James R. Adler, CPA, CFE, PhD

Adler Consulting, Ltd.

A lease is an agreement conveying the right to use property, plant, or equipment, usually for a stated period of time. Since World War II, the leasing industry has become a major economic force, and leasing has become a method by which to finance acquisitions of property.

The rapid growth created by the demand to lease everything from equipment to automobiles, furniture, and even people has caused a highly price-competitive environment. Lessors earn their profits by buying equipment at lower prices than ordinary buyers, charging brokerage fees, and getting tax deductions for equipment write-offs. The 1986 Tax Reform Act has wiped out tax credits, removing some of the traditional cash flow advantages that lessors could gain upon initiating a leasing transaction.

Traditionally, lessees prefer to have operating leases rather than capital leases so that the future lease payment obligations do not appear on the balance sheet as a liability.

The financing advantages associated with leasing include the following:

Leasing permits 100 percent financing, whereas a normal equipment loan may require a 20 percent to 40 percent initial down payment. Leasing can thereby conserve cash and working capital.

Longer terms than are normally available with loans can be arranged for leasing many types of capital equipment.

Financing of initial acquisition costs is possible because these costs can be included in a lease. Such costs, for example, delivery charges, interest on advance payments, sales or use taxes, and installation costs, are not normally financed under other methods of equipment financing.

Leasing offers greater convenience than either debt or equity financing because of the reduced documentation.

The risk of obsolescence can be avoided by the lessee as compared with the risk he would assume on the purchase of such equipment.

Some of the financing disadvantages associated with leasing are as follows:

The effective interest rate is generally greater than if the lessee obtained a bank loan for the same term. This may not be true, however, for leveraged leases.

The lessee suffers the loss of residual rights to the property at the termination of the lease.

The lessee does not enjoy the tax benefits of accelerated depreciation and interest expense.

Exhibit 23.1 lists the technical accounting pronouncements concerning leases. These numerous pronouncements are an indication of the complexity and controversy surrounding the accounting for leases. The manufacturer or dealer is concerned with the issue of when a lease becomes a sale with the respective profit and loss recognition. Other lessors are perceived as either renting out their asset or providing financing for the acquisition of this asset by a lessee, depending on the circumstances. Likewise, the lessee either has an asset and a liability or is committed to an obligation to rent an asset. The accounting issues can then be summarized according to the following four questions:

On whose balance sheet should the leased asset appear?

What is the timing of financial statement recognition of lease events?

How are measurements made for both balance sheet and income statement effects of leases?

What disclosures should be made in the financial statements?

The Financial Accounting Standards Board (FASB) issued Statement of Financial Accounting Standards (SFAS) No. 13 in November 1976 to resolve the issues. The SFAS No. 13 superseded all preceding technical literature and established the primary current standard in accounting for leases. Under this pronouncement, when substantially all of the risks and rewards of ownership have passed from the lessor to the lessee, the leased property transfers from the lessor to the lessee. The questions of whose asset it is and the related income statement effect are answered by establishing where the substantial risks and rewards of ownership lie. Timing is at the inception of the lease, and measurement is usually at the fair value of the leased property to the lessor at that date.

The FASB regularly releases a codification of the authoritative pronouncements issued on lease accounting. The last codification was in 1998. Essentially, the codification is a reproduction of the lease accounting section included in the FASB Current Text. All of the FASB Statements, Interpretations, and Technical Bulletins were utilized and integrated into this publication. However, the discussion of issues by the Emerging Issues Task Force (EITF) concerning lease accounting were not included in the codification. When a consensus is reached by the Task Force, the agreement represents current thoughts where no lease accounting standards exist. Additional decisions and issues will be considered by the Task Force in the future, and any such consensus previously reached is subject to change. A summary of the proceedings of the Task Force on each lease accounting issue is published by the FASB in the EITF Abstracts.

From the standpoint of the lessee, a lease may be classified as either a capital lease or an operating lease. If the lease meets any one of the following four criteria, then the lessee should classify and account for the arrangement as a capital lease:

The lease transfers ownership of the property to the lessee at the end of the lease term.

The lease contains a bargain purchase option.

The lease term is equal to at least 75 percent of the estimated economic life of the property. (If the beginning of the lease term falls within the last 25 percent of the total estimated life including earlier use, this criterion should not be used.)

The present value of the minimum lease payments at the beginning of the lease term, excluding that portion of the payments representing executory costs, is 90 percent or more of the fair value of the leased property to the lessor at the inception date, less any related investment tax credit retained by and expected to be realized by the lessor. The discount rate that the lessee used in computing the present value of the lease payments is the lessee's incremental borrowing rate, defined in SFAS No. 13 as "The rate that, at the inception of the lease, the lessee would have incurred to borrow the funds necessary to buy the leased asset on a secured loan with repayment terms similar to the payment schedule called for in the lease." However, if the lessee knows the implicit rate used by the lessor and that rate is less than the lessee's borrowing rate, SFAS No. 13 requires use of the implicit rate. (If the beginning of the lease term falls within the last 25 percent of the total estimated life including earlier use, this criterion should not be used.)

Leases that do not meet any of these criteria are classified as operating leases by the lessee.

SFAS No. 13 specifies the following classifications of leases for lessors:

Direct financing

Sales type

Operating

Leveraged

A lease is classified as a direct financing lease if it meets any one of the four lease classification criteria and, in addition, meets both of the following criteria:

Collectibility of the minimum lease payments is reasonably predictable.

No important uncertainties surround the amount of unreimbursable costs yet to be incurred by the lessor under the lease.

A lease is classified as a sales-type lease if it qualifies as a direct financing lease and, in addition, has a fair market value in excess of the property's carrying value. Sales-type leases are generally associated with dealers and manufacturing lessors. Leases that do not meet these criteria are classified as operating leases. Leveraged leases are covered in Subsection 23.8(a).

The following 28 technical terms have been defined in accounting pronouncements on leases:

Bargain Purchase Option. A provision allowing the lessee, at the lessee's option, to purchase the leased property for a price that is sufficiently lower than the expected fair value of the property at the date the option becomes exercisable so that exercise of the option appears, at the inception of the lease, to be reasonably assured.

Bargain Renewal Option. A provision allowing the lessee, at the lessee's option, to renew the lease for a rental sufficiently lower than the fair rental of the property at the date the option becomes exercisable so that exercise of the option appears, at the inception of the lease, to be reasonably assured.

Capital Lease. A lease that must be capitalized by a lessee because it meets one of the four SFAS No. 13 lease classification criteria.

Contingent Rentals. The increases or decreases in lease payments that result from changes occurring subsequent to the inception of the lease in the factors (other than the passage of time) on which lease payments are based, except as provided in the following sentence. Any escalation of minimum lease payments relating to increases in construction or acquisition cost of the leased property or for increases in some measure of cost or value during the construction or preconstruction period shall be excluded from contingent rentals. Lease payments that depend on a factor directly related to the future use of the leased property, such as machine hours of use or sales volume during the lease term, are contingent rentals and, accordingly, are excluded from minimum lease payments in their entirety.

However, lease payments that depend on an existing index or rate, such as the consumer price index or the prime interest rate, shall be included in minimum lease payments based on the index or rate existing at the inception of the lease; any increases or decreases in lease payments that result from subsequent changes in the index or rate are contingent rentals and thus affect the determination of income as accruable.

Direct Financing Leases. A lease that meets any one of the four SFAS No. 13 lease classification criteria for a lessor plus two additional criteria:

Collectibility of minimum lease payments must be reasonably predictable.

No uncertainties may surround the amount of unreimbursable costs to be incurred by the lessor under the lease.

Estimated Economic Life of Leased Property. The estimated remaining period during which the property is expected to be economically usable by one or more users, with normal repairs and maintenance, for the purpose for which it was intended at the inception of the lease, without limitation by the lease term.

Estimated Residual Value of Leased Property. The estimated fair value of the leased property at the end of the lease term.

Executory Costs. Those costs such as insurance, maintenance, and taxes incurred for leased property, whether paid by the lessor or lessee. Amounts paid by a lessee in consideration for a guarantee from an unrelated third party of the residual value are also executory costs. If executory costs are paid by a lessor, any lessor's profit on those costs is considered the same as executory costs.

Fair Value of the Leased Property. The price for which the property could be sold in an arm's-length transaction between unrelated parties. The following are examples of the determination of fair value:

When the lessor is a manufacturer or dealer, the fair value of the property at the inception of the lease will ordinarily be its normal selling price, reflecting any volume or trade discounts that may be applicable. However, the determination of fair value shall be made in light of market conditions prevailing at the time, which may indicate that the fair value of the property is less than the normal selling price and, in some instances, less than the cost of the property.

When the lessor is not a manufacturer or dealer, the fair value of the property at the inception of the lease will ordinarily be its cost, reflecting any volume or trade discounts that may be applicable. However, when there has been a significant lapse of time between the acquisition of the property by the lessor and the inception of the lease, the determination of fair value shall be made in light of market conditions prevailing at the inception of the lease, which may indicate that the fair value of the property is greater or less than its cost or carrying amount, if different.

Finance Lease. A financing device by which a user can acquire use of an asset for most of its useful life. Rentals are net to the lessor, and the user is responsible for maintenance, taxes, and insurance. Rent payments over the life of the lease are sufficient to enable the lessor to recover the cost of the equipment plus interest on its investment.

Inception of the Lease. The date of the lease agreement or commitment, if earlier. For purposes of this definition, a commitment shall be in writing, signed by the parties in interest to the transaction, and shall specifically set forth the principal provisions of the transaction. If any of the principal provisions is yet to be negotiated, such a preliminary agreement or commitment does not qualify for purposes of this definition.

Initial Direct Costs. Only those costs incurred by the lessor that are (a) costs to originate a lease incurred in transactions with independent third parties resulting directly from and essential to acquiring that lease and which would not have been incurred had that leasing transaction not occurred, and (b) certain costs directly related to specified activities performed by the lessor for that lease. Those activities include evaluating the prospective lessee's financial condition; evaluating and recording guarantees, collateral, and other security arrangements; negotiating lease terms; preparing and processing lease documents; and closing the transaction. The costs directly related to those activities include only that portion of the employees' total compensation and payroll-related fringe benefits directly related to time spent performing those activities for that lease and other costs related to those activities that would not have been incurred but for that lease. Initial direct costs do not include costs related to activities performed by the lessor for advertising, soliciting potential lessees, servicing existing leases, and other ancillary activities related to establishing and monitoring credit policies, supervision, and administration. They also do not include administrative costs, rent, depreciation, any other occupancy and equipment costs and employees' compensation and fringe benefits related to ancillary activities, unsuccessful origination efforts, and idle time.

Interest Rate Implicit in the Lease. The discount rate that, when applied to (a) the minimum lease payments, excluding that portion of the payments representing executory costs to be paid by the lessor, together with any profit thereon, and (b) the unguaranteed residual value accruing to the benefit of the lessor causes the aggregate present value at the beginning of the lease term to be equal to the fair value of the leased property to the lessor at the inception of the lease, minus any investment tax credit retained by the lessor at the inception of the lease and minus any investment tax credit retained by the lessor and expected to be realized by him. (This definition does not necessarily purport to include all factors that a lessor might recognize in determining his rate of return.)

Lease. An agreement conveying the right to use property, plant, or equipment (land or depreciable assets or both) usually for a stated period of time.

Lease Term. The fixed noncancelable term of the lease plus:

All periods, if any, covered by bargain renewal options.

All periods, if any, for which failure to renew the lease imposes a penalty on the lessee in such amount that a renewal appears, at the inception of the lease, to be reasonably assured.

All periods, if any, covered by ordinary renewal options during which a guarantee by the lessee of the lessor's debt directly or indirectly related to the leased property is expected to be in effect or a loan from the lessee to the lessor directly or indirectly related to the leased property is expected to be outstanding.

All periods, if any, covered by ordinary renewal options preceding the date as of which a bargain purchase option is exercisable.

All periods, if any, representing renewals or extensions of the lease at the lessor's option. However, in no case shall the lease term be assumed to extend beyond the date a bargain purchase option becomes exercisable. A lease that is cancelable only upon the occurrence of some remote contingency, only with the permission of the lessor, only if the lessee enters into a new lease with the same lessor, or only if the lessee incurs a penalty in such amount that continuation of the lease appears, at inception, reasonably assured shall be considered "noncancelable" for purposes of this definition.

Lessee's Incremental Borrowing Rate. The rate that, at the inception of the lease, the lessee would have incurred to borrow over a similar term the funds necessary to purchase the leased asset.

Leveraged Lease. A lease that meets the definition as a direct financing lease for a lessor and, in addition, has all the following characteristics:

At least three partners are involved: a lessee, a lessor, and a long-term lender.

The financing provided by the lender is substantial to the transaction and without recourse to the lessor.

The lessor's net investment declines during the early years of the lease and rises during the latter years of the lease.

Minimum Lease Payments.

From the standpoint of the lessee: The payments that the lessee is obligated to make or can be required to make in connection with the leased property. Contingent rentals are excluded from minimum lease payments. However, a guarantee by the lessee of the lessor's debt and the lessee's obligation to pay (apart from the rental payments) executory costs in connection with the leased property shall be excluded. If the lease contains a bargain purchase option, only the minimum rental payments over the lease term and the payment called for by the bargain purchase option shall be included in the minimum lease payments. Otherwise, minimum lease payments include the following:

The minimum rental payments called for in the lease over the lease term.

Any guarantee by the lessee or any party related to the lessee of the residual value at the expiration of the lease term, whether or not payment of the guarantee constitutes a purchase of the leased property. When the lessor has the right to require the lessee to purchase the property at termination of the lease for a certain or determinable amount, that amount shall be considered a lessee guarantee. When the lessee agrees to make up any deficiency below a stated amount in the lessor's realization of the residual value, the guarantee to be included in the minimum lease payments is the stated amount, rather than an estimate of the deficiency to be made up.

Any payment that the lessee must make or can be required to make upon failure to renew or extend the lease at the expiration of the lease term, whether or not the payment would constitute a purchase of the lease property. In this connection, it should be noted that the definition of lease term includes "all periods, if any, for which failure to renew the lease imposes a penalty on the lessee in an amount such that renewal appears, at the inception of the lease, to be reasonably assured." If the lease term has been extended because of that provision, the related penalty is not included in minimum lease payments.

From the standpoint of the lessor: The payments described above plus any guarantee of the residual value or of rental payments beyond the lease term by a third party unrelated to either the lessee or the lessor, provided the third party is financially capable of discharging the obligations that may arise from the guarantee.

Net Lease. In a net lease, executory costs in connection with the use of the equipment are to be paid by the lessee and are not a part of the rental. For example, taxes, insurance, and maintenance are paid directly by the lessee. Most finance leases are net leases.

Nonrecourse Financing. Lending or borrowing activities in which the creditor does not have general recourse to the debtor but rather has recourse only to the property used for collateral in the transaction or other specific property.

Operating Lease. A lease that does not meet any of the lease classification criteria of a capital lease (lessee) or direct financing lease (lessor). Also describes a short-term rental agreement by which a user can acquire use of an asset for a fraction of the useful life of that asset.

Penalty. Any requirement that is imposed or can be imposed on the lessee by the lease agreement or by factors outside the lease agreement to disburse cash, incur or assume a liability, perform services, surrender or transfer an asset or rights to an asset or otherwise forgo an economic benefit, or suffer an economic detriment. Factors to consider when determining if an economic detriment may be incurred include, but are not limited to, the uniqueness of purpose or location of the property, the availability of a comparable replacement property, the relative importance or significance of the property to the continuation of the lessee's line of business or service to its customers, the existence of leasehold improvements or other assets whose value would be impaired by the lessee vacating or discontinuing use of the leased property, adverse tax consequences, and the ability or willingness of the lessee to bear the cost associated with relocation or replacement of the leased property at market rental rates or to tolerate other parties using the leased property.

Related Parties. A parent company and its subsidiaries, an owner enterprise and its joint ventures (corporate or otherwise) and partnerships, and an investor (including a natural person) and its investees, provided that the parent company, owner enterprise, or investor has the ability to exercise significant influence over operating and financial policies of the related party. In addition to the foregoing examples of significant influence, significant influence may be exercised through guarantees of indebtedness, extensions of credit, or through ownership of warrants, debt obligations, or other securities. If two or more enterprises are subject to the significant influence of a parent company, owner enterprise, investor (including a natural person), or common officers or directors, those enterprises shall be considered related parties with respect to each other.

Renewal or Extension of a Lease. The continuation of a lease agreement beyond the original lease term including a new lease under which the lessee continues to use the same property.

Sale-Leaseback Accounting. A method of accounting for a sale-leaseback transaction in which the seller-lessee records the sale, removes all property and related liabilities from its balance sheet, recognizes gain or loss from the sale, and classifies the leaseback as a financing or operating lease as appropriate.

Sales Recognition. Any method to record a transaction involving real estate, other than the deposit method, or the methods to record transactions accounted for as financing, leasing, or profit-sharing arrangements. Profit recognition methods commonly used to record transactions involving real estate include, but are not limited to, the full accrual method, the installment method, the cost recovery method, and the reduced profit method.

Sales-Type Lease. A direct financing lease that also contains a dealer or manufacturer's profit; the fair market value of the property at lease inception exceeds the related carrying value.

Unguaranteed Residual Value. The estimated residual value of the leased property exclusive of any portion guaranteed by the lessee or by a third party unrelated to the lessor.

Normally, rental on an operating lease is charged to expense over the lease term as it becomes payable. If rental payments are not made on a straight-line basis, rental expense nevertheless is recognized on a straight-line basis unless another systematic and rational basis is more representative of the time pattern in which use benefit is derived from the leased property, in which case that basis would be used (see Section 23.9).

The following three items of information with respect to operating leases must be disclosed in the lessee's financial statements or the notes thereto:

For operating leases having initial or remaining noncancelable lease terms in excess of one year:

Future minimum rental payments required as of the date of the latest balance sheet presented, in the aggregate and for each of the five succeeding fiscal years.

The total of minimum rentals to be received in the future under noncancelable subleases as of the date of the latest balance sheet presented.

For all operating leases, rental expense for each period for which an income statement is presented, with separate amounts for minimum rentals, contingent rentals, and sublease rentals. Rental payments under leases with terms of a month or less that were not renewed need not be included.

For all operating leases, a general description of the lessee's leasing arrangements including, but not limited to, the following:

The basis on which contingent rental payments are determined

The existence and terms of renewal or purchase options and escalation clauses

Restrictions imposed by lease agreements, such as those concerning dividends, additional debt, and further leasing

Operating leases are accounted for by the lessor as follows:

Leased property is included with or displayed near other property, plant, and equipment in the balance sheet.

Depreciation is recorded following the lessor's normal depreciation policy for like assets, and accumulated depreciation is displayed as a reduction of the leased property.

Rent is recorded as income over the lease terms as it becomes receivable under the provisions of the lease. However, if the rentals vary from the straight-line basis, the income is recognized on a straight-line basis unless another systematic and rational basis is more representative of the time pattern in which the benefit from the leased property is diminished, in which case that basis is used.

Initial direct costs are deferred and allocated over the lease term in proportion to revenue recognition under the lease. However, these costs may be expensed when incurred if the effect is not materially different from that which would have resulted from the use of the method prescribed above.

The Williams Company leases property with a cost and fair value of $5,000 and a life of 10 years to the Scotts Company for 4 years with a rental of $2,000 per year for years 1 and 2 and $1,000 per year for years 3 and 4.

This example assumes that some other time pattern other than straight-line is not of benefit to the lessee and dimunition of benefit to the lessor does not exist. For simplicity, the straight-line depreciation method was used although other methods could be selected by the lessor.

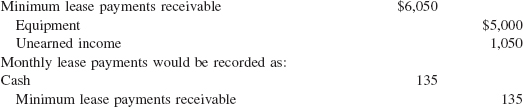

For capital leases, the lease transaction is viewed as a form of financing in which an asset is acquired and a liability is incurred. The lessee records a capital lease as an asset and a liability on the balance sheet. The amount recorded on the balance sheet is the present value of the minimum lease payments. Executory costs such as insurance, maintenance, and taxes to be paid by the lessor are excluded from the minimum payments. However, the amount recorded as an asset and liability must not exceed the fair value of the leased property.

The lessee will record depreciation expense and interest expense on capitalized leases. A capitalized asset should be depreciated by the lessee in a manner consistent with the lessee's normal depreciation policy. The depreciation period to be used is the lease term, unless there is a bargain purchase or transfer of ownership at the end of the lease term, in which case the depreciation is over the life of the assets, as if owned.

Interest expense is recognized by the lessee in proportion to the remaining balance of the capitalized lease obligation. This is accomplished by allocating each minimum lease payment between interest expense and reduction of lease obligation so as to produce a constant periodic rate of interest on the remaining lease obligation. This method is called the effective interest method.

The following five areas of information on capital leases must be disclosed.

The gross amount of assets recorded under capital leases as of the date of each balance sheet presented by major classes according to nature or function. This information may be combined with the comparable information for owned assets.

Future minimum lease payments as of the date of the latest balance sheet presented, in the aggregate and for each of the five succeeding fiscal years, with separate deductions from the total for the amount representing executory costs, including any profit thereon, included in the minimum lease payments and for the amount of the imputed interest necessary to reduce the net minimum lease payments to present value.

The total of minimum sublease rentals to be received in the future under noncancelable subleases as of the date of the latest balance sheet presented.

Total contingent rentals actually incurred for each period for which an income statement is presented.

Assets recorded under capital leases and the accumulated amortization thereon shall be separately identified in the lessee's balance sheet or in notes thereto. Likewise, the related obligations shall be separately identified in the balance sheet as obligations under capital leases and shall be subject to the same considerations as other obligations in classifying them with current and noncurrent liabilities in classified balance sheets. Unless the charge to income resulting from amortization of assets recorded under capital leases is included with depreciation expense and the fact that it is so included is disclosed, the amortization charge shall be separately disclosed in the financial statements or notes thereto.

SFAS No. 13 offers an example illustrating classification and accounting for leases. Assume that lessee and lessor sign a lease with the following provisions:

The lease has a noncancelable term of 30 months, and payments of $135 are due at the beginning of each month.

The equipment costs $5,000, has a 5-year economic life, and has a residual value guaranteed by lessee of $2,000.

Lessee receives any excess of the sales price over the guaranteed amount.

Lessee pays executory costs.

Lessee's incremental borrowing rate is 10.5 percent.

The interest rate implicit in the lease is unknown to the lessee because the lessor's unguaranteed residual value assumption is unknown to the lessee.

Lessee depreciates similar equipment on a straight-line basis.

No investment tax credit is available.

Minimum lease payments for both lessee and lessor are calculated as follows:

Payments $135 × 30 months | $4,050 |

Residual value guarantee | 2,000 |

Total minimum lease payments | $6,050 |

The lease is classified by reviewing the four lease capitalization criteria presented in Section 23.3.

Not Met. The lease does not transfer ownership.

Not Met. The lease does not contain a bargain purchase option.

Not Met. The lease is not for a term equal to or greater than 75 percent of the economic life of the property.

Met. For the lessee, the present value of the minimum lease payments using the lessee's incremental borrowing rate exceeds 90 percent of the fair value of the property at the inception of the lease (calculations below). Even if the lessee knows the implicit rate, he uses his incremental borrowing rate because it is lower. Therefore lessee classifies the lease as a capital lease.

Present values using the lessee's incremental borrowing rate of 10.5 percent are as follows:

Present value: | |

Rental payments (present value of $135 at 0.875 percent per month for 29 months) | $3,580 |

Residual guarantee (present value of $2,000 in 30 months at 0.875 percent per month) | 1,540 |

Total | $5,120 |

Although the lessee's incremental borrowing rate produces a present value of $5,120 for lease classification criteria, SFAS No. 13 stipulates that the lease is not to be capitalized in excess of fair value, or $5,000 in this example. When the present value is adjusted to total $5,000, the interest rate raises to 12.036 percent or 1.003 percent per month as follows:

Present value: | |

Rental payments (present value of $135 at 1.003 percent per month for 29 months) | $3,517 |

Residual guarantee (present value of $2,000 in 30 months at 1.003 percent per month) | $1,483 |

Total | $5,000 |

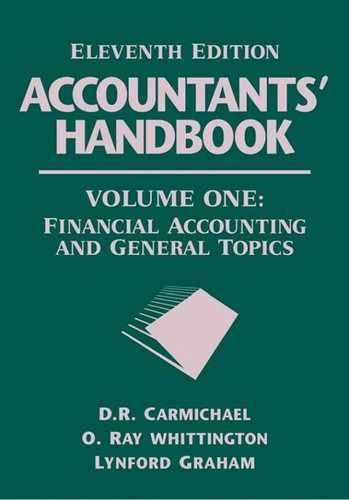

At the beginning of the lease, the lessee's journal entries are:

Depreciation would be taken on a straight-line basis over 30 months.

Total depreciation to be taken equals the capitalized lease value of $5,000, less its estimated residual value of $2,000. Each month's depreciation would be recorded as follows:

Each lease payment contains both interest and principal, and SFAS No. 13 requires that interest be calculated on the effective interest method, as follows:

Payment Number | Lease Payment | Interest (1.003%) on Principal | Reduction of Principal | Net Lease Obligation |

|---|---|---|---|---|

1 | $135 | 0 | 0 | $4,865 |

2 | 135 | $49 | $86 | 4,779 |

3 | 135 | 48 | 87 | 4,692 |

4 | 135 | 47 | 88 | 4,604 |

5 | 135 | 46 | 89 | 4,515 |

In a direct financing lease, a lessor accounts for the investment in the lease as a receivable. A direct financing lease is accounted for by recording the following:

Gross investment. The minimum lease payments (excluding executory costs paid by the lessor) plus any unguaranteed residual value accruing to the lessor are recorded as the gross investment in finance leases.

Unearned income. The difference between the gross investment and the cost or carrying amount of the leased property is recorded as unearned income. This unearned income, reduced by an amount equal to initial direct costs, is amortized to income over the lease term, applying the effective interest method to produce a constant rate of return on the net investment in the lease.

Net investment. The net investment consists of the gross investment less the unearned income.

Initial direct costs. These costs are expensed as incurred.

Earned income. Earned income consist of two elements: (1) An amount equal to initial direct costs, which is recorded at the inception of the lease; and (2) the remaining unearned income, which is amortized to income over the lease term using the effective interest method.

Assume that a lessor executes the same lease described earlier. In addition, for simplicity, assume that there were no initial direct costs. This lease does not meet the first three criteria for a direct finance lease, but it does meet the 90 percent of fair value test. Having met this test and assuming that the collectibility and uncertainty tests are also met, the lessor will classify this lease as a direct financing lease. The interest rate implicit in this lease is the internal rate of return that discounts the minimum lease payments ($135 × 30 plus $2,000 residual value) to the fair value of the property at the inception of the lease ($5,000). That rate is 12.036 percent or 1.003 percent per month.

In this case, the rate is shown by adding the present values of the components of return:

Present value of 29 payments of $135 at 1.003 percent per month | $3,382 |

Plus $135 for first payment | $0,135 |

Equals present value of rental payments | $3,517 |

Plus present value of $2,000 in 30 months at 1.003 percent per month | 1,483 |

$5,000 |

The lessor uses this rate to calculate the present value of the minimum lease payments in the 90 percent of fair value test, as follows:

Present value: | |

Rental payments | $3,517 |

Residual guarantee | $1,483 |

Total | $5,000 |

Fair value of property at inception of lease | $5,000 |

Present value of minimum lease payments as percentage of fair value | 100 percent |

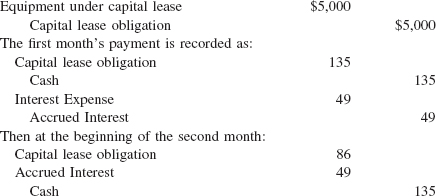

In all direct financing leases where an unguaranteed residual value is recorded, the fair value of property will exceed the present value of minimum lease payments. This is because the unguaranteed residual value is excluded from the lessor's present value calculation. The lessor must produce the following information to record the lease:

Gross investment is $6,050. Payments of $135 × 30 plus $2,000 guaranteed residual value.

Unearned income is $1,050. Gross investment less $5,000 cost of equipment.

Net investment is $5,000. The gross investment less the unearned income.

The entries for the lessor at the inception of the lease are:

Earned income (excluding any applicable income to cover initial direct costs) for the first month would be recorded as:

A similar pattern is followed for the remainder of the lease term.

The following table summarizes the income recognition and net investment of the lessor over the term of the lease.

Payment Number | Payment | Interest Income on Net Investment | Principal Reduction | Net Investment Beginning of Month |

|---|---|---|---|---|

1 | $ 135 | $ 0 | $ 35 | $4,865 |

2 | 135 | 49 | 86 | 4,779 |

3 | 135 | 48 | 87 | 4,692 |

4 | 135 | 47 | 88 | 4,604 |

— | — | — | — | — |

— | — | — | — | — |

— | — | — | — | — |

30 | 135 | 21 | 114 | 1,980 |

0 | $20 | $(20) | $2,000 | |

$4,050 | $1,050 | $3,000 |

The major difference between a direct financing lease and a sales-type lease is the presence of a manufacturer's profit in a sales-type lease; for example, the fair market value of the property is greater than the carrying value of such property.

A sales-type lease is accounted for by recording the following four items:

Gross investment. The minimum lease payments (excluding executory costs paid by the lessor) plus any unguaranteed residual value accruing to the lessor are recorded as the gross investment in finance leases.

Unearned income. The difference between the gross investment and the cost or carrying amount of the leased property is recorded as unearned income. This unearned income is amortized to income over the lease term, applying the effective interest method to produce a constant rate of return on the net investment in the lease.

Net investment. The net investment consists of the minimum lease gross investment less the unearned income.

Cost of goods sold or cost of sales. The cost or carrying amount of the lease property less the present value of any unguaranteed residual value accruing to the benefit of the lessor.

In the case presented in Section 23.6, assume that the lessor produces the equipment for a cost of $4,000. The information needed to record the salestype lease consists of these four items:

Gross investment is $6,050 ($4,050 of lease payments plus $2,000 of guaranteed residual value).

Unearned interest income is $1,050 (gross investment of $6,050 less $5,000).

Sales price is $5,000 (present value of minimum lease payments).

Cost of goods sold is $4,000 less the present value of any unguaranteed residual value accruing to the benefit of the lessor. Because there is no unguaranteed residual value, the cost of goods sold equals the lessor's cost to produce the equipment under lease.

The transaction is recorded by the lessor as follows:

Lease payments receivable | $6,050 |

Cost of goods | 4,000 |

Sales revenue | 5,000 |

Equipment | 4,000 |

Unearned income | 1,050 |

Thereafter, the accounting for lessors would follow the example of the direct financing lease.

SFAS No. 135 requires the sale or assignment of a lease or of property subject to a lease that was accounted for as a sales-type lease or a direct financing lease not to negate the original accounting treatment for the lease. A transfer of minimum lease payments or guaranteed residual values subject to a sales-type lease or direct financing lease is required to be accounted in conformity with SFAS No. 140. (See Chapter 19.) Transfers of unguaranteed residual values are not subject to SFAS No. 140.

Leveraged leases derive their name from a characteristic of the transaction, namely that the lessor tends to have a small equity in the leased property and borrows or otherwise finances a large part of the cost of owning the asset. Frequently the lessor's equity is reduced by an immediate return from investment tax credits related to the leased property, which offsets income taxes otherwise payable by the lessor. The lessor (equity participant) is frequently a financial institution able to finance the leverage at a relatively low cost. This combination, together with the security of a high-quality lessee (or lease), tends to produce a comparatively low usage cost of the asset to the lessee.

The lessor's investment in a finance lease may be zero or even negative at certain times during the lease period. The concept of recognizing a profit during a period of negative investment caused some theoretical problems in determining the proper accounting for leveraged leases.

The SFAS No. 13 defines a leveraged lease to be one having all of the following four characteristics:

It meets the definition of a direct financing lease.

It involves at least three parties: a lessee, a long-term creditor, and a lessor (commonly called the equity participant).

The financing provided by the long-term creditor is nonrecourse as to the general credit of the lessor (although the creditor may have recourse to the specific property leased and the unremitted rentals relating to it), and the amount of the financing is sufficient to provide the lessor with substantial "leverage" in the transaction.

The lessor's net investment declines during the early years once the investment has been completed and rises during the later years of the lease before its final elimination. Provided the lease meets these requirements and the investment tax credit, if any, is not accounted for using the flow-through method, the lease is treated as a leveraged lease.

From the viewpoint of the lessee, leveraged leases are classified and accounted for in the same manner as nonleveraged leases.

The lessor records the investment in a leveraged lease net of the nonrecourse debt. The net balance of the following four accounts represents the initial and continuing investment in leveraged leases:

Rentals receivable, net of that portion of the rental applicable to principal and interest on the nonrecourse debt

A receivable for the amount of the investment tax credit to be realized on the transaction

The estimated residual value of the leased asset

Unearned income (the remaining amount of estimated pretax lease income or loss and investment tax credit to be allocated to income over the lease term, after deducting initial direct costs)

The lessor in a leveraged lease transaction recognizes income by use of the investment with separate phases method. Under this method, lease income is recognized at a level aftertax rate of return on net investment in those years in which the net investment at the beginning of the period is positive. Deferred taxes should be used to calculate the net investment for use in computing income from the lease. However, deferred taxes should not be offset against the investment in the lease for balance sheet presentation. Usually, the lessor's net investment in a leveraged lease is as follows:

Early period. Positive, due to the initial investment in leased property.

Middle period. Negative, due to income tax reductions provided by accelerated depreciation, interest on nonrecourse debt, and investment tax credits, the cash flows are shielded from payment of taxes. In this period, the lessor has not only recovered his initial investment but has received additional funds, which are temporarily invested in other operations.

Later period. Positive, due to a transfer from a tax shelter position to a tax-paying position arising primarily from reduced depreciation and interest charges.

Final period. Zero, when the residual value is realized on sale of the property.

The investment with separate phases method identifies two separate and distinct types of earnings: primary earnings and earnings from reinvestment. Primary earnings consist of three elements: pretax lease income, tax effect of pretax lease income, and investment tax credit. The income that is recognized at a level rate of return in the years in which the net investment is positive consists only of the primary earnings from the lease.

In the middle years of a leveraged lease, the net investment is typically negative. The lessor has recovered his initial investment and has the further use of cash that is shielded from tax by high depreciation and interest expense charges. The earnings from the reinvestment of excess funds are taken into income during the years when the net investment is negative and are independent of the reporting of the leveraged lease income. The result is that lease income is recognized at a level rate of return on the net investment (cost of property less nonrecourse debt and less the investment tax credit) in the years in which the net investment is positive at the beginning of the year. During the years when the net investment is negative, only the earnings from the reinvested funds are realized.

When leasing activities, exclusive of leveraged leasing, are a significant part of the lessor's business activities in terms of revenue, net income, or assets, the following three items of information with respect to leases should be disclosed in the financial statements or notes:

For sales-type and direct financing leases:

The components of the net investment in sales-type and direct financing leases as of the date of each balance sheet presented:

Future minimum lease payments to be received, with separate deductions for amounts representing executory costs, including any profit thereon, included in the minimum lease payments and the accumulated allowance for uncollectible minimum lease payments receivable.

The unguaranteed residual values accruing to the benefit of the lessor.

For direct financing leases only, initial direct costs.

Unearned income.

Future minimum lease payments to be received for each of the five succeeding fiscal years as of the date of the latest balance sheet presented.

Total contingent rentals included in income for each period for which an income statement is presented.

For operating leases:

The cost and carrying amount, if different, of property on lease or held for leasing by major classes of property according to nature or function, and the amount of accumulated depreciation in total as of the date of the latest balance sheet presented.

Minimum future rentals on noncancelable leases as of the date of the latest balance sheet presented, in the aggregate and for each of the five succeeding fiscal years.

Total contingent rentals included in income for each period for which an income statement is presented.

A general description of the lessor's leasing arrangements.

Leases involving real estate can be categorized in one of the following four ways:

Land only leases

Land and building leases

Real estate and equipment leases

Leases involving part of a building

The same criteria are used to determine classification as an operating or capital lease.

If land is the only item of property leased and the lease transfers ownership of the property or contains a bargain purchase option, the lessee should account for the lease as a capital lease; because ownership of the land is expected to pass to the lessee, the asset recorded under the lease is not normally amortizable. If the lease does not meet either of those criteria, the lease is an operating lease.

If the lease transfers ownership and meets the requirements of collectibility and uncertainty, the lessor accounts for the lease as either a sales-type or a direct financing lease, whichever is appropriate. If the lease does not meet those requirements, it is an operating lease. The lessor does not use the bargain purchase option criterion to classify the lease.

When the lease either transfers ownership or contains a bargain purchase option, there are two forms of accounting:

Lessee's accounting. If the lease transfers ownership or contains a bargain purchase option, the land and the buildings are separately capitalized by the lessee. The present value of the minimum lease payments is apportioned between land and buildings in relation to their fair values at the inception of the lease. The building should be amortized under the normal accounting policies of the lessee.

Lessor's accounting. If the lease transfers ownership and meets both the collectibility and uncertainty tests, the lessor accounts for the lease as a single unit. If there is a manufacturer or dealer profit, the lease would be a sales-type lease. Without such profit, it would be a direct financing lease or leveraged lease, as appropriate. If the lease does not meet these tests, the lessor accounts for the lease as an operating lease. The lessor does not use the bargain purchase option criterion to classify the lease.

When the lease neither transfers ownership nor contains a bargain purchase option, whether the land and the building are considered together or separately depends on the relation of the fair value of the land to the total fair value of the leased property.

If the fair value of the land is less than 25 percent of the total fair value of the leased property, both the lessee and the lessor must consider the land and the building as a single unit, the economic life of the building.

If the lease term is at least 75 percent of the property's estimated economic life or if the present value of the minimum lease payments is 90 percent or more of the fair value of the property, the lessee capitalizes the land and buildings as a single unit and amortizes it. If the lease does not meet those requirements, it is accounted for as an operating lease.

If the lease term is at least 75 percent of the property's economic life or if the present value of minimum lease payments is 90 percent or more of the fair value of the property and both the collectibility and uncertainty tests are met, the lessor accounts for the lease as a single unit, a sales-type lease, a direct financing lease, or a leveraged lease. If the lease does not meet those requirements, it is accounted for as an operating lease.

If the building in the lease meets the economic life or 90 percent fair value tests, the building is accounted for as a capital lease by the lessee. The land element of the lease is separately accounted for as an operating lease. However, if the building element in the lease meets neither the economic life nor the fair value test, both the building and the land are accounted for as a single operating lease by the lessee.

If the building in the lease meets the economic life or fair value test as well as the criteria for uncertainty and collectibility, the lessor accounts for the building elements as a sales-type lease, a direct financing lease, or a leveraged lease, as appropriate. The land is accounted for as an operating lease. As with lessees, if the building does not meet the economic life or fair value tests and does not meet the tests for collectibility, both the building and the land are accounted for collectively as a single operating lease.

If a lease involves land and equipment, the portion of the minimum lease payments applicable to the equipment is estimated by whatever means is appropriate and reasonable. The equipment is then to be treated separately for purposes of applying the criteria and accounted for separately according to its classification by both lessee and lessor.

When the leased property is part of a larger entity, its cost and fair value may not be objectively determinable as, for example, if a floor in an office building was leased. If the cost and fair value of the leased property are objectively determinable, both the lessee and the lessor should classify and account for the lease as described above.

Unless both the cost and the fair value are objectively determinable, the lease is classified and accounted for in the following two ways:

Lessee. If the fair value of the leased property is not objectively determinable, the lessee shall classify the lease pursuant to whether it meets the 75 percent of economic life test.

Lessor. If either the cost or the fair value of the property is not objectively determinable, the lessor shall account for the lease as an operating lease.

The sale or assignment of a lease or property subject to a lease to a third party does not change the original accounting for the lease. Any profit or loss on the sale should be recognized at the time of the transaction, unless the transaction is between related parties or is sold with recourse (see SFAS No. 140, "Accounting for the Transfers and Servicing of Financial Assets and Extinguishments of Liabilities").

In general, related party leases are classified in accordance with the same criteria as all other leases, unless it is clear that the terms of the transaction have been significantly affected by the relationship of the lessees and lessor. The economic substance of such a transaction may cause the accounting for such leases to be modified from that which would be suggested by the strict terms of the lease.

If the original lease was classified as a capital lease because of transfer of title or a bargain purchase option, the sublease by the lessee should be treated as a new lease and classified according to the same criteria as any other lease. If the original lease was classified as a capital lease because of the economic life or 90 percent fair value tests, only the economic life test should be used to classify the sublease except where the lessee who is now becoming a lessor was really only an intermediary between the new lessee and original lessor. In that event, the 90 percent fair value test should also be used. If the original lease was an operating lease, the sublease must also be an operating lease.

From the standpoint of the lessor, three changes can take place as follows:

The change does not give rise to a new agreement. A new agreement is defined as a change that, if in effect at the inception of the lease, would have resulted in a different classification.

The change does give rise to a new agreement that would be classified as a direct financing lease.

The change gives rise to a new agreement classified as an operating lease.

If either (1) or (2) occur, the balance of the minimum lease payment receivable and the estimated residual value are adjusted to reflect the effect of the change. The net adjustment is to be charged (or credited) to the unearned income account, and the accounting for the lease adjusted to reflect the change.

If the new agreement is an operating lease, then the transaction should be accounted for under the sale-leaseback requirements.

A renewal or extension involves one of two circumstances that affect the accounting for an existing lease:

A guarantee or penalty is rendered inoperative.

A new agreement exists.

In both circumstances, the lessee in a capital lease adjusts the current balance of the leased asset and obligation to the present value of the future minimum lease payments based on the implicit interest rate in the original lease. If a new agreement exists and it is classified as an operating lease, then the lessee continues to account for the existing capital lease until the end of the term. The renewal or extension is an operating lease and is accounted for as such. In both circumstances, the lessor in a direct financing lease would adjust the lease receivable and estimated residual value charging or crediting unearned income for the difference. An upward revision to estimated residual value is prohibited, however. If a renewal or extension constitutes a new agreement and is an operating lease, then the lessor continues to account for the existing lease until the end of the term and accounts for the renewal/extension as an operating lease. If the new agreement is a sales-type lease, the renewal or extension is accounted for as a sales-type lease providing the renewal/extension occurred at or near the end of the existing lease term.

In a termination, the lessor eliminates the remaining net investment and records the leased asset at its lower of present fair value, current book value, or historical cost. The net difference is reflected in the income statement of the current period. The lessor in a capital lease will eliminate the asset and obligation from the financial statements recording a gain or loss on termination. In an operating lease, no adjustment is required.

If, in connection with a business combination, the provisions of a lease are modified such that the revised lease is essentially a new agreement, this new lease should be classified as any new lease would be.

In a pooling of interests, unless the lease has been modified as above, no changes should be made in the accounting for the leases in effect.

In a purchase, unless the terms of the lease have been changed, the previous classification would remain in effect. However, the amounts assigned to the assets and liabilities arising from the accounting for leases should be determined in accordance with the guidelines under FASB No. 141, "Business Combinations."

A lessor should at a minimum annually review the estimated residual values in any leasing transactions. For any decline in value that is deemed to be permanent, a loss should be recognized in the period of decline and the residual value should be revised. For any declines that are deemed to be temporary, no such action need be taken. No change in residual values is ever recognized for estimated increases in such values.

A sale and leaseback transaction is one involving the sale of property by the owner (seller-lessee), who simultaneously leases it back from the new owner. Sale and leaseback transactions are frequently entered into as a means of raising additional cash from assets that are owned and used by a company. For example, a company may sell a building it owns and simultaneously lease it back. The facilities of the building are still available to the company. The cash received can be invested in the company's productive process or business at a relatively high rate of return. Since real estate investors, who purchase and lease the building, frequently accept lower rates of return than are available to the company from its normal operations, overall rate of return is improved. In effect, the company transfers funds invested in real estate (or similar) assets to higher yielding, more active investments. The lease in a sale and leaseback transaction is frequently a net lease, which provides that the lessee remains liable for all executory costs, taxes, maintenance, and so on.

If the lease meets one of the criteria for treatment as a capital lease, the seller-lessee accounts for it as a capital lease. If the lease does not meet one of the criteria, then it is an operating lease. In general, any profit or loss on the sale is deferred and recognized in proportion to the amortization of the leased asset in a capital lease or to the gross rental expense in an operating lease. The three exceptions to the general rule are:

The seller-lessee relinquishes rights to substantially all of the property sold, retaining only a minor portion. Both the sale and leaseback are treated as separate transactions unless they require an adjustment due to the unreasonable amount of rentals called for by the leaseback compared to market conditions.

The seller-lessee retains more than a minor part of the property but less than substantially all. Only the profit on the sale in excess of the present value of the minimum lease payments or recorded value of the leased asset is recognized at the date of sale.

The fair value of the property is less than its net book value, in which case a loss should be immediately recognized.

If the lease meets any one of the lease classification criteria and both criteria for collectibility and uncertainty, the purchaser-lessor must record the transaction as a purchase and a direct financing lease. If the lease does not meet these criteria, the lessor records the transaction as a purchase and an operating lease.

A sale-leaseback for real estate involves any transaction that involves real estate, including real estate with equipment or furniture and fixtures, regardless of the relative value of the equipment or furniture and fixtures and the real estate. Sale-leaseback can be used by a seller-lessee only if the agreement includes all of the following:

A normal leaseback

Payment terms and provisions adequately demonstrating the buyer-lessor's initial and continuing investment in the property (see SFAS No. 66, "Accounting for Sales of Real Estate," [FASB, 1982])

Payment terms and provisions transferring all of the other risks and rewards of ownership as demonstrated by the absence of any other continuing involvement by the seller-lessee A normal leaseback involves active use of the property by the seller-lessee in exchange for the payment of rent except for minor subleasing (10 percent or less of the fair value). Terms and provisions substantially different than those that an independent lessor or lessee would normally accept are considered an exchange of unstated rights or privileges that should be considered in evaluating continuing involvement by the seller-lessee. These may include sales price or interest rate. A sale-leaseback that does not qualify for a normal leaseback because of the continuing involvement by the seller-lessee should be accounted for by the deposit method or as a financing.

Continuing involvement includes these five:

Sale-leaseback of property improvements or equipment without leasing the underlying land

Buyer-lessor shares the future appreciation of the property with the seller-lessee

Seller-lessee has an option or obligation to repurchase

Seller-lessee guarantees buyer-lessor's investment or return on investment for some period of time

Guarantee by the seller-lessee such as fair value of property at end of lease, providing nonrecourse financing, remaining as liable on obligation, and so on

Disclosures required include the terms of the sale-leaseback, the obligation for future minimum lease payments in the aggregate and for each of the five succeeding fiscal years, and the total of minimum sublease rentals in the aggregate and for each of the five succeeding fiscal years.

In recent years, numerous complexities regarding leasing transactions have required the EITF to address the accompanying accounting issues:

Issue. Certain inconsistencies have been perceived between Statement No. 13, as amended by Statement No. 28, and Statement No. 66. The four issues are:

In a sale-leaseback transaction with a short initial lease term and one or more renewal options, over what period profit should be recognized if the lease does not meet the criteria for classification as a capital lease.

In a real estate sale-leaseback transaction in which (a) the seller has an obligation to repurchase the leased property, (b) the buyer can compel the seller to repurchase the property, or (c) the seller has an option to repurchase the property, whether it is appropriate to report the transaction as a sale.

In a real estate sale-leaseback transaction in which the seller finances the purchaser's acquisition, whether the lease term includes the renewal periods exercisable during the term of the loan.

How rental shortfall agreements that would warrant accounting as an adjustment of the purchase price by the buyer-lessor (as addressed in Issue No. 85-27, "Recognition of Receipts from Made-Up Rental Shortfalls") should be distinguished from a sale-leaseback transaction (as addressed by Statement No. 13).

Issue 1: The Task Force was unable to reach a consensus on this issue. Some Task Force members stated that the period over which the gain should be amortized is dependent on the individual facts and circumstances, such as the economic consequences of not renewing the lease, the intent to renew, and the existence of viable alternatives to renewal. Others discussed the use of an arbitrary period of time in circumstances in which the lease period does not appear to be appropriate. (Note: See section Status.)

Issue 2: The Task Force was unable to reach a consensus on this issue.

Issue 3: The Task Force was unable to reach a consensus on this issue.

Issue 4: The Task Force was unable to reach a consensus on this issue.

Status. In May 1988, the FASB issued Statement No. 98, which affects the above issues as summarized next.

Issue 1: Statement No. 98 revises the definition of lease term for all leasing transactions to include all periods, if any, during which a loan from the lessee to the lessor directly or indirectly related to the leased property is expected to be outstanding. Statement No. 98 also defines the term penalty as used in the lease terms provisions of paragraph 5(f) of Statement No. 13 and thereby may cause lease terms to be longer than previously contemplated. Those modifications of the lease term provisions of Statement No. 13 apply to all leases, not just to sale-leaseback transactions involving real estate. Thus, the period over which profit would be recognized on a sale-leaseback transaction may be affected by the guidance in Statement No. 98.

Issue 2: Statement No. 98 states that sale-leaseback accounting (as defined in Statement No. 98) shall be used by a seller-lessee only if, among other criteria, the sale-leaseback transaction includes payment terms and provisions that transfer all of the risks and rewards of ownership other than the leaseback itself as demonstrated by the absence of any continuing involvement by the seller-lessee. Paragraphs 25–39 and 41–43 of Statement No. 66 describe forms of continuing involvement by the seller-lessee with the leased property that result in the seller-lessee not transferring the risks and rewards of ownership to the buyer-lessor.

Issue 3: Statement No. 98 revises the definition of lease term for all leasing transactions to include all periods, if any, during which a loan from the lessee to the lessor directly or indirectly related to the leased property is expected to be outstanding.

Issue 4: This issue is not addressed in Statement No. 98.

Issue. In a sale-leaseback transaction, the seller-lessee guarantees to the lessor that the residual value will be a stipulated amount. The seller-lessee retains more than a minor part but less than substantially all of the use of the property through the leaseback. The lease does not meet the criteria for classification as a capital lease.

The issue is how the residual value guarantee should affect the determination of profit to be deferred on the sale in accordance with Statement No. 28. If the residual value guarantee affects the determination of deferred profit, should the gross amount of the guarantee or its present value be used?

EITF Discussion. The Task Force reached a consensus that profit equal to the present value of the periodic rent plus the gross amount of the guarantee should be deferred at the date of sale. The amount of deferred profit equal to the gross guarantee should be deferred until the guarantee is resolved at the end of the lease term. The remaining deferred profit, equal to the present value of the periodic rents, should be amortized in relation to gross rent expense over the lease term. Some Task Force members believed that this accounting is appropriate because the guaranteed amount represents a contingent gain.

Status. In May 1988, the FASB issued Statement No. 98, which addresses the accounting for sale-leaseback transactions involving real estate. Statement No. 98 states that sale-leaseback accounting (as defined in Statement No. 98) shall be used by a seller-lessee only if, among other criteria, the sale-leaseback transaction includes payment terms and provisions that transfer all the risks and rewards of ownership other than the leaseback itself as demonstrated by the absence of any other continuing involvement by the seller-lessee.

Issue. An entity owns an interest in property and also is a lessee under an operating lease for all or a portion of the property. Acquisition of an ownership interest in the property and consummation of the lease occurred at or near the same time. This owner-lessee relationship can occur when the entity has an investment in a partnership that owns the leased property. The entity sells its interest or the partnership sells the property to an independent third party and the entity continues to lease the property under the pre-existing operating lease. The four issues are:

Whether the transaction should be accounted for as a sale-leaseback transaction

Whether the amount of profit deferred, if any, should be affected by the seller-lessee's prior ownership in the property

Whether Statement No. 98 should be applied to transactions involving property under the scope of that Statement if pursuant to provisions in the pre-existing lease, the seller-lessee vacates and intends to sublease the property or exercises a renewal option

Whether Statement No. 98 should be applied to transactions involving property under the scope of that Statement if the pre-existing lease is between parties under common control of the seller

EITF Discussion. The Task Force reached a consensus on the first issue that a transaction should be considered a sale-leaseback transaction if the pre-existing lease is modified in connection with the sale, except for insignificant changes. Under this consensus, transactions with modifications to the pre-existing lease involving property within the scope of Statement No. 98 should be accounted for under that Statement. The Task Force also reached a consensus on the first issue that if the preexisting lease is not modified in conjunction with the sale, except for insignificant changes, profit should be deferred and recognized in accordance with Statement No. 28. If the transaction involves real estate, Statement No. 66 must also be applied in all cases; however, Statement No. 98 is applicable only if the lease was entered into after June 30, 1988. In applying Statement No. 77 when Statement No. 98 is not applicable, all continuing involvement included in the pre-existing lease is not considered for purposes of determining if a sale should be recognized.

The Task Force reached a consensus on the second issue that, irrespective of lease modifications, the calculation of the amount of deferred profit should not be affected by the seller-lessee's prior ownership percentage in the property.

The Task Force reached a consensus on the third issue that the exercise of a renewal option for a period that was included in the original minimum lease term [as lease term is defined in paragraph 5(f) of Statement No. 13] or a sublease provision contained in the pre-existing lease, does not affect the accounting for the transaction. Under this consensus, however, exercise of a renewal option for a period that was not included in the original lease term is a new lease, and Statement No. 98 should be applied.

The Task Force reached a consensus on the fourth issue that a lease between parties under common control should not be considered a pre-existing lease for purposes of this consensus and that Statement No. 98 should be applied to transactions that include property within its scope, except when Statement No. 71 applies. That is, if one of the parties under common control is a regulated enterprise with a lease that has been approved by the appropriate regulatory agency, that lease should be considered a pre-existing lease.

The Task Force did not address the accounting when the acquisition of the ownership interest in the property and the consummation of the lease did not occur at or near the same time.

Issue. Executory costs (such as insurance, maintenance, and taxes) of property leased in a sale-leaseback transaction (1) may be paid by the buyer-lessor who expects to recover the costs through the monthly rentals established in the lease, (2) may be paid by the buyer-lessor and in turn billed to the seller-lessee as an addition to the rent, or (3) may be paid directly by the seller-lessee. The issue is how to consider executory costs in the calculation of profit to be deferred in a sale-leaseback transaction.

EITF Discussion. The Task Force reached a consensus that executory costs of the leaseback should be excluded from the calculation of profit to be deferred on a sale-leaseback transaction irrespective of who pays the executory costs or the classification of the leaseback.

Issue. A U.S. enterprise purchases a depreciable asset and enters into an arrangement with a foreign investor that provides the foreign investor with an ownership right in, but not necessarily title to, the asset. That ownership right enables the foreign investor to claim certain benefits of ownership of the asset for tax purposes in the foreign tax jurisdiction.

The U.S. enterprise also enters into an agreement in the form of a leaseback for the ownership right with the foreign investor. The lease agreement contains a purchase option for the U.S. enterprise to acquire the foreign investor's ownership right in the asset at the end of the lease term.

The foreign investor pays the U.S. enterprise an amount of cash based on an appraised value of the asset. The U.S. enterprise immediately transfers a portion of that cash to a third party, and that third party assumes the U.S. enterprise's obligation to make the future lease payments, including the purchase option payment. The cash retained by the U.S. enterprise is consideration for the tax benefits to be obtained by the foreign investor in the foreign tax jurisdiction. The U.S. enterprise may agree to indemnify the foreign investor against certain future events that would reduce the availability of tax benefits to the foreign investor. The U.S. enterprise also may agree to indemnify the third party trustee against certain future events.

The result of the transaction is that both the U.S. enterprise and the foreign investor have a tax basis in the same depreciable asset.

The issue is whether the cash consideration received by the U.S. enterprise from the foreign investor for tax benefits that the foreign investor will obtain in the foreign tax jurisdiction should immediately be recognized in income or deferred.

EITF Discussion. The Task Force acknowledged that practice is diverse and that in some cases the cash consideration received by the U.S. enterprise has been recognized in income immediately and in other cases has been deferred. The Task Force reached a consensus that the timing of income recognition should be determined based on individual facts and circumstances but that immediate income recognition is not appropriate if there is more than a remote possibility of loss of the cash consideration received due to indemnification or other contingencies.

Issue. Subsidiary S (seller-lessee), a subsidiary of Company A, enters into a sale-leaseback transaction for a building with Company B (buyer-lessor). Company B requires Company A to provide an unsecured guarantee of the lease payments. The transaction otherwise meets all of the provisions under Statement No. 98 for Subsidiary S to use sale-leaseback accounting.

The issue is whether Company A's unsecured guarantee of Subsidiary S's lease payments is a form of continuing involvement that precludes the application of sale-leaseback accounting under Statement No. 98 in (1) Subsidiary S's separate financial statements and (2) Company A's consolidated financial statements.

EITF Discussion. The Task Force expressed the view that an entity's unsecured guarantee of its own lease payments is not a form of continuing involvement that precludes sale-leaseback accounting under Statement No. 98 because such a guarantee does not provide the buyer-lessor with additional collateral that reduces the buyer-lessor's risk of loss, except in the event of the seller-lessee's bankruptcy. The Task Force reached a consensus that an unsecured guarantee of the lease payments of one member of a consolidated group by another member of the consolidated group is not a form of continuing involvement that precludes sale-leaseback accounting under Statement No. 98 in the consolidated financial statements. However, the Task Force also reached a consensus that an unsecured guarantee of the lease payments of one member of a consolidated group by another member of the consolidated group is a form of continuing involvement that precludes sale-leaseback accounting under Statement No. 98 in the separate financial statements of the seller-lessee because such a guarantee provides the buyer-lessor with additional collateral that reduces the buyer-lessor's risk of loss.

Issue. Company A (seller-lessee) enters into a real estate sale-leaseback transaction with unrelated Company B (buyer-lessor). Company B requires Company A to provide an irrevocable letter of credit securing all or a portion of the lease payments as required under the lease agreement. The issuer of the letter of credit does not require Company A to pledge specific assets as collateral. The transaction otherwise qualifies for sale-leaseback accounting under Statement No. 98. The issue is whether Company A's uncollateralized, irrevocable letter of credit is a form of continuing involvement that precludes sale-leaseback accounting under Statement No. 98.