Appendix J

PRICING

After studying this chapter, you should be able to:

1. Compute a target cost when the market determines a product price.

2. Compute a target selling price using cost-plus pricing.

3. Use time and material pricing to determine the cost of services provided.

4. Determine a transfer price using the negotiated, cost-based, and market-based approaches.

5. Explain the issues involved in transferring goods between divisions in different countries.

5. Explain the issues involved in transferring goods between divisions in different countries.

*6. Determine prices using absorption cost pricing and variable-cost pricing.

*Note: All asterisked (*) items relate to material contained in the Appendix to the chapter.

PREVIEW OF APPENDIX J

Few management decisions are more important than setting prices. In this chapter, two types of pricing situations are examined. The first part of the chapter addresses pricing for goods sold to external parties. The second part of the chapter addresses pricing decisions faced when goods are sold to other divisions within the same company. The content and organization of this chapter are as follows:

Pricing Goods for External Sales

- (L.O. 1) Some of the many factors that can affect pricing decisions include:

- Pricing Objectives

- Gain market share

- Achieve a target rate of return

- Environment

- Political reaction to prices

- Patent or copyright protection

- Demand

- Price sensitivity

- Demographics

- Cost Considerations

- Fixed and variable costs

- Short-run or long-run

- Pricing Objectives

- In most cases, a company does not set prices. Instead the price is set by the competitive market (laws of supply and demand). These companies are called price takers and price taking often happens when the product is not easily differentiated from competing products, such as farm products (corn or wheat) or minerals (coal or sand).

- Companies can set prices (1) where the product is specially made for a customer, (2) when there are few or no other producers capable of manufacturing a similar item, or (3) when a company can effectively differentiate its product or service from others.

Pricing in a Competitive Market

4. Once a company has identified its segment of the market, it does market research to determine the target price. The target price is the price that the company believes would place it in the optimal position for its target audience. Once the company has determined the target price, it can determine its target cost by setting a desired profit. The difference between the target price and the desired profit is the target cost of the product. The target cost includes all product and period costs necessary to make and market the product.

Cost-Plus Pricing

(L.O. 2) When the price is set by the company, price is commonly a function of the product or service. Cost-plus pricing involves establishing a cost base and adding to this cost base a markup to determine a target selling price. The size of the markup (the “plus”) depends on the desired operating income return on investment (ROI) for the product line, product, or service. The cost-plus pricing formula is expressed as follows:

Target selling price = Cost + (Markup Percentage × Cost)

6. The cost-plus approach has a major advantage: it is simple to compute. However, the cost model does not give consideration to the demand side—that is, will the customers pay the price. In addition, sales volume plays a large role in determining per unit costs. The lower the sales volume, the higher the price a company must charge to meet its desired ROI (because fixed costs are spread over fewer units and therefore the fixed costs per unit increases).

7. Instead of using both fixed and variable costs to set prices, some companies simply add a markup to their variable costs. Using variable costing as the basis avoids the problem of using poor cost information related to fixed cost per unit computations.

Time and Material Pricing

8. (L.O. 3) Under time and material pricing, the company sets two pricing rates—one for the labor used on a job and another for the material. The labor rate includes direct labor time and other employee costs. The material charge is based on the cost of direct parts and materials used and a material loading charge for related overhead costs.

9. Using time and material pricing involves three steps: (1) calculate the per-hour labor charge, (2) calculate the charge for obtaining and holding materials, and (3) calculate the charges for a particular job.

The per-hour labor charge typically includes the direct labor cost of an employee, selling, administrative, and similar overhead costs, and an allowance for a desired profit of employee time. The charge for materials typically includes the invoice price of any materials used on the job plus a material loading charge. The charges for any particular job are then a result of (1) the labor charge, (2) the direct charge for materials, and (3) the material loading charge.

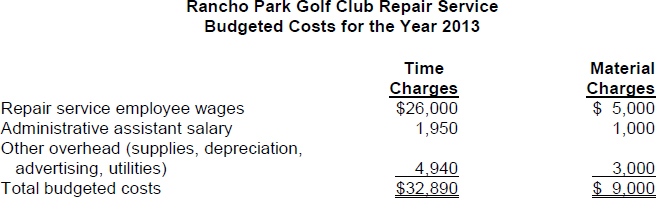

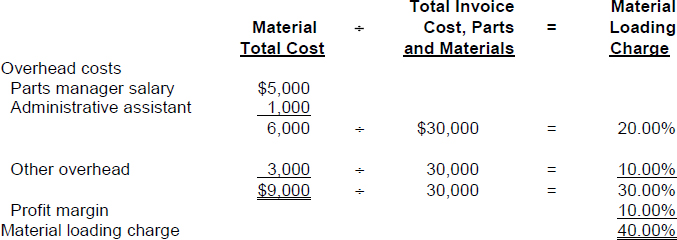

10. To illustrate a time and material pricing situation, assume the following data for Rancho Park Golf Club Repair Service:

Step 1: During 2013 Rancho Park budgets 1,300 of hours for repair time, and it desires a profit margin of $6 per hour of labor. Computation of the hourly charges are as follows:

Step 2: Rancho Park estimates that the total invoice cost of parts and materials used in 2013 will be $30,000 and it desires a 10 percent profit margin markup on the invoice cost of parts and materials. The computation of the material loading charge used by Rancho Park during 2013 is as follows:

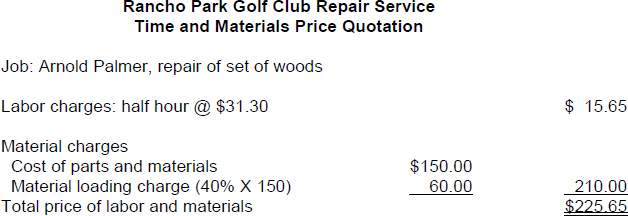

Step 3: Rancho Park prepares a price quotation to estimate the cost to fix a set of woods for a patron. Rancho Park estimates the job will require a half hour of labor and $150 in parts and materials. Rancho Park's price quotation is as follows:

Internal Sales

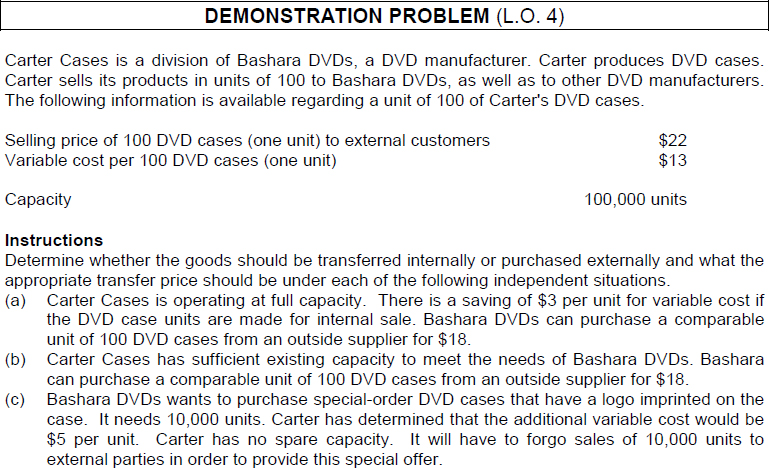

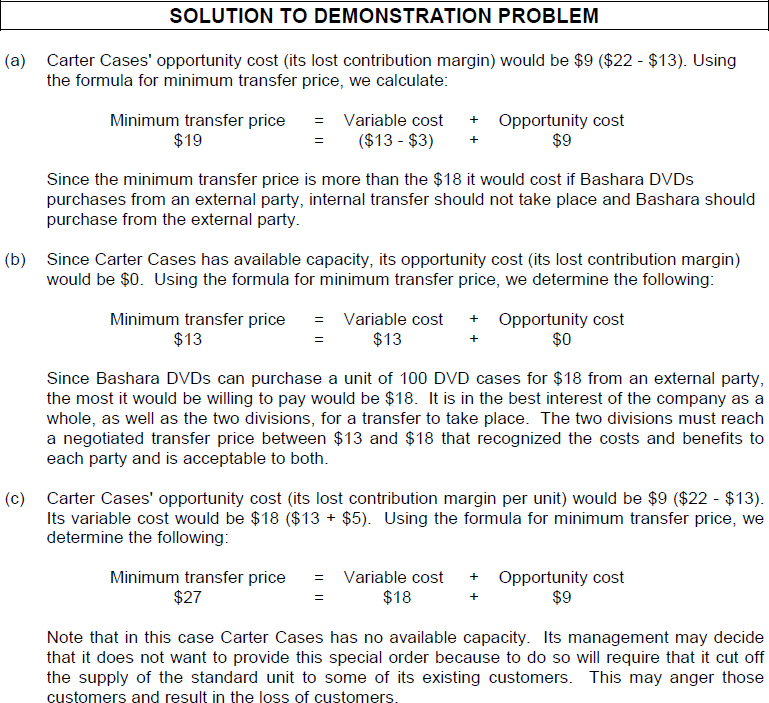

11. (L.O. 4) Divisions within vertically integrated companies normally transfer goods or services to other divisions within the same company, as well as to customers outside the company. When goods are transferred internally, the price used to record the transfer between the two divisions is called the transfer price. Three possible approaches for determining a transfer price are (1) negotiated transfer prices, (2) cost-based transfer prices, and (3) market-based transfer prices.

Negotiated Transfer Prices

12. The negotiated transfer price is determined through agreement of division managers. Using the negotiated transfer pricing approach, a minimum transfer price is established by the selling division, and a maximum transfer price is established by the purchasing division.

Calculating the minimum transfer price depends on whether the selling division has excess capacity or not. If the selling division has no excess capacity, then the minimum transfer price is the variable cost plus its lost contribution margin (also known as opportunity cost). If the selling division has excess capacity, then the minimum transfer price is the variable cost.

Cost-Based Transfer Prices

13. Another method of determining transfer prices is to base the transfer price on the costs incurred by the division providing the goods. If a transfer price is used, the transfer price may be based on variable costs alone, or on variable costs plus fixed costs. A markup may be added to these cost numbers. This method, however, may lead to a loss of profitability for the company and unfair evaluations of division performance.

Market-Based Transfer Prices

14. The market-based transfer price is based on existing market prices of competing goods or services. A market-based system is often considered the best approach because it is objective and generally provides the proper economic incentives. Unfortunately, however, there is often not a well-defined market for the good or service being transferred and thus companies resort to a cost-based system.

Transfers Between Divisions in Different Countries

15. (L.O. 5) As more companies “globalize” their operations, an increasing number of transfers are between divisions that are located in different countries. Companies must pay income tax in the country where income is generated. In order to maximize income, and minimize income tax, many companies prefer to report more income in countries with low tax rates, and less income in countries with high tax rates. This is accomplished by adjusting the transfer prices they use on internal transfers between divisions located in different countries. The division in the low-tax-rate country is allocated more contribution margin, and the division in the high-tax-rate country is allocated less.

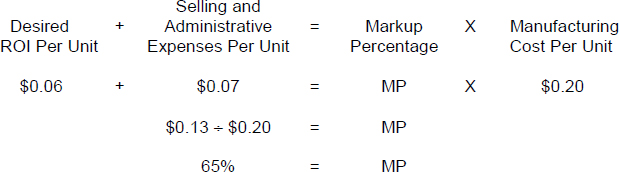

*Absorption Cost Pricing

*16. (L.O. 6) Absorption cost pricing is consistent with generally accepted accounting principles (GAAP) because it defines the cost base as the manufacturing cost. Both variable and fixed selling and administrative costs are excluded from this cost base. Thus, selling and administrative costs plus the target ROI must be provided through the markup.

The steps in using the absorption cost approach are as follows:

- Compute the unit manufacturing cost.

- Compute the markup percentage using the formula:

- Set the target selling price using the formula:

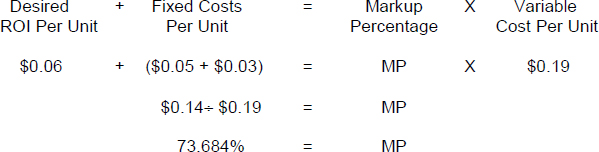

*17. Under variable-cost pricing, the cost base consists of all of the variable costs associated with a product, including variable selling and administrative costs. Because fixed costs are not included in the base, the markup must provide for fixed costs (manufacturing and selling and administrative) and the target ROI. The contribution approach is more useful for making short-run decisions because it displays variable cost and fixed cost behavior patterns separately.

The steps in using the contribution approach are as follows:

- Compute the unit variable cost.

- Compute the markup percentage using the formula:

- Set the target selling price using the formula:

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following is an not generally the type of product sold by a price taker?

- Sand.

- Corn.

- A designer dress.

- Coal.

- (L.O. 2) The cost-plus pricing formula is:

- Target selling price = Cost + (Markup percentage × Cost)

- Target selling price = Cost − (Markup percentage × Cost)

- Target selling price = Cost + (Markup percentage ÷ Cost)

- Target selling price = Cost − (Markup percentage ÷ Cost)

- (L.O. 2) The following information is provided for Roth Company for the new product it recently introduced:

Total unit cost $40 Desired ROI per unit $12 Target selling price $52 What would be Roth Company's percentage markup on cost?

- 23%

- 30%

- 70%

- 130%

Items 4, 5, and 6 relate to the following information:

Carmalita Company is going to sell a new V1 stereo speaker system. The per unit variable cost estimates for the speaker system are as follows:

| Direct materials | $45 |

| Direct labor | 25 |

| Variable manufacturing overhead | 15 |

| Variable selling and administrative expenses | 10 |

The fixed costs per speaker system at a budgeted sales volume of 20,000 units are as follows:

| Fixed manufacturing overhead | $160,000 |

| Fixed selling and administrative expenses | 100,000 |

Carmalita has decided to price its new speaker system to earn a 25 percent return on its investment (ROI) of $800,000.

4. (L.O. 2) On a per unit basis, what is the desired ROI of Carmalita Company?

- $ 5

- $10

- $15

- $20

5. (L.O. 2) What is the sales price Carmalita should sell the V1 speaker system to receive the desired return on its investment?

- $ 95.

- $105.

- $118.

- $128.

6. (L.O. 2) What is the percentage markup on cost for the V1 speaker system for Carmalita?

- 9.26%

- 13.25%

- 14.87%

- 17.21%

7. (L.O. 6) Which of the following is not considered a limitation of cost-plus pricing?

- It is difficult to compute.

- The model does not give consideration to the demand side.

- The model does not guarantee that customers will pay the price computed.

- Sales volume plays a large role in determining per unit costs.

Items 8, 9 and 10 relate to the following information:

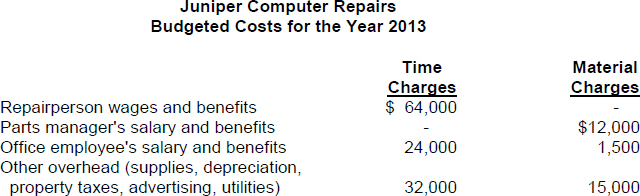

Juniper Computer Repairs has the following budgeted costs for the year 2013:

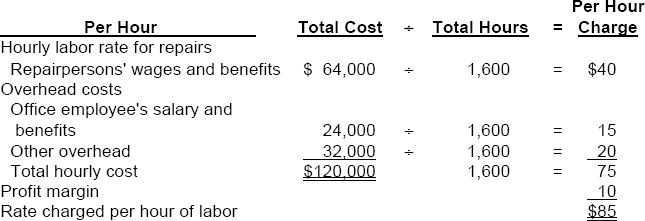

8. (L.O. 3) If Juniper budgets 1,600 hours of repair time in 2013, and it desires a profit margin of $10 per hour of labor, what is the labor charge per hour for any particular job?

- $65.

- $75.

- $85.

- $95.

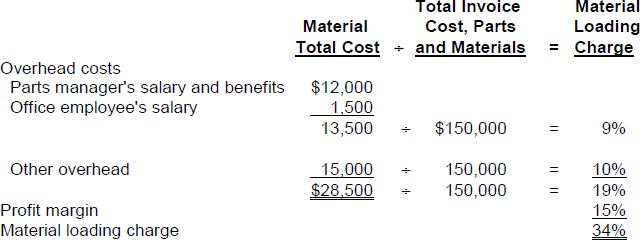

9. (L.O. 3) If Juniper estimates that the total invoice cost of parts and materials used in 2013 will be $150,000 and desires a 15 percent profit margin on the invoice cost of parts and materials, what should be the material loading charge used by Juniper in 2013?

- 34%

- 40%

- 44%

- 50%

10. (L.O. 3) Juniper estimates that a repair job for Buxter Company will require 3 hours of labor and $400 in parts and materials. Juniper's price quotation for the job should be:

- $487.

- $791.

- $852.

- $912.

11. (L.O. 4) Under negotiated transfer pricing, when the selling division has no excess capacity, how should the minimum transfer price by the selling division be calculated?

- Variable cost per unit.

- Variable cost per unit less its lost contribution margin per unit.

- Variable cost per unit plus its lost contribution margin per unit.

- Contribution margin per unit.

12. (L.O. 4) Lost contribution margin is often referred to as:

- sunk cost.

- contribution cost.

- lost cost.

- opportunity cost.

Items 13 and 14 relate to the following information:

The Howell Company primarily sells dishes, and recently purchased a cardboard box company. Howell's new cardboard box division has no excess capacity and produces and sells 40,000 boxes to outside customers. The variable cost of each box is $1.25 and usually has a contribution margin per box of $0.75. Management of Howell's dish division has decided it would like the box division to provide it with boxes.

13. (L.O. 4) What is the minimum transfer price the box division should find as acceptable?

- $0.50

- $0.75

- $1.25

- $2.00

14. (L.O. 4) Assuming that Howell's box division has excess capacity to provide all the boxes to the dish division without any loss in sales to outside customers, what is the minimum transfer price the box division should find as acceptable?

- $0.50

- $0.75

- $1.25

- $2.00

15. (L.O. 4) What transfer pricing method is known to have the disadvantage that it can lead to a loss of profitability for the company and unfair evaluations of division performance?

- Negotiated transfer prices.

- Cost-based transfer prices.

- Market-based transfer prices.

- Time and material transfer prices.

16. (L.O. 4) What transfer pricing method is often considered the best approach because it is objective and generally provides the proper economic incentives?

- Negotiated transfer prices.

- Cost-based transfer prices.

- Market-based transfer prices.

- Time and material transfer prices.

17. (L.O. 5) The Prine Company sells suit jackets and buttons. The suit jacket division is located in a country that has a tax rate of 26% and the buttons division is located in a country that has a tax rate of 32%. How should the Prine Company set transfer prices to minimize income taxes when the buttons division provides buttons to the suit jacket division?

- The division in the high-tax-rate country should be allocated more contribution margin.

- The suit jacket division should be allocated more contribution margin.

- The buttons division should be allocated more contribution margin.

- The suit jacket division should be allocated less contribution margin.

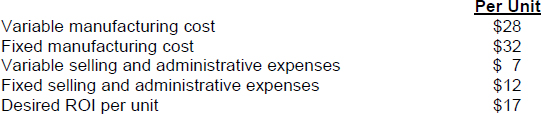

*Items 18, 19, 20 and 21 relate to the following information:

Monty Company sells a golfing aid called “The Monty Swing King” which is used to help golfers keep a steady tempo during their golf swing. Monty has the following cost information related to its production of the Swing Kings:

*18. (L.O. 6) What is the markup percentage assuming that Monty Company uses absorption cost pricing?

- 28%

- 36%

- 50%

- 60%

*19. (L.O. 6) What is the target selling price assuming that Monty Company uses absorption cost pricing?

- $ 78

- $ 86

- $ 96

- $104

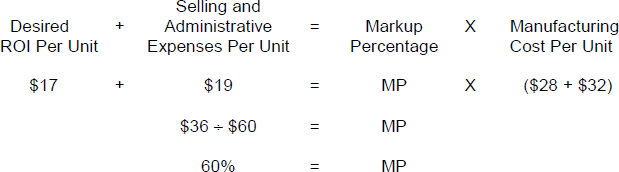

*20. (L.O. 6) What is the markup percentage assuming that Monty Company uses variable-cost pricing?

- 125.0%

- 174.3%

- 218.2%

- 229.6%

*21. (L.O. 6) What is the target selling price assuming that Monty Company uses variable-cost pricing?

- $ 78

- $ 86

- $ 96

- $104

![]()

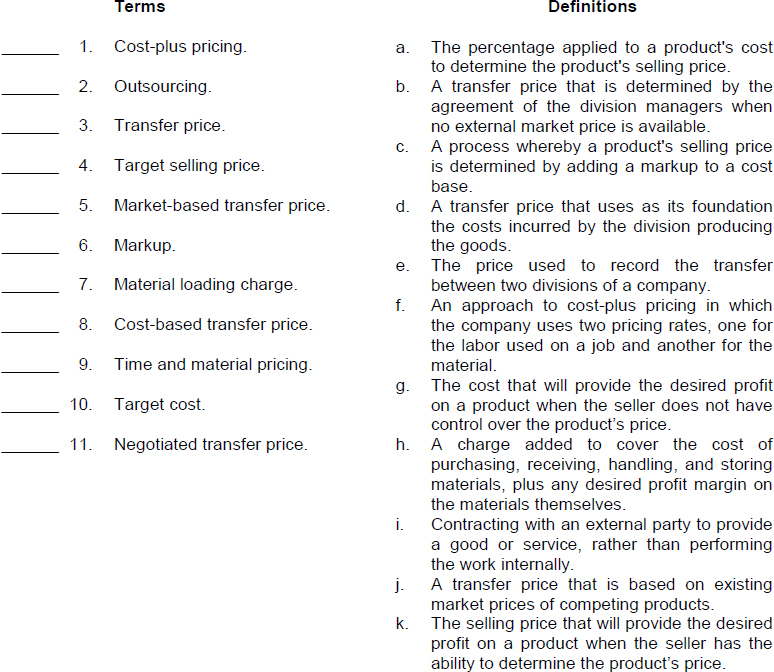

Match each term with its definition by writing the appropriate letter in the space provided.

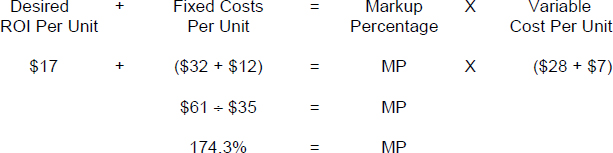

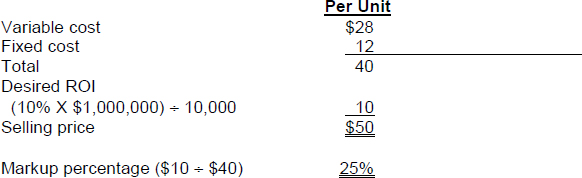

EX. J-1 (L.O. 2) Picture Frame, Inc. is in the process of setting a selling price on its new X1 frame. The variable cost per X1 frame is $28 and the fixed cost per X1 frame at a budgeted sales volume of 10,000 frames is $12. Picture Frame, Inc. has decided to price its new X1 frame to earn a 10% return on its investment (ROI) of $1,000,000.

Instructions

Compute the target selling price and the markup percentage that Picture Frame, Inc. should set for its X1 frame.

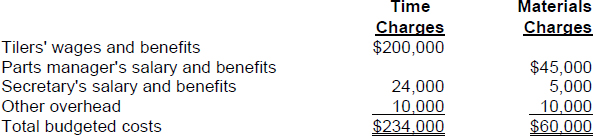

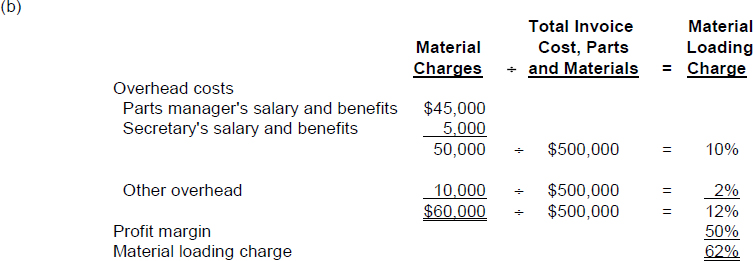

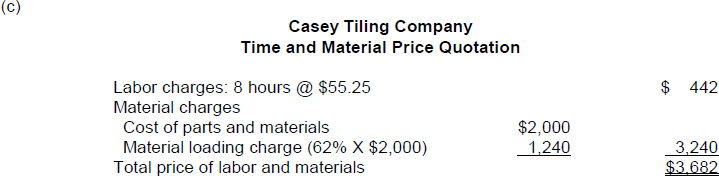

EX. J-2 (L.O. 3) Casey Tiling Company sells and installs tiles on kitchen cabinet tops. The following budgeted cost data is available:

The company has budgeted for 8,000 tiler hours of time during the coming year. It desires a $26 profit margin per hour of labor and a 50% profit on parts. It estimates the total invoice cost of parts and materials in 2013 will be $500,000.

Instructions

(a) Compute the rate charged per hour of labor (round to 2 decimal places).

(b) Compute the material loading charge (round to 2 decimal places).

(c) Casey has just received a request for a bid on a new kitchen tiling job. The company estimates that it would require 8 hours of labor and $2,000 of parts. Compute the total estimated bill.

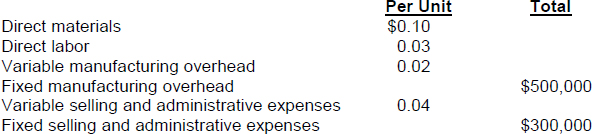

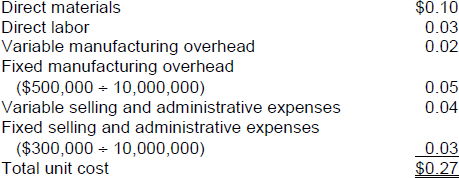

EX. J-3 (L.O. 6) Williams Notebook Corporation makes the Student Spiral Notebook. The following information is available for Williams' anticipated annual volume of 10,000,000 units.

The company has a desired ROI of 30%. It has invested assets of $2,000,000.

Instructions

(a) Compute the total cost per unit.

(b) Compute the desired ROI per unit.

(c) Using the absorption cost approach, compute the markup percentage and target selling price.

(d) Using the contribution approach, compute the markup percentage and target selling price.

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (F) | Price takers are companies that cannot easily set the prices on the products or services they sell. Instead, the prices are generally set by the competitive market (the laws of supply and demand). |

| 2. (T) | |

| 3. (T) | |

| 4. (F) | Cost-plus pricing involves establishing a cost base and adding a markup to determine a target selling price. |

| 5. (F) | The cost-plus pricing approach has a major advantage: It is simple to compute. |

| 6. (T) | |

| 7. (T) | |

| 8. (F) | Time and material pricing is widely used in service industries. |

| 9. (F) | The charge for labor time includes (1) the direct labor cost of the employee, including hourly rate or salary and fringe benefits; (2) selling, administrative, and similar overhead costs; and (3) an allowance for a desired profit or ROI per hour of employee time. Purchasing, receiving, handling, and storing materials are typically covered in the material loading charge. |

| 10. (T) | |

| 11. (F) | When goods are transferred internally, the price used to record the transfer between the two divisions is the transfer price. |

| 12. (T) | |

| 13. (T) | |

| 14. (F) | A cost-based approach can sometimes lead to unfair evaluations of division performance. |

| 15. (T) | |

| 16. (T) | |

| 17. (F) | To minimize income taxes when there are transfers between divisions in different countries, the division in the low-tax-rate country is allocated more contribution margin, and the division in the high-tax-rate country is allocated less. |

| *18. (F) | Under absorption cost pricing, both variable and fixed selling administrative costs are excluded from the cost base. |

| *19. (T) | |

| *20. (T) |

MULTIPLE CHOICE

MATCHING

- c

- i

- e

- k

- j

- a

- h

- d

- f

- g

- b

EX. J-1

EX. J-2

*EX. J-3

(a)

(b) Desired ROI = (30% × $2,000,000) ÷ 10,000,000 = $.06

(c) The unit manufacturing cost under absorption cost pricing is as follows:

| Per Unit | |

| Direct materials | $0.10 |

| Direct labor | 0.03 |

| Variable manufacturing overhead | 0.02 |

| Fixed manufacturing overhead | 0.05 |

| Total unit manufacturing cost | $0.20 |

The markup percentage is calculated as follows:

The target selling price is calculated as follow:

(d) The unit manufacturing cost under variable cost pricing is as follows:

| Per Unit | |

| Direct materials | $0.10 |

| Direct labor | 0.03 |

| Variable manufacturing overhead | 0.02 |

| Variable selling and administrative expenses | 0.04 |

| Total unit manufacturing cost | $0.19 |

The markup percentage is calculated as follows:

The target selling price is calculated as follow: