CHAPTER 5

How to Convert Existing Clients: Be Passionate, Not Zealous

The most popular question I receive after “How do I create value-based fees?” is “How do I move existing clients from hourly billing to value-based fees?”

The answer is, “Very carefully.”

You've spent a considerable amount of time educating those clients “incorrectly”—and you've been very effective at it. You've also consistently enabled their behavior by replying to their demands for hourly or daily rates, reductions in rates, reductions in time, and perhaps reduction in numbers of people. They've become quite comfortable using your services in the manner maximally beneficial to them and minimally beneficial to you.

Other than that, it's been great.

Furthermore, you're highly credible! After all, your advice has been well received, your suggestions well taken, and your plans well thought through. Why shouldn't your billing scheme be as adept and effective as your consulting expertise?

Fortunately, that's the extent of the bad news. (I know, that's sufficient!) You've also developed a solid relationship with a buyer who would probably be very loath to see you leave, no matter how vigorous the protests against your fees and rates in the past. You also have a client base that permits you to set some criteria for which clients may be most suitable for “transfer” to a new billing arrangement. Finally, you're successful enough so that you might want to “fire” some clients rather than keep working with them on a basis that is unfair to you.

Nothing raises fees like your willingness to walk away from business. But remember, the first sale is always to yourself. While you don't want to take bread off the table, you also don't want your time so entangled with low-profit clients that you can't work for more and tastier bread in the future. We'll deal with that contingency in this chapter as well.

THE LITMUS TEST—SETTING PRIORITIES

The first order of business is to establish the decision criteria to determine which clients even to approach. A general “triage” system works best:

- High-potential clients for change to value-based projects

- Clients who could go either way but require more work

- Clients who will not change short of having their legs broken

To establish who's who on your list,1 I've created the test in Exhibit 5.1.

Depending on your client base, you might have as few as three or four candidates or as many as a dozen or so. The key is to approach each one with a clear and customized strategy (which we'll talk about in the following sections). But the good news is that you've been able to establish some parameters for your efforts. In essence, the top priorities can't be lost, so while the goal is to move them to a value-based system, the essential is not to drive them away.

Conversely, the bottom-tier companies aren't worth your time anyway. (One of my tenets is to deliberately abandon the bottom 15 percent of your business at least every two years, and these are your candidates. See my book Million Dollar Consulting for the details.) You could, theoretically, simply announce the change in your billing to them and allow the majority to disappear. (They may well be one-time clients in any case.) Those in the middle will require individual decisions, but their potential isn't high enough to demand that kind of attention at the moment. You might as well continue to collect hourly rates until you're ready to deal with them.

Let's be clear: You don't want to lose significant clients; that's the bottom line. You would like to transfer as many of them as possible to value-based fees. That's the goal. Ignore low-potential clients, and focus on increasing perceived value to high-potential clients.

Once you've identified the top priorities with which to attempt conversion, you can build those plans into your normal visits. In other words, you can lay the groundwork during your regular interactions with the buyer, rather than spring the “new approach” on the buyer in one fell swoop.

That groundwork can be laid with the following dialogue, observations, and reminders with the buyer:

- “Your people indicate they'd like to call on me more often, but they're justifiably sensitive to ‘running up a bill’ every time they need me, despite the fact that I can provide immediate help.”

- “Neither one of us can estimate how much time your request is going to require. I think we need to ‘stop the meter’ so that we can both invest whatever is necessary.”

- “I've begun a new relationship with new clients, and I'd be remiss if I didn't offer it to my best clients. Could we put some time aside to discuss it on my next visit?”

- “I know you've been somewhat unhappy about a ‘meter running’ and uncapped costs. I'd like to suggest a way to change that dynamic that will help both of us.”

- “I'd like to automatically be able to provide you with updates to my intellectual property whenever they develop.”

- “I think we'd both feel better if I were able to perform audits on the progress every 90 days for at least a year.”

- “You often have board meetings on Monday or early mornings during the week. It may be valuable for me to be available on some weekends or late nights for you.”

- Remote work and advice is far easier to arrange without your people having to calculate the time spend on Zoom or Skype or even the phone.

Before we turn to the actual strategies, please keep these four critical factors in mind:

- Every piece of new and potential business should be treated exclusively as a value-based prospect. Never offer any other kind of arrangement to new clients. Educate them correctly from the beginning.

- The first sale is always to yourself. You must convince yourself first of the advantages to the buyer before you can effectively employ this change strategy.

- Although the idea is to retain the client at all costs, you can't be fearful. Enthusiasm, assurance, and absolute belief carry the day. Hesitancy, tentativeness, and uncertainty will waste everyone's time.

- You must provide additional value as perceived by your buyer.

OFFERING NEW VALUE

The most important and most effective method for converting existing clients to a value-based fee system is to offer new value. There is no reason in the world for a client to move from your hourly or daily rate to a fixed fee for the exact same value the buyer is now receiving. Think about it: If people change only in accordance with their own self-interests (“What's in it for me?”), why abandon a clear, reasonable (that is, cheap), and long-standing billing arrangement?

Well, you abandon it if a new system provides more value and better appeals to their self-interest. I'm going to say that again: Clients will abandon an old system if a new system provides more value and better appeals to their self-interest.

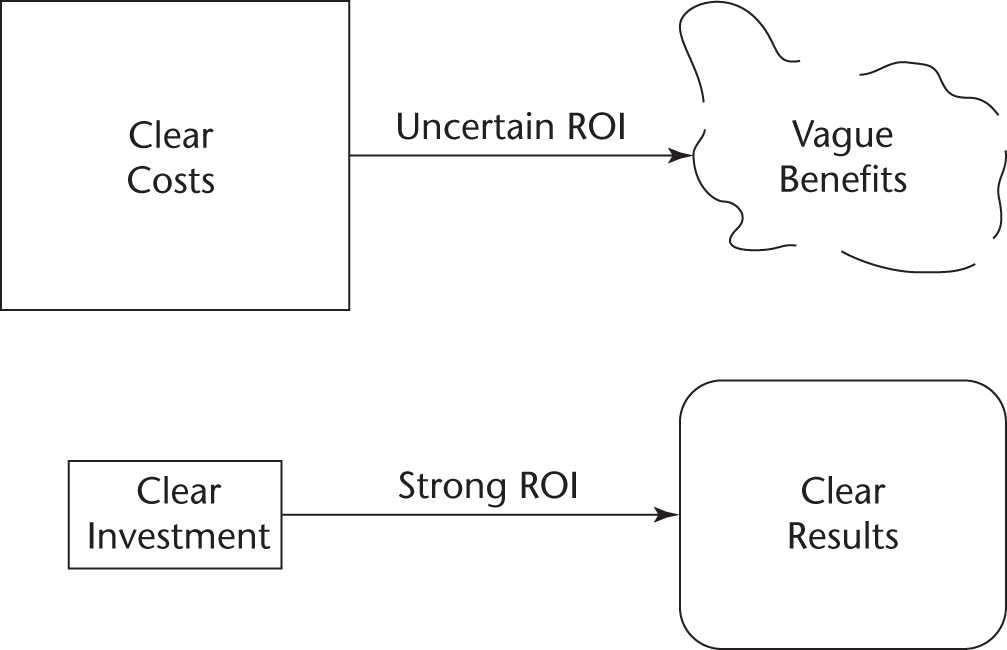

If you focus on nothing else, focus on that. What new value can you offer the buyer in the next phase of the project, in a new project, or in the negotiation of a new agreement that will encourage consideration of switching to a value-based system? Remember our graphic from Chapter 1, repeated in Figure 5.1. We have to create a dynamic in which the buyer appreciates the greater value inherent in a new, clear set of benefits so that the investment seems extraordinarily reasonable.

Here are some examples:

- I would pay more for postage if the postal service picked up at my door or delivered in the early morning.

- I would pay more for groceries if they were delivered (as they are in some major cities).

- I would pay more for copy services that also sent my work automatically to chosen destinations (which some shops will do).

- I would pay more for more leg room on an aircraft.

Figure 5.1 Revisiting ROI

- I would pay more for technical assistance available 24 hours a day by phone.

- I would pay more for medical testing that provides same-day results, preferably within an hour.

You would pay more for your own set of high-value needs. Ergo, you must determine what your client would pay more for, since value-based pricing must provide more income than hourly or daily work.

Here are some generic methods to provide increased value with existing clients (whether on new projects, which are easier, or existing projects up for expansion or renewal). You can further modify and strengthen these with specific details for each unique client relationship.

Unlimited Access

Provide “unlimited access” to you. That's not as severe as it sounds. At the moment, the client must make an investment decision every time you're needed (“Is this problem and Alan's help worth $4,500?”). That's a terrible position for the buyer to be in. Offer access at any time, subject to mutually convenient schedules, by phone, Zoom, e-mail, or in person, if needed.

No client will abuse this privilege (just as no executive was ever prohibited from performing by too many people walking through an “open door”). However, it does provide the immediate perception of far more extensive interaction for a fixed fee.

I've been providing “unrestricted access” to my elite coaching clients for over 20 years and not one person has ever abused the offer.

New Services

Let's say you've been doing executive coaching. Introduce a 360-degree feedback intervention, and tell the buyer that you'd like to combine, in the buyer's best interests, the existing coaching work and the new instrument into a single fee for management coaching services. If you're helping with strategy formulation, offer a planning process that bridges to implementation. If you're doing diversity audits, offer a training package for managers to use the feedback properly.

New services, which might seem prohibitive on a per diem, cumulative basis, will seem like a bargain when combined with ongoing services under a single fee for a finite time frame.

Wider Access

Demonstrate that the results you've been generating for the financial area can be readily duplicated in other support areas: human resources, IT, legal, and so forth. But show that the current hourly basis will be unnecessarily severe, since a great deal of the work is repetitive.

Offer to combine as many other operations as requested under a single fee (even if various budgets contribute to it).

Combined Buyers

If your projects typically involve several buyers who each contribute to the budget, then suggest that by operating under a single fee, their respective contributions are capped, they no longer have to battle about who should pay for which aspect, and you can be responsive to all of them without additional investment.

Value-based fees can be strong compromises for the client who is unsure which budgets should be used, how to charge back time, and how often to take advantage of the consultant as a resource.

New Access Points

Perhaps you can provide a special set of web pages to that client only, using a password; or you can create a newsletter oriented toward the client's employees; or you can arrange a special toll-free number; or you can place the client's logo in books that are ordered from you. As part of a value-based proposition, find new and unique access points so that the client feels a more comprehensive relationship.

Don't be afraid to ask the buyer what he or she would find most desirable in terms of a more comprehensive, sustained, and interactive partnership. You may be able to provide the desired service at virtually no cost but use it as the basis for a higher, value-based fee.

Finally, discipline yourself to unbundle the potential value propositions that you can deliver to a client. Use an easel sheet or a spreadsheet or have a colleague help you determine the full array of services you can deliver. I guarantee you that (a) it's far more than you think or (b) it's all combined into a single, grand alternative that you deliver each time.

“Membership” in Perceived Benefit

This can include an “insider” web site or newsletter, automatic provision of “best practices” regularly from around the globe, discounts from other professional service providers, and joint bylines on articles contributed to by the client.

Use the strength of your own community to include excellent clients in interactions (breakfasts, teleconferences, chat rooms, and so on) only available to your elite buyers.

FINDING NEW BUYERS WITHIN EXISTING CLIENTS

If you operate in the small-business, closely held market (for my examples, under $50 million in revenues), there is probably a single buyer who is the owner or CEO. But in larger markets, there are scores or even hundreds of buyers. The problem is that we don't reach out laterally while we're effectively delivering our consulting help.

A new buyer within an existing business does not necessarily have to undertake a project with you on the same basis as others have. The important strategy is to refrain from educating the new buyers incorrectly, as you have the existing buyers!

The advantages of new buyers within existing businesses include the following:

- There are no marketing or acquisition costs.

- The buyers have heard of you or can readily become familiar with your work elsewhere within that client system.

- They respect and know the people who have hired you in the past.

- They are probably not familiar with your prior billing policy.

- It's easy to see them and to accommodate their schedules, since you're onsite frequently.

- Results you've generated elsewhere can be made relevant for them.

Remember that buyers are seldom perched solely at the very peak of the organizational hierarchy. They need to meet only two criteria:

- Does your value proposition enhance their goals (their self-interests) professionally and/or personally?

- Can they write a check (or cause the computer to disgorge one) to acquire that value?

I've seen consultants virtually wade through groups of potential buyers while hurriedly on their way to the cafeteria. That's a lost opportunity. You have to be willing to do a little marketing while you're on the client site.

How do you do that gracefully? Well, if you believe that new buyers within the client organization represent new sales that can be placed on a value basis, then they deserve quite a bit of effort. Here are seven tactics to reach them efficiently and effectively:

- Ask your current buyer for recommendations. This is anathema to many consultants, but a pleased buyer should have no hesitation about sharing your value in the company so long as that buyer is not shortchanged. (In fact, in terms of self-interest, the buyer can often claim credit for “discovering” you.) The salient point here is to ask and even to seek an introduction. This is the single most overlooked avenue of expanded business and potential conversion business (to a value basis).

- Seek out meetings at which to present your reports and suggest that “interested others” and support groups attend. I've presented results at any number of management meetings where people have come up to me and asked, “Can you do that same thing for a support organization?” or “Is it possible to do that overseas?” Guess what? It always is.

- Listen for key names of power brokers, and when you find yourself with them for any reason at all, introduce yourself. After a second or third encounter, ask them for some time to discuss the ramifications of your work in their area.

- Publish in the organization's house organ or, even better, allow them to interview you and discuss the results of your work. I once received a six-page, color spread in Merck's in-house magazine on my ethics audits, which brought inquiries from managers I had never even heard of. This is a very effective, objective way to reach out to other buyers.

- Offer to brief support units, internal customers, internal suppliers, and any other even remotely interested parties. Explain to your client that a synopsis of your work might help others help your client and that sharing the work will certainly earn admiration in any case. One-on-one or small group briefings are usually the best, since you want to focus only on potential decision makers.

- Volunteer within the company. I've donated to company-sponsored charities, attended award ceremonies, participated in picnics and recreational opportunities, and tried to become a “part of the crowd.” You never know who you'll wind up meeting in comfortable, social, and convivial circumstances.

- Monitor personal changes, promotions, transfers, and other internal events. You never know when someone with whom you've had positive interactions will move into a buying position. It helps to read the house organ, bulletin boards, and other in-house media and to use things like Google Alerts to receive any press releases sent out by your client.

Finding new buyers within existing clients is essential for any highly successful consultant but absolutely critical for the consultant who wants to convert existing, high-potential hourly clients into long-term value-based clients. Start off with them as “new” clients whom you can educate properly.

FINDING NEW CIRCUMSTANCES

The final tactic for converting clients to value-based pricing is to find some client in a market, or environmental circumstance that supports the reasoning for such a change at this particular juncture.

Some new circumstances will be obvious, but others are more subtle. Yet all can serve as your “transfer mechanism.” Here are some examples:

The Great Year. The client has had an outstanding year, not least in part thanks to your assistance. Suggest to the buyer that this is a time to consider a more comprehensive and more flexible relationship. Also, never neglect the fact that at the end of any budget year, there are funds often crying to be used or lost. It's tough to put those funds against hourly billing that is not based on any specific amount of hours, but it's relatively easy to put those funds against a clear-cut $100,000 project.

The Horrible Year. Your client might have had a disaster, not due to anything you did, of course. There might have been some client defections, unexpected costs, loss of technology, whatever. Think pandemic if you need an example. If the client is happy with your help, however, suggest an easier and less burdensome way to work with you next year, since the fees will be capped, fixed, and otherwise locked in cement. That way, you can't be part of an escalating cost problem, and you can't be cut in a client's effort to address a cost problem. That's win-win.

The New Buyer. Most consultants search for arsenic when their buyer is promoted, fired, replaced, transferred, or otherwise misplaced. But this is really an opportunity to educate a new buyer correctly, rather than try to re-educate an old one accustomed to old habits. View a new buyer as an opportunity, and don't allow past practices to continue (hourly fees) without strong resistance (in the form of the buyer's self-interest). And make sure to track your old buyer like a beagle.

The Acquisition. Chaos generally ensues when even the most orderly acquisition is contemplated and consummated. Suggest that this is the time to simplify everything possible, including your billing arrangements. The acquisition might also present an opportunity in terms of the other conversion factors (such as a new buyer) we have discussed.

The Divestiture. Although not strictly within the existing client, the new spun-off or purchased unit probably represents high potential for you because you were familiar with it when it was still part of the original organization. Do your best to remain in contact with current acquaintances moving into the new configuration.

The Competition. If the competition has pulled a surprise or the competitive marketplace is heating up, suggest that the increasing demands and uncertainties create an unfair situation for the client on any kind of per diem basis. Since ambiguity makes it nearly impossible to calculate hours or time, offer a set fee to create at least some order out of the uncertainty.

The New Initiative. Almost every organization regularly trots out a new initiative, hot product, reinvention of itself, or some other strategic change (often fostered by a new leader in a key position or the latest academic's fad). Jump on that bandwagon, and use the initiative as an excuse to alter the past fee basis.

The Travel Need. Where travel is a necessary aspect of your project—especially international travel—demonstrate that per diem fees often keep running, although you're just traveling from one place to another. (If you don't charge when you spend two days flying and acclimating to Europe or Asia, you're suffering from more than merely jet lag—you're crazy.) A value-based project fee, including all travel time (although, of course, not travel reimbursement),2 will remove that unnecessary expense.

Within your existing clients who are still on a time-and-materials basis, be alert for opportunities to promote a change to value-based fees. In fact, you can use this “new circumstances” approach with your moderate-priority clients as well.

THE RESISTANCE

Don't push so hard that you cause ill will if your clients resist converting. Position your intent as serving their best interests, and point out that other clients—and all new clients—have chosen to take advantage of the new arrangement. But by offering them this as an option, you're not taking bread off the table, since the client may still choose to continue along the current path.

Of course, if you prefer to end your relationship with a client—see my comments about abandoning the bottom 15 percent of your business periodically—then this is an ideal way to do it! See the next section.

But if your top-priority clients resist, here is the course of action that might still win the day later on:

- Don't persist, but do remind. Once a quarter, remind your buyer that the option is still on the table. Every time one of the conversion opportunities discussed in this chapter arises, raise the issue again as the basis for a decision about the new project. There is too much potential profit at stake not to remain persistent, and the more money you make from a client who is resisting a value-based approach, the more money you are actually losing over the long term.

- Appeal to the buyer's sense of fair play. If you can demonstrate a multimillion-dollar savings or improvement (see Chapter 4 for objectives, metrics, and value), and you can show that your total hourly fees added up to 0.001 percent of that improvement (which they well may have), you do have a case to point out that future projects should be more of a win-win endeavor. Many buyers will be reluctant to allow a disproportionate situation to persist if they envision needing your help on an even larger scale in the future.

- For some clients, you may be able to cite their own methods as a justification for how you should be treated. Does the client charge for value (everyone from automakers to restaurants actually do), or do they charge by the hour and are themselves unhappy about their own meager profitability? (Bentley doesn't charge based on how long it takes to build a car.)

- Try to arrive at a halfway point by influencing the buyer to commit to a minimum amount of time, guaranteeing you some basic revenue figure. Point out that you've had to put blocks of time aside in anticipation of the client's needs and often short-term demands and that some quid pro quo is appropriate. It's less of a jump from guaranteed fees based on minimum days to value-based projects.

- Provide the client with some independent endorsement of the value of project fees over time and materials. Use some third-party articles, trade journals, newsletters, and whatever else you can find that objectively demonstrate to the client that he or she is falling out of step with the times.

- Revisit at the proper time. The buyer may change, conditions may change, and finances may change. Don't take a refusal as a permanent denial. Simply bide your time and make another attempt when the situation seems better for you.

If you have a strong relationship with these clients and you continue to deliver results, they have the option of continuing as they have been, and there is only a minuscule chance of losing them by asking them to consider a different fee basis. However, you are at great potential risk if you choose not to do this out of fear of losing them, since the more work you obtain from them, the more profit you are leaving on the table.

Remember, leaving $100,000 “on the table” each year creates a half million “lost” over five years that you'll never recoup.

ABANDONING BUSINESS

This has remained one of the most controversial concepts I've ever introduced but also one of the most powerful in providing consultants with the means to acquire higher-profit, value-based clients.

We become accustomed to certain kinds of business. We tend not to question that business but rather to allow it to accrete, like a stalactite growing from the ceiling of our office. It's always been there. Why fret about it now?

Unless we abandon business regularly, we give ourselves no leeway to reach out for new and more profitable business. Our time is usurped and our energies depleted by business that not only can't be converted to more lucrative arrangements but is actively impeding us from converting (or acquiring) other, higher-potential business.

We tend to rationalize hanging on to certain business with a death grip, reassuring ourselves with platitudes:

- They were there when we needed them. Early business that helped pay the bills is not something we easily forget.

- The job's easy to do. (We don't feel we're really exerting ourselves, so why not? It beats working hard.)

- It's fun. (We love the adulation or the experience or the environment. Our ego is rewarded, and it brightens our day.)

- We have an enduring friendship. (The buyer or others have become friends to whom we feel we owe an allegiance beyond mere business considerations. We don't want to jeopardize that relationship.)

- We need to await promised returns. (We've been promised, time and time again, “exposure” for our earlier, inexpensive work, and we still haven't cashed in. Like poker players who have gone too far in a hand they can't possibly win, we're reluctant to cut our losses.)

- We have the time. (The erroneous belief that “something is better than nothing” drives us to accept and perpetuate questionable business.)

- What if other business disappears? How can we then justify cutting this business loose? (Actually, not cutting it loose will cause other business not to appear.)

- We're trapped. (Scope creep and constant concessions have built up a raft of commitments that we honestly won't ever be able to discharge, not unlike miners who, despite their pay, were forever in debt to the company store. Remember the song “Sixteen Tons”? Okay, I'm older than you.)

- We feel it's a personal failure to lose a client, even if we initiate the departure. (Don't take it personally; it's just smart business.)

Abandoning business doesn't have to be as draconian as it sounds. First, make an objective assessment of all of your business every 18 months or so. (Do it between fiscal years so you won't be influenced by your own planning needs.) Ask yourself these questions about each single client:

- Am I learning regularly?

- Am I still adding value that others can't?

- Am I being paid as well and is my profit as great as with new clients?

- Am I being stretched and forced to grow?

- Am I introducing new products and services on a regular basis?

- Am I using the client as a referral or springboard into other systems?

- Am I able to experiment or use marketing leverage in this “lab”?

- Am I enjoying this project and having fun?

- Am I constantly reducing my labor intensity?

If the answer to two or more questions (it doesn't matter which questions) is “no,” plan to move on.

Next, contact the client and arrange for a constructive transfer to another consultant. There is no need to leave the client high and dry. Simply point out the answers to your own questions (“I'm not learning, and I'm no longer contributing unique value”) and arrange for someone to take on the project who will see it—at this point in his or her career—as thrilling, subject to further improvement, and lucrative. Remain on board for a time or until the next renewal, or depart as soon as new introductions are made. But get out.

My advice, by the way, is not to subcontract this or otherwise take a “piece of the action,” such as a referral fee. Doing so ethically obligates you to be accountable for the outcome and may leave you continually accessible to the client (directly or through the new consultant). Cut the cord, forsake the revenue, and move on.

If the client balks about “abandonment,” simply point out that it's really in the client's best interest. You can't afford the requisite time any longer, and the client will be better served with “new blood.”

Danger: If the client responds with an offer of more money, which sometimes happens (because you've been working so cheaply), turn it down cold. The new amount will still be less than your new margin goals, and your time will be usurped as much as, if not more than, before in return for an insignificant increase in fees. Don't be lured by the client's guilty conscience.

Finally, remain in touch, and use the client as a reference and referral source. Maintain a friendly relationship, although not a business one. You're actually doing the client a favor, and you shouldn't feel the need to skulk out the door.

Unless you deliberately, proactively, and methodically abandon business, you'll be unable to convert any higher-priority clients to a value-based approach, nor will you have the time to acquire new business at the rate or pace that makes sense.

You have to let go to reach out. Let go of those who can most easily go their own way before more important clients let go of you.

CHAPTER ROI

- Existing clients can be converted to value-based clients, but you must set a careful priority.

- Never take bread off the table: offer the option to continue the current relationship or to change. Sweeten the latter by pointing out that new clients prefer it, and you'd be remiss if you didn't offer it to existing important clients.

- Always offer more value, find new buyers, or look for new circumstances. The change must always be clearly perceived as in the buyer's best interests.

- You can use the test in Exhibit 5.1 to determine the highest-potential opportunities and then devise a strategy around each particular client.

- Approach only a few clients at a time, because the process demands careful and rapt attention. The buyer must clearly see the increased value, so be prepared to demonstrate that improved condition (for example, “unlimited access” to your time and expertise).

- The lowest-priority clients for conversion are also those who are your highest priority for dropping. Every 18 months or so, you should systematically examine your client base—again using objective templates and criteria—to determine which ones you can let go of in order to reach out to new and more lucrative business.

- All new business should be approached as value-based prospects and should never be given the option of a time-based or time-and-materials arrangement. By also culling out and setting priorities among your existing business, you should be able to convert your practice to an entirely value-based one in a few short years. That alone will represent a dramatic increase in your profits without any substantial increase in your work.

- Don't give up. Try at various times as conditions warrant. They can't say yes if you stop asking them.

Don't try to convert every client to value-based fees, and don't stop trying if some balk or resist. If you convert one or two high-potential clients, you will have created huge new margins for yourself. Life is about success, not perfection.

INTERLUDE: THE CASE OF THE LOADED LOADING DOCK

I once worked for a training firm that charged either by the number of boxes of training material purchased or the number of people sitting in a room. This is the antipodal position from value-based fees, and it's why I swore I would never get into that business again once I left it.

Essentially, whatever the printing presses, onsite long before digital printing, could disgorge onto the loading dock, we were to sell. As the year wore on and we were closer to year-end, the more the dock filled and the harder we sold. To give you an idea, we sold two-thirds of our total revenue in the fourth quarter and two-thirds of the fourth quarter in December.

As you can imagine, many of our clients caught on to our predicament and deliberately waited to buy near the end of the year, fully aware that we were desperate to clear the loading dock. Thus we drove our own prices down, offering “fire sales” that our clients became conditioned to anticipate. That meant that we had to sell even more material to make up for the lower prices.

It was a vicious cycle, repeated each year with the repetition and discipline of penguins marching to the pole to lay eggs that had only a 50 percent chance of hatching.

It dawned on me at some point that we were not driven by our technology, our clients, our markets, or even our products. We were driven by the production capability. We were actually a production-driven outfit, no less than U.S. Steel or International Paper. This wasn't the professional services future I had in mind for myself!

Don't allow your production ability to determine what you sell or what you charge. In the depths of oversupply of paper, the big paper companies used to reduce prices and take deliberate losses, since that was cheaper than shutting down the papermaking machines!

Don't burden yourself with delivery people, software, inventory, and other stuff that demands that you unload it, use it, or move it.

Moral: If you live to move materials, hire a moving company, but don't go into consulting.

NOTES

- 1. Since this series is aimed at highly successful consultants, my assumption is that your firm has a dozen to two dozen active clients and another dozen to two dozen periodic clients. But even if you have fewer than that, the criteria will still apply, and you should use them to differentiate among your buyers.

- 2. There is nothing wrong with including all your projected travel costs in your fee, as long as you feel you have a firm idea of what they will be. That's even a purer billing form, since everything is included.