b. the same as under absorption costing.

c. lower than under absorption costing.

d. indeterminate compared to absorption costing.

*17. (L.O. 7) In the Heenemen Company, sales are $800,000, cost of goods under absorption costing is $600,000 and total operating expenses are $120,000. If cost of goods sold is 70% variable and total operating expenses are 60% fixed, what is the contribution margin under variable costing?

a. $380,000.

b. $332,000.

c. $308,000.

d. $260,000.

*18. (L.O. 8) Variable costing is:

a. not compatible with responsibility accounting.

b. acceptable under generally accepted accounting principles.

c. acceptable for income tax purposes.

d. only acceptable for internal use by management.

*19. (L.O. 8) One of the problems with absorption costing is that management may be tempted to increase income by:

a overproducing.

b. decreasing inventories.

c. underproducing.

d. falsifying the records.

*20. (L.O. 8) Which of the following is not considered an advantage of variable costing?

a. Net income computed under variable costing is unaffected by changes in production levels.

b. It is allowed under generally accepted accounting principles.

c. The use of variable costing is consistent with cost-volume-profit and incremental analysis.

d. The presentation of fixed and variable cost components on the face of the variable costing income statement makes it easier to identify these costs and understand their effect on the business.

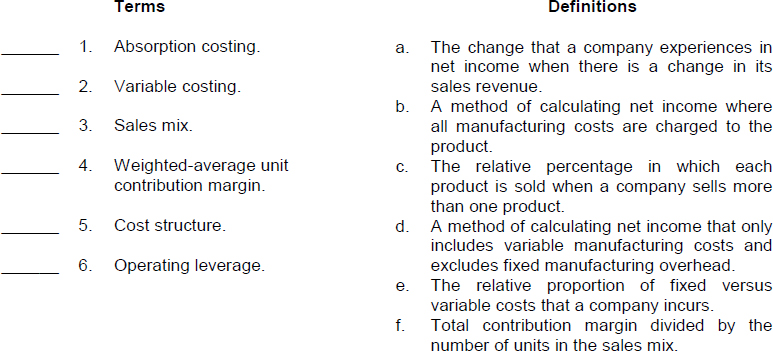

Match each term with its definition by writing the appropriate letter in the space provided.

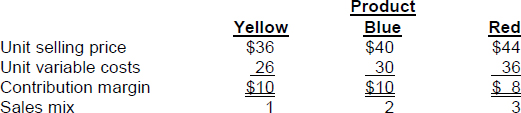

EX. 19-1 (L.O. 3) Smuthers Company manufactures and sells three products. Selling price and variable cost data for the models are as follows:

Instructions

(a) Compute the break-even point in units, assuming the total fixed costs are $320,004.

(b) Prove the correctness of your answer.

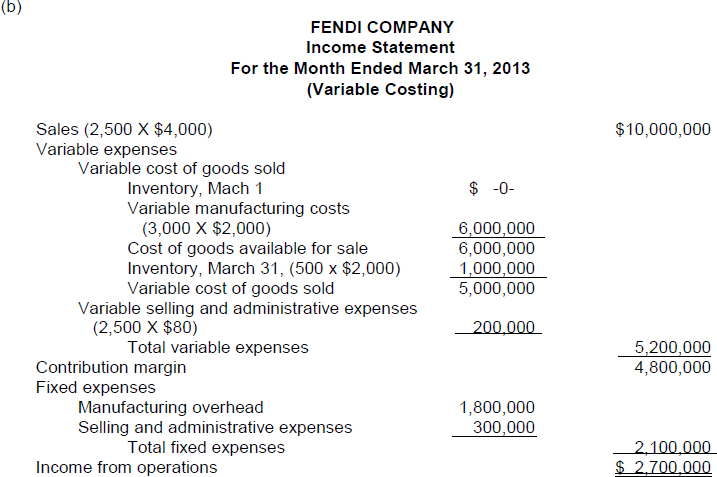

EX. 19-2 (L.O. 6 and 7) During March of 2013 Fendi Company produced 3,000 units but only sold 2,500 units. The company had no beginning inventory. The unit selling price was $4,000. Manufacturing costs were: variable $2,000 per unit produced and fixed $1,800,000. Selling and administrative expenses were: variable $80 per unit of sales and fixed $300,000.

Instructions

(a) Compute the manufacturing cost of one unit of product using (1) absorption costing and (2) variable costing.

(b) Prepare an income statement for March using the variable costing approach.

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (F) | Contribution margin is the amount of revenue remaining after deducting variable costs. |

| 2. (T) | |

| 3. (T) | |

| 4. (T) | |

| 5. (T) | |

| 6. (F) | At any level of units sold, net income will be greater if more high contribution margin units are sold than low contribution margin units. |

| 7. (F) | The formula for computing the break-even point in dollars is fixed costs divided by the weighted-average contribution margin ratio. |

| 8. (T) | |

| 9. (F) | The contribution margin per unit of limited resource is calculated by dividing the contribution margin per unit of each product by the number of units of the limited resource required for each product. |

| 10. (F) | Cost structure refers to the relative proportion of fixed versus variable costs that a company incurs. |

| 11. (T) | |

| 12. (F) | A cost structure that relies on higher fixed costs has more risk and can be good when revenues are increasing, but can be bad when revenues are decreasing. |

| *13. (F) | The approaches only differ concerning fixed manufacturing overhead costs which are treated as a product cost under absorption costing and treated as a period cost under variable costing. |

| *14. (T) | |

| *15. (F) | In this circumstance, income is higher under absorption costing than under variable costing. |

| *16. (T) | |

| *17. (T) | |

| *18. (F) | One of the problems with absorption costing is that managers may have greater incentive to overproduce inventories. |

| *19. (T) | |

| *20. (F) | A disadvantage of variable costing is that it is not allowed under generally accepted accounting principles. |

- b

- d

- c

- f

- e

- a

EXERCISES

EX. 19-1

(a) The total contribution margin for the sales mix is:

[($10 × 1) + ($10 × 2) + ($8 × 3)] = $54

The weighted average unit contribution margin is:

$54/6 units = $9.00

The computation of break-even sales in units assuming $320,004 of fixed costs is as follows:

$320,004 ÷ $9.00 = 35,556 units

In order to break even with a sales mix of 1:2:3, Smuthers must sell 5,926 yellow units (1/6 × 35,556), 11,852 blue units (2/6 × 35,556), and 17,778 red units (3/6 × 35,556).

(b) The proof for (a) is as follows: