Chapter 24

PLANNING FOR CAPITAL INVESTMENTS

After studying this chapter, you should be able to:

- Discuss capital budgeting evaluation and explain inputs used in capital budgeting.

- Describe the cash payback technique.

- Explain the net present value method.

- Identify the challenges presented by intangible benefits in capital budgeting.

- Describe the profitability index.

- Indicate the benefits of performing a post-audit.

- Explain the internal rate of return method.

- Describe the annual rate of return method.

PREVIEW OF CHAPTER 24

The process of making capital expenditure decisions is referred to as capital budgeting. Capital budgeting involves choosing among various capital projects to find the one(s) that will maximize a company's return on its financial investment. The purpose of this chapter is to discuss the various techniques used to make effective capital budgeting decisions. The content and organization of the chapter are as follows:

The Capital Budgeting Evaluation Process

- (L.O. 1) The capital budgeting evaluation process generally has the following steps:

- Project proposals are requested from departments, plants, and authorized personnel;

- Proposals are screened by a capital budget committee;

- Officers determine which projects are worthy of funding; and

- Board of directors approves capital budget.

Cash Flow Information

2. While accrual accounting has advantages over cash accounting in many contexts, for purposes of capital budgeting, estimated cash inflows and outflows are preferred for inputs into the capital budgeting decision tools.

3. Sometimes cash flow information is not available, in which case adjustments can be made to accrual accounting numbers to estimate cash flows.

4. The capital budgeting decision, under any technique, depends in part on a variety of considerations:

a. The availability of funds;

b. Relationships among proposed projects;

c. The company's basic decision-making approach; and

d. The risk associated with a particular project.

Cash Payback

5. (L.O. 2) The cash payback technique identifies the time period required to recover the cost of the capital investment from the net annual cash inflow produced by the investment. The formula for computing the cash payback period is:

Cost of Capital Investment ÷ Net Annual Cash Flow = Cash Payback Period

Net annual cash flow can be approximated by adding depreciation expense to net income.

6. The evaluation of the payback period is often related to the expected useful life of the asset.

a. With this technique, the shorter the payback period, the more attractive the investment.

b. This technique is useful as an initial screening tool.

c. This technique ignores both the expected profitability of the investment and the time value of money.

Net Present Value Method

7. (L.O. 3) Under the net present value (NPV) method, cash flows are discounted to their present value and then compared with the capital outlay required by the investment. The difference between these two amounts is the net present value (NPV).

a. The interest rate used in discounting the future net cash flows is the required minimum rate of return.

b. A proposal is acceptable when NPV is zero or positive.

c. The higher the positive NPV, the more attractive the investment.

8. When there are equal annual cash inflows, the table showing the present value of an annuity of 1 can be used in determining present value. When there are unequal annual cash inflows, the table showing the present value of a single future amount must be used in determining present value.

9. The discount rate used by most companies is its cost of capital—that is, the rate that the company must pay to obtain funds from creditors and stockholders.

10. The net present value method demonstrated in the text requires the following assumptions:

a. All cash flows come at the end of each year;

b. All cash flows are immediately reinvested in another project that has a similar return; and

c. All cash flows can be predicted with certainty.

Intangible Benefits

11. (L.O. 4) By ignoring intangible benefits, such as increased quality or improved safety, capital budgeting techniques might incorrectly eliminate projects that could be financially beneficial to the company. To avoid rejecting projects that actually should be accepted, two possible approaches are suggested;

a. Calculate net present value ignoring intangible benefits, and then, if the NPV is negative, ask whether the intangible benefits are worth at least the amount of the negative NPV.

b. Project rough, conservative estimates of the value of the intangible benefits, and incorporate these values into the NPV calculation.

Mutually Exclusive Projects

12. (L.O. 5) In theory, all projects with positive NPVs should be accepted. However, companies rarely are able to adopt all positive-NPV proposals because (1) the proposals are mutually exclusive (if the company adopts one proposal, it would be impossible to also adopt the other proposal), and (2) companies have limited resources.

13. In choosing between two projects, one method that takes into account both the size of the original investment and the discounted cash flows is the profitability index. The profitability index formula is as follows:

![]()

The project with the greater profitability index should be the one chosen.

14. Another consideration made by financial analysts is uncertainty or risk. One approach for dealing with uncertainty is sensitivity analysis. Sensitivity analysis uses a number of outcome estimates to get a sense of the variability among potential returns. In general, a higher risk project should be evaluated using a higher discount rate.

Post-Audit of Investment Projects

15. (L.O. 6) A post-audit is a thorough evaluation of how well a project's actual performance matches the projections made when the project was proposed. Performing a post-audit is beneficial for the following reasons:

a. Management will be encouraged to submit reasonable and accurate data when they make investment proposals;

b. A formal mechanism is used for determining whether existing projects should be supported or terminated;

c. Management improves their estimation techniques by evaluating their past successes and failures.

16. A post-audit involves the same evaluation techniques that were used in making the original capital budgeting decision—for example, use of the net present value method. The difference is that, in the post-audit, actual figures are inserted where known, and estimation of future amounts is revised based on new information.

Internal Rate of Return Method

17. (L.O. 7) The internal rate of return method results in finding the interest yield of the potential investment. This is the interest rate that will cause the present value of the proposed capital expenditure to equal the present value of the expected annual cash inflows. Determining the internal rate of return can be done with a financial (business) calculator, computerized spreadsheet, or by employing a trial-and-error procedure.

18. The decision rule is: Accept the project when the internal rate of return is equal to or greater than the required rate of return, and reject the project when the internal rate of return is less than the required rate.

Annual Rate of Return Method

19. (L.O. 8) The annual rate of return method indicates the profitability of a capital expenditure and its formula is:

20. The annual rate of return is compared with management's required minimum rate of return for investments of similar risk. The minimum rate of return (the hurdle rate or cutoff rate) is generally based on the company's cost of capital. The decision rule is: A project is acceptable if its rate of return is greater than management's minimum rate of return; it is unacceptable when the reverse is true.

21. When the rate of return technique is used in deciding among several acceptable projects, the higher the rate of return for a given risk, the more attractive the investment.

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

MULTIPLE CHOICE

Circle the letter that best answers each of the following statements.

- (L.O. 1) Which of the following is incorrect?

- Capital budgeting is the process of making capital expenditure decisions.

- Capital budgeting decisions are the opposite of incremental analysis.

- Accounting data are indispensable in capital budgeting decisions.

- Capital budgeting involves the allocation of limited resources.

- (L.O. 1 Which of the following is typically considered a cash inflow?

- Repairs and maintenance.

- Increased operating costs.

- Sale of old equipment.

- Overhaul of equipment.

- (L.O. 2) The cash payback formula is:

- Cost of Capital Investment ÷ Net Income.

- Cost of Capital Investment ÷ Net Annual Cash Flow.

- Average Investment ÷ Net Income.

- Average Investment ÷ Net Annual Cash Flow.

- (L.O. 2) Sue Bonno Company has identified that the cost of a new computer will be $40,000, but with the use of the new computer, net income will increase by $5,000 a year. If depreciation expense is $3,000 a year, the cash payback period is:

- 20 years.

- 10 years.

- 8 years.

- 5 years.

- (L.O. 3) Melvin's annual cash inflows are expected to be $32,000 for the next 8 years. Assuming a discount rate of 10%, the present value of cash flows for Melvin is:

- $14,928.

- $16,421.

- $170,718.

- $214,723.

- (L.O. 3) Which of the following is not part of the discounted cash flow techniques?

- Annual rate of return.

- Net present value method.

- Internal rate of return method.

- All of the above are part of the discounted cash flow technique.

- (L.O. 3) Which of the following is not considered in the net present value method?

- Present value of net annual cash flows.

- Present value of depreciation expense.

- Present value of liquidation proceeds.

- Capital investment.

- (L.O. 3) To approximate net annual cash flow, depreciation is:

- subtracted from net income because it is an expense.

- subtracted from net income because it is an outflow of cash.

- added back to net income because it is an inflow of cash.

- added back to net income because it is not an outflow of cash.

- (L.O. 3) A negative net present value means that the:

- project's rate of return exceeds the required rate of return.

- project's rate of return is less than the required rate of return.

- project's rate of return equals the required rate of return.

- project is acceptable.

- (L.O. 3) The salvage value on a piece of equipment is expected to be $10,000 in 12 years. If the discount rate is 8%, what is the present value of the equipment's salvage value?

- $3,168.

- $3,220.

- $3,971.

- $4,039.

- (L.O. 3) Mobley Corporation estimates that it will have the following future cash inflows over the next three years: 2013—$18,000; 2014—$19,000; and 2015—$20,000. If the discount rate is 6%, what is the present value of the future cash inflows?

- $50,683.

- $51,342.

- $53,561.

- $57,331.

- (L.O. 5) The profitability index is calculated by:

- dividing the initial investment by the present value of future cash flows.

- dividing the present value of cash flows by the initial investment.

- multiplying the initial investment by the present value of cash flows.

- multiplying the discount rate by the initial investment.

- (L.O. 5) Francisco Trujillo is contemplating a project with an initial investment of $50,000. Francisco also has a discount rate of 8%. If the project has estimated net annual cash flows of $12,000 for the next six years, what is the profitability index for the project?

- 1.03.

- 1.07.

- 1.11.

- 1.27.

- (L.O. 7) Which of the following statements about the internal rate of return method is false?

- It is widely used in practice.

- It results in finding the interest yield of the potential investment.

- It does not recognize the time value of money.

- The internal rate of return factor can be computed with a computerized spreadsheet.

- (L.O. 7) Jesilow Company is contemplating purchasing equipment for $60,000 with expected future annual cash inflows of $18,100 for the next 4 years. What is the estimated internal rate of return?

- 5%.

- 6%.

- 8%.

- 10%.

- (L.O. 7) Richman Company is contemplating a project with an initial capital investment of $40,000. The expected future annual cash inflows from the project are estimated to be $7,500 for the next 8 years. What is the estimated internal rate of return for the project?

- 4%.

- 6%.

- 8%.

- 10%.

- (L.O. 8) The formula for the annual rate of return method is:

- Annual Cash Flow ÷ Cost of Capital Investment.

- Annual Cash Flow ÷ Average Investment.

- Expected Annual Net Income ÷ Cost of Capital Investment.

- Expected Annual Net Income ÷ Average Investment.

- (L.O. 8) In the annual rate of return method, the minimum rate of return is not:

- based on the cost of capital.

- also called the annual rate of return.

- also called the hurdle rate.

- also called cutoff rate.

- (L.O. 8) Ehrlich Company had an investment which cost $260,000 and had a salvage value at the end of its useful life of zero. If Ehrlich's expected annual net income is $20,000, the annual rate of return is:

- 7.7%.

- 13%.

- 15.4%.

- 20%.

- (L.O. 8) Which of the following is not correct about the annual rate of return method?

- The calculation is simple.

- The accounting terms used are familiar to management.

- The time value of money is considered.

- The timing of the cash inflows is not considered.

Match each term with its definition by writing the appropriate letter in the space provided.

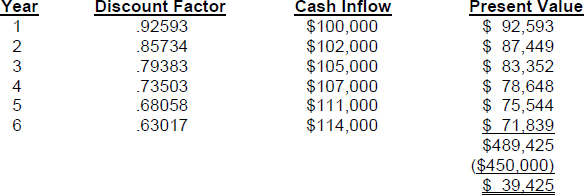

EX. 24-1 (L.O. 2, 3, and 8) Bianca Company is considering a long-term investment project. The project will require an investment of $450,000, and it will have a useful life of 6 years. Annual net income is expected to be: Year 1, $25,000; Year 2, $27,000; Year 3, $30,000; Year 4, $32,000; Year 5, $36,000; and Year 6, $39,000. Depreciation is computed by the straight-line method with no salvage value. The company's cost of capital is 8%. (Hint: Assume cash flows can be computed by adding back depreciation expense to net income.)

Instructions

(a) Compute the cash payback period for the project.

(b) Compute the net present value for the project.

(c) Compute the annual rate of return for the project.

EX. 24-2 (L.O. 2, 3, 7 and 8) Jenny Durdil Company is considering an investment of $200,000 in new equipment which will be depreciated on a straight-line basis (8-year life, no salvage value). The expected annual revenues and costs of the new product that will be produced from the equipment are:

Instructions

(Hint: Assume cash flows can be computed by adding back depreciation expense to net income.)

(a) Compute the cash payback period.

(b) Compute the net present value assuming a 12% required rate of return.

(c) Determine the internal rate of return.

(d) Compute the annual rate of return.

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

TRUE-FALSE

| 1. (T) | |

| 2. (F) | While accrual accounting has advantages over cash accounting in many contexts, for purposes of capital budgeting, estimated cash inflows and outflows are preferred for inputs in the capital budgeting decision tools. |

| 3. (T) | |

| 4. (F) | When the payback technique is used to decide among acceptable alternative projects, the shorter the payback period, the more attractive the investment. |

| 5. (T) | |

| 6. (T) | |

| 7. (F) | The net present value method considers both estimated total cash flows and the time value of money. |

| 8. (T) | |

| 9. (F) | The higher the positive net present value, the more attractive the investment. |

| 10. (T) | |

| 11. (F) | When making capital budgeting decisions, management should identify intangible benefits such as increased quality or safety or employee loyalty. |

| 12. (F) | “Mutually exclusive” means that if a company adopts one proposal, it would be impossible also to adopt the other proposal. |

| 13. (T) | |

| 14. (T) | |

| 15. (T) | |

| 16. (T) | |

| 17. (F) | The internal rate of return is widely used in practice and most managers find it easy to interpret. |

| 18. (T) | |

| 19. (F) | Under the annual rate of return method, a project is acceptable if its rate of return is greater than management's minimum rate of return. |

| 20. (T) |

MATCHING

- c

- i

- g

- d

- a

- e

- h

- b

- f

EX. 24-1

(a) Average annual net income: ($25,000 + $27,000 + $30,000 + $32,000 + $36,000 + $39,000) ÷ 6 = $31,500

Depreciation expense: $450,000 ÷ 6 = $75,000

Cash payback period: $450,000 ÷ ($31,500 + $75,000) = 4.23

(b)

(c) $31,500 ÷ ($450,000 ÷ 2) = 14%

EX. 24-2

(a) $200,000 ÷ ($16,170 + $25,000) = 4.86 years.

(b)

(c) $200,000 ÷ $41,170 = 4.8579 internal rate of return factor. The approximate internal rate of return is slightly greater than 12%.

(d) $16,170 ÷ [($200,000 + $0)/2] = 16.17%.