3. Retail

More than any other industry, retail has developed leading-edge analytic techniques to capture the minds and wallets of customers.

Introduction

The fundamentals of the retail industry are straightforward: Buy or make goods, place them on a shelf, and sell them at a profit. There are many types of stores that sell merchandise, including department stores like Nordstrom and Saks, large chains like Walmart and Target, warehouses like Costco and Sam’s Club, and Internet sites like Amazon.

The industry is huge and 50% larger than healthcare. Retail sales in the U.S. were about $3.8 trillion in 2010, according to the U.S. Census Bureau.1 This represented about 27% of the economy in terms of GDP. It employs more than 14 million people in the U.S. alone.2 In comparison, the U.S. healthcare industry had revenues of $2.6 trillion in 2010, represented 18% of GDP, and employed almost 12 million people.3 Walmart is the world’s largest retailer. In the U.S. it had 3,868 stores and $264 billion in net sales in 2011.4 The largest U.S. healthcare player in 2011 was United Healthcare Group (an insurer), at $102 billion in revenues.5

In terms of the current economic landscape for the industry, it has recovered modestly from the lows hit during the Great Recession of 2008. However, poor holiday sales in 2012 might portend a reversal in the upward trend.6 Industry watchers characterize the future as being “hypercompetitive,” both online and in stores, necessitating the mastery of many tough challenges, not the least of which is being much more data driven.7

No other industry is so customer focused. The art and science of marketing has been fully developed in retail. But the times are changing. Customers are becoming more demanding and less loyal. And power has shifted to them. Technological innovations enable full transparency on products, pricing, peer satisfaction, and availability. Consumers can touch and feel merchandise in the store, use their mobile device to instantaneously compare alternative prices, and buy from the lowest-cost provider either online or offline.

Retailers’ approach to customers has also changed dramatically, driven primarily by the squeeze in profits caused by a number of factors to be discussed shortly. In the “old days,” shopkeepers had a one-on-one relationship with customers that offered the opportunity for deep product understanding, reliable customer experience, and the sustenance of trust. Today, most retailers have reversed this and have changed to a decidedly less personal, mass-retailing approach. Few stores, except those at the high end, are likely to emphasize personal customer relationships. But customer analytics can bridge this divide somewhat and offers the technologies to provide more high-tech personalized and tailored services with scale and efficiency while avoiding the seemingly unaffordable costs of high touch.

Retailers are at the cutting edge of using analytics for marketing. A treasure-trove of new data is available through records of purchases online and off and through shoppers’ clicks online and apps on mobile devices. Additionally, retail is at the cutting, and potentially bleeding, edge of exploiting a wide range of personal data to increase the effectiveness of marketing and sales tactics. This newfound intelligence promises a significantly higher return on marketing investments. However, there is an emerging backlash against using personal data without consent, or losing it, or selling it, which could lead to serious injury to the brand.

Industry Challenges

Industry challenges are important determinants in defining and making—or breaking—a business. For retailers, there are three superordinate challenges: the economy, the battle between bricks and clicks, and winning over customers.

It’s the Economy

The most serious exogenous factor affecting the retail industry, like every other industry, is the economy. Spending for retail goods is driven by personal income, consumer confidence, job growth, and interest rates, all of which have suffered during the Great Recession. Profits in the industry are razor thin compared to other industries, averaging between 2% and 4%. Profits were particularly low during the recession, plunging to 1.4% in 2008 and 2.4% in 2009 and returning to the relatively low prerecession level of 3% in 2010.8 Another pressure on profits related to the economy has been the increase in (overall) commodity prices which increased more than 100% during the period for many items including food, fuel, and agricultural raw materials.9 These combined economic pressures threatened the survival of retailers and many went bankrupt, including Sharper Image, Linens ’n Things, Bombay Co., and the mail-order firm Lillian Vernon. And, as with all industries under cost pressure, there has been considerable consolidation, for example, the acquisition of Sears by Kmart and the merger of May Department Stores with Federated Stores.

The Battle Among and Between Bricks and Clicks

Superstores are battling with each other on every major block of commerce. Pricing is very competitive. The in-store experience has to be compelling. And to add more pressure to the mix, online retailers are gaining ground with substantial year-over-year growth in sales.

Brick-and-mortar stores are very expensive to operate relative to online sites. So the lure of brick-and-mortar has to be more than a simple place to view and buy merchandise. It needs to be unique, even a destination experience:

• Malls like the Mall of America are so large and have so much entertainment wrapped around the stores that one needs a travel agent to navigate them.

• Some stores are more like wired living rooms that happen to sell coffee, like Starbucks.

• Others are hip and trendy and cater to younger segments, like H&M and Urban Outfitters.

• Still others are like four-star hotels, beautifully decorated and with piano music in the foyer, like Saks and Nordstrom.

However, for an increasingly large segment that goes to warehouse stores, including the unvarnished concrete floors, fluorescent lighting, and industrial shelving, price reigns supreme and people are willing to forgo pleasant surroundings and accept nary a customer service person in site.

The clicks are gaining on the bricks. It is projected that online sales will amount to about $250 billion by 2015, or about 8% of all retail sales.10 The projected compound annual growth rate for online sales is 10%. A majority of online shoppers think the best deals are available online.11 As shoppers get more comfortable with paying online, online delivery times improve, and the types of purchases expand from relatively small-ticket items to a broader mix, the growth potential might get much larger.

Offline stores are not going away. Major retailers sell the vast majority of merchandise in-store rather than on their own Web sites. And different customer segments have different preferences in relation to bricks and clicks. But the overarching trend toward impersonal selling, with price being the utmost buying factor, makes it harder for the old bricks formula to work, which included good customer experience and brand loyalty. As stated earlier, analytics might be an answer to approaching a market of one through radical personalization based on innovative uses of big data.

Winning Over Customers

Marketing is all about customers—acquiring, retaining, growing, and optimizing them. And treating customers well is good for the bottom line. A recent multi-industry survey found that 64% of consumers switched from at least one service provider in the past 12 months—for example, a bank, utility, wireless carrier—due to poor customer service.12 They conclude, “As consumerism trends continue, we expect customer service performance to emerge as a source of differentiation and contributing factor to loyalty and retention.” But as traditional customer “amenities” wane, there is a paradox on what constitutes a good and profitable customer experience.

People definitely have a preference about the relationships they want to have with companies, and many are loyal and active advocates on a company’s behalf as a result of good customer experience. We all know companies we enjoy interacting with and others that are a pain to deal with and are best avoided.

Customer experience can be measured. Forrester Research rates customer experiences across 14 industries, including airlines, banks, credit card providers, health plans, hotels, insurance firms, Internet service providers, investment firms, parcel shipping services, PC manufacturers, retailers, TV service providers, utilities, and wireless carriers. It defines customer experience in terms of (1) meeting needs, (2) being easy to work with, and (3) enjoyability. It produces a ratings and rankings by industry and across the 133 companies in the survey.13

The industry with the highest average score is retail, with a score of 82 out of 100. Following closely behind is the hotel industry at 80, and parcel delivery/shipping firms at 78. Retailers take 12 of the top 20 rankings. The highest-rated retailers on the top-ten list were a mix of store types and included Barnes and Noble (#1), Amazon (#4), Kohl’s (#6), JCPenney (#7), Macy’s (#7), BJ’s Wholesale Club (#7), and Costco (#7).* Note that all of these retailers, with the exception of Amazon, have online and offline outlets. However, Amazon had $48 billion in online sales, which was more than six times the online sales of all these other stores combined.14 And offline sales were 30 times greater than online sales for these non-Amazon stores.15

* Other categories of the retail industry not included in these sales figures are gasoline, food service, and automobiles. Note that the survey includes a small number of retailers and appears to include the largest ones. The destination retailers mentioned earlier were not in the sample.

In comparison, health plans/systems are dead last among all industries, with an average score of 51. This score is even lower than those of credit card providers and Internet service providers. Kaiser Permanente is the highest-rated health plan/system of those sampled, with a ranking of 75 out of the 133 companies rated. Medicare is 102, and Anthem, Medicaid, and United Healthcare are close to the bottom of the list at 129, 130, and 131, respectively. In between the top-ten-rated customer experience companies and the highest-rated healthcare company (Kaiser), there are many brands representing many industries, including SunTrust Bank (14), Federal Express (27), Southwest Airlines (28), Charles Schwab (40), MasterCard (57), and Cablevision (71).

The curious thing is that the essence of a healthcare company is to make people feel and function better; thus, it would seem it would have a greater opportunity to satisfy customers (if they did their job well) than a credit card company, a bank, or an investment firm, which handles monetary transactions. Presuming that the data are reasonably valid, it would appear that something has gone awry with customers in healthcare, especially with health plans. (Note that other types of insurers, for example, for cars and casualty, score much higher than health insurers, at 71% on average.) Given the low performance for the healthcare industry, the opportunity for improvement is huge. For example, if the average health insurance plan performed like the average retailer, there would be a 61% improvement.

Industry Strengths

Industries develop unique responses to challenges and market demands, which result in strengths that can be optimized for business success. For retailers, there are three areas of industry strengths including optimizing customer value, customer analytics, and mobile devices and social media.

Optimizing Customer Value

The business success of retailers depends on optimizing the customer’s perception of value. There are six traditional dimensions of the value equation, including store factors, service factors, merchandise, price, supply chain, and technology:16

1. Store factors have to do with the look and feel and overall pleasantness of the store experience. Some stores emphasize beautifully decorated atmospherics like Crate and Barrel. Some emphasize sparsely appointed and industrialized surroundings to highlight efficiency and low costs.

2. Service factors are primarily about how the customer is helped in shopping, purchasing, and returning merchandise. Some stores are surprisingly stingy with customer service. Others place a lot of emphasis on servicing the customer, including Trader Joe’s, the Container Store, and Lowe’s.

3. Merchandise is the raison d’être for retailers and is why customers come to the store or the Web site. The store needs to carry what the customer wants and do it in a reliable way; for example, having the item on the shelf when the customer comes calling.

4. Price is a critical factor, especially when the store is selling (most) items that are also available from competitors. Pricing is dynamic and can change by the minute on Internet sites depending on supply, demand, and competitor pricing, or it can be dependably stable and low as with some warehouse stores.

5. Supply chain involves the efficient and effective integration of suppliers, manufacturers, warehouse, stores, Internet sites, and transportation such that merchandise is produced and distributed in the right volumes, for the right locations, and at the right times.

6. Technology is an important differentiator for retailers as it is for most industries. In the next two sections we highlight the importance of customer analytics and mobile devices and associated applications as particularly important technology solutions. Other important technology approaches are used in supply-side management. For example, CPFR (Collaborative Planning, Forecasting, and Replenishment) systems use sales data to inform the need for product replenishment. RFID (radio frequency identification) is the use of chips placed on merchandise to track its location through the supply chain. And CRM (customer relationship management) systems collect lots of data from customers, including purchases and customer service encounters, with the goal of building good relationships and loyalty with high-value customers.

Customer Analytics

“Winning retailers will have a better understanding of their customers than their competition.”

—“Retailing 2020: Winning in a Polarized World,” PricewaterhouseCoopers/Kantar Retail, 2012

Knowing the customer is a function of marketing and the retail industry does it the best. It uses marketing analytics extensively to this end. Marketing is all about understanding, predicting, and influencing customer behaviors in relation to buying and loyalty. It does this through four stages:

1. Acquiring new customers through marketing campaigns that target specific subpopulations of consumers (segments) with tailored messages and preferred media.

2. Keeping the customers you have through ongoing personalized communications and better-informed customer service.

3. Growing revenues through cross-selling associated existing products and developing new ones.

4. Optimizing return on investment (ROI) of marketing campaigns by concentrating on customers with the highest customer lifetime value.

The conversion rate, that is, the percentage of people who shop for a particular item and then buy it, is an important performance metric of retail marketers. These rates can range from a low of 0.2% to a possible high of 38% depending on the method.17 The marketing methods and associated conversion rates* are listed here:

• Information cost reduction: 0.2%–2.9%

Target addressable mail to reduce postal costs and lower cost of communications.

• Fact-based marketing: 1.9%–4.8%

Identify loyal customers, target specific customer segments, use analytics in campaign management.

• Information sharing: 6.2%–18.7%

Integrate multichannel buying data; for example, browse in one channel, purchase in other, and pick up in another.

• Information responsiveness: 16.9%–38.2%

Analyze “raw” data from streams of customers’ social media commentary to address changing moods and factoring these into point-of-sale rules.

* These percentages are cumulative; e.g., fact-based marketing includes the gains achieved in the prior method.

Clearly, the more technically driven approaches are producing the highest conversion rates.

Are these conversion rates good? Certainly, it must be disappointing to achieve only a 5% success rate with fact-based marketing and to just double that with multichannel marketing. When comparing to another industry like healthcare, by one standard, it is pretty low and by another it is pretty high. If a patient has a problem (a need-to-buy in retail) and visits a doctor (the store), and is offered a treatment (a product or service), most patients will buy it on the spot (although an uncomfortably high percentage do not follow through with the treatment). On the other hand, health plans that attempt to change behaviors of its members, for example, to ask them to change from a brand-name drug to a generic or to fill out a health-risk-assessment survey, do worse than retailers.

The retail industry thinks that technology advances will bump up these rates. For example, a recent survey of retail chief marketing officers (CMOs) indicated that more than 80% say they expect to increase their use of four technologies in the next three to five years, including customer analytics, customer relationship marketing, social media, and mobile applications.18

Big data brings big promises and challenges to retail. More and more data are needed to understand customers better and better...and to do it faster than the competition. The hallmark of customer analytics in retail as compared to other industries is the availability of purchasing and loyalty data both online and offline. Additionally, retail is more adventurous in using personal data on customers than other industries. And huge volumes of data are available from customers’ clicks as they browse through the Internet that are tracked by scores of firms that put cookies on consumers’ computers.

One of the challenges is that retailers are struggling to figure out what all the new data means. The best is truly yet to come as analytics unveils the secrets of consumer behavior and uses predictive modeling and other techniques to improve customer relationships and buying behaviors. The trick will be to understand shoppers’ passions and interests along with purchasing data and to use these data in real time to make the “next best offer.” (Examples of these are in the next section.)

However, as retailers blaze into new frontiers in the use of big data, there are risks. For example, in addition to using purchasing and loyalty data, the industry buys publicly available data through data brokers on parameters such as the value of a house, religious preference, and more to improve its predictions. And it scrolls and scrapes personal data using cookies and software in mobile phone apps and the Internet. And it does this without the knowledge or consent of the customers it is tracking.

It also pushes the envelope in matching personal data with real-time interventions. For example, some retailers use cameras in digital advertisement displays and change the message based on photographable personal characteristics. If a passerby appears to be young and female, certain apparel promotions might appear on the display. Other retailers use cameras for face recognition, integrate these data with customer profiles, and then produce real-time messaging to store salespeople on approach and messaging to the client; for example, “Hello, Mr. Smith, are you interested in the latest sport coats from Ralph Lauren to wear on your next cruise?”

Many feel that the use of personal data without consent is getting “creepy” and leading to a bevy of privacy concerns. In fact, federal legislators are concerned with buyer classification scoring, which might redline certain buyers because they do not provide optimal lifetime values. This is analogous to credit ratings but is not regulated at all, unlike the credit industry.

Because it stores so much personal information, including credit card information, the retail industry is also prone to security breaches that can include hackers stealing credit card numbers and other sensitive information that can lead to identity theft and credit card fraud. These activities can tarnish the brand. But the real challenge ahead might be consumers’ rebuff of the use of personal data, obtained through cookies and other covert tactics, for marketing. This might stop mass customization in its tracks and turn back the rising tide for online sales. More likely, retailers will evolve new approaches, including creating data-free zones, third-party reputation protectors, and new data-sharing relationships between seller and buyer that are transparent and provide mutual value.

Mobile Devices and Social Media

More and more consumers are perpetually connected to smartphones, tablets, and other mobile devices to search for products, find coupons, find the best deals, and make a purchase. For example, there are price-comparison mobile phone apps that enable shoppers to scan the bar code of products in-store and get a real-time comparison of prices from competing retailers.

Additionally, customers expect to communicate with retailers through “omni-channels” and use their preferred device at any given time, on a 24/7 basis. They expect that all the channels will talk with one another and provide consistent and reliable information about the store.

Smartphones have become a key tool for shopping. A recent survey by Deloitte indicates that 67% of smartphone users between 14 and 34 years of age have used their device to shop, and 55% said that smartphones influenced their decision to make a purchase. The survey also addresses the “influence” of smartphones on store sales in relation to product research and price comparison, which is different from using smartphones to actually complete the sales transaction. The study concludes that almost 20% of total store sales, or $689 billion, will be influenced by smartphones by 2016.19

Social media is just emerging as a tool for conducting e-commerce. According to Booz Allen Hamilton in a 2010 report, the market is embryonic with sales of $5 billion. It projects sixfold growth over five years and estimates that $30 billion will be spent by 2015. It will complement other channels, including stores and the Web. Social e-commerce includes platforms that sell merchandise like Groupon and Gilt; social apps that facilitate group buying, group-gifting, and social shopping; and additional functionality for present sites like Facebook and Twitter to enable e-commerce.

In addition to the opportunity for commerce, social media serves other functions for retailers. This includes driving awareness and “buzz” and generating leads. It also facilitates the improvement on conversion rates. And its unique type of communication in the social nexus improves loyalty and can foster advocacy of its product and brand.20 An example is included in the following section.

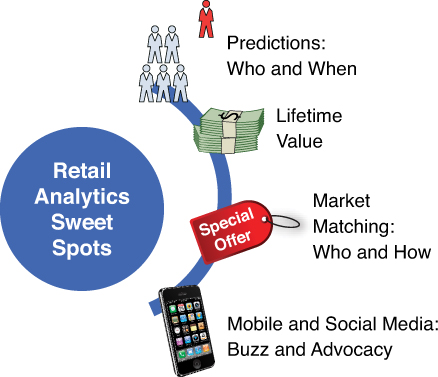

Analytics Sweet Spots

Relative to the key business drivers just described, this section turns to selected analytic sweet spots that support business solutions that are unique to retail and offer promise for healthcare (see Figure 3.1). It boils down to four areas: (1) predictions: who and when, (2) lifetime value, (3) market matching: who and how, and (4) mobile and social media: buzz and advocacy.

Predictions: Who and When

“Just wait. We’ll be sending you coupons for things you want before you even know you want them.”

—Andrew Pole in “How Companies Learn Your Secrets,” New York Times, February 16, 2012

The retailer Target uses predictive analytics to increase sales to pregnant woman.21 Why pregnant women? They buy a lot of merchandise for the new baby and the new family lifestyle. Further, this particular life event presents a window of opportunity to influence buying habits. Most buying habits are fixed, relatively autonomic, and not amenable to new decisions rules. But “moments that matter” are the windows of opportunity that marketers home in on.

Target’s prediction challenge was to identify the women through a “pregnancy prediction score” and to estimate the delivery date. The delivery date is critical because they determined that buying habits change during the course of the pregnancy; that is, different items are bought at different times. They did this by looking at what women on the store’s baby registry were buying. It turned out that these women bought larger quantities of unscented lotion during the second trimester; supplements around 20 weeks; and soap, extra big bags of cotton balls, and washcloths when the delivery date was getting close. From these findings, they developed a model that provides a pregnancy prediction score and estimated delivery date based on purchasing data. Tens of thousands of women were identified.

The next challenge was to trigger new buying behavior by presenting coupons to the targeted women, for the right products, at the right time, via the right channel, and with the right message. Target will “be sending you coupons for things you want before you even know you want them.” This was accomplished through the collection and integration of a wide array of data. Andrew Pole, a (former) statistician at Target, said, “If you use a credit card or a coupon, or fill out a survey, or mail in a refund, or call the customer help line, or open an e-mail we’ve sent you or visit our Web site, we’ll record it and link it to your Guest ID...and we can buy data about you...[such as] charitable giving and cars you own.” All these sources provide data on a customer’s age, marital status and how many kids, neighborhood lived in, estimated salary, credit cards carried, Web sites visited, and more.

The results of the campaign showed that Target’s Mom and Baby sales exploded. Overall revenue following this campaign increased dramatically. The campaign was presumed to be a great success.

So if this approach works for revenue enhancement for pregnant women, what about other marketing segments and “moments that matter,” such as month three after a wedding engagement when the gift registry list is developed, or month two after the death of a parent when the inheritance is assimilated and thoughts about a vacation or investments are under consideration? These habit-changing moments are determinable, and sophisticated analytics can home in on the target segment with a high degree of accuracy.

However, there are risks to data mining of personal purchasing data. A father complained that his teenage daughter was receiving coupons for pregnancy products and thought it was inappropriate given that she was not pregnant. Turned out she was pregnant and the father apologized. But this is indicative of a widely held, uncomfortable concern about the covert gathering and analysis of personal data for the purpose of persuading/manipulating purchasing habits. On the other hand, some people appreciate it when trusted sellers make recommendations to them based on purchasing history; for example, Netflix and Amazon. It might even be a good trade-off relative to receiving reams of irrelevant advertisements for some consumers.

What are the implications for healthcare? First, of course, the healthcare and retail industries are very different in many respects. The retail industry sells merchandise used in everyday living, such as soap, clothing, and flat-screen TVs. Much of the merchandise sold includes such necessities as food and gas. Some merchandise brings happiness to buyers because it improves some aspect of their lives, such as a computer or a smartphone or jewelry. Retail items are also of relatively low cost. When it comes to healthcare, however, purchases can be very complex, involving high-tech treatments and extensive, ongoing contact with providers. And the treatments can be very expensive, requiring insurance to protect individuals from bankruptcy in the case of an accident or a terrible illness.

The industries are also very different in terms of commerce. People buy things in healthcare with “other people’s money” because of insurance and are relatively oblivious to actual costs. Similarly, people tend to rely on others to make the buying decisions for them in healthcare, whether it is the choice of insurance plan made by an employer or the treatment prescribed by a physician.

The ways things are sold are also very different between the industries. Retailers have a different value proposition than healthcare, as discussed earlier. They sell through stores and the Internet and compete on price, quality, and innovation. Healthcare is sold largely in doctors’ offices and in the hospitals they affiliate with. Transparency on price and quality in healthcare is far less complete than in retail.

The incentives given to consumers are also quite different. Retailers use discounting through coupons and rebates and other forms of price reductions, for example, the “blue-plate special.” In healthcare, a monetary incentive is seldom given by the seller (physician) to the patient to get better. In fact, going to the doctor for a serious condition usually costs a lot out-of-pocket, the outcomes are not always known, and the experience is not often pleasant. And the only incentive from the doctor is to follow his expert advice to “do it or die.” This should be sufficient, one would think, but then again the rate of medication compliance, that is, taking the medications as prescribed by a physician, is only about 50%.22 Clearly, this “conversion rate” for patients to hear and act on the message to change behavior and improve one’s own health is abysmal in healthcare and needs to change dramatically to achieve better treatment outcomes.

How customers are engaged is also different. For example, the clinical encounter is a very personal, one-on-one relationship and transaction. However, many patients might feel that their interactions with the healthcare system are very mechanical and depersonalized. As discussed earlier, most retailers have all but given up on the value of close personal relationships and have gone in the other direction, toward lower costs and mass customization.

So the real question is how might mass customization and the associated use of customer analytics, so refined in retail, benefit healthcare? Perhaps the answer lies in understanding the “patient” customer in different ways through the use of multiple streams of data, as used in retail. It might also lie in the relatively under-developed approach to improving population health rather than individual health.

In terms of predictive modeling, clinical decision making is quite advanced. It is certainly possible to predict the health outcomes of individual patients, based on their age, results from screening tests, clinical histories, genetic profiles, and so on. Indeed, that is the purpose of diagnostics. And making predictions on which treatments are the best fit and the estimated life years remaining (prognostics) are also core skills of care providers. The patient’s data is applied to well-researched models of disease and the most likely fit is determined.

There are ways to improve the clinical encounter with retail-induced customer analytics, and examples are provided throughout the book. But the real lessons come into play with managing the health of populations. Although healthcare can be very good at treating illness, it is relatively weak in preventing illness in the first place and in partnering with patients to help them take the actions they need to engage in to improve care. The clinical data used in medical predictions is not sufficient to this purpose. Retail offers a look into the use of data outside the usual sandbox of an industry.

One example is the use of nonconventional, personal data to predict which people are obese and are at risk for serious health conditions, including diabetes and heart disease. The best indicator of obesity is the body mass index (BMI). It is very simple to calculate from data on height and weight. Yet, surprisingly, these data are not collected and stored by health plans. They might be available in electronic health records (EHRs) but these would include data only on patients who are presently sick. And the EHRs are usually not accessible by health plans. So how does a health plan get these important data on the vast majority of their members who do not seek healthcare, but might be at risk, and subsequently accrue more treatment and costs, if not identified early on in the progression of the disease?

Health plans might try to mine their claims data and come up with predictive algorithms that indicate the probability of obesity. But, again, the diagnostic codes on claims forms are for services provided for treated diseases, and most forms of obesity, with the exception of morbid obesity, are not diseases. It might be possible to look at the longitudinal records of patients who end up with diabetes and determine whether there are precursors that are reliable and valid indicators of diabetes and thereby develop a predictive model. (This is similar to what Target did in calculating the pregnancy prediction score.)

Somebody from outside the health insurance claims world might ask innocently and incredulously, “Why not just ask your members directly?” It’s important information, they should care about their health, they will certainly provide it. That’s what health-risk-assessment (HRA) surveys are about. Many companies provide incentives for employees to provide this information to a third party that can use it to motivate the individual to lose weight, stop smoking, drink less, and wear seat belts. Companies might pay $100 or so for employees to do this. But many employees might not want their employer even remotely knowing about their health risks, and therefore the only ones who might reliably fill it out are the healthy and young employees. In any event, the response rates to HRAs are low. But the response rate to surveys is better in other industries. Indeed, healthcare can learn from politics and its use of polling. Its customers get engaged because they think the cause is meaningful. In Chapter 4, “Politics (Presidential Election Campaigns),” we present some ideas about how to make the cause meaningful in healthcare.

Another approach is to take the blindfolds off and try a whole new way instead. Other industries buy reams of personal data and use it for commercial purposes to sell more products and services. In healthcare, the data can also be put to good use. In the case of height and weight, the information is obtainable from data purveyors along with a treasure trove of other data at relatively low cost (for example, $20 per 1,000 member matches). Almost all of these data are in the public domain and some come from more covert sources such as Internet clicks. This is much cheaper than $100 incentives for HRAs and more inclusive in terms of the response rate. The computational task is very simple—just two variables. The additional information obtained from the new personal file would also facilitate the building of many predictive models.

So why not try this whole new way to attack obesity and diabetes risk? We will discuss adaptation challenges in the last chapter. These include important considerations of privacy; for example, HIPPA rules, and organizational readiness. But what is clear is that the data and analytics are ready for prime time, at least to identify individuals. Getting the job done has more to do with the sociology than the technology.

What happens subsequently in the chain of events that has to take place to affect behavior change, in this case to lose weight? Identification in and of itself is quite useless. What is the model on the “moments that matter” to effect a habit change? Is sending out educational literature the answer? Would people respond to a health plan’s coupon to join a health club, or would receiving an app to monitor food intake make a difference? Should health plans provide a Fitbit23 monitor to track movement? Is the medical system the right system to lead the charge on the obesity initiative? Are the factors related to obesity more social than medical? Is the role of analytics mostly in the identification of microsegments? It’s the sociology of program change that matters most. Later in this chapter, we provide an example about how identification data (segmentation) is combined with a program intervention to effect an important health outcome.

One could envision all types of predictive algorithms for many other population segments that would be relevant for population health management. What are the questions that were never asked because either the absence of data expunged the very thought or the customary mental models of an industry narrowed the scope of possibilities? For example, in the banking chapter, we think about a banking adaptation for healthcare that uses easily available personal data to make predictions about the challenges and capabilities of people to respond and carry through with treatment. Not in the biological sense, but in the social sense. We all have a FICO score, which is absolutely critical in getting a loan. The score is important to the lender because it indicates the person’s capability to carry through with a promise made to repay a loan. In healthcare, it’s not so much what the doctor does, it’s what we do as people to adopt healthy behaviors. And sometimes all our wishes to behave in a healthy way are subverted because of other social factors that create barriers to do the right thing. But there is no measurement of a patient’s willingness, capability, and social constraints to improve one’s own health. And the measurements are easy...if one uses the right data, as is done in banking.

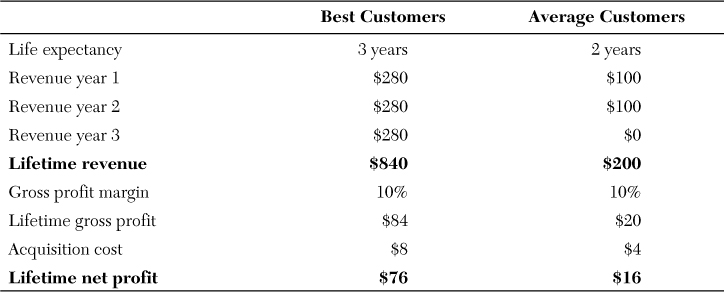

Lifetime Value to Concentrate Marketing Spend

Customer lifetime value (CLV) is a measure of the revenues/profits attributable to a given customer over her career with a company. It represents how much each customer is worth in monetary terms and how much a marketing department should spend to acquire and keep her based on the return on investment. In Table 3.1, the lifetime revenue and profit for hypothetical average customers versus the best customers is calculated.

The bottom line is that the CLV for the best customers is almost five times greater than that for the average customer. Marketing, concerned about its ROI for its investments, would quite logically focus its investments on the best customers. For example, one retail customer analytics firm says, “We’ll let you know how much a Groupon customer is worth and how customer value varies across ad networks and channels. And we let you know early, so you can take actions on the results.”24

What are the implications for healthcare? CLV can be approached quite differently depending on a few parameters: actors (providers or payers); payment system (fee for service or global payments); value metric (dollars or clinical outcomes). For providers in the fee-for-service system, the prediction of medical utilization and revenues is relatively easy. The 80/20 rule applies; that is, 80% of utilization is attributable to 20% of patients. A quick calculation might suggest that retirees with multiple chronic diseases would produce the highest revenues under the fee-for-service system. However, Medicare reimbursement rates are lower than those of commercial insurance for the same services, and more volume might not produce better net profit. Similarly, certain procedures produce better profits because of payment formulas. For example, cardiac surgeries produce a high profit, especially when performed in “focused factories.” And, of course, certain medical specialties produce better lifetime revenues than others.

But providing more services does not necessarily produce better health and there is growing concern about overtreatment. And as global payment approaches achieve more coverage and as transparency and risk adjustment methods level the playing field, lifetime value based on profitable volume will become less useful.

For payers, profits increase when the utilization/cost experience of members, factored into premiums, is less than predicted. Utilization can be moderated by good medical care, a focus on prevention and medication compliance, and disease management of chronic conditions. It can also be hedged by increasing the pool of healthy individuals to begin with.

The payer business model will change dramatically over the next few years as payers go retail through health insurance exchanges, perhaps doing most of their business directly with consumers rather than employers. Additionally, insurers will have to take all comers with no exclusions for preexisting conditions. Community rating, rather than experience rating, will be the norm.

This presents a marketing conundrum for health plans. Using CLV precepts from retail, insurers should identify the best, most profitable members. This segment is the young, healthy, and wise. After targeted marketing to enroll this group, the next strategy would be to keep them healthy through wellness programs and keep them loyal through good customer experiences.

Insurers can also disenfranchise the sick/costly members. Customer relationship marketing systems can provide information to deliver poor customer service and frustrate them in other ways, such as not paying on time, excessive Explanation of Benefits (EOB) notices, and harsh communication tactics. One marketing firm refers to disenfranchising strategies as “rooting out unproductive relationships.”25

Skimming, or selecting the healthy, is easier, less expensive, more assured, and more immediate than medical management. Lifetimes are uncertain in healthcare. Some plans and providers believe that improving health outcomes through prevention and disease management efforts might not pay off for them although it might reduce costs for Medicare. Employers change insurance plans often. Also, there is low member loyalty to health plans, employees change/lose jobs, patients have low compliance rates with disease management, successful implementation can be difficult with independent doctors, and it takes a long time and costs a lot. Although skimming is the wise thing to do for quarterly earnings, it misses the mark on the primary obligation of healthcare: to save lives and improve health.

What if lifetime value were actually about the length of a life? What if health plans/systems were rewarded for producing longer and more functional lives? And what if there were financial incentives for this lifetime value rather than the production of more services? So the concept of lifetime value all turns on the value orientation. Using analytical methods for tracking people longitudinally over a lifetime would put the focus on long-term improvements in healthcare. Also, CLV analytics can be used to improve health for everyone, to lift all boats, and by doing so can add value to the bottom line and fortify the brand through its integrity and dedication of purpose to the health and well-being of all customers.

Market Matching: Who and How

Segmentation is about isolating distinct clusters of homogenous customers that can be characterized by certain buying patterns, for example, “brand loyalists,” “social media-ites,” and “bargain with me.”

These clusters can be activated when trigger events occur, including moments that matter, inbound call content, changes in insurance coverage, spikes in medical costs, social media sentiment, and insights from advanced predictive analytics.

Marketing messages are crafted to fit the cluster’s habit/buying receptor site in terms of language, argument, and specific offering; for example, coupons. The messages are delivered through the preferred channel, such as mobile device, outbound call, customer portal, e-mail, or face to face.

The major dependent variable (outcome) in the equation is CLV or specific revenue from targeted campaigns. The major independent variables are the cluster, channel, trigger, message type, and intervention. The precision of the equation can be improved by gathering more and more data on the individual to drive more segment differentiation.

How does this model apply to healthcare? First, the dependent variable needs to be specified. The model can be applied to attract new customers to sign up for a health plan or provider system (acquisition), to keep them in the fold as a loyal and satisfied customer (retention), to grow revenues through up-sell (more expensive health benefit plan, more medical services if FFS), or to cross-sell (from medical to disability insurance).

But the real benefit might come from changing customer behavior to improve health and functioning, especially in global payment settings. The goal is to encourage and reinforce customers as co-producers of health. The clusters become very different from retail because they need to predict health improvements. And the data needed to define them is very different than that in retail.

CVS/Caremark has multiple stakes in healthcare. It is a retailer of prescription medication and health products through its chain of CVS drug stores, a healthcare provider through its MinuteClinics, and a pharmacy managed care program through its Caremark pharmacy benefit program (PBM). It promotes a better healthcare system through its emphasis on medication adherence, which leads to improved health outcomes and lower costs. It improves its bottom line through a paradox of increased retail sales and decreased prescription costs to employers through its PBM.

Its Consumer Engagement Engine pools data from all customer touch points, including retail and specialty pharmacies, mail order, MinuteClinics, Web sites, the telephone pharmacy service, and the ExtraCare loyalty program. It develops a full picture of a person’s prescription drug purchase and usage behavior, as well as related personal and healthcare information including demographics, medication history, prescribing physicians, drug usage, and so on. It identifies customers with suboptimal pharmacy care—for example, not taking medication—and those at risk for it. It then uses its Pharmacy Advisor program to change behavior regarding compliance by communicating with patients at the right time and with the right message. The right time is usually when patients need to renew medications and they come to a retail store or fulfill through mail order. The pharmacist has the information available at the point of service to counsel the patient on the importance of the medication and to answer any questions the patient might have.26

The results of the program, for patients with diabetes, show modest improvements in medication compliance of 2.1%. The rate was better with face-to-face contact with pharmacists through store consultations than with phone calls made by pharmacists through mail order.27 They estimate that the total cost recovery from perfect medication compliance for all medical conditions in the U.S. would be $300 billion. So if their improvement percent were brought to scale, there would be savings of about $6 billion.

This example demonstrates a sophisticated use of analytics to collect and integrate customer data from all corners of the enterprise and apply the analytics for segmentation, multichannel matching, messaging, and interventions. It focuses on the laudable goals of saving lives and dollars through pharmacist interventions.

There are some limitations. The “over the counter” brief dialogue with a pharmacist, who is multitasking in doing her day job of filling prescriptions and other new jobs such as giving flu shots, might not be concentrated enough. And customer communications from PBMs have often been focused on switching to a cheaper drug and appearing to benefit the company’s bottom line rather than the customer’s health needs.

Also, pharmacists do not know the patient’s medical history and might not have the knowledge or context to answer important medical questions. The pharmacist cannot substitute for the medical team. In fact, a big part of the problem with medication compliance is the high prevalence of side effects or no effects, and the difficulties in achieving a satisfactory level of communications with the medical team to address issues in a timely way before the patient becomes uncomfortable and stops taking the medication.28 Of course, fragmentation of healthcare delivery systems and the high cost of some medications also inhibit compliance.

The obvious point is that if CVS can do this from its important, but limited, pharmacy perspective, why can’t medical teams do it from an overall medical management perspective?

What if patients/members/customers were known more fully through more complete data than claims, enrollment, and medical records, and new clinical segments were defined beyond diagnosis, stage of disease, and other medical classifications to include propensity to engage, self-monitor, partner on shared decision making, and change behavior patterns? What if there were a radical change in the dependent variable to include patient/customer control and how to support it? What if this information on mass, radical customization to a person-of-one facilitated a change in the discourse to improve coordination of care and mining of EHRs, and to foster a true transformation in the role of the customer/patient?

Mobile and Social Media: Creating Buzz and Advocacy

Customers have a lot more information about attitudes, preferences, and suggestions in their heads than is evident from their data streams.

Mobile devices are the new nexus of communications among individuals and with businesses for commerce. As mentioned earlier, customers expect 24/7 omni-channel reliability. And customers have a new power through transparency for comparison shopping.

There is valuable data to be harvested through mobile devices, including clicks, sentiment, purchasing behavior, and more. But the curious thing is that most of the data from most industries including retail does not come directly from the customer. In fact, most is covert and is used without the customer’s awareness or consent.

Mobile devices represent the ultimate in communication capabilities and most users love them; when polled, one-third said they would rather give up sex than give up their mobile phones.29 The point is that using the device to simply scrape usage data might be useful but misses a larger opportunity. The reality is that customers have a lot more information about attitudes, preferences, and suggestions in their heads than is evident from their data streams.

Marketers realize that more data is better, but the usual ways of engaging with customers do not work well. For example, Internet retailers often ask for feedback on a product through a brief survey or requests for customers to post reviews, but not many customers feel the allegiance to a company/product to do this in a constructive way. Some surveyors are now paying for responses to surveys to induce better response rates. E-Rewards pays a modest amount, for example, $3.50 in loyalty points, to answer many questions on a wide variety of issues, from travel to electronics preferences.30 Appreciating the customer’s time by paying for it is a step in the right direction, but the process might feel like a survey mill that does not provide much connection between the company and the respondent. And some companies offer the “privilege” to be on an “insight panel,” which feels like being on an advisory panel, but seems to be more their taking information than an exchange of mutual value.

New ways to get customer input are emerging. These can include extending a positive experience to customers by making the focus of communications fun, engaging, and dedicated to purpose. Instead of focusing on the few who will not wean themselves off brand-name drugs to save money, it can focus on the many who do go to generics and provide positive reinforcements to improve health; for example, with games that teach about health, and free smartphone apps that monitor health. These can be offered and won through a lottery or quiz. Health Prize is an example of such a company with a tag line of “Driving measurable medication adherence with rewards, education, and fun!”31

And traditional marketing has its limits. Marketers acknowledge that many customers do not trust their hard-sell tactics and are more likely to take the advice of friends and fellow shoppers. Shoppers increasingly depend on customer product reviews, for example, from TripAdvisor or Amazon, and feel a responsibility to reciprocate with peers with their own published reviews. New marketing strategies focus on inducing a “buzz” and accelerating online word of mouth through social media such as Twitter and Pinterest.32 But this is not relinquishing marketing to the wisdom of the crowd entirely. Rather, it is smartly inducing the conversation and facilitating its spread.

How does this apply to healthcare? The traditional ways of collecting information from patients and members are not working well enough toward the critical goal of dramatically improving communication and coordination among providers, insurers, and customers. There is a reliance on what data are “under the lamppost,” such as claims data, and not on what data are available outside the industry that might be of use, as in other industries. Moreover, there is a huge cache of data available directly from people/patients that goes untapped. This includes data on health risks, ongoing functioning and emerging symptoms, behavior patterns related to self-care, feedback on care received, and much more.

Patients are being asked about their experience of care in hospitals; however, these surveys reach a small minority of patients. But people are tired of filling out forms. They do this multiple times during the same encounter at a physician’s office. They are reluctant to provide information to health plans because the trust level is low. People are tired of giving lots of data without being clear how about how it is being used.

Increasingly, people are circumventing the healthcare system in giving their feedback and are sharing it with friends on Internet sites, as they do when rating travel and merchandise. The challenge for healthcare is how to gather more data about members and patients, in order to service them better and help make them well, in a way that is mutually beneficial.

The answer might be complicated. What if the rules of the relationship were changed such that patients and families had much more say and the healthcare providers fully believed and practiced a cardinal rule about the use of data in healthcare: “No decisions about me are made without me”? What if the data collected were clearly linked to the patient’s well-being and outcome rather than helping organizations improve their own processes and profits? What if care were truly patient-centric? What if care was less bureaucratic and people felt that providers had the time to address their concerns? What if insurers led by putting the member first and started by changing the primary mode of communications to members, the Explanation of Benefits letter, so that it was understandable and helpful? What if people were really invited in to co-produce health? It really is about renewing the trust in the relationship bolstered by demonstrable attention to the customers’ needs that will increase information flow. And the key to communication about all these things might be the mobile phone.

Conclusions

Retailers are masters of customer analytics for marketing. The extreme challenges faced by the industry from the Great Recession, hypercompetition, and disruptive innovation from Internet sellers and digital technologies have resulted in increased attention to the customer. More than any other industry, retailers have developed leading-edge analytic techniques to capture the minds and wallets of customers. They have used transaction data from within the industry, clicks data from the Internet, purchased data on a wide range of personal attributes, and video recognition technologies to make tailored offers in real time.

Although retail is the highest-rated industry for customer experience, and healthcare is the lowest, the industry does not achieve this through close personal relationships with customers. Most marketing and much of sales are accomplished through mass customization. Retailers have refined this to the point that a store like Target can predict what you want to buy before you realize it and then provide the messages and incentives to close the deal.

There are four analytic sweet spots that have relevance to healthcare, including predictive modeling and the use of nontraditional data, customer lifetime value, market matching, and mobile phone devices, along with social media. Insights on the use of these methods in healthcare include using nonconventional data to predict obesity and other microsegments not usually ascertainable with within-industry data such as claims; using CLV, not to skim for the healthy and disenfranchise the sick, but to concentrate on producing longer and more functional lives by measuring lifetime functioning and paying for it accordingly; using data to understand behavior change opportunities during “moments that matter” for many health microsegments; and realizing that mobile is the platform for better communications, the collection of data that matter, and truly listening to customers.