260 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

three general approaches under which each of the methods fall. Table13.2

summarizes the three accepted methods.

We will discuss each of these approaches in the subsequent paragraphs.

13.5.1 Income Approach

This determines the value based on how much the business is forecasted

to earn in the future. This approach is based on the theory that fair mar-

ket value is the present value of all future benets. Fair market value is the

amount at which the property would change hands between a willing buyer

and a willing seller, when the buyer is not under compulsion to buy and the

seller is not under compulsion to sell, and both parties have a reasonable

knowledge of relevant facts.

4

Figure13.4 illustrates the pros and cons of the

income approach.

Capitalized Returns Method

is method determines value by dividing a single return (income) amount by

a capitalization rate in the following formula:

Return (income) = Investment Value

Capitalization rate

Example: Calculate investment value of $150,000 at a capitalization rate

(discount rate; hurdle rate) of 15%

$ 150,000 = $1,000,000

15%

Note: this method tends to be appropriate when the estimated future return

is expected to be consistent with a normal, predictable growth rate.

Figure 13.4 Capitalized returns method—Value determined by dividing economic

benets by a capitalization rate.

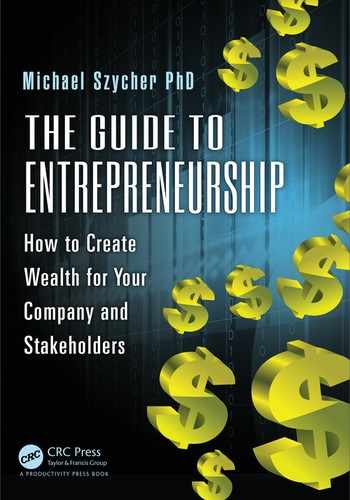

Table13.2 Valuation Methods for Companies with Revenues

Approach Based On

Income Present and future earnings capacity

Market Comparable companies valuations

Asset based or cost Current market value

Valuation Techniques ◾ 261

Mathematically, the income approach involves computing future benets

and discounting them to their present value at a rate that reects the inher-

ent risks associated with the operations. The primary three include:

1. Discounted future returns method

2. Capitalized return method

3. Excess earnings method

13.5.2 Discounted Future Returns Method

Proper use of this method assumes the appraiser can estimate future returns

with a reasonable degree of accuracy, and there is a reasonable probability

that those returns will continue. The value determined under an income

approach is based on discount or capitalization rates using public market

data or internally generated hurdle rate. Hurdle rate is the minimum ROR

(interest rate) on a project or investment required by an investor in order to

compensate for risk. Thus, from an investment standpoint, the riskier the

project, the higher the hurdle rate should be.

5

Figure13.5 shows Present Value (PV) multiple cash ows in multiple time

periods are discounted, and it is necessary to sum them as in the gure.

13.5.3 Capitalized Returns Method

The capitalization of earnings valuation method is a method within the

income approach to value whereby economic benets for a representative

single year are converted to value through division by a capitalization rate.

How Do Entrepreneurs Raise

Money over time?

Sweat Equity (Bootlegging)

Savings, 2nd

Mortgage, etc.

SBIR (government grants)

Friends, Family, Fools (3 Fs)

Banks (debt)

Angel groups

Venture capitalist investments

IPO (initial public offering)

Figure 13.5 How do entrepreneurs raise money—The possible sources of capital

available to entrepreneurs.

262 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

The valuation concept is a company’s value as established primarily by the

income it can be expected to earn on an ongoing annual basis, in relation-

ship to a capitalization rate measuring ROR, investment risk, and potential

earnings growth (Figure13.6).

6

13.5.3.1 Assumptions

Fair Value Standard of Value. “Standard of value,” as it is generally dened

for business valuation purposes, is the fundamental way in which the

value of a business or ownership holding will be established, based on the

purpose of the valuation. For the subject valuation, the standard of value

being employed is “fair value,” which is an opinion as to what is fair from a

nancial point of view as dened by law and precedent.

Net Income. “Earnings” for the method have been dened as “Net Income.”

The value used in the method is the one-year extension of a straight-line

trend based on ve historical years rounded to the nearest $1,000.

Net Income Capitalization Rate. A capitalization rate is a rate of return

divisor used for converting an earnings value into an investment value. The

25.0% capitalization rate used here is a 28.0% ROR reduced by 3.0% for

expected future earnings growth. Reducing the capitalization rate for the

expected future earnings growth is mathematically equivalent to adjusting

the earnings value for growth in perpetuity.

Discount for Lack of Marketability of 25.0%. A discount for lack of mar-

ketability is a recognized business valuation concept and, as dened in

the International Glossary of Business Valuation Terms, is “an amount or

• Magnitude of investment; market potential

• Staging of investment (early; first; mezzanine)

• Years to break even

• Syndication possibilities

• Target IRR

• Investment time horizon

• Terminal value of firm at exit

• % ownership required by VC partners

• Deal structure (board seat; management)

VC investment criteria at-a-glance

Figure 13.6 VC investment criteria—How do venture capitalists think?

Valuation Techniques ◾ 263

percentage deducted from the value of an ownership interest to reect the

relative absence of marketability.” The discount applied here is such a reduc-

tion in value applicable to the subject valuation.

Discount for Lack of Control of 15.0%. A discount for lack of control is a

recognized business valuation concept and, as dened in the International

Glossary of Business Valuation Terms, is “an amount or percentage deducted

from the pro rata share of value of 100% of an equity interest in a business

to reect the absence of some or all of the powers of control.” The discount

applied here is such a reduction in value applicable to the subject holding.

13.6 Market Approach

The market approach determines the proposed value based on the price for

which similar businesses are being sold. The foundation of this approach

is the principle of substitution, which states, “a prudent buyer will pay no

more for a property than it would cost to acquire a substitute property with

the same utility.” The three primary methods are:

1. Comparable sales method—actual transactions

2. Guidelines companies method—public company data

3. Industry or broker rules of thumb

13.7 Asset-Based or Cost Approach

This determines the proposed value based on what the assets in that busi-

ness are worth. This approach separately values each asset and liability in

the business. It does not value the unidentiable, intangible attributes of the

enterprise. The two primary methods are:

1. Adjusted book value method

2. Liquidation value method (assumes that operations will be

discontinued)

13.8 Venture Capital Valuation

“Life is a dogsled team. If you ain’t the lead dog, the scenery never

changes.” —Lewis Grizzard

If you are seeking venture capital (VC) nancing, it is because you “have

arrived.” VC nancing is the last step in the private equity market. After VC,

264 ◾ The Guide to Entrepreneurship: How to Create Wealth for Your Company

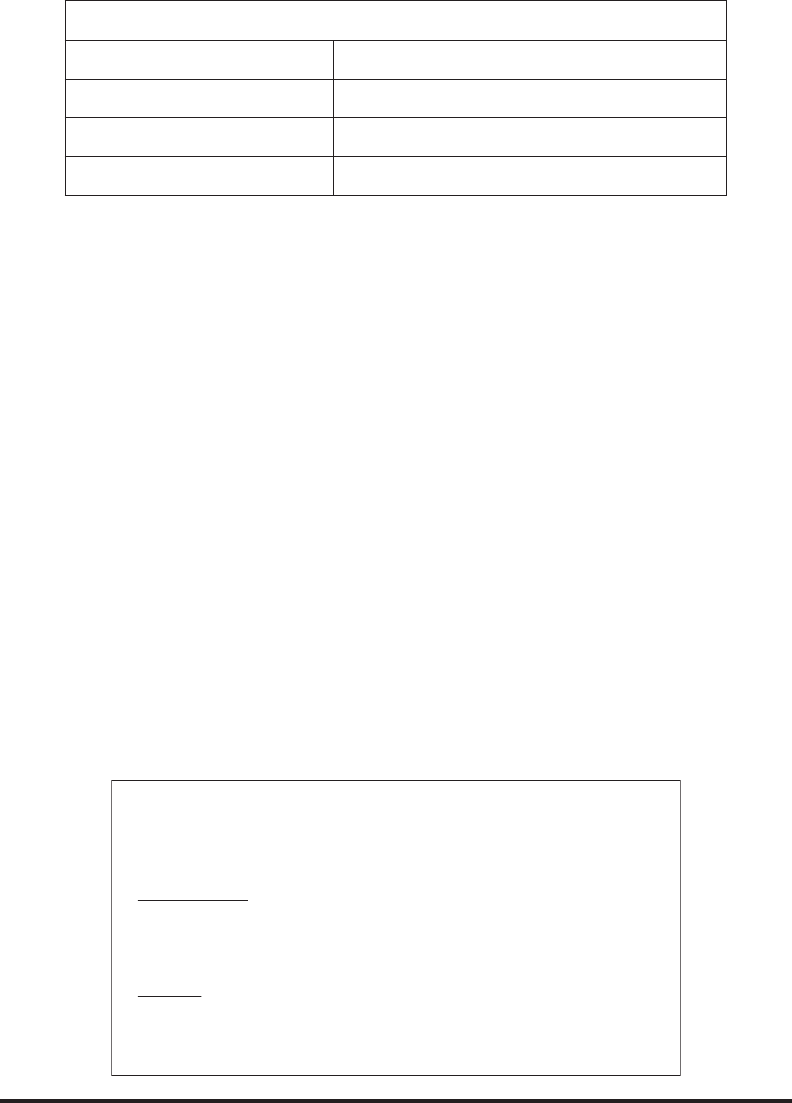

many companies opt to go public. The entire process can be summarized as

shown in Figure13.7.

A VC fund is a nancial intermediary, collecting money from inves-

tors and investing the money in certain companies on behalf of the inves-

tors. The VCs invest only in private companies that meet stringent nancial

requirements. After the initial investment, the VC actively monitors and helps

the management of the portfolio rms. The VC mainly focuses on maximiz-

ing nancial return by exiting through a sale or an initial public offering

(IPO). Last, the VC invests to fund internal growth of companies (organic

growth), rather than helping rms grow through acquisitions.

7

VC is a subset of the larger private equity eld, and refers to institu-

tional investments in early-stage, high-potential, privately held growth

companies. Institutional refers to investors that are not investing their

own capital (like the 3Fs or Angels), but instead invest moneys obtained

from pension funds, endowments, corporations, institutions, and very

wealthy individuals.

VC clients only are paid when there is a liquidity event, such as a com-

pany sale or an IPO. Liquidity events are popularly known as “exits.”

Liquidity events are infrequent; thus, VC investments are very risky. VC is

very risky because the equity investment is made in an immature company,

V.C. Financing rounds

Time

1st

2nd

3rd

Mezzanine

Later Stage

Early Stage

Seed Capital

Angels, FFF

IPO

Public

Marke

t

Bootlegging

Venture capital investments

Venture capital investments

Modified after Cumming, Johan “Venture Capital

and Private Equity Contracting”

Bank borrowings

2

nd

mortgages

Savings

Break

Even

Valley of

Death

Profits

Figure 13.7 Venture capital investments—VC nancial rounds start at the early stage

of development.

..................Content has been hidden....................

You can't read the all page of ebook, please click here login for view all page.