132 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

weeks to hear something from the VC, suddenly you get an unexpected

phone call from the Managing Partner. “I am in the elevator going to a meet-

ing. Tell me why I should fund your company now.” The Partner has just

asked you to answer three questions: Why me? Why you? Why now?

Guess what? You only have one chance of being funded. Thus, an

Elevator Pitch must be a concise, carefully planned, and well-practiced

description of your company that anyone should be able to understand in

the time it would take to ride up three oors in an elevator. Like Babe Ruth,

your pitch needs to touch these bases:

◾ A burning market need and your proposed solution to the burning need

◾ Your team and how they are uniquely qualied to manage the company

◾ How you will make money for your investors

◾ Memorable tagline/pitch closing

6.10.1 Must Haves

Your pitch should have a riveting opening; that is, grab the interest of your

recipient. Your pitch should show passion—if you are not excited about

your idea, no one else will be.

I. Too many slides (not enough time)

II. Speaking to the slides; not the audience

III. Reading the slide

(although audience is literate)

IV. Presentation does not match the audience

(Talking birth control to retirees)

V. Fonts too small (unreadable from a

distance) (what is the room size?)

VI. To o much information in one slide

VII. Using light background with dark print

(did you hear about eye strain?)

VIII. Not practicing beforehand

How to screw up a presentation

Figure 6.8 How to screw up—How to fail at your presentation in eight easy steps.

Financing Your Dream ◾ 133

6.10.2 Brief Descriptions

Following the pitch be prepared to answer questions briey. You must pre-

pare a brief description of how the business is different from the competi-

tion, how you will make money, the resources you need from investors,

and the returns/payback the investor can expect.

6.10.3 Last Three Bits of Advice

Always use the KISS principle—Keep It Simple, Stupid. Do not use techno-

Latin, a language that only you understand. Highlight marketing advantages,

not technical benets.

6.11 Estimating StartUp Costs

Expenses incurred prior to the commencement of operations, startup

expenses are incurred after the decision to proceed with the new business

but before beginning operations, including:

◾ Business investigation expenses

◾ Organization costs

◾ Advertising

◾ Bank service charges

◾ Commissions

◾ Ofce and laboratory supplies

◾ Taxes (other than federal)

◾ Licenses, accounting fees, and legal fees

◾ Salaries and wages

◾ Utilities

6.12 Valuing You and Your Team

“It is better to invest in an ‘A’ team with a ‘B’ technology than in a

‘B’ team with an ‘A’ technology.”

Just about everyone will tell you that management is the top factor for a suc-

cessful startup. Furthermore, the entrepreneur represents 80% of the value

given to teams. It is not surprising to hear seasoned investors speak of the

134 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

“ABCs” of their entrepreneurial investments. The “ABC” philosophy can be

summarized as follows:

1. Type “A”. The entrepreneur is technologically experienced, and has a

successful record of running innovative companies. (Least risky)

2. Type “B”. The entrepreneur is technologically experienced, but does

not have managerial experience. (Average investment risk)

3. Type “C”. The entrepreneur is neither technologically nor managerially

experienced. (High risk)

Also, keep in mind that investors rarely provide you with all the required

capital, preferring instead to invest in pre-determined stages (milestone-

based). By staging their funding, investors retain the ability to abandon the

project or re-value the company.

6.13 Valuing Your New Venture. (Calculating

Pre-Revenue Valuation)

Valuation is the core determinant of return for investors. Unfortunately, seed

and early-stage venture valuation creates the most contentious negotiations

between the owner and investors. Aligning owner and investor expecta-

tions, particularly in the pre-revenue stages, is difcult and often leads to

an impasse.

In this section, we will undertake a simple case of nancing to illustrate

how the process works and to demonstrate that valuation is more an art

than a science and is ultimately determined by the marketplace and recali-

brated annually.

6.13.1 Basic Calculations

Pre-Money valuation is the value of the company before any money is invested,

while Post-Money valuation is the value after the money has been invested.

If an investment adds cash to a company, the company’s post-money

valuation will increase immediately after the investment.

External investors such as Angels and VCs will use Pre-Money valuation

to calculate how much equity to negotiate in return for their cash infusion

on a fully diluted basis.

Financing Your Dream ◾ 135

Post-Money Valuation = Pre-Money Valuation + Money (investment)

Post-Money Valuation = Investment × (Total investment shares

outstanding/shares issued for the new investment)

Pre-Money Valuation = Post-Money Valuation – new investment

6.13.2 Valuation Examples

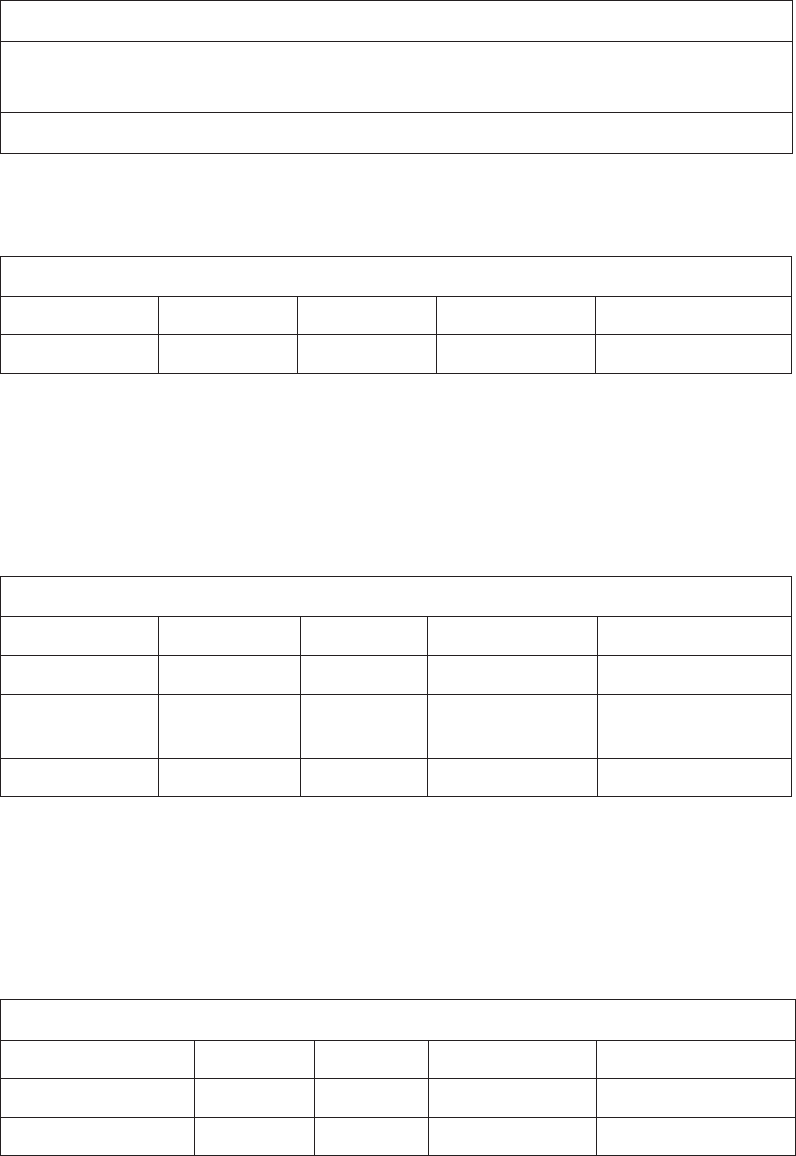

Startup Capitalization Table

Stockholders # Shares $/Share % Ownership Enterprise $ Value

Founders 1000 N/A 100 N/A

Financing Series “A” Objective = Negotiate raising $1 million for 200

newly issued Series “A” shares.

Series “A” per share value = $1 million/200 shares = $5/share

Implied Post-Money Valuation = $1 million * (1200/200) = $ 6 million

Implied Pre-Money Valuation = $6 million − $1 million = $ 5 million

Capitalization Table Following Series “A” Investment

Stockholders # Shares $/Share % Ownership Enterprise $ Value

Founders 1000 5 1200/1000 = 83.3 5 million

Series “A”

Investor

200 5 1200/200 = 16.7 1 million

Total 1200 100.0 6 million

Financing Series “B” Objective = Negotiate raising $2 million for 300

newly issued shares.

Series “B” per share value = $2 million/300 shares = $6.67/share

Implied Post-Money Valuation = $2 million × (1500/300) = $10 million

Implied Pre-Money Valuation = $10 million – $5 million = $5 million

Capitalization Table Following Series “B” Investment

Stockholders # shares $/share % Ownership Enterprise $ Value

Founders 1000 6.67 1500/1000 = 66.7 6.67 million

Series “A” Investor 200 6.67 1500/200 = 13.3 1.33 million

136 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

Series “B” Investor 300 6.67 1500/300 = 20.0 2 million

Total 1500 100.0 10 million

A successful company can expect to have a series of investment rounds,

ideally at Up-Round valuations (a higher Pre-Money valuation in each suc-

cessive round). If the reverse were true, it would be called a Down-Round.

In our example, notice that the founders went from owning 100% of zero

to owning 66.7% of a $10 million enterprise, that is, $6.67 million in equity.

That is called value creation—get the picture?

References

1. Shapiro, J. http://thenextweb.com/entrepreneur/2012/04/22/

before-naming-your-startup-read-this/.

2. http://en.wikipedia.org/wiki/Corporate_title

3. http://www.investopedia.com/terms/s/sweatequity.asp

4. http://www.angelblog.net/Startup_Funding_the_Friends_and_Family_Round.

html

5. Hoeksema, A. http://blog.startupprofessionals.com/2010/08/friends-and-

family-largest-startup.html.

6. http://en.wikipedia.org/wiki/Venture_capital

7. WGBH Public Broadcasting Service. Who made America?—Georges Doriot.

8. Ante, S.E. Creative Capital: Georges Doriot and the Birth of Venture Capital.

Cambridge, MA: Harvard Business School Press, 2008.

9. Venture Impact: The Economic Importance of Venture Backed Companies to

the U.S. Economy. NVCA.org. Retrieved 2013.

10. Lucas, S.E. Speaking to Persuade. Chapter 15. http://www.jdcc.edu/includes/

download.php?action=2023&download_le_id=5274&action=2023&table_

num=.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.