CHAPTER 2

Accounting for Equity Investments: Trading

After studying this chapter, you should have a grasp of the following:

- Accounting standards for equity investments.

- Definition of equity securities and the different types of investment that an investor can make.

- Definition according to U.S. GAAP and exclusions from this definition.

- Definition according to IFRS.

- Distinction between passive investments, significant influence, and controlling interest in an investment.

- Classification of investments from the intention perspective: trading and available-for-sale.

- Exchange-traded securities versus over-the-counter (OTC) securities.

- Trade life cycle of equity investments held for trading purposes.

- Journal entries to be recorded during the different phases of the trade life cycle.

- Illustration of investments in long equity shares held for trading.

- Preparation of general ledger accounts, income statement, and balance sheet, after the equity investments are made.

- Foreign exchange (FX) revaluation and FX translation process.

- Consummated FX translation entries versus transient FX translation entries.

- Trade date accounting versus settlement date accounting.

- Functional currency and presentation currency.

- Distinction between capital gains and currency gains in unrealized gains.

- Illustration of investments in long equity shares in foreign currency.

ACCOUNTING STANDARDS FOR EQUITY INVESTMENTS

This chapter covers the accounting requirements for equity investments. At the highest level, the appropriate accounting for long-term investments in equity shares depends upon the percentage of shares acquired in the investee company, management’s intention regarding the holding period, and the extent of marketability of these investments.

Investments in marketable equity securities are referred to as passive investments or nominal investments if the investor holds less than 20 percent interest of outstanding voting stock in the company in which the investments are made. These small investments in marketable equity securities are classified into two categories: trading securities and available-for-sale securities. The accounting treatment under the U.S. generally accepted accounting principles (GAAP) for both these categories is covered by the Financial Accounting Standard (FAS) 115. Under the International Financial Reporting Standards (IFRS), International Accounting Standard (IAS) 39 deals with this. A brief introduction to the accounting standards—U.S. GAAP as well as IFRS—is given elsewhere in this chapter.

| Relevant Accounting Standards | |

| U.S. GAAP | IFRS |

| FAS 52—Foreign Currency Translation | IFRS 7—Financial Instruments: Disclosure |

| FAS 94—Consolidation of All Majority-owned Subsidiaries | IAS 21—The Effects of Changes in Foreign Exchange Rates |

| FAS 109—Accounting for Income Taxes | IAS 32—Financial Instruments: Presentation |

| FAS 115—Accounting for Certain Investments in Debt and Equity Securities | IAS 36–Impairment of Assets IAS 39—Financial Instruments: Recognition and Measurement |

| FAS 130—Reporting Comprehensive Income | |

| FAS 157—Fair Value Measurements | |

| FAS 159—The Fair Value Option for Financial Assets and Financial Liabilities | |

DEFINITION OF EQUITY SECURITIES

Equity securities are represented by ownership shares as common stock or preferred stock, as well as rights to acquire ownership shares such as stock warrants, rights, or call options. Ownership of equity securities also includes rights to dispose of ownership in shares by way of put options. It should be noted that equity securities do not include preferred stock shares that are redeemable at the option of the investor or stock that is redeemed by the issuer. Shares of its own stock purchased by the company are often known as treasury stock and convertible bonds. However, this chapter examines the accounting requirements of equity securities that are represented by ownership shares by way of common stock or preferred stock. The other forms of equity securities are dealt with elsewhere in this book.

Note, however, that call options and put options that meet the definition of derivatives are outside the scope of the definition of equity securities for the purpose of accounting as equity securities.

Definition according to FAS 115 (U.S. GAAP)

Equity security is defined in FAS 115 as any security representing an ownership interest in an enterprise (for example, common, preferred, or other capital stock) or the right to acquire (for example, warrants, rights, and call options) or dispose of (for example, put options) an ownership interest in an enterprise at fixed or determinable prices. However, the term does not include convertible debt, nor does it include preferred stock that either must be redeemed by the issuing enterprise or is redeemable at the option of the investor. In other words, the definition includes preferred stock but does not include redeemable preference stock.

Exclusions from This Definition

This accounting standard does not apply to investments in equity securities accounted for under the equity method or to investments in consolidated subsidiaries. It is also not applicable for those entities that apply specialized accounting practices like accounting for investments in debt and equity securities at market value or fair value, with changes in value recognized in earnings or in the change in net assets.

Thus, brokers and dealers in securities, defined benefit pension plans, and investment companies are outside the purview of FAS 115. This statement also does not apply to not-for-profit organizations.

Note: Preference shares with fixed or determinable payments are classified as loans and receivables rather than as equity investments. It should be noted that such preference shares would be recorded as liabilities by the issuer, according to the accounting standard, if they have fixed or determinable payments and are not quoted in an active market.

Definition According to IAS 32 (IFRS)

An equity instrument is any contract that evidences a residual interest in the assets of an entity after deducting all of its liabilities. A financial asset is defined, among other things, as an equity instrument of another entity.

PASSIVE INVESTMENTS: LESS THAN 20 PERCENT

Investments in equity securities that are purchased and held for the short term, principally for the purpose of generating gains on resale, are classified as trading securities and reported at fair value with unrealized gains and losses included in the earnings.

Investments in equity securities that are not trading securities are classified as available-for-sale (AFS) securities and reported at fair value with unrealized gains and losses excluded from earnings and reported in a separate component of shareholders’ equity. These are typically short-term investments made by the investor. It is generally presumed that if the investor holds less than 20 percent of the voting rights of the investee company then no significant influence can be exercised on the investee company unless there is evidence to prove otherwise. The cost method is adopted for investments of this nature.

Investments in equity securities are recorded at cost, including the brokerage fees, securities transaction taxes, and any other cost associated with the procurement of the securities. Both trading and available-for-sale types of investments are carried in the books of accounts at the fair value by a process known as mark-to-market. For marketable equity securities that are listed on recognized stock exchanges, fair value is determined based on the market quotes at the end of the day. For other equity securities, the rates are obtained from the over-the-counter (OTC) market. Investments that are considered to be non-tradable are carried at cost except for any permanent impairment in value of the investment. Even tradable securities that do not have any determinable market value are also carried at cost in the books of accounts.

What Is Readily Determinable Fair Value?

According to FAS 115, paragraph 3, the fair value is determinable if any of the following three conditions is fulfilled:

1. The fair value of an equity security is readily determinable if sales prices or bid-and-ask quotations are currently available on a securities exchange registered with the Securities and Exchange Commission (SEC) or in the over-the-counter market, provided that those prices or quotations for the over-the-counter market are publicly reported by the National Association of Securities Dealers Automated Quotations systems or by the National Quotation Bureau. Restricted stock does not meet that definition.

2. The fair value of an equity security traded only in a foreign market is readily determinable if that foreign market is of a breadth and scope comparable to one of the U.S. markets referred to above.

3. The fair value of an investment in a mutual fund is readily determinable if the fair value per share (unit) is determined and published and is the basis for current transactions.

Trading Securities

The categorization from the accounting standards perspective is fair value through profit and loss, commonly referred to as FVPL. As mentioned in the previous chapter, securities meant for trading are categorized as FVPL.

Trading securities are normally held by banks and other financial institutions that engage in active buying and selling of securities with a view to make gains on trading. The mark-to-market process values the securities at market rates, recording the unrealized gains/loss on such securities. The realized and unrealized gains/loss on those securities classified as trading securities is included in the income of the investor. However, when realized gains or losses have been previously reported as unrealized, only changes in the current period are reported as realized in the period during which the equity security is sold. Dividends on such equity securities are recognized as income when declared by the company. If the dividends received by the investor exceed the cumulative earnings by way of dividends since the acquisition of the shares, then the excess dividends received are accounted for as liquidating dividend.

A financial asset should be classified as held for trading if it is part of a portfolio of identified financial instruments that are managed together and for which there is evidence of a recent actual pattern of short-term profit taking. Even though the term portfolio is not explicitly defined in the accounting standards, the context in which it is used suggests that a portfolio is a group of financial assets that are managed as part of that group, and if there is evidence of a recent actual pattern of short-term profit taking on financial instruments included in such a portfolio, those financial instruments qualify as held for trading even though an individual financial instrument may in fact be held for a longer period of time.

Available-for-sale (AFS) Securities

When the investor invests in equity securities just to utilize idle cash without any intention to hold it for a long period or without any intention to generate gains on current resale, then such investments in equity securities are classified as available-for-sale securities.

From the accounting standards perspective, available-for-sale securities are designated as such during the recognition of the financial asset or an item of non-derivative financial asset that is not categorized as any of the following:

- Loans and receivables.

- Held-to-maturity investments.

- Financial assets at fair value through profit or loss.

Equity investments classified as available-for-sale are also subject to the same mark-to-market process as mentioned earlier, resulting in unrealized gains/loss on such investments. However, such unrealized gains/loss are not included in the income of the period, but are reported as other comprehensive income (OCI). Other comprehensive income is included in the stockholders’ equity on the balance sheet and is not reported as income in the income statement of the current period.

If the securities classified as available-for-sale are sold, then the realized gains/loss on such sale is taken to the current period income statement. Simultaneously, the OCI is reduced by that amount.

This is covered in detail in the next chapter.

SIGNIFICANT INFLUENCE: 20–50 PERCENT

Where the investor owns between 20 and 50 percent of the equity of the investee company, the investor is presumed to have a significant influence in the operating and financial decisions of the investee company. It should be noted that the 20 percent threshold is not a fixed limit and it is just a guide as per the accounting standards interpretation. There could be instances where the investor may not have a significant influence in spite of holding close to 50 percent of the equity of the investee company. Where the investor commands significant influence, the equity method of accounting is adopted.

CONTROLLING INTEREST: MORE THAN 50 PERCENT

When the investor acquires more than 50 percent of the outstanding voting stock of the investee company, the investor has controlling interest because of its majority ownership of the voting stock. Investments of this nature will necessitate the preparation of consolidated financial statements.

The preparation of consolidated financial statements is statutory for presentation of the final accounts to the outside world. However, internally, the investor may use either the cost method or the equity method to account for its investments. There is no requirement to consolidate if the ownership is temporary or if the ownership is not directly held by the investor, but instead through a trustee. Consolidation of accounts is necessary for domestic, foreign, similar, or dissimilar subsidiaries. Consolidation is necessary even if the subsidiary has a different accounting year. Where the difference between the accounting years of the two companies is less than three months, the investor should consolidate the accounts of the subsidiary, taking into account any material events occurring during the intervening period that impact the accounting statements. For the investor having a significant influence or having a controlling interest, there is no election-option to value the investments at fair value.

EXCHANGE-TRADED SECURITIES VERSUS OVER-THE-COUNTER SECURITIES

Equity investments are also divided into two types: (1) equity shares of publicly traded shares in recognized stock exchanges and (2) private equity investments. Even though the accounting requirements for both are more or less the same, there are subtle differences.

Equity shares are bought and sold through share brokers who are registered with the stock exchange concerned. In the case of equity shares traded in stock exchanges, usually the principle of novation is applicable. This means that the stock exchange acts as the counterparty in the strictest sense for any transaction made through the exchange. For example, if you buy some equity share through the exchange, it is the responsibility of the exchange to ensure that you get the equity share concerned. Equally, the exchange will ensure that the counterparty gets paid on time at the contracted rate.

In the case of private equity investments, the trade is executed over-the-counter, or simply OTC. Here, the broker becomes the actual counterparty and is responsible for the fulfillment of his part of the obligation. If the counterparty fails to perform his obligation under the contract, there are no means to enforce the specific performance other than to approach the appropriate court of law.

THE TRADE LIFE CYCLE FOR EQUITY TRADING SECURITIES

- Buy the share.

- Pay brokerage/commission on the buy transaction.

- Pay the contracted amount for the share.

- Ascertain the fair value at the end of reporting period.

- Reversal of mark to market.

- Dividend declaration by the company.

- Receipt of dividend and tax withholding on dividend.

- Sell the share.

- Pay brokerage/commission on the sell transaction.

- Receive the consideration.

- Ascertain the profit/loss on the sale.

- FX revaluation entries.

- FX translation entries.

Buy the Share

For exchange-traded shares, the buy order is placed with the broker registered with the stock exchange concerned. The stock exchange usually takes the responsibility for specific performance of the contract, ensuring that both the legs of the contract are fulfilled by the respective parties. When the investor places the buy order and when the broker executes the same, it becomes a binding contract between the investor and the stock exchange. Usually the trade date is referred to as “T + 0” or simply trade date. At this stage, the asset being the equity shares and the liability being the amount payable to the broker concerned are recognized in the books of accounts. (See trade date accounting versus settlement date accounting discussed elsewhere in this chapter.)

When the net holding of any share is positive, it is usually referred to as long position, and if the net holding is negative—that is, the shares sold are greater than the shares bought of the same security—it is referred to as a short position.

For example, Alan Kimberly Inc. acquires 1,000 equity shares of Gold Crest at $490 per share from the stock exchange through the broker Silver Man on October 3. The accounting entry recorded in the books of accounts is as follows:

Brokerage/Commission on the Transaction

The broker of the stock exchange charges a commission for the services rendered. This is usually settled along with the purchase value of the shares. Accounting standards require that this be treated as part of the cost of the shares procured. Hence, this is usually built into the cost of purchase of the shares.

On the 1,000 Gold Crest shares purchased through Silver Man, the brokerage payable per share is $3. The accounting entry that is recorded in the books of accounts is as follows:

Pay the Contracted Amount for the Share

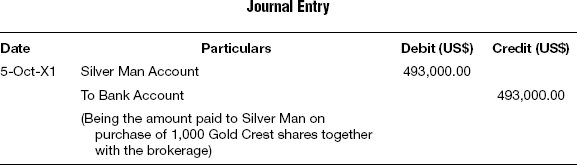

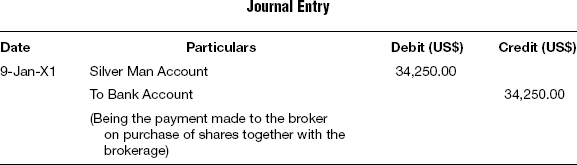

The next event in the trade life cycle is the payment of the contracted amount for the shares bought. Usually the receipt of the shares and the payment for them happens two days after the date of the trade, referred to as “T + 2.” However, this varies from exchange to exchange. The shares are usually delivered electronically by the seller and the payment is made by the buyer on the same date. During this stage, the actual asset comes into the physical possession of the buyer and the liability created earlier is settled. For exchange-traded securities, the settlement automatically takes place on the settlement date through the clearing system of the exchange concerned. For OTC trades, both parties resort to their own accepted method of settlement to ensure that they effectively avoid each other’s counterparty risk.

Payment and Delivery

For exchange-traded securities, the delivery of the securities in either physical or electronic form takes place immediately after the payment is received by the stock exchange. In this case, due to the principle of novation, both the parties avoid counterparty risk altogether. For OTC trades, neither party wants to take any risk of not being able to get the securities after making payment. Hence the counterparties resort to a system known as delivery versus payment (DvP). In this case, simultaneous exchange of securities and cash takes place between the counterparties, namely, the buyer and seller, either directly or through their respective custodians. When DvP is agreed upon by both parties, the buyer need not pay for the shares until they are delivered by the seller, and the seller need not deliver the shares so long as the buyer has not paid for them. In this case both parties avoid what is known as the counterparty risk.

Assuming that the broker is paid on T + 2, the accounting entry that is recorded in the books of accounts is as follows:

Ascertain the Fair Value at the End of the Reporting Period

At the end of every reporting period, the fair value of the shares is ascertained and the shares are marked-to-market. This process is known as portfolio valuation, when the market rate at the end of the period is determined from the primary stock exchange where the shares are traded. If there is an increase in the market rate over and above the purchase rate, then such increase is recognized as a gain on the one hand, and the corresponding amount is reflected as an increase in the value of such shares. This accounting entry is reversed on the next day or the next valuation date, when a fresh entry for the then value is recorded in the books of accounts. Alternatively, the accounting entry can also be recorded only for the incremental value. If the investor follows this incremental value method, there is no need to reverse the entry for mark-to-market recorded earlier.

Assuming that the market rate of Gold Crest on October 31 (which is the next valuation date) is $497, the accounting entry that is recorded in the books of accounts is as follows:

Reversal of Mark-to-market Entry

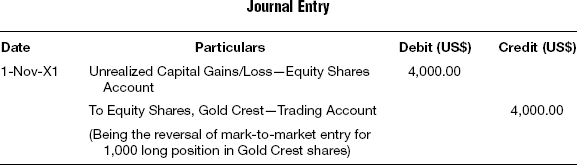

The accounting entry for mark-to-market is reversed on the next day or the next valuation date, when a fresh entry for the then value is recorded in the books of accounts. However, as mentioned earlier, if the investor follows this incremental value method, there is no need to reverse the entry for mark-to-market recorded earlier.

The accounting entry that is recorded in the books of accounts is shown below:

Corporate Action

Corporate action is, as the name implies, an action taken by the issuing company that impacts the investments or earnings from such investments. Typical examples of corporate actions include cash dividend declaration by the company, stock dividends, stock splits, reverse splits, mergers and acquisitions by the company that result in change of the name or number of shares held by the investor, and so on. The nature of the corporate actions and the accounting entries that are to be recorded on such announcements of corporate actions by the company are given here.

Dividend Declaration by the Company

One of the key activities during the trade life cycle is the corporate action in the form of cash dividend. The company will announce the rate of dividend and the date on which it becomes ex-dividend. In other words, from the ex-dividend date, the shares purchased from the exchange are not entitled for the dividend announced by the company. Technically, the shares would be quoted lower by the amount of the dividend declared by the company on the ex-dividend date. The dividend income should be recognized by the holder of the shares on the date on which it becomes ex-dividend.

There are two types of dividends a company can issue: cash dividends and stock dividends. While generally only one or the other is issued at a specific period of time—either quarterly, biannually, or yearly—both may occur simultaneously. A cash dividend is straightforward in the sense that for each share owned, a certain amount of money is distributed to each shareholder. Thus, if an investor owns 100 shares and the cash dividend is $0.50 per share, the shareholder will receive $50 as dividends.

A stock dividend also comes from distributable equity but in the form of stock instead of cash. A stock dividend of 10 percent, for example, means that for every 10 shares owned, the shareholder receives one additional share. If the company has 1,000,000 of common stock outstanding, such a stock dividend would increase the company’s outstanding shares to a total of 1,100,000. The increase in shares outstanding, however, has the effect of diluting the earnings per share and hence the stock price would decrease.

The following accounting entry that is recorded in the books of accounts assumes that Gold Crest announces a dividend of $7 per share and the ex-dividend date is October 17.

Stock Split

A stock split is also referred to as declaration of bonus shares, even though technically there is a subtle difference between the two. Typically the term stock split is applicable for corporate entities having no par value shares, while bonus shares are declared by corporate entities having shares with par value. From the company perspective, certain accounting entries are required to be recorded when bonus shares are issued, as this will have the effect of reducing the reserves and increasing the share capital of the company.

A stock split divides each of the outstanding shares of a company in the ratio of the split announced by the company, thereby lowering the price per share, as the market will adjust the price on the day the stock split is implemented. A stock split, however, is a non-event, meaning that it does not affect a company’s equity or its market capitalization, as only the number of shares outstanding changes. A stock split does not directly change the value or net assets of a company.

A company announcing a two-for-one (2:1) stock split, for example, will distribute an additional share for every one outstanding share, so the total shares outstanding will double. If the company had 50 shares outstanding, it will have 100 after the stock split. At the same time, because the value of the company and its shares did not change, the price per share will drop by half. So if the presplit price was $100 per share, the new price will be $50 per share.

The only journal entry needed for a stock split is a memo entry to note that the number of shares changed and that the par value per share has changed (if the stock has a par value.) However, a typical journal entry with debits and credits is not needed since the total dollar amounts for the par value and other components of paid-in capital and stockholders’ equity do not change.

For example, if a corporation has 100,000 shares of $1.00 par value stock and it declares a two-for-one stock split, the corporation will have 200,000 shares with a par value of $0.50 per share. Before and after the stock split, the total par value is $100,000. Other account balances within stockholders’ equity also remain the same.

However, in the case of receipt of bonus shares, the investor will have to adjust the existing cost of investments in proportion to the quantity of shares received as bonus shares and accordingly calculate the realized gains on every sale made thenceforth.

Reverse Split

A reverse split is implemented by a corporate entity that would like to increase the price of its shares. If a $1 stock had a reverse split of 1 for 10 (1:10), shareholders would have to exchange 10 of their old shares for one new one, but the paid-up value of the stock would increase from $1 to $10 per share. Sometimes a company decides to use a reverse split to shed its status as a penny stock company.

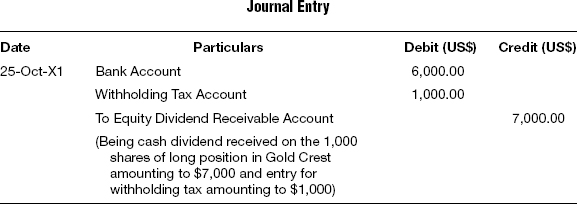

Receipt of Dividend and Withholding Tax

The actual receipt of the cash itself may take from one week to six weeks depending upon the regulatory requirement of the exchange on which the stock is listed.

Tax authorities in many countries require that tax be deducted on the dividend disbursed by a company. Withheld tax is claimed as such during the submission of income tax returns by the taxpayer. Until then, it is kept as an asset in the books of the buyer. In several countries, the tax is deducted only if the amount exceeds a specified amount; otherwise no tax is deducted. Assuming that the actual cash is received by the investor on October 25, and that $1 per share is deducted as withholding tax, the accounting entry that is recorded in the books of accounts is as follows:

Sell the Share

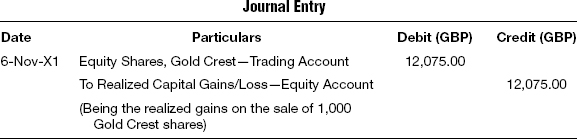

Ultimately when the shares are sold through a broker of the exchange, an accounting entry is recorded for the contracted amount to be received on such sale.

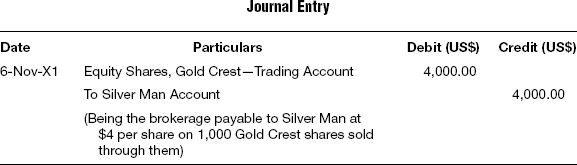

Assuming that the entire quantity of 1,000 shares of Gold Crest is sold on November 6 for a consideration of $520 each, and assuming the brokerage fee per share amounts to $4, then the accounting entry that is recorded in the books of accounts is shown as follows:

Brokerage/Commission on the Sell Transaction

The brokerage is paid while the shares are sold and only the net proceeds are taken into account. The accounting entry that is recorded in the books of accounts is shown as follows:

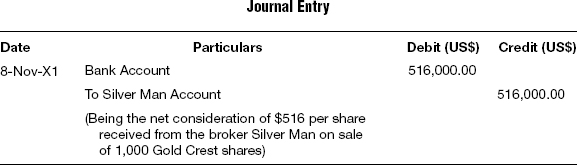

Receive the Consideration

The consideration is received on T + 2 or based on the exchange concerned. The consideration is received net of brokerage. The accounting entry that is recorded in the books of accounts is shown as follows:

Ascertain the Profit/Loss on the Sale

The profit or loss on liquidation of the shares is ascertained by deducting the cost of sales from the net sale consideration. Cost of sales is arrived at by following the first in first out (FIFO), last in first out (LIFO), or weighted-average method.

In this case 1,000 shares of Gold Crest were bought at the rate of $490 and $3 was paid per share towards brokerage fees, resulting in the cost of acquisition of Gold Crest shares being $493 per share. These were subsequently sold for a consideration of $520 per share, and a brokerage fee of $4 per share was incurred, resulting in the net realization of $516 per share. Hence the profit on each share is $23 and the total profit for the entire lot amounts to $23,000. The profit or loss realized is always recognized on the date of liquidation and not on the date on which the net proceeds are received from the broker.

The accounting entry that is recorded in the books of accounts is as follows:

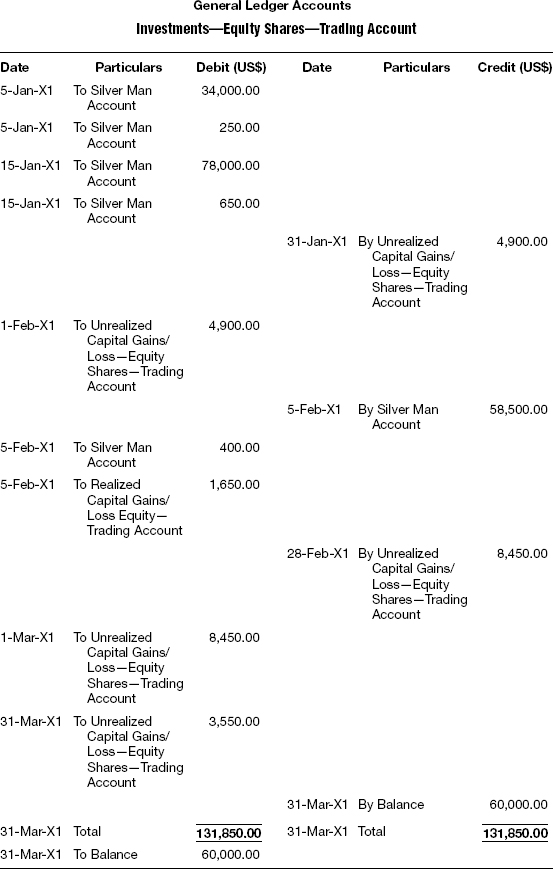

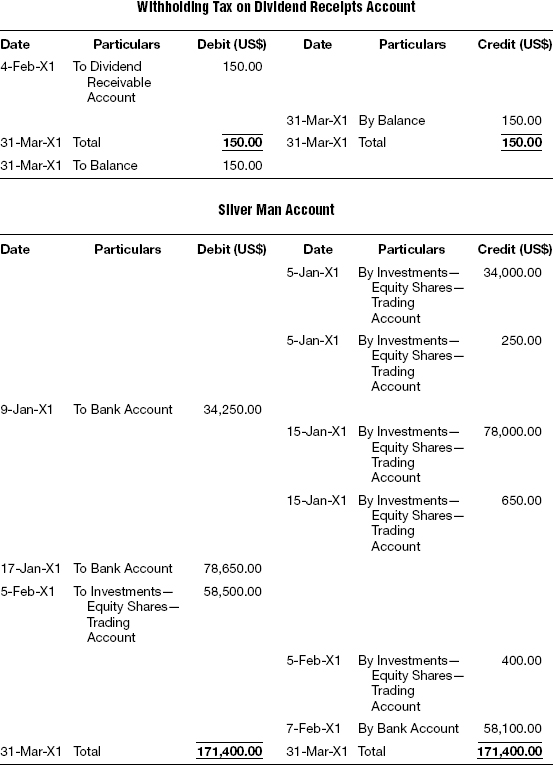

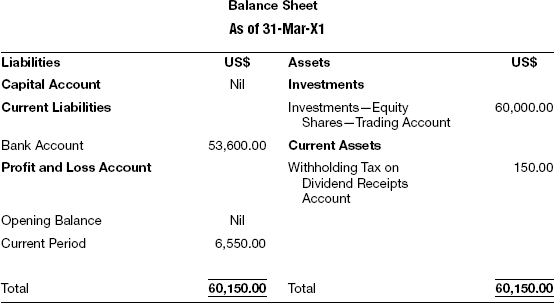

Illustration: Long Equity Shares—Trading

Assume that Alan Kimberly Inc. trades in Microsoft shares in a U.S. stock exchange through Silver Man brokers, and the details are as follow:

Trade Details

Other Details

- Settlement date T + 2

- Purchases on January 5 are settled on January 9 due to intervening holidays.

- A dividend of $0.45/share is declared by Microsoft on January 28, $0.05 being the withholding tax.

- The dividend is paid by Microsoft on February 4.

Liquidation Method

Weighted average

Market Rate

January 31: 36.00

February 28: 32.00

March 31: 40.00

Prepare

Journal entries, general ledgers, trial balance, income statement, and balance sheet for Alan Kimberly Inc., for the period January 1 to March 31.

Solution

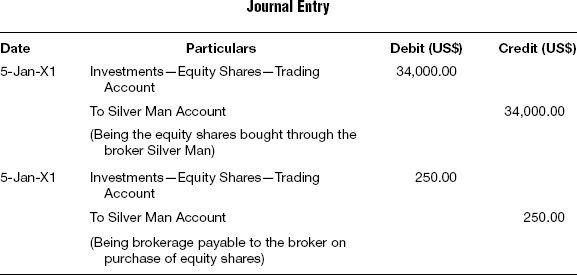

T-1 On Purchase of Equity Shares and Brokerage

T-2 On Payment of Contracted Sum

T-3 On Purchase of Equity Shares and Brokerage

T-4 On Payment of Contracted Sum

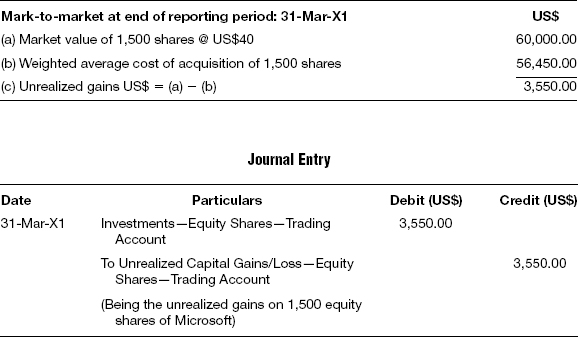

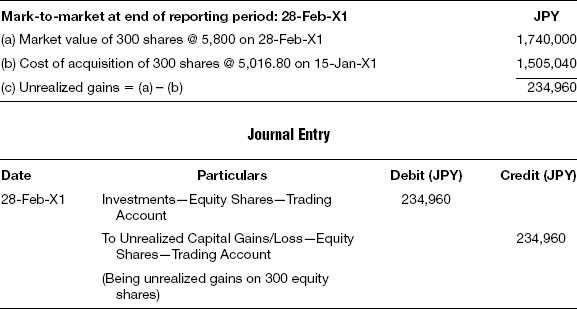

T-5 Mark-to-market at End of Reporting Period

The total long position adds up to 3,000 shares and the market value of the shares is compared with the original cost of acquisition including brokerage to arrive at the mark-to-market. Since the market rate at the end of reporting period is lower than the cost of acquisition, this results in mark-to-market loss, which is reflected as a decrease in the value of investments. Since the shares are held in the trading category, the losses are taken to the profit and loss account.

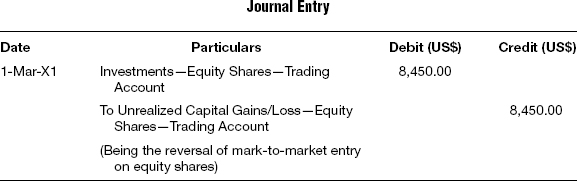

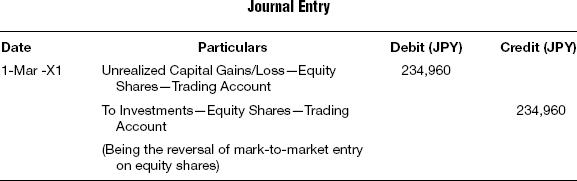

T-6 Reversal of Mark-to-market Entry

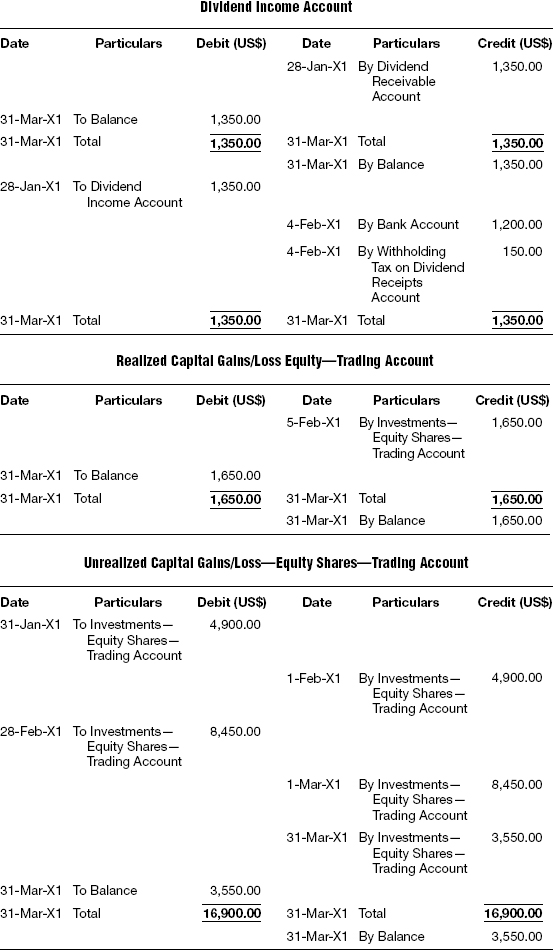

T-7 On Declaration of Dividend

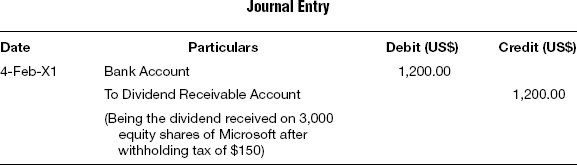

T-8 On Receipt of Dividend

T-9 Withholding Tax on Dividend

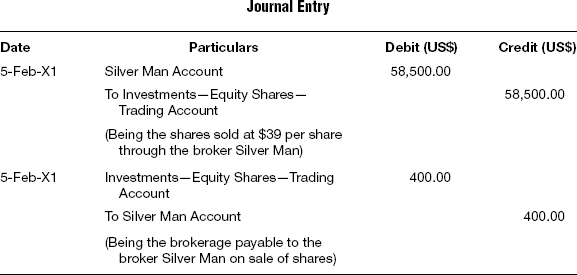

T-10 On Sale of Shares and Brokerage

T-11 On Recording Profit/Loss on Sale of Shares

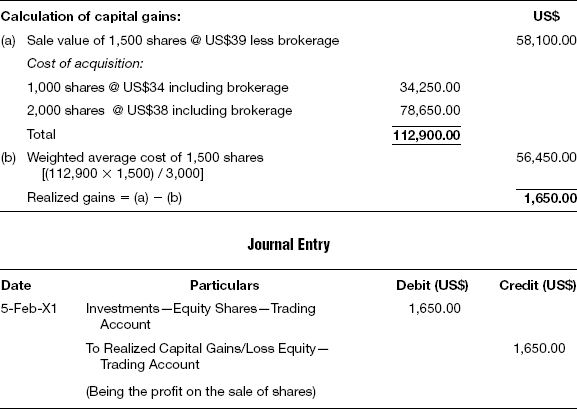

The liquidation methodology is the weighted average method. Hence the weighted average cost of acquisition of 1,500 shares is first arrived at and compared with the net sales realization to arrive at the realized gains on liquidation.

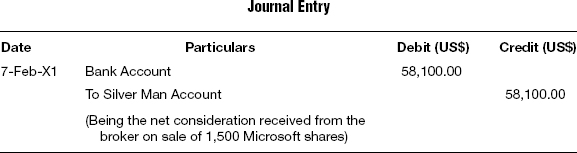

T-12 On Receipt of the Contracted Sum

T-13 Mark-to-market at End of Reporting Period

T-14 Reversal of Mark-to-market Entry

T-15 Mark-to-market at End of Reporting Period

FX REVALUATION AND FX TRANSLATION PROCESS

Functional Currency and Presentation Currency

The currency of the primary economic environment in which the investor operates is the functional currency. The financial accounting records should be maintained in the functional currency and the investor is not free to choose otherwise. The investor’s investment activities and the currency in which the fund raises money from investors predominantly determine the functional currency. Presentation currency is the currency in which the financial statements are presented to the investors.

Accounting standard FAS 52 provides general guidance on the indicators of facts to be considered in identifying the functional currency. When the indicators are mixed and the functional currency is not obvious, the standard mentions that the management’s judgment will be required to determine the functional currency that most faithfully portrays the economic results of the entity’s operations and thereby best achieves the objectives of foreign currency translation. The salient economic factors that are enumerated as indicators are cash flow indicators, sales price indicators, sales market indicators, expense indicators, financing indicators, and intercompany transactions and arrangements indicators.

A foreign currency transaction is a transaction that is denominated in a currency other than the investor’s functional currency. According to the accounting standard FAS 52, denominated means that the balance is fixed in terms of the number of units of a foreign currency regardless of changes in the exchange rate. For example, when a U.S. company buys equity shares of a company listed on the Singapore stock exchange in Singapore dollars (S$), then on purchase of the equity shares, the number of units of S$ that is payable for such purchase is fixed and it stays the same regardless of the foreign exchange rates between the US$ and S$. Hence, until the liability is settled, the U.S. company assumes the foreign exchange risk on account of the purchase of the shares. Upon payment of the liability, based on the exchange rate at that point of time, the amount in US$ terms is crystallized, resulting in realized currency gains/loss.

Translation of Foreign Currency Statements

Under the relevant accounting standards (IAS 21), foreign currency monetary items are treated differently than foreign currency non-monetary items. The essential feature of a monetary item is the right to receive or an obligation to deliver a fixed or determinable amount of units of currency. A non-monetary item does not have this right.

Examples of monetary items include the following:

- Trade receivables and payables.

- Cash dividends recognized as a liability.

- Investments in debt securities.

- Deferred taxes.

- Pension and other employee benefits to be paid in cash.

- Provisions that are to be settled in cash.

Examples of non-monetary items include:

- Prepaid amounts for goods or services.

- Deferred income.

- Investments in equity instruments.

- Inventories and other fixed assets.

- Goodwill, patents, trademarks, and other intangible assets.

It should be noted that investments in equity instruments are regarded as non-monetary items.

For assets and liabilities, the exchange rate at the balance sheet date is used to translate foreign currency statements into the functional currency. For revenues, expenses, gains, and losses, the exchange rate at the dates on which such revenue or expense is recognized is used. The accounting standard allows weighted average exchange rate to be used for translating revenues, expenses, gains, and losses where the transactions are numerous and it is found impractical to translate on a daily basis.

If an entity’s functional currency is a foreign currency, there would be translation adjustments occurring as a result of the translation process that converts the financial statements into the reporting currency. Such translation adjustments should not be included in determining the net income but should be reported separately and accumulated in a separate component of equity. It is only upon the sale or upon the substantial liquidation of such investment in foreign currency that the amount accumulated in the translation adjustment component of equity should be removed from the separate component of equity and should be reported as part of the gain or loss on liquidation of the investment for the period during which the sale or liquidation takes place. However, see the accounting treatment permitted for investment companies by SOP 93-4 later in this chapter.

FX Revaluation Process

If the reporting currency is different from the trading currency, then every journal entry recorded in the previous illustration is first revalued in the reporting currency, based on the market quote available for the trade currency. This process is known as FX revaluation. FX revaluation is performed on all the accounting entries recorded by the investor. FX revaluation of revenues, expenses, gains, and losses at the currency exchange rate freezes the amounts in the functional currency and they do not undergo any change due to fluctuation in the FX rates at the reporting period.

FX Translation Process

The income statement and balance sheet of the investor should be prepared in the functional currency, also known as the reporting currency. Hence, on the reporting date, all the assets and liabilities of the investor that are designated in foreign currency should be converted into the functional currency based on the official FX conversion rates on the reporting date. This is achieved by the FX revaluation process. However, apart from the revaluation process, another process known as FX translation is required to be performed by the investor to adjust the FX rate differential between the transaction date and the reporting date with respect to all assets and liabilities. Thus, the value of assets and liabilities is adjusted for fluctuations in the exchange rate between the date on which the asset or liability is recorded in the books of account and the reporting date. For profit and loss items, the actual amount gets crystallized on the date on which the income is realized or the expense is incurred and hence does not need any further treatment.

The FX translation process is applied on all the accounts that represent an asset or a liability. The variation in the value of the asset or liability on account of fluctuation in the exchange rate is recognized as a gain or loss, and such a gain or loss is recognized as a separate component of equity, on the one hand, and on the other, the value of the asset or liability would be restated based on the exchange rate on the reporting date. However, upon realization, the same would be taken to the income statement and the actual effect of such gains would be represented in the respective cash account.

FX Revaluation Entries

All the entries recorded heretofore are initially entered in the respective trade currencies. If the functional currency is different from the trade currency, then each and every entry recorded in the trade currency should be entered again in the functional currency by converting the entries at the respective day’s FX rates. In other words, for each trade currency that the investor deals with, there will be a complete set of books representing that trade currency. This includes journal entries, general ledger postings, trial balance, income statement, and balance sheet. After revaluing each and every journal entry of all the trade currencies into the functional currency, a separate set of books is prepared, again comprising all the elements previously mentioned: journal entries, general ledger postings, trial balance, income statement, and balance sheet. It should be noted that the ultimate financial reports would be prepared and presented to all the stakeholders based on the financial statements prepared in the functional currency only, as this will encompass all the transactions of the investor in all trade currencies dabbled with.

Some accountants follow the method of revaluing the income and expense entries in functional currency based on the average rate for the month under review, meaning all the entries would be consolidated and one entry passed for each item of income or expense at the end of the month. Whatever method is adopted, it should be followed consistently.

However, in this book all illustrations are worked out on the basis of revaluing every single journal entry recorded in currencies other than the functional currency at the foreign exchange rate applicable on the day of the transaction.

Let us assume, for the sake of illustration (only for this paragraph), the functional currency of Alan Kimberly, Inc., is pounds sterling and the FX rate on November 6 for US$/GBP is 0.525.

The accounting entry in the books of accounts to record the profit or loss on sale of shares is shown as follows:

FX Translation Entries

After revaluing all the entries in the functional currency at the respective FX rates for the day concerned, another entry needs to be passed in the books of the functional currency. This is mainly to adjust the currency gains or losses due to the fluctuations in FX rates between the reporting date and the date of recording the original entries. FX translation entries are recorded only for the asset and liability accounts. For income and expense accounts, the amount gets crystallized on the date of passing the FX revaluation entries in the books of the functional currency.

There are fundamentally two types of FX translation entries that are recorded in the books of the functional currency. The first type represents accounting for currency gains or losses that are realized or consummated. An example of this type is the currency gains realized on the amounts payable to the broker versus the amount actually paid to the broker as recorded in the functional currency. The difference between the amount payable and the actual amount paid recorded in the functional currency represents the realized currency gains or losses. Let us call this consummated FX translation entries.

The second type represents accounting for currency gains or losses that are seen on the continuing assets or liabilities of the investor. An example of this type is the currency gains on the market value of the equity shares as recorded in the functional currency. This type of gain or loss is temporary in nature and will be either reversed the next day or passed on an incremental basis, meaning that it is subject to change on a daily basis depending upon the FX rates prevailing on that day. Let us call this transient FX translation entries.

Consummated FX Translation Entry

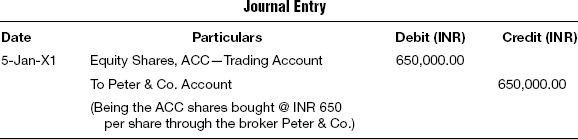

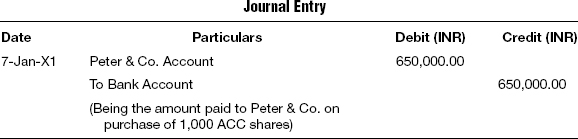

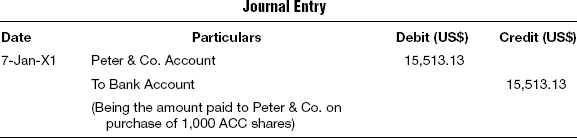

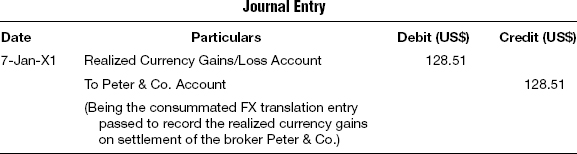

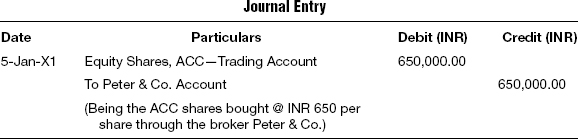

Let us assume the following facts: Ram acquires 1,000 shares of ACC Ltd. at INR 650 (Indian rupees) each on January 5 when the US$/INR FX rate is 42.25, through the broker Peter & Co. Let us assume there is no brokerage fee involved here. The settlement for the purchases through the National Stock Exchange, India, is made on January 7 when the US$/INR FX rate is 41.90. Functional currency for Ram is US$. Let us find out the amount for which a consummated FX translation entry needs to be passed.

The following entries will be passed by Ram in trade currency, which is INR, on acquiring the shares and for making the payment to the broker.

T-1 On Purchase of Equity Shares

T-2 On Payment of Contracted Sum

The following are the revaluation entries for this exchange in functional currency, which is US$.

F-1 On Purchase of Equity Shares (T-1 @ FX Rate: 42.25)

F-2 On Payment of Contracted Sum (T-2 @ FX Rate: 41.90)

Consummated FX translation entry: While the broker Peter & Co. is settled in full in trade currency, the same when recorded in functional currency looks as if Peter & Co. is paid $128.51 more than what is actually due to him. But this is due to the fluctuation in FX rate between the date of trade and date of settlement. Hence, this amount represents realized currency loss and the consummated FX translation entry would be as follows:

F-3 Consummated FX Translation Entry to Record the Realized Currency Gains/Loss on Settlement Date

Transient FX Translation Entries

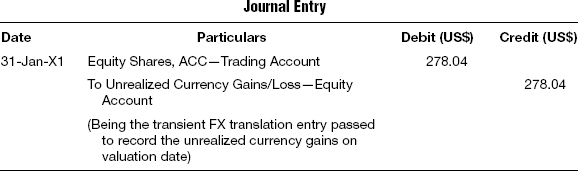

Let us assume the following facts: Ram acquires 1,000 shares of ACC Ltd. at INR 650 each on January 5 when the US$/INR FX rate is 42.25. Assume that the US$/INR FX rate on January 31, the reporting date, is 41.50, and for the sake of this example the market rate of ACC Ltd. is the same at INR 650 per share. Functional currency for Ram is US$. The following entries will be passed by Ram in trade currency, which is INR, on acquiring the shares.

T-1 On Purchase of Equity Shares

T-2 On Valuation of Shares Based on the Market Rate

No entry is required as there is no change in the value of the shares held. It is the same as the cost of acquisition of the shares.

The following are the revaluation entries for the preceding example in functional currency, which is US$.

F-1 On Purchase of Equity Shares (T-1 @ FX Rate: 42.25)

F-2 On Valuation of Shares Based on the Market Rate (T-2 @ FX Rate: 41.50)

No entry is required as there is no change in the value of the shares held. It is the same as the cost of acquisition of the shares. There is no FX revaluation entry passed as there is no original entry in trade currency for mark-to-market valuation. However, in the functional currency, there is a change in the market value for which FX translation entry is passed, which is illustrated next.

Transient FX translation entry: While the market value of the shares bought on January 5 is the same as the cost of acquisition, in dollar terms the value is different and hence a transient FX translation entry should be recorded on January 31. This is called transient entry as either the entry will be reversed the next day or, on a subsequent day, when such an entry is passed, it will be done on an incremental basis.

The market value of the shares in functional currency is INR 650,000/41.50 = $15,662.65. Hence, the difference between this market value and the cost of acquisition in US$ terms, namely 15,384.62, is $278.04 and will be recorded as unrealized FX gains. The accounting entry is as follows:

F-3 Transient FX Translation Entry to Record the Unrealized Currency Gains or Losses on Valuation Date

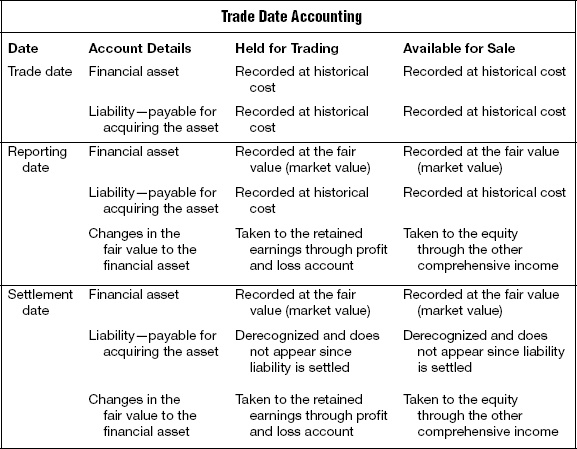

TRADE DATE ACCOUNTING VERSUS SETTLEMENT DATE ACCOUNTING

Under the trade date accounting method, both the asset and the liability for the asset purchased are recognized on the date of trade, and the payable is derecognized once the payment is made. Under the settlement date accounting method, the entire transaction is recognized only on the date of settlement. While FAS 115 is silent regarding the date on which the transaction should be recorded, the other levels of U.S. GAAP literature require trade date accounting to be followed for regular-way securities contracts, especially for broker-dealers and investment companies. For regular-way contracts, the International Accounting Standards Board (IASB) gives the option to follow either trade date accounting or settlement date accounting, provided that one is followed consistently for purchases and sales of financial assets in the same category. However, the changes in the fair value of the asset should be treated properly depending upon the classification of the asset acquired.

Trade Date Accounting

When an asset is purchased, in trade date accounting, the asset is recognized and brought into the books of account on the date of trade and a corresponding liability is established. The liability is knocked off when the settlement of the liability happens.

When the asset purchased is in a foreign currency, it leads to a little more complication. The asset is recognized in the functional currency in which the reporting is made, on the basis of the foreign exchange rate that prevails on the date of trade. The corresponding liability is also created equivalent to the asset purchased. However, when the settlement is done after a few days, the foreign exchange rate is likely to be different from the rate at which the asset was converted. Hence, when recording the settlement event in the functional currency, the liability would appear to be either overpaid or underpaid. This is dealt with by passing an appropriate FX translation entry known as consummated FX translation entry, previously discussed in this chapter.

Settlement Date Accounting

Following settlement date accounting, the asset as well as the liability are recognized on the settlement date. Here the asset gets recorded only at the value at which it is actually settled. The difference between the actual cost of acquisition for the investment and the value at which it is recorded in the books of accounts is taken as realized gains on the date of acquisition itself. If the asset is held for trading, then it is taken to the profit and loss account directly, whereas if it is an available-for-sale asset, then it is taken directly to the equity account as other comprehensive income.

Even if the asset happens to be in foreign currency, since the asset is recorded only on the date of settlement, the revaluation entry in the functional currency is recorded only at the rate at which it actually gets settled and hence there is no necessity to record any FX translation entries in this case.

Broker-dealers that use the trade date basis of record keeping are in compliance with the AICPA Guide for Audits of Brokers and Dealers in Securities, while broker-dealers that use the settlement date basis of recordkeeping are in compliance with the Guide only if the difference between trade date and settlement date accounting is not material.

A broker-dealer must have a consistent policy of reflecting all transactions either on a trade date or a settlement date basis and must compute its net capital on the same basis as it uses in recording its transactions.

However, if settlement date accounting is used, and there is a “material difference” between trade date accounting, the net capital computation must reflect the trade date position for proprietary positions, and if there is a material difference on more than an occasional basis (i.e., twice in a six-month period), trade date accounting should probably be used on a consistent basis.

SEC Letter to AICPA, April 23, 1986

DISTINCTION BETWEEN CAPITAL GAINS AND CURRENCY GAINS

When the trade currency is different from the functional currency, then the total unrealized gains or loss consists of two components: capital gains and currency gains. The U.S. GAAP Statement of Position for investment companies pertaining to the disclosure and treatment of these two components in relation to investment companies is given in the accompanying box, with a suitable illustration.

U.S. GAAP Statement of Position (SOP 93-4) for Investment Companies

The change in value of an investment in respect of an asset denominated in a foreign currency on the valuation date from the original value at which it is recorded in the books of account in functional currency has two components, namely the capital gains/loss due to change in the market rate of the asset, and currency gains/loss due to change in the foreign exchange rate. Investment companies can either choose to combine these two elements for investment transactions or disclose the currency gains/loss due to change in the FX rate separately. According to the SOP, it is not mandatory to show them separately, even though it indicates that such separate reporting would provide valuable information to the users of the financial statements.

A. Net unrealized gains in functional currency:

(Market value in foreign currency × Valuation date spot rate) − (Cost in foreign currency × Transaction date spot rate)

B. Unrealized capital gains in functional currency:

(Market value in foreign currency − Cost in foreign currency) × (Valuation date spot rate)

C. Unrealized currency gains in functional currency:

(Cost in foreign currency × Valuation date spot rate) − (Cost in foreign currency × Transaction date spot rate)

A should be equal to B + C.

Example

New Century Indian Fund acquired 1,000 shares of Bajaj Auto at INR 2,700 per share when the US$/INR was 45. The market rate of Bajaj Auto on valuation date was INR 3,000 and the exchange rate was 41. Find out the capital and currency gains on reporting date.

A. Net unrealized gains in functional currency:

(Market value in foreign currency × Valuation date spot rate) − (Cost in foreign currency × Transaction date spot rate)

= [3,000,000 × (100/45)]−[2,700,000 × (100/41)]−[2,700,000 × (100/45)]

= $66,666.67 − 65,853.67 = $813 (Gain)

B. Unrealized capital gains in functional currency:

(Market value in foreign currency − Cost in foreign currency) × (Valuation date spot rate)

= [(3,000,000 − 2,700,000) × (100/41)]

= $7,317.07 (Gain)

C. Unrealized currency gains in functional currency:

(Cost in foreign currency × Valuation date spot rate) − (Cost in foreign currency × Transaction date spot rate)

= [3,000,000 × (100/41)] − [3,000,000 × (100/45)]

= $73,170.73 − 66,666.67 = $6,504.06 (Loss)

A should be equal to B + C.

Here the capital gains amounting to $7,317.07 is reduced by adverse currency movement amounting to $6,504.06, resulting in net unrealized gains of just $813.

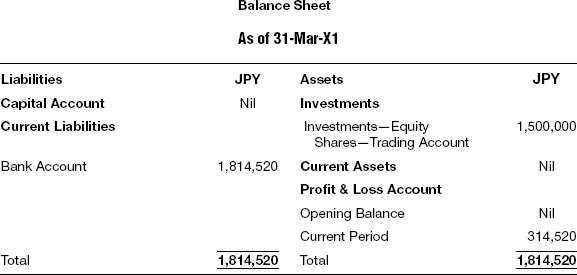

Illustration: Long Equity, Trade Currency JPY

Japan Opportunities Fund traded in DoCoMo shares on the Tokyo Stock Exchange through Yoshio & Co. brokers and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

First in first out (FIFO)

Market Rate of DoCoMo Shares in JPY

January 31: 5,500

February 28: 5,800

March 31: 5,000

FX Rate, US$/JPY

January 5: 116.00

January 8: 114.00

January 15: 118.00

January 18: 120.00

January 31:119.00

February 5: 115.00

February 8: 111.00

February 28:116.00

March 31: 118.00

Functional Currency

US$

Prepare

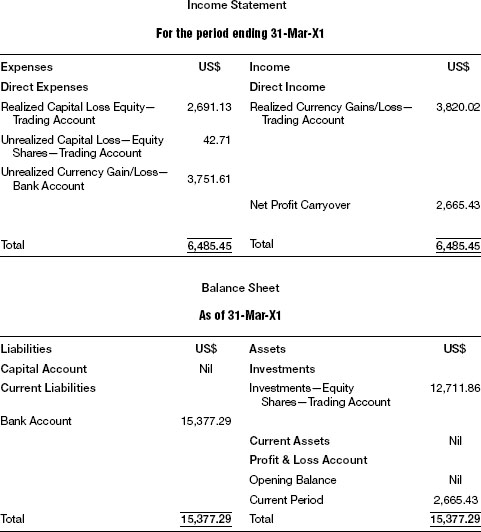

Journal entries, general ledgers, trial balance, income statement, and balance sheet.

Solution—Long Equity Shares, Trade Currency JPY

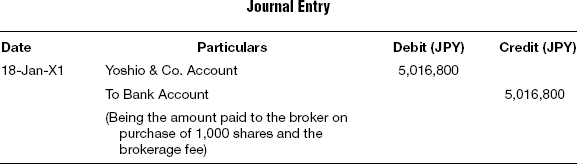

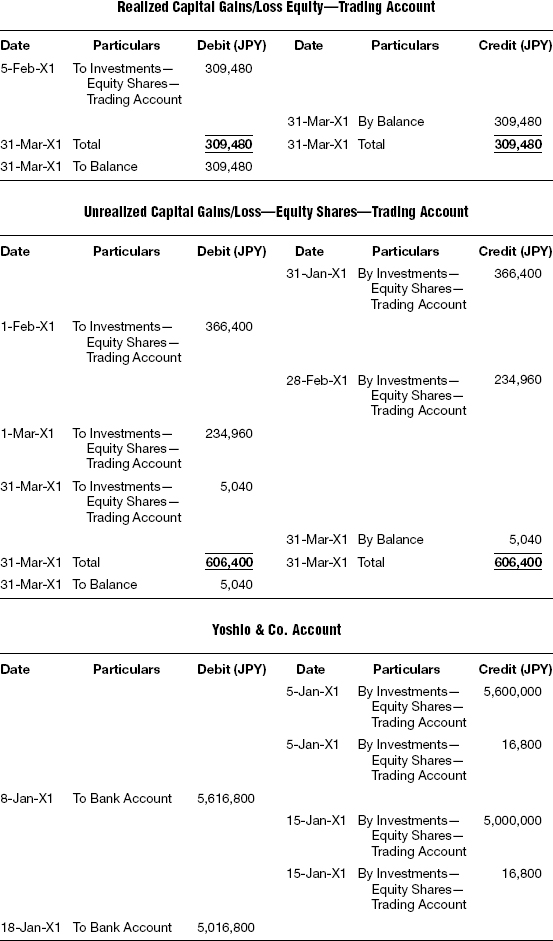

T-1 On Purchase of Equity Shares and Brokerage

T-2 On Payment of Contracted Sum

T-3 On Purchase of Equity Shares and Brokerage

T-4 On Payment of Contracted Sum

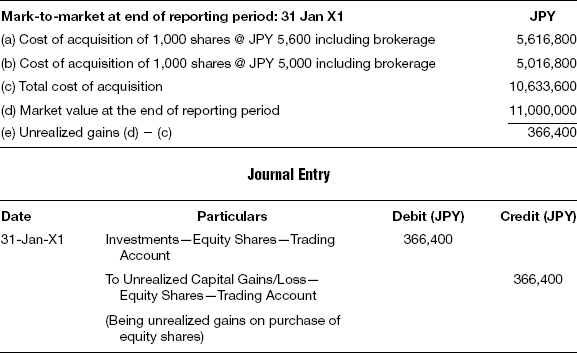

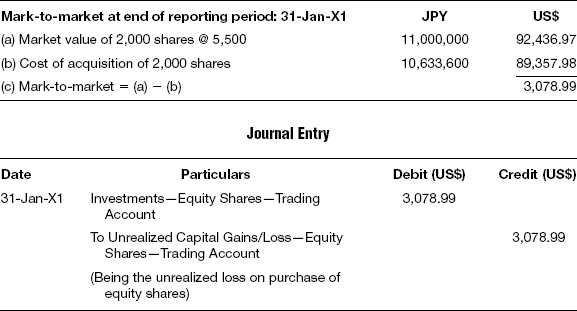

T-5 Mark-to-market End of Reporting Period

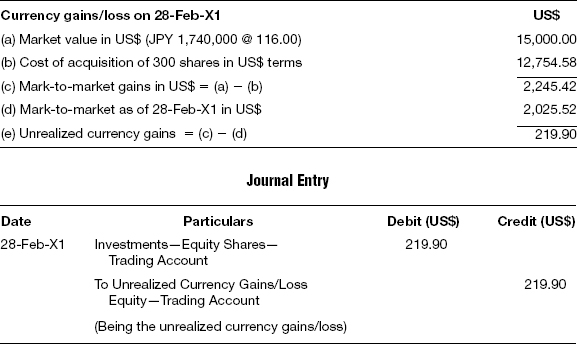

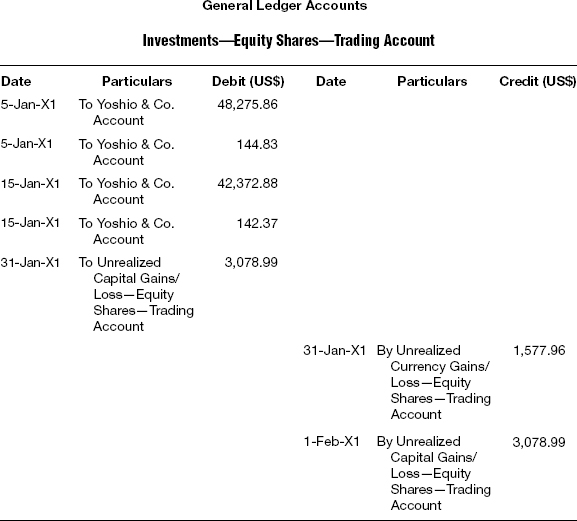

The total long position adds up to 2,000 shares and the market value of the shares is compared with the original cost of acquisition including brokerage to arrive at the mark-to-market. The market rate at the end of the reporting period is more than the cost of acquisition, resulting in mark-to-market gains, which is reflected as an increase in the value of the investments. Since the shares are held in the trading category, the gains are taken to the profit and loss account.

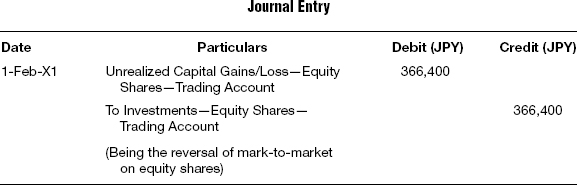

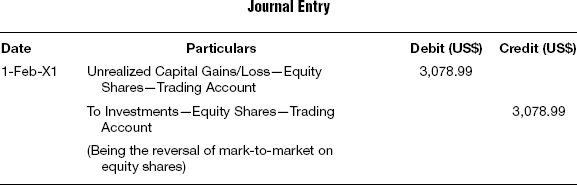

T-6 Reversal of Mark-to-market Entry

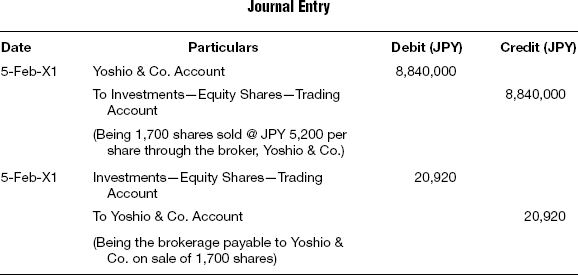

T-7 On Sale of Shares and Brokerage

T-8 Recording the Profit/Loss on Sale of Shares

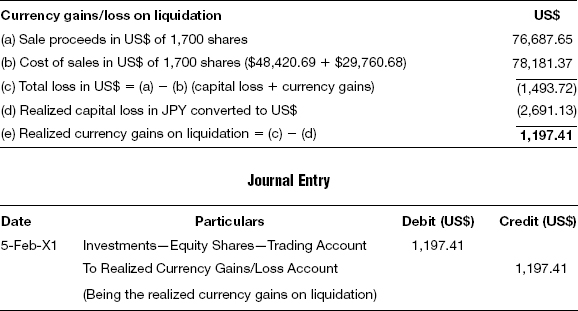

The liquidation methodology is first in, first out (FIFO); hence, the cost of acquisition of 1,700 shares is first arrived at and compared with the net sales realization to arrive at the realized gains on liquidation.

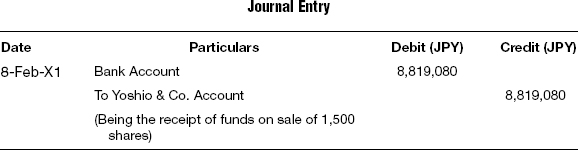

T-9 On Receipt of Contracted Sum

T-10 Mark-to-market at End of Reporting Period

T-11 Reversal of Mark-to-market Entry

T-12 Mark-to-market at End of Reporting Period

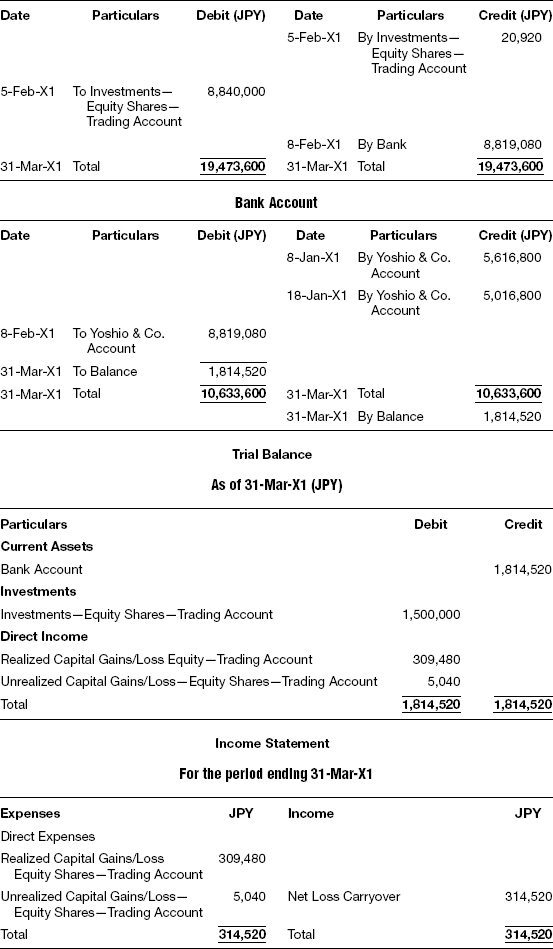

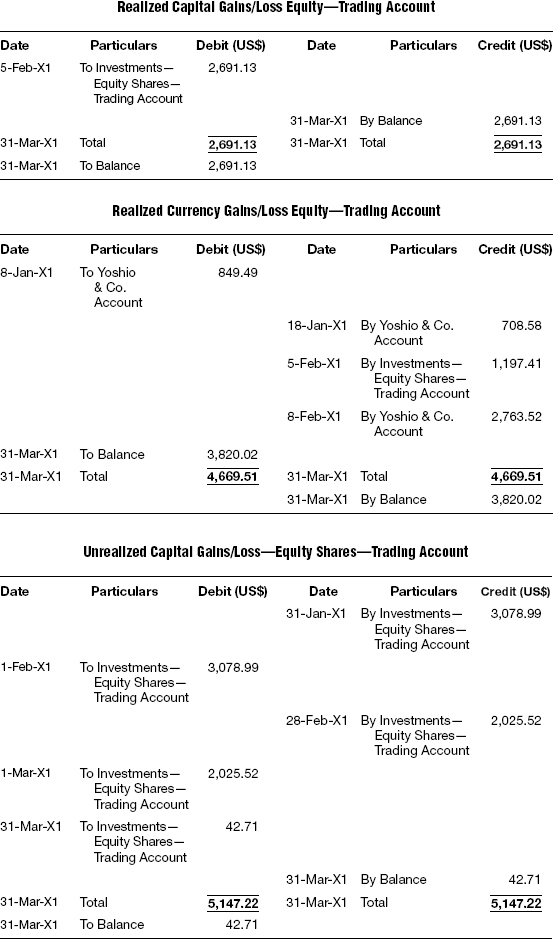

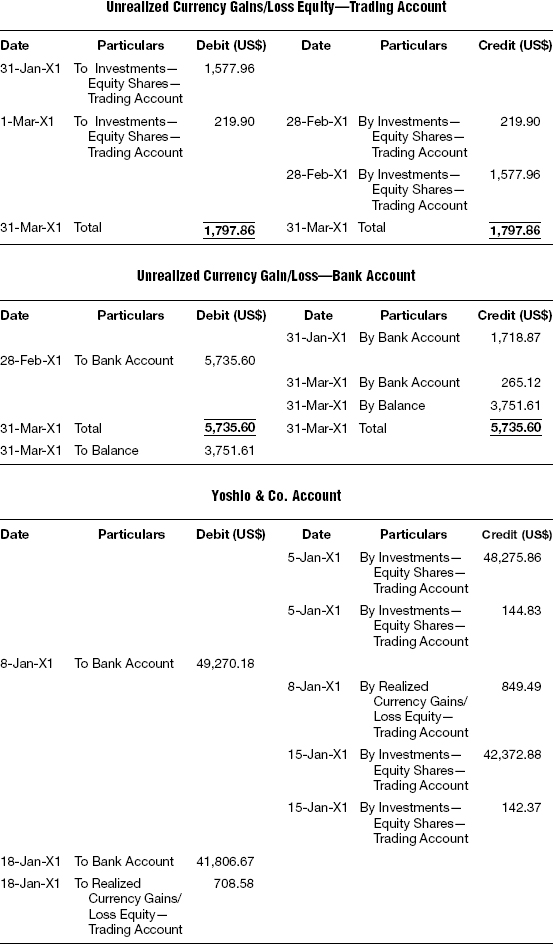

Long Equity Shares, Functional Currency US$

The following are the FX revaluation entries in the functional currency converted at the respective FX rate, which is given within parenthesis. FX translation entries are clearly specified, indicating whether each is a consummated FX translation entry or a transient FX translation entry.

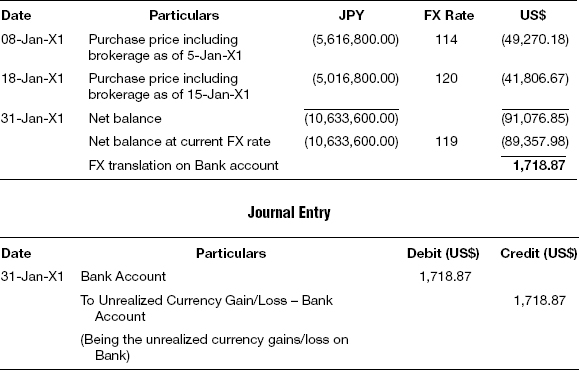

F-1 On Purchase of Equity Shares and Brokerage (T-1 @ FX Rate: 116.00)

F-2 On Payment of Contracted Sum (T-2 @ FX Rate: 114.00)

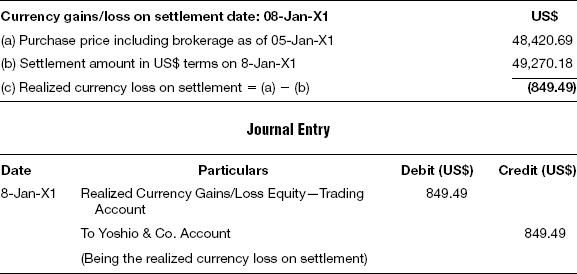

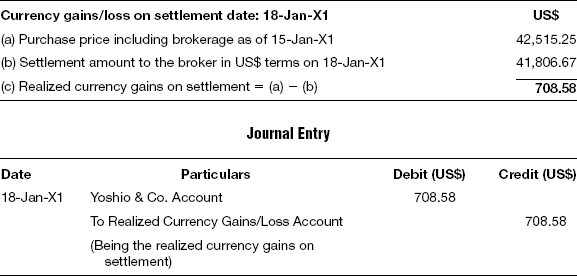

F-3 Recording the Currency Gains/Loss on Settlement of Broker (Consummated FX Translation Entry)

The settlement amount when converted into US$ based on the FX rate on the date of settlement results in a different amount than the contracted amount in US$ terms. This represents the currency gains or loss and is taken directly to the profit and loss account. If this FX translation entry is not passed, then the liability account of the broker will continue to have a balance even though the broker is settled in full in the respective local currency.

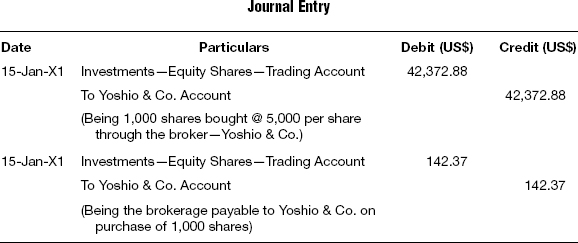

F-4 On Purchase of Equity Shares and Brokerage (T-3 @ FX Rate: 118.00)

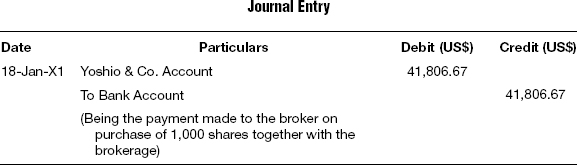

F-5 Payment of Contracted Sum (T-4 @ FX Rate: 120.00)

F-6 On Recording Currency Gains/Loss on Settlement to Broker (Consummated FX Translation Entry)

The settlement amount when converted into US$ based on the FX rate on the date of settlement results in a different amount than the contracted amount in US$ terms. This represents the currency gains or loss and is taken directly to the profit and loss account. If this FX translation entry is not passed, then the liability account of the broker will continue to have a balance even though the broker is settled in full in the respective local currency.

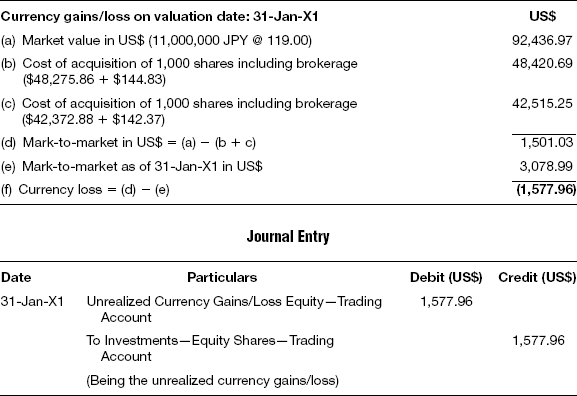

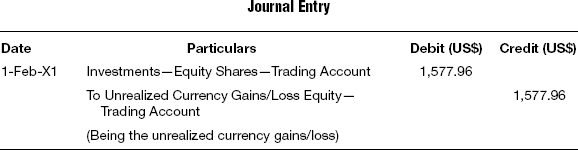

F-7 Mark-to-market at End of Reporting Period (T-5 @ FX Rate: 119.00)

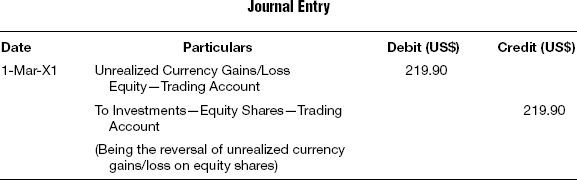

F-8 Reversal of Mark-to-market Entry (T-6 @ FX Rate: 119.00)

F-9 Currency Gains/Loss—FX (Transient FX Translation Entry)

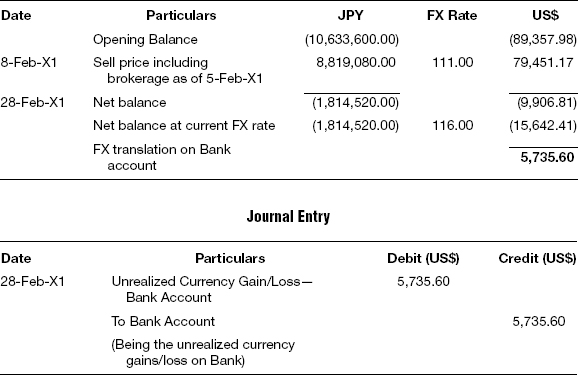

F-10 Reversal of Mark-to-market Entry

F-11 Currency Gains/Loss—Bank FX (Transient FX translation entry)

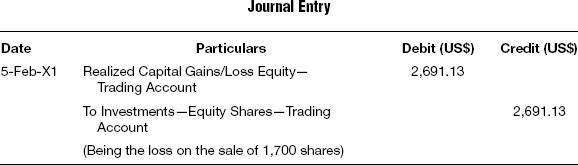

F-12 On Sale of Shares and Brokerage (T-7 @ FX Rate: 115.00)

F-13 On Recording the Profit/Loss on Sale of Shares (T-8 @ FX Rate: 115.00)

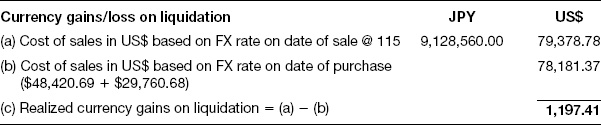

F-14 On Recording Realized Currency Gains/Loss on Liquidation (Consummated FX Translation Entry)

The total realized loss in US$ terms on this liquidation amounts to $1,493.72. Even though we are able to arrive at this number directly by subtracting the cost of sales from the net sale proceeds, there is no direct journal entry passed for this amount. Instead, the capital loss amounting to US$2,691.13 is accounted for and, due to favorable FX movement, the realized currency gain is accounted for separately, amounting to US$1,197.41. Adding these together results in a net realized loss of $1,493.72.

This calculation can also be counter-checked with the following table where the total capital loss is first arrived at, and from that the realized capital loss component is subtracted.

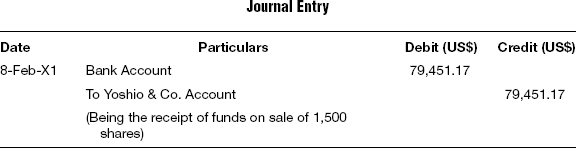

F-15 On Receipt of the Contracted Sum (T-9 @ FX Rate: 111.00)

F-16 Currency Gains/Loss on Settlement from Broker (Consummated FX Translation Entry)

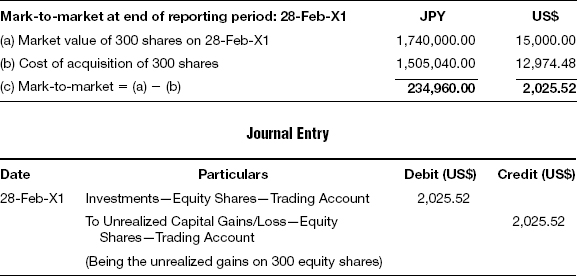

F-17 Mark-to-market at End of Reporting Period (T-10 @ FX Rate: 116.00)

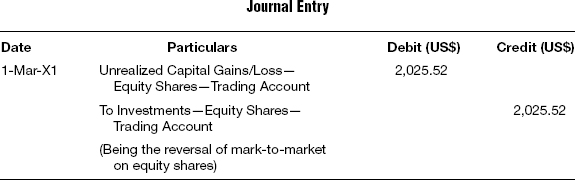

F-18 Reversal of Mark-to-market Entry (T-11 @ FX Rate: 116.00)

F-19 Currency Gains/Loss—FX (Transient FX Translation Entry)

F-20 Reversal of Mark-to-market Entry

F-21 Currency Gains/Loss—Bank FX (Transient FX translation entry)

F-22 Mark-to-market at End of Reporting Period (T-12 @ FX Rate: 118.00)

F-23 Currency Gains/Loss—Bank FX (Transient FX translation entry)

- Equity securities are represented by ownership shares as common stock or preferred stock, rights to acquire ownership shares such as stock warrants or rights, or call options. The category also includes rights to dispose of ownership in shares by way of put options.

- Equity security is defined in FAS 115 as any security representing an ownership interest in an enterprise (for example, common, preferred, or other capital stock) or the right to acquire (for example, warrants, rights, and call options) or dispose of (for example, put options) an ownership interest in an enterprise at fixed or determinable prices. However, the term does not include convertible debt or preferred stock that by its terms either must be redeemed by the issuing enterprise or is redeemable at the option of the investor. The definition does not include redeemable preference shares.

- Under the trade date accounting method, both the asset and the liability for the asset purchased are recognized on the date of trade and the payable is derecognized once the payment is made.

- Under the settlement date accounting method, the entire transaction is recognized only on the date of settlement. While FAS 115 is silent as to the date on which the transaction should be recorded, the other levels of U.S. GAAP literature require trade date accounting to be followed for regular-way securities contracts, especially for broker-dealers and investment companies.

- For regular-way contracts, the IASB gives the option to follow either trade date accounting or settlement date accounting, provided that one is followed consistently for purchases and sales of financial assets in the same category. However, the changes in the fair value of the asset should be treated properly depending upon the classification of the asset acquired.

- Investments in equity securities that are purchased and held principally for the purpose of generating gains on resale are classified as trading securities. Investments in equity securities that are not trading securities are classified as available-for-sale (AFS) securities.

- Trading securities are normally held by banks and other financial institutions that engage in active buying and selling of securities with a view to make gains on trading. The mark-to-market process values the securities at market rates, recording the unrealized gains/loss on such securities.

- When the investor invests in equity securities just to utilize the idle cash, without any intention to hold it for a long period or without any intention to generate gains on current resale, then such investments in equity securities are classified as available-for-sale securities.

- Where the investor owns between 20 and 50 percent of the equity of the investee company, then the investor is presumed to have a significant influence in the operating and financial decisions of the investee company.

- When the investor acquires more than 50 percent of the outstanding voting stock of the investee company, then the investor has controlling interest because of its majority ownership of the voting stock. Investments of this nature will necessitate the preparation of consolidated financial statements.

- The currency of the primary economic environment in which the investor operates is the functional currency. The financial accounting records should be maintained in the functional currency and the investor is not free to choose the same. The investor’s investment activities and the currency in which the fund raises money from investors predominantly determine the functional currency. Presentation currency is the currency in which the financial statements are presented to the investors.

- For assets and liabilities, the exchange rate at the balance sheet date is used to translate foreign currency statements into the functional currency.

- For revenues, expenses, gains, and losses, the exchange rate at the dates on which such revenue or expense is recognized is used.

- If the reporting currency is different from the trading currency, then every journal entry recorded is first revalued in the reporting currency, based on the market quote available for the trade currency.

- On the reporting date, all the assets and liabilities of the investor that are designated in foreign currency should be converted into the functional currency based on the official FX conversion rates on the reporting date. This is achieved by the FX revaluation process.

- As per the U.S. GAAP Statement of Position (SOP) 93-4, it is not mandatory to show the capital gains/loss due to change in the market rate of the asset and currency gains/loss due to change in the foreign exchange rate separately, even though the SOP indicates that such separate reporting would provide valuable information to the users of the financial statements.

Theory Questions

1. Define equity shares as per the accounting standard FAS 115.

2. How are passive investments classified for accounting purposes?

3. What is readily determinable fair value as per FAS 115?

4. What is the fundamental difference between the trading and available-for-sale classifications of equity investments?

5. When is an investor supposed to have significant influence on the investee company, and what is the method of accounting for such investments?

6. Controlling interest is acquired if an investor holds more than 50 percent—is this statement true? Discuss your answer with examples.

7. What are the main differences between exchange-traded securities and over-the-counter securities?

8. Explain in brief the functions and functioning of stock exchanges.

9. List the various events during the trade life cycle for equity shares that are held as trading, along with the accounting entries to be recorded.

10. What are corporate actions and what is their impact with regards to accounting?

11. Commissions and other expenses for acquiring the shares are treated as part of the cost of the equity—is this true, and if so, what are the exceptions?

12. What are the differences between trade date accounting and settlement date accounting?

13. What is the reversal journal entry for mark-to-market?

14. Explain the process of FX revaluation and FX translation. What are the differences between the two?

15. What is meant by functional currency and how it is determined?

16. How do you distinguish between capital gains and currency gains due to fluctuation in foreign exchange rate? Is it mandatory to divulge the two gains separately?

Objective Questions

1. The equity method of accounting is adopted in:

a. Controlling interest

b. Significant influence

c. Passive investments

d. None of the above

2. In trade date accounting, a liability payable for acquiring the asset will be recorded on:

a. The trade date

b. The reporting date

c. The settlement date

d. All of the above

3. A broker-dealer who records the transactions on settlement date basis should compute the net capital on:

a. The trade date

b. The reporting date

c. The settlement date

d. Any of the above

4. The definition of equity security as per FAS 115 does not apply to:

a. Investment companies

b. Nonprofit organizations

c. Brokers and dealers in securities

d. All of the above

5. The shareholder will recognize the dividend income:

a. On the date of dividend declaration

b. On the ex-dividend date

c. At the end of accounting period

d. None of the above

6. A shareholder is said to have controlling interest in the company if he holds:

a. Less than 20 percent shares of the investee company

b. From 20 to 50 percent shares of the investee company

c. More than 50 percent shares of the investee company

d. None of the above

7. Unrealized gains or loss computed for available-for-sale (AFS) securities will be reported as:

a. Income/loss on the income statement

b. Other comprehensive income

c. Dividend income

d. None of the above

8. For private equity investment, the responsibility of fulfillment of the obligation is vested with:

a. The stock exchange

b. The broker

c. The seller

d. All of the above

9. If the net holding of any share is negative, then it is referred to as:

a. Available-for-sale (AFS)

b. A long position

c. A short position

d. Trading securities

10. Under the incremental value method, mark-to-market entry is reversed:

a. On T + 2

b. At the end of the accounting period

c. On the next valuation date

d. None of the above

11. The fair value of securities that are listed and traded through stock exchanges is determined based on:

a. The highest bid price quoted on the exchange for each day

b. Market quotes at the end of each day

c. Market quotes at the opening of each day

d. The forecasted price received from stock broker

e. The average price of the high and low recorded in the exchange

12. In private equity investments where the trade is executed over-the-counter, who among the following will be the actual counterparty?

a. The stock exchange in which the stock is listed

b. The buyer

c. The seller

d. The custodian bank

e. The broker

13. When the net holding of any given share is shown in negative value, it refers to:

a. Quantity of short position

b. Loss from long position

c. Unrealized loss from short position

d. Quantity of long position

e. Dividend receivable

14. For exchange-traded securities, the delivery of the securities either in physical or in electronic form takes place:

a. When the trade is booked

b. When the broker confirms the receipt of payment

c. Immediately after the payment is received by the stock exchange

d. On T + 1

e. At a predetermined future date

15. When a company announces a dividend, who is entitled to receive it?

a. An investor listed as holder of stock as of the dividend declaration date

b. An investor listed as holder of stock as of the ex-dividend date

c. An investor listed as holder of stock as of the day before ex-dividend date

d. An investor listed as holder of stock as of the record date

e. An investor listed as holder of stock as of the dividend payment date

16. If an investor buys 1,000 shares at $50 and the initial margin is 60 percent and the maintenance margin is 30 percent, he will receive the first marginal call when the stock price falls below:

a. $14.00

b. $21.00

c. $28.57

d. $49.99

Journal Questions

Journalize the following transactions.

1. Michael James bought 8,500 shares of NovoSotia on April 15 for $12 per share. On the same day, the closing price of NovoSotia was $11.45 per share. Calculate the unrealized gains/loss at end of day and pass the journal entry.

2. On April 24, he sold 4,000 shares of NovoSotia at $14 per share. Pass necessary journal entries to record the sale of these shares and also the subsequent realized/unrealized gain or loss as of that date. The closing rate of NovoSotia shares on April 24 is $13.60.

3. On May 31, NovoSotia declared a dividend of $1 per share with record date of April 20. On June 10, the payment was made. Calculate the dividend amount received by Michael James and also pass entries for dividend declaration and actual receipt of such dividend.

4. On June 25, Mr. James bought an additional 2,000 shares of NovoSotia at $16 per share. On July 28, he sold another 4,000 shares at $14.65 per share. Mr. James follows the last in, first out (LIFO) method and the shares were held for trading purposes. Calculate the realized gains or loss and pass entry to give the effect for the same.

5. Prepare realized/unrealized gains and loss account (ledger account) giving effect to the preceding transactions.

Trading Securities: Foreign Currency—HKD

For the following scenario, prepare journal entries, general ledgers, trial balances, income statements, and balance sheets.

James Trading Inc. traded in Avichina Industry shares in a Hong Kong stock exchange through Nomura Securities brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

FIFO

Market Rate of Avichina Industry Shares in HKD

January 31: 1.28.

February 28: 1.42.

March 31: 1.55.

FX Rate: US$/HKD

January 8: 7.72

January 11: 7.79

January 12: 7.69

January 15: 7.90

January 31: 7.83

February 15: 7.75

February 18: 7.81

February 28: 7.76

March 31: 7.99

Functional Currency

US$

Trading Securities: Foreign Currency—IDR

For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet.

Jakarta Trading Fund traded in PT. Perusahaan Gas shares in a Hong Kong stock exchange through Vickers & Co. brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

FIFO

Market Rate of PT. Perusahaan Shares in IDR

January 31: 10,101.10

February 28: 10,800.42

March 31: 10,255.15

FX Rate: US$/IDR

January 5: 9,013

January 8: 9,040

January 15: 9,115

January 18: 9,102

January 31: 9,100

February 5: 9,070

February 8: 9,109

February 28: 9,120

March 31: 9,125

Functional Currency

US$

Trading Securities: Foreign Currency—PKR

For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet.

Karachi Overseas Fund traded in Adamjee Insurance shares in the Pakistan stock exchange through Auerbach & Co. brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

FIFO

Market Rate of Adamjee Insurance Shares in PKR

February 28: 190

March 31: 185

April 30: 205

FX Rate: US$/PKR

February 15: 60.81

February 18: 60.68

February 28: 60.71

March 15: 60.75

March 18: 60.72

March 31: 60.73

April 30: 60.78

Functional Currency

US$

Trading Securities: Foreign Currency—JPY

For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet.

Itochu Capital Japan Fund traded in Nissan shares in the Nikkei through Akita Mori brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

FIFO

Market Rate of Nissan Shares in JPY

February 28: 1,620

March 31: 1,800

April 30: 1,760

FX Rate: US$/JPY

February 11: 104.50

February 14: 104.75

February 28: 104.85

March 20: 105.25

March 23: 105.35

March 31: 105.00

April 30: 105.50

Functional Currency

US$