Juan Aguerrebere, Jr., CPA

Perez Abreu, Aguerrebere, Sueiro LLC

An enterprise reports its results of operations in a set of financial statements that includes an income statement. The format of the income statement and its components of income have been the subject of controversy, and as a result numerous pronouncements of professional accounting bodies have addressed related issues. For the most part the central issues discussed in these pronouncements involve the distinction between normal recurring items of profit and loss and other items that affect the determination of income.

One such pronouncement, Accounting Principles Board (APB) Opinion No. 9, "Reporting the Results of Operations," states that net income reported on an income statement should reflect all items of profit and loss recognized during the period with the exception of prior period adjustments. The APB also refined the appropriate reporting format in APB Opinion No. 30, "Reporting the Results of Operations—Reporting the Effects of Disposal of a Segment of a Business, and Extraordinary, Unusual and Infrequently Occurring Events and Transactions." Both of these Opinions required that extraordinary items, as defined in Section 6.3, be segregated from the results of continuing and ordinary operations of the entity. Opinion No. 30 expanded the categories to be segregated from continuing and ordinary operations by specifying the treatment of discontinued operations and unusual or infrequently occurring items.

In general, the term discontinued operations refers to the operations of a "segment of a business" which has been or is planned to be abandoned or otherwise disposed of. The term segment of a business is defined as a component of an entity whose operations encompass a separate major line of business or class of customer. A component can be a subsidiary, division, joint venture, or unconsolidated investee. This definition of segment of a business should not be confused with the use of the term segment in Statement of Financial Accounting Standards (SFAS) No. 14, "Financial Reporting for Segments of a Business Enterprise."

The component should be reported as discontinued during the first reporting period in which management having the requisite authority commits itself to a formal plan of disposal. This is referred to as the measurement date. Once the decision to dispose of the component has been made, the component's operating results prior to the measurement date should be presented on the income statement as a separate category before extraordinary items. Any financial statements for a prior period, presented for comparative purposes, should be restated to conform to this presentation.

The formal plan of disposal should include (1) an identification of the major assets to be disposed, (2) the expected method of disposal, (3) the expected period required to complete the disposal, which should generally be within 12 months of the plan's adoption, (4) an estimate of the results of operations from the measurement date to the disposal date (phase-out period), and (5) the estimated proceeds to be realized by disposal.

The disposal date is the closing date if a sale is contemplated. Any gain or loss on the actual disposal of the segment, combined with the operating results of the discontinued operations, should be disclosed separately on the face of the income statement or in a note. Income taxes applicable to both items should also be disclosed on the face of the income statement or in a note to the financial statements.

APB Opinion No. 30 states that the discontinuance of a part of a segment of a business, that is the phasing out of a product line or class of service, or a shift in production or marketing emphasis or location is incidental to the evolution of an entity and, accordingly, does not qualify for treatment as a discontinued operation. Although in theory the criteria may seem straightforward, accountants have had difficulty interpreting these broad criteria in practice. Recognizing this difficulty, the American Institute of Certified Public Accountants (AICPA) issued "Accounting Interpretation of APB Opinion No. 30" in November 1973 to provide guidance on the classifications found in Opinion No. 30. The interpretations provide the following examples as situations that qualify as discontinued operations:

The sale of a major division that represents an entity's only activity in a specific industry; the assets and results of operations of the division are clearly separable.

The sale by a meat-packing company of a 25 percent interest in a professional ball club that they had accounted for under the equity method.

The sale by a communications company of all its radio stations (constituting 30 percent of total consolidated revenues). The remaining activities are television stations and a publishing company. The assets and results of operations of the radio station are clearly separable both physically and operationally.

The disposal by a food distributor of one of its two food divisions, which use significantly different channels of distribution. One division sells food wholesale primarily to supermarket chains, and the other division sells food through its chain of fast food restaurants, some of which are franchised and some of which are company-owned. Although both divisions are in the business of distribution of food, the sale of food through fast food outlets is vastly different in nature from wholesaling food to supermarket chains. Thus, by having two major classes of customers, the company has two segments of business.

The method of recording the discontinuation or disposition of a business segment is determined by whether there is a gain or a loss. A gain should be recognized when it is realized, usually at the disposal date. Losses, on the other hand, should be anticipated and recorded at the measurement date. The gain or loss on disposal is calculated at the measurement date, using estimates of the results of operations during the phaseout period. The APB was concerned that the gain or loss on disposal could conceal normal write-downs on a going-concern basis, for example, inventory or receivable adjustments. Thus it stated that such write-downs should be included in results of operations prior to the measurement date unless clearly and directly associated with the disposal decision. The Emerging Issues Task Force (EITF) in Issue No. 85-36, "Discontinued Operations with Expected Gain and Interim Operating Losses," considered the need for clarification of APB Opinion No. 30 and the related interpretations thereof in accounting for any expected losses from the measurement date to the disposal date when a gain on disposal was expected. The Task Force consensus stated that estimated losses from operations should only be deferred until the disposal date if there is reasonable assurance that a net gain will be realized. The Task Force also reached consensus on two underlying issues. The first consensus applied the previous consensus to sales that do not meet the criteria of a segment. Second, it stated that all multiple disposals of segments under the same formal plan should be reported as a combined amount. However, if the criteria for discontinued segments are not met, these disposals, such as a portion of a line of business, should not be combined.

The EITF, "Accounting for Discontinued Operations Subsequently Retained" in Issue 90-16, considered a situation in which a company decides to dispose of a segment of its business in accordance with APB No. 30. In accruing the loss on disposition of the segment, the company wrote down assets to net realizable value. The assets would not have been treated as impaired and no loss would have been accrued if the company had not decided to discontinue the operations of that segment. In the next period, management decided to retain the segment. The following accounting issues are present:

Issue 1—Should any of the accrued losses on writing down the segment to net realizable value be reversed now that the segment is no longer being discontinued?

Issue 2—Should the financial statements of the prior period be restated or reclassified as a result of the subsequent decision to retain the business segment?

The EITF reached a consensus that the remaining estimated accrued loss should be reversed in the period the company decides to retain the business segment. The portion of the prior period loss related to actual operations of the business in the prior period should not be reversed. There is to be continual evaluation of the business segment following impairment guidelines as practiced by the company, and any individual asset impairments are to be classified as continuing operations.

The EITF concluded that the reversal is not an error and the prior periods should not be restated. However, the business segment's results of operations reported in prior periods should be reclassified from discontinued to continuing operations. The remaining estimated accrued loss should continue to be reported as discontinued segments in the prior period financial statement. In the current reporting period, continuing operations should include current period operating results of the segment. The remaining unaccrued loss should be reversed as part of discontinued operations.

For those filing with the Securities and Exchange Commission, the observer called for the following six additional disclosures:

Reason for reversal of decision

Total segment assets, liabilities, revenues, and operating results of the segment previously reported as discontinued

Amount of loss recognized when the segment was recorded at net realizable value and basis for calculation

Disclosure of impairment losses recorded by business segment (Losses due to asset impairment must be classified before income from continuing operations.)

Disclosure of amount and components of amounts of accrued losses subsequently reversed

Management discussion and analysis (MD&A)

The EITF also considered the questions of whether interest or general corporate overhead could be allocated to a discontinued operation. The Task Force reached a consensus that general corporate overhead may not be allocated. Interest may be allocated, although it is not required to be allocated. If interest is allocated, the calculation of the method to be used is described in EITF Issue No. 87-24, "Allocation of Interest to Discontinued Operations." The SEC observer indicated that public companies must clearly disclose the accounting policy to allocate interest, the method used to determine the amount of interest allocated and the amount allocated to premeasurement date, and estimated predisposal date periods.

Certain disclosures are required for the periods from the measurement date to the disposal date:

Identification of the discontinued segment

Expected disposal date and manner of disposal (sale or abandonment)

Remaining assets and liabilities of segment at the balance sheet date

Results of operations and any proceeds from disposal of the segment during the period from the measurement date to the balance sheet date (and a comparison with any prior estimates)

Disclosure of per share data, although not separately required for discontinued operations, is commonly given on the face of the income statement or in the notes.

In the Staff Accounting Bulletin (SAB) 93, "Accounting and Disclosure Regarding Discontinued Operations," the SEC considered seven clarification issues with respect to discontinued operations: (1) the method of disposal is not determined, (2) the disposal plan requires more than one year to complete, (3) accounting for the abandonment of a business segment, (4) disposal of an operation with significant interest retained, (5) classification and disclosure of contingencies relating to discontinued operations, (6) accounting for subsidiaries that management intends to sell, and (7) accounting for the spin-off of a subsidiary.

The SEC considered the circumstances where an entity adopts and announces a plan to discontinue a segment but has not determined the manner by which certain material operations will be discontinued (sale, spin-off, or liquidation). The SAB indicates that in such circumstances paragraph 14 of APB 30 has not been complied with since the "expected method of disposal ... and the expected proceeds or salvage to be realized by disposal" are not known.

Where there are multiple sales of assets or divisions contemplated under a plan of disposal, all such sales should occur within one year. The SEC believes that to qualify under paragraphs 15–17 of APB 30 for classification outside of continuing operations, the plan of disposal must contemplate the consummation of the disposal of all portions of the business segment within 12 months of the plan's adoption. The staff of the SEC believes that the accounting estimates needed under accounting for a discontinued operation cannot be developed with sufficient reliability if projections beyond 12 months from the plan's adoption are required.

If a company adopts a plan of discontinuance but is required by contract or regulation to continue to provide services for periods remaining under existing contracts which may exceed one year, discontinued operation accounting may be appropriate. The staff will not object if discontinued accounting is used when the company will not accept new business (other than it is required to do under existing contracts or regulations) within 12 months of a plan's adoption. The operating results of the segment through final termination must be estimable with reasonably accuracy.

When a company sells a majority interest in a segment but retains an interest sufficient to require equity accounting under APB 18, discontinued accounting is not appropriate. The staff believes that the transaction should be accounted for as a disposal of a portion of a line of business.

If a company had appropriately accounted for the disposal of a segment in a previous year, but had continuing obligations under the contract so that estimates were required, revisions of those estimates are to be classified as discontinued operations as indicated in paragraph 25 of APB 30. However, the staff believes that any changes in the carrying value of assets received in the exchange as consideration should be classified within continuing operations.

When a company plans to sell a segment but discontinued accounting is not yet appropriate, the company cannot deconsolidate the segment under the view that control is temporary under SFAS 94. The staff believes that the concept of control as indicated in SFAS 94 does not encompass planned sales. The concept of temporary control is intended to encompass events that are outside the control of the entity.

If a company spins off a subsidiary, it should not ordinarily account for the transaction by restating previous financial statements as a change in entity under paragraph 30 of APB 20, as if the company never had an investment in the subsidiary. In limited circumstances involving an initial public offering (IPO), the staff has not objected to such accounting if the spin-off was completed prior to the effectiveness of the offering and certain conditions are met.

An extraordinary item is an event or transaction that meets two criteria: It must be both unusual in nature and infrequent in occurrence. Otherwise, an event or transaction is generally presumed to be either an ordinary or a usual activity of the entity. Being either unusual in nature or infrequent in occurrence does not qualify it as an extraordinary item [see Subsection 11.3(e)].

As mentioned above, the first criteria an item must meet to be considered extraordinary is to be unusual. The underlying event or transaction should be clearly unrelated to the ordinary and typical activities of the entity. This definition encompasses the specific characteristics of the entity, including, for example, the industry in which it operates, the geographical location of its operations, and the extent of government regulation. Thus an event or transaction may be unusual for one industry but normal for another.

The second criterion for an extraordinary item to meet is that the event or transaction is not reasonably expected to recur in the foreseeable future and is not considered to be frequently occurring. This definition considers the same features as items of unusual nature, such as industry, geographical location, and government regulation. Thus this criterion may be met by one company whereas the same underlying event would not be infrequent to another company. Past history of the company provides evidence to assess the probability of recurrence of an event.

Certain gains and losses are, by definition (APB Opinion No. 30, par. 23), considered not extraordinary items, such as:

Write-down of receivables, inventories, equipment leased to others, or intangible assets

Gains or losses from foreign exchange transactions or translations (including major devaluations and revaluations)

Gains or losses on the disposal of a segment of a business (discontinued operations)

Gains or losses from the sale or abandonment of property, plant, or equipment used in a business

Effects of a strike (including an indirect effect such as a strike against a major supplier)

Adjustment of accruals on long-term contracts

Only in rare instances may an event or transaction included in first and fourth bullets above clearly meet the criteria and be included in extraordinary items. Such instances would occur if the gain or loss on such an event or transaction is the direct result of a major casualty, an expropriation, or a prohibition under a newly enacted law.

Some items that apparently would not meet the criteria of an extraordinary item must be classified as such under existing authoritative literature. Two such items that fit this description are gains and losses on extinguishment of debt as cited in SFAS No. 4, "Reporting Gains and Losses from Extinguishment of Debt," and gain on the restructuring of debt in a troubled situation as discussed in SFAS No. 15, "Accounting by Debtors and Creditors for Troubled Debt Restructurings." The accounting and reporting for extinguishments and troubled debt restructurings are discussed in Chapter 20.

The effect of an extraordinary item should be segregated if its effect is material to income before extraordinary items, to the trend in earnings before extraordinary items, or to other appropriate criteria. The materiality of individual events or transactions is considered separately and not aggregated unless the effects result from a single identifiable transaction or event that meets the criteria of an extraordinary item. The preference expressed in APB Opinion No. 30 is for individual descriptive captions and amounts for each extraordinary event or transaction on the face of the income statement. However, disclosure in the notes to financial statements describing the nature of the event or transaction comprising the extraordinary item and the principal items entering the calculation of the gain or loss is acceptable. The extraordinary item should be shown net of applicable income taxes.

Per share amounts for income before extraordinary items and net income should be given on the face of the income statement. There is no requirement to give the per share amount of the extraordinary items, but such disclosure is common.

A material event or transaction that is either unusual or infrequently occurring, but not both, is by definition not an extraordinary item. Material gains or losses of this nature should be shown separately on the face of the income statement as a component of income from continuing operations. These items are not shown net of tax, nor is per share disclosure permitted on the face of the income statement. However, note disclosure may be given that presents the item net of tax and discloses the per share effects. The discussion that follows covers four special items and their reporting: disposal of part of a segment, restructuring charges, takeover defense, and sale of stock by a subsidiary.

The gain or loss on the disposal of part of a segment of a business is not an extraordinary item or a discontinued operation. Thus it may be reported as a separate component of continuing operations. The measurement principles used to calculate gain or loss on disposal are described in paragraph 15 of SFAS No. 121, "Accounting for the Impairment of Long-Lived Assets and for Long-Lived Assets to Be Disposed Of." Unlike the disposal of a segment, a company is not permitted to accrue expected operating losses when a commitment date is reached to dispose of part of a segment. The results of operations prior to the measurement date should not, however, be shown separately on the income statement. This information may be disclosed in the notes to financial statements along with per share data.

Some examples of situations not qualifying as discontinued operations that were also given in the interpretations of APB Opinion No. 30 are:

Sale of a major subsidiary in one country by an entity that has other activities in the same industry in other countries

Sale of an interest in an equity investee in the same line of business as the investor

Sale of assets related to the manufacture of wool suits when the entity manufactures suits from synthetic products elsewhere (considered only product line disposal)

During the middle to late 1980s, enterprises began to restructure their operations. These corporate restructurings involved sales of equipment or facilities, severance of employees, and relocation of operations. The EITF considered the income statement presentation (ordinary or extraordinary) of such restructurings but was unable to reach a consensus in EITF Issue No. 86-22, "Display of Business Restructuring Provisions in the Income Statement." It only stated that entities should use their own judgment. The SEC subsequently addressed this issue in SAB No. 67, "Income Statement Presentation of Restructuring Charges," issued in December 1986. The SEC position stated that restructuring charges should be shown as a component of continuing operations and separately disclosed if material. Since Staff Accounting Bulletins (SABs) do not apply to nonpublic companies, the EITF considered in Issue No. 87-4, "Restructuring of Operations: Implications of SEC Staff Accounting Bulletin No. 67," whether the SEC position was GAAP for nonpublic companies. The Task Force indicated that following the SAB provisions is not required for nonpublic enterprises to be in accordance with GAAP. The Task Force agreed that consistent with its views expressed in Issue No. 86-22, nonpublic companies should exercise judgment in selecting the most meaningful income statement presentation.

The SEC observer later provided clarification of the extent of SAB No. 67, such as:

SAB No. 67 was not intended to address the presentation of a simple sale of assets or a portion of a line of business.

The SAB restates the position of the SEC observer that showing "earnings from operations before provisions for restructuring of operations," which is acceptable under EITF Issue No. 86-22, is not acceptable for SEC registrants.

In the early 1990s, companies were reporting restructuring charges on an increasing basis. Restructuring charges as reported comprised various broad types of expenses. Restructuring charges included costs of severance and termination, costs to eliminate or consolidate product lines, costs to close or relocate operations or plants, costs to restrain employees to use newly developed systems, and losses on impairment or disposal of assets. In EITF Issue 94-3, "Liability Recognition for Certain Employee Termination Benefits and Other Costs to Exit an Activity Including Certain Costs Incurred in a Restructuring," the Task Force reached the following tentative conclusions.

A liability for employee termination benefits should be recognized when management approves the plan if all the following conditions exist:

Prior to the date of the financial statements, management with the appropriate authority to involuntarily terminate employees approves and commits the company to the plan (termination plan) that establishes the benefits to be received upon termination.

Prior to the date of the financial statements, the plan and benefit arrangements are communicated to employees in sufficient detail to enable affected employees to calculate their benefits.

The plan specifies the number of employees, job classification, or function and their location.

The foregoing provisions do not apply to termination benefits paid as part of the disposal of a segment, pursuant to an ongoing benefit plan, or under the terms of a defined compensation contract.

Costs that have no future economic benefit should be accrued on the commitment date. The commitment date is the date when all the following conditions are met.

Management with the appropriate authority commits the company to the exit plan.

The plan identifies all actions to be taken (i.e., activities to be continued or closed/sold, including method of disposition and expected date of plan completion).

Actions required to implement the plan begin as soon as possible after the commitment date, and the period of time to complete the plan indicates that changes to the plan are not likely.

The costs to be recognized under the exit plan can have no future benefit to continued operations. Costs meeting this requirement should be recognized at the commitment date if they are not associated with or are not incurred to generate revenues after the commitment date of the exit plan and meet either criterion (1) or (2) below.

The cost is incremental to other costs incurred prior to the commitment date and is incurred as a direct result of the exit plan.

The costs will be incurred under a contractual commitment existing prior to the commitment date and will not economically benefit the company.

Costs should be recorded when they are reasonably estimable. Any unrecognized costs should be recorded when they can be reasonably estimated.

Results of operations after the commitment date are not exit costs. Costs to sell assets under the exit plan are also not exit costs. Costs not qualifying as exit costs should not be recognized at the commitment date but when an obligation is actually incurred.

The EITF Issue 94-3 has significant disclosure requirements and also provides many examples to illustrate applications of its provisions.

A question created by the takeover surge is the appropriate presentation of takeover defense expenses on the income statement. The FASB issued Financial Technical Bulletin (FTB) No. 85-6, which makes the following two statements:

A company should not classify the cost to defend itself from a takeover or the costs attributable to a "standstill" agreement as an extraordinary item.

If a company repurchases shares for a price significantly in excess of current market from an unwanted suitor, it must include stated or unstated rights. Accordingly, only the amount representing fair value should be accounted for as the cost of Treasury shares, any excess should be accounted for according to its substance, presumably charged to expense. The SEC has stated that in applying FTB No. 85-6 quoted market represents fair value; use of appraised values that differ from public market values is not acceptable.

Prior to the issuance in 1983 of SAB No. 51, "Accounting for Sales of Stock by a Subsidiary," most parent companies had accounted for the effects on its equity in the subsidiary of a sale of additional stock by a subsidiary as a capital transaction. In SAB No. 51, the SEC indicated that it had reconsidered this position where the sale of such shares by the subsidiary is not part of a broader corporate reorganization. The SEC, in its reconsideration, stated that it accepts the advisory conclusions of the AICPA issues paper "Accounting in Consolidation for Issuances of a Subsidiary's Stock," which indicates that profit or loss should be recognized in these situations. The SEC concluded that if gains (losses) are recognized from issuances of a subsidiary's stock as income statement items, they should be shown as a separate line item (without regard for materiality) and clearly designated as nonoperating. Subsequently SAB No. 81, "Gain Recognition on the Sale of a Business or Operating Assets to a Highly Leveraged Entity," was issued in 1989, indicating that gain recognition may not be appropriate where a subsidiary is sold to a highly leveraged entity. Further, SAB No. 84, "Accounting for Sales of Stock by a Subsidiary," which was also issued in 1989, gives additional guidance on recognizing a sale of stock by a subsidiary as a gain.

The income statement treatment in consolidation of gains or losses for the sale of stock by a subsidiary represents a choice among acceptable accounting methods and, once chosen, should be applied consistently to all stock transactions for any subsidiary that meet the conditions for income statement treatment. In SAB 84, the staff also deals with other interpretation matters, such as what constitutes a broader corporate reorganization.

The Financial Accounting Standards Board has exposure drafts under consideration that will affect accounting for guarantees and consolidation of special purpose entities. On final approval, the proposed exposure drafts will affect the accounting and income statement presentation for these areas.

The FASB stated in SFAS No. 154 "Accounting Changes and Error Corrections," that:

A presumption exists that an accounting principle once adopted shall not be changed in accounting for events and transactions of a similar type. Consistent use of the same accounting principle from one accounting period to another enhances the utility of financial statements for users by facilitating analysis and understanding of comparative accounting data.

FASB No. 154 defines the term accounting change to mean "a change in (1) an accounting principle, (2) an accounting estimate, or (3) the reporting entity. The correction of an error in previously issued financial statements is not an accounting change."

A change in accounting principle involves the adoption of a generally accepted accounting principle different from the one previously used for reporting purposes. Thus a change in accounting principle involves a choice among two or more generally accepted accounting principles and the method of applying the chosen principle. It does not include (1) initial adoption of an accounting principle to report first-time or previously immaterial events or transactions, or (2) adoption or modification of an accounting principle because of events or transactions that are clearly different in substance from previously occurring events or transactions.

SFAS No. 154 provides that an entity should change an accounting principle only if the change is required by a newly issued accounting pronouncement or the entity can justify its use based on the basis that it is preferable.

An accounting change should be reported through retrospective application of the new principle to all prior periods, unless it is unpractical to do so. Retrospective application involves the following:

The cumulative effect of the change on periods prior to those presented shall be presented as adjustments to carrying values of the assets and liabilities as of the beginning of the first period presented.

An offsetting adjustment, if any, to the opening balance of retained earnings.

Financial statements for each individual prior period presented shall be adjusted to reflect the effects of applying the new principle.

Sometimes it is not practical to determine the cumulative effect of applying a change in accounting principle to all prior periods presented. In such cases, the new accounting principle should be applied to the carrying amounts of the assets and liabilities as of the beginning of the earliest period to which the new principle can practically be applied. Finally, if it is impractical to determine the cumulative effect on any prior period, the new accounting principle shall be applied prospectively to the current and future periods.

SFAS No. 154 indicates that it should be consider impractical to apply the effects of a change in accounting principle retrospectively only if one of the following conditions exist:

After making every reasonable effort to do so, you are unable to apply the requirement.

Retrospective application requires assumptions about management's intent in a prior period that cannot be independently substantiated.

Retrospective application requires significant estimates of amounts, and it is impossible to distinguish objectively information about those estimates that (1) provides evidence about circumstances that existed on the date(s) at which those amounts would arise under retrospective application, and (2) would have been available when the financial statements for that prior period were issued.

SFAS 154 requires that the entity include in the restated periods only the direct effects of a change in accounting principle, including any related income tax effects. Indirect effects, such as changes profit sharing or royalty payments, should not be recognized in restated periods. Instead, such amounts should be recognized in the period the change is made.

Changes in accounting estimates are a normal part of the operations of an entity, and the estimation of the effects of future events is an inherent part of preparing financial statements. Accounting estimates involve the judgments that management of the entity must make concerning incomplete transactions or events on the basis of the information presently available. Obviously these estimates change as new or better information becomes available or new events occur. Examples of items that require estimates are (1) uncollectible receivables, (2) inventory obsolescence, (3) service lives and salvage value of depreciable assets, (4) warranty costs, (5) amortization period of deferred charges, and (6) recoverable mineral reserves.

Changes in estimates are sometimes difficult for the accountant to distinguish from an accounting principle change as they cannot clearly be classified as either one or the other. For example, a change from deferral and amortization of an expense item to expensing as incurred, when the future benefits of the deferred item are doubtful, may have been made in partial or complete recognition of a change in estimated future benefits. Such changes in principle that are inseparable from changes in estimate are treated as changes in estimate.

The effects, if material, of a change in estimate on income from continuing operations and net income (including per share amounts) for the current year and for future years, if applicable, should be disclosed in a note describing the change. A change in estimate should not be accounted for retroactively or by reporting pro forma amounts. Disclosure of changes in estimates made in the ordinary course of business (e.g., uncollectible receivables, percentage complete on long-term contracts, or inventory obsolescence) is not required; however, it is recommended if the effect of a change in estimate is material.

A change in reporting entity is a change in accounting principle. This type of change results in financial statements of a different reporting entity and usually is limited mainly to (1) presenting consolidated or combined financial statements in place of financial statements of individual reporting entities, (2) changing specific subsidiaries or companies included in the financial statements of the consolidated or combined group of companies, and (3) changing among cost, equity, and consolidation methods of accounting for subsidiaries or other investments in common stock. The financial statements for the period of a change in reporting entity should disclose the nature and reason for the change and the effect on income before extraordinary items and net income (including per share amounts). A change in reporting entity due to a pooling of interests should be reported as provided in APB Opinion No. 16, "Business Combinations." In June 2001, the FASB issued SFAS No. 141, "Business Combinations." SFAS No. 141 requires that all business combinations be accounted for by using the purchase method of accounting. The provisions of SFAS No. 141 apply to all business combinations initiated after June 30, 2001. SFAS No. 141 also applies to all business combinations accounted for using the purchase method for which the date of acquisition is July 1, 2001, or later.

Although not an accounting change, the correction of an error in previously issued financial statements involves factors similar to those encountered in reporting a change in accounting principle. Errors arise from (1) mathematical mistakes, (2) oversight or misuse of facts existing at the time when financial statements are prepared, and (3) mistakes in the application of accounting principles, including a change from an unacceptable accounting principle to a generally accepted accounting principle.

Corrections of errors should be reported as prior period adjustments (see Section 11.6). The nature of the error and the effect on income before extraordinary items and net income (including per share amounts) should be disclosed in the period when the error was discovered and corrected.

Materiality, applicable to accounting changes and corrections of errors, is considered in relation to both the effects of individual changes and the aggregate effect of all changes. A change or correction may be material to (1) income before extraordinary items or net income of the current year, or (2) the trend in earnings. In both cases the disclosures referred to above should be made. If the change or correction is not material according to these criteria but is reasonably certain to have a material effect in later periods, disclosure of the change or correction should be made whenever the period of change is presented. SAB No. 40 stated that, if prior periods' income statements are not restated because the amounts are immaterial, the cumulative effect of the change should be included in the determination of income for the period in which the change was made. However, if the cumulative effect is material to the current period's income, or to the trend in earnings, prior period income statements would have to be adjusted.

The following disclosures are required when an entity effects a change in accounting principle:

The nature and reason for the change, including an explanation of why the new principle is preferable

The effect of the change on income from continuing operations, net income, any other affected financial statement line item, and any affected per-share amounts for the current period and any prior periods retrospectively adjusted

The cumulative effect of the change on retained earnings or other components of equity or net assets as of the beginning of the earliest period presented

If retrospective application to all periods is impracticable, disclosure of the reasons therefore, and a description of the method used for the change

If indirect effects of a change are recognized, the financial statements should disclose (1) a description of the indirect effects including the amounts that have been recognized in the current period, and (2) if practicable, the amount of the total recognized indirect effects of the accounting change that are attributable to each prior period presented

The first Form 10-Q, quarterly financial statements, filed with the SEC subsequent to an accounting change, must include a preferability letter prepared by the company's accountants. A preferability letter for a change made in the fourth quarter of the fiscal year may be submitted in the company's annual report on Form 10-K. If this is not done, the preferability letter must be submitted when filing the next Form 10-Q.

Disclosure of a change in accounting principle should include an explanation of why the new accounting principle is preferable. Auditing standards require that the accountant assess the reasonableness of management's justification for the change in accounting principle before concurring. In FRR No. 1 (ASR No. 177), the SEC issued requirements beyond those specified in professional standards. By amending Form 10-Q, FRR No. 1 (ASR No. 177) requires the accountant to issue a letter indicating whether the newly adopted accounting principle is preferable under the circumstances. A letter need not be issued, however, if the change in accounting principle was mandated by the FASB or another authoritative standards setter such as AcSEC or EITF.

Corrections of errors should be reported as prior period adjustments, as specified in paragraph 10 of SFAS No. 16, "Prior Period Adjustments," as amended by SFAS No. 109. The disclosure of their effects, both gross and net of taxes, on net income of prior periods is required in the financial statements for the year of the adjustment. Disclosure of the effects on each prior period presented and on per share earnings are also required.

In the deliberations leading to the issuance in 1977 of SFAS No. 16, questions arose as to the statement's applicability to interim as well as annual financial statements. The FASB concluded that certain practices regarding interim information and prior period adjustments should be continued and others should be discontinued. A section entitled "Adjustments Related to Prior Interim Periods of the Current Fiscal Year" was included in SFAS No. 16. Interim reporting is covered in Chapter 13.

The following listings should provide guidance to accountants in the reporting of events and transactions as extraordinary, or material gains and losses not considered extraordinary, and accounting changes. The reporting of these items requires considerable judgment.

A listing for discontinued operations is not presented because the reporting of this type of event does not vary in practice. Furthermore, the issuance of SFAS No. 16 has restricted the type of items to be reported as prior period adjustments to the extent that such a listing is not necessary.

The primary source used to obtain this listing is: Accounting Trends and Techniques (AICPA, 1994).

Extraordinary Items | |

Adjustment of prior period extraordinary item | Expropriation |

Debt extinguishments | Major casualties (fire) |

Material Gains and Losses Not Considered Extraordinary | |

Diminished value of assets | Partial closing of operation facility |

Discontinuance of part of a business | Plant relocation expenses |

Environmental claims | Restructuring charges |

Excess insurance proceeds | Retirement plans expense |

Gain/loss from sale of assets | Settlement of claims |

Gain on sale of equity interest | Strike expense |

Litigation settlement | Takeover defense |

Accounting Changes | |

Change in depreciation method | Computational error |

Change in method of determining inventory costs | Subsequent discovery of facts existing at date of accountants' report |

Change from the full-cost method to successful efforts method of oil and gas properties | Change in Reporting Entity |

Change from LIFO method to FIFO method of inventory valuation | Effects impractical to determine |

Change to conform to FASB statements that require or permit retroactive restatement | Change from FIFO cost to LIFO method inventory valuation Change in depreciation method for new assets only |

Correction of an Error | |

Change from unacceptable principle to GAAP | Change in Estimate |

Of allowance for doubtful accounts | |

Of depreciable lives | |

Of income taxes | |

Of restructuring costs |

The SEC expressed its views in SAB No. 1 (codified in 1981 in SAB No. 40) on including leased or licensed departments' revenues in the caption "Total revenues," as is common in the financial statements of department stores. The SEC stated that this practice is acceptable but the amounts should be disclosed separately in the income statement or notes thereto. Further, the service fee income from finance subsidiaries of retail companies should be separately disclosed in the income statement or a note.

SFAS No. 90 "Regulated Enterprises—Accounting for Abandonments and Disallowances of Plant Costs," issued in 1986, implies that a utility must charge a portion of the cost of an abandoned power plant to expense. In addition, any costs of a completed plant expected to be disallowed should also be charged to expense. The SEC was asked if these charges could be shown as extraordinary. The SEC responded in SAB No. 72, "Classification of Charges for Abandonments and Disallowances," issued in 1987, that these costs do not meet the criteria of APB Opinion No. 30 for unusual and infrequently occurring and should be shown as part of continuing operations.

In 1987, the SEC stated in SAB No. 69, "Income Statement Presentation," that registrants having casino and hotel operations should show the income from these operations separately. Thus, casino, hotel, and restaurant operations are commonly disclosed separately. In June 1997, the FASB issued SFAS No. 131, "Disclosures about Segments of an Enterprise and Related Information." SFAS No. 131 requires public enterprises to report certain information about operating segments in complete sets of financial statements of public enterprises and in condensed financial statements of their interim reporting periods. It also requires public enterprises to report certain information about their products and services, the geographic areas in which they operate, and their major customers. SFAS No. 131 requires general-purpose financial statements to include selected information reported based on a single segment. SFAS No. 131 requires that an enterprise report a measure of segment profit or loss and certain items included in determining segment profit or loss, segment assets, and certain related items. The reported information should correspond with the periods presented in the income statement of the public enterprise.

The FASB (the Board) was urged to address concerns of various users of financial statements regarding the practice of reporting some comprehensive income items directly within a balance sheet equity component. To promote harmonization of international standards, the FASB also discussed the concept of comprehensive income with various international accounting standards setting organizations. After exposing the FASB's tentative conclusions in this area, the Board issued FASB No. 130, "Reporting Comprehensive Income," in June 1997. This standard supplements and adds to but does not modify the previous discussion on income statement presentation.

The Statement establishes standards for reporting and display of comprehensive income and its components. The scope of this standard covers all enterprises that provide a full set of financial statements (financial position, results of operations, and cash flows). The provisions of the statement need not be followed by enterprises that do not have any elements of comprehensive income in any period presented nor by not-for-profit entities reporting under statement No. 117, "Financial Statements of Not-For Profit Organizations." Publicly held enterprises are required to apply this statement in externally reported summarized data or financial statements.

Thus, U.S. generally accepted accounting principles generally follow the all-inclusive concept of reporting (i.e., all items of income and expense flow through the income statement). In prior standards, certain specific exceptions to the all-inclusive income concept were made. Certain items that reflect changes in assets or liabilities were not reported in the income statement but were shown as a separate component of equity (i.e., items of foreign currency translation). The statement adopts the definition of comprehensive income used in concepts statement 6: "the change in equity [net assets] of a business enterprise during a period from transactions and other events and circumstances from nonowner sources. It includes all changes in equity during a period except those resulting from investments by owners and distributions to owners."

"Comprehensive income" is used to describe all components of comprehensive income including the results of operations. "Other comprehensive income" refers to those items that under GAAP are included in comprehensive income but not results of operations.

This standard was issued to better assist users of financial statements in gaining an understanding of and assessing an enterprise's activities and the timing and magnitude of cash flows. The FASB also believes that information on the separate components of comprehensive income needs to be disclosed to gain a more complete understanding of the enterprise's activities; accordingly, such disclosure of the components of comprehensive income is required.

All components of comprehensive income are to be reported in the periods when recognized. The Board believes that information about the components of comprehensive income may be more important than the total amount of comprehensive income. Therefore, the statement divides comprehensive income into two broad captions, net income and other comprehensive income.

Previous standards that require reporting of income from continuing operations, discontinued operations, extraordinary items, and cumulative effects of changes in accounting principles are unchanged by this standard.

Existing standards require separate classification of foreign currency items, minimum pension liability adjustments, and unrealized gains and losses on certain investments securities, are unchanged by this standard. The Board believes that leaving this requirement intact provides a familiar format for users of financial statements.

Reclassification adjustments that arise because of the double counting of certain items as part of net income for a period that were previously displayed as part of other comprehensive income need to be separately shown. For example, securities gains realized in the current period could have previously been included as unrealized gains in a previous comprehensive income statement. Accordingly, these must be offset in the period in which they are shown in net income to avoid including them twice in comprehensive income. The presentation of reclassification adjustments may be disclosed gross on the face of financial statements or net on the financial statements with appropriate disclosure in the notes to financial statements. The Board decided that it was not practicable to calculate the adjustment for minimum pension liability; therefore, a net display should be used for this item.

The Statement does not mandate a specific format for reporting comprehensive income. However, it does require that net income be separately displayed as a component of comprehensive income. Therefore, a one-statement approach or a two-statement approach may be used. These approaches are similar to current practice for displaying a statement of retained earnings. In addition, tax effects of the items displayed as elements of other comprehensive income may be shown either gross on the face of the statement or in notes to the financial statements. This treatment is similar to reclassification adjustments.

As a consequence of this change in display of other comprehensive income, the Board needed to consider its effects on other financial reporting criteria. Items such as reporting of prior period adjustments, statement of cash flows, other items reported in equity, and the reporting of equity investees needed to be considered.

The Board concluded that the reporting and display of any prior period adjustments would not conflict with current reporting of comprehensive income because of the retroactive restatement provisions of prior period adjustments.

It is possible that use of either the indirect method or the direct method reconciliation of the operating section of the statement of cash flows would be affected if elements of comprehensive income were noncash items. The Board concluded that the cash flow statement should not be amended for the impact of any of these items since it would not substantively add informational content.

The display of certain other items reported in equity were considered. The Board considered whether the display of deferred compensation expense arising from the issuance of shares before services are rendered (APB Opinion No. 25) or SFAS No. 123 or employee stock ownership plans (SOP 76-3) should be addressed in this statement. The Board concluded that these items have elements of both equity and expense characteristics, accordingly it was beyond the scope of the consideration of comprehensive income at this time and these items should be considered equity transactions. Similarly, taxes not payable due to reorganization accounting (SOP 90-7) gains and losses resulting from indexed contracts in company shares (EITF No. 94-7) should be considered as equity transactions.

In 1993, the FASB decided to amend the existing accounting literature on computing "earnings per share (EPS)" as detailed in APB Opinion No. 15, as amended. Users of financial statements believed that Opinion No. 15 was complex and had arbitrary provisions. Further, most of the rest of the world followed the methodology issued by the International Accounting Standards Committee (IASC). Accordingly, to simplify the computation of EPS and to harmonize U.S. standards with international standards, FAS No. 128, "EPS" was issued, and concurrently the IASC issued IAS 33, "EPS," which was substantially the same provision as FAS No. 128.

The terms "basic EPS" and "diluted EPS" are used to identify required per share data.

The amount of earnings for the period available to each share of common stock presumed to be outstanding during the reporting period.

The amount of earnings for the period available to each share of common stock outstanding during the reporting period and to each share that would have been outstanding assuming all dilutive potential common shares were outstanding during the reporting period.

Shares issuable for little or no cash consideration upon satisfaction of certain conditions pursuant to a contingent stock agreement. These shares include (a) shares issuable in future upon satisfaction of specified conditions, (b) shares that have been issued but are returnable if specified conditions are not met, and (c) shares that are held in escrow which are returnable.

The mean average of outstanding shares and those presumed to be outstanding during the period. Shares are presumed to be outstanding when there is no circumstance under which the shares would not be issued. These would include shares issued in poolings of interests and contingently issuable shares where the contingent conditions have been met.

Most other definitions or terms used in FAS No. 128 are similar to those terms used in APB No. 15 and in current practice.

Basic EPS is considered to be a measure of financial performance over the reporting period. It is required to be presented on the face of the income statement. Basic per share amounts are at a minimum required to be shown for income from continuing operations and net income. The calculation of basic EPS is computed by dividing the appropriate income statement amount (i.e., income available to common shareholders) by the weighted average number of outstanding common shares during the period.

Diluted EPS is intended to measure performance after giving effect to the maximum potentially dilutive common shares outstanding during the period. Diluted EPS is calculated as follows: Numerator same as basic EPS, then amended for effect of dilutive shares; denominator is basic EPS plus number of additional common shares that would have been outstanding if the potentially dilutive shares have been issued. These dilutive shares could arise from options, warrants, convertible securities, or shares issuable under acquisition or compensation agreements.

The numerator is adjusted to reflect the (1) add back to any convertible preferred dividends, or (2) after-tax effected interest on convertible debt associated with the respective dilutive securities and any nondiscretionary effects of the add backs, if any, such as pension or compensation expense. Also net of tax conversion is assumed to be at the most advantageous price to the security holder. Changes subsequent to the reporting period (i.e., active conversions or market price changes if applicable) are not adjusted retroactively.

As with Opinion No. 15, only the potential shares that are dilutive are used. If the potential conversion, exercise, and so forth are antidilutive, it is not assumed for the computation. This situation can arise if there is a loss from continuing operations for the period or the options or warrants are out of the money. Antidilution is measured against income from continuing operations after preferred dividends if there are multiple income captions required to be shown.

The treasury stock method should be used to reflect the dilutive effect of call options, warrants, and their equivalents (stock purchase contracts, partially paid subscriptions, and nonvested stock granted to employees). Under this method, exercise is assumed only when the average market price during the reporting period exceeds the exercise price. If options are exercised or expired, the period of time during the reporting period prior to such exercise or expiration must be added to the denominator. The treasury stock method assumes that:

For unexercised securities (options, warrants, etc.) that were outstanding at the beginning of the period, common shares are assumed issued.

The proceeds from any assumed exercise are used to purchase shares at an average market price during the period regardless if that is not the intent. Unlike APB Opinion No. 15, the modified treasury stock method (20 percent limitations) is not used.

The resulting incremental shares are included in the denominator.

Convertible securities are those that could result in the issuance of common shares for convertible debt or preferred stock. The impact of the potential issuance of the common shares on diluted EPS is determined using the if-converted method. The if-converted method is calculated as follows:

When dealing with convertible preferred, the applicable dividends are added to the numerator. The amount of such dividends to add back is the amount deducted from income from continuing operations. Remember, only convertible preferred dividends are added back for diluted EPS. Nonconvertible preferred dividends always reduced income available to common shareholders for both basic and diluted EPS.

If the convertible security is debt, then (a) applicable interest expense is added to the numerator, (b) the numerator is adjusted for other nondiscretionary income adjustments assuming a recalculation for the add back of interest in (A) above are made, and (B) the income tax effects of items (a) and (b), if any, are also added or subtracted from the numerator.

The denominator should be increased for the common shares issuable upon the assumed conversion of the preferred stock or debt at the beginning of the period. As with all diluted EPS calculations, if the effect of conversion upon income from continuing operations is antidilutive, conversion should not be assumed. If actual conversion occurs or the conversion period lapses, then conversion for diluted EPS is assumed for the period of time prior to conversion, redemption, or lapse. This results in any issued common shares being considered outstanding for diluted EPS calculations for the full period. After actual conversion, these shares are included as outstanding in the weighted average calculation for both basic and diluted EPS and are assumed converted for the period of time prior to conversion for diluted EPS calculations.

Under FAS No. 128, contingently issuable shares are included in basic EPS only when all necessary conditions prior to exercise have been satisfied, but the shares were not issued. However, for diluted EPS such shares are included in the denominator as of the beginning of the interim period in which the conditions were satisfied.

The calculation of diluted EPS prior to the end of the contingency period (period before all necessary conditions have been satisfied) assumes that the end of the reporting period is the end of the contingency period. Accordingly, the denominator would be increased for the number of shares that would be issuable based upon the conditions as they exist at the end of the reporting period if, and only if, the effect is dilutive.

It is possible that the sequence of assumed conversions could affect the amount of dilution. Thus a convertible security may be dilutive by itself but antidilutive when combined with other potential issuances of common stock. To reflect maximum dilution, each security or issue of security is stratified from the most dilutive to the least dilutive. If the effect of including the next issue of security in the calculation of dilutive EPS results in higher EPS, then such securities are antidilutive to the diluted EPS calculation as a whole and should not be included. Therefore, the resultant dilutive EPS will reflect the lowest earnings per common share. Options and warrants will usually not be impacted by this rule since the use of the treasury stock method does not increase the numerator.

Each reporting period is treated as a discrete period for both basic and diluted EPS. Quarterly diluted EPS calculations under the treasury stock method should use the average market price for the period. For annual calculations, the sum of the shares used in each quarter divided by 4 should be used only if all quarters were profitable. If a loss was experienced, the effect on the quarters would be antidilutive. For annual calculations, when a loss was experienced during at least one quarter, the average market price for the period should be used for the treasury stock method. Thus, it is still possible that diluted EPS for the year or year-to-date amounts may not equal the sum of the respective quarters.

It is also possible that contingently issuable shares under performance preferred would also be considered outstanding for one quarter and not another. Year-to-date calculations, if all quarters are profitable, are the same as above. If a quarter is a loss, the inclusion of all contingently issuable shares would be antidilutive to the quarter and therefore excluded. However, as with the treasury stock method, these contingently issuable shares would be included in year-to-date calculations if they are dilutive.

Interim period EPS are not restated because of the resolution of the contingent issuance criteria.

The presentation under FAS No. 128 is similar to that of APB Opinion No. 15. Enterprises that have a simple capital structure need report on the face of the income statement only basic EPS. Basic EPS should be shown for at least income from continuing operations and net income. Enterprises with more complex capital structures (i.e., those with potential common shares) should show both basic and diluted EPS for these captions.

If the enterprise has another required reporting caption on the income statement (i.e., extraordinary items, cumulative effect of accounting change), it can present the EPS information (basic and dilutive) on the face of the income statement or in the notes to the financial statements.

The EPS data should be presented for all periods for which an income statement or summary of earnings is presented. If diluted EPS is shown for any period, it should be shown for all periods. In a situation in which basic and diluted EPS are the same for all periods shown, they may be shown as one line item. Unlike APB Opinion No. 15, there is no materiality exception for presenting diluted EPS. Thus, if diluted EPS is different from basic EPS for any period, it must be shown regardless of the size of the difference. Although the terms "basic EPS" and "diluted EPS" are used in FAS No. 128, there is no requirement to use that specific terminology. Traditional language such as "earnings per common share" and "earnings per common share—after dilution" are also appropriate.

The FAS No. 128 requires the following three items for each period an income statement is presented:

A reconciliation of the numerators and denominators used in the calculation of basic and diluted EPS for income from continuing operations. This requirement pertains to the net effect of each class of potential dilution. Accordingly, supporting calculations or methodology (i.e., weighted average shares or treasury stock calculations) need not be shown.

The effect of preferred dividends on basic EPS in arriving at income from continuing operations available to common shareholders must be given. Theoretically, this could be met by including the preferred dividend requirement as a reconciling item of the numerator above. It should be noted that the SEC requires disclosure of income available to common shareholders on the face of the income statement when the difference between this calculation and net income is material.

Disclosure must be made of any securities that were omitted from the diluted EPS calculation because their effect was antidilutive but could be dilutive in the future.

If any transactions occur after the end of the period but before the financial statements are issued that would have changed the number of shares or potential shares materially, these must be disclosed. This disclosure requirement is similar to supplementary EPS under APB Opinion No. 15, although no calculation needs to be given.

Stock dividends and splits. If a stock dividend, split, or reverse split occurs, all per share calculations should be retroactively restated. This should be done even if the dividend or split occurs after the period but before the issuance of the financial statements. A stock right issued whose terms have an exercise price at issuance, less than the stock's face value, should be treated the same as a stock dividend.

Prior period adjustments. Certain accounting standards require retroactive restatement of financial statements for changes in accounting or error correction. The affected EPS data should be restated. When restating such data, all calculations are made as if new. Accordingly, items that either were or were not included in the original calculation could change. Potential shares that were dilutive could become antidilutive and vice versa. The effect of any restatement should be disclosed and expressed in per share terms.

Effective date. FAS No. 128 is effective for both interim and annual statements for periods ending after December 15, 1997. Earlier application is not permitted. Subsequent to this date, all EPS data (both interim and annual) need to be restated to conform to FAS No. 128. This requirement includes summaries presented outside the financial statements.

Exhibit 11.1 summarizes the effect of FAS No. 128 on pronouncements that were not specifically amended by FAS No. 128.

Basically, EPS is earnings available for common shareholders divided by the number of shares outstanding. More precisely, it is:

Adjustments are required for stock dividends or splits (including those affected after the balance sheet date but prior to issuance of the financial statements) and after adjustments to reflect the number of shares issued in poolings of interest retroactively to the beginning of year.

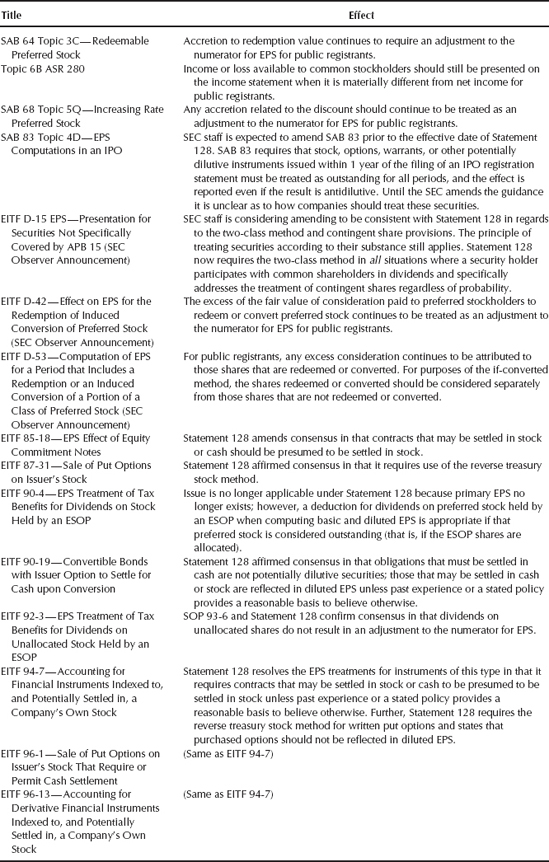

Figure 11.1. EITF and SEC literature on EPS. (Source: "Earnings per Share," FASB Statement 128. Copyright Ernst & Young LLP, October 1997.)

The following example illustrates the computation of the weighted average number of shares outstanding. Assume that the changes in a company's outstanding common shares during a year are as follows:

Date | Change in Common Shares | Number of Shares |

|---|---|---|

January 1 | Outstanding at start of year | 900 |

January 16 | Issued on exercise of options | 100 |

April 1 | Issued as 10% stock dividend | 100 |

August 11 | Issued in pooling of interests | 500 |

September 2 | Repurchase of treasury shares | (200) |

October 19 | Issued for cash | 400 |

December 31 | Outstanding at end of year | 1,800 |

Computation of the weighted average number of shares on a "days outstanding" basis would be as follows:

Date | Increase (Decrease) | Cumulative Total | Days Outstanding | Shares Days | ||

|---|---|---|---|---|---|---|

January 1 | 900 | |||||

Plus adjustments for: | ||||||

10% stock dividend | +90 | |||||

Shares issued in pooling | +500 | |||||

January 1 adjusted | 1,490 | × | 15 | = | 22,350 | |

January 16 issuance of options | 100 | |||||

Plus adjustments for: | ||||||

10% stock dividend | +10 | 1,600 | × | 229 | = | 366,400 |

September 2 Treasury repurchase | –200 | 1,400 | × | 47 | = | 65,800 |

October 19 cash issuance | +400 | 1,800 | × | 74 | = | 133,200 |

365 | 587,750 |

The weighted average number of shares outstanding for the year would be

In computing the weighted average number of outstanding shares, 90 of the 100 shares issued on April 1 as a 10 percent stock dividend are treated as outstanding retroactively to January 1, and 10 of the 100 stock dividend shares are treated as outstanding retroactively to January 16 (the date on which the options to which those shares related were exercised), for the following reason. When a stock dividend occurs, ownership in the company has been divided into a greater number of shares, each of which represents a proportionately smaller piece of the company. Retroactive recognition of the stock dividend for EPS computation purposes simply equates the prestock dividend shares with the poststock dividend shares. A stock split would be handled similarly. Prior years' EPS would also be restated for stock dividends and splits.

The 500 shares issued on August 11 in a business combination accounted for as pooling of interests are treated as outstanding retroactively to January 1 (with recomputation of prior years' EPS) because the earnings of the combining companies are pooled retroactively.

Item 601 of Regulation S-K requires an exhibit to the principal filing forms (Forms S-1, S-2, S-4, S-11, 10, 10-Q, and 10-K) as follows: A statement setting forth in reasonable detail the computation of per share earnings, unless the computation can be clearly determined from the material in the registration statement or report. Since FAS No. 128 expressly requires disclosure of the number of shares used in computing EPS and the computation itself, many SEC registrants that filed the computational exhibit will no longer need to file them. In addition, SAB No. 40 requires explanatory disclosure of material changes in EPS amounts that are due principally to changes in the number of shares outstanding rather than to changes in net income. For example, disclosure is required if EPS increases materially as a result of the purchase of treasury shares by the issuer, even though aggregate earnings may remain relatively unchanged. Such disclosure would be made in "Management's Discussion and Analysis of the Summary of Earnings," which SEC registrants are required to present.

Where an IPO is occurring and stock, options, warrants, and other potentially dilutive securities have been granted or issued during the one year prior to the IPO and the exercise or issuance price is less than the public offering price, the SEC, in SAB No. 64, "Applicability of Guidance in Staff Accounting Bulletins; Reporting Income or Loss Applicable to Common Stock; Accounting for Redeemable Preferred Stock; Issuances of Shares Prior to an Initial Public Offering," issued in 1986, stated that all EPS calculations should be made assuming use of the treasury stock method as if these securities had been outstanding for all periods. The SEC, in SAB No. 83, "Earnings per Share Computations in an Initial Public Offering," added that the inclusion of potentially dilutive securities in an IPO (as required by SAB No. 64) does not change the registrant's responsibility under GAAP to determine if compensation expense should be recorded.

Accounting Principles Board, "Reporting the Results of Operations," APB Opinion No. 9. AICPA, New York, 1966.

———, "Omnibus Opinion," APB Opinion No. 12. AICPA, New York, 1967.

———, "Business Combinations," APB Opinion No. 16. AICPA, New York, 1970.

———, "Accounting Changes," APB Opinion No. 20. AICPA, New York, 1971.

———, "Reporting the Results of Operations—Reporting the Effects of Disposal of a Segment of a Business, and Extraordinary, Unusual and Infrequently Occurring Events and Transactions," APB Opinion No. 30. AICPA, New York, 1973. American Institute of Certified Public Accountants, "Statement of Position 93-6, "Employers' Accounting for Employee Stock Ownership Plans." AICPA, New York, 1993.

———, "Accounting Trends and Techniques." AICPA. New York, 1994.

———, Financial Accounting Standards Board, "Discontinued Operations with Expected Gain and Interim Operating Loss, EITF Issue No. 85-36. FASB, Stamford, CT, 1985.

———, "Display of Business Restructuring Provisions in the Income Statement, EITF Issue No. 86-22. FASB, Stamford, CT, 1986.

———, "Restructuring of Operations: Implications of SEC Staff Accounting Bulletin No. 67," EITF Issue No. 87-4. FASB, Stamford, CT, 1987.

———, "Accounting for Discontinued Operations Subsequently Retained," EITF No. 90-16. FASB, Norwalk, CT, March 19, 1991.

———, "Convertible Bonds with Issuer Option to Settle for Cash upon Conversion," EITF Issue No. 90-19, FASB, Norwalk, CT, July 11, 1991.

———, "Liability Recognition for Certain Employee Termination Benefits and Other Costs to Exit an Activity Including Certain Costs Incurred in a Restructuring," EITF Issue No. 94-3. FASB, Norwalk, CT, September 22, 1994.

———, "Allocation of Interest to Discontinued Operations," EITF Issue No. 87-24. FASB Stamford, CT, 1987.

———, "Reporting Gains and Losses from Extinguishment of Debt," Statement of Financial Accounting Standards No. 4. FASB, Stamford, CT, 1975.

———, "Financial Reporting for Segments of a Business Enterprise," Statement of Financial Accounting Standards No. 14. FASB, Stamford, CT, 1976.

———, "Accounting by Debtors and Creditors for Troubled Debt Restructuring," Statement of Financial Accounting Standards No. 15. FASB, Stamford, CT, 1977.

———, "Prior Period Adjustments," Statement of Financial Accounting Standards No. 16. FASB, Stamford, CT, 1977.

———, "Regulated Enterprises—Accounting for Abandonments and Disallowances of Plant Costs," Statement of Financial Accounting Standards No. 90. FASB, Stamford, CT, 1986.

———, "Consolidation of All Majority-Owned Subsidiaries," Statement of Financial Accounting Standards No. 94. FASB, Stamford, CT, 1987.

———, "Accounting for the Impairment of Long-Lived Assets and for Long-Lived Assets to be Disposed of," Statement of Financial Accounting Standards No. 121. FASB, Norwalk, CT, 1995.

———, "Earnings per Share," Statement of Financial Accounting Standards No. 128. FASB, Norwalk, CT, 1997.

———, "Disclosures about Segments of an Enterprise and Related Information," Statement of Financial Accounting Standards No. 131. FASB, Norwalk, CT, 1997.

———, "Business Combinations," Statement of Financial Accounting Standards No. 141. FASB, Norwalk, CT, 2001.

———, "Accounting for a Purchase of Treasury Shares at a Price Significantly in Excess of the Current Market Price of Shares and the Income Statement Classification of Costs Incurred in Defending against a Takeover Attempt," FASB Technical Bulletin No. 85-6. FASB, Stamford, CT, 1985. Securities and Exchange Commission, "Codification of SAB Nos, 1–38," Staff Accounting Bulletin No. 40. SEC, Washington, DC, 1981.

———, "Accounting for Sales of Stock by a Subsidiary," Staff Accounting Bulletin No. 51. Washington, DC, 1983.

———, "Income Statement Presentation of Restructuring Charges," Staff Accounting Bulletin No. 67. SEC, Washington, DC, 1986.

———, "Income Statement Presentation," Staff Accounting Bulletin No. 69. SEC, Washington, DC, 1987.

———, "Classification of Charges for Abandonments and Disallowances," Staff Accounting Bulletin No. 72. SEC, Washington, DC, 1987.

———, "Gain Recognition on the Sale of a Business or Operating Assets to a Highly Leveraged Entity," Staff Accounting Bulletin No. 81. SEC, Washington, DC, 1989.

———, "Accounting for Sales of Stock by a Subsidiary," Staff Accounting Bulletin No. 84. SEC, Washington, DC, 1989.

———, "Accounting and Disclosure Regarding Discontinued Operations," Staff Accounting Bulletin No. 93. SEC, Washington, DC, 1993.

———, "Codification of Financial Reporting Polices," Financial Reporting Release No. 1, ASR No. 177. SEC, Washington, DC, 1982.