CHAPTER 6

Resist the Razzle Dazzle: How to Judge the Beauty Contest

Overheard:

A well‐known investment strategist shared an embarrassing episode. During a sales call he was asked a question by a prospective client. After he proudly delivered his “expert” answer, the investor replied with exasperation, “I asked you what time it was, and you told me how to make a watch!”1

Investors don’t want to know every detail of the portfolio management process, and often complain about how dry—or worse, truly boring—many investment professionals are. On the other hand, nobody wants a song‐and‐dance routine like Richard Gere’s in Chicago, when he dances across the courtroom dressed as a nightclub entertainer.

The common complaint of investors—that advisors give too much detail and go on and on with arcane terminology—is a valid one. Frustrated and bored, the investor tunes out. But there are ways to remedy this situation.

First, level the playing field

The process of interviewing several advisors is often called a “beauty contest.” And like all beauty contests, you need to know what’s going on behind the scenes lest you risk being fooled. One family hired an advisor after interviewing three others because the winner showed them what their portfolio would have made if they had invested with that firm for the past three years—right up to the week before the presentation. Wow! Everyone was so impressed at the portfolio’s stellar performance—in the simulation.

What the family forgot, however, was that all the other advisors they interviewed should have been given exactly the same opportunity to show how they would have performed over that same period. They also should have been more attentive to start dates. Part of the reason why their returns showed such an upswing was that the presentation began on March 9, 2009—the very lowest point of the market’s collapse post–financial crisis. Had this family compared all four firms fairly, their initial “Wow!” would likely have become a much smaller, qualified “wow.” Requesting such uniformity in presentations can guarantee fairer competition and better due diligence.

Do you want an apple or an orange?

Another classic mistake is having a competition among four very different advisors. That’s like having a fruit contest—best‐in‐show for all kinds of apples, but you let bananas, oranges, and blueberries enter the contest. No wonder you get confused. Trying to compare apples to oranges is lunacy. The same is true in the world of selecting advisors.

All too often, investors will invite an investment banking firm, an asset management firm, a private bank, and a financial planner to compete for their assets. The professionals at the firms are each calling themselves “advisors to clients like you,” so you believe they can be easily compared. Unfortunately, the firms are so different in their structure and their fees that you end up judging a beauty contest between an orange and an apple. You will probably select the professional you “like” the best, not necessarily the best advisor for you. You make this mistake because of the very confusing nature of the financial advice industry. With so many different regulators, regulations, and fee structures, it’s no surprise you end up befuddled.

Do go ahead and interview all four if they seem like interesting and deserving candidates to become your advisor. However, insist that all four firms answer the same exact set of questions. That way, you’ll protect yourself from comparing an apple to an orange.

When it comes to fees, the fruit basket becomes a huge challenge!

Brokers may charge you for each transaction (their commission), but will custody your securities for free—unless you are a wrap fee (sometimes called a Turnkey Asset Management Program or TAMP) client. If you are, the broker’s fee will resemble the asset management firm’s, and there will be no commissions per transaction.2 The broker does receive a commission for selling you a TAMP account. But so, too, might any advisory firm’s professional who wins you as a new client.

Banks may charge to custody your assets, and for asset management as well, but there is probably no commission for each transaction.

Financial planners may charge you an all‐inclusive fee for asset management, custody, transactions, and a financial plan. Or they might offer you a “menu” that you select from as you wish.

Asset management firms may charge an asset management fee, and brokerage fees may be extra for each transaction. Most firms should, and do, insist that you hire a separate and independent custodian.

OCIO firms use a wide variety of fee models. An Outsourced Chief Investment Officer [OCIO] might be employed by any of these other firms, or be an independent entity.

Confused yet?

So, given this jumble of fruit, how can you ever tell who will provide the best value? You can’t for sure, but your own insistence on clear answers in writing will move you closer to a reasonable fee comparison.

See what’s included in that all‐inclusive package

What you also need to evaluate here is the depth and the quality of advice you receive, including service, online reports, tax or other special/customized advice, and performance. Just as more expensive fruit may have features you consider important (e.g., organically grown, no pits), an advisor you interview will have capabilities or services you may not wish to pay for, like serving as a trustee, an alternative investment fund, or offering tax advice. You might ask the advisor to unbundle the fee, or see if you can opt out of certain services in order to reduce your fees. Simply asking that question establishes you as an informed investor—one who wants to know precisely what you are paying for.

Are you my mother?

In P. D. Eastman’s childhood classic, Are You My Mother?, a baby bird who fell from the nest first asks a dog, then a cat, “Are you my mother?” before finally reuniting with the mother bird.

Be careful not to let your fervent hope of finding the best advisor (aka “your mother”) distract you from a clear‐eyed evaluation of every advisor you interview. The following three tips can work wonders and make the entire “beauty contest” far more objective and successful.

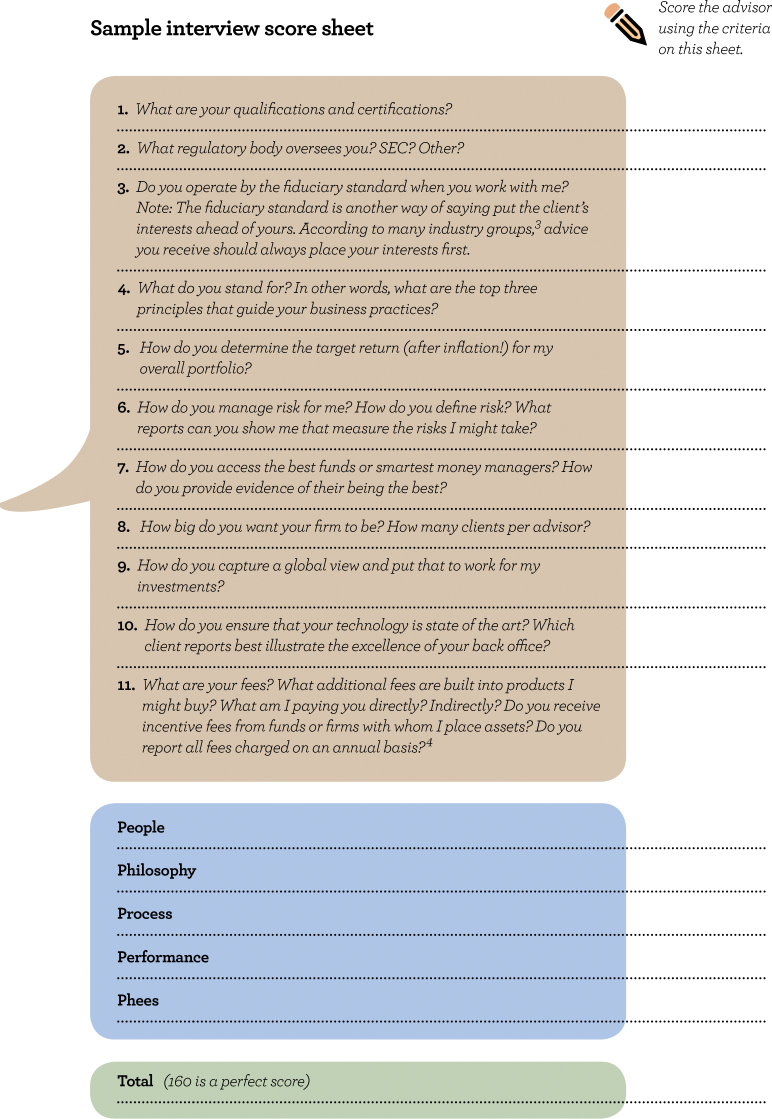

- Have all firms you interview answer the exact same questions.

- Answer each question with a number that allows you to see a total score that may surprise you.

- Incorporate the five Ps—people, process, philosophy, performance, and phees—into your evaluation, also assigning a numeric rating to each.

When you are done interviewing everyone, look at your total scores for the firms—not because you will necessarily make your decision based on these scores, but because you will gain insight into your own reactions while you were actually in the interview. For instance, was one presenter so personable that you listened more intently? In contrast, was one presenter arrogant but had a very impressive track record? You may be smarter by the fourth interview, or see things quite differently by the third interview—all useful insights that will help you make a more informed final decision.

One last question to ask yourself: “Do I like this advisor?” It’s a simple question, but an important one. Just as a tie goes to the runner in baseball, if you see two advisors who score equally well on the tangible items, likeability can be the tiebreaker. Remember: If you don’t feel comfortable interacting with—or enjoy listening to—this advisor, you are headed for trouble in future meetings.

A perfect match?

The more your advisor’s current clients resemble you, the more likely you are to be happy with that advisor and firm. For instance, if the advisor has mostly unsophisticated investors as clients, the firm may not relish the questions you ask. Or, if the advisor communicates primarily by email to his or her clients, that style may be incompatible with your preference for phone calls. But how can you be sure that these issues of incompatibility won’t surface before it’s too late and you’ve already hired the advisor? One way to learn more about the values of an advisory firm you are interviewing is to ask who the firm considers to be its competition. Then ask how the firm is different from those competitors. If no competitors are named, that may also be cause for concern. If you are surprised by the names you hear, probe further to uncover why those firms are viewed as competition. Every firm has competed for business, and most know which ones they resemble. Hearing advisors describe how their firm is different can be very educational.

Candor is a two‐way street

A common complaint from advisors is that investors don’t devote enough time to understanding their own investor personality or approach to decisions about money. However, if you did your homework from earlier chapters, you have your own list of what you expect from your advisor. Just as investors prefer their advisors to just “tell them what time it is” as opposed to “how to make a watch,” you must first tell the advisor what time zone you live in!

You need to be candid at your first interview about what you want and expect from this advisor. You and your advisor can custom tailor an investment plan only if there’s an equal give and take.

Most investors hope (and even strongly believe) that there is just one perfect investment strategy or best advisor for them. In fact, this depends on what “time zone” you are in—where you, the investor, “live.” Where you live depends on your personality, self‐awareness, family situation, the depth of your experience with securities markets, and most importantly, the goals for your wealth.

Next, turn the tables and ask the advisor to tell you where his or her ideal client resides on the quadrants of sophistication and control.5 Then reveal where you land, and discuss the implications. This conversation initiates a most valuable dialogue on what services you expect and how willing this advisor is to provide what you want.

What about references?

Do not hesitate to ask other investors about this advisor in online forums or at conferences. Do a Google search on the firm, and last but not least, do a search on the SEC website for any violations or open litigation. All SEC data on registered advisors, including the disclosure forms, are required to be filed annually and are available on the SEC website at www.sec.gov.6 For other professionals such as brokers, there are self‐regulatory groups like FINRA7 that post background information on both the individual and the firm. Be wary. A 2014 report in the Wall Street Journal revealed that 1,600 stockbrokers’ records failed to disclose bankruptcy filings, criminal charges, or other red flags, a violation of regulations.8 There can be rotten apples in any barrel, and you may need to dig deeper. References can help.

Once you are ready to hire this advisor, ask to speak with at least two or three current clients. Everyone knows this is not a perfect process because what firm will give you names of unhappy clients? However, you may also ask for, but may not receive, the names of former clients to contact. I was asked only once for a former client as a reference in my 20+ years on Wall Street, and we so wanted that business that we gave a name for this prospect to call. Happily, we won the business because of our willingness to provide a riskier reference.

When you call (sometimes firms prefer the client call you at a designated time), be open‐ended in your questions. Write down the answers you hear.

- What do you like best about working with this advisor?

- How long have you been a client?

- Tell me about a problem you had, and how the advisor addressed it.

- What advice might you give me on being a new client?

Be patient. This phase of your search can take a while. However, you will be well prepared for a smoother beginning if three references answer your questions in any detail.

Did you ever have to finally decide . . . pick up on one advisor and leave the other behind?

You have made your decision.9 Congratulations! Now the work begins to build a truly successful and mutually beneficial partnership with your advisor.