Financing Your Dream ◾ 127

technology industries, for example, biotechnology, IT, or software. The typi-

cal VC investment occurs after the seed-funding round, frequently referred

to as growth funding round (or Series A round). The VC seeks to generate

returns through an eventual realization event, such as an IPO or a trade sale

of the company.

6

VC is a subset of private equity.

One of the rst steps toward a professionally managed VC industry was

the passage of the Small Business Investment Act of 1958; this Act ofcially

permitted the U.S. Small Business Administration (SBA) to license private

“Small Business Investment Companies” (SBICs) to help nance and manage

small entrepreneurial businesses in the U.S.

Before World War II, money orders (originally known as “development

capital”) were primarily the exclusive domain of wealthy individuals and

families. Modern private equity investments began to emerge after World War

II with the founding of the rst two VC rms in 1946—American Research

and Development Corporation (ARDC) and J.H. Whitney & Company.

ARDC was founded by Georges Doriot,

7

the “father of venture capital-

ism” (and former dean of Harvard Business School and founder of INSEAD),

8

with Ralph Flanders and Karl Compton (former president of MIT), to encour-

age private sector investments in businesses run by soldiers returning from

World War II. ARDC was the rst institutional private equity investment rm

that raised capital from sources other than wealthy families, although it had

several notable investment successes as well. ARDC is credited with the rst

trick when its 1957 investment of $70,000 in Digital Equipment Corporation

(DEC) would be valued at over $355 million after the company’s IPO in 1968

(representing a return of over 1200 times on its investment and an annual-

ized rate of return of 101%).

9

6.8 Principles of Raising Capital

The amount of money you plan to raise should be sufcient to accomplish

key milestones that will either (1) make your startup self-sufcient or (2)

enable you to raise additional capital at a higher valuation. Higher valuations

enable management to keep a greater percentage of the company.

The entrepreneur needs to prepare for the due diligence process. Due

diligence is the analysis and evaluation conducted by rms considering an

investment in your company, and focuses primarily on (1) your management

team, (2) the market opportunity, and (3) your technology, including intellec-

tual property protection.

128 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

Prepare a list of references and accomplishments of key management

team members (including your scientic advisory board members) and your

technology. Furthermore, have your patent rm prepare a status report on

your patents, including a freedom to operate opinion, so you can verify that

your products are proprietary and that you are not encumbered by the pat-

ents of others.

Most startups follow a predictable series of steps, prior to raising capital.

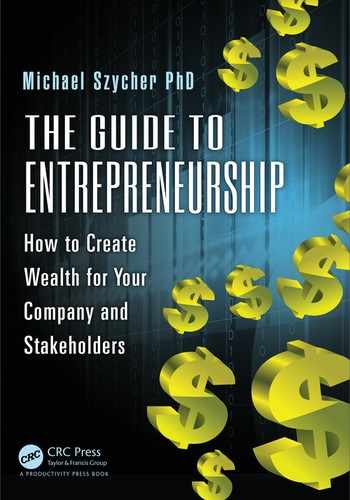

Figure6.4 summarizes the typical history of a startup.

The equity nancing characteristics for startups is summarized in

Table6.4.

Table6.5 summarizes the differences between debt and equity nancing.

6.9 Persuasive Business Presentations

“Leadership is communication.”

As a budding entrepreneur, you might as well get used to this: as an entre-

preneur, you will be giving presentations until the cows come home.

Moreover, persuasive presentations will be your trademark.

Proof of principle Sweat equity

Typical Historical Development

Working prototype

Beta site

Friends & family

investments

Initial sale (s)

Angel investors

Rapid expansion

Financial event

IPO sale

Strategic partnership

Venture capital

Figure 6.4 Typical historical development—Predictable steps undertaken by startups

pre-funding.

Financing Your Dream ◾ 129

A persuasive presentation (speech) aims to get your audience to accept

your business premise by prompting them to act, think, or feel in a desired

manner, without coercion or force. Figure6.6 presents the four cornerstones

of persuasive presentations.

Pathos refers to presenting your reasons to believe in something, over-

coming risks, natural apprehensions, perceived problems, etc. Ethos refers

to your personal technical competence, goodwill, and dynamism to be

trusted with investor’s moneys. Logos are your set of rational, logical, and

validated proofs. Last, mythos is the combined forces of ethical values,

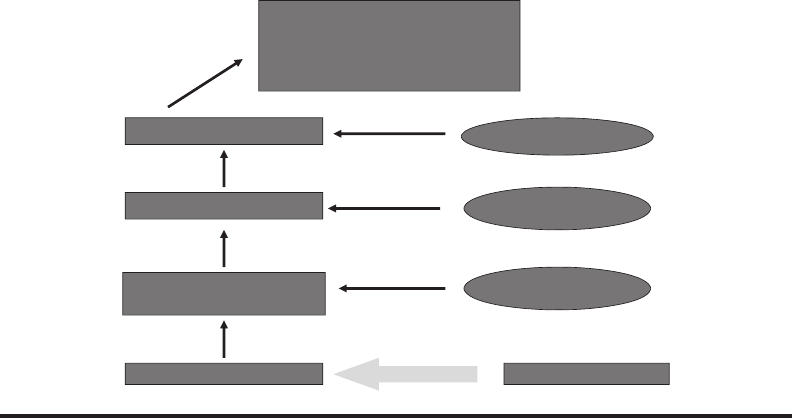

Types of Financing for Startups

Equity

Capital

Debt

Capital

Other

Family & friends

Angels

Joint

ventures

Family & friends

SBIRs, STTRs

Customers

Small business

administration

Banks

Figure 6.5 Types of nancing—You can nance your startup with (1) equity, (2) debt,

or (3) other hybrid forms.

Table6.4 Equity Financing

Friends and family

Typical round: $10–$100,000

Not necessarily “accredited” individuals

“Passive” investment

Personally interested in the technology

Angels

Typical round: $50–$500,000

Increasingly as angel groups

Accredited individual

Expertise and personal investments

Bets on the jockey, not the horse

VC

Typical round: $1–$5 million

Looks for “exit”

Professional investors

LLP, GP

Follow-on investments

130 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

industry beliefs, and national culture that may prompt investments in you

and your company.

Persuasive speech is the most complicated form of verbal communication.

It involves moving your audience to accept your premise from a position

of deep skepticism/opposition to strongly/enthusiastically embracing your

proposed solution based on its perceived benets.

10

The entire sequence is

shown in Figure6.7.

• Pathos (risk, apprehension)

• Ethos (speaker’s competence)

• Logos (rational, logical arguments)

• Mythos (values, beliefs, culture)

e Four Cornerstones

of Persuasive Presentations

Note: If this sounds Greek to you, you are right. It is Greek.

Figure 6.6 The four cornerstones—Your basic forms of persuasion (prompting action

without coercion).

Table6.5 Summarizes the Differences Between Debt and Equity Financing

Debt (Bank loan) Equity (angels, VC)

Emphasis on collateral and cash ow Return on investment

Repayment starts immediately after

funding

Deferred repayment

Debt return based on ability to pay Repayment based on nancial

performance

Lowest risk for lender Highest risk for investor

Lowest cost if business is successful Higher cost if business is successful

No ownership dilution Heavy ownership dilution

Focused on short-term expansion Focused on long-term business

prospects

Monitoring relationship May demand Board plus upper

management participation

Boilerplate documents Complex documentation

Financing Your Dream ◾ 131

6.9.1 Rookie Mistakes

There is an old adage that goes, “Your presentation is 20% what you say, and

80% how you say it.” Most rookie entrepreneurs tend to ignore their demeanor

when making presentations, believing that their data “speaks for itself.”

Another hurdle is the fact that most people become tongue-tied when

placed in front of an audience. Most of us “freeze” when asked to give an

important presentation. Did you hear the joke about the survey that asked

aspiring entrepreneurs what are their three greatest fears in life? Their

answers are as follows:

1. Fear of dying.

2. Fear of speaking in public.

3. Fear of dying while speaking in public.

Figure6.8 presents a tongue-in-cheek list of don’ts for the young readers

of this Guide.

6.10 Your Elevator Pitch

“I only had one superstition. I made sure to touch all the bases

when I hit a homerun.” —Babe Ruth

The “Elevator Pitch” derives its name from an apocryphal story: after hav-

ing submitted a “teaser” document to a VC, and after having waited many

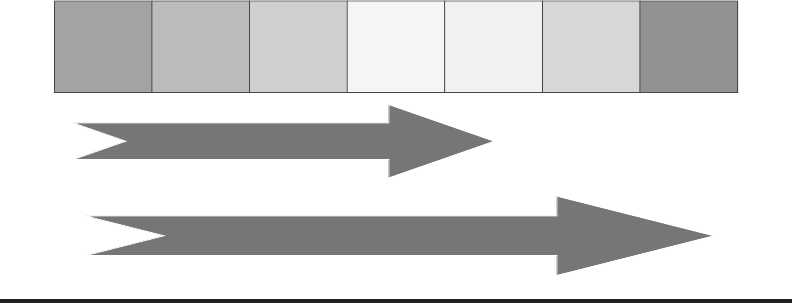

Degrees of Convincing, Persuading

Convincing and persuading involves the degree

of movement by a listener from left to right

Strongly

Opposed

Moderately

Opposed

Slightly

Opposed

Neutral

Slightly

in Favor

Moderately

in Favor

Strongly

in Favor

Convinced

Persuaded

Figure 6.7 Degrees of convincing—Differences between convincing and persuading.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.