CHAPTER 10

Aging—Grave Concerns

Overheard: “I may be 70 chronologically, but I’m still 19 years old in my mind.”

Well, it happened anyway. You, the generation who loved to proclaim, “Don’t trust anyone over 30,” is now officially old! You Baby Boomers (I’m in that cohort, too) are now all in your sixties and early seventies. There is a ticking time bomb of aging that no one can stop. Your attitude toward your life—and your inevitable death—will color everything you do, or fail to do. Begrudgingly or good‐naturedly, you learn how to adapt to your changing physical self. How you handle managing your wealth must also change before it’s too late. Here’s why.

While research has proven how aging brains do indeed reduce financial decision‐making capabilities, you may be in denial, pretending that this decay won’t happen to you. Witness the elderly investor who entrusted 80 percent of his portfolio to Bernie Madoff in 2004, ignoring his family’s urging not to concentrate so much with one money manager. Those “striking and costly financial inconsistencies in financial behavior”1 can destroy even your most well‐thought‐out portfolio.

Besetting sins of the elderly

Compounding erratic financial behavior is the stubborn streak so often apparent as you age. “Don’t tell me” is the chorus of the aging investor, causing consternation for the family and frustration for the advisor. Many advisors resign or are fired by the aging investor because of an upset of some kind, the origin of which no one may even recall. The source of irritation might be: “They missed the bull market.” “They held too much cash.” “They made the wrong call on emerging markets.” It could also be: “They didn’t return my phone call.”

Even worse is your stubborn insistence that there is no need to change anything—I should keep my driver’s license; I should keep making all investment decisions; I don’t need 24/7 care, I’m just fine alone in my big house. Your family, and often your advisor, know better, and yet what if you shut down any discussion before it even gets started? I’ve heard too many horror stories where there is no estate plan. Or after the funeral a family discovers the will is woefully out of date. Taxes end up eating up far more than they would have with a better plan. How sad to hear a family’s frustration with the patriarch’s or matriarch’s obstinate refusal to even think about “after I’m gone.”

Before it’s too late

If you are the aging investor, it’s vital to discuss all options with your family, your advisor, a lawyer, or a trusted friend. Ask yourself these questions:

- Does my will express my true wishes, and is it up to date with new tax regulations?

- What do I want to tell the children about their inheritance, and when?

- Is it time to give up discretion of my investments? If not now, how will I (or we) know when it is the right time?

- Should I consider a durable power of attorney2?

- Is ownership of my assets set up for optimum transfer upon my death?

- Whom can I trust to look out for me when dementia or other disability strikes?

Incapacitation does not herald its arrival to your family or advisor with a clear trumpet blare. That’s why planning is so critical before you and your family are confronted with these unhappy circumstances. These questions are far more difficult to ask—and trust the answers—once no one trusts your mental state.

Who is ultimately responsible for insisting all the important questions be asked? The advisor? The family? You? It takes courage to confront you, who’ve been happily in charge for many, many years. What if everyone is in denial? Many years—or maybe just one or two—from now, you might not be in any position to participate much less have a meaningful vote on how these questions are answered. The time is now. Bring up the subject. Tackle the difficult conversation.

Bedside manner meets kitchen table dialogue

It is unfortunate that these candid conversations do not take place earlier. When exactly should you start talking about these sensitive topics? At age 50, or 60, or 70? The questions can almost feel overwhelming but each is too important to ignore.

- How should you (or your loved one) talk about your will?

- How should difficult subjects like end‐of‐life care be handled?

- How should you approach your choice between a nursing home versus staying at home? You can likely afford the more expensive 24/7 care at home, but is there a downside?

In writing financial plans for tens of millions of Baby Boomers, professionals can feel limited to archaic approaches better suited to an earlier era. You and the advisor have trusted that financial services—the financial calculations, actuarial assumptions, and an array of well‐intentioned financial products3—are the only solutions. Or perhaps you believe legal devices will save the day—trusts that lock up assets and protect your wealth from greedy ex‐spouses or spendthrift children. You may not even want to discuss:

- The legal restrictions on health‐care choices

- Decisions that must be made quickly in the midst of a health crisis

- The ability of your family to agree when they are forced to make medical decisions on your behalf

Advisors, attorneys, and health‐care professionals all may have perfectly logical approaches. That logic, however, no longer serves you or your family as well as it could.

“Imagine if you can . . .”

Your first financial plan might be done at age 30 or 40, or even at 60. Just as you have your car inspected every year, pasting that new sticker in the car windshield, you need to review your financial plan annually. Software affords a cost‐effective way to do this,4 incorporating and integrating new and complicating variables.

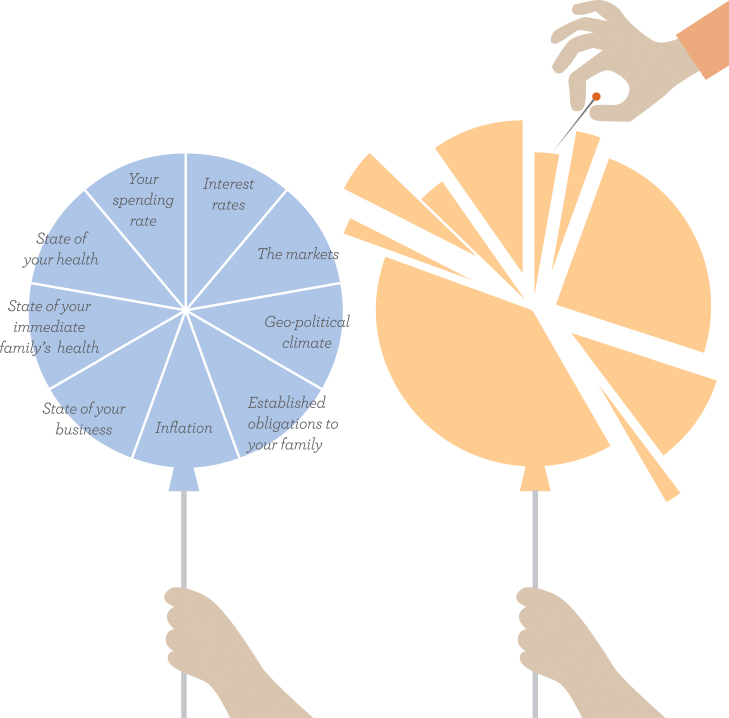

For example, typically, retirement planning with a financial plan5 calculates how much money is needed to last your lifetime, relying on economic projections, market forecasts, actuarial assumptions, and financial products in order to reach a monetary target.6 Software programs used by many firms allow you to see if you have “enough.” Countless scenarios can be run by making changes to savings rate, life expectancy, inflation, spending rate, and market returns and showing the varying results and probabilities. Every variable, though, is like quicksand; you never know where solid ground is—or when you’ll sink. Exercises showing how long your money may last7 may provide a reality check and illustrate possible future circumstances, but what if you live 20 years past your estimate?

Just as GPS has replaced paper maps, so, too, your financial plan will soon look very different. Many of these variables can be incorporated in your plan, just as a GPS processes far more than old‐fashioned paper maps.

As you age, your plan can accommodate changes in physical health as well as your emotional or mental state. Invite your family to be actively engaged, too, supporting you in the planning process every year.

Each impacted family member (e.g., a spouse or adult child who is your primary caregiver) has a voice, helping you determine needed changes each year. All these variables are carefully incorporated into the plan for next year just as a GPS shows you a different route when heavy traffic or an accident lies ahead.8 The accepted remedies9 to address shortfalls are to save more, spend less, and have more realistic expectations. These remedies need a refresh. There’s more to consider.

What exactly is a good outcome?

Obviously, this gets complicated because how on earth can you assess outcomes (that is, your plan’s success) before your death? By describing what you want, just as any CEO can and does describe the vision for the company, you can establish the best financial plan to achieve that outcome.

Siri, what’s my destination?

No one can know all the answers to the many questions a financial plan tries to answer because a plan makes assumptions—about your health, your family, your spending, the markets, inflation, and so forth.

Most importantly, outcomes need to incorporate intangible metrics like wellness, peace of mind, and happiness.10 And don’t forget—your family’s wellness, peace of mind, and happiness are important, too! These conversations are far from easy, but having them today can avoid heartbreaking dilemmas tomorrow.

Break the silence

Be prepared for your own adult children to push back, most especially if this is the first time you are initiating this conversation. They don’t want to engage in this conversation, and may even protest, “Stop being so morbid!” Why? Because the most radioactive taboo in our society remains a candid conversation about preparing for your own death. As you turn 65, 60, or even 50, however, you can be brave and begin a new conversation—about end‐of‐life care and quality of life.

The late Peter Drucker noted, “The most important part of communication is what’s left unsaid.” You, as the CEO of My Wealth, Inc., can break the silence. You can encourage the candid conversation and urge your family and all your advisors to craft creative solutions. Together you plan ahead and make the very wisest decisions, ones that work for you and those you love, too.

RIP denial and delusion

Courageously facing your own mortality is not easy! Whether you are 40, 60, or 80, you can seize the opportunity now and avoid confusion or hurt feelings later. You can leave a meaningful legacy, one that fosters family harmony, well‐informed heirs, and fond memories. Thanks to your meticulous planning and candid conversations, your advisors know you well and help you craft your estate plan. Thanks to your willingness to speak to your loved ones about a future that does not have you in it, your family feels prepared and protected, ready to carry on your legacy. As awkward as it may be to imagine a world without you in it, you gain peace of mind, and feel a confidence that you have planned and completed the journey, at least the part that you can see.