Knowing the Cost of Things

It is probably best to start this section by asking what is meant by cost? The answer to this question may seem, at first sight, very obvious. Most readers will say that cost is how much was paid for an item of goods being supplied or a service being provided. Unfortunately, it is not that simple. In the context of our organization, cost may be explained as the valuation in money terms of the effort, material, use of long-lived resources, consumption of utilities, wasted time, risks incurred, and opportunities foregone in making a product or service available to our customers.

For all organizations, one of the key essentials in determining our selling prices is to know the total cost of each of our products or services. This total cost is made up of two distinct components: There are those costs that are driven by a particular cost object and those costs that maintain our support functions. Let’s pause for a moment because I’ve used some terminology that you may not be familiar with. What do I mean by cost object? Many of you will immediately associate this term with the products or services your organization sells. That would be a reasonable starting point. On the other hand, they may not be the prime drivers of the money that you spend. I’m sure that in a number of organizations, especially service organizations, it is your customers, and their requirements, that really drive your cash outflows. If this is the case, then the customer is your cost object.

Think!

What is the primary cost object in your firm? Is it possible for us to have multiple cost objects? How might we try to manage that?

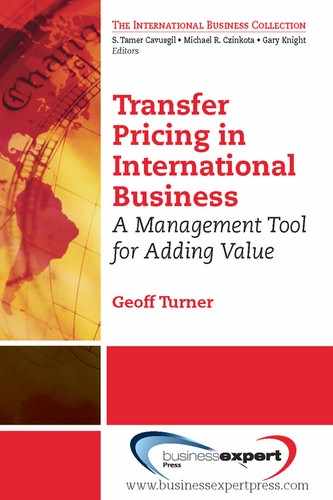

Nevertheless, whatever our cost object, we need to break down our total cost into those costs that are readily traceable to our cost object—the direct costs—and those costs that are necessary to support our productive activities but that we are not able to readily trace to our cost object—the indirect costs, which are often referred to as overheads. Figure 2.2 provides a graphical illustration of where the particular costs of a professional services organization, such as a law firm, might lie. In this case, the cost object is the customer, whereas in a manufacturing firm, the cost objects are more likely to be the products that are made. Any item of cost may be either direct or indirect depending on its traceability to a particular cost object. As a result of their traceability, direct costs are usually considered to be variable costs because they increase or decrease in line with changes in the level of activity of the cost object.

Figure 2.2. Cost elements.

Indirect costs, on the other hand, are more likely to remain unchanged in the face of moderately changing levels of activity and so are considered fixed costs. Since it is imperative, in the longer term, that we recover all of our costs to remain profitable, it is important that we have an appropriate mechanism to allocate these indirect, or fixed, costs to our cost objects in order to understand the full cost. This process of allocation is a significant problem for many organizations because it is not easy to understand how much of their indirect costs are consumed by their cost objects. If it was understandable, then we would probably consider them direct costs and our problem would go away.

Unfortunately, when using the total cost concept as a determinant of selling prices, this arbitrary allocation of indirect costs often results in misleading information about the total cost of a cost object. This, in turn, leads to inappropriate prices being offered for our goods or services. Indeed, on this basis, some folks like to say: Well, we’d have these costs anyway. Why should we include them in the cost of our products and services? The answer is simple: Indirect costs add up and significantly affect profitability. What is more, some products or services we sell consume significantly more overhead than others, which makes the perceived profitability of those products often inaccurate.

To make it easier for us to establish selling prices, we should strive to identify as many costs as possible in the direct category but, since we do need to understand the total cost of the things we sell, we may still be left with the need to allocate some costs. How should we go about that? Traditionally, the most common methods of allocating indirect cost have been based on a relevant direct input such as labor hours, or machine hours, or units of material. Old traditions die hard but the nature of our competitive environment is changing rapidly and the ways of old are proving insufficiently flexible to deal with the complexity encountered in our modern organizations.

Think!

How does your organization allocate indirect costs? Is that method really suitable for your business environment?

There are a variety of costing systems available for us to use,2 one or more of which will be relevant for our organizational situation. What is absolutely clear is that if we do not properly understand the cost of making a product or service available to our customers, we are likely to develop inappropriate pricing and marketing strategies. Even so, it is not essential to have the most accurate cost system. The aim should be to consistently understand the cost of making a product or service available to our customers, accurate to within 5% or 10%. The idea is to have the most effective costing system, one that balances the cost of errors made from inaccurate measurements with the cost of measurement. Getting close to understanding our true costs is exceedingly more valuable than not including any part of that cost in our pricing calculations.