CHAPTER 4

Assessing the Subject Company

This chapter addresses the information collection and basic analysis of the subject company. A firm understanding of the company, supported by documentation, is necessary in order to effectively make comparisons under both the income and market methods. What we are really assessing is, according to Eddie Davis: “people, processes, and profits.”

No matter how complex a company or situation may seem while working through a valuation, when complete, the valuation analyst should be able to provide a concise and clear analysis. If the analyst cannot do that, then more work is needed. Being able to simplify is a major indication that you are achieving the Art of Business Valuation. Companies are people, processes, and profits. This chapter is about understanding the company.

DOCUMENTS NECESSARY FOR A BUSINESS VALUATION

An engagement to estimate value results in either an opinion or conclusion, or a calculation. In all these cases, the estimate needs to be based on the combination of facts and the opinions of key people inside and outside the company, the assumptions provided to the valuator as well as the assumptions made, and estimates performed by the valuator. Here we are going to look at the documents, forms, and possible interviews used to build a foundation for the statement of value.

Sample Detailed Document Request

A detailed document request could be worded like this:

We have been engaged to prepare a valuation. Please provide all information requested below. If the information does not exist, please note on the form and return with the information. Thank you for your patience and assistance.

- Brief history of the company

- Last 3/5 years tax returns with all schedules including depreciation schedule

- Last 3/5 years financial information including:

- income statement

- balance sheet

- statement of cash flows if prepared

- audit/review/compilation report, notes and schedules, etc., if prepared.

- Internal year to date financial statements with prior year comparison data

- Trailing twelve months (last twelve months) income statement if available

- Current accounts payable and accounts receivable aging

- Copy of all notes payable

- W-2s or 1099s for owner and/or key manager

- Equipment list with estimated current market value

- List of top 10 clients and last year's revenues from each

- Summary of key customer or supplier contracts, including term, minimum and maximum amounts, classifications of owner/company if applicable, extensions (particularly important for government contractors, may be referred to as “vehicles”)

- Work in Process or Work in Progress (WIP) schedules if used by industry, company (construction contractors, software writers, some manufacturers)

- Business plan

- Cash flows, budgets, forecasts, projections for future, current and past 3 years

- File copy resumes of owners and top tier employees along with organization chart

- Breakdown and back-up for

- all compensation to owners

- all compensation to owner's family

- all benefits to owners

- all benefits to owner's family

- all duties and time spent for owner's family.

- Unusual one-time charges (e.g., large one-time legal expense)

- Copies of LLC operating agreement or all corporate charter information, by-laws, and minutes

- Any buy-sell agreements or shareholders agreements

- Related transactions details

- Any purchases or sales of stock

- Information on Key Man life insurance policies

- Real estate leases

- Appraisals of the real estate used if owned by an owner of the company or the company

- Franchise documents and, if for a sale, prospective franchise documents for buyer

- Any franchise industry analysis or information provided in last 3–5 years

- Any valuation performed within the last 5 years

- Information and back-up on any:

- advantageous or disadvantageous contracts

- contingent or off-balance sheet liabilities or assets

- trademarks or other intellectual property

- litigation

- information on prior offers or sales of stock or LLC interests

- if in construction or manufacturing, bid waterfalls, contract backlog reports

- Web URL

- Anything you feel would materially affect the value of the firm

- Completion of questionnaire form

Subject Company Backbone or Primary Documents

Subject company backbone documents are those documents that provide the framework of the business valuation. They are the starting point of the analysis. They provide documentation to build a historic financial model of the subject company. When collecting the documents and entering and reviewing them, remember the following:

- What is the likely cash flow that is going to be chosen for modeling and comparison?

- What are the likely valuation methods that will be used?

- What information is needed to create a reasonable comparable subject company based on the above two criteria?

- What is not being asked for or looked at that could materially move the needle up or down?

- Has a reasonable level of support documentation been requested, particularly for add-back adjustments?

- Does this make sense?

Now a little more detail on key documents. Many of these documents are addressed in much more detail in Chapter 11, “Accounting Issues with Small and Very Small Businesses.”

- Tax returns. For many small and very small businesses this is often the only financial document that has been reviewed by a third-party financial person. Sometimes even these are prepared by the owner. Fortunately, that is rare. Because they are examined by an independent or semi-independent person and because they are filed with the government, they have the presumption of being the most accurate and useful source of financial data in most cases. They sometimes are still wildly wrong. Examples of errors include no opening inventory (but they purchased and sold inventory over the year) when a company with inventory was purchased. Inventory starting and ending amounts that never vary. Uncollectable accounts on accrual basis that have never been written off and are far in excess of the contra account. The list goes on and on.

- Internal financial statements. Larger businesses will have both financial statements and tax returns. Many small businesses really do not. Usually the accountant will make year-end adjustments so the tax returns and the financial statements tie together but not always. Balance sheets tend to be less complete than income statements. Ask for both. If the tax returns appear in order and were prepared by an outside firm, that is likely to be the best data available.

- Compiled, reviewed, or audited financial statements. Few small companies have audited financial statements. Those with loans or bonding may have reviewed financial statements. Where available, notes attached to properly prepared audited or reviewed financials or occasionally compiled financials are one of the most useful sources of data available. In some cases, notes are more useful than the financial statements as they provide clarity about the stated amounts and many details on operations and liabilities. This quality financial statement is a luxury. If these statements (particularly reviewed or audited) are accrual-based and the tax returns are cash basis or quite different, the valuation may be based on these statements and not tax returns. Audited financials are better than tax returns. They are just as rare as hens' teeth with small and very small businesses.

- Forecasts. If the company has forecasts, this may become a backbone document. They should be requested in all circumstances. Most small businesses will not have forecasts. In general, that is OK. Review of forecasts is covered in greater detail later in the book.

- Discretionary and other add-back questions and support. Many small businesses bury or hide their discretionary owner's expenses/benefits. Seller's discretionary earnings (SDE) is the most important cash flow figure with small and very small businesses. These expenses and adjustments may not be easy to find. Ask for a chart or list of owner benefits and perks. It is common to require additional follow-up support documents for these adjustments.

- W-2s or 1099s for owner, owner's family, and/or key managers. If the owner's salary is not shown as a breakout (or if all owners' salaries are not shown), the W-2 will provide salary support. If the owner is not an owner/operator, then often the key manager's compensation can be substituted for the owner in the seller's discretionary earnings formula. While salaries are not supposed to be paid to partners in partnership returns, many small business owners take a salary and pay payroll taxes. Do not assume there is no owner's salary with partnerships just because it is not clearly shown. Guaranteed payments can be treated as salary when shown for partnerships. Technically guaranteed payments is a distribution.

- Accounts payable and accounts receivable agings. These are helpful to understand cash flow and working capital for both cash and accrual accounting methods when available. Sometimes with accrual-based accounting, you will find old receivables that are uncollectable and not written off. Similar but rarer are old accounts payable that were expensed but never paid and will never be paid. Depending on the details, these can call for adjustment.

- Questionnaires. Standards bodies require management interviews. Questionnaires provide consistency and an efficient way to start or do a management interview. These will be covered in greater detail in the next section.

These documents provide the information to determine cash flows and make adjustments so the comparables and the subject company are using comparable measures for cash flow. The data will also be valuable in assessing the quality of the company as it compares to the comparables under the market method. The income method uses the same processes to adjust cash flows.

OTHER DOCUMENTS FOR DETERMINING ENTERPRISE VALUE

Enterprise value is the value of the company itself. It is equal to the value of a 100% interest in the stock or assets of the company.

- Top 10 client list. This provides the analyst with a better understanding of customer concentrations. If the business has strong repeat customers, generating the list over 3–5 years to show consistency of customers is also strong evidence of continuing relationships. Continuing relationships are evidence of better-run companies in many industries.

- Real estate lease. Many businesses have advantages due to locations, low lease rates, or special build-outs, making the lease assignability and extensions a key to value. While often the lease assignment or extension will be assumed, for many purposes, issues surrounding the lease term and assignability can greatly diminish value. The lease should be reviewed to see:

- What is the term of the lease?

- Are there extensions or options to continue at the will of the tenant?

- If close to the termination date, have notices been given?

- How is rent determined at an extension

- a continuation of the historic rent increases?

- a larger automatic increase?

- an appraisal or other negotiation with no cap?

- Is the lease assignable?

- What is the history of the landlord with assignable or more so, unassignable leases?

Lease terms need to be reviewed. In one mall lease, the business had agreed to give 10% of the sales price (not equity after debt) to the landlord. In another retail lease, rent went from $100,000 per year to $150,000 at the extension. Other landlords are known to not cooperate with assignments, no matter what the lease says. These are difficult matters that greatly impact business value for businesses with advantages due to location or rate.

Finally, is the company subject to percentage rent? These are common in malls and high end retail locations. In those cases, ask if the landlord has performed an audit or if the client prepared an excess revenue worksheet to calculate additional rent.

- Franchise agreements. Transferability, including franchise transfer fees, can greatly impact value. More and more franchises are charging almost as much to transfer between owners as to start a new unit. Another wild card is the cost to upgrade facilities at the time of transfer. Upgrades can sap the value of many smaller franchise operations like sub-shops. Further ongoing fees should be checked against the financials to ensure they are consistent with the documents. Sometimes the old fees are not consistent with new fees. Finally, franchisors often have rights of first refusal and approval rights at time of sale. These too can impact value as they add time and sometimes reduce buyers. I have seen these rights exercised very late in the sale process. Do not assume the franchisor will not buy-in the unit without investigation.

- Other contracts. If the firm relies on one or two contracts for either supply or customers, these should be obtained. Time periods that the agreements remain in place need to be noted. This can be particularly important with government contractors and construction contractors. It is very important to know the type of contract, how long it extends, extension options, and terms, or if the contract was based on an owner status, such as disabled veteran or other.

- Employment agreements. Employment agreements of shareholder officers, key management, and perhaps other employees can contain non-competes and other restrictive covenants. Frequently the officer may be required to sell his or her shares of stock if employment terminates.

- Lending documents. Larger loans can contain loan covenants that specify requirements that the business has to meet. If the business does not meet them, interest rates can increase or the loan may be called. Also, in some industries like construction, be aware that short-term lines of credit may be called in recessions when they may be needed the most. (Early in my career as a homebuilder, I was given this advice about bankers. This advice has never failed me, “A banker is someone who gives you an umbrella and when it starts to rain, they ask for it back.” Remember that for yourself and your clients.)

- Equipment leases and financing agreements. For many small businesses these payments can be substantial. They often also tend to slip past the request for all liabilities. Double-check if these exist and are properly shown on the financials. Even if they are not required to be shown on the financials, make sure they are in the cash flows.

- Work In Process or Work In Progress (WIP) schedules. For contractors and some large item manufacturers, work in process is an inventory category and the schedule is an effective tool for measuring job progress, backlog, profitability, and the like. Comparing WIP schedules over time can be quite useful to see trends.

- Bid waterfall. Organized contractors maintain data on prior bids and bids outstanding, along with a ranking of future likelihood based on past results with the contracting company and type of work. Often they will not provide it in sales situations out of fear of misleading the valuator as relationships and markets can change quickly. But, when available, they provide insight into the possible future.

- Contract backlog. Evidence of future work is an important indicator of value.

Most of the remainder of the documents on the list relate to valuing interests which constitute less than 100% interest in the company and will be discussed in Chapter 9, Valuing Partial Interests in a Business.

Add-Back Documents

Creating an apples-to-apples cash flow is a major component of doing a business valuation. Here we will list a few documents that may be required to verify add-backs. In general, if the valuation is a calculation, for internal use, and is not for dispute purposes “taking the seller at his word” is often acceptable. Do properly document the level of documentation and examination you are performing in your engagement agreement letter and report. Make your level of examination clear in the report also, just in case the report is given to a third party. Clarity is a valuator's best defense.

This list is assuming there is not a situation requiring forensic accounting-type work which is not covered in this book. Do note that the American Institute of Certified Public Accountants (AICPA) Statement on Standards for Forensic Services No. 1 becomes effective for engagements accepted on or after January 1, 2020. If an engagement is for litigation or investigation purposes, review and comply with the new standards.

- Salary related. W-2s for owners, if not shown on the tax return. W-2s for managers and family members, as applicable. Payroll reports for year to date as necessary.

- Other family benefits. If family members work at the business, develop a chart of titles, tasks, hours worked. Obtain 1099s or W-2s. Make reasonable estimates of the true economic value of the work performed and the profit distribution portion. A sample of an analysis of family benefits is shown in Table 4.1.

- Auto expenses. If the business really is not reliant on transportation, often the shown auto expense can just be added back. If the business does have delivery or other transportation expenses, then an understanding of how they are assessed is necessary. Verification documents will vary but could include credit card payments and statements, mileage information, number of vehicles, and who uses them. Document what is said and use reason and judgment. In general, few people will argue that an owner-used company car is worth $5,000–$7,000 or so between gas, maintenance, insurance, and so on. Sometimes it is reasonable to plug a figure like that if the accountant left the expenses in the tax return. Again, depending on the purpose, in some cases, if a “personal” auto is owned by the business, the cost of the auto and depreciation should also be removed from the balance sheet.

- Debt payments, including auto loans. Take care to check that loan principal is not being added back. Many owners and untrained bookkeepers do not understand that principal is not an expense in financial statements. Usually, but not always, if an outside accountant is used for tax returns, they will have corrected this. As a final check, when material, obtain the lender's payoff statement (sometimes the remaining balance is shown on the payment statement) for the loan and tie into the balance sheet.

- Meals and entertainment, travel, etc. Usually add back 50–100%, depending on the fact pattern. Rarely is additional support necessary unless amounts are very large or it is a divorce or litigation situation requiring forensic work.

TABLE 4.1 Sample Family Add-back Chart

Name Relation Title Salary Employer Payroll Tax Auto Health Ins 401(K) Other Total Benefit Estimated Labor Value EBITDA Adjustment SDE Adjustment Mary Smith Owner $100,000 $8,000 $10,000 $20,000 $5,000 $10,000 $153,000 $150,000 $3,000 $153,000 Sam Smith Spouse Bookkeeper $50,000 $4,000 $10,000 $2,500 $5,000 $71,500 $20,000 $51,500 $51,500 Tammy Smith Daughter Labor $45,000 $3,600 $5,000 $2,200 $55,800 $12,000 $43,800 $43,800 Theo Smith Son Driver $65,000 $5,200 $3,000 $73,200 $50,000 $23,200 $23,200 Notes: EBITDA Add-Back $121,500 SDE Add Back (Includes all of Mary's compensation unless already added back elsewhere) $271,500 It was reported by Mary Smith that: Sam Smith works on Saturday putting the books together. Payroll is done by an outside service. Tammy Smith is at college four hours away and works about 3-4 months per year. Theo Smith graduated college last year and does a variety of things. It is hoped he will stay. Notes:

This is viewing all benefits as part of compensation. Often each benefit will be added back and just salary adjusted.

Estimated Labor Value Calculations–pull data from Census or other source along with local knowledge

Mary Smith - This $3,000 adjustment would only be made for EBITDA. Using SDE, her entire compensation is an add-back.

Sam Smith - 8 hours a week times $40 per hour times 52 = $20,000.

Tammy Smith - 8 hours a day $16 per hour 90 days per year = $12,000

Theo Smith - Maybe the most difficult as it is unclear what his role really is. Likely to depend on starting pay scale in industry.

- Health insurance. Obtain payment statements to verify total monthly payment. Ask what percentage is paid by the company. Verify that it was not removed from the statements you are using as a basis for the valuation. Health insurance is complex and changing and treatment on tax returns for owners varies over years and entity types.

- Credit card statements. Generally, the statement must be examined. For most businesses, Victoria's Secret is an add-back. Home Depot for a contractor would be difficult unless delivery tickets or work order to personal home or office, and so on.

- Vacation home, other personal items, children's schooling, mistress, etc. Not getting into morality, the mistress's apartment in New York City is probably an add-back.

QUESTIONNAIRES AND MANAGEMENT INTERVIEWS

Questionnaires and management interviews are where the valuator really learns what is under the hood of the business. I refer to many of these factors as “soft” factors. Soft factors tie into motivations, culture, attitude and can be difficult to understand and quantify.

The financial information is a type of score. It indicates success or failure financially. The ability to quickly obtain clear financial information is also an indication of organization and effective business processes. Certainly, the old adage that “success breeds success” applies, yet the continuation of success into an uncertain future depends on many factors including soft factors. Those internal factors are learned by asking questions and listening to understand how the company really works.

Every valuator tends to use their own questionnaire. Several different forms and formats are provided on the website for this book. There is always a conflict between the amount of information the valuator would like to obtain and what the small business owner is willing and able to provide. In many cases, if you ask for too much, you end up getting nothing. Remember at all times, businesses are people, processes, and profits.

Does the business have a culture of: “forever and continuous improvement” or “resiliency in the face of problems”? These two factors often are the biggest indicators of future success or failure. They are also cultural matters that may be hard to quantify.

For small businesses, the following seem to be the major areas of emphasis:

- Company history, including start date, dates of ownership changes, timeline of major changes in products, services, business policy that made a difference

- Business culture, mission statements, employee handbooks1

- Current industry, products and services, unique niches

- Competitors and changes in market

- Sales and marketing methods

- Customer, supplier, referrer or other concentration

- Bid or sales waterfalls, backlog

- Licenses, permits, bonding issues

- Contingent liabilities not on the books, disgruntled former employees, union pension liabilities, customer complaints

- Organizational structure chart and key people. Number of full-time and part-time people at supervisory and production levels. Time with the company and likelihood of staying in future. This is often supplemented by a website or resumes if they exist.

- Human resource issues, union, unemployment and workers compensation, insurance matters, lawsuits, compensation and raise policies, benefit package

- Are key people independent contractors or employees? How is this impacted by employment tax law? Is this normal in the industry or a reason to be concerned?

- Processes and systems used in all areas of the business

- Are there commodity pricing risks or other “uncontrollable” parts of the revenue/expense chain?

- Intellectual property, trademarks (often very little and it is relatively unprotected)

- Accounting policies, cash, accrual or tax basis, attitude to personal expenses, cash handling processes

- Owner and owner's family personal benefits and add-backs

- Organization type and tax status. State tax issues, particularly if multi-state.

- SWOT analysis: Strengths, Weaknesses, Opportunities, and Threats

- Overall assessment of the last few years and some years in the future.

In every instance, the history and policies of the company are important. But, the fact is, the most important thing is what the foreseeable future is going to look like. How are these policies, people, processes, and so on going to impact the company over the next few years?

These items need to be reviewed against the following screen:

- Does this business have a defensible market position?

- “Working harder” businesses or “trains run on time,” namely, we out-hustle the competition can be very good businesses. They tend to be very dependent on culture and/or the owner/manager as a hustle and work ethic is a human resource. For this reason, they often have lower multiples. This can particularly be the case with businesses which often have HR/personnel issues, like restaurants, auto repair shops and the like.

- Sticky businesses with continuing income streams like service mechanical companies, software as a service, and other recurring income streams often receive a premium.

- Are there customer concentrations or supplier concentrations? What is being done or can be done to reduce these risks?

- Does the company have systems in place?

- Quality systems are “when average people get extraordinary results every time.” Use this as the standard to determine systems. One indicator is if there are, “lots of reasons why things are not working,” generally, their systems do not work.

- Are proper systems in place to control cash, inventories, production, including production of services?

- Is the sales and marketing process stable or growing the business? Is it all based on the owner or a single salesperson?

- Who are the people running the systems?

- Even quality systems need trained qualified people. How does the company obtain, retain, train people?

- Are there key people in place? What are the tenure and likely future for these people?

- Are they subcontractors, contractors, or employees?

- Is the culture a “can-do” culture or other?

- Does the owner have the ability to continue growing and adopting or is the owner reaching their maximum capacity and/or interest?

- Does the company have other sources of resiliency that will allow it to survive as business continues to change?

- How does this fit within the industry and economic outlook?

- How does the company fare against “the Amazon effect,” namely, ever-changing technology? (Although it seems to the author that Amazon is just a modern Sears Catalogue company.) These changes have been very detrimental to newspapers, taxis, retailers, distributors without a service component. It was recently reported that phone apps have started to replace some advertising premiums.

Again, will the people, processes, and profits in place promote the growth or retraction of cash flows for the business in the foreseeable future?

Questions that may be helpful for major important areas in most companies include:

Product/service

- What are the products or services provided by the company?

- Does it serve a very narrow niche or is it a broad base?

- Does the company have systems to improve the products and services?

- Is there an ability to change the products and services?

- What does the company do so well that the market allows them to make a profit?

History of the firm

- What is the story?

- How long has the business run substantially as it does today?2

- What need was being met?

- Have the primary services or products changed?

- What does the chain of ownership look like?

- Does the firm have a history of litigation, labor problems, and other risk indicators?

Systems

Quality systems are when ordinary people get exceptional results––every time.

Richard V. Caruso

Businesses have many systems, most of which are rarely thought about but each of which is necessary for the company. In each case, how does the company document these systems (usually orally in small businesses) and train the people who run them? Understanding this is essential to understanding the resiliency of the company. Figure 4.1 is a list of systems that exist in a typical business.

| Product and Service-Related | |||

| Product development | |||

| Cost estimating | |||

| Bidding | |||

| Purchasing / buying | |||

| Contract negotiation / administration | |||

| Testing | |||

| Accounting | |||

| General Ledger | |||

| Accounts Payable | |||

| Accounts Receivable | |||

| Payroll | |||

| Job cost / Product sales & gross margin | |||

| Tax preparation | |||

| Regulatory requirement data collection | |||

| Sales and Marketing | |||

| Advertising placement and evaluation | |||

| Lead collection / CRM or other tracking | |||

| Website | |||

| Events, other marketing | |||

| Sales | |||

| Order taking | |||

| Delivery | |||

| Production | |||

| Receipt / storage | |||

| Production / processing | |||

| Quality control | |||

| Packaging | |||

| Delivery | |||

| Human Resources | |||

| Hiring | |||

| Compensation | |||

| Review | |||

| Promotion / Release | |||

FIGURE 4.1 Systems in a Typical Business

Sales and Marketing

In small companies these are often combined. How are new customers attracted? Advertising, word of mouth, commission, independent contractor, salespeople? Some companies and industries are very sales-oriented, such as mortgages and specialty products. Others such as institutional food service and many distribution companies are very customer service-oriented.

How does the business retain and attract customers? Is the pipeline managed or is it more haphazard?

People

The value of most businesses goes home every night. Even most commodity businesses require service. Service requires people. Many small and very small businesses are labor suppliers for larger businesses.

How does the business attract, obtain, retain, train people? What do the results look like? Some industries and businesses have constant turn-over. Others are quite stable. How does the company compare to the industry?

Is there a culture of forever and continuous improvement?

This really gets down to the culture. Is the culture open, caring, can-do? How does this tie into results and how will it facilitate or hobble the future plans for the business? Employee energy along with a can-do attitude has gotten many companies through tough times and eventually into high profits. This can be a key factor.

Key management team. All employees are important in small and very small businesses. As the businesses grow, the management team becomes more important. Often in small businesses, the “management team” will be an administrator who handles purchases, a bookkeeper accounts receivable/accounts payable (A/R A/P) clerk and a salesperson or two.

It is important to know the age, health, and likely retirement of the management team. Often management teams are about the same age as the owner. If they are all retiring when the owner does, this can be a problem. For instance, a family business consisting of three brothers, one wife, and son, who are the management team of a small mechanical contractor, will have a problem as four of the five managers intend to retire within a year or two of each other.

Is there an up-and-coming “star” in the management team? Sometimes small companies sell for a premium because they have extremely talented sales or technical talent that is staying.

The likelihood of the management team staying with a successful business at a sale is a major factor in the value. Marketability even of a 100% interest is greatly reduced if there is no transition team staying with the company.

Facilities and Equipment

Facilities and equipment generally form a straightforward category. It is the stuff used by the people and systems to produce or distribute the goods and services. Important factors to consider are:

- Age and remaining life on equipment

- Capacity of equipment – if capacity is reached, what are the upgrade costs?

- Maintenance costs and maintenance practices to extend equipment life

- Possible obsolescence of equipment, particularly before leases or loans are up.

As an example, if the company has five trucks and they are varied in age and mileage, that should not cause an adjustment. If the company has five brand new trucks that could cause a small upward drift in value but probably not nearly enough to pay off the loans if the trucks were financed. If the company trucks all need replacement, that will lower value.

Facilities, particularly real estate, can affect a company in several ways and need to be investigated. Some companies have very favorable locations. Convenience stores, gas stations, and the like require long-term leases or owning the real estate to maintain value. They are clearly location-dependent. Others, while less clear, gain significant advantage by facilities location, such as some construction companies with yards close to major cities cutting transportation costs and driver labor, and companies with under market lease rates locked in. Some companies have an unusual build-out that would be costly to reproduce, such as bowling centers.

At the other extreme are companies that have long-term leases that a buyer would want to extinguish. Industrial, distribution, and service operations often consolidate locations to reduce overhead.

These changes may or may not be synergistic. Use of these facts will depend on the overall fact pattern, standard of value, and purpose.

Technology

Technology is affecting every business differently but it is affecting every business. A few pointers on different things seen in different businesses:

- Software. The movement to the Cloud is making the transfer of software at closing simpler. New issues are constant updates, security, backup, and what happens when the Cloud goes down or is locked up for “ransom”?

- ERP (Enterprise Resource Planning) software can help small businesses by providing a framework and standardization.

- Quickbooks is a mixed bag. It has simplified accounting but has also made it much easier to do things wrong.

- Does the company have a somewhat unified system or many separate systems?

- Is there an industry standard and a strong reason to use the standard? For instance, larger government contractors tend to use Delteck ERP and accounting software. If used by the subject company, this will allow for simpler integration of the company when sold.

- Integration with suppliers and customers. Larger customers and suppliers now require working through their systems. How does that affect the company?

- The Amazon effect. Is there something on the horizon that will change the whole industry or supply chain or customer relationships for the industry? What is the prognosis for the industry for the foreseeable future?

- Obsolescence. At various times new equipment that is cheaper to buy and use has come out that replaces earlier versions, causing substantial losses to companies. An example is CAT scan machines in radiologists' offices around 2010. New equipment came out and lowered reimbursement rates for CAT scans below the cost of operating two-year-old CAT scan equipment that cost $1,000,000 each with five-year payment plans. Needless to say, this created substantial one-time losses for those businesses.

Concentrations

Concentrations kill. Concentrations are the main reason why small businesses are so much riskier than larger businesses. A large customer or supplier or other concentration can cause major disruption and bankruptcy when relationships end. Small and very small businesses have all sorts of concentrations. Some almost by definition, others by choice. Many concentrations are unavoidable at least for periods of time.

- Customer concentrations. Industries where larger jobs are common, such as construction or software writing, are rife with this. Quality companies show a history of starting new jobs and relationships as old ones end. This greatly increases risk. Finally, there are small consultants and construction subcontractors who may only have one customer. In some small markets there may only be one or two primary customers. Great risk.

- Product concentration. Small companies may only have one or a few primary products putting them at risk of change of the product, supply chain, and so on.

- Supplier concentrations. Sometimes the company only has one or two suppliers for critical goods. Or perhaps the company is essentially a sales agent for one company. Can the supply be replaced quickly and cost effectively?

- Referral concentrations. In some cases, the company may have many customers but they only come from a few defined sources. Internet sales can come this way. For instance, if key words are used as a primary marketing means and they become too expensive. Or the engineering firm that has many customers but they all come from two or three architectural firm referrals. This can be harder to learn about and adjust for but can add just as much risk to the equation.

- Key people concentration. Almost impossible to avoid in small business. However, it greatly increases risk vs. a department of people with similar skill sets. Look for non-competes or non-solicits and/or employee contracts from/with key salespeople and top management. These do provide some protection from key people leaving immediately with other staff and customers.

- Commodities concentration risk. Transportation companies gain and lose profitability with fuel costs. Shippers that focus on one product carry risk if the product price or desirability changes. Lumber yards, concrete suppliers, junk yards selling scrap metal may have commodity price and sometimes availability issues.

Site Visits

Site visits are an underutilized tool. Site visits are expensive and sometimes just not feasible. But a site visit can tell the valuator a great deal about the company. Particularly when the company is in full operation, the look and feel of the company can provide a greater sense of underlying company behavior than many days of financial analysis.

Preparing for the Site Visit. Often site visits are broken down into three parts. Meet and greet, the tour, and technical questions. Prior to the site visit, whenever possible, all financials should have been reviewed. The company information should be compiled and reviewed. Often a first draft work product may have been developed. From this work, general and specific questions can be developed for the visit.

Things to look for:

- Where is the business located?

- Are there logistical or permit reasons for the location?

- Would this place make employees and customers feel good?

- Is it clean and safe?

- Entering the business

- Is the appearance clean and organized?

- If a company/industry that receives people at their offices, are the reception area and greeting proper?

- Tour

- Again, is there a logical organization?

- Are things clean and organized?

- What is the feel or “energy” of the management and staff?

- Are equipment and means of production current?

- Is the equipment maintained?

- Is inventory adequate and safe?

- What is utilization of the equipment and space?

- Questions

- Ask technical questions

- Did anyone else participate besides the owner?

- Does there appear to be management depth?

- Overall, how did the visit go?

One sign of organization is if companies can get backup and detail in a reasonable timeframe. If every request requires building a spreadsheet from scratch, the company probably does not have proper organization in place (or you are asking for unimportant information).

Take notes through the interview. Remember nonverbal cues and look and feel and energy in a room often can say more about a company than questions and answers.

Skipping the Site Visit. Many businesses do not require a site visit to value them fairly. When performing a conclusion of value, if this step is not taken, it must be noted in the report. Small engineering firms, accounting firms, other firms located in offices may not require a visit. A franchise that must follow standards may not require a visit.

In the modern world many elements of a site visit can be duplicated. Google maps can show the location and street views for most businesses. Many retail businesses have pictures of inside the shop and many reviews. Menus, price lists, and other information can be listed on the website. Yelp, Facebook, and Google will often have rankings and references. These certainly tell you something.

Questions and answers can be handled over the phone or using a video service like Zoom. The main thing that is missing is being able to gauge the energy of the firm. Happy people and good energy somehow solve many problems that come up in business. Combine that with earnings and you have a powerful combination.

Ranking Strengths and Weaknesses

It is important to take the time to review the critical strengths and weaknesses of the business. Some businesses and certain industries are driven by different skill sets than others. Does this business have those skill sets? That would be a clear strength. A second way of looking at it is: What are the one or two critical factors that allow this company to compete? For example:

- Does it import parts for a low cost?

- Does it have strong goodwill with customers?

- Does the company have IT that creates efficiencies?

- Is the culture strong?

Weaknesses come from concentrations and limitations of all sorts:

- Is the business dependent on the owner/personal goodwill?

- Is the business dependent on other key personnel?

- Does the company have supplier or customer concentrations?3

- Is technology changing supply or sales chains?

Of note: What are the strengths?

- One or two people's brilliance may indicate transferability issues. If the key to success is that the team works harder, that can wear out over time or change when leadership changes. These are important strengths but may not give maximum value. If the strengths are more protectable, such as true trade secrets, or lower production costs, integrated and sticky systems with customers, then the strengths often create more value.

Typical strengths and weaknesses are shown in Figure 4.2.

| Possible Strengths | Possible Weaknesses |

| High revenues | Low revenues |

| Gross profit margin | Low gross margin |

| Profit margin | Low profit margin |

| Low cost suppliers | High costs |

| Market leader products | Generic products |

| Supply contracts | Unstable supply |

| Franchise name & relationship | No name |

| Relationships with …. | No relationships / unproven |

| Customer agreements | |

| Technology | Industry technology threats |

| Equipment | Worn equipment |

| Patents, licenses, etc. | |

| Limited competition | Easy entry / lots of competition |

| Trained workforce | No available talent |

| Managers, others with upside / long careers | Old management close to retirement |

| Sales system | Owner salesperson or sales in spite of self |

| Manufacturing system | Too much personal goodwill |

| Location | Concentrations of any type |

| Non-solicits, non-competes | Problems with staff / contractors |

| Positive enthusiasm, energy | Lawsuits |

| Barriers to entry |

FIGURE 4.2 Possible Strengths and Weaknesses

In most instances the analyst will select two to five strengths and the same range of weaknesses. These should be weighted heavily later in the process when selecting the multiplier or capitalization rate. The analyst can also provide strengths and weaknesses in each section of the business description.

Another way of presenting company strengths and weaknesses is shown in Figure 4.3 which is at the top of the next page.

DEAL KILLERS

The name is a bit of cliché but the following are items that can quickly reduce value and need to be investigated. Often they only last a year or two and in many cases they are eventually resolved. Yet, during the time they exist, they may cast a blight over the company and significantly reduce value.

- State tax issues. Very small companies may not have state sales, employment, and income tax issues in multiple states. But with the spread of virtual workers and the ability to sell over the internet, many more companies are facing potential penalties and taxes from multiple states. The Wayfair case4 has expanded the definition for having a nexus in the state. Once a company has a nexus in a state, it can be sued and taxed by the state. Many small business owners do not realize or choose to ignore nexus issues and the related sales tax, income tax, and payroll tax issues. If they are not addressed, they can become significant when penalties and interest are included and reduce value. Transaction due diligence over this issue has become heightened in recent years.

Strengths / Weakness Factors Comments Increase or Decrease Profitability History of Growth / Stability Concentrations Owner Transition Systems Key People Workforce Location Equipment Goodwill / Customer Relationships Goodwill / Supplier Relationships Other Risks / Opportunities FIGURE 4.3 Company Strengths and Weaknesses

- Lawsuits. Lawsuits happen to companies. The pall they cast is usually much greater than the actual risk. Nonetheless while lawsuits are proceeding, particularly those for large dollar amounts that may not be fully insured, value is often reduced and marketability is affected.

- Inability to extend or renew real estate lease. Location-dependent businesses that cannot get lease extensions or assignments lose significant value until the problem can be resolved. Sometimes it cannot be resolved as the landlord wants to take over the business, take the profit from the transaction for himself, or change the use of the property.

- Licensing issues. Many businesses rely on licenses to perform their operations. If these are in jeopardy or become non-transferable, value can quickly diminish. While bars and restaurants losing their liquor licenses is common, this issue extends to many businesses with many levels of permits. Water discharge permits, zoning and occupancy permits including grandfathering restrictions, hazardous waste permits, professional licenses of all types, interstate and intrastate hauling road permits, bridge over-weight truck permits.5 The list is long.

- Government regulation/certifications. Beyond licensing issues many small and very small businesses provide goods and services to various governmental entities. These governmental entities often have guidelines to promote small business, women's, veterans, minority participation, and other groups in their communities. These certifications can greatly increase the revenues of the business but in many cases those revenues and contracts can only be assumed by companies or owners who can obtain similar certifications. Since the classifications and certifications are generally for disadvantaged groups, it is logical that in many cases this will reduce the marketability of the company verses companies in the same industry without classifications. An extreme example of this is the 8(a) Disadvantaged Certification. Under that certification, certain qualifying minorities and disadvantaged people are able to obtain contracts at advantageous rates. But, the certification only lasts nine years with three additional years to complete contracts.6 The statistics for companies staying in business at “graduation” from the program are terrible. It is reported that two years after graduation, 90% of the companies are out of business. This is something that must be factored into a valuation of an eight-year old 8(a) company.

- Internal disputes. Internal disputes between owners is a major source of disruption and loss of value for small and very small businesses. Many companies are formed without proper documentation and thought as to the long-term relationships between owners. When situations change, there is no guidance or rules and a stalemate can ensure. Worse yet, one partner leaves with all or part of the business. Larger businesses have the momentum to survive these conflicts. They also have rules and agreements in place. The lack of proper documentation in the form of buy-sell agreements, operating agreements, employment agreements and the like can reduce the value of a business beyond the reduction in current operating results.

- Consistent downward financials. Small and very small businesses generally do not have forecasts, as stated before. They do not have trained financial people who can build forecasts and, more importantly, make a case for forecasts that show results different from the recent past. They also often just have limited markets and services and products, reducing their ability to change course. For this reason, consistent downward financial results produce very low prices. Exactly how this is translated into value is always up for discussion.

- Poor balance sheet. Weak balance sheets that indicate little long-term earnings (no income, no retained earnings, few distributions) weaken the valuation. For many small and very small businesses no or a weak balance sheet in the traditional sense may not hurt the value. But evidence that the company has never been profitable, or was marginally profitable shown in the equity section of the balance sheet can hurt the value or maybe right-size the value of a business that is showing a sudden surge in profitability. Some of the smartest business people the author has ever known spend most of their time examining the balance sheet when looking to acquire companies. That alone is something to think about.

- Key employee agreements. Signed employment agreements with non-solicits for customers and employees and non-competes can add value. Stay agreements that provide a bonus for staying a year or two years after a transaction or owner disability may also be viewed favorably.

EXTERNAL FACTORS AFFECTING THE COMPANY VALUE

The company operates in an environment with many factors beyond its control that are going to influence results in the foreseeable future. In this section we will review a few of those factors.

Key important factors to focus on from the economic and industry data are: does the background that the business operates in support growth or will it create challenges to growth? If the external future appears to create challenges, is it reasonable to believe this company will survive and at some point prosper?

In addition, consider how these external factors affect your subject company in ways that may vary from the comparison company set. This could be comparables for market methods or buildup data used for income methods.

The Economy

For small and very small businesses the impact of the economy on cyclical industries is underestimated in the short run. Many industries are tied into the economic cycle. All types of engineering firms, contractors, home-builders, appliance shops, moving companies, furniture stores, and the list goes on. A few small firms are well diversified and perhaps have a large component of service work but many will have two or three breakeven/hopefully small loss years and then five to seven good years as part of the economic cycle. Very small companies in cyclical industries that carry a lot of debt often do not survive the downturn. Figure 4.4 provides the number of electrical contractor transactions shown in DealStats between 1998 and 2019. While certainly not conclusive, it appears that there are significantly less transactions in the years following the start of a recession (year 2001 had a recession and between the end of 2007 through early 2009 was a recession). This is very difficult to factor into a company value properly.

FIGURE 4.4 Electrical Contractor Sales by Year

The most difficult part of evaluating the economy is that most people are pretty optimistic, particularly when things are going well. Obviously economic cycles are such that the best economic times come before the downturn. When times are really, really good, we “should” be downgrading our valuations because bad times are around the corner. For some reason as humans, we have a hard time doing that. It is always safer to look to the last few years rather than really honestly look at the future. Plus, how do we really know? By the way, it's not just valuation specialists, it's also the economists we need to rely on for this information.7

Having spent most of my life on the East Coast in Maryland, it was hard to understand just how much the local economy can impact a business. In Maryland, the local economy is really the regional economy, including much of the Federal government, and it is huge.

Recently having spent time in a ski resort town of 20,000 people in Colorado, which is 45 minutes from the next town (which has 2,000 people) and over 3 hours away from a major city, Denver, it has become clear in some instances how the local economy can be quite different from the regional one. In these cases, when that local economy is really the entire market, best efforts should be made to understand the primary drivers of the really local, local economy and evaluate them too.

Economic Data

Economic data can come from many sources and levels. International, national, regional, and, in some areas, local can all have an impact. There are many economic reporting bodies. A major one is the Federal Reserve. The Federal Reserve Market Committee regularly provides updates on the international and national economic outlook. The Beige Books provide an anecdotal-type analysis of the Federal Reserve districts. The Federal Reserve of Philadelphia publishes the Livingston Survey in June and December. Therein they provide their estimate of the maximum, mean (average), and minimum forecast of the growth of the economy for the next ten years. Finally, FRED, Economic Research from the Federal Reserve Bank of St. Louis has an amazing assortment of information, data, and even a downloadable mobile app because we all need instant economic data.

Economic data from international, to national, to regional and even local can be purchased from many sources, including BVR and ValuSource among others.

Industry Information

Industry information is available from a number of sources, including IBIS World, First Research, Hoover's Online, Value Line, and Current Industrial Reports from the U.S. Census, trade associations, and industry groups.

Industry information is the best source of data concerning the future of the industry. Is the industry growing or contracting related to the economy as a whole? Is the industry consolidated or fractured? What are expected changes in the industry? If major changes are expected, does it appear that the company being valued is in a position to benefit or lose out from the changes? Often suggested interview questions and areas of focus are provided.

Many major trade associations report economic data and indicators for their industry. Much of this must be purchased but often some indicators are available on the websites and blog posts and the like. Examples are the National Association of Realtors Economists' Outlook. One of the indices is Pending Home Sales Index.8 Many people believe four months of downward pending home sales is a signal of a recession in twelve to eighteen months. At the time of writing the book, it fell from June of 2018 until December of 2018. It then recovered through July of 2019. We will see if it indicates the next recession.

Another example is the National Restaurant Association data. This information can be quite useful when valuing restaurants or restaurant-related suppliers and service companies.9

Sometimes local associations and boards may have indicative data. For example, real estate listings and sales data are available for many markets and are a leading indicator for many housing-related cyclical businesses.

The Amazon Effect

The Amazon effect is a term for the relentless rate of change primarily due to technology. How is the service and supply chain changing? If change is occurring in the company's industry, how will the company withstand and gain from it––or perhaps it will not.

Remember Moto Photos. If you are under 40, you probably do not. Amazing little businesses that printed pictures in kiosks located in shopping center parking lots with 35% profit (that is not a misprint) margins. Digital photos and phones quickly ended that business.

Industry data and parties to the business valuation are most likely to provide information on technology change. Careful questioning is the best way to reveal these issues.

The Amazon effect has had devastating consequences for many retailers. Yet large well-located convenience stores with gas have thrived. Small wholesalers have been decimated yet ones that provide repair and consulting services can carve out a niche and prosper. Be sure to understand how the company being valued is dealing with technological change.

FINANCIAL ANALYSIS

Financial analysis is important for determining how the business being valued ranks compared to businesses in general and more particularly comparable businesses. For small and very small businesses, which are the focus of this book, financial analysis may be of limited usefulness due to poor or incomplete bookkeeping of the subject company. However, it should be looked at for what it is worth.

One of the most important features of financial analysis is the trends. While attempts to compare a company to comparables is useful, paying attention to clear trends is essential. If clear trends exist, they will indicate if the company is improving or heading for trouble. Remember, the past is evaluated to form an opinion about the foreseeable future.

Limitations

A concern about all small business comparable data is that business brokers believe that only the top 50% of most small businesses are saleable. Therefore, how does data from a broad cross-section of companies get compared to market data which is compiled from saleable companies? Even more perplexing is how this fact compares when using the income method, which cannot really be tied into any referenceable small business data. When using the income method, we are comparing the subject company data to public companies. Quite a stretch for most small companies.

Comparable data has not had any adjusting entries made. Therefore, when comparing comparable data to adjusted data, remember that the adjusted data results are not as highly ranked as may appear. (A result that appears to be equal to a 70% or better comparable may be more of a 50% comparable, but it is impossible to know the exact ranking.)

Newer versions of market data comparable sale information usually contain data on some key ratios. This allows comparison of the company being valued to “typical companies” in RMA (Risk Management Associates) or other sources and to the actual comparables. But, caution must be taken when assuming correlations between key ratios and multipliers. This will be reviewed further in the Market Data sections.

Common Size Statements

Common size financial statements convert financial statements to ratios as opposed to dollars. For instance, if revenues are $100 and the cost of goods sold is $65, then the common size cost of goods sold is 65% (65/100). This ratio and other ratios calculated using this methodology can facilitate easy comparisons across companies.

Common size income statements are quite useful for comparing profitability and, depending on the level of data, for comparing the cost of goods sold and sometimes major expenses, such as rent. Major cost and profitability trends indicate if the business is becoming more efficient, more profitable, or if results are creeping away. Often with small and very small businesses the common size ratios change over time and a review of the trends will be more useful than the comparison to commensurate data.

While common size comparisons are important, the analyst must also evaluate the dollars on the statements independently. Both ratios and raw numbers can raise questions and provide reason for further query. An example of a common size balance sheet is shown in Figure 4.5 and a common size income statement is shown in Figure 4.6.

Balance sheet common size statements are harder to compare. Many small companies do not properly maintain their balance sheets. This is most pronounced in restaurants and cash-based retail and other smaller operations. In many cases even if the statement is accurate, the owner moves money interchangeably between personal and business accounts and does not expect the business to be self-supporting without an occasional infusion. In fact, due to the taxation of undistributed income for pass-through entities, some owners distribute all profits every year and then re-invest if they must. Therefore, cash accounts may be artificially low on year-end balance sheets which are usually used for comparison. There can be similar issues with the recognition of receipt of receivables and overpayment of payables for cash basis businesses at year-end. If the company being valued “manages” earnings for tax purposes, request a balance sheet and the related payables and receivable aging for another more typical month just to see what “typical” balances look like.

| Adjusted | Historic | Historic | Historic | Historic | ||

| RMA | 2018 | 2018 | 2017 | 2016 | 2015 | |

| Cash & Equivalents | 12.30 | 1.69 | 44.65 | 28.36 | 44.59 | 64.66 |

| Accounts Receivable | 31.90 | 29.45 | 12.38 | 64.38 | 49.36 | 28.71 |

| Inventory | 2.20 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Current Assets | 5.20 | 0.00 | 11.65 | 0.00 | 0.39 | 0.00 |

| Total Current Assets | 51.60 | 31.14 | 68.68 | 92.73 | 94.34 | 93.37 |

| Fixed Assets Net | 39.60 | 68.86 | 28.95 | 6.31 | 5.57 | 6.21 |

| Intangibles Net | 3.10 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Non-Current Assets | 5.70 | 0.00 | 2.36 | 0.96 | 0.09 | 0.42 |

| Total Assets | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 |

| Accounts Payable | 12.30 | 0.00 | 0.65 | 11.14 | 6.43 | 24.26 |

| Short-Term Notes Payable | 6.50 | 0.00 | 0.00 | 0.00 | 4.17 | 5.39 |

| Current Maturity LT Debt | 6.50 | 0.00 | 0.00 | 0.00 | 0.00 | 0.00 |

| Other Current Liabilities | 8.30 | 0.00 | 3.74 | 1.63 | 3.02 | 3.12 |

| Total Current Liabilities | 33.60 | 0.00 | 4.40 | 12.77 | 13.62 | 32.77 |

| Long-Term Debt | 20.50 | 0.00 | 0.00 | 0.00 | 3.52 | 9.53 |

| Other Non-Current Liabilities | 3.60 | 0.00 | 0.00 | 81.54 | 53.32 | 33.88 |

| Total Liabilities | 57.70 | 0.00 | 4.40 | 94.30 | 70.46 | 76.19 |

| Total Equity | 42.40 | 100.00 | 95.60 | 5.70 | 29.54 | 23.81 |

| Total Liabilities & Equity | 100.10 | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 |

FIGURE 4.5 Sample Common Size Historic Balance Sheet

| Dec | Dec | Dec | Dec | ||

| RMA | 2018 | 2017 | 2016 | 2015 | |

| Revenue | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 |

| Cost of Goods | 69.00 | 72.51 | 78.24 | 64.32 | 72.37 |

| Gross Profit | 31.00 | 27.49 | 21.76 | 35.68 | 27.63 |

| Operating Expenses | 24.30 | 17.53 | 17.26 | 13.99 | 12.77 |

| Operating Profit | 6.70 | 9.96 | 4.51 | 21.69 | 14.85 |

| Other Income/(Expense) Net | –0.50 | 0.70 | 0.00 | 0.24 | 0.00 |

| Pre-Tax Profit | 6.20 | 10.66 | 4.51 | 21.93 | 14.85 |

Notes: ANNUAL STATEMENT STUDIES, (TM) RMA THE RISK MANAGEMENT ASSOCIATION, (TM) and the RMA Logo are trademarks of the Risk Management Association. RMA owns the copyright in the ANNUAL STATEMENT STUDIES(TM) data. The data is used under license from RMA.

FIGURE 4.6 Sample Common Size Historic Income Statement

Source: Risk Management Association, Philadelphia, PA 2018

Common size balance sheets should be compared if the statements are reasonable and include accruals but in many instances little or no weight will be applied as the trends may not be reliable.

Ratio Analysis

Most ratios are a comparison of a balance sheet account to an income statement account. Therefore, most ratios will be of little value or impossible to calculate if the balance sheet is not reasonably accurate. When accurate statements are available, ratio analysis can be quite indicative of strengths and weaknesses.

Huge numbers of ratios exist. Some industries rely on certain ratios. Common ratios that are useful for business valuation are shown below. This is by no means all ratios but they are highly indicative and use high-level data that may be available even with small businesses. The following are the most common important ratios:

- Current ratio. The current ratio is a liquidity ratio that measures a firm's ability to pay its short-term liabilities with current assets. The formula is:

Current assets are cash, accounts receivable, inventory, other current assets. Current liabilities are accounts payable and other current liabilities.

The higher the ratio, the more cash available (and presumably the higher the level of liquidity) for payment of current liabilities. A higher figure is good, yet at some point cash should be put to other uses.

- Quick ratio or acid test ratio is a liquidity ratio which measures the ability of a company to use its quick assets to pay current liabilities. It excludes inventories that may not be easily converted into cash. The formula is:

Quick assets are cash and accounts receivable. Current liabilities are accounts payable and other current liabilities.

The higher the ratio, the more cash available for payment of current liabilities. Again, a higher figure is good yet at some point cash should be put to other uses.

Days receivables outstanding or days sales outstanding is a measure of the rate of collection of accounts receivable. The formula is:

In general, a smaller number of days outstanding shows good accounts receivable management. But, at some point perhaps the extension of more credit would result in more sales.

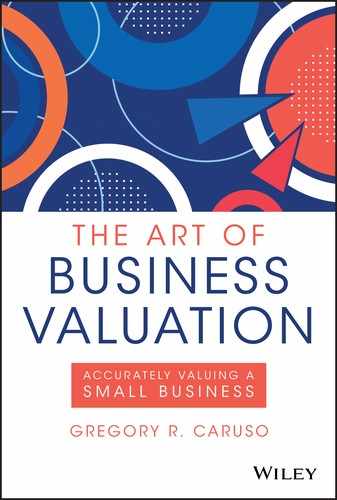

- Inventory turn is a ratio showing how efficiently a company is using its inventory. The formula is:

In general, higher inventory turn shows efficient inventory management. This can be offset if there are inventory shortages that reduce sales.

- Debt to equity is the ratio of total debt divided by total equity. It is a measure of leverage. The formula is:

Note: suppose the debt = $40,000 and the equity = $60,000. The debt/equity ratio is 66.667%. Now divide this ratio into the number 1 and this results in a 1.5 relationship. Therefore, $40,000 times 1.5 = $60,000. This is very helpful when the relationship is provided and not the ratio.

In general, the lower the debt to equity ratio, the less debt and the safer the company is.

- Return on investment (ROI) is a measure of overall financial performance. ROI shows the ratio of profit or loss made in a year to the total investment. It is a measure of return/income. The formula is:

- Total investment is the total capital structure of debt and equity. Investors clearly prefer higher returns on investment.

- Return on equity is a measure of financial performance. Equity is total assets – total liabilities so it is also called return on net assets. The formula is

Again, investors clearly prefer higher returns on equity.

More common financial ratios are shown in Figure 4.7.

| Liquidity Ratios | |

| Current Ratio | Current assets/current liabilities |

| Quick Ratio | Quick Assets / current liablities |

| Quick assets are cash and accounts receivable | |

| Accounts Receivable Turnover | Revenue / Accounts Receivable; Note this assumes all sales are on credit. For some companies Sales on Credit would be substituted for Revenue. |

| Average Collection Period | 365 / Average Receivable Turnover |

| Inventory Turnover | Cost of Goods Sold / Average Inventory for the Year |

| Days Sales Inventory | 365/ Inventory Turnover |

| Leverage Ratio | |

| Debt to Equity | Total liabilities / Total Stockholders Equity |

| Coverage Ratios | |

| Times Interest Earned | Earnings Before Interest and Taxes / Interest Expense |

| Operating Ratio | |

| Return on Equity | Net Income after Taxes / Average Shareholders Equity |

| Expense to Revenue Ratios | |

| Gross Margin | Gross Profit / Net Sales |

| % Depreciation, Amortization / Revenue | |

| % Officers Comp / Revenues | |

| Profit Margin | Profit / Net Sales |

FIGURE 4.7 Common Financial Ratios

Sources of Common Size and Ratio Data

Always ask your client if they have access to an industry periodical or association that tracks financial data and ratios. Often these have a cost associated with them. These are often the most useful when available at a reasonable price.

- RMA data. The RMA (Risk Management Association) compiles data sent to banks. Some formats of the data show the number of tax returns, compilations, reviewed statements and audits. For smaller businesses, the data is heavily weighted to compilations and tax returns. Most of these financials are prepared on a tax basis and most owners have a bias to lower taxable income wherever possible. Therefore, while this is one of the best sources of data, it has limitations due to the origin of the data.

- Integra. Integra has data sources that represent the financial performance of 4.5 million privately held businesses in over 900 industries. It includes an income statement, balance sheet, cash flow analysis and over 60 financial ratios. They pull data from 32 different proprietary and government data sources.

- BizMiner. BizMiner (https://www.bizminer.com/) reports receiving over a billion sourced data points from 15 million business operations. BizMiner can be searched by NAICS, size, and a radius from an address. BizMiner has many uses, including a ranking system based on the results of a review of the financial information.

- Industry data. Many industry associations have outstanding data. But accessing the data can be expensive. Certainly, if the firm being evaluated has quality data and if the level of the valuation and purpose support it, this can be the best data. In many cases the industry data must be purchased year by year. Examples of industry associations with outstanding data include the Electrical Contractors Association, the Associated Building Contractors, the National Association of Homebuilders, and the National Restaurant Association.

- SEC, census, government and government-related sources. Edgar Online, https://www.census.gov/, OSHA, and others can call provide useful data.

NOTES

- 1. A saying I have found helpful but do not know to whom to attribute is, “Company culture statements are just words on the wall until the management is willing to fire someone for not complying”. Something to think about when assessing the soft factors of a company.

- 2. Recently I evaluated a 10-year-old firm that had changed so substantially that the owner only would allow 2.5 years of data to be reviewed. Results were very good but it was valued as a start-up, not an established company.

- 3. Tariffs and changing international relations have added new risks to importers.

- 4. South Dakota v. Wayfair, Inc. No. 17-494. https://www.supremecourt.gov/opinions/17pdf/17-494_j4el.pdf

- 5. That was a real contingency on a recent transaction. The buyer wanted to run larger trucks to the facility and the only route in and out had a small bridge with weight limits limiting truck size. The permit was obtained.

- 6. See https://www.targetgov.com/government-contracting-institute/myths-realities-of-8a-certification-golden-ticket-or-not/

- 7. See https://www.bloomberg.com/news/articles/2019-03-28/economists-are-actually-terrible-at-forecasting-recessions

- 8. See https://www.nar.realtor/blogs/economists-outlook?page=1

- 9. See https://restaurant.org/research/economy/snapshots