APPENDIX D

Time Value of Money

This appendix addresses the difference between simple interest, which is computed on principal only, and compound interest, which is computed on both principal and interest earned that has not been paid or withdrawn. Simple interest is the product of the principal, the rate, and the time, but the formula used for compound interest depends on whether you are solving for the present value or future value and whether the amount involved is a single sum or an annuity (a series of equal dollar amounts paid or received periodically).

LO1. Distinguish between simple and compound interest.

![]() Interest is basically a rental charge for the use of another person's money. The amount of interest involved in any financing transaction is based on three elements:

Interest is basically a rental charge for the use of another person's money. The amount of interest involved in any financing transaction is based on three elements:

1. Principal (p): the original amount borrowed or invested.

2. Interest Rate (i): an annual percentage of the principal.

3. Time (n): the number of periods that the principal is borrowed or invested.

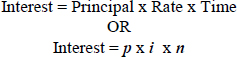

![]() Simple interest is computed on the principal amount only. Simple interest is usually expressed as:

Simple interest is computed on the principal amount only. Simple interest is usually expressed as:

![]() Compound interest is computed on principal and on any interest earned that has not been paid or withdrawn. It is the return on (or growth of) the principal for two or more time periods.

Compound interest is computed on principal and on any interest earned that has not been paid or withdrawn. It is the return on (or growth of) the principal for two or more time periods.

LO2. Solve for future value of a single amount.

![]() The future value of a single amount is the value at a future date of a given amount invested assuming compound interest. Future value is usually expressed as:

The future value of a single amount is the value at a future date of a given amount invested assuming compound interest. Future value is usually expressed as:

FV = p × (1 + i)n

- FV = future value of a single amount

- p = principal (or present value)

- i = interest rate for one period

- n = number of periods

![]() The Future Value of 1 table is used for obtaining a factor which is multiplied by the principal to calculate the future value.

The Future Value of 1 table is used for obtaining a factor which is multiplied by the principal to calculate the future value.

![]() Table 1 on page C4 is such a table, showing factors with 5-digit decimals.

Table 1 on page C4 is such a table, showing factors with 5-digit decimals.

LO3. Solve for future value of an annuity.

![]() The future value of an annuity is the sum of all the payments (receipts) plus the accumulated compound interest on them. In computing the future value of an annuity, it is necessary to know the (1) interest rate, (2) the number of compounding periods, and (3) the amount of the periodic payments or receipts. When the periodic payments or receipts are the same in each period, the future value can be computed by using a future value of an annuity of 1 table.

The future value of an annuity is the sum of all the payments (receipts) plus the accumulated compound interest on them. In computing the future value of an annuity, it is necessary to know the (1) interest rate, (2) the number of compounding periods, and (3) the amount of the periodic payments or receipts. When the periodic payments or receipts are the same in each period, the future value can be computed by using a future value of an annuity of 1 table.

![]() Calculating the future value of each individual cash flow is required when the period payments or receipts are not equal in each period.

Calculating the future value of each individual cash flow is required when the period payments or receipts are not equal in each period.

![]() Table 2 on page C6 shows the future value of 1 to be received periodically for a given number of periods.

Table 2 on page C6 shows the future value of 1 to be received periodically for a given number of periods.

![]() This table assumes that each payment is made at the end of each period.

This table assumes that each payment is made at the end of each period.

LO4. Identify the variables fundamental to solving present value problems.

![]() The present value is based on three variables: (1) the dollar amount to be received (future amount); (2) the length of time until the amount is received (number of periods); and (3) the interest rate (the discount rate).

The present value is based on three variables: (1) the dollar amount to be received (future amount); (2) the length of time until the amount is received (number of periods); and (3) the interest rate (the discount rate).

![]() Present value computations are used for principal and interest payments for determining the market price of bonds, as well as notes payable and lease liabilities.

Present value computations are used for principal and interest payments for determining the market price of bonds, as well as notes payable and lease liabilities.

LO5. Solve for present value of a single amount.

![]() If the future amount to be received in n periods is discounted at interest rate i, then the computation of a single amount to be invested is calculated as:

If the future amount to be received in n periods is discounted at interest rate i, then the computation of a single amount to be invested is calculated as:

- PV = present value

- FV = future value

- i = interest rate

- n = number of periods

![]() The present value of 1 may also be determined through tables that show the present value of 1 for n periods.

The present value of 1 may also be determined through tables that show the present value of 1 for n periods.

![]() Table 3 on page C8 is used to find the present value of a single amount.

Table 3 on page C8 is used to find the present value of a single amount.

LO6. Solve for present value of an annuity.

![]() In computing the present value of an annuity, it is necessary to know (1) the discount rate, (2) the number of discount periods, and (3) the amount of the periodic receipts or payments. When the future receipts are the same in each period, there are two other ways to compute the present value. First, the annual cash flow can be multiplied by the sum of the present value factors. Second, annuity tables may be used.

In computing the present value of an annuity, it is necessary to know (1) the discount rate, (2) the number of discount periods, and (3) the amount of the periodic receipts or payments. When the future receipts are the same in each period, there are two other ways to compute the present value. First, the annual cash flow can be multiplied by the sum of the present value factors. Second, annuity tables may be used.

![]() Discounting may also be done over shorter periods of time such as monthly, quarterly, or semiannually. When the time frame is less than one year, it is necessary to convert the annual interest rate to the applicable time frame.

Discounting may also be done over shorter periods of time such as monthly, quarterly, or semiannually. When the time frame is less than one year, it is necessary to convert the annual interest rate to the applicable time frame.

![]() Table 4 on page C10 is used to find the present value of an annuity.

Table 4 on page C10 is used to find the present value of an annuity.

LO7. Compute the present value of notes and bonds.

![]() The present value (or market price) of a long-term note or bond is a function of three variables: (1) the payment amounts, (2) the length of time until the amounts are paid, and (3) the discount rate.

The present value (or market price) of a long-term note or bond is a function of three variables: (1) the payment amounts, (2) the length of time until the amounts are paid, and (3) the discount rate.

![]() The first variable (dollars to be paid) is made up of two elements: (1) a series of interest payments (an annuity) and (2) the principal amount (a single sum). To compute the present value of the bond, both the interest payments and the principal amount must be discounted: This involves two different computations.

The first variable (dollars to be paid) is made up of two elements: (1) a series of interest payments (an annuity) and (2) the principal amount (a single sum). To compute the present value of the bond, both the interest payments and the principal amount must be discounted: This involves two different computations.

![]() When the investor's discount rate is equal to the bond's contractual interest rate, the present value of the bonds will equal the face value of the bonds.

When the investor's discount rate is equal to the bond's contractual interest rate, the present value of the bonds will equal the face value of the bonds.

LO8. Use a financial calculator to solve time value of money problems.

![]() Once an understanding of the basic time value of money concepts is gained, many professionals use financial calculators to solve the computations.

Once an understanding of the basic time value of money concepts is gained, many professionals use financial calculators to solve the computations.

![]() The most common keys used for solving time value of money problems with a financial calculator include:

The most common keys used for solving time value of money problems with a financial calculator include:

2. I = interest rate per period (some calculators use I/YR or i)

3. PV = present value (occurs at the beginning of the first period)

4. PMT = payment (all payments are equal, and none are skipped)

5. FV = future value (occurs at the end of the last period)

![]() Most problems give three of four variables and require solving for the remaining variable. The fifth key (key not used) is given a value of zero to ensure that this variable is not used in the computation.

Most problems give three of four variables and require solving for the remaining variable. The fifth key (key not used) is given a value of zero to ensure that this variable is not used in the computation.

![]() Financial calculators are particularly useful where interest rates and compounding periods are not presented in tables.

Financial calculators are particularly useful where interest rates and compounding periods are not presented in tables.

APPENDIX SELF TEST

As you work the exercises and problems, remember to use the Decision Toolkit discussed and used in the text:

- Decision Checkpoints: at this point you ask a question.

- Info Needed for Decision: you make a choice regarding the information needed to answer the question.

- Tool to Use for Decision: at this point you review just what the information chosen in step 2 does for the decision-making process.

- How to Evaluate Results: you perform evaluation of information for answering the question.

Note: The notation (LO1) means that the question was drawn from learning objective number one.

Completion

Please write in the word or words that will complete the sentence.

- (LO1) _______________________ interest is computed on the principal amount only.

- (LO1) _______________________ interest is computed on principal and on any interest that has not been paid or withdrawn.

- (LO3) An _______________________ is a series of equal dollar amounts to be paid or received periodically.

- (LO3) If you wish to know how much money you will have if you invest $3,000 at the end of each year for 5 years, you must solve for the _______________________ value of an annuity.

- (LO5) If you wish to know how much to invest today so that you will have $2,000 at the end of 2 years, you must solve for the _______________________ value of a single amount.

Multiple Choice

Please circle the correct answer.

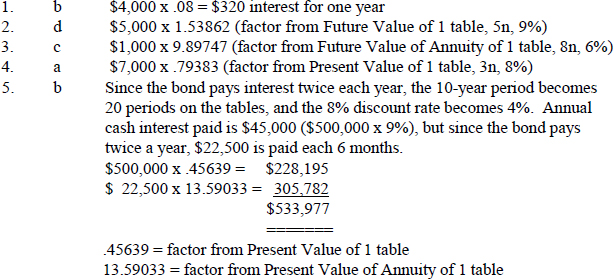

- (LO1) What is the annual simple interest on $4,000 borrowed for 3 years at 8%?

- $160

- $320

- $480

- $960

- (LO2) Erin has invested $5,000 for 5 years compounded annually at an interest rate of 9%. How much money will she have available at the end of the 5 years?

- $29,923.55

- $19,448.25

- $16,248.25

- $ 7,693.10

- (LO3) Jerry plans to invest $1,000 at the end of each year for 8 years with interest compounded annually at 6%. How much money will he have available at the end of the eighth year?

- $ 5,019.28

- $ 6,209.79

- $ 9,897.47

- $12,750.80

- (LO5) Angela needs to have $7,000 available in 3 years. How much must she invest today, with interest compounded annually at 8%, to have that amount available when she needs it?

- $5,556.81

- $6,013.23

- $7,574.93

- $8,817.97

- (SO7) On January 2, 2014, Culloden Corporation issued $500,000 of 9% bonds with a maturity date of January 2, 2024. The bonds pay interest each January 1 and July starting on July 1, 2014. On the sale date, the discount rate was 8%. How much did Culloden receive when it sold the bonds?

- $545,000

- $533,977

- $522,500

- $500,000

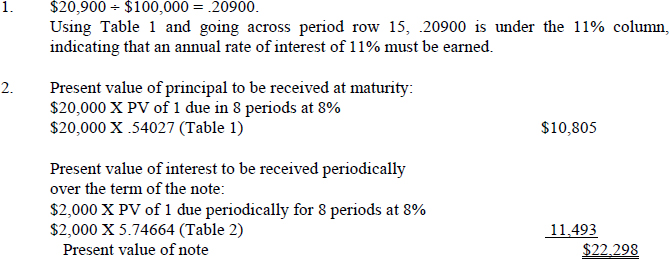

1. If Elizabeth invests $20,900 now and wants to receive $100,000 at the end of 15 years, what annual rate of interest will Elizabeth earn on her investment?

2. Boyd Corporation receives a $20,000, 8-year note bearing interest of 10% (paid annually) from a customer at a time when the discount rate is 8%. What is the present value of the note received by Boyd?

SOLUTIONS TO SELF-TEST

Completion

- Simple

- Compound

- annuity

- future

- present

Multiple Choice