CHAPTER 4

Transfer of Categories

After studying this chapter, you should have a grasp of the following:

- Transfer of equity investments between trading and available-for-sale categories.

- Presentation in income statement.

- Impairment of securities.

- Deferred tax effects on unrealized gain/loss in trading and available-for-sale securities.

- How to record and report trade transactions of equity investments comprehensively.

Relevant Accounting Standards

| U.S. GAAP | IFRS |

| FAS 52—Foreign Currency Translation FAS 94—Consolidation of All Majority-owned Subsidiaries FAS 109—Accounting for Income Taxes FAS 115—Accounting for Certain Investments in Debt and Equity Securities FAS 130—Reporting Comprehensive Income FAS 157—Fair Value Measurements FAS 159—The Fair Value Option for Financial Assets and Financial Liabilities |

IFRS 7—Financial Instruments: Disclosure IAS 21—The Effects of Changes in Foreign Exchange Rates IAS 32—Financial Instruments: Presentation IAS 36—Impairment of Assets IAS 39—Financial Instruments: Recognition and Measurement |

The classification of securities should be reviewed at each balance sheet date. When the equity securities are transferred from trading securities to the available-for-sale category, then the gain/loss recognized as unrealized should not be reversed and no adjustment should be made to the other comprehensive income (OCI). When the equity securities are transferred from the available-for-sale category to the trading category, then the unrealized gain/loss on such securities based on the fair value of the securities should be transferred from OCI and thus recognized as income immediately on such transfer.

The following table gives the summary of treatment of transfer between the two categories.

| Securities Transferred from | Securities Transferred to | Accounting treatment |

| Available-for-sale | Trading | Unrealized gain/loss is recognized based on fair value |

| Trading | Available-for-sale | No reversal of gain/loss recognized as unrealized |

PRESENTATION IN INCOME STATEMENT

Impairment of Securities

Temporary impairment of the equity securities that are held for trading is automatically tracked by valuing the securities at mark-to-market on every reporting day. Such temporary impairment is not to be recognized and acted upon for available-for-sale securities. However, if the impairment is anything other than temporary, then such impaired security must be written down to fair value. The realized loss on such impairment must be reported in the income statement. Once the impairment is recorded as loss, then even if the security recovers from such impairment, it would not be recognized in the earnings unless it is liquidated through the sale of the security.

Stock Dividend

While the cash dividends received from investments held as trading or as available-for-sale should be reported as income of the current period, the stock dividend should not be reported as income. Instead the shares received as stock dividend should be added to the original shares, and when the mark-to-market process is performed, the impact of the stock dividend will be automatically accounted for as unrealized gains and will be reported as income during the period.

Realized and Unrealized Gain/Loss

To summarize, the accounting standards require that investments classified as trading securities, the realized and unrealized gains and losses should be included in the current period’s income statement. In the case of investments classified as available-for-sale, however, only realized gains should be taken to the current period’s income statement. The unrealized gains on available-for-sale securities should be taken directly to the OCI, which is grouped with the shareholders’ equity and is not regarded as income of the current period. However, when the available-for-sale securities are sold, the realized gain/loss should be taken to the income statement and to that extent reversed from the other comprehensive income.

Permanent impairment to the value of the securities held as available-for-sale should be written off as expense in the income statement. This should not be reversed, even if the security recovers from impairment, till such time as the security is liquidated and the actual realized gain/loss is computed.

DEFERRED TAX EFFECTS ON UNREALIZED GAIN/LOSS

The mark-to-market process ensures that the marketable investments held either as trading securities or as available-for-sale securities are to be reported in the balance sheet at fair value and the gain/loss on such investments is to be reported either as income or as other comprehensive income. Such unrealized gain/loss is not recognized for income tax purposes until the same is realized through liquidation. Hence the unrealized gain/loss included in the income or OCI, as the case may be, represents temporary differences as defined by FAS 109.

The tax effects of all temporary differences are to be recognized in the financial statements as deferred tax benefits or deferred tax liabilities. Also, in the case of deferred tax benefits, there is a requirement to provide for an allowance in case it is “more likely than not” going to be unrealized.

Deferred Tax Effect in Trading Securities

For securities classified as trading, the unrealized gain/loss is included in the income and as such represents the temporary differences as defined in the accounting standards. The deferred tax effect of those changes should also be presented in the income statement itself.

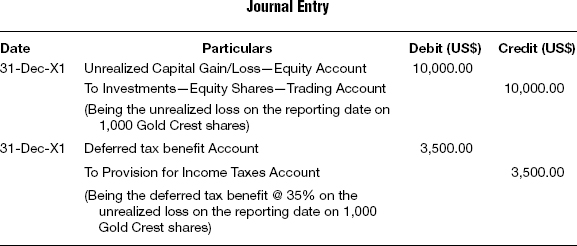

Assuming that the fair value of 1,000 Gold Crest shares purchased at $490 is $480 per share, then the unrealized loss on such an investment classified as trading securities would be $10,000. If the effective tax rate of the investor is 35 percent, then $3,500 should be taken to the debit of the deferred tax benefit account.

The accounting entry that is recorded in the books of accounts would be as follows:

Deferred Tax Effect in Available-for-sale Securities

For securities classified as available-for-sale, the unrealized gain/loss is included in the OCI and as such forms part of the temporary differences as defined in the accounting standards. The deferred tax effect of those changes should also be presented in the OCI itself.

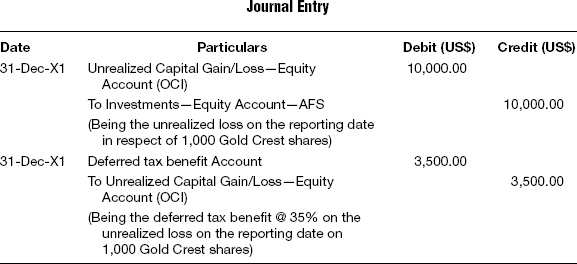

Assuming that the fair value of 1,000 Gold Crest shares purchased at $490 is $480 per share, then the unrealized loss on such investment classified as available-for-sale securities would be $10,000. If the effective tax rate of the investor is 35 percent, then $3,500 should be taken to the debit of the deferred tax benefit account, and the OCI should be reduced to that extent. The accounting entry that is recorded in the books of accounts would be as follows:

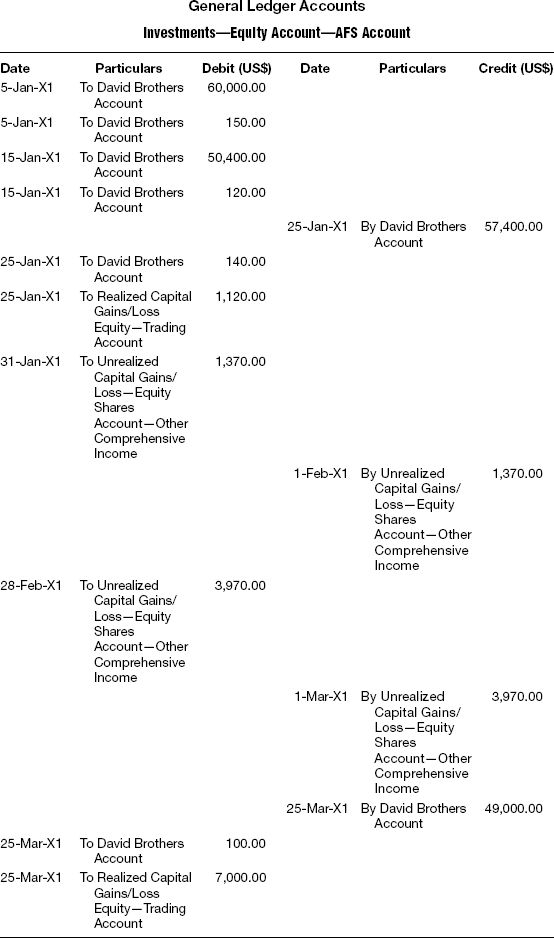

Illustration—Transfer of Category and Deferred Tax Benefit

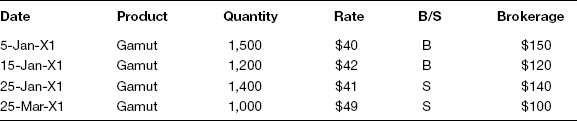

Jonathan Swift Inc. traded in Gamut shares that are listed in a U.S. stock exchange through David Brothers Brokers, and the details are as follows:

Trade Details

Other Details

Settlement: T + 2

Liquidation Method

FIFO

Market Rate

January 31: 43

February 28: 45

March 31: 35

The shares were purchased without any intention of trading, nor were they meant to be a long-term investment. However, management changed its mind and decided that Gamut shares will be classified as trading shares on March 31. Jonathan Swift is charged tax on all its earnings at the rate of 40 percent. Prepare the accounts through March 31.

Prepare

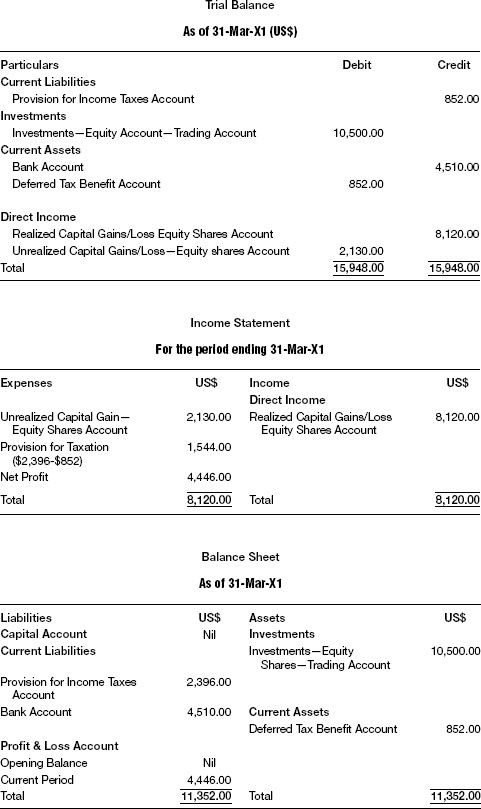

Journal entries, general ledgers, trial balance, income statement, and balance sheet.

Solution

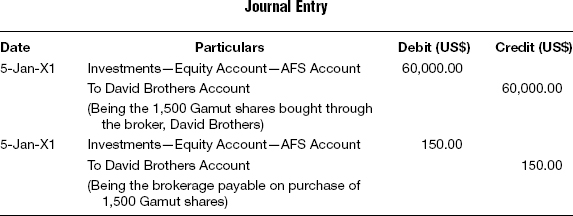

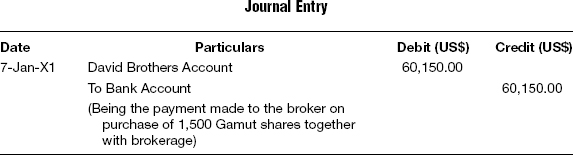

T-1 On Purchase of Equity Shares and Payment of Brokerage

T-2 On Payment of Contracted Sum

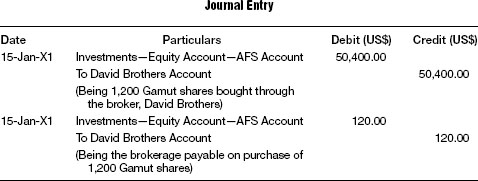

T-3 On Purchase of Equity Shares and Brokerage

T-4 On Payment of Contracted Sum

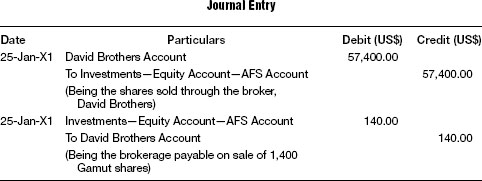

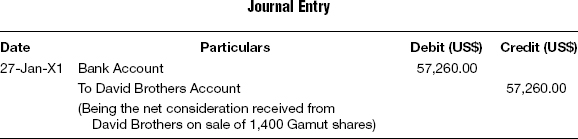

T-5 On Sale of Shares and Payment of Brokerage

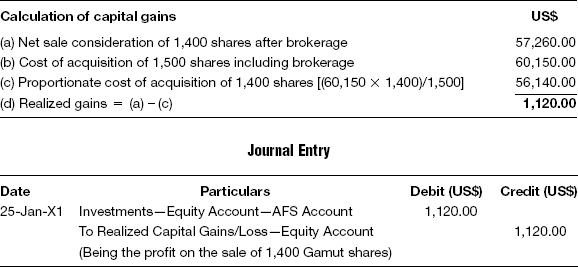

T-6 On Recording the Profit/Loss on Sale of Shares

T-7 On Receipt of Sale Consideration Net of Brokerage

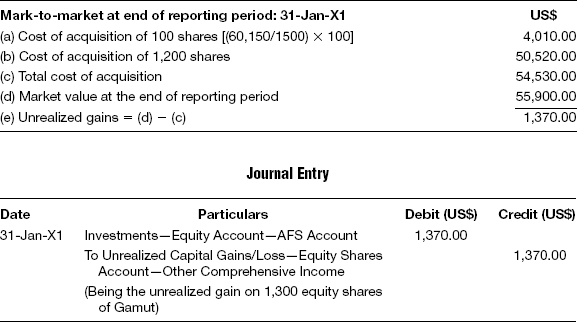

T-8 Mark-to-market at End of Reporting Period

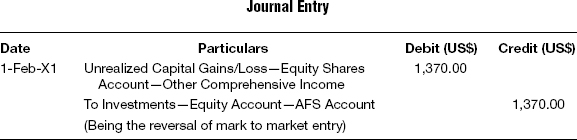

T-9 Reversal of Mark-to-market on the Next Date

T-10 Mark-to-market at End of Reporting Period

T-11 Reversal of Mark-to-market on the Next Date

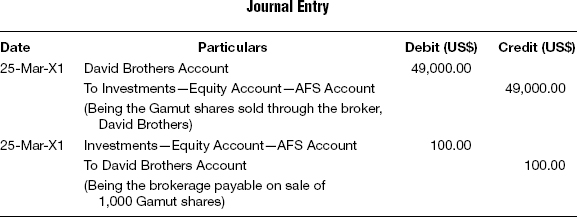

T-12 On Sale of Shares and Payment of Brokerage

T-13 On Recording the Profit/Loss on Sale of Shares

T-14 On Receipt of Sale Consideration Net of Brokerage

T-15 Mark-to-market at End of Reporting Period

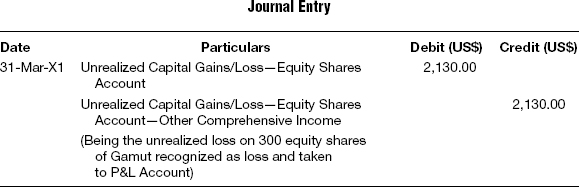

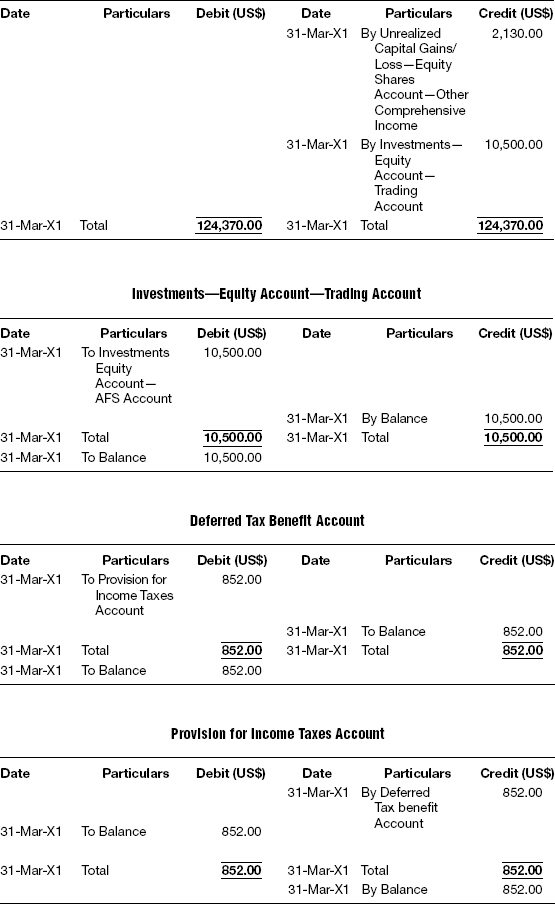

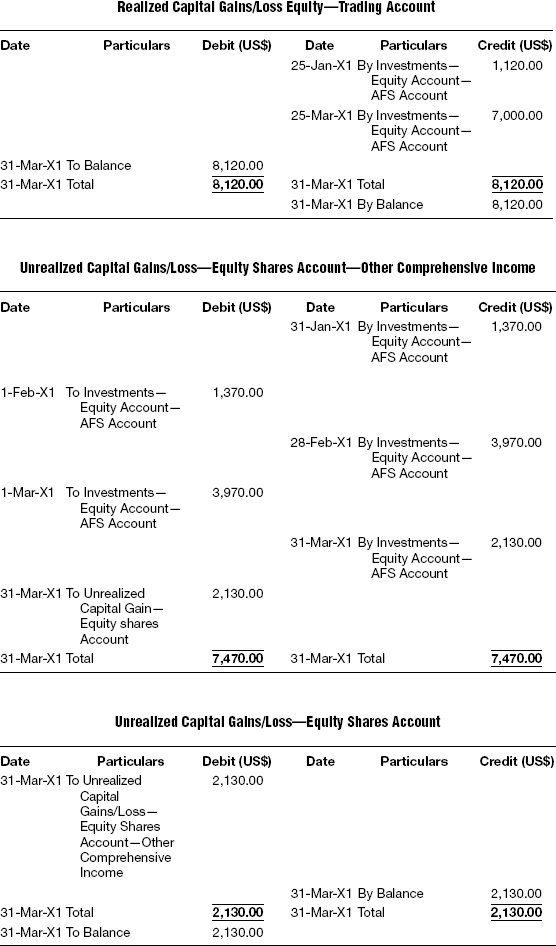

T-16 Transfer of Unrealized Loss from OCI to P&L Account

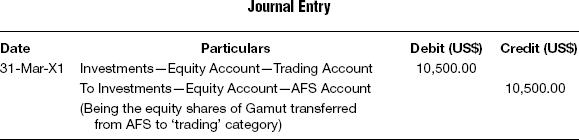

T-17 Transfer of Category from AFS to Trading

T-18 Deferred Tax Impact on Unrealized Capital Loss

The provision to be made for taxation is $2,396.

- If the equity securities classified as available-for-sale are sold, then the realized gain/loss on such sale is transferred from the other comprehensive income (OCI) to the income statement and an entry is recorded to that effect.

- When the equity securities are transferred from trading securities to the available-for-sale category, then the unrealized gain/loss should not be reversed and no adjustment should be made to the OCI.

- When the equity securities are transferred from the available-for-sale category to the trading category, then the unrealized gain/loss on such securities based on the fair value of the securities should be transferred from OCI and thus recognized as income immediately on such transfer.

- Temporary impairment with respect to the equity securities that are held for trading is automatically tracked by valuing the securities at mark-to-market on every reporting day. Such temporary impairment is not to be recognized and acted upon for available-for-sale securities. However, if the impairment is anything other than temporary, then such impaired security must be written down to fair value. The realized loss on such impairment must be reported in the income statement. Once the impairment is recorded as loss, then even if the security recovers from such impairment, it would not be recognized in the earnings unless it is liquidated through the sale of the security.

- Unrealized gain/loss is not recognized for income tax purposes until the same is realized through liquidation. Hence the unrealized gain/loss included in the income or OCI represents temporary differences as defined by FAS 109. The tax effects of all temporary differences are to be recognized in the financial statements as deferred tax benefits or deferred tax liabilities.

- For securities classified as trading, the unrealized gain/loss is included in the income and as such represents the temporary differences as defined in the accounting standards. The deferred tax effect of those changes should also be presented in the income statement itself.

- For securities classified as available-for-sale, the unrealized gain/loss is included in the OCI and as such forms part of the temporary differences as defined in the accounting standards. The deferred tax effect of those changes should also be presented in the other comprehensive income itself.

- As per FAS 115, under U.S. GAAP, for securities classified as available-for-sale, all reporting enterprises shall disclose:

- Aggregate fair value.

- Gross unrealized holding gains.

- Gross unrealized holding losses.

These should be grouped by major security type as of each date for which a statement of financial position is presented.

- IFRS 7 comes into effect for annual periods beginning on or after January 1, 2007. This standard requires that preparers provide quantitative and qualitative disclosures that would enhance a user’s understanding of the entity’s exposures to financial risks and how the entity manages those risks.

Theory Questions

1. Can the securities that are classified once be transferred to other category? If so, what precautions should be taken to adjust the unrealized gains or losses?

2. How is the impairment of securities presented in the balance sheet?

3. What is the proper treatment of stock dividends? Can you report this as income?

4. How are the tax effects on unrealized gains/losses treated in the books of accounts in the securities classified as trading and as available-for-sale?

Objective Questions

1. When securities are transferred from trading securities to available-for-sale, then

a. Gain/Loss recognized as unrealized should be reversed

b. Gain/Loss recognized as unrealized should not be reversed

c. Gain/Loss recognized as unrealized will be adjusted with OCI

d. None of the above

2. When securities are transferred from available-for-sale to trading, then

a. Unrealized gain/Loss will be transferred from OCI and treated as income

b. Unrealized gain/Loss should not be reversed

c. No changes are required at all

d. None of the above

3. Impairment other than temporary with respect to equity securities should be

a. Written down to fair value

b. Treated alike as temporary impairment

c. Considered a loss to be treated as temporary

d. None of the above

4. Stock dividend declared should be treated as

a. Income

b. Increase in the value of original shares held

c. Increase to the quantity (position) of shares held

d. All of the above

5. For securities classified as available-for-sale, which of the following items will be reported in the income statement of the current period?

a. Both realized and unrealized gains

b. Realized gain alone

c. Unrealized gain alone

d. None of the above

6. For income tax purposes, unrealized gain/loss will be recognized for reporting

a. Automatically at the end of the financial year

b. Only if the securities are liquidated and realized

c. As and when, depending upon the corporate action

d. None of the above

7. Unrealized gain/loss included in the income/OCI represents

a. Temporary difference recognized as deferred tax benefits

b. Permanent difference recognized as deferred tax benefits

c. No effect

d. None of the above

8. For available-for-sale securities, the deferred tax effect should be presented in

a. The income statement itself

b. Other comprehensive income itself

c. No need for accounting

d. None of the above

9. For trading securities, the deferred tax effect should be presented in

a. The income statement itself

b. Other comprehensive income itself

c. No need for accounting

d. None of the above

10. As per U.S. GAAP, changes in fair value for available-for-sale securities are reported in

a. The income statement

b. Other Comprehensive Income

c. No need to report

d. None of the above

11. When the equity securities are transferred from AFS to trading securities,

a. The unrealized gain/loss is recognized on T + 2

b. The unrealized gain/loss is not recognized at all

c. The realized gain/loss is recognized immediately

d. The unrealized gain/loss is recognized immediately

e. Realized gain/loss of trading securities is treated in the same way as in AFS

12. Shares received as stock dividend should be added to the original shares, and when the mark-to-market process is performed, the impact of the stock dividend

a. Should be treated as unrealized gains and reported as income for the period

b. Should be treated as dividend income

c. Should be treated as dividend income but should be shown as a current asset on the asset side of the balance sheet

d. Should be treated as realized gain/income for the period

e. Items b and c

13. According to the definition in FAS 109, the tax effects of all temporary differences arising from unrealized gain/loss are to be recognized in the financial statements as

a. Non-trading income

b. Items exempted from taxes

c. Deferred tax benefits or deferred tax liabilities

d. They are not recognized for the current period, but are carried forward to the next accounting period

e. Income or expense for the current period

14. According to FAS 115, under U.S. GAAP, for securities classified as available-for-sale, all reporting enterprises shall disclose

a. Aggregate fair value

b. Gross unrealized holding gains

c. Gross unrealized holding losses

d. None of the above

e. All the above

Journal Questions

Transfer the following from AFS to trading category.

Aspen Onshore Fund LLC traded in Epson shares that are listed on the New York Stock Exchange through Remount stockbrokers. The details are as follows:

Trade Details

Other Details

Settlement: T + 2

Liquidation Method

FIFO

Market Rate

January 31: 101.00

February 28: 98

March 31: 97.85

The shares were bought without any intention of trading, nor was this meant to be a long-term investment. However, management changed its mind and decided that Epson shares would be classified as trading shares on March 31. Aspen Onshore Fund is charged tax on its earnings at an average rate of 40 percent. Prepare the accounts through March 31.

Prepare

Journal entries, general ledgers, trial balance, income statement, and balance sheet.