CHAPTER 2

State of the Market

TRENDS IN INTERNET USE

This chapter looks at the state of the market and current trends in Internet use. The discussion includes a description of the market, an overview of the state of e-commerce, and a look at specific trends in music sales online, including digital downloads.

Who’s Using the Internet?

According to the Pew Internet Project's research in 2007 and 2008, 75% of U.S. adults use the Internet, with a whopping 92% of young adults (ages 18 to 29) online. Sixty-nine percent said they had used the Internet within the past 24 hours. Ninety-three percent of adults with household income above $75K use the Internet, whereas only 55% of adults making less than $30K a year are online. Internet users are also more likely to be well educated. Only 47% of adults have high-speed access at home.

Ninety-three percent of teens use the Internet, and more of them than ever are using it for social interaction. Sixty-four percent of teenagers create some kind of content for the Internet, usually through social networking sites. Girls continue to dominate most elements of content creation with some 35% of all teen girls blogging, compared with 20% of online boys, and 54% of web-using girls post photos online compared with 40% of boys who use the Internet. Boys, however, are twice as likely to post videos on the Web. Older teens, especially girls, are more likely to use social networking sites. Almost half of teens who use social networking sites visit the sites either once a day (26%) or several times a day (22%).

Among adults, e-mail and search engine use are the most popular online activities, yet nearly three-fourths of Internet users have made an online purchase. Thirty-four percent have listened to music online, whereas 27% have

downloaded music files. An equal number (27%) state they have shared files from their computer with others.

TRENDS IN E-COMMERCE

Music is a dream product for e-commerce—it is one of only a handful of products that can be sold, distributed, and delivered all via the Internet. Many products are sold online as retailers shift some marketing efforts from retail stores or mail-order catalogs to online stores. Of course, this is a double-edged sword. The ease with which music can be transferred over the Internet has also led to the ongoing crisis of illegal file sharing. Online commerce is just an extension of the mail-order business that has been around since the days of the first Sears- Roebuck catalog. In the 1960s and 1970s, credit cards and toll-free numbers helped to expand the mail-order industry. In the mid-1990s, as online became a household word and Internet use skyrocketed, consumers were still somewhat reluctant to purchase products online for a number of reasons: credit card security, lack of trust in the online retailers, inability to see the product before ordering, and clunky, complex storefronts and shopping carts. In 1992, CompuServe offered its users the chance to buy products online. In 1994, Netscape introduced a browser capable of using encryption technology, called secure socket layers (commonly referred to as SSL), to transmit financial information for commercial transactions online. Then as shopping interfaces improved, more established

FIGURE 2.2 Percentage of Internet users engaged in online activities.

stores began an online presence, alternate payment methods evolved, and consumers became more comfortable with making purchases online. In 1995, two online retail giants, Amazon and eBay, were introduced.

In January 2008, Nielsen Online reported that globally, 875 million consumers had shopped online, which is more than 85% of Web users. This was up by 40% from 2006. South Korea had the highest percentage of online shoppers, with 99% of Internet users, followed by the United Kingdom, Germany, and Japan, all with 97%. In the United States, 94% of Internet users purchase products online. The top-selling online retailers for the 2007 holiday season were eBay, Amazon, Target, Wal-Mart, Best Buy, Circuit City, Sears, ToysRUs, Overstock.com, and JC Penney. Table 2.1 shows the most popular products to purchase online.

| Table 2.1 Most Popular Online Purchases—2007* | |

| Books | 41% |

| Clothing/accessories/shoes | 36% |

| Videos/DVDs/games | 24% |

| Airline tickets/reservations | 24% |

| Consumer electronics | 23% |

| Music | 19% |

* Percent of responses when consumers were asked what items they had purchased online in the past 3 months.

Source: Nielsen.

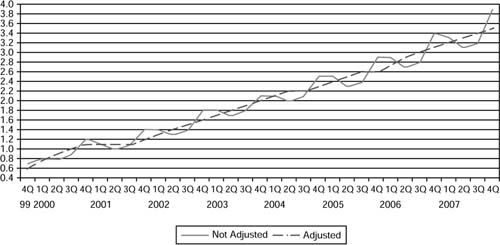

FIGURE 2.3 U.S. Census Bureau E-Commerce Retail Sales. (Source: U.S. Census Bureau.)

Sixty percent of online shoppers used a credit card for purchases in 2007, whereas 25% have used PayPal. According to Nielsen, shoppers tend to stick with shopping on sites they are familiar with, and 60% said they buy mostly from the same site.

MUSIC SALES TRENDS

In an effort to monitor recorded music sales and determine trends and patterns, the industry in general and SoundScan in particular have come up with a way to measure digital album sales and compare them with music sales in previous years. When SoundScan first started tracking digital download sales, the unit of measurement for downloads was the single track, or in cases where the customer purchased the entire album, the unit of measurement was an album. But this did not give an accurate reflection of how music sales volume had changed, because most customers who download buy songs a la carte instead of in album form. In an attempt to more accurately compare previous years with the current sales trend, SoundScan came up with a unit of measurement called track equivalent albums (TEA), which means that 10 track downloads are counted as a single album. Thus, the total of all the downloaded singles is divided by ten and the resulting figure is added to album downloads and physical album units to give a total picture of “album” sales. Here is an example of how this works from Billboard.biz.

When albums are tallied using the formula of 10 digital track downloads equaling one album, the 582 million digital track downloads last year translates into 58.2 million albums, giving overall albums a total of 646.4 million units. The overall 2006 total of 646.4 million is a drop of 1.2% from 2005’s overall album sales of 654.1 million.

Ed Christman, Billboard, January 4, 2007

Having established the TEA as a new unit of measurement, industry trends show the following: U.S. album sales have continued to slide every year from a high in 2000 of 785 million units to 646.4 million units in 2006 (including TEA). (Without the addition of the TEA, album units in 2006 were 588 million.) This represents a drop of 1.2% from the 2005 overall album sales of 654.1 million.

By the close of 2007, album sales were down 15% from the previous year and down 20% for the holiday season. With track-equivalent albums factored in, the slide was 9.5% from 2006. The one bright spot for physical units has been online sales. Meanwhile, retail stores continued to reduce the amount of shelf space they devoted to recorded music as online sales and digital downloads continued to erode at the physical unit market share. Sales of physical albums fell nearly 19%. Digital album sales reached the 50 million mark in 2007, a 53.5% increase over 2006. Digital album sales accounted for 10% of total album sales (without TEA included).

FIGURE 2.4 U.S. Album sales in millions.

FIGURE 2.5 2007 Global digital sales by channel. (Source: IFPI.)

Sales of song downloads grew at 45% over 2006, but this increase was less than the 65% increase recorded a year earlier. In the United States, more than 844 million digital tracks were sold (SoundScan) compared to 582 million in 2006. When all music formats are included (music videos, singles, albums, digital, etc.), the U.S. industry fell 14.3% in 2007.

The International Federation of the Phonographic Industry’s (IFPI) Digital Music Reports for 2007 and 2008 outline some trends in global online music sales, including the following highlights:

- More than 500 online music services were available in more than 40 countries.

- Portable player sales totaled around 120 million in 2006, an increase of 43% on the previous year. Portable player sales grew another 15% in 2007 to 140 million.

- Record companies’ digital music sales are estimated to have nearly doubled in value in 2006 and were up another 53% in 2007 to reach 1.7 billion legally downloaded tracks.

- Social networking sites exploded in popularity, and advertising-supported models such as imeem emerged as a potentially exciting revenue stream for record companies. In 2007, all four major labels worked out agreements with imeem to provide full-length streaming of much of its catalog in exchange for a percentage of ad revenue.

- Ringtone sales seemed to peak in 2007 as users began to turn to other sources and sideloading for ringtones and ringtunes. In January 2008, Nielsen reported, “There were 220 million ringtone purchases in 2007 resulting in sales of $567 million, and ringtone sales spiked 22 percent in the last week of the year. 91 percent of ringtone sales were mastertones, and the top 100 mastertones sold 65.1 million, accounting for 30 percent of ringtone sales.” In the United States, ringtone sales fell from 10% to 9% of overall mobile content. According to Jupiter Research, ringtone’s share of the overall mobile content market in Europe was down to 29% of mobile content in 2007, compared to 33% the previous year (Shannon, 2007).

Sales of music downloads have continued to grow, although that growth is slowing from the rapid pace earlier in the decade. In 2007, digital sales in the United States accounted for 30% of all music sold according to the IFPI (2008), but only 23% according to SoundScan. And in South Korea, digital sales accounted for over 60%. With sales revenue of $2.9 billion globally, the digital market grew 40% in 2007, up from $380 million in 2004. In market share, digital sales have grown from 2% of the market to 15% in the same fouryear time period.

The number of licensed tracks available for sale online increased from 1 million in 2003 to more than 6 million in 2007. Digital sales, especially album sales,

| Table 2.2 Top 5 Digital Markets, Sales by Channel, 2007 | |||

| Online | Mobile* | ||

| 1 | United States | 67% | 33% |

| 2 | Japan | 9% | 91% |

| 3 | UK | 71% | 29% |

| 4 | South Korea | 63% | 37% |

| 5 | Germany | 69% | 31% |

* Includes full tracks and ringtones.

Source: IFPI.

FIGURE 2.6 Global digital music sales 2004–2007. (Source: IFPI.)

have been stronger for catalog titles than their CD counterpart. In 2008, The Wall Street Journal commented:

[D]igital-album sales have consistently been more weighted to catalog and “deep catalog” items (generally speaking, releases more than 18 months old) than sales of physical CDs, and catalog and deep-catalog sales have shown stronger growth.

Fry (2008)

In 2004, catalog products accounted for 46% of all digital music sales compared with 35% for physical products. This was at a time when the replacement cycle for CDs was at an end. In the late 1980s and early 1990s, labels enjoyed record profits as consumers sought to replace their vinyl and cassette music collections with the improved digital CD format. As a result, catalog sales ran as high as 50% of units sold. Although the conversion from CD to MP3 or other portable format has generated some interest in catalog sales, consumers are not repurchasing music they already own on CD. Instead they are rounding out their catalog collection by cherry- picking songs they want in their library. The digital downloading format has, however, allowed major record labels to reissue recordings that previously had been deleted from the active catalog because, now, the cost of making them available is low.

Digital stores offer consumers a far greater virtual shelf space than the largest traditional brick and mortar stores. This means that a broader range of repertoire, including specialist, vintage or hard-to-find recordings is now available to fans.

IFPI Digital Music Report (2008)

The switch from CDs to digital downloading varies when separated out by genres. According to Nielsen SoundScan, digital album sales for 2007 were as follows: the genres of alternative, rock, soundtracks, and electronic showed an active downloading market, with fans of these genres more likely to select to download an album rather than buy the CD. Fans of country, R&B, rap, and Latin are more likely to buy CDs than to download albums.

FIGURE 2.7

U.S. album sales by format for CD and digital. (Source: SoundScan.)

Business Models

A la carte downloads remain the dominant business model, with iTunes leading the way. In the United States, iTunes surpassed Amazon and Target in 2007 to become the third largest music retailer, behind Wal-Mart and Best Buy. By early 2008, iTunes had moved to first place among music retailers. Lack of interoperability between services and devices has hampered the development of the digital music market.1 Labels have addressed this concern by offering digital rights management (DRM)-free downloads, first on a trial basis and then a larger rollout. Subscription-based services are not as popular (although these services grew 63% from mid-2005 to mid-2007), but they are also plagued by interoperability issues. Labels, artists, and services have been experimenting with offering free, advertiser-supported music, either for streaming or downloading.

Headway has been made on the streaming aspect of ad-supported music, with services such as MySpace, Bebo, imeem, YouTube, and LastFM striking licensing deals with the majors in exchange for a portion of the advertising revenue. In January 2008, CBS-owned LastFM announced it had licensing agreements with all major labels and 150,000 indies to provide full-track streaming music to fans. The basic service is advertiser supported and free to consumers, but consumers are limited to listening to a song three times before being prompted to sign up for the subscription version.

UPDATE: A correction. Though Qtrax claimed its service will be endorsed by the four biggest music labels—distributing music from all of them— three of the four big studios have denied signing any deal. So Qtrax’s announcement of broad music industry support—which would have been unprecedented—doesn’t seem to be true at all. Warner Music, EMI and Universal deny having licensing deals, and the fourth, Sony, isn’t commenting.

Media Money with Julia Boorstin, www.cnbc.com/id/22894228,

January 29, 2008

Less developed are the advertiser-supported music downloading systems, with startup QTrax stumbling out of the gate at the 2008 MIDEM show by announcing the service was in place only to have the major labels refute the claim that licensing had been established. Under this model, advertisers pick up the tab for the cost of the download. Consumers must watch an advertisement for the sponsor’s product in exchange for the download. Since then QTrax has struck deals with several of the majors, making up for the false start. Meanwhile, SpiralFrog has had mixed success with its advertiser-supported downloads. The company lost $6.7 million dollars in 2006 and was still in the red in 2007. As of January 2008, Universal Music Group was the only major to have a licensing deal in place with SpiralFrog.

On the SpiralFrog web site, music lovers can get free, legal and unlimited downloads. Anyone can access and download files from a library of more than one million songs and four thousand music videos. All you need to do to access this library is to fill out a simple and quick registration form. The company generates its revenues from relevant, targeted advertising.

Raju Shanbhag, www.TMCNet.com

TRENDS IN MUSIC DELIVERY AND MARKETING

The trend in the industry continues with music sales moving away from the CD and toward music downloading services. The attraction is in the a la carte or cherry picking that consumers prefer over purchasing an entire album. The fact that the CD has maintained the market share that it currently enjoys can be partially attributed to the belief that some consumers sometimes prefer to own music without digital rights management restricting how and where they can place copies of that music. The majority of CD music is not coupled with copy restriction software. The fact that more legitimate music downloads are becoming available without DRM protection may further erode CD sales in the coming years. For 2007, paid song downloads jumped to 844.2 million units in 2007, up from 581.9 million in 2006. Nine individual songs exceeded 2 million in download sales for 2007, up from just one song the previous year. Forty-one songs passed the 1 million mark compared with 22 songs the previous year.

For 2007, downloads:

- The top-selling download artist: Fergie, with 7.54 million downloads

- The most downloaded track: “Crank That” by Soulja Boy Tell ‘Em, with 2.7 million tracks

- The most downloaded album: It Won’t Be Soon Before Long by Maroon 5, with 252,000 units.

- Top-selling ringtone: “Buy U A Drank” by T-Pain, with 2.3 million units sold

In January 2008, Stuart Dredge published a list of 30 trends in digital music for 2008 in Tech Digest. Some of the more notable developments include the following:

1. Advertiser-funded music. Dredge stated that we are already comfortable with advertiser-sponsored television and radio programming, magazines, newspapers, and web sites, so it is not a great leap to extend this to music. SpiralFrog was an early entrant into the concept but has yet to make the business model successful. Dredge stated, “Nobody has found the secret formula for making ad-funded music pay off yet, but everybody is trying to.” imeem has managed to strike licensing deals with all the major labels to provide full track streams in exchange for a percentage of advertising revenue. The imeem site then offers links to purchase music on Amazon and iTunes and provides widgets to post playlists on several social networking sites.

2. Music downloads for console games. The concept here is that once a consumer has purchased a video game, he or she can update and alter the soundtrack to include fresh new music purchased and downloaded from the Internet.

3. Music search engines. This point should also include music recommendation sites. The plethora of collaborative filtering sites for finding new music should improve the outlook for online music sales and consumption and the discovery of new music in the long tail.

4. Choosing your own pricing. Other artists are looking at what Radiohead initiated in 2007 when they offered their new album for download and asked fans to pay whatever they thought the music was worth. AmieStreet has a concept where the price of a track rises with its popularity.

5. Record labels taking on iTunes. Labels are nervous about Apple’s market share of the downloading business and its unwillingness to restructure the payment model. The brainchild of UMG’s Doug Morris, TotalMusic, made its debut in 2008.

6. DRM-free music. This trend started in 2007 when EMI announced it would start offering a DRM-free version of its catalog on iTunes for $1.29 per track. The company eventually dropped the price to the same as its other tracks. Meanwhile, Amazon launched a DRM-free MP3 store in September 2007 but has been slow to set up licensing agreements with a couple of the majors to offer their catalogs. The trend continues with more stores offering tracks that are not player-specific. This trend may actually speed the demise of the CD market. Some consumers are steadfastly continuing to buy and rip CDs so they can have the freedom to load music on to several noncompatible devices.

7. Music identification goes interactive. Digital radio offers listeners track information that can lead to increased sales. One of the consistent complaints from radio listeners for the past several decades has been the inability to identify and thus purchase the music they hear on the radio. Several features have been developed to remedy the situation. In addition to digital radio with the LED readout, mobile phones now offer a music ID service, which allows you to dial in a code and hold your phone up to the music source, and the service identifies the music; soon users will have the ability to click through and purchase. Another mobile application, Cliq, lets you check out the most recent playlists of radio stations and click through to buy tracks.

8. The rise of mobile music. Asia and Europe are already ahead of the United States in terms of mobile music, but with the introduction of the iPhone in 2007 and several other multimedia third-generation phone sets, mobile music is set to take off. Nokia has already launched and is now offering a music store. Sony Ericsson has plans to open one in 2008. Sideloading makes music on mobile devices more economical as consumers opt to rip and load their previously purchased music onto an iPhone or other device rather than subscribe to a mobile music service.

9. Bands giving away their music for free. Without ties to major labels, established bands have the option of using their music—even an entire album—as a promotional tool to be given away for free. The plan is to build a larger fan base and make up the difference in the sale of concert tickets and swag.

10. The Net Neutrality policy is challenged. Internet service providers (ISP) have long held to the policy of providing access to the Internet without filtering or editing the content that users access. This has allowed illegal file sharing to thrive. But as more ISPs get into the content business, their interest in protecting their own content assets calls for greater scrutiny of abuse of copyright law.

11. Unexpected companies distributing digital music. We have already seen Wal-Mart and Amazon dive in to the digital music market. Starbucks has now teamed up with iTunes to sell music—sometimes offering exclusives (CDs or special versions of albums available only in that chain’s stores). In the future, there may be other retailers who are more interested in generating store traffic than turning a profit on digital downloads. It’s the old loss leader game in digital format.

12. Music-based widgets. Since Facebook opened its doors to third-party developers in early 2007 and MySpace followed suit, music-based widgets have been popping up everywhere. SNOCAP enabled any musician with a MySpace account to sell digital downloads on its artist page, but it has been struggling financially as of late and was subsequently purchased by imeem. Other widgets allow artists to use their fans to virally spread their music using a variety of widgets that allow them to pass along music and videos.

13. Social networking goes musical. The latest generation of social networking sites are centered around music and videos, allowing users to upload, mash up, listen to, and share music and other forms of electronic entertainment.

14. Ticket sales go mobile. What TicketMaster did for buying tickets online, the next generation of concert ticketing is doing even more conveniently by going entirely mobile, including the use of the mobile phone as the ticket to get in to the show. “Mobi-tickets” sends a bar code to a mobile phone as a picture message, which can then be scanned by a typical point-of-sale system at the concert gates. This marketing relationship with consumers’ cell phones can then be expanded by generating impulse buys on special mixes and outtakes available for a limited window of time for download to the portable communication device. It also opens the door for marketing text messages directing consumers to products. There is even discussion of tying in to a customer’s physical location so that appropriate marketing messages can be delivered that are location specific. For example, consumers shopping in a particular mall may be sent text messages notifying them of a special offering or giveaway item at one store in that mall for the next 30 minutes.

CONCLUSION

The Internet continues to siphon off recorded music sales and is accounting for a larger percentage of total retail sales in many sectors. Record labels are finding new, creative ways to sell music as the role of the CD as the primary source of revenue for recorded music diminishes. New business models are being developed that generate revenue from advertising on music-related sites, advertisersponsored music downloads, and using music as a promotional tool to sell other products such as concert tickets or portable music devices. Record labels have instituted something called a “360-degree model,” where they are responsible for and share in all revenue streams in an artist’s career. Then the music can be used as a tool to generate revenue elsewhere that is shared between the artist and the label. As these models develop and as record labels scramble to remain relevant, recorded music will start generating profits in new and unusual ways.

GLOSSARY

Digital rights management (DRM) - Copyright protection software incorporated into music files so that they cannot be shared freely with peers or copied to more than the maximum number of specific portable devices.

Exclusives - CDs or special versions of albums available only in that chain’s stores.

Internet service providers (ISP) - An ISP (Internet service provider) is a company that provides individuals and other companies access to the Internet and other related services.

Loss leader - Products are sold at below wholesale cost as an incentive to bring customers into the store so that they may purchase additional products with adequate markup to cover the losses of the sale product.

Music-based widgets - A portable chunk of code that an end user can install and execute within any separate HTML-based web page without requiring additional configuration. End users use them to install add-ons such as iLike and Snocap to social networking pages.

Sideloading - The act of loading content on to a mobile communication device through a port in the device rather than downloading through the wireless system.

Track equivalent albums (TEA) - Ten track downloads are counted as a single album. All the downloaded singles are divided by ten and the resulting figure is added to album downloads and physical album units to give a total picture of “album” sales.

REFERENCES AND FURTHER READING

Beta News Staff. NPD: iTunes now #3 music retailer. Beta News, June 22, 2007, www.betanews.com/article/NPD_iTunes_Now_3_Music_Retailer/1182537375.

Christman, Ed. (2007, January 4). Nielsen SoundScan releases year-end sales data. Billboard. http://www.billboard.biz/bbbiz/content_display/industry/e3iXZLO0IdrWu AOeIRwz3vtYA%3D%3D

Dredge, Stuart. (2008, January 4). 30 Trends in digital music: the full list. Tech Digest, http://techdigest.tv/2008/01/30_trends_in_di_6.html.

DMW Daily. (2008, January 3). U.S. album sales down 9.5%, digital sales up 45% in 2007, www.dmwmedia.com/news/2008/01/03/u.s.-album-salesdown-9.5%25,-digital-sales-45%25-2007.

E-Commerce as a revenue stream. http://newmedia.medill.northwestern.edu/courses/nmpspring01/brown/Revstream/history.htm.

Ecommerce news. (2008, January 3). Holiday online shopping up 19 percent, www.ecommercenews.org/e-commerce-news-010/0284-010308-ecommercenews.html.

Fry, Jason. (2008, January 27). Beyond the album: 2007 brings new signs that the era of a beloved musical form is ending. Wall Street Journal.

IFPI Digital Music Report: 2008. www.ifpi.org.

Pearce, James. (2003). Picture this: Tickets on your cell phone. CNetNews.com, www.news.com/2100-1026_3-5103968.html.

Pew Internet and American Life Project. www.pewinternet.org.

Shanbhag, Raju. (2008). Music download site SpiralFrog announces traffic milestones. TMCnet. www.tmcnet.com/news/2008/01/28/3233924.htm (January 28)

Shannon, Victoria. (2007, December 31). Global market for cell phone ring tones is shrinking. New York Times. http://www.nytimes.com/2007/12/31/business/31ringtone.html?ex=1199682000&en=1d8772ac7ea7a942&ei=5058&partner=IWON

1 Initially, labels sought to protect their music by including copy protection on music provided to legal downloading services so that the files could not be copied and shared with other consumers. As a result, different standards and platforms were developed that prevented the seamless transfer from one type of platform (such as Ipod) to another (Zune). This process is referred to as digital rights management.