Evaluating the Result

The first task in our evaluation is to look at the data that have been used in this example and restate it in more traditional terms. Figure 6.5 does that and expresses the outcome in just one currency, that of the home of Penny Farthing plc’s HQ, The United Kingdom.

Even without the operating profit generated by the final sale of the bicycles, the traditional performance measures suggest that a reasonable return is being made by the organization for all of those functions that are essentially driven by a transfer pricing mechanism. Nowhere, in any of our calculations to this point, was a profit requirement, perhaps the most contentious element of transfer pricing, used. While there will no doubt be debate surrounding the determination of the capital base on which the required return on capital is calculated, perhaps this model of determining transfer prices will find acceptance in the economic times in which we live.

Figure 6.5. Traditional performance measurement of Penny Farthing plc.

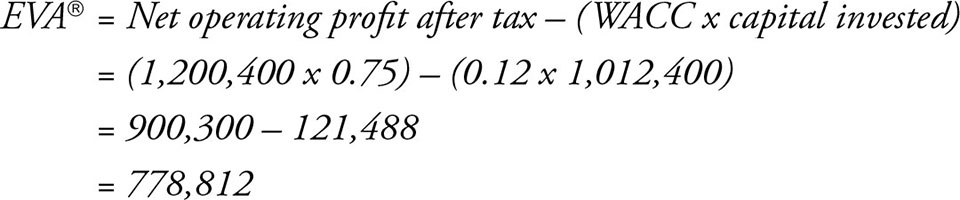

Finally, to complete the task that I set out to achieve, that is whether the transfer pricing model creates additional economic value for the owners of Penny Farthing plc, we return to the use of EVA®. Applying an average tax rate of 25% to the total operating profit, this transfer pricing model shows that we are creating the additional value added that is the fundamental objective of transfer pricing. Here is the calculation to support that statement:

Summary

I said in my preface to this book that any transfer pricing model should focus on managerial issues and in particular as a driver to add value throughout the organization. The model that I have presented to you in this chapter, which is based on the foundation that was developed throughout the book, has done just that. It will not be everyone’s ideal solution but it provides a starting point for discussion and further development.

No doubt many of you will be bewildered by the calculations that have to take place to arrive at an effective transfer price using this model. Fear not for, as long as you have the data available, an experienced user of enterprise resource planning (ERP) systems will be able to generate the necessary calculations from those data so that you will have access to an instantaneous transfer price for any product or service that you offer within your organizational family. If your organization is not big enough to run an ERP system, someone more proficient than me with an Excel spreadsheet will be able to build one for you as long as you are able to give them the underlying parameters.

This is achievable with thought but I’d imagine that the biggest task of all will be getting all of the data that’s needed in one accessible place. I can safely say it’s a task that needs to be done for you and will benefit considerably in the long run from doing so. Good luck with constructing your transfer pricing model!