Steven Rubin, CPA

Deloitte & Touche LLP

Consolidation, translation, and the equity method are related sets of accounting practices used mainly in the preparation of consolidated financial statements.

Consolidated financial statements present the financial position, results of operations, and cash flows of a consolidated group of companies essentially as if the group were a single enterprise with one or more branches or divisions. With limited exceptions, a consolidated group of companies includes a parent company and all subsidiaries in which the parent company has a direct or indirect controlling financial interest. Because the reporting entity for consolidated financial statements transcends the legal boundaries of single companies, consolidated financial statements have special features, which require consideration in preparing and interpreting them.

Consolidation is required when one company, the parent, owns—directly or indirectly—more than 50 percent of the outstanding voting shares of another company, unless control is likely to be temporary or does not rest with the parent. For instance, a majority-owned subsidiary is not consolidated if it (1) is in legal reorganization or bankruptcy or (2) operates under foreign exchange restrictions, controls, or other governmentally imposed uncertainties so severe that they cast doubt on the parent's ability to control the subsidiary. Majority-owned subsidiaries excluded from consolidation because control is likely to be temporary or does not rest with the parent are called unconsolidated subsidiaries.

Investments in unconsolidated subsidiaries, like other investments that give an investor the ability to exercise significant influence over the investee's operating and financial activities, are accounted for by the equity method, which is discussed below.

The fact that a particular subsidiary is located in a foreign country, has a large minority interest, or engages in principal activities substantially different from those of its parent is irrelevant to the consolidation requirement. That was not always the case, however. Until 1988, those factors were quite relevant and, indeed, were considered to be legitimate reasons for excluding a particular subsidiary from consolidation. The rules were changed by the issuance of Statements of Financial Accounting (SFAS) No. 94, "Consolidation of All Majority-Owned Subsidiaries," and that no longer is the case. The SFAS No. 94 requires consolidation of all majority-owned subsidiaries unless control is temporary or does not rest with the majority owners.

A difference in fiscal periods of a parent and a majority-owned subsidiary does not in itself justify the subsidiary's exclusion from consolidation. In that case, the subsidiary has to prepare, for consolidation purposes, financial statements for a period that corresponds with or closely approaches the parent's fiscal period.

If, however, the difference between the parent's and the subsidiary's fiscal periods does not exceed about three months, the subsidiary's financial statements may be consolidated with those of the parent even though they cover different periods. In that case, recognition has to be given in the consolidated financial statements by disclosure or otherwise of this fact and the effect of any intervening events that materially affect consolidated financial position or results of operations.

Only legal entities can own assets, owe liabilities, issue capital stock, earn revenues, enjoy gains, and incur expenses and losses. A group of companies as such cannot do those things. So the elements of consolidated financial statements are the elements of the financial statements of the members of the consolidated group of companies—the parent company and its consolidated subsidiaries. They are the assets owned by the member companies, the liabilities owed by the member companies, the equity of the member companies, and the revenues, expenses, gains, and losses of the member companies.

Some elements of the financial statements of member companies are not elements of the consolidated financial statements, however. The elements of the financial statements of a reporting entity are relationships and changes in relationships between the reporting entity and outside entities. But some elements of the financial statements of members of a consolidated group are relationships and changes in relationships between member companies, called intercompany amounts. (They would more accurately be described as intragroup amounts.) Intercompany amounts are excluded from consolidated financial statements.

It is convenient to prepare consolidated financial statements by starting with the financial statements of the member companies, which include intercompany amounts. The intercompany amounts are removed by adjustments and eliminations in consolidation. The items are:

Intercompany stockholdings. Ownership by the parent company of capital stock of the subsidiaries and ownership, if any, by subsidiaries of capital stock of other subsidiaries or of the parent company.

Intercompany receivables and payables. Debts of member companies to other member companies.

Intercompany sales, purchases, fees, rents, interest, and the like. Sales of goods or provision of services from member companies to other member companies.

Intercompany profits. Profits recorded by member companies in transactions with other member companies reflected in recorded amounts of assets of member companies at the reporting date.

Intercompany dividends. Dividends from members of the consolidated group to other members of the consolidated group.

After the intercompany amounts are eliminated, the consolidated financial statements present solely relationships and changes in relationships with entities outside the consolidated reporting entity. They present:

Amounts receivable from and amounts payable to outside entities

Investments in outside entities

Other assets helpful in carrying out activities with outside entities

Consolidated equity equal to the excess of those assets over those liabilities

Changes in those assets, liabilities, and equity, including profits realized or losses incurred by dealings with outside entities

Consolidated financial statements present the financial affairs of a consolidated group of companies united for economic activity by common control.

In 2003, the Financial Accounting Standards Board (FASB) issued FASB Interpretation (FIN) No. 46 (Revised December 2003), "Consolidation of Variable Interest Entities (VIEs)—An Interpretation of Accounting Research Bulletin (ARB) No. 51," to clarify the circumstances where and how VIEs should be consolidated. As defined in paragraph 2c of FIN 46 R, interests in a VIE are contractual, ownership, or other interests in an entity that change with changes in the fair value of the entity's net assets, thus the term variable interest entity. VIEs are often are created for a specific purpose (e.g., to facilitate the securitization of receivables). In FIN No. 46 R, VIEs are defined by the nature and amount of their equity investment and the rights and obligations of their equity investors

FIN 46 defines a VIE as a legal entity whose equity, by design, has any of the following characteristics:

The equity investors do not have an obligation to absorb the expected losses of the entity,

The equity investors do not have the right to receive the expected returns,

The total equity at risk is not sufficient to finance the entity's activities without additional financial support,

The equity investors do not have the ability to make decisions through voting rights, or,

The voting rights of equity investors are not proportional to their expected share of losses or residual returns and substantially all of the entity's activities are on behalf of an entity with few voting rights.

In general, VIEs should be consolidated by their primary beneficiaries (e.g., the party that will absorb the majority of the losses or receive the majority of the benefits), even when the primary beneficiary is not the majority owner.

The issue of accounting for such entities received considerable public attention and accounting focus after revelations about the role of certain unconsolidated entities in possibly obscuring the underlying economic effect of certain transactions relating to Enron's financial statements. FIN 46 will make it harder to exclude debt from the balance sheet via specialized finance affiliates, and likely will require more entities to be consolidated.

Entities holding a majority of voting stock will still follow the ownership-based guidelines for consolidation in ARB No. 51, Consolidated Financial Statements.

Variable interests may include:

Investments in common or preferred stock

Loans or notes

Guarantees

Certain insurance contracts and derivative contracts

Leases, and service or management contracts.

Not all entities that qualify as VIEs are consolidated. For example, when a VIE has sufficient equity at risk such that the VIE can operate on a stand-alone basis, there may be no need for another entity to consolidate the VIE.

This topic continues to be a complex area of practice. Familiarity with the Interpretation's concepts and requirements is evolving, but FIN 46 provides much needed guidance to shore up perceived weaknesses in the consolidation requirements when VIEs exist.

FIN 46 also identifies certain required disclosures for primary beneficiaries as well as for unconsolidated VIEs.

Consolidation policy, that is, the composition of the consolidated group, needs to be disclosed in the notes to the consolidated financial statements. Also, a member of a consolidated group that files a consolidated tax return discloses the following information related to income taxes in its own separately issued financial statements:

The amount of current and deferred tax expense for each statement of earnings presented and any tax-related balances due to or from other group members as of each balance sheet date

The principal provisions of the method by which the consolidated amount of current and deferred tax expense is allocated to members of the consolidated group and the nature and effect of any changes in that method

A company can start a subsidiary by having it incorporated and investing resources in it. Including such a subsidiary in consolidated financial statements presents no special problem. The amount of the investment recorded by the parent company equals the initial equity of the subsidiary, each of which is eliminated in consolidation. Business combinations are the subject of Chapter 12 in this Handbook.

Financial statements of a parent company are stated in the domestic unit of currency, such as the U.S. dollar for U.S. parent companies. Financial statements of a foreign subsidiary are stated in a foreign unit of currency, a unit of currency other than the domestic unit of currency, such as the U.K. pound for U.K. subsidiaries. Such foreign currency financial statements cannot be consolidated with domestic currency financial statements; the result would be a set of financial statements stated in more than one unit of currency, which would make them unintelligible.

Before the financial statements of a foreign subsidiary can be consolidated with the financial statements of its parent company, therefore, the amounts in its foreign currency financial statements are changed to amounts stated in the domestic unit of currency. Changing the amounts from those stated in the foreign unit of currency to those stated in the domestic unit of currency is called translation, analogous to translation from one language to another. Translation is discussed and illustrated in Section 13.2.

Translation uses foreign exchange rates. Such rates are ratios of exchange, prices of units of one kind of currency in terms of units of another kind of currency, such as $(U.S.) 1.50 for £(U.K.) 1. Foreign exchange rates change, as all other prices do. That causes two problems in translation: (1) how to select the foreign exchange rates to use for translation; and (2) how to treat translation differences, items unique to translated financial statements caused by translating amounts in a single set of financial statements at two or more foreign exchange rates.

The equity method is used to account for investments that give an investor the ability to exercise significant influence over the investee's operating and financial activities, including investments in majority-owned subsidiaries that do not qualify for consolidation. The investee may be a corporation, a partnership, or a joint venture. An investment accounted for by the equity method is initially recorded at cost. After that, the investment's carrying amount is increased or decreased for the investor's share of changes in the underlying net assets of the investee and for certain other transactions and other events. Principles relating to the equity method are discussed in Section 13.3.

Circumstances exist in which combined financial statements of commonly controlled corporations are likely to be more meaningful than their separate financial statements. Such circumstances include, for example, ownership by one person of a controlling interest in several corporations related in their operations.

If combined financial statements are prepared, they present only relationships and changes in relationships with entities outside the combined group. That means that intercompany sales and purchases, profit, and receivables and payables are eliminated. Intercompany stockholdings, if any, are eliminated.

The separate components of equity of each corporation are aggregated with the corresponding separate components of the other corporations. Presentation of a table showing each corporation's portion of each component of combined equity in either the balance sheet or the notes, though not required by the authoritative accounting literature, would likely enhance the usefulness of the combined statements.

If all else fails to present information on a group of related companies in a helpful way, consolidating statements are often used as an effective means of presenting the pertinent information. Such statements are essentially presentations as in worksheets used to derive consolidated financial statements together with notes and other kinds of necessary disclosures.

Beyond the concepts and procedures involving all consolidated financial statements, the Security and Exchange Commission (SEC), in its Regulation S-X, has published regulations for registrants that file their consolidated financial statements with the commission.

The rules require that the application of principles for inclusion of subsidiaries in consolidated financial statements "clearly exhibit the financial position and results of operations of the registrant and its subsidiaries." A company not majority owned may not be consolidated. A subsidiary whose financial statements are as of a date or for periods different from those of the registrant may not be consolidated unless all the following conditions apply:

The difference is not more than 93 days.

The closing date of the subsidiary's financial information is expressly indicated.

The necessity for using different closing dates is briefly explained.

Due consideration must be given to consolidating foreign subsidiaries operating under political, economic, or currency restrictions. If such foreign subsidiaries are consolidated, the effects, if determinable, of foreign exchange restrictions on the consolidated financial position and results of operations must be disclosed.

Intercompany items and transactions between members of a consolidated group generally are eliminated in consolidated financial statements, and unrealized intercompany profits and losses on transactions with investees accounted for by the equity method are also eliminated. If such items are not eliminated, the registrant is required to state its reason for not doing so.

The SEC rules require brief descriptions in the notes to consolidated financial statements of the principles of consolidation followed and any changes in principles or in the composition of the companies constituting the consolidated group since the last set of consolidated financial statements was filed with the commission.

The rules require that consolidated financial statements also present:

An explanation and reconciliation of differences between (1) the amount at which investments in consolidated subsidiaries are carried on the registrant's books and (2) the equity of the registrant in the assets and liabilities of the subsidiaries

An explanation and reconciliation between (1) dividends received from unconsolidated subsidiaries and (2) earnings of unconsolidated subsidiaries

An analysis of minority interest in capital stock, in retained earnings, and in net income of consolidated subsidiaries

A subsidiary or another unit within a consolidated group of companies (or within a company or an affiliated group of companies), such as a joint venture, a division, or a branch, may be a foreign operation, an operating unit that prepares foreign currency financial statements. Before such statements can be included in domestic currency consolidated financial statements, they ordinarily have to be translated into the domestic currency used in the consolidated financial statements, the currency of the parent company's country. The SFAS No. 52, "Foreign Currency Translation," sets forth current generally accepted accounting procedures (GAAP) for translation.

The SFAS No. 52 states objectives to be achieved in translation in the face of changes in foreign exchange rates, ratios of exchange between two currencies. The principles in SFAS No. 52 were adopted with the intention of achieving those objectives. The basic objective is:

Compatibility with expected effects. Information concerning foreign operations should be generally compatible with the expected effects of changes in foreign exchange rates on the parent company's cash flows and equity. If a change in an exchange rate is expected to have an overall beneficial effect, translation should reflect that. If a change is expected to have an overall adverse effect, translation should likewise reflect that. The expected effects of a change in a foreign exchange rate on the carrying amounts of all assets and liabilities of a foreign operation should therefore be recognized currently.

Other major objectives are:

Conformity with GAAP. Translation should produce amounts that conform with GAAP. For example, inventories and land, buildings, and equipment should be stated at acquisition cost after translation.

Retaining results and relationships. The financial results and relationships in the foreign currency financial statements of a foreign operation should be retained in its statements after translation. Profits should translate into profits and losses should translate into losses. Relationships before translation, such as a current ratio of two to one or a ratio of gross profit to sales of 35 percent, should be the same after translation.

In SFAS No. 52, the FASB also considered whether to adopt another objective:

To use a "single unit of measure" for financial statements that include translated foreign amounts. (par. 70)

It did not adopt that objective (par. 75). It forces accountants to put into financial statements the equivalent of the four that results from adding one yard and three feet, thus making them meaningless and worthless. The FASB not only acknowledged that the principles in SFAS No. 52 require accountants to violate the single-unit-of-measure rule of arithmetic, but it defended it strenuously:

[The FASB] believes that, for an enterprise operating in multiple currency environments, a true "single unit of measure" does not, as a factual matter, exist.... The Board concluded that for many foreign entities, adhering to a "single unit of measure" was artificial and illusory. (pars. 85, 88)

But no unit of measure exists until it is defined for the purpose at hand. Moreover, if no single unit of measure could be soundly defined for multiple currency environments, sound consolidation, or combination involving foreign operations would be impossible.

The single unit of measure should be the unit used in the parent company's financial statements.

SFAS No. 52 states these assumptions concerning translation on which the principles in the statement are based:

Two types of foreign operations. Foreign operations are of two types, which differ from each other so much that translation procedures for the two types have to differ. The two types are (1) self-contained and integrated foreign operations and (2) components or extensions of the parent company's domestic operations.

Self-contained and integrated foreign operations. A foreign operation may be relatively self-contained and integrated in a foreign country. Such an operation should be treated in consolidated financial statements as a net investment of the parent company. The entire net investment, not merely certain assets and liabilities of the foreign operation, is exposed to the risk of changes in the exchange rate between the currency of the foreign country and the domestic currency. Though such changes affect the parent company's net investment, they do not affect its cash flows. The effects of such changes on a foreign operation should therefore be excluded from reported consolidated net income unless the parent company sells part or all of its investment in the foreign operation or completely or substantially liquidates its investment in the foreign operation.

Components or extensions of parent company domestic operations. A foreign operation may be a direct and integral component or an extension of the parent company's domestic operations, such as an import or export business. It should be treated as an integral part of the parent company's operations. Changes in the exchange rate between the currency of the country in which the foreign operation is conducted and the domestic currency directly affect certain individual assets and liabilities of the foreign operation, for example, its foreign currency receivables and payables, and thereby affect the parent company's cash flows. The effects should be recognized currently in reported consolidated net income.

Functional currencies. The most meaningful measuring unit for the assets, liabilities, and operations of a foreign operation is the currency of the primary economic environment in which the operation is conducted, its functional currency. Consolidated financial statements should therefore use one measuring unit for each functional currency of the operating units in the consolidated group of companies, including the domestic currency, which is the functional currency of the parent company. If only one measuring unit were used, the resulting information generally would be incompatible with the expected effects of changes in foreign exchange rates on the parent company's cash flows and equity. It would therefore be contrary to the basic objective of translation.

Highly inflationary economies. Currencies of countries with highly inflationary economies are unsatisfactory as measuring units for financial reporting. A highly inflationary economy is one that has cumulative inflation of approximately 100 percent or more over three years. An operation in the environment of such a currency should be treated as if the domestic currency were its functional currency.

Effective hedges. Some contracts, transactions, and balances are, in effect, hedges of foreign exchange risks. They should be treated that way regardless of their form.

SFAS No. 52 (par. 69) states that to achieve the objectives of translation and to conform with its assumptions, these four major tasks are required for each foreign operation:

Identifying the functional currency of the [operation's] economic environment

Measuring all elements of the financial statements in the functional currency

Using the current exchange rate for translating from the functional currency to the reporting currency, if they are different

Distinguishing the economic impact of changes in exchange rates on a net investment from the impact of such changes on individual assets and liabilities that are receivable or payable in currencies other than the functional currency

SFAS No. 52 indicates that identifying the functional currency of a foreign operation by determining the primary economic environment in which the operation is conducted is essentially a matter of management judgment. Management assesses the economic facts and circumstances pertaining to the foreign operation in relation to the objectives of translation, discussed above. Economic factors are considered both individually and collectively to determine the functional currency, so that the financial results and relationships are measured with the greatest degree of relevance and reliability.

Exercise of management's judgment is simplified if a foreign operation is either clearly self-contained and integrated in a particular foreign country, so that the currency of that country obviously is its functional currency, or clearly a direct and integral component or extension of the parent company's operations, so that the domestic currency obviously is its functional currency.

The functional currency of a foreign operation normally is the currency of the environment in which it primarily generates and expends cash. But sometimes observable facts are ambiguous in pointing to the functional currency. For example, if a foreign operation conducts significant amounts of business in two or more currencies, its functional currency might not be easily identifiable. For those operations, individual economic facts and circumstances need to be assessed.

Appendix A of SFAS No. 52 provides guidance for making those assessments in particular circumstances. The guidance is grouped in sets of indicators: cash flow indicators, sales price indicators, sales market indicators, expense indicators, financing indicators, and intercompany transactions and arrangements indicators.

Most foreign operations prepare their financial statements in their functional currencies. Some, however, prepare their financial statements in other foreign currencies. Before the financial statements of a foreign operation are translated from its functional currency to the domestic currency, its foreign currency financial statements obviously have to be stated in its functional currency. If its financial statements are stated in another currency because its records are maintained in the other currency, they have to be remeasured into the functional currency before translation.

SFAS No. 52 (par. 10) distinguishes between remeasurement and translation. It states the goal of remeasurement to be "to produce the same results as if the ... books of record had been maintained in the functional currency."

Remeasurement requires, as does translation, use of foreign exchange rates. For remeasurement, they are the rates between the foreign currency in which the financial statements of a foreign operation are stated and its foreign functional currency. Unlike translation, however, remeasurement requires the use of historical foreign exchange rates in addition to the current foreign exchange rate. Historical rates are rates at dates before the reporting date as of which certain financial statement items are recorded, such as items recorded at acquisition cost.

Remeasurement takes three steps. First, amounts to be remeasured at historical rates are distinguished from amounts to be remeasured at current rates. Second, the amounts are remeasured using the historical and current rates, as appropriate. Third, all exchange gains and losses identified by remeasurement are recognized currently in income. Such gains and losses are identified by remeasuring amounts at rates current at the reporting date, mainly monetary assets and liabilities not denominated in the functional currency, that differ from rates current at the preceding reporting date or an intervening date at which they were acquired.

Amounts remeasured at historical rates generally are amounts stated in historical terms, such as acquisition cost, and related revenue and expenses, such as depreciation.

SFAS No. 52 specifies that amounts resulting from interperiod income tax allocation and amounts related to unamortized policy acquisition costs of stock life insurance companies are to be remeasured using the current rate.

To remeasure an amount recorded in a currency other than the functional currency at the lower of cost and market, its cost in the foreign currency is first remeasured using the historical exchange rate. That amount is compared with market in the functional currency, and the remeasured amount is written down if market is lower than remeasured cost. If the item had been written down in the records because market was less than cost in the currency in which it was recorded, the write-down is reversed if market in the functional currency is more than remeasured cost.

If an item is written down to market in the functional currency, the resulting amount is treated as cost in subsequent periods in which it is held in applying the lower of cost and market rule.

The financial statements of a foreign operation in a highly inflationary economy are remeasured to the domestic currency the way they would be remeasured were the domestic currency its functional currency.

Amounts remeasured into the domestic currency need not be translated, because the domestic currency is used as the reporting currency in the consolidated financial statements. Amounts measured in a foreign currency or remeasured into a foreign currency are all translated using the current foreign exchange rate between the foreign currency and the domestic currency.

For assets and liabilities, that is the rate at the reporting date. For income statement items, that is the rates as of the dates during the reporting period at which the items are recorded. An appropriately weighted average rate may be used to translate such items if they are numerous.

Translation adjustments result from translating all amounts in foreign currency financial statements at rates current at the reporting date or during the reporting period different from rates current at the previous reporting date or during the previous reporting period. Remeasurement of a foreign operation's foreign currency financial statements involves recognition in current income of exchange gains and losses. In contrast, translation adjustments are not recognized in current income but are accumulated in a separate component of equity.

The translation adjustments pertaining to a foreign operation are transferred from equity to gain or loss on disposition of the foreign operation when it is partly or completely sold or completely or substantially liquidated.

The functional currency of a foreign operation that is a component or extension of the parent company's operations is the domestic currency. If it prepares its financial statements in a foreign currency, those financial statements are remeasured into the domestic currency by procedures discussed above. No translation is required for such a foreign operation.

Some transactions of a unit in a consolidated group of companies may take place in a currency other than the functional currency of the unit. For example, a unit whose functional currency is the Mexican peso may buy a machine on credit for U.K. pounds or may sell securities on credit for French francs. Except in a forward exchange contract (discussed below), the amounts in such a foreign currency transaction are measured at the transaction date at the foreign exchange rate at that date—in the example, between the peso and the pound or between the peso and the franc.

At the next reporting date or at an intervening date at which the receivable or payable is settled, the receivable or payable is remeasured at the rate current at that date. Changes in its amount as measured in the functional currency since the previous reporting date or an intervening date at which it was acquired are transaction gains or losses, to be included in current reported consolidated net income, except as discussed later.

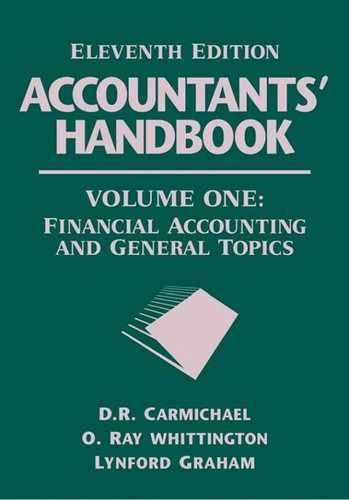

To illustrate: Corporation P, whose functional currency is U.S. dollars, borrowed £(U.K.)1,000,000 on January 1, 20X1, and agreed to repay £100,000 on December 31, 20X1, and £1,100,000 on December 31, 20X2. Exchange rates were $1.60/£1 at January 1, 20X1, and $1.50/£1 at December 31, 20X1.

The payment of £100,000 on December 31, 20X1, is remeasured as interest expense of $150,000. The liability in dollars at December 31, 20X1, is remeasured for the change in exchange rate and a transaction gain of $100,000 is determined, for presentation in P's income statement for the year 20X1, as shown in Exhibit 13.1.

Forward exchange contracts are contracts that require currencies of two countries to be traded in specified amounts at specified future dates and specified rates, called forward rates. Such contracts are foreign currency transactions that require special treatment.

A forward exchange contract may involve a discount or premium, a difference between the foreign exchange rate specified in the contract and the rate at the date the contract is entered into, multiplied by the amount of foreign currency specified in the contract. Ordinarily, a discount or premium is allocated to income over the duration of the forward exchange contract. However, a discount or premium may be treated differently in these circumstances:

If the contract is designated as and is effective as a hedge of a net investment in a foreign operation (discussed further on). If so, the discount or premium may be included with translation adjustments and thus not be reported in income.

If the contract meets the tests of a hedge of an identifiable foreign currency commitment (also discussed farther on). If so, the discount or premium may be included in the amount at which the foreign currency transaction related to the commitment is stated.

A gain or loss on a forward exchange contract to be reported in the current reporting period is computed by multiplying the amount of the foreign currency to be exchanged by the difference between (1) the foreign exchange rate at the reporting date and (2) the rate (a) on the date on which the contract was made or (b) the previous reporting date, whichever is later. A gain or loss on a forward exchange contract is recognized in income as a transaction gain or loss in the period of the gain or loss, unless it is in one of the categories of transaction gains and losses excluded from net income, discussed later.

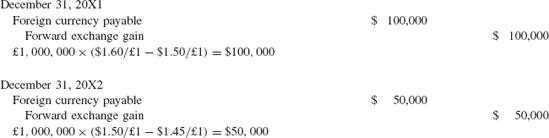

To illustrate a forward exchange contract: On January 1, 20X1, P and Q enter into a contract in which Q agrees to buy £(U.K.)1,000,000 from P for $(U.S.)1,550,000, incorporating a forward rate of $1.55/£1, on December 31, 20X2. The exchange rate at January 1, 20X1, is $1.60/£1. The contract therefore involves a premium to P and a discount to Q of £1,000,000 × ($1.60/£1 – $1.55/£1) = $50,000.

Q makes this entry:

P and Q allocate the $50,000 to forward exchange gain or loss over the years 20X1 and 20X2. P makes this entry in each of the two years:

Q makes this opposite entry in each of the two years:

The exchange rate changes to $1.50/£1 at December 31, 20X1, and $1.45/£1 at December 31, 20X2. P records these entries based on the changes in the exchange rate:

Q records these opposite entries based on the changes in the exchange rate:

On settlement of the contract on December 31, 20X2, P makes this entry:

Q makes this opposite entry:

The contract may be summarized as shown in Exhibit 13.2.

The net gain of P and loss of Q of $100,000 equal the difference between the forward rate and the rate on the settlement date times the amount of currency transferred:

Gains and losses on some foreign currency transactions are not recognized in income when they occur.

SFAS No. 52 (par. 20) requires amounts that otherwise fit the definition of gains and losses on foreign currency transactions to be treated as translation adjustments if

[They] are designated as, and are effective as, economic hedges of a net investment in a foreign entity, commencing as of the designation date [or]

[They are] intercompany foreign currency transactions that are of a long-term investment nature (that is, settlement is not planned or anticipated in the foreseeable future), when the [units that are parties] to the transaction[s] are consolidated, combined, or accounted for by the equity method in the reporting [entity's] financial statements.

Recognition of transaction gains and losses in consolidated income is deferred for such gains and losses resulting from transactions intended to hedge identifiable foreign currency commitments; they are included in accounting for the transaction resulting from the commitment. However, recognition of losses is not deferred if deferral would lead to recognition of losses in subsequent periods.

SFAS No. 52 (par. 21) states two conditions that have to be met for a foreign currency transaction to be considered a hedge of an identifiable foreign currency commitment:

The foreign currency transaction is designated as, and is effective as, a hedge of a foreign currency commitment.

The foreign currency commitment is firm.

Other topics concerning translation by the current rate method include income tax considerations, intercompany profit eliminations, selection of exchange rates, approximations, and required disclosures.

Treatment of foreign operations involves these special income tax accounting treatments:

Unremitted earnings. Deferred taxes are not recognized on translation adjustments that meet the tests in APB Opinion No. 23, "Accounting for Income Taxes—Special Areas," concerning unremitted earnings.

Intraperiod allocation. Income taxes related to transaction gains and losses or translation adjustments reported in separate components of the income statement or the statement of changes in equity are allocated to the separate components.

An exception in the current rate method to the use of the current exchange rate for translation is the method to eliminate intercompany profits on transactions between combined or consolidated companies or between affiliates accounted for by the equity method. They are eliminated at the rates at the dates of the transactions, because those are the rates at which the profits are embedded in the recorded amounts. Such eliminations precede applying the current exchange rates to the foreign currency amounts.

To illustrate: Corporation P, a domestic parent company, sold a parcel of land last year to Corporation S, its foreign subsidiary, at a profit of $24,000, when the exchange rate was $1/Z8 (Polish zlotys). S recorded the land in zlotys. The current exchange rate is Z6 = $1. The profit is eliminated at Z8/$1. The remaining amount at which S has the land recorded is translated at Z6/$1. However, exchange restrictions between dollars and zlotys may be severe enough to call into question the soundness of including S in the consolidated reporting entity.

The current foreign exchange rate is used for most translation required by SFAS No. 52. Circumstances in which the rates at the dates of transactions are used instead are discussed above. These are other special considerations in selecting exchange rates:

If the two currencies involved could not be exchanged on the date of the transaction or the reporting date, the rate at which they could be exchanged at the first succeeding date is used.

If the inability to exchange the two currencies is not merely temporary, including the foreign operation in a consolidated group or accounting for it by the equity method is questioned.

Foreign currency transactions are translated at the rates at which they could have been settled at the dates of the transactions. Resulting receivables and payables are translated subsequently at the rates at which they could be settled at the reporting dates.

If there is more than one rate at a particular date, the rate at which foreign currency could be exchanged for domestic currency to remit dividends is used.

If the reporting date of the foreign currency financial statements being translated differs from the reporting date of the reporting entity in which the foreign operation is included, the current rate is the rate in effect on the reporting date of the foreign currency financial statements.

Approximations of the results of applying the required translation principles are acceptable if the cost of applying them to every detail exceeds the benefits of such precision and the results do not materially differ from what they would be by applying them to every detail. Judgment is required to determine whether to use approximation, because determining the extent of the differences precisely would require the very calculations to be avoided by approximations.

These disclosures are required concerning foreign operations:

The total transaction gains or losses, including, for this purpose, gains and losses on forward contracts other than those excluded from income

An analysis of the changes in the separate component of equity for translation adjustments, including at least:

The beginning and ending accumulated balances

The net change from translation adjustments and gains and losses from hedges and intercompany balances treated the way translation adjustments are treated

Income taxes allocated to translation adjustments

Transfers from the equity component into income because of the partial or complete sale of an investment in a foreign operation or the complete or substantial liquidation of a foreign operation

The equity method, which is the focus of APB Opinion No. 18, is used to account for investments in unconsolidated subsidiaries, corporate joint ventures, and common stock that provide the investor with the ability to exercise significant influence over the operating and financial policies of the investee.

Under the equity method, an investor initially records an investment at cost. It adjusts the carrying amount of the investment at the end of the period in which it is acquired and in succeeding periods by the investor's proportionate share of changes in the investee's assets and liabilities and for the effects of intercompany profits. The principles for determining the cost of an investment accounted for by the equity method are essentially the same as those for determining the cost of an investment leading to a business combination accounted for by the purchase method, discussed in Chapter 12.

An investor's net income for a period and its equity at a point in time with its investment accounted for by the equity method are generally the same as they are with the investee consolidated. Application of SFAS No. 34, "Capitalization of Interest Cost," and SFAS No. 58, "Capitalization of Interest Cost in Financial Statements That Include Investments Accounted for by the Equity Method" cause differences, however.

Under SFAS No. 34, the total amount of interest cost capitalized in a set of consolidated financial statements cannot exceed the total amount of interest cost incurred by all the members of the consolidated group after intercompany amounts are eliminated. Under SFAS No. 58, however, for investments accounted for by the equity method, the total amount of interest cost capitalized in the investor's financial statements cannot exceed the total amount of interest cost incurred solely by the investor. That is, interest costs incurred by an investee accounted for by the equity method are excluded in accounting for amounts in the investor's financial statements on which interest is capitalized. Interest cost incurred by the investee can be capitalized only on amounts in the investee's financial statements.

An investor generally uses the equity method to account for each of the following types of investments.

If a subsidiary does not qualify for consolidation, its financial statement elements are not combined with corresponding elements of the parent company line by line, but are instead reported in the parent company's balance sheet and income statement on one line on each statement, the one called investment in unconsolidated subsidiary or the like and the other called investment revenue or the like.

An enterprise may be formed and operated by a number of other enterprises as a joint venture—a separate business or means to carry out a specific project for the benefit of its investors, also called venturers. The venturers pool their resources, knowledge, and talents and share risks for the purpose of ultimately sharing rewards. In many joint ventures, each venturer has more than just a passive interest or investment; each participates—either directly or indirectly—in managing the venture. Investments in joint ventures are generally accounted for by the equity method.

In the absence of evidence to the contrary, an investor with an investment of from 20 percent to 50 percent of the voting common stock of an investee is presumed to have the ability to exercise significant influence over the financial and operating policies of the investee and, because of that, uses the equity method to account for such an investment. Conversely, in the absence of evidence to the contrary, an investor with an investment of less than 20 percent of the common stock of an investee is presumed not to have the ability to exercise significant influence over the financial and operating policies of the investee and, therefore, does not use the equity method to account for such an investment but uses the method discussed in Subsection 13.4 (a).

The ability to exercise significant influence may be inferred from, for example:

Representation on the investee's board of directors

Participation in policy-making processes

Material intercompany transactions

Interchange of managerial personnel

Technological dependency

The inability to exercise significant influence may be inferred from, for example:

Opposition by the investee that challenges the investor's ability to exercise significant influence, such as litigation or complaints to government authorities

An agreement by the investor surrendering significant rights as a stockholder

Concentration of the majority ownership of the investee among a few stockholders, who operate the investee without regard to the views of the investor

Inability of the investor to obtain representation on the investee's board of directors after attempting to do so

Inability of the investor to obtain financial information necessary to apply the equity method after attempting to do so

No one item in either of those lists is the sole determining factor as to whether an investor has the ability to exercise significant influence over the investee. Instead, all items are considered collectively.

If an investor owns two investments of, say, 20 percent each in unrelated corporations, one investment might qualify for the equity method and the other not, because their circumstances differ. Judgment is always necessary in determining whether an investment gives an investor the ability to exercise significant influence over the investee.

Application of the equity method is discussed and illustrated below.

Under the equity method, the investor's initial investment, in essence, comprises three bundles:

Bundle A. A proportionate share of the book values of the investee's assets and liabilities on the date of the purchase.

plus

Bundle B. A proportionate share of the differences between the book values and the fair values of the investee's assets and liabilities on the date of the initial investment (commonly referred to as net unrealized appreciation or unrealized depreciation). The principles for determining the fair values of the investee's assets and liabilities parallel the principles in applying the purchase method of accounting for business combinations, discussed in Chapter 12.

plus

Bundle C. Goodwill, which is the excess at the date of purchase of (1) the cost of the investment over (2) the investor's proportionate share of the fair values of the investee's assets and liabilities (the sum of A + B) at the date of the purchase. If (2) exceeds (1), this bundle is negative goodwill. The principles of accounting for goodwill and negative goodwill under the equity method parallel the principles to account for them in consolidation.

The investor adjusts the carrying amount of the investment in succeeding periods by its proportionate share of changes in each bundle and for the effects of intercompany profits.

Changes in the investee's equity are caused by earnings or losses from operations, extraordinary items, prior period adjustments, the payment of cash or property dividends, and other transactions by the investor or the investee in stock of the investee.

The investor charges the investment account for its proportionate share of the investee's earnings from operations and credits investment revenue. If the investee reports a loss, the investor credits the investment account for its proportionate share of the investee's loss from operations and charges investment revenue. A negative balance in the investment revenue account for a reporting period is disclosed as a loss from investment. The investor adjusts its investment account for its proportionate share of the investee's prior period adjustments and extraordinary items and correspondingly charges or credits prior period adjustments and extraordinary items in its own financial statements.

An investor recognizes receipt of a cash dividend by crediting its investment account.

The portion of the investment that represents the investor's proportionate share of the differences between the fair values and the book values of each of the investee's assets and liabilities at the date of the investment (unrealized appreciation or depreciation) is amortized to investment revenue over the remaining estimated useful lives of the underlying assets and liabilities.

The portion of the difference between the cost of an investment and the amount of underlying equity in assets and liabilities of an investee accounted for by the equity method that represents goodwill, known as equity method goodwill, is not amortized. Equity method goodwill is not tested for impairment in conformity with FASB Statement No. 142. Equity method investments continue to be tested for impairment in conformity with paragraph 19(h) of APB Opinion No. 18, "The Equity Method of Accounting for Investments in Common Stock."

Intercompany profit or loss on assets bought from or sold to an investee is eliminated in the period of sale by adjusting the investment and the investment revenue accounts. That entry is reversed in the period in which the asset is sold to unrelated parties. The amount of unrealized profit or loss to be eliminated depends on whether the underlying transactions are considered to be at arm's length. If the transactions are not considered to be at arm's length, all the intercompany profit or loss is eliminated. If, however, the underlying transactions are considered to be at arm's length, only the investor's proportional share of the unrealized profit or loss is eliminated.

Applying the equity method sometimes involves the following special considerations.

An investor computes its proportionate share of the investee's net income or loss after deducting cumulative preferred dividends, regardless of whether they are declared.

An investor accounts for transactions between the investee and its stockholders (e.g., issuances and reacquisitions of its stock) that directly affect the investor's proportionate share of the investee's equity in the same way that such transactions of a consolidated subsidiary are accounted for.

An investor's reporting period may differ from that of the investee or the financial statements of the investee may not be available in time for an investor to record in its financial statements the information necessary to apply the equity method currently. In either case, the investor applies the equity method using the investee's most recent available financial statements. The same lag in reporting is used each period for consistency.

The recorded amount of an investment accounted for by the equity method is normally not reduced for declines in market value. But if the decline brings that market value below the carrying amount of the investment and is judged to be permanent, the investment is written down to its recoverable amount, usually market value, and a loss is charged to current income. The distinction between a decline that is permanent and one that is not is often not clear. However, evidence of a permanent decline might be demonstrated by, for example, the investor's inability to recover the carrying amount of the investment, the investee's inability to sustain an earnings capacity that would justify the carrying amount of the investment, or a history of losses or market values substantially below cost.

To illustrate: On January 1, 20X4, Corporation P accounts for its investment in Corporation S by the equity method. The carrying amount is $24,000 and the market value of the investment is $13,000. If the decline is judged to be permanent, P discontinues applying the equity method and records this entry to reduce the investment to its recoverable amount, in this case market value:

If the market subsequently recovers, $13,000, not $24,000, is the basis at which to resume applying the equity method.

A company that accounts for an investment by the equity method ordinarily discontinues applying that method when the carrying amount of the investment in and net advances to the investee is reduced to zero, unless the investor has guaranteed obligations or is otherwise committed to providing further financial support for the investee. An investor resumes applying the equity method after the investee returns to profitable operations and the investor's proportionate share of the investee's subsequent net income equals the proportionate share of net losses the investor did not recognize during the period that application of the equity method was suspended.

If an investment no longer qualifies for the equity method because the investor no longer has the ability to exercise significant influence over the investee, the investor stops applying the equity method and starts applying the cost method from that point on. The investor does not retroactively adjust the carrying amount of the investment to reflect what the carrying amount of the investment would have been had that method been applied since the investment was acquired.

To illustrate: On January 1, 20X4, Corporation P's investment in Corporation S ceases to give P the ability to exercise significant influence over S. On that date the investment in Corporation S is reported in P's financial statements at $28,000. That becomes the investment's cost for purposes of applying the cost method from that point on.

If an investment accounted for by the cost method subsequently qualifies for the equity method because the investor subsequently gains the ability to exercise significant influence over the investee, the investor stops applying the method and starts applying the equity method from that point on. In that case, in contrast, the investor does retroactively adjust the carrying amount of the investment to what it would have been had it been accounted for by the equity method starting with its first acquisition by the investor, in a manner consistent with the accounting for a step-by-step acquisition of a subsidiary.

To illustrate: P acquired stock of S on January 1, 20X3, for $24,000. The investment did not give P the ability to exercise significant influence over S. The investment is reported in P's balance sheet on December 31, 20X3, at $24,000, in accordance with the cost method. Had the investment previously qualified for the equity method, the investment in S would have been reported in P's balance sheet at $32,000.

On January 1, 20X4, P gains the ability to exercise significant influence over S without a change in its holding of S's stock. P therefore increases its investment account to $32,000, as follows:

It applies the equity method from then on the way it would have been applied had P first obtained the ability to exercise significant influence when it first acquired the investment.

The following information about investments accounted for by the equity method, as applicable, is disclosed on the face of the financial statements, in the notes to the financial statements, or in supporting schedules or statements:

The names of the investees and the percentages of ownership.

Reasons investments of 20 percent or more of the voting stock of an investee are not accounted for by the equity method.

Reasons investments of less than 20 percent of the voting stock of an investee are accounted for by the equity method.

The amounts of net unrealized appreciation or depreciation and how the amounts are amortized.

The amounts of goodwill and how they are amortized.

The quoted market prices of the investments, if available.

Summarized information about the assets, liabilities, and results of operations of investments in unconsolidated subsidiaries or in corporate joint ventures, if they are material individually or collectively in relation to the financial position or results of operations of the investor. The information can be either about each investment accounted for by the equity method or combined information of all investments accounted for by the equity method.

Descriptions of possible conversions, exercises of warrants or options, or other contingent issuances of stock of investees that may significantly affect the investor's shares of reported earnings.

The following sections summarize some of the major pronouncements that deal with the topics covered in this chapter.

ARB No. 43, Chapter 12, "Foreign Operations and Foreign Exchange," provides criteria for the treatment of foreign subsidiaries in consolidated financial statements.

ARB No. 51, Consolidated Financial Statements, describes the purpose of consolidated financial statements and selection of a consolidation policy, and it discusses concepts underlying consolidation and procedures to prepare consolidated financial statements.

SFAS No. 94, Consolidation of All Majority-Owned Subsidiaries, amends ARB No. 51 to require consolidation of all majority-owned subsidiaries unless control is temporary or does not rest with the majority owners.

FIN No. 46(R). "Consolidation of Variable Interest Entities—An Interpretation of ARB No. 51." Revised, December 2003.

EITF Issue No. 87-15, "Effect of a Standstill Agreement on Pooling-of-Interests Accounting," holds that the existence of a standstill agreement does not by itself preclude an otherwise qualifying business combination from being accounted for by the pooling-of-interests method. A standstill agreement is an agreement that prohibits a more than 10 percent shareholder from acquiring additional shares of the enterprise or its successors for a specified period.

In EITF Issue No. 87-27, "Poolings of Companies That Do Not Have a Controlling Class of Common Stock," concludes that a business combination may still qualify for the pooling-of-interests method even if the issuing company has to convert voting preferred stock into voting common stock so as to create a controlling class of common stock.

In EITF Issue No. 88-27, "Effect of Unallocated Shares in an ESOP on Accounting for Business Combinations," specifies the circumstances in which unallocated shares held by an employee stock option plan should and should not be considered "tainted" for purposes of determining whether a business combination should be accounted for by the pooling of interests method.

FTB No. 85-5, "Issues Relating to Accounting for Business Combinations, Including Costs of Closing Duplicate Facilities of an Acquirer; Stock Transactions between Companies under Company Control; Downstream Mergers; Identical Common Shares for a Pooling of Interests; Pooling of Interests by Mutual and Cooperative Enterprises," clarifies the following matters:

That costs incurred to close duplicate facilities as a result of a business combination should not be considered part of the cost of the business combination

How a parent company should account for minority interest in an exchange of stock between two of its subsidiaries

That an exchange by a partially owned subsidiary of its common stock for the outstanding common stock of its parent should be accounted for under the purchase method

That the pooling-of-interests method may not be used to account for a business combination in which one company issues common stock identical to other outstanding common shares except that the issuer retains a right of first refusal to reacquire the shares issued in certain specified circumstances

That the conversion of a mutual or cooperative enterprise to a stock company within two years of a business combination does not by itself bar the combination from being accounted for by the pooling-of-interests method

EITF Issue No. 94-2, "Treatment of Minority Interests in Certain Real Estate Investment Trusts," and the related EITF Issue 95-7, "Implementation Issues Related to the Treatment of Minority Interests in Certain Real Estate Investment Trusts," specify how, and at what amount, the sponsor's interest and partnership income or loss should be reported in the financial statements of a real estate investment trust (REIT).

EITF Issue No. 96-16, "Investor's Accounting for an Investee When the Investor Has a Majority of the Voting Interest but the Minority Shareholder or Shareholders Have Certain Approval or Veto Rights," describes circumstances in which certain rights held by the minority interest may preclude consolidation by the controlling shareholder.

EITF Issue No. 97-2, "Application of FASB Statement No. 94 and APB Opinion No. 16 to Physician Practice Management Entities," discusses circumstances in which interests in practice management entities should and should not lead to the consolidation of the entity's financial statements.

EITF Issue No. 97-6, "Application of Issue No. 96-20 to Qualifying Special-Purpose Entities Receiving Transferred Financial Assets Prior to the Effective Date of FASB Statement No. 125," reached a consensus that was nullified by the issuance of FASB Statement No. 140.

EITF Issue No. 99-16, "Accounting for Transactions with Elements of Research and Development Arrangements," discusses reporting by an enterprise that is a party to a research and development arrangement through which it obtains the results of research and development funded partially or entirely by others.

EITF Issue No. 00-4, "Majority Owner's Accounting for a Transaction in the Shares of a Consolidated Subsidiary and a Derivative Indexed to the Majority Interest in That Subsidiary," discusses reporting by a parent company that owns a majority of a subsidiary's outstanding common stock and consolidates the subsidiary at the inception of a derivative contract of a type described in the Issue.

EITF Issue No. 02-5, "Definition of 'Common Control,'" in relation to FASB Statement No. 141, "Business Combinations," discusses how to determine whether separate entities are under common control, in the context of Statement No. 141, when common majority ownership exists by an individual, a family, or a group affiliated in some other manner.

ARB No. 43, Chapter 12, "Foreign Operations and Foreign Exchange," provides criteria for the treatment of foreign subsidiaries in consolidated financial statements.

SFAS No. 52, "Foreign Currency Translation," specifies the accounting for foreign operations reported in the financial statements of a domestic company. It supersedes SFAS No. 8, "Accounting for the Translation of Foreign Currency Transactions and Foreign Currency Financial Statements."

FIN No. 37, "Accounting for Translation Adjustments upon Sale of Part of an Investment in a Foreign Entity," prescribes that the accounting in SFAS No. 52 that applies to a sale or complete or substantially complete liquidation of an investment in a foreign entity also applies to a partial disposal by an enterprise of its ownership interest.

EITF Issue No. 90-17, "Hedging Foreign Currency Risks with Purchased Options," provides guidance on the accounting for purchased foreign currency options that are not specifically addressed in SFAS No. 52.

EITF Issue No. 91-1, "Hedging Intercompany Foreign Risks," concludes that (a) transactions between members of a consolidated group with different functional currencies can result in foreign currency risk that may be hedged for accounting purposes and (b) the appropriate accounting for the risk depends on the type of hedging instrument used.

EITF Issue No. 91-4, "Hedging Foreign Currency Risks with Complex Options and Similar Transactions," led to (a) a consensus on the type of information that should be disclosed by an entity that hedges foreign currency risks with complex or similar transactions and (b) an SEC staff position regarding the deferral of gains or losses on complex options and similar transactions.

EITF Issue No. 92-4, "Accounting for a Change in Functional Currency When an Economy Ceases to Be Considered Highly Inflationary," states that an entity with a foreign subsidiary operating in an economy that ceases to be considered highly inflationary should restate the functional currency accounting bases of nonmonetary assets and liabilities as of the date of cessation.

EITF Issue No. 92-8, "Accounting for the Income Tax Effects under FASB Statement No. 109 of a Change in Functional Currency When an Economy Ceases to Be Considered Highly Inflationary," states that deferred income taxes associated with temporary differences arising from a change in functional currency when an economy ceases to be considered highly inflationary should be reflected as an adjustment to the cumulative translation adjustment component of stockholders' equity.

EITF Issue 93-10, "Accounting for Dual Currency Bonds," discusses whether the effect of foreign currency exchange rates on dual currency bonds (bonds whose principal is repayable in U.S. dollars, but whose periodic interest is payable in a foreign currency) should be recognized (a) as an adjustment of future interest expense or (b) currently as an adjustment of the liability's carrying amount.

EITF Issue No. 97-7, "Accounting for Hedges of the Foreign Currency Risk Inherent in an Available-for-Sale Marketable Equity Security," concludes that foreign currency transaction gains or losses on a foreign currency forward exchange contract or foreign-currency-denominated liability should be reported in the Statement 115 separate component of stockholders' equity.

EITF Issue No. 01-5, "Application of FASB Statement No. 52 to an Investment Being Evaluated for Impairment That Will Be Disposed Of," discusses whether a reporting enterprise should include the accumulated foreign currency translation adjustment in the carrying amount of the investment in assessing impairment of an investment in a foreign entity that is held for disposal if the planned disposal will cause some or all of the accumulated foreign currency translation adjustments to be reclassified to net income.

APB Opinion No. 18, "The Equity Method of Accounting for Investments in Common Stock," specifies the circumstances in which an investment in common stock should be accounted for by the equity method of accounting and the principles that apply to the method.

SFAS No. 58, "Capitalization of Interest Cost in Financial Statements That Include Investments Accounted for by the Equity Method," specifies the circumstances in which investments accounted for by the equity method should be considered qualifying assets for purposes of interest capitalization.

FIN No. 35, "Criteria for Applying the Equity Method of Accounting for Investments in Common Stock," clarifies that the presumptions concerning the applicability of the equity method may be overcome by predominant evidence to the contrary, based on an evaluation of all facts and circumstances relating to the investment.

FTB No. 79-19, "Investor's Accounting for Unrealized Losses on Marketable Securities Owned by an Equity Method Investee," emphasizes that an investor should not combine the portfolios of its marketable securities with the portfolios of the marketable securities of its investees that are accounted for by the equity method, for purposes of determining the investor's unrealized losses on marketable securities.

FASB Statement No. 142, "Goodwill and Other Intangible Assets," indicates the treatment of equity method goodwill after it is first recognized.

EITF Issue No. 98-13, "Accounting by an Equity Method Investor for Investee Losses When the Investor Has Loans to and Investments in Other Securities of the Investee," provides guidance on how the equity method loss pickup from the application of APB Opinion No. 18, when the carrying amount of the common stock has been reduced to zero, interact with the applicable literature relating to investments in the other securities of the investee, FASB Statement No. 114, or FASB Statement No. 115.

EITF Issue No. 00-1, "Investor Balance Sheet and Income Statement Display under the Equity Method for Investments in Certain Partnerships and Other Ventures," discusses whether there are circumstances in which proportionate gross presentation is appropriate under the equity method of accounting for an investment in a legal entity.

EITF Issue No. 00-8, "Accounting by a Grantee for an Equity Instrument to Be Received in Conjunction with Providing Goods or Services," discusses issues involved contemporaneous exchange of equity instruments for goods or services with contingent conditions.

EITF Issue No. 00-12, "Accounting by an Investor for Stock-Based Compensation Granted to Employees of an Equity Method Investee," discusses accounting for stock-based compensation based on the investor's stock granted to employees of an investee accounted for under the equity method when no proportionate funding by the other investors occurs and the investor does not receive any increase in the investor's relative ownership percentage of the investee.

EITF Issue No. 01-2, "Interpretations of APB Opinion No. 29," discusses how to account for the exchange of an equity method investment for a similar equity method investment.