30

CAPITALIZATION OF INTEREST COSTS

PERSPECTIVE AND ISSUES

The cost of an asset should include all of the costs necessary to get the asset set up and functioning properly for its intended use. FASB ASC 835-20 provides the GAAP requirements concerning the capitalization of interest. While the requirements for interest capitalization are generally the same for not-for-profit organizations as for commercial enterprises, not-for-profit organizations need to pay particular attention to the rules discussed in this section for capital assets acquired through gifts or grants.

The principal purposes to be accomplished by the capitalization of interest costs are:

- Achieve a more accurate original asset investment cost.

- Achieve a better matching of costs deferred to future periods with revenues of those future periods.

CONCEPTS, RULES, AND EXAMPLES

All assets that require a time period to get ready for their intended use should include a capitalized amount of interest costs. However, accomplishing this level of capitalization would usually violate a reasonable cost/benefit test because of the added accounting and administrative costs generated. In many situations, the effect of interest capitalization would be immaterial. Thus, interest costs should only be capitalized as a part of the historical cost of the following qualifying assets when such costs are considered to be material:

- Assets constructed for an entity's own use or for which deposit or progress payments are made.

- Assets produced as discrete projects that are intended for lease or sale.

- Equity method investments when the investee is using funds to acquire qualifying assets for its principal operations that have not yet begun.

Generally, inventories and land that are not undergoing preparation for intended use are not qualifying assets. When land is being developed, it is a qualifying asset. If land is developed for lots, the capitalized interest cost is added to the cost of the land. The interest is then matched against revenues when the lots are sold. If, however, the land is developed for a building, then the capitalized interest cost is added to the cost of the building. The interest is then matched against revenues as the building is depreciated.

The capitalization of interest costs does not apply to the following situations:

- When assets are acquired with grants and gifts restricted by the donor to the extent that funds are available from those grants and gifts;

- When effects are not material;

- When qualifying assets are already in use or ready for use;

- When qualifying assets are not being used and are not awaiting activities to get them ready for use;

- When qualifying assets are not included in the statement of financial position;

- When principal operations of an investee accounted for under the equity method have already begun;

- When regulated investees capitalize both the cost of debt and equity capital.

The Amount of Interest Capitalized

Interest cost includes the following:

- Interest on debt having explicit interest rates;

- Interest related to capital leases;

- Interest required to be imputed on payables.

The most appropriate rate to use as the capitalization rate is that rate which is applicable to specific new debt that resulted from the need to finance the acquired assets. If there were no specific new debt, the capitalization rate should be a weighted average of the rates of the other borrowings of the entity. This latter case reflects the fact that the previous debt of the entity was indirectly incurred to finance the identified qualifying asset and its interest should be part of the cost of the new asset. The selection of borrowings to be used in the calculation of the weighted average of rates requires judgment. The amount of interest to be capitalized is that portion which could have been avoided if the qualifying asset had not been acquired. Thus, the capitalized amount is the incremental amount of interest cost incurred by the entity to finance the acquired asset.

The base used to multiply the rate by is the average amount of accumulated net capital expenditures incurred for qualifying assets during the relevant time frame. Capitalized costs and expenditures are not the same terms. Theoretically, a capitalized cost financed by a trade payable for which no interest is recognized is not a capital expenditure to which the capitalization rate should be applied. Reasonable approximations of net capital expenditures are acceptable, however, and capitalized costs are generally used in place of capital expenditures unless there is a material difference.

If the average capitalized expenditures exceed the specific new borrowings for the time frame involved, then the excess expenditures should be multiplied by the weighted average of rates and not by the rate associated with the specific debt. This requirement more accurately reflects the interest cost incurred by the entity to acquire the fixed asset.

The interest being paid on the debt may be simple or compound. Simple interest is computed on the principal alone, whereas compound interest is computed on principal and on any interest that has not been paid. Most fixed assets will be acquired with debt having interest compounded. Compound interest can be found by using compound interest tables.

The total amount of interest actually incurred by the entity is the ceiling for the amount of interest cost capitalized. The amount capitalized cannot exceed the amount actually incurred during the period involved. On a consolidated basis, the ceiling is defined as the total of the parent's interest cost plus that of the consolidated subsidiaries. If financial statements are issued separately, the interest cost capitalized should be limited to the amount that the separate entity has incurred and that amount should include interest on intercompany borrowings. The interest incurred is a gross amount and is not netted against interest earned except in cases involving externally restricted tax-exempt borrowings.

- On January 1, 20X4, Housing the Homeless Center, a not-for-profit organization, contracted with Leo Construction Company to construct a building for $2,000,000 on land that the center had purchased years earlier.

- The center was to make five payments in 20X4 with the last payment scheduled for the date of completion, December 31, 20X4.

- The center made the following payments during 20X4:

January 1, 20X4 $ 200,000 March 31, 20X4 400,000 June 30, 20X4 610,000 September 30, 20X4 440,000 December 31, 20X4 350,000 $2,000,000 - The center had the following debt outstanding at December 31, 20X4:

a. A 12%, four-year note dated 1/1/20X4 with interest compounded quarterly. Both principal and interest due 12/31/20X7 (relates specifically to building project). $850,000 b. A 10%, ten-year note dated 12/31/20X0 with simple interest and interest payable annually on December 31. $600,000 c. A 12%, five-year note dated 12/31/20X2 with simple interest and interest payable annually on December 31. $700,000

The amount of interest to be capitalized during 20X4 is computed as follows:

| Average Accumulated Expenditures | |||

| Date | Expenditure | Capitalization period* | Average accumulated expenditures |

| 1/1/20X4 | $ 200,000 | 12/12 | $200,000 |

| 3/31/20X4 | 400,000 | 9/12 | 300,000 |

| 6/30/20X4 | 610,000 | 6/12 | 305,000 |

| 9/30/20X4 | 440,000 | 3/12 | 110,000 |

| 12/31/20X4 | 50,000 | 0/12 | -- |

| $2,000,000 | $915,000 | ||

* The number of months between the date expenditures were made and the date interest capitalization stops (December 31, 20X4).

| Potential Interest Cost to Be Capitalized | ||||

| ($850,000 | × | 1.12551)* – $850,000 | = | $106,684 |

| 65,000 | × | 0.1108** | = | 7,202 |

| $915,000 | $113,886 | |||

* The principal, $850,000, is multiplied by the factor for the future amount of $1 for four periods at 3% to determine the amount of principal and interest due in 20X4.

** Weighted-average interest rate as follows:

| Principal | Interest | |

| 10%, ten-year note | $ 00,000 | $ 60,000 |

| 12%, five-year note | 700,000 | 84,000 |

| $1,300,000 | $144,000 |

The actual interest is:

| 12%, four-year note [($850,000 × 1.12551) − $850,000] | = | $106,684 |

| 10%, ten-year note ($600,000 × 10%) | = | 60,000 |

| 12%, five-year note ($700,000 × 12%) | = | 84,000 |

| Total interest | $250,684 |

The interest cost to be capitalized is the lesser of $113,886 (avoidable interest) or $250,684 (actual interest), which is $113,886. The remaining $136,798 ($250,684 – $113,886) would be exposed.

Determining the Time Period for Interest Capitalization

Three conditions must be met before the capitalization period begins:

- Necessary activities are in progress to get the asset ready to function as intended.

- Qualifying asset expenditures have been made.

- Interest costs are being incurred.

As long as these conditions continue, interest costs can be capitalized.

Necessary activities are interpreted in a very broad manner. They start with the planning process and continue until the qualifying asset is substantially complete and ready to function. Brief, normal interruptions do not stop the capitalization of interest costs. However, if the entity intentionally suspends or delays the activities for some reason, interest costs should not be capitalized from the point of suspension or delay until substantial activities in regard to the asset resume.

If the asset is completed by parts, the capitalization of interest costs stops for each part as it becomes ready. An asset that must be entirely complete before the parts can be used capitalizes interest costs until the total asset becomes ready.

Interest costs should continue to be capitalized until the asset is ready to function as intended, even in cases where lower of cost or market rules are applicable and market is lower than cost. The required write-down should be increased accordingly.

Capitalization of Interest Costs Incurred on Tax-Exempt Borrowings

If qualifying assets have been financed with the proceeds from tax-exempt, externally restricted borrowings and if temporary investments have been purchased with those proceeds, a modification is required. The interest costs incurred from the date of borrowing must be reduced by the interest earned on the temporary investment in order to calculate the ceiling for the capitalization of interest costs. This procedure must be followed until the assets financed in this manner are ready. When the specified assets are functioning as intended, the interest cost of the tax-exempt borrowing becomes available to be capitalized by other qualifying assets of the entity. Portions of the tax-exempt borrowings that are not restricted are eligible for capitalization in the normal manner.

Assets Acquired with Gifts or Grants

Qualifying assets which are acquired with externally restricted gifts or grants are not subject to capitalization of interest. The principal reason for this treatment is the belief that there is no economic cost of financing when a gift or grant is used in the acquisition.

Land

Land that is not being prepared for its intended use is not a qualifying asset and related interest costs should not be capitalized. Once activities to prepare land for its intended use begin, however, the interest incurred during the preparation period related to buying and improving the land should be capitalized as part of the cost of the resulting asset. (FASB ASC 835-20-15)

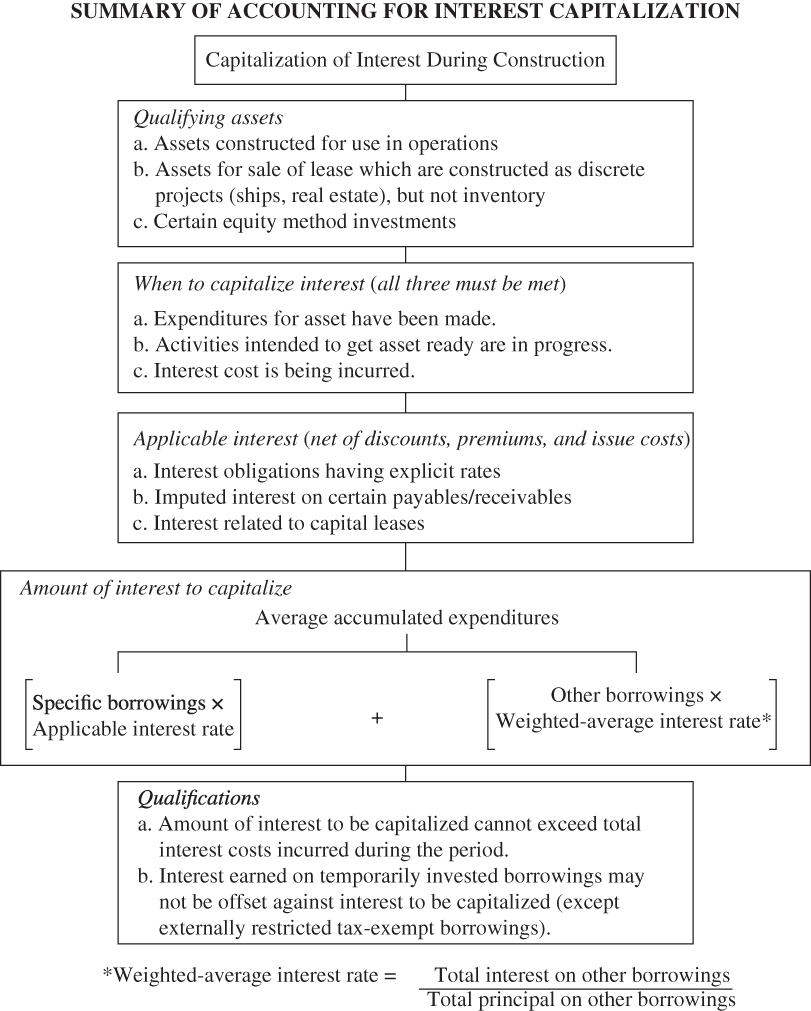

Summary of Interest Capitalization Requirements

The following diagram summarizes the accounting for “interest capitalization.”

DISCLOSURE REQUIREMENTS

The following information should be disclosed in the financial statements or related notes: (FASB ASC 835-20-50)

- The amount of interest cost incurred and charged to expense during the period;

- The total amount of interest cost capitalized during the period, if any.