Chapter 21

BUDGETARY PLANNING

CHAPTER LEARNING OBJECTIVES

After studying this chapter, you should be able to:

- Indicate the benefits of budgeting.

- State the essentials of effective budgeting.

- Identify the budgets that comprise the master budget.

- Describe the sources for preparing the budgeted income statement.

- Explain the principal sections of a cash budget.

- Indicate the applicability of budgeting in nonmanufacturing companies.

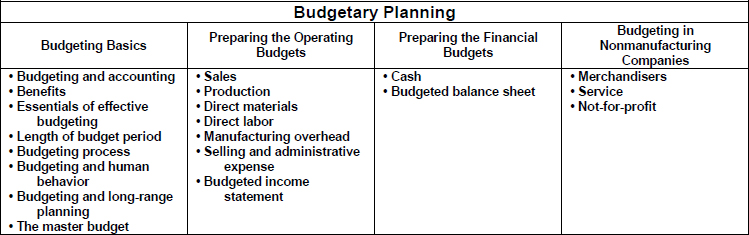

PREVIEW OF CHAPTER 21

Our primary focus in this chapter is budgeting—specifically, how budgeting is used as a planning tool by management. Through budgeting, it should be possible for management to maintain enough cash to pay creditors, to have sufficient raw materials to meet production requirements, and to have adequate finished goods to meet expected sales. The content and organization of this chapter are as follows:

CHAPTER REVIEW

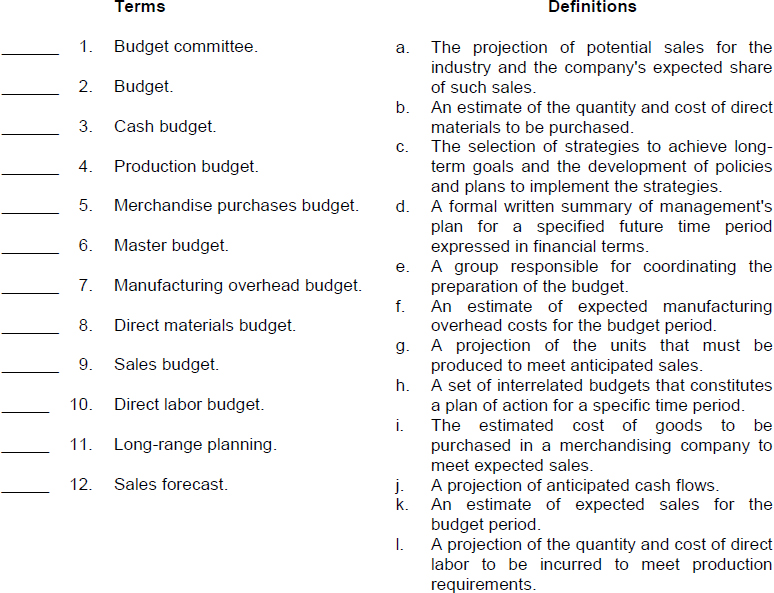

- (L.O. 1) A budget is a formal written statement of management's plans for a specified time period, expressed in financial terms.

- The role of accounting during the budgeting process is to (a) provide historical data on revenues, costs, and expenses, (b) express management's plans in financial terms, and (c) prepare periodic budget reports.

Benefits of Budgeting

3. The primary benefits of budgeting are as follows:

a. It requires all levels of management to plan ahead.

b. It provides definite objectives for evaluating performance.

c. It creates an early warning system for potential problems.

d. It facilitates the coordination of activities within the business.

e. It results in greater management awareness of the entity's overall operations.

f. It motivates personnel throughout the organization.

Essentials of Effective Budgeting

4. (L.O. 2) In order to be effective management tools, budgets must be based upon

a. A sound organizational structure in which authority and responsibility are clearly defined.

b. Research and analysis to determine the feasibility of new products, services, and operating techniques.

c. Management acceptance which is enhanced when all levels of management participate in the preparation of the budget, and the budget has the support of top management.

5. The most common budget period is one year. A continuous twelve-month budget results from dropping the month just ended and adding a future month. The annual budget is often supplemented by monthly and quarterly budgets.

6. The responsibility for coordinating the preparation of the budget is assigned to a budget committee. The budget committee usually includes the president, treasurer, chief accountant (controller), and management personnel from each major area of the company.

7. A budget can have a significant impact on human behavior. A budget may have a strong positive influence on a manager when

a. Each level of management is invited and encouraged to participate in developing the budget.

b. Criticism of a manager's performance is tempered with advice and assistance.

8. Long-range planning involves the selection of strategies to achieve long-term goals and the development of policies and plans to implement the strategies. Long-range plans contain considerably less detail than budgets.

9. (L.O. 3) The master budget is a set of interrelated budgets that constitutes a plan of action for a specified time period. It is developed within the framework of a sales forecast which shows potential sales for the industry and the company's expected share of such sales.

10. There are two classes of budgets in the master budget.

a. Operating budgets are the individual budgets that result in the preparation of the budgeted income statement.

b. Financial budgets focus primarily on the cash resources needed to fund expected operations and planned capital expenditures.

11. The sales budget is the first budget prepared. It is derived from the sales forecast, and it represents management's best estimate of sales revenue for the budget period. It is prepared by multiplying the expected unit sales volume for each product by its anticipated unit selling price.

12. The production budget shows the units that must be produced to meet anticipated sales. It is derived from the budgeted sales units plus the desired ending finished goods units less the beginning finished goods units.

13. The direct materials budget shows both the quantity and cost of direct materials to be purchased. It is derived from the direct materials units required for production plus the desired ending direct materials units less the beginning direct materials units.

14. The direct labor budget shows the quantity (hours) and cost of direct labor necessary to meet production requirements. The direct labor budget is critical in maintaining a labor force that can meet expected levels of production.

15. The manufacturing overhead budget shows the expected manufacturing overhead costs. The selling and administrative expense budget is a projection of anticipated operating expenses. Both budgets distinguish between fixed and variable costs.

Budgeted Income Statement

16. (L.O. 4) The budgeted income statement is the important end-product in preparing operating budgets. This budget indicates the expected profitability of operations and it provides a basis for evaluating company performance.

a. The budget is prepared from the budgets described in review points 11-15.

b. For example, to find cost of goods sold, it is necessary to determine the total unit cost of a finished product using the direct materials, direct labor, and manufacturing overhead budgets.

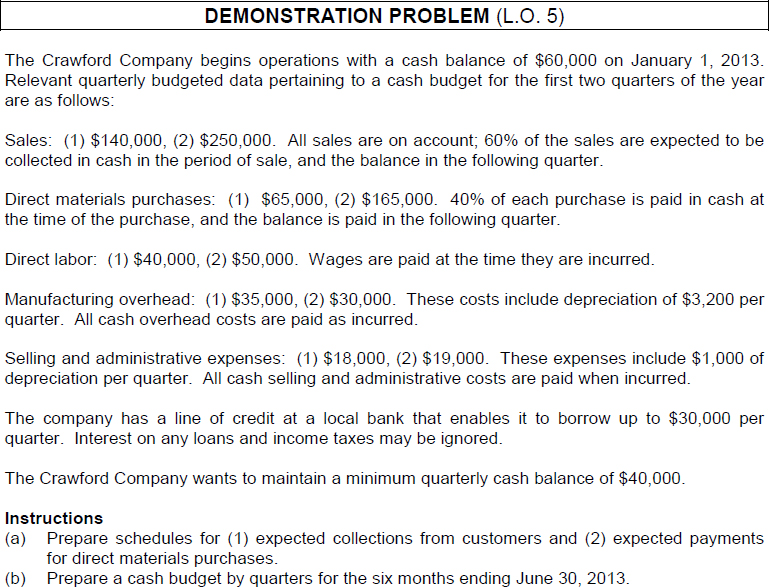

Cash Budget

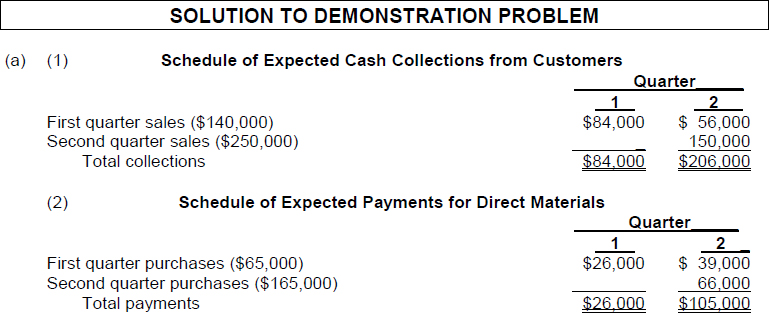

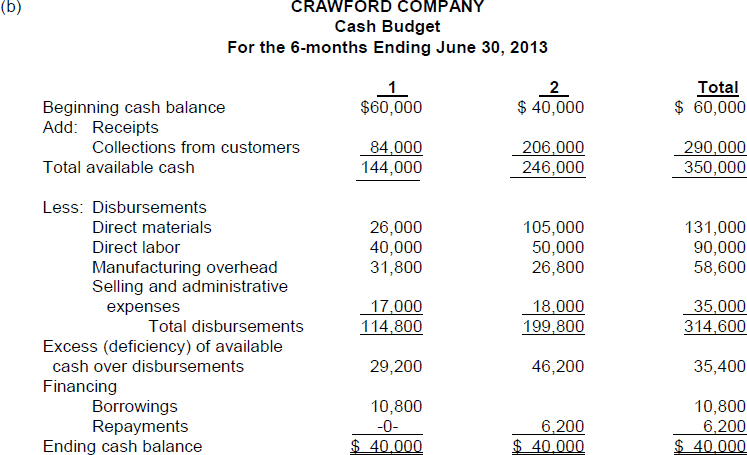

17. (L.O. 5) The cash budget shows anticipated cash flows. It contains three sections (cash receipts, cash disbursements, and financing) and the beginning and ending cash balances. Data for preparing this budget are obtained from the other budgets.

18. The budgeted balance sheet is a projection of financial position at the end of the budget period. It is developed from the budgeted balance sheet for the preceding year and the budgets for the current year.

Budgeting in Nonmanufacturing Companies

19. (L.O. 6) The major differences in the master budget of a merchandiser and a manufacturing company are that a merchandiser (a) uses a merchandise purchases budget instead of a production budget and (b) does not use the manufacturing budgets (direct materials, direct labor, and manufacturing overhead).

20. In service enterprises, the critical factor in budgeting is coordinating professional staff needs with anticipated services. Budget data for service revenue may be obtained from expected output or expected input.

21. In the budget process for not-for-profit organizations, the emphasis is on cash flows rather than on a revenue and expense basis. For governmental units, the budget must be strictly followed and overspending is often illegal.

REVIEW QUESTIONS AND EXERCISES

TRUE—FALSE

Indicate whether each of the following is true (T) or false (F) in the space provided.

Circle the letter that best answers each of the following statements.

- (L.O. 1) The responsibility for expressing management's budgeting goals in financial terms is performed by the:

- accounting department.

- top management.

- lower level of management.

- budget committee.

- (L.O. 1) Which of the following would not be considered a benefit of budgeting?

- Facilitates the coordination of activities.

- Requires all levels of management to plan ahead.

- Always motivates personnel.

- Results in greater management awareness of the entity's overall operations.

- (L.O. 2) In order for budgets to be effective there must be:

- sound organizational structure.

- research and analysis.

- management acceptance of the budget program.

- all of the above.

- (L.O. 2) For better management acceptance, the flow of input data for budgeting should begin with the:

- accounting department.

- top management.

- lower levels of management.

- budget committee.

- (L.O. 2) Responsibility for coordinating the preparation of the budget is assigned to the:

- accounting department.

- top management.

- lower levels of management.

- budget committee.

- (L.O. 2) Which of the following is not a characteristic of long-range planning?

- It encompasses a period of at least five years.

- Consideration is given to the economic and political environment.

- More detail is presented than in a budget.

- It is used to review progress rather than as a basis for control.

- (L.O. 3) The starting point in preparing the master budget is the:

- cash budget.

- budgeted income statement.

- direct materials budget.

- sales budget.

- (L.O. 3) The Turlington Company has 12,000 units in beginning finished goods. If sales are expected to be 60,000 units for the year and Turlington desires ending finished goods of 15,000 units, how many units must Turlington produce?

- 57,000.

- 60,000.

- 63,000.

- 75,000.

- (L.O. 3) The Evangelista Company has 3,000 units in beginning finished goods. The sales budget shows expected sales to be 12,000 units. If the production budget shows that 14,000 units are required for production, what was the desired ending finished goods?

- 1,000.

- 3,000.

- 5,000.

- 9,000.

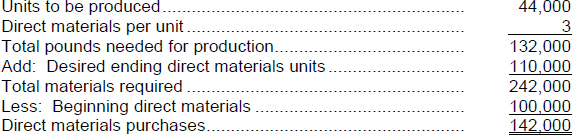

- (L.O. 3) In the Campbell Company required production for June is 44,000 units. To make one unit of finished product, three pounds of direct material Z are required. Actual beginning and desired ending inventories of direct material Z are 100,000 and 110,000 pounds, respectively. How many pounds of direct material Z must be purchased?

- 126,000.

- 132,000.

- 136,000.

- 142,000.

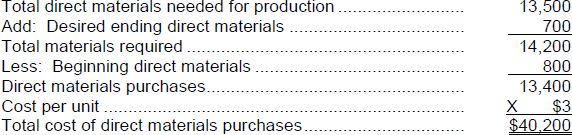

- (L.O. 3) Taylor Company determines that 13,500 pounds of direct materials are needed for production in July. There are 800 pounds of direct materials on hand at July 1 and the desired ending inventory is 700 units. If the cost per unit of direct materials is $3, what is the budgeted total cost of direct materials purchases?

- $39,600.

- $40,200.

- $40,800.

- $41,400.

- (L.O. 3) Navia Company is preparing its direct labor budget for May. Projections for the month are that 8,350 units are to be produced and that direct labor time is three hours per unit. If the labor cost per hour is $9, what is the total budgeted direct labor cost for May?

- $217,350.

- $221,400.

- $225,450.

- $243,000.

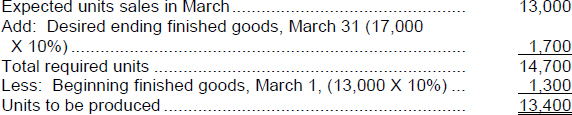

- (L.O. 3) Porizkova Company requires that ending finished goods inventory for each month be 10% of the next month's budgeted sales. Budgeted sales in units are February 15,000, March 13,000 and April 17,000. What should be the level of production scheduled for March?

- 12,800.

- 13,000.

- 13,400.

- 14,700.

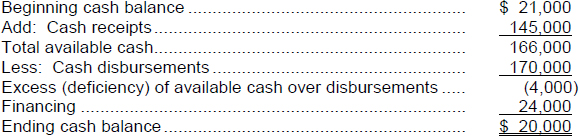

- (L.O. 5) On January 1, Ghauri Company has a beginning cash balance of $21,000. During the year, the company expects cash disbursements of $170,000 and cash receipts of $145,000. If Ghauri requires an ending cash balance of $20,000, the Ghauri Company must borrow:

- $16,000.

- $20,000.

- $24,000.

- $46,000.

- (L.O. 5) The Tennant Company has the following budgeted sales: January $40,000, February $60,000, and March $50,000. 40% of the sales are for cash and 60% are on credit. For the credit sales, 50% are collected in the month of sale, and 50% the next month. The total expected cash receipts during March are:

- $56,000.

- $53,000.

- $52,500.

- $50,000.

- (L.O. 5) The Auermann Company's direct materials budget shows total cost of direct materials purchases for January $125,000, February $150,000 and March $175,000. Cash payments are 60% in the month of purchase and 40% in the following month. The budgeted cash payments for March are:

- $165,000.

- $160,000.

- $150,000.

- $130,000.

- (L.O. 6) Which of the following statements about budgeted financial statements is incorrect?

- The budgeted balance sheet is developed entirely from the budgets for the current year.

- Once established, the budgeted income statement provides the basis for evaluating company performance.

- Cost of goods sold is determined by multiplying the budgeted unit sales by the budgeted total unit production cost.

- The budgeted income statement is developed from the budgets for the current year.

- (L.O. 6) A purchases budget is used instead of a production budget by:

- merchandising companies.

- service enterprises.

- not-for-profit organizations.

- manufacturing companies.

- (L.O. 6) Entities that budget on the basis of cash flows (expenditures and receipts) rather than on a revenue and expense basis are:

- merchandising companies.

- service enterprises.

- not-for-profit organizations.

- manufacturing companies.

- (L.O. 6) Which of the following statements is incorrect?

- A continuous twelve-month budget results from dropping the month just ended and adding a future month.

- The production budget is derived from the direct materials and direct labor budget.

- The cash budget shows anticipated cash flows.

- In the budget process for not-for-profit organizations, the emphasis is on cash flow rather than on revenue and expenses.

MATCHING

Match each term with its definition by writing the appropriate letter in the space provided.

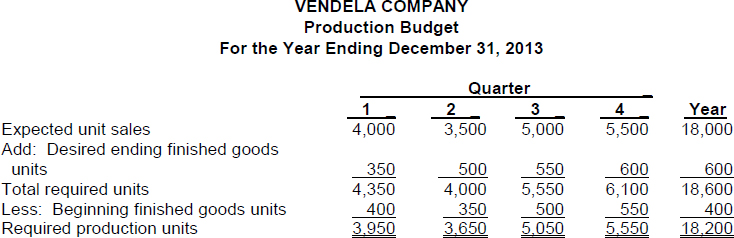

EX. 21-1 (L.O. 3) Vendela has the following sales budget for the year ending December 31, 2013:

On the basis of past experiences, Vendela Company believes it can meet future sales requirements by maintaining an ending inventory equal to 10% of the next quarter's budgeted sales volume. On January 1, 2013, Vendela has beginning finished goods of 400 units. Vendela expects sales for the first quarter of 2014 to be 6,000 units.

Instructions

Prepare a production budget for Vendela Company for the year ending December 31, 2013.

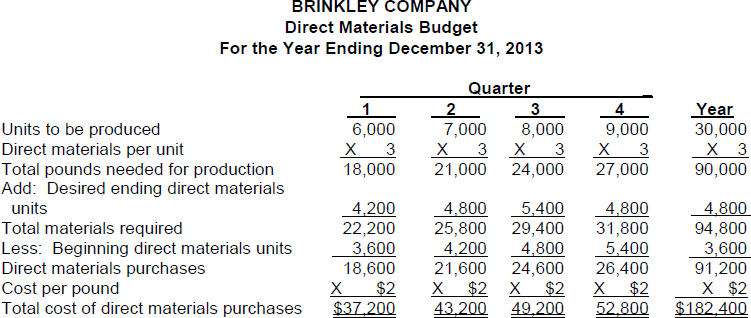

EX. 21-2 (L.O. 3) Brinkley Company's production budget for 2013 by quarters is as follows: (1) 6,000, (2) 7,000, (3), 8,000, and (4) 9,000. For the first quarter of 2012, the budget is 8,000 units. The manufacture of each unit requires three pounds of direct materials and an expected cost per unit of $2. The ending inventory of direct materials is expected to be 20% of the next quarter's production needs. At December 31, 2012, Brinkley had 3,600 pounds of direct materials.

Instructions

Prepare a direct materials budget for Brinkley Company for the year ending December 31, 2013.

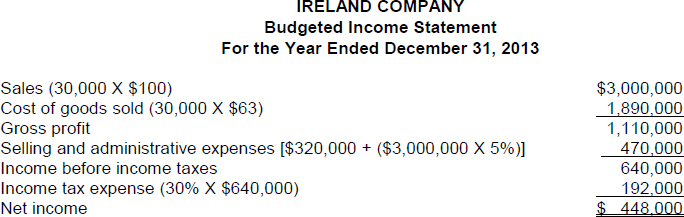

EX. 21-3 (L.O. 3 and 4) The Ireland Company has accumulated the following budget data for the year 2013.

- Sales 30,000 units; unit selling price $100.

- Cost of one unit of finished goods; direct materials $15, direct labor $30, and manufacturing overhead 60% of direct labor cost.

- Selling and administrative expenses: variable 5% of sales, fixed $320,000.

Instructions

Prepare a budgeted income statement for the year assuming an income tax rate of 30% on income before income taxes.

SOLUTIONS TO REVIEW QUESTIONS AND EXERCISES

| 1. (F) | The budget itself, and the administration of the budget, are entirely management responsibilities. |

| 2. (T) | |

| 3. (F) | A budget is an aid to management; it is not a substitute for management. |

| 4. (F) | Management acceptance of budgets occurs more frequently when the flow of input data is from the lowest level of responsibility to the highest level of responsibility. |

| 5. (T) | |

| 6. (F) | The budget committee is usually made up of people inside the organization such as the president, treasurer, chief accountant (controller), and management personnel from each of the major areas of the company. |

| 7. (T) | |

| 8. (F) | Budgeting is concerned with meeting annual profit objectives. Long-range planning involves the selection of strategies to achieve long-term goals and the development of policies and plans to implement the strategies. |

| 9. (T) | |

| 10. (F) | The production budget is derived from the sales budget. |

| 11. (F) | The production budget shows only unit production data. |

| 12. (T) | |

| 13. (F) | The direct labor budget contains both quantity and cost data. |

| 14. (T) | |

| 15. (T) | |

| 16. (T) | |

| 17. (T) | |

| 18. (F) | In service enterprises, the critical factor in budgeting is coordinating professional staff needs with anticipated services. |

| 19. (T) | |

| 20. (T) |

MULTIPLE CHOICE

MATCHING

- e

- d

- j

- g

- i

- h

- f

- b

- k

- l

- c

- a

EX. 21-1

EX. 21-2

EX. 21-3