Building a Transfer Price

Starting at the top of the tree with the organization’s HQ, which is based in the United Kingdom, there are four functional areas that we need to examine: strategic management, knowledge management, financial management, and legal services. Each of these has employees, some expenses, and an asset base that needs to be taken into consideration when determining the amount of management fee that will be passed on to every other unit in the organizational family in the form of a monthly or quarterly management fee.

The strategic management function provides advice and support in the establishment of business plans as well as conducting regular performance reviews with each of the member organizations in the organizational family. The knowledge management function focuses on human resource management as well as attending to all of the information technology needs of the organizational family. Data are processed in the cloud and performance reporting is online, real-time at each unit. The financial management function is responsible for negotiating for the financial requirements of the group and the preparation of statutory financial reporting for all units. In addition, it assumes responsibility for overall risk management, including the treasury function. Finally, legal services provide advice on legal issues arising anywhere in the world and are responsible for tax planning and the submission of all the necessary documentation with regard to tax matters in every jurisdiction. These activities form the basis of determining the annual HQ charge.

Figure 6.2 provides a summary of the calculations that are made to determine the management fee that will be charged and nominates the basis of making that charge to the other units in the family. Utilizing the basis of apportionment shown for each of the four functional areas, the annual HQ charge for each member of the family would be:

Figure 6.2. Headquarters capital base and costs.

|

DD |

£118,000 |

|

AY |

£825,600 |

|

BU1 |

£148,400 |

|

BU2 |

£187,300 |

|

BU3 |

£125,700 |

|

BU4 |

£139,100 |

|

BU5 |

£157,300 |

|

BU6 |

£148,400 |

The next member of the organizational family that we shall look at is the DD team, which is based in Switzerland. Perhaps, the most significant difference here is the amount of structural capital that exists in this area as a result of design patents and development improvements as well as the detailed instructions that are provided to the AY division to ensure the quality of the final product.

We also need to remember that the HQ charge that is incorporated into this cost structure is in Pounds Sterling and needs to be converted into Swiss Francs. This process is managed by the financial management team at HQ and the cost of doing it is built into the HQ annual charge.

Figure 6.3 provides a summary of the calculations that are made to determine the amount to be recovered and nominates the basis of making that charge to the other units in the family. Utilizing the basis of apportionment shown for each of the two functional areas, and assuming that the development cost will be recovered entirely from the AY unit, which in turn will pass this along to the individual business units, the annual DD charge for each member of the family would be:

|

AY |

CHF 507,600 |

|

BU1 (1 model) |

CHF 48,400 |

|

BU2 (2 models) |

CHF 96,800 |

|

BU3 (2 models) |

CHF 96,800 |

|

BU4 (3 models) |

CHF 145,300 |

|

BU5 (3 models) |

CHF 145,300 |

|

BU6 (1 model) |

CHF 48,400 |

Figure 6.3. Design and development capital base and costs.

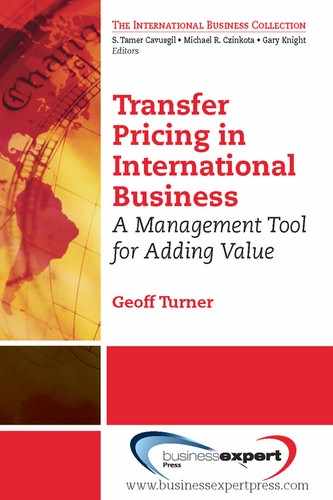

As we progress through the organizational family in the construction of our relevant transfer prices, we come to the end of the chain, which is the AY division based in Hong Kong. From here, the bicycles, of which there are four different models, are delivered to the six business units that are the Sales, Marketing, and Distribution outlets. From there, they are sold to independent retailers at various prices depending on what the local markets will bear. So, let’s focus on the AY function. Apart from collecting the charges from HQ and DD, the AY function has its own costs and capital base to consider. Perhaps, the most important difference here is the large amount of economic web capital. This arises because all of the component parts, including painted frames, are bought in from a network of suppliers located around the world. Also, most of its workforce is only considered to be human resources as they could be replaced very easily with equally suitable employees. Even so, there are a number of employees here who are treated as human capital because their knowledge of AY procedures, the various business divisions’ requirements, and management skills are highly valued.

Figure 6.4 provides a summary of the cost to produce one of each of the four models of bicycles and, as such, represents the FOB (free on board) selling price to all of the six business units that are the Sales, Marketing, and Distribution outlets. Individually, they will have different shipping costs, import tariffs, and operating costs of their own associated with the receipt and sale of the bicycles that need to be taken into account when deciding if they are able to make an adequate return for Penny Farthing plc overall. Although this last part is not a transfer pricing activity, it is essential to understand the whole picture. For now, we need to understand, using the more traditional measures of performance, whether building transfer prices in this way produces a positive result for the organization.

Figure 6.4. Assembly capital base, costs, and free-on-board selling prices.