CHAPTER 3

Accounting for Equity Investments: Available-for-Sale

After studying this chapter, you should have a grasp of the following:

- Accounting standards for equity investments held as available-for-sale (AFS).

- Basic understanding of available-for-sale securities.

- Trade life cycle for equity investments held as available-for-sale.

- Journal entries to be recorded during the different phases of the trade life cycle.

- FX translation on available-for-sale securities.

- Impairment of AFS securities.

- Illustration of investments in equity shares held as available-for-sale.

- Preparation of journal entries and general ledger accounts.

- Preparation of income statement and balance sheet after the equity investments are made.

- Illustration of available-for-sale investments in foreign currency.

ACCOUNTING STANDARDS FOR EQUITY INVESTMENTS: AVAILABLE-FOR-SALE

According to the accounting standards, available-for-sale financial assets are those non-derivative financial assets that are designated as available-for-sale or are not classified as one of the following:

- Loans and receivables.

- Held-to-maturity investments.

- Financial assets at fair value through profit or loss.

Thus, equity instruments that are not designated as financial assets at fair value through profit or loss are categorized as available-for-sale instruments. Additionally, investments in equity instruments that do not have a quoted market price in an active market, and whose fair value cannot be reliably measured, should not be designated as at fair value through profit or loss, and such instruments are designated as available-for-sale securities.

Relevant Accounting Standards

| U.S. GAAP | IFRS |

| FAS 52—Foreign Currency Translation FAS 94—Consolidation of All Majority-owned Subsidiaries FAS 109—Accounting for Income Taxes FAS 115—Accounting for Certain Investments in Debt and Equity Securities FAS 130—Reporting Comprehensive Income FAS 157—Fair Value Measurements FAS 159—The Fair Value Option for Financial Assets and Financial Liabilities |

IFRS 7—Financial Instruments: Disclosure IAS 21—The Effects of Changes in Foreign Exchange Rates IAS 32—Financial Instruments: Presentation IAS 36—Impairment of Assets IAS 39—Financial Instruments: Recognition and Measurement |

Available-for-sale securities are debt or equity investments that are held for an indefinite period of time without any intention to resell for profit. They are not trading assets as in the case of short-term assets held for speculation, nor are they acquired with an intention to hold till maturity. In the case of equity securities, there is no concept of holding till maturity. Hence, whatever investments in equity are acquired without any intention to resell for profit are classified as available-for-sale (AFS) securities. Thus, AFS securities are a hybrid. While AFS securities are recorded at fair value or market value, the unrealized gains/losses on them are excluded from current earnings (P&L) and are instead recorded as an adjustment to equity on the balance sheet.

The AFS category includes all equity securities except those classified as fair value through profit or loss (FPVL). Available-for-sale financial assets are carried at fair value subsequent to initial recognition. Usually the fair value can be readily determined for most financial assets through an active market or by a reasonable estimation process. The exception to this rule is equity securities that are not actively traded and hence do not have a quoted market price for arriving at a reliable fair value. Such instruments, however, are measured at cost instead of fair value.

For available-for-sale financial assets, unrealized gains and losses are deferred until they are realized or impairment occurs. The unrealized gains on such financial assets are shown as other comprehensive income and adjusted directly in the equity without being routed through the income statement. Only interest income and dividend income, impairment losses, and certain foreign currency gains and losses are recognized in profit or loss.

THE TRADE LIFE CYCLE FOR AVAILABLE-FOR-SALE EQUITY

The trade life cycle for investment in equity securities that are designated as available-for-sale is identical to that given in Chapter 2 for trading securities, except that at the time of ascertaining the fair value at the end of the reporting period, the accounting entry that is recorded in the books of account is different. Also, when the equity securities classified as available-for-sale are sold, the realized gains/loss on such sale is transferred from the other comprehensive income (OCI) to the income statement and an entry is recorded to that effect. Thus, the two events in the trade life cycle which call for a different treatment than the ones given for trading securities are as follows:

1. Ascertain the fair value at the end of reporting period.

2. Ascertain the profit/loss on the sale and adjust OCI.

Overview of the Trade Life Cycle

Ascertain the Fair Value at the End of the Reporting Period

At the end of the reporting period, the fair value of the shares is ascertained and the shares are marked-to-market. The mark-to-market process adopted here is the same as the one followed for trading securities. However, if the market rate rises above the purchase rate, then such increase is recorded as part of the other comprehensive income and is not recognized as income in the current period. The other comprehensive income is shown as part of the shareholders’ equity in the balance sheet.

This accounting entry is reversed on the next valuation date when a fresh entry for the then value is recorded in the books of accounts. Alternatively, the accounting entry can also be recorded only for the incremental value. If the investor follows this incremental value method, there is no need to reverse any entry for mark-to-market recorded earlier.

The exception to this general rule is when there is a permanent impairment to the value of the securities held as available-for-sale. Such permanent impairment should be recognized in the income and as such should be part of the income statement. If the perceived permanent impairment is later recovered, such increase in the value of the investments need not be recorded in the books until the liquidation of such securities.

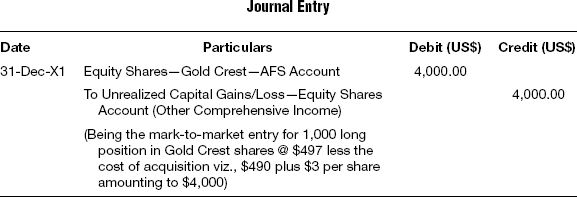

Assuming that the market rate of Gold Crest, which is held by the investor as available-for-sale investments, is valued at $497 as of December 31, the accounting entry that is recorded in the books of accounts is shown in the following journal entry.

Ascertain the Profit/Loss on the Sale and Adjust OCI

The profit or loss on liquidation of the shares is ascertained by deducting the cost of sales from the net sale consideration. Cost of sales is arrived at by following first in first out (FIFO), last in first out (LIFO), or the weighted average method. For available-for-sale securities the increase or decrease in the value of the investment is not reported as income until the same is liquidated. Hence, on liquidation, when the profit/loss on the liquidation is ascertained, the same is transferred from other comprehensive income to the income account.

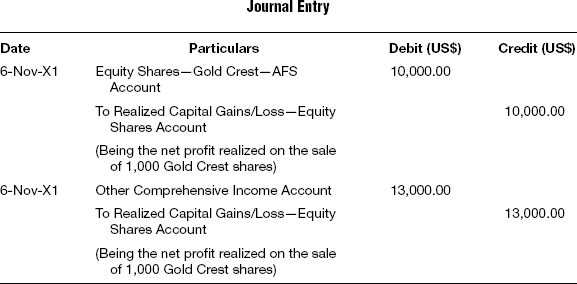

Assume that the Gold Crest shares are sold on November 6 for a consideration of $520 and a brokerage of $4 is incurred for the same, resulting in the net realization of $516 per share. Assume further that the Gold Crest shares were valued on October 31 at $510. Hence the profit on each share is $23 and the total profit for the entire lot amounts to $23,000. However, $13,000 would have been already credited to the OCI on October 31, being the previous valuation date. The profit/loss realized that is recognized on the date of liquidation should be taken to the income account, and the amount that was credited earlier to the OCI income account should be reversed.

The accounting entries that are recorded in the books of accounts are shown as follows:

FX TRANSLATION ON AFS SECURITIES

According to the accounting standards, equity instruments are nonmonetary items for the purpose of treatment of foreign exchange differences. Any foreign exchange gains and losses on monetary assets are recognized in the statement of profit and loss except for those items that are designated as hedging instruments. A monetary available-for-sale financial asset is treated as if it were carried at amortized cost in the foreign currency. This applies for debt instruments that are monetary assets. However, for nonmonetary assets such as equity instruments, the gain or loss, including any related foreign exchange component, is recognized directly in the appropriate equity account.

In the balance sheet, a nonmonetary financial asset such as an investment in an equity instrument is translated using the closing rate if it is carried at fair value in the foreign currency, and using a historical rate if it is not carried at fair value when its fair value cannot be reliably measured.

The entire change in the carrying amount of equity instruments held as available-for-sale, including the effect of changes in foreign currency rates, is reported in the equity account.

If an equity instrument measured at fair value with gains and losses recognized in the appropriate equity account becomes impaired, the cumulative net loss recognized in the equity account including any portion attributable to foreign currency changes should be recognized in the statement of profit and loss.

Illustration: AFS—Functional Currency

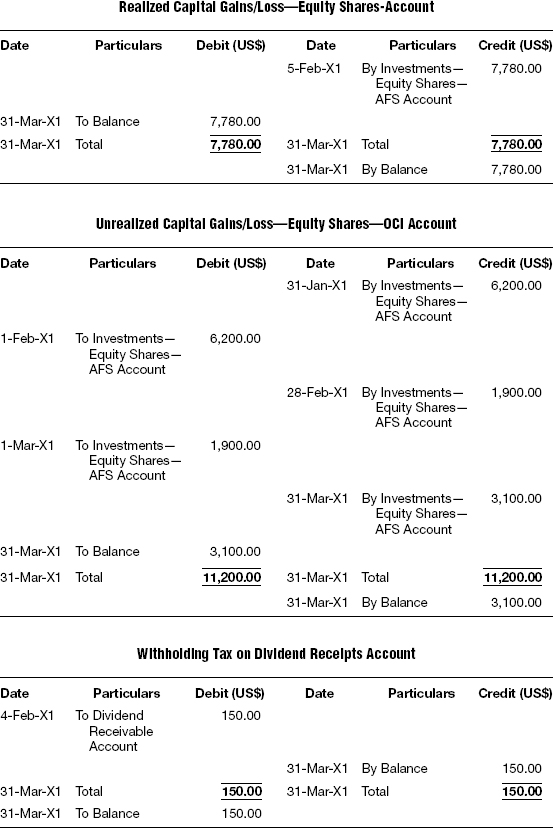

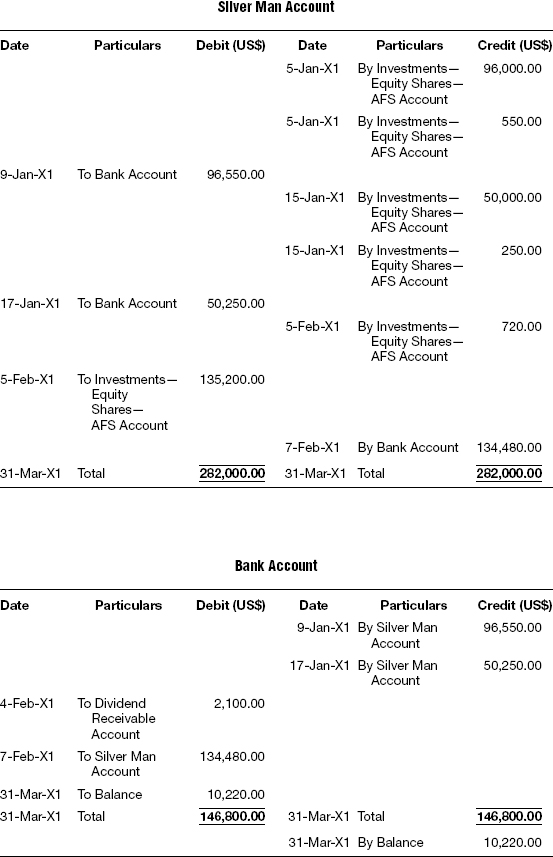

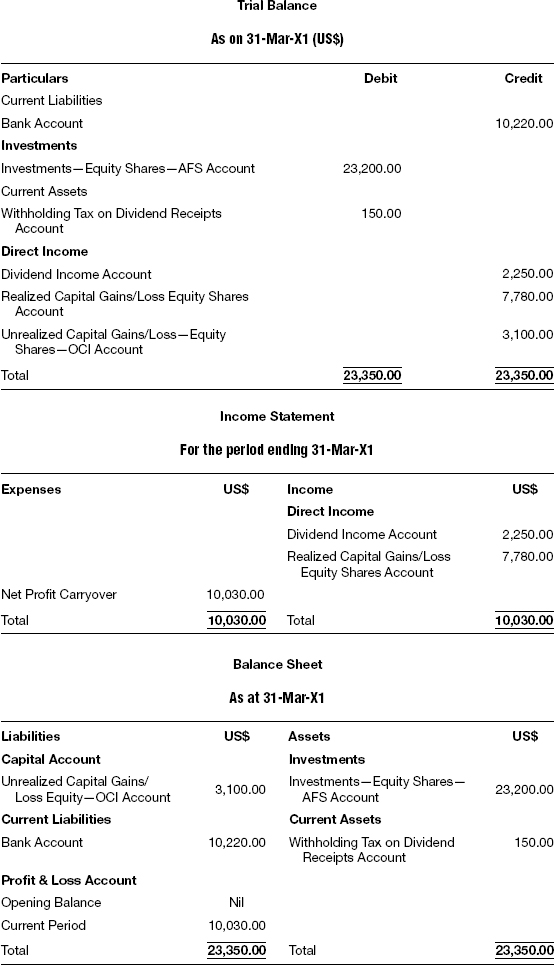

ABC Fund LLC traded in IBM shares at a U.S. stock exchange through Silver Man & Co. brokers, and the details are as follows:

Trade Details

Other Details

- Settlement: T + 2.

- Purchases on January 5 are settled on January 9 due to intervening holidays.

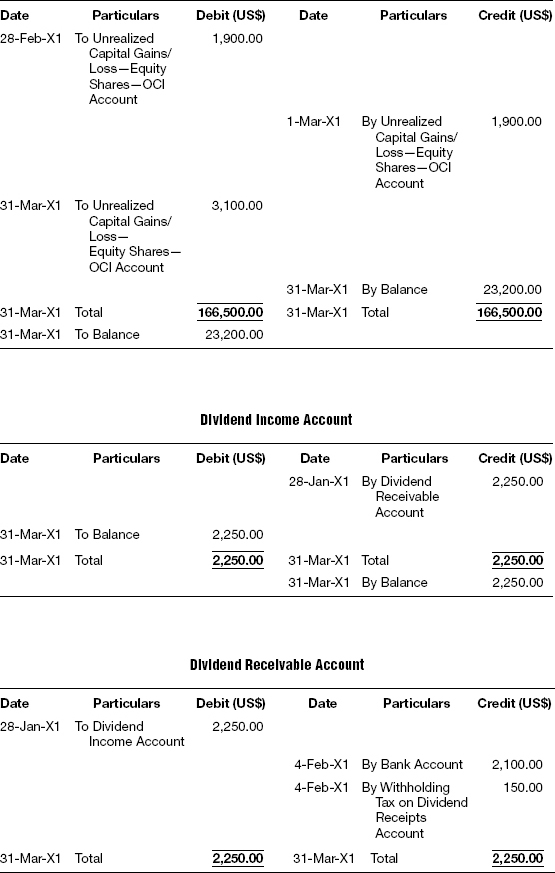

- January 28: A dividend at $0.75 per share is declared by IBM, $0.05 being the withholding tax.

- February 4: Dividend is paid by IBM.

Liquidation Method

First in first out (FIFO)

Market Rates

January 31: 51.00

February 28: 55.00

March 31: 58.00

Functional Currency

US$

Prepare

Journal entries, general ledgers, trial balance, income statement, and balance sheet.

Solution

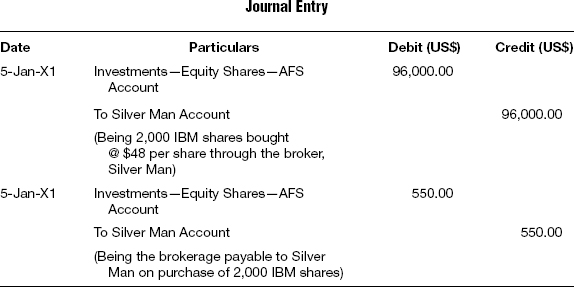

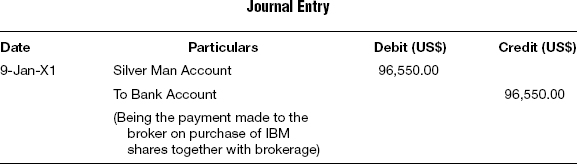

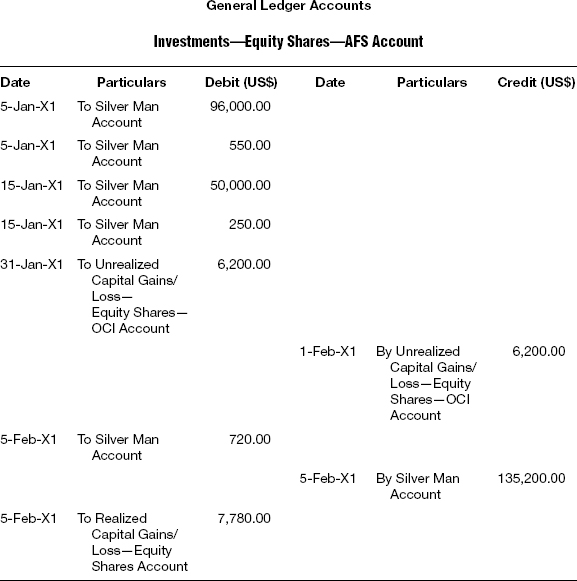

T-1 On Purchase of Shares and Payment of Brokerage

An investment in equity shares here is classified as available-for-sale. The brokerage paid is part of the cost of acquisition and hence the investment account is debited to account for the brokerage.

T-2 On Payment of Contracted Sum

T-3 On Purchase of Shares and Payment of Brokerage

T-4 On Payment of Contracted Sum

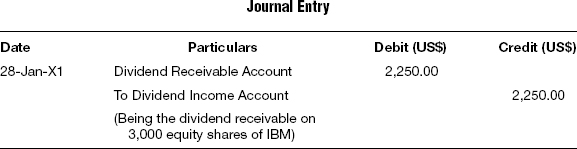

T-5 On Declaration of Dividend

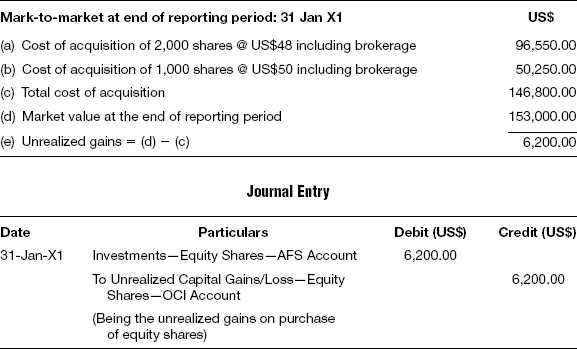

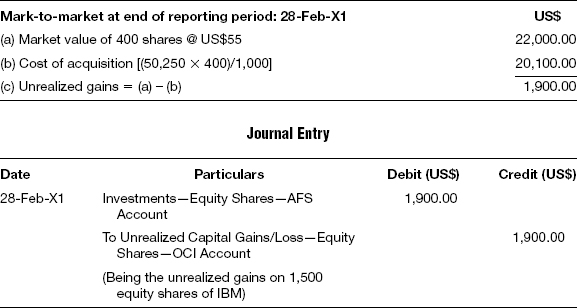

T-6 Mark-to-market at End of Reporting Period

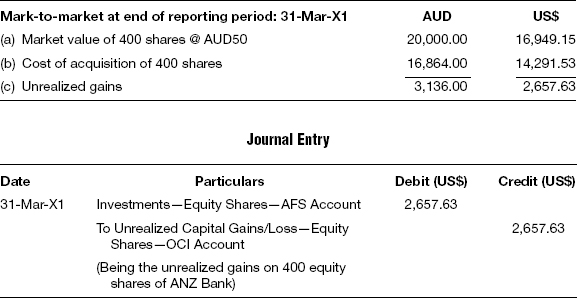

The total long position adds up to 3,000 shares and the market value of the shares is compared with the original cost of acquisition, including brokerage, to arrive at the mark-to-market. The market rate at the end of the reporting period is greater than the cost of acquisition, resulting in mark-to-market gains, which are reflected as an increase in the value of investments. Since the shares are held in the available-for-sale category, the gains are directly taken to the equity and are not routed through the profit and loss account.

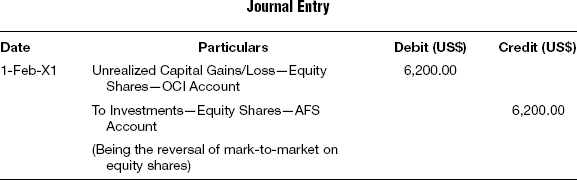

T-7 Reversal of Mark-to-market Entry

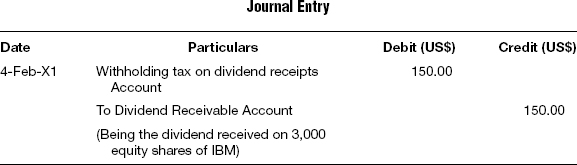

T-8 On Receipt of Dividend

T-9 Withholding Tax on Dividend

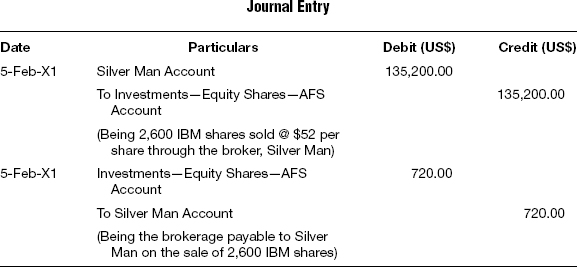

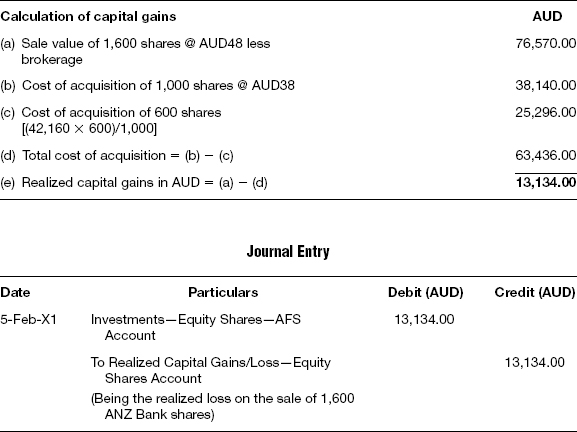

T-10 On Sale of Shares and Payment of Brokerage

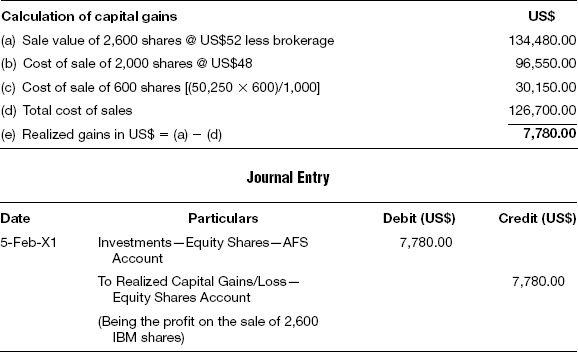

T-11 On Recording Profit/Loss on Sale of Shares

The liquidation methodology is first in, first out (FIFO) method. Hence the cost of acquisition of 2,600 shares is first arrived at and compared with the net sales realization to arrive at the realized gains on liquidation.

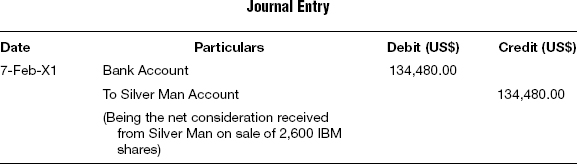

T-12 On Receipt of Contracted Sum

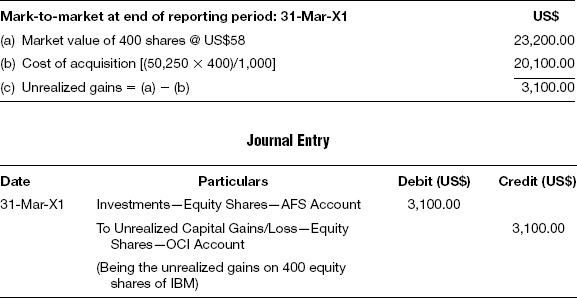

T-13 Mark-to-market at End of Reporting Period

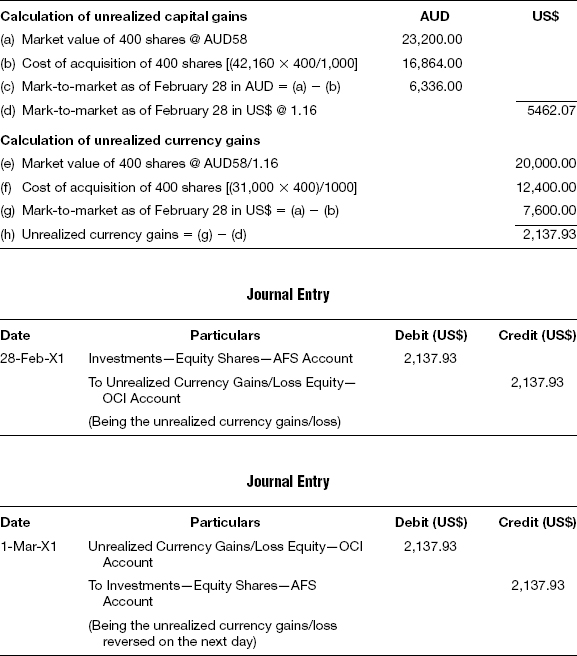

The net long position adds up to 400 shares and the market value of the shares is compared with the original cost of acquisition, including brokerage, to arrive at the mark-to-market. The market rate at the end of the reporting period is greater than the cost of acquisition, resulting in mark-to-market gains, which are reflected as an increase in the value of investments. Since the shares are held in the available-for-sale category, the gains are directly taken to the equity and are not routed through the profit and loss account.

T-14 Reversal of Mark-to-market Entry

T-15 Mark-to-market at End of Reporting Period

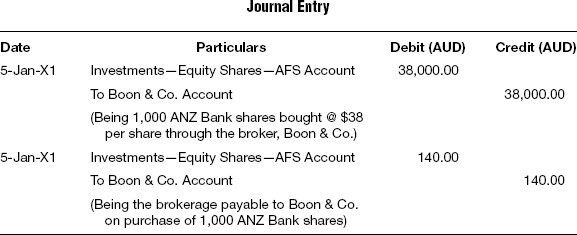

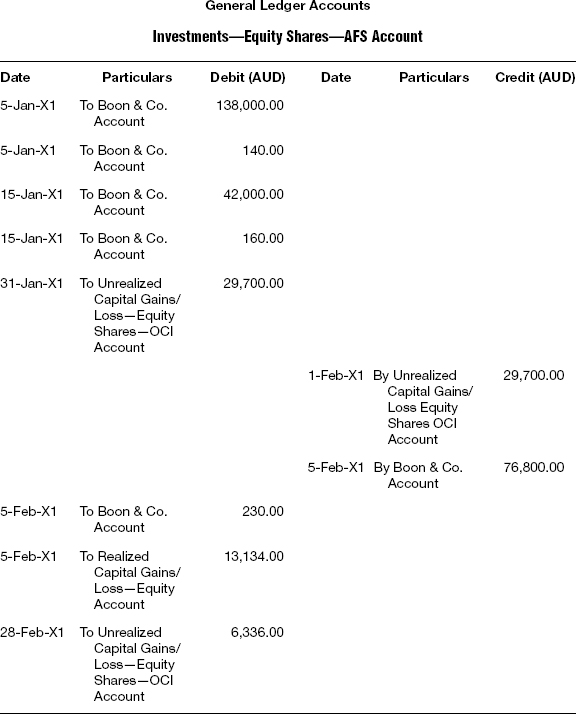

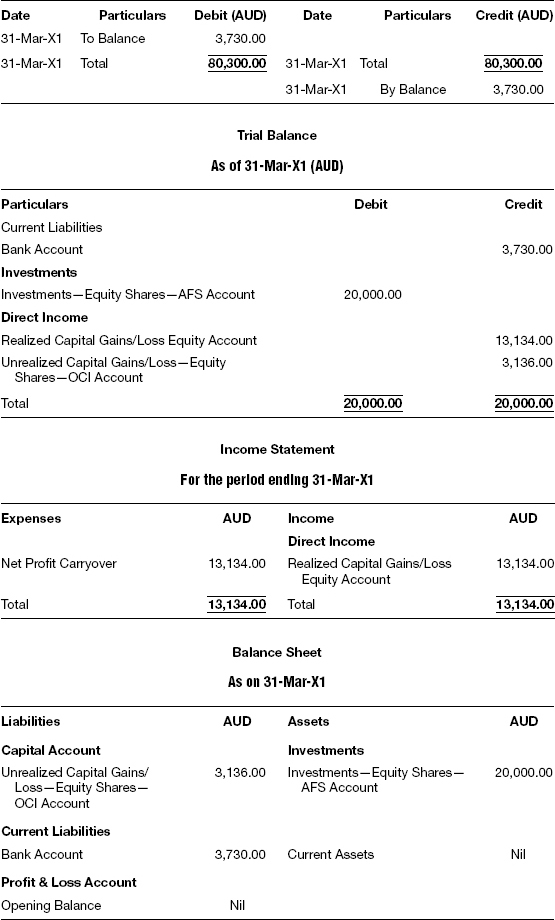

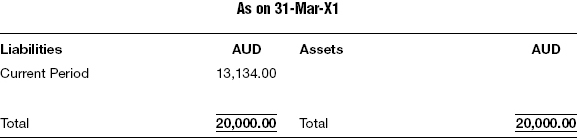

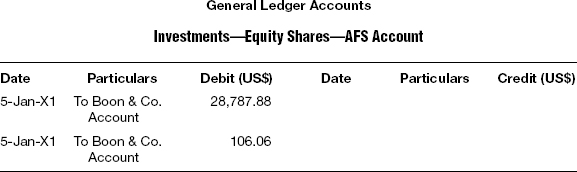

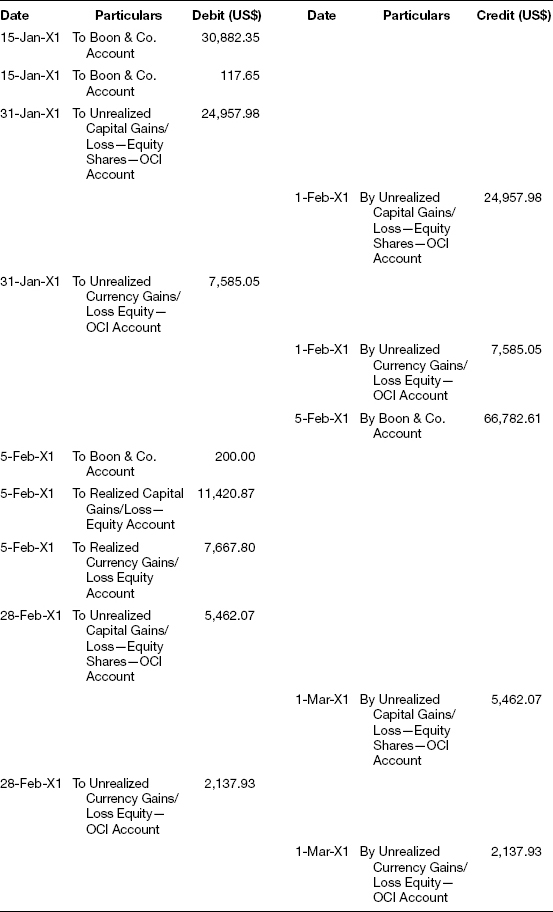

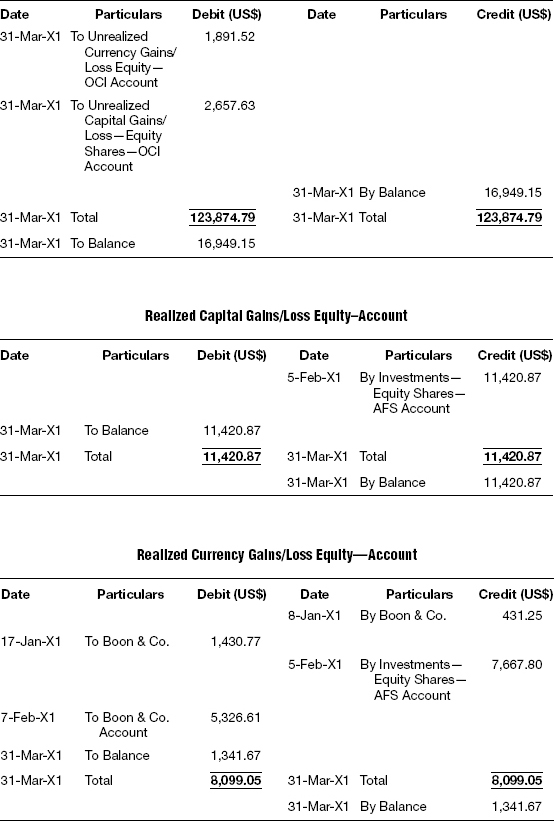

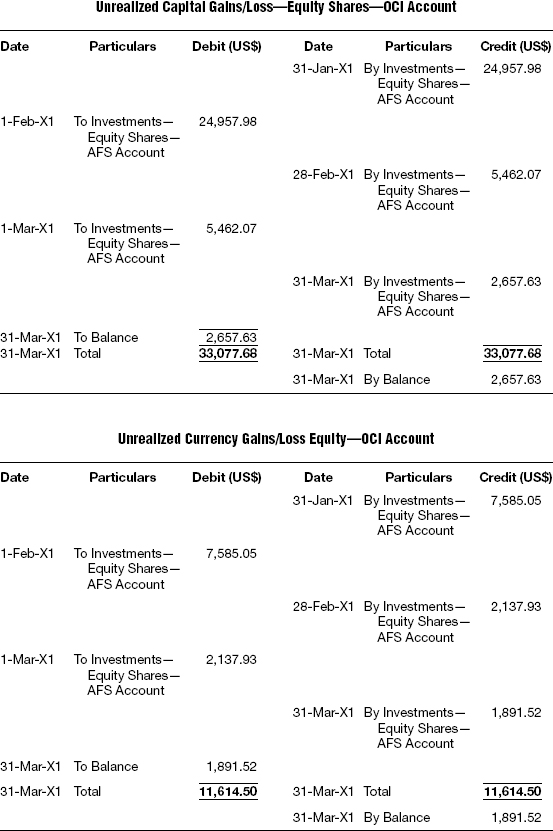

Illustration: AFS Securities—Trade Currency AUD

Sydney Long Term Fund traded in ANZ Bank shares in the Sydney stock exchange through Boon & Co. brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 2

Liquidation Method

FIFO

Market rate of ANZ Bank Shares in AUD

January 31: 55.00

February 28: 58.00

March 31: 50.00

FX Rate: US$/AUD

January 5: 1.32

January 7: 1.34

January 15: 1.36

January 17: 1.30

January 31: 1.19

February 1: 1.19

February 5: 1.15

February 7: 1.25

February 28: 1.16

March 1: 1.17

March 31: 1.18

Functional Currency

US$

Prepare

Journal entries, general ledgers, trial balance, income statement, and balance sheet.

Solution

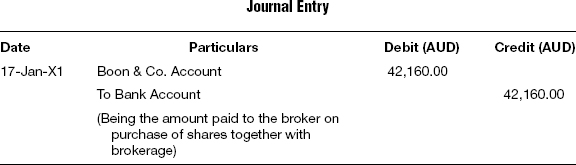

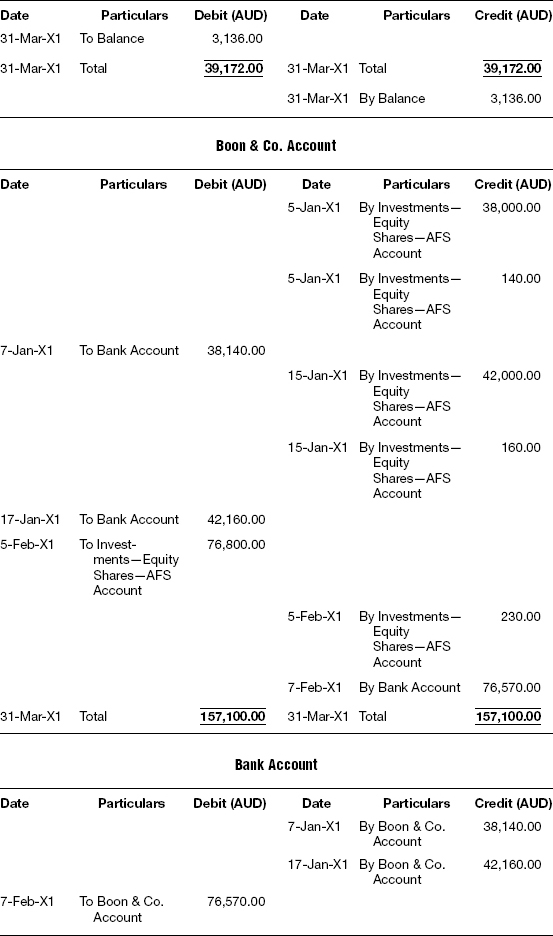

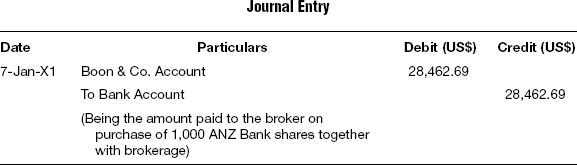

T-1 On Purchase of Shares and Payment of Brokerage

T-2 On Payment of Contracted Sum

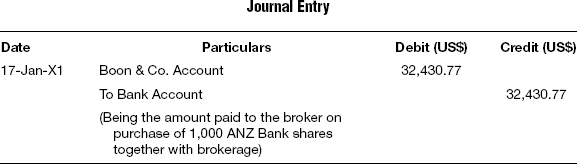

T-3 On Purchase of Shares and Payment of Brokerage

T-4 On Payment of Contracted Sum

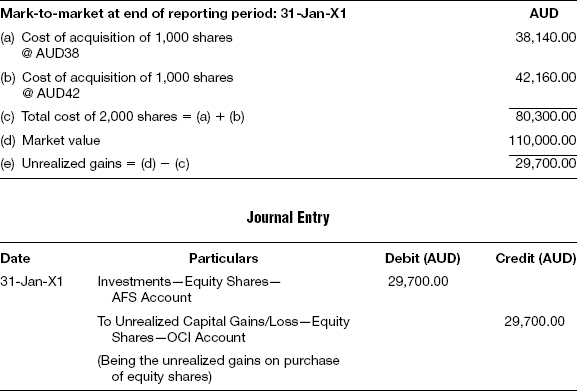

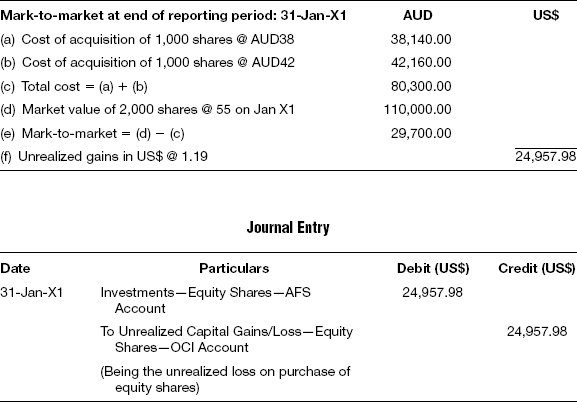

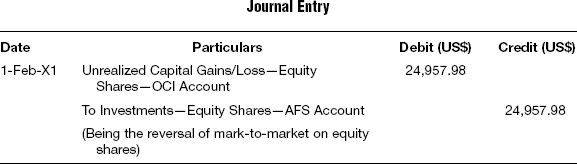

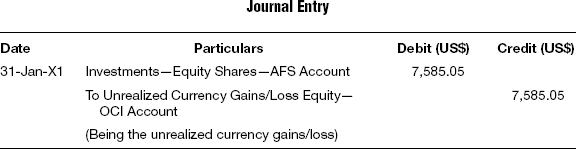

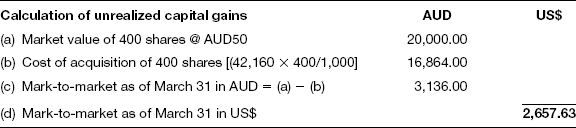

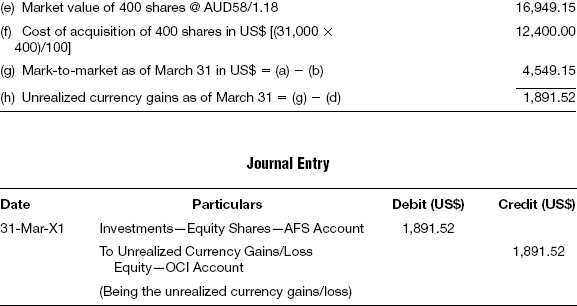

T-5 Mark-to-market at End of Reporting Period

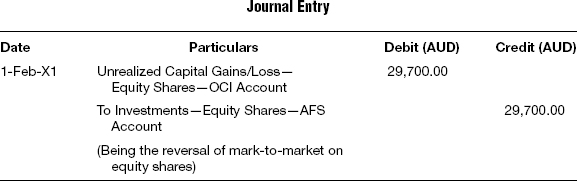

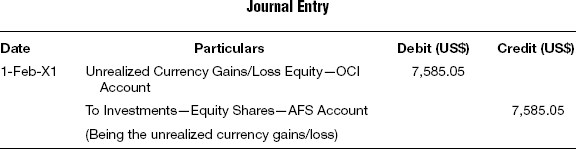

T-6 Reversal of Mark-to-market Entry

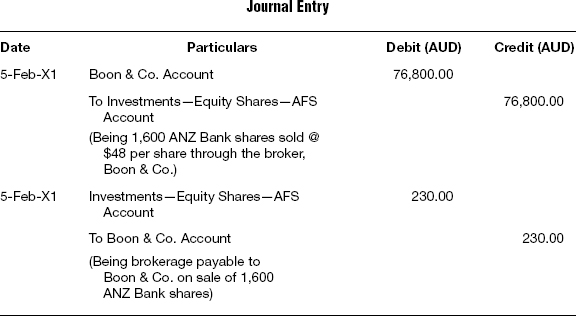

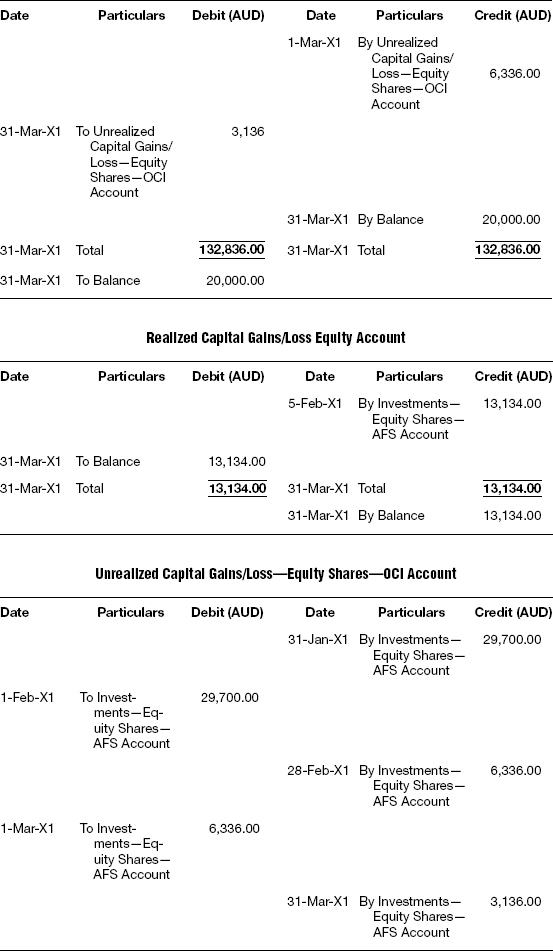

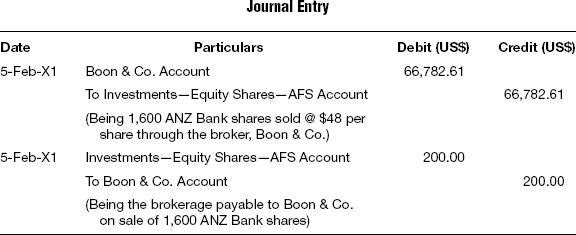

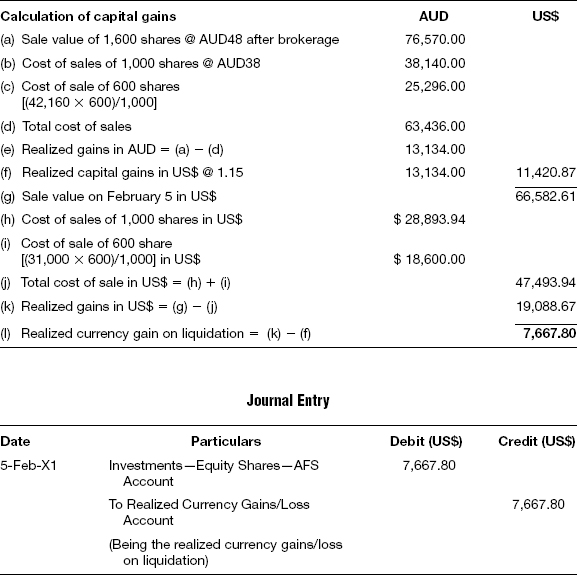

T-7 On Sale of Shares and Payment of Brokerage

T-8 Profit/Loss on Sale of Shares

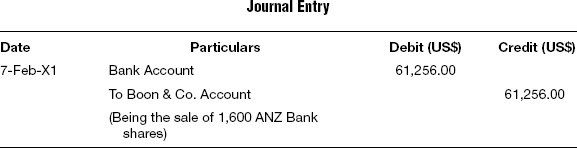

T-9 On Receipt of Contracted Sum

T-10 Mark-to-market at End of Reporting Period

T-11 Reversal of Mark-to-market

T-12 Mark-to-market at End of Reporting Period

Equity Shares AFS; Functional Currency US$

The following are the FX revaluation entries in the functional currency converted at the respective FX rate which is given within parentheses. FX translation entries are clearly specified, indicating whether each is a consummated FX translation entry or a transient FX translation entry.

F-1 On Purchase of the Shares (T-1 @ FX Rate: 1.32)

F-2 Payment of Contracted Sum (T-2 @ FX Rate: 1.34)

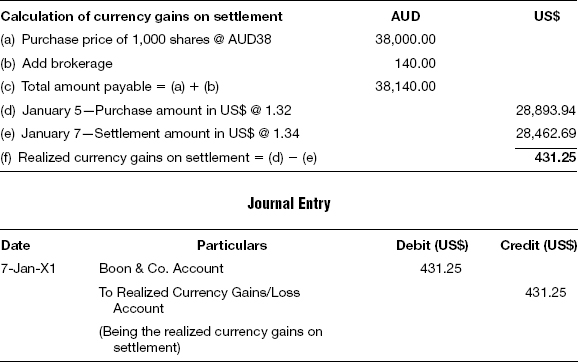

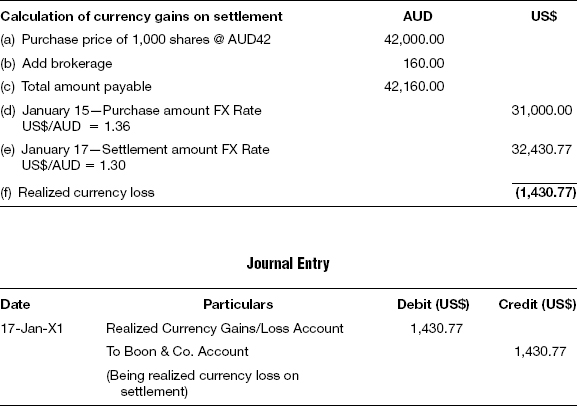

F-3 Currency Gains/Loss on Settlement (Consummated FX Translation Entry)

The settlement amount when converted into US$ based on the FX rate on the date of settlement results in a different amount than the contracted amount in US$ terms. This represents the currency gains or loss and is taken directly to the profit and loss account. If this FX translation entry is not passed, then the liability account of the broker will continue to have a balance even though the broker is settled in full in the respective local currency.

F-4 On Purchase of Equity Shares and Payment of Brokerage (T-3 @ FX Rate: 1.36)

F-5 On Payment of Contracted Sum (T-4 @ FX Rate: 1.30)

F-6 Currency Gains/Loss on Settlement (Consummated FX Translation Entry)

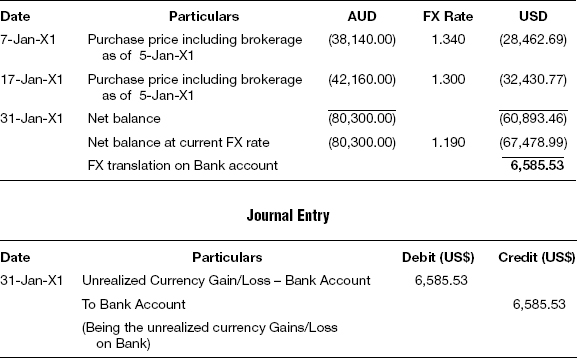

F-7 Mark-to-market at End of Reporting Period (T-5 @ FX Rate: 1.19)

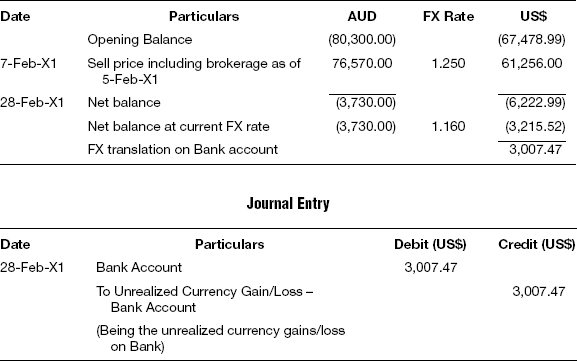

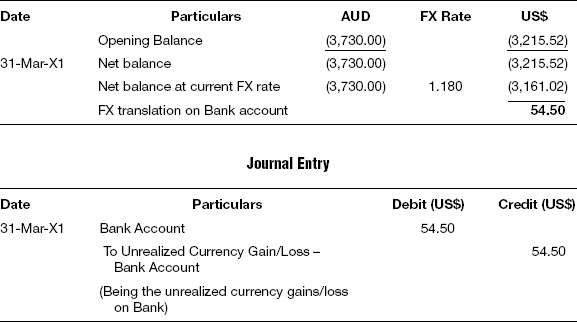

F-8 Currency Gains/Loss—Bank FX (Transient FX translation entry)

F-9 Reversal of Mark-to-market Entry (T-6 @ FX Rate: 1.19)

F-10 Currency Gains/Loss (Transient FX Translation Entry)

F-11 On Sale of Equity Shares and Payment of Brokerage (T-7 @ FX Rate: 1.15)

F-12 Recording the Profit/Loss on Sale Shares (T-8 @ FX Rate: 1.15)

F-13 Realized Currency Gains/Loss on Liquidation (Consummated FX Translation Entry)

F-14 On Receipt of Contracted Sum (T-9 @ FX Rate: 1.25)

F-15 Currency Gains/Loss on Settlement (Consummated FX Translation Entry)

The settlement amount when converted into US$ based on the FX rate on the date of settlement results in a different amount than the contracted amount in US$ terms. This represents the currency gains or loss and is taken directly to the profit and loss account. If this FX translation entry is not passed, then the liability account of the broker will continue to have a balance even though the broker is settled in full in the respective local currency.

F-16 Mark-to-market at End of Reporting Period (T-10 @ FX Rate: 1.16)

F-17 Reversal of Mark-to-market (T-11 @ FX Rate: 1.16)

F-18 Currency Gains/Loss—FX (Transient FX Translation Entry)

F-19 Currency Gains/Loss—Bank FX (Transient FX translation entry)

F-20 Mark-to-market at End of Reporting Period (T-12 @ FX Rate: 1.18)

F-21 Currency Gains/Loss—FX (Transient FX Translation Entry)

F-22 Currency Gains/Loss—Bank FX (Transient FX translation entry)

- According to the accounting standards, available-for-sale (AFS) financial assets are those non-derivative financial assets that are designated as available for sale or are not classified as loans and receivables, held-to-maturity investments, or financial assets at fair value through profit or loss.

- Available-for-sale securities are debt or equity investments that are held for an indefinite period of time without any intention to resell for profit.

- They are not trading assets, as in the case of short-term assets held for speculation, nor are they acquired with an intention to hold till maturity.

- If the market rate is above the purchase rate of AFS securities, then such increase is recorded as part of the other comprehensive income (OCI) and not recognized as income in the current period. This is shown as part of the shareholders’ equity in the balance sheet.

- Any foreign exchange gains and losses on monetary assets are recognized in the statement of profit and loss except for those items that are designated as hedging instruments.

- Equity instruments, being nonmonetary assets, the gain or loss including any related foreign exchange component is recognized directly in the appropriate equity account.

- In the balance sheet, a nonmonetary financial asset such as an investment in equity instrument is translated using the closing rate if it is carried at fair value in the foreign currency, and using the historical rate if it is not carried at fair value when its fair value cannot be reliably measured.

- As per the U.S. GAAP Statement of Position, it is not mandatory to show separately the capital gains/loss due to change in the market rate of the asset, or currency gains/loss due to change in the foreign exchange rate, although the SOP indicates that such separate reporting would provide valuable information to the users of the financial statements.

- If an equity instrument measured at fair value with gains and losses recognized in the appropriate equity account becomes impaired, the cumulative net loss recognized in the equity account, including any portion attributable to foreign currency changes, should be recognized in the statement of profit and loss.

- If the equity securities classified as available-for-sale are sold, then the realized gains/loss on such sale is transferred from the OCI to the income statement and an entry is recorded to that effect.

Theory Questions

1. When would you classify an investment as available-for-sale (AFS)?

2. What are the major differences between trading and available-for-sale securities?

3. What is other comprehensive income (OCI) and where is it presented in the final accounts?

4. How is the foreign exchange translation impact on AFS equity securities handled? Is this any different from debt securities? If so, explain why it is so.

5. How is the impairment of AFS securities treated?

Objective Questions

1. AFS securities are debt or equity investments that will be held:

a. Till maturity

b. For a predefined period

c. Only till the current financial year

d. For an indefinite period of time

e. None of the above

2. The unrealized gains/losses for AFS securities are:

a. Recorded as an adjustment to equity on the balance sheet

b. Not recorded in the balance sheet

c. Recorded as earnings in P&L for the current period

d. Both a and c

3. When there is a permanent impairment to the value of the securities held as available-for-sale, such permanent impairment should be recognized as:

a. Mark-to-market

b. Current liabilities

c. Income

d. Accrued expense

e. Cost

4. For AFS securities, cost of sales is arrived at by which of the following methods?

a. Weighted average method

b. FIFO

c. LIFO

d. All of the above methods

e. None of the above methods

Journal Questions

Available-for-sale, Trade Currency TWD

Taiwan Opportunities Fund traded in Feng Tay Enterprises Co. Ltd., shares in the Taiwan stock exchange through KGI Securities Co. brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

FIFO

Market Rate of Feng Tay Shares in TWD

February 28: 26.95

March 31: 27.90

April 30: 30.15

FX Rate: US$/TWD

February 5: 32.67

February 8: 32.63

February 15: 32.76

February 18: 32.79

February 28: 32.98

March 5: 32.83

March 8: 32.87

March 31: 32.90

April 30: 32.77

Functional Currency

US$

Prepare

Journal entries, general ledgers, trial balance, income statement, and balance sheet.

Available-for-sale, Trade Currency SGD

Singapore Fund traded in OCBC Ltd shares in Singapore Exchange through Grayson & Co. brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

FIFO

Market Rate of OCBC LTD Shares in SGD

February 28: 10.15

March 31: 9.80

April 30: 10.35

FX Rate: US$/SGD

February 8: 1.54

February 11: 1.52

February 15: 1.51

February 18: 1.53

February 28: 1.52

March 9: 1.55

March 12: 1.53

March 31: 1.50

April 31: 1.54

Functional Currency

US$

Prepare

Journal entries, general ledgers, trial balance, income statement, and balance sheet.

Available-for-sale, Functional Currency CAD

U.S. Fund traded in DSP shares in a Canadian stock exchange through Amazon brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 3

Liquidation Method

FIFO

Market Rate of DSP LTD Shares in CAD

February 28: 16.15

March 31: 16.80

April 30: 16.35

FX Rate: US$/CAD

February 18: 1.0130

February 21: 1.0140

February 25: 1.0185

February 28: 1.0150

March 19: 1.0220

March 22: 1.0230

March 31: 1.0245

April 31: 1.0190

Functional Currency

US$

Prepare

Journal entries, general ledgers, trial balance, income statement, and balance sheet.

Available-for-Sale, Functional Currency JPY

Dianna Smith buys 10,000 shares of GoldWinner on January 10 for $5.40 per share. Ms. Smith’s reporting currency is Japanese yen. The shares are bought without any intention of trading for short-term gains. Record the necessary journal entries for the following events:

1. For the purchase of the 10,000 shares.

2. The US$/JPY rate on January 10 is 109.15. The shares bought on January 10 are settled on January 12. On January 12 the US$/JPY rate is 108.05. Record the FX revaluation entries for these events. Calculate the FX gain/loss and pass relevant entries for FX translation.

3. The shares are sold on January 29 for $6.80 per share and US$/JPY rate on January 29 is 109.00. Calculate the realized gain or loss and pass entry. The US$/JPY rate on January 31(settle date) is 109.24.

4. Prepare relevant ledger accounts to give effect to these transactions.