350 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

15.7 Mergers and Acquisitions

Mergers and acquisitions (abbreviated M&A) is an aspect of corporate

strategy, corporate nance and management dealing with the buying, sell-

ing, dividing, and combining of different companies and similar entities that

can help an enterprise grow rapidly in its sector or location of origin, or a

new eld or new location, without creating a subsidiary, other child entity,

or using a joint venture.

5

15.7.1 Mergers

Theoretically, a merger happens when two rms agree to go forward as

a single new company rather than remain separately owned and operated.

This kind of action is more precisely referred to as a “merger of equals.”

In practice, however, actual mergers of equals do not happen very often.

Usually, one company will buy another and, as part of the deal’s terms, sim-

ply allow the acquired rm to proclaim that the action is a merger of equals,

even if it is technically an acquisition.

6

15.7.2 Acquisitions

Practically speaking, an acquisition is the process through which one com-

pany completely takes over the controlling interest of another company. Such

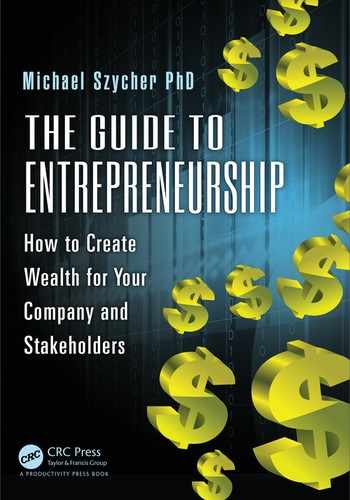

Post

Merger

integration

Seller

decision

to sell

Buyer’s

strategy

Negotiations +

Valuation

Offer

Acceptance

Consideration

Closing

Legal, tax

Acc’t

Finance

Management

Sales

Marketing

Market

impact

M&A process at a glance

Figure 15.9 M&A process at a glance—Visual representation of the M&A process

from start of negotiations to post-closing activities.

Harvesting ◾ 351

controlling interest may be 100%, or nearly 100%, of the assets or ownership

equity of the acquired entity. An “acquisition” usually refers to a purchase of

a smaller rm by a larger one (Figure15.10).

There are two sets of stockholders affected by a merger or acquisition:

those of the rm being acquired and those of the rm doing the acquiring.

15.7.3 The Challenge of M&A

There are many examples of successful M&A (and many more failures).

The most spectacular M&A failure of all times was the acquisition of Time

Warner by AOL. In January 2000, America Online merged with Time Warner

in a deal valued at a stunning $350 billion. It was then, and is now, the larg-

est merger (and eventual de-merger) in American business history.

Due to the larger market capitalization of AOL, they would own 55% of

the new company while Time Warner shareholders owned only 45%. So in

actual practice AOL had acquired Time Warner, even though AOL had far

less assets and revenues.

7

What was the perception of the average stockholder when AOL offered

such a large premium over market price to purchase Time Warner? The aver-

age AOL stockholder wondered whether the acquisition was being made in

their interest or in the interest of management. Some important lessons have

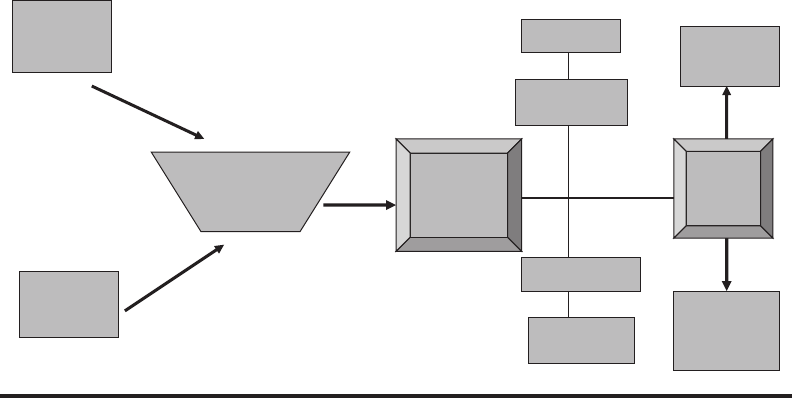

M/A Occur in Waves

Monopolies

2.5%

2.0%

1.5%

1.0%

0.5%

0.0%

1926

1930

1935

1940

1945

1949

1954

1959

1964

Quarters

Percentage of All Public Companies

1968

1973

1978

1983

1987

1992

1997

2002

2005

60s

conglomerate

deals

80s hostile

takeovers

2000s global,

synergistic

Figure 15.10 M/A occur in waves—Due to economic/regulatory changes, M/A activ-

ity occurs in waves.

352 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

been learned from the AOL/Time Warner failure. The following ve criteria

have been offered as success principles for M&A/strategic alliances:

8

◾ Compatible strategy and culture

◾ No overpayment

◾ Comparable contribution

◾ Compatible strengths

◾ No conict of interest

So, what is an M&A success and what is an M&A failure? Is it a matter of

luck, perception, or timing? The author recommends a quantitative measure,

based on Return on Invested Capital (ROIC) and Weighted Average Cost of

Capital (WACC) as shown next:

Failure ROIC < WACC

Success ROIC > WACC

where

ROIC = earnings before interest and taxes divided by (invested capital

equity + long-term liabilities)

WACC = Sum of after-tax of debt and equity, multiplied by their respec-

tive percentage of capital structure

15.7.4 The Enduring Questions

Prior to consummation of the transaction, the buyer and the seller nd

themselves in an adversarial position. Table15.4 lists the ten most frequently

asked questions in buying or selling a business. Paradoxically, although the

questions look similar, the answers are not.

15.8 The Day That Little David Acquired

Giant Goliath—A Case Study

When academicians talk about acquisitions, they are usually referencing

events such as: “Johnson & Johnson acquires Company X for billions,” or

“Apple Inc. acquires Company Y for billions.” Seldom do small companies

undertake acquisitions as part of a well-reasoned strategy for growth even

mentioned in the literature or the classroom. Following is the story of an

acquisition by a small company called CardioTech.

By 2002, CardioTech (a company founded by Dr. Michael Szycher and

publically traded in the AMEX), had decided to grow inorganically by

Harvesting ◾ 353

opportunistically pursuing an accretive acquisition strategy. To reduce any

managerial impulsive and emotional decisions, CardioTech pre-established a

systematic, quantitative acquisition criteria matrix, as shown in the following:

◾ Balance Sheet Criteria

− Debt-to-equity ratio

− Working capital

− Liquidity requirements

◾ Performance Criteria

− Return on equity

− Return on invested capital

− Return on assets

− Earnings growth rates

◾ Business Characteristics Criteria

− Relative market position

− Market share

− Competitive strengths

− Product line

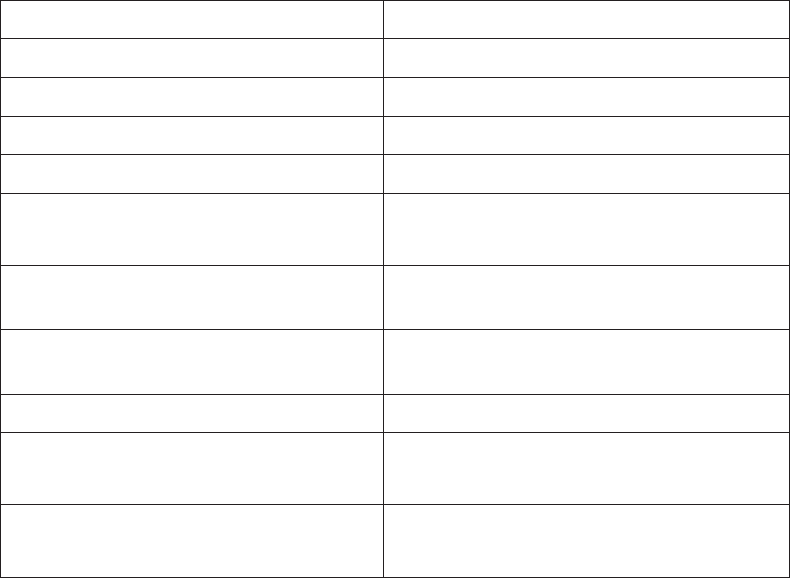

Table15.4 The Most Frequently Asked Questions by Sellers and Buyers

Seller Buyer

Why is their offering price so low? Why is their asking price so high?

Are they bottom shing? Are they serious about selling?

Is it okay for us to shop around? Should this be a no-shop negotiations?

Why are they interested in us? What do we really know about them?

Do we really need money now?

Is this transaction for cash or shares?

What will they do with our money?

What are their future nancial demands?

Who should be part of our negotiation

team?

Are we really negotiating with the

decision makers?

How much independence do we retain

post-transaction?

How do we integrate them into our

winning culture?

Could we do better on our own? Do we really need them?

What happens if the deal collapses?

How vulnerable do we remain?

What if we nd deal-killers during due

diligence?

What happens if our CEO is run over by

the mythical train during negotiations?

How indispensable is their CEO?

Do they have a succession strategy?

354 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

− Cash generation

− Price and cost structure

− Geographical reach

◾ Market/Industry Characteristics Criteria

− Barriers to entry

− Governmental regulations

− Industry growth

− Company growth cycle

◾ Investment Criteria

− Quality of earnings

− History of labor relations

− Labor intensive or technology intensive

◾ Intellectual property portfolio

This case study exemplies the unusual occurrence when CardioTech

(little David with $3 million in sales) acquired Gish Biomedical (giant

Goliath with $17 million in sales). Please note this was not a merger;

it was an acquisition. At the end of the transaction, CardioTech owned

100% of Gish. That is, Gish became an operating, fully owned subsidiary

of CardioTech.

After establishing the above criteria for the acquisition, CardioTech started

the search for an appropriate target. The following paragraphs enumerate

the history behind the acquisition.

15.8.1 The Acquisition

On April7, 2003, CardioTech completed the acquisition of Gish Biomedical.

Gish shareholders were issued 1.3422shares of CardioTech stock for each of

their shares of Gish common stock. Gish Biomedical,Inc., a California corpo-

ration, was founded in 1976 to design, produce, and market innovative spe-

cialty surgical devices. Gish developed and marketed its innovative and unique

devices for various applications within the medical community. Gish operated

in the medical devices segment—the manufacture of medical devices—which

were marketed through direct sales representatives and distributors domesti-

cally and through international distributors. All of Gish’s products were sin-

gle-use disposable products or had a disposable component. Gish’s primary

markets included products for use in cardiopulmonary bypass surgery, myo-

cardial management, infusion therapy, and postoperative blood salvage.

Prior to the transaction, Gish had been experiencing a steady 10% decline

in annual sales for the previous 5 years. This followed the overall downward

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.