CHAPTER 8

Accounting for Equity Call Options

After studying this chapter you should have a grasp of the following:

- Accounting standards for derivative instruments and hedging activities.

- Trade life cycle of exchange-traded options (ETOs) for long call.

- Journal entries to be recorded during the different phases of the trade life cycle.

- FX revaluation and FX translation process for these trades.

- Illustration of long call, non-hedging trades.

- Preparation of journal entries and general ledger accounts.

- Preparation of income statement and balance sheet after the call option trades are made.

- Illustration of long call, non-hedging trades in foreign currency.

- Trade life cycle of exchange-traded options when writing call options.

- Journal entries to be recorded during the different phases of the trade life cycle.

- Illustration of written call options in functional currency.

- Preparation of journal entries and general ledger accounts.

- Preparation of income statement and balance sheet after writing the call options.

ACCOUNTING STANDARDS—DERIVATIVE INSTRUMENTS AND HEDGING ACTIVITIES

The accounting treatment of call options prima facie will depend upon the intention with which the call options are purchased, either for hedging or for speculation (non-hedging). If the position is taken as a hedge against some other position, the relevant accounting standards will be applicable and certain conditions must be fulfilled.

Relevant Accounting Standards

| U.S. GAAP | IFRS |

| FAS 52—Foreign Currency Translation | IFRS 7—Financial Instruments: Disclosure |

| FAS 94—Consolidation of All Majority-owned Subsidiaries | IAS 21—The Effects of Changes in Foreign Exchange Rates |

| FAS 115—Accounting for Certain Investments in Debt and Equity Securities | IAS 32—Financial Instruments: Presentation |

| FAS 130—Reporting Comprehensive Income | IAS 36—Impairment of Assets |

| FAS 157—Fair Value Measurements | IAS 39—Financial Instruments: Recognition and Measurement |

| FAS 159—The Fair Value Option for Financial Assets and Financial Liabilities |

TRADE LIFE CYCLE FOR ETOs—LONG CALL NON-HEDGING

If the call is purchased purely as a speculative trade, then the premium paid towards the purchase of the call option is taken to the expense and the premium received on sale of the options is treated as revenue. However, the value of the option is written back on the valuation date and shown as an asset in the case of purchase of call options.

- Buy the call options.

- Brokerage/commission on the buy transaction.

- Pay for the call options bought.

- Ascertain the fair value at the end of reporting period.

- Reversal of mark-to-market.

- Expiry of options.

- Exercise of options.

- Sell the options.

- Receive the consideration.

- Ascertain the profit/loss on the sale.

- FX revaluation entries.

- FX translation entries.

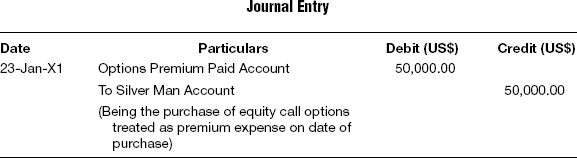

Buy the Call Options

If the options are purchased other than as a hedge, it is either for speculation or for arbitrage. In this case the income account is debited when the options are purchased. On the valuation date the entire value of the options is written back as income on the one hand and asset on the other. In both cases, the net income and the net value shown on the balance sheet would be the same.

Assume that 10,000 equity call options of Metadata with a strike price of $50 are bought at $5 each through Beckerman & Co. Assume that the market rate of the underlying share is $52 at the time of purchase of these options. The accounting entry that is recorded in the books of accounts is shown as follows:

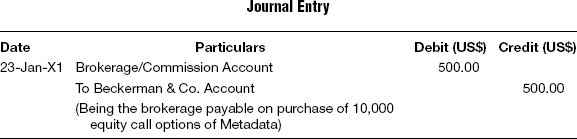

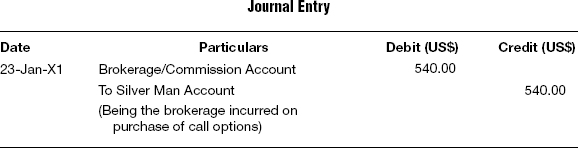

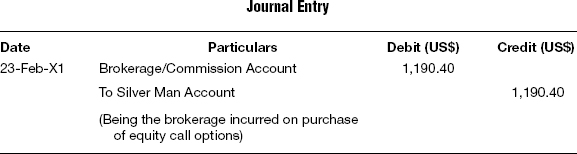

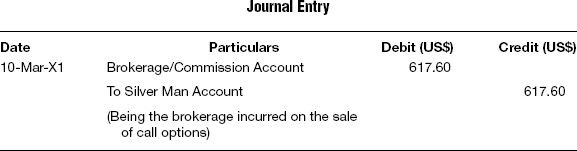

Brokerage/Commission on the Buy Transaction

The broker of the stock exchange charges a commission for the services rendered. This is usually settled along with the purchase value of the options. For option contracts, the brokerage/commission is not treated as part of the cost of the options contract; instead it is debited to the brokerage/commission account.

Assume that the brokerage for this deal is $500. The accounting entry that is recorded in the books of accounts is shown as follows:

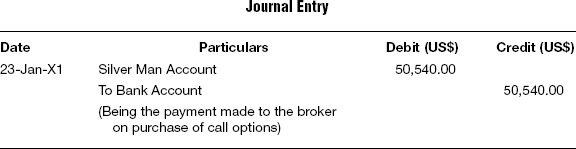

Pay for the Options Bought

The next event in the trade life cycle is the payment of the contracted amount for the options bought. Usually this payment happens the same day.

The accounting entry that is recorded in the books of accounts is shown as follows:

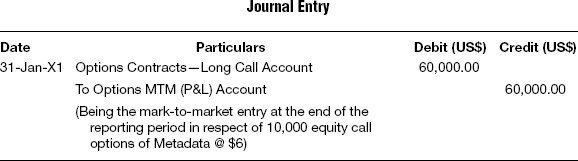

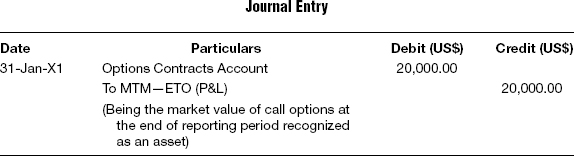

Ascertain the Fair Value at the End of the Reporting Period

The value of the entire position is written back to the profit and loss account and the same amount is shown as an asset in the balance sheet. This is because the entire value of the options at the time of purchase is taken to the expense account.

Assuming that the value of the options at the end of the reporting period is $6 then, the entire amount of $6 per option is recognized as income and is shown as an asset on the balance sheet. The accounting entry that is recorded in the books of accounts is shown as follows:

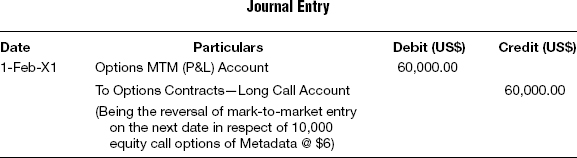

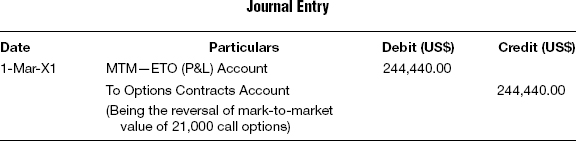

Reversal of Mark-to-market

The accounting entry for mark-to-market is reversed on the next day or the next valuation date when a fresh entry for the then value is recorded in the books of accounts. However, if the investor follows this incremental value method then there is no need to reverse the entry for mark-to-market recorded earlier.

The accounting entry that is recorded in the books of accounts is shown next.

Expiry of Options

The options expire on the expiry date of the contract. For call options that are bought, the market value of the underlying over and above the strike price of the options represents the profit. In this case, the call option is said to expire in-the-money. By contrast, if the call options expire out-of-the-money—that is, if the market value of the underlying is less than the strike price of the option—then the premium paid by the investor represents the loss. The maximum loss that could be incurred in a long call option can never exceed the premium paid on the purchase of the option.

Case 1: When the options expire worthless, there is no need to record any entry in the books of accounts. The option premium paid is already treated as an expense, and since the options expire worthless there is no need to write back the value of the options on the expiry date.

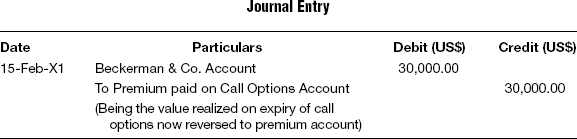

Case 2: When the options expire in-the-money—that is, where the market rate of the underlying is more than the strike price of the option—the amount of value of the underlying that exceeds the strike price represents the gain accruing to the investor. However, if the price of the underlying is below the strike price and the premium paid to acquire the options, the investor will still lose money. Assuming that the underlying shares close at $53 on the expiry date, the accounting entry that is recorded in the books of accounts is shown as follows:

In several stock exchanges, exchange traded options (ETOs) which are settled only by cash—usually options on index—that expire in the money are automatically taken care of by the stock exchange. The intrinsic value of the options is credited to the investor without the investor having to liquidate the position. However in cases where the options can be settled by delivery, the investor should either liquidate the position or should take delivery of the underlying in order to profit from an in-the-money option. In the illustrations given in this book it is assumed that either the stock exchange concerned credits the intrinsic value or the investor takes appropriate action that results in his getting the intrinsic value of the options when it expires in the money.

Case 3: The investor makes a profit when the options are exercised in-the-money—that is, when the market rate of the underlying is more than the strike price of the option. Assuming that the underlying shares close at $59 on the excercise date, the accounting entry that is recorded in the books of accounts is shown as follows:

Exercise of Options

The buyer of the call option has the right but not the obligation to buy the underlying at the strike price. When the call options are exercised, it results in the acquisition of the underlying asset. In such a scenario, the investor has to pay for the underlying at the contracted strike price. The actual cost of carry of the underlying asset would then be the strike price of the contract plus the premium paid on the purchase of the call option. The profit or loss would be arrived at only after the underlying asset is liquidated. Until such time, the asset would be carried in the books at cost. Exercise of options happens only in the case of stock options and not in the case of options on indexes.

Assume that the options are exercised on the date of expiry when the price of the underlying share is $57, and that the equity shares are acquired for trading purposes. The accounting entry that is recorded in the books of accounts is shown as follows:

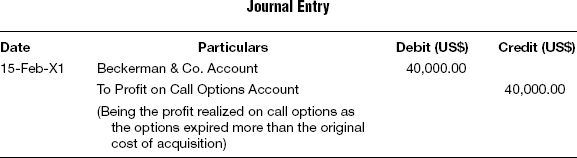

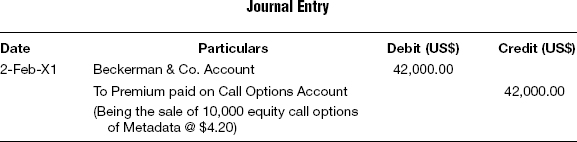

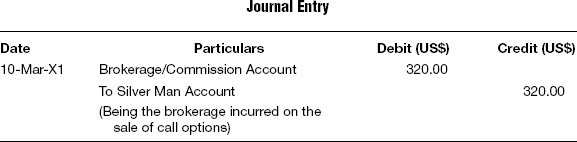

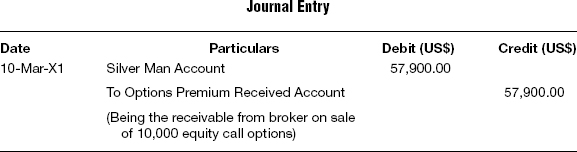

Sell the Options

The long position of call options could be liquidated by selling such options. Since the sale results in only squaring up of the existing position, there is no requirement of any margin payment to the exchange on account of this sale of call options.

Assuming that the options are liquidated at $4.20, the accounting entry that is recorded in the books of accounts is shown as follows:

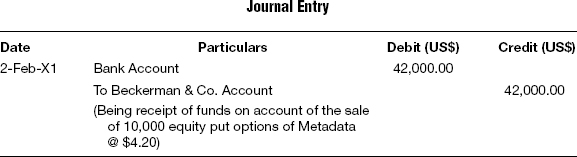

Receive the Consideration

The consideration is received on day T + 2 or according to the requirements of the exchange concerned. The consideration is received net of brokerage. The accounting entry that is recorded in the books of accounts is shown as follows:

Ascertain the Profit/Loss on the Sale

Since the expense account is debited while purchasing the options, there is no need to record a separate entry to determine the profit or loss on sale of options in this case.

FX Revaluation Entries

All the entries recorded to this point are initially entered in the respective trade currencies. If the functional currency is different from the trade currency, then each and every entry recorded in the trade currency should be entered again in the functional currency by converting the entries at the respective day’s FX rates. In other words, for each trade currency that the investor deals with, there will be a complete set of books representing that trade currency. This includes journal entries, general ledger postings, trial balance, income statement and balance sheet.

After revaluing each and every journal entry of all the trade currencies into the functional currency, a separate set of books is prepared again comprising all the elements just mentioned—that is, journal entries, general ledger postings, trial balance, income statement and balance sheet. It should be noted that the ultimate financial reports would be prepared and presented to all the stakeholders based on the financial statements prepared in the functional currency only as this will encompass all the transactions of the investor in all trade currencies dabbled with. (For illustration and detailed explanation please refer to Chapter 2.)

FX Translation Entries

After revaluing all the entries in the functional currency at the respective FX rates for the day concerned, another entry needs to be passed in the books of the functional currency. This is mainly to adjust the currency gains or losses due to the fluctuations in FX rates between the reporting date and the date of recording the original entries. FX Translation entries are recorded only for the asset and liability accounts. For income and expense accounts the amount gets crystallized on the date of passing the FX revaluation entries in the books of the functional currency.

There are fundamentally two types of FX translation entries that are recorded in the books of the functional currency: consummated FX translation entries and transient FX translation entries. (For illustration and detailed explanation please refer to Chapter 2.)

Consider the following examples.

Long Call, Non-hedging

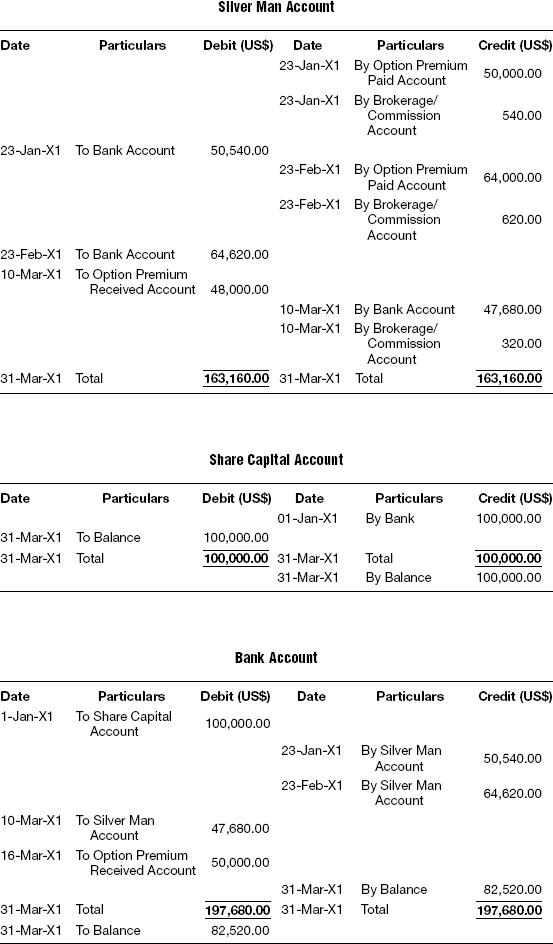

Victory Fund had the following trades in Metadata in the options market through Silver Man brokers. The stock exchange requires that the writer of the options maintain 10 percent of the value of the contract as margin money throughout the life of the contract. On January 1, $100,000 was introduced as capital into the fund. Journal entries, general ledgers, trial balance, income statement, and balance sheet are as follows:

Liquidation Method

FIFO

Market Rate of Underlying Stock Metadata

31-Jan-X1: 40.00; 28-Feb-X1: 55.00; 16-Mar-X1: $55

Market Rate of Metadata Call Option with Strike Price $50, Expiry March 16

January 31: 2

February 28: 6.00

March 16: 6.00

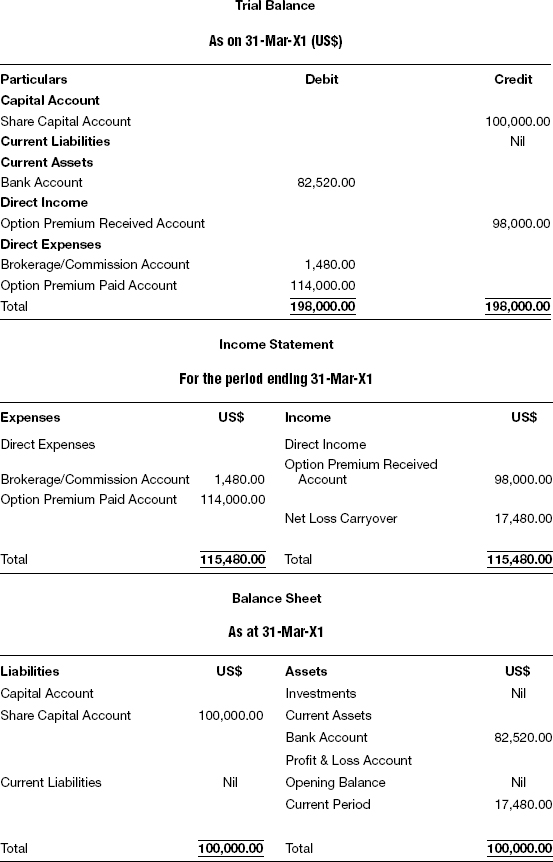

Long Call Option, Non-hedging—Functional Currency US$

T-1 Capital Brought In

T-2 On Purchase of Call Option

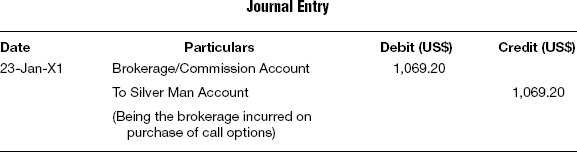

T-3 Brokerage/Commission

T-4 On Payment of Contracted Sum

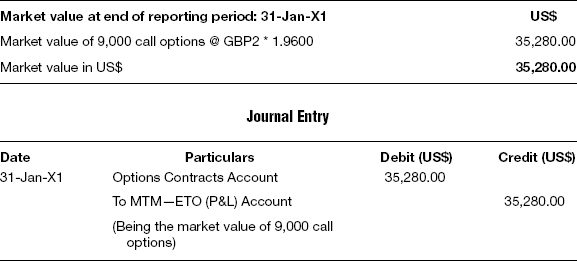

T-5 Market Value at End of Reporting Period

T-6 Reversal of Mark-to-market Value

T-7 On Purchase of Call Option

T-8 Brokerage/Commission

T-9 Payment of Contracted Sum

T-10 Market Value at End of Reporting Period

T-11 Reversal of Mark-to-market on Sale

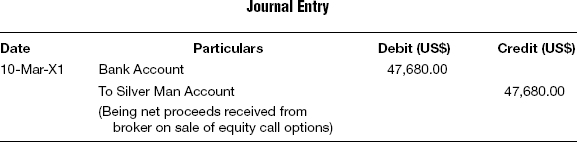

T-12 On Sale of Call Options

T-13 Brokerage/Commission on Sale

T-14 Receipt of Sale Proceeds

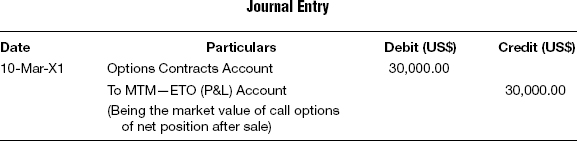

T-15 Market Value of Net Position after Sale

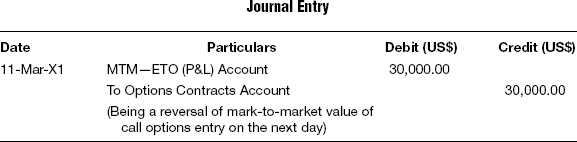

T-16 Reversal of Mark-to-market Value

T-17 On Expiry Date of Call Options

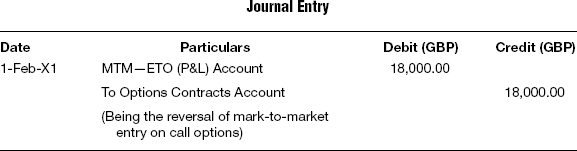

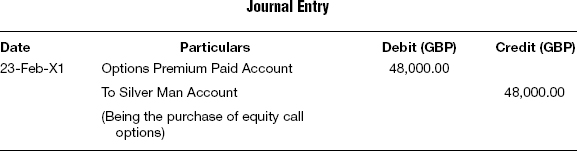

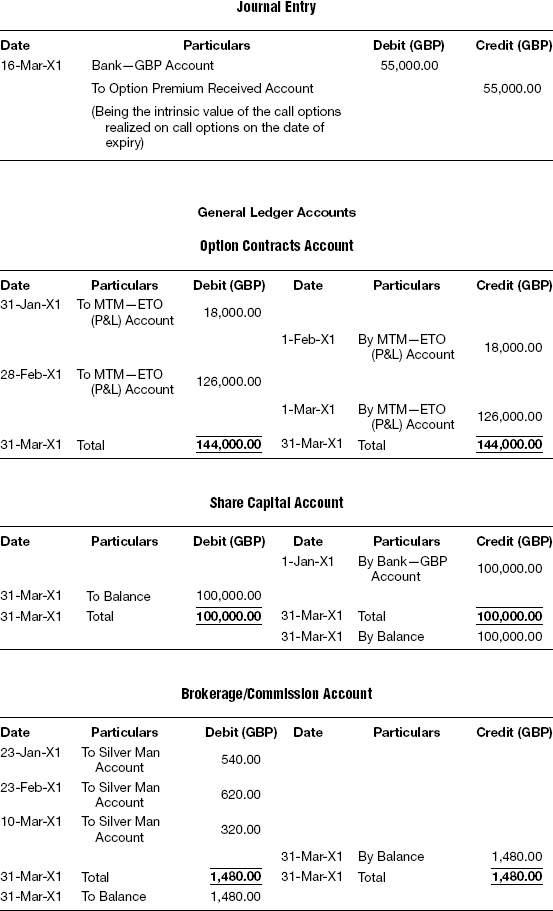

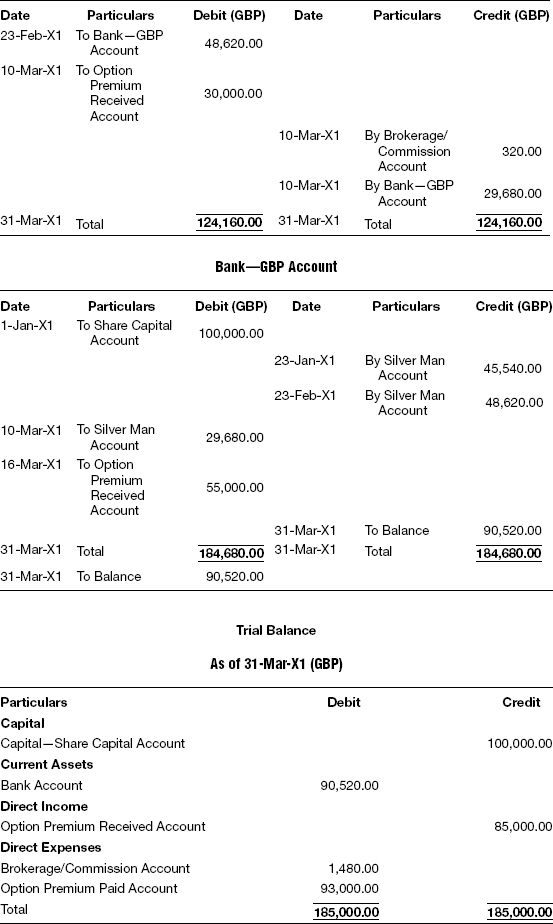

Long Call Options

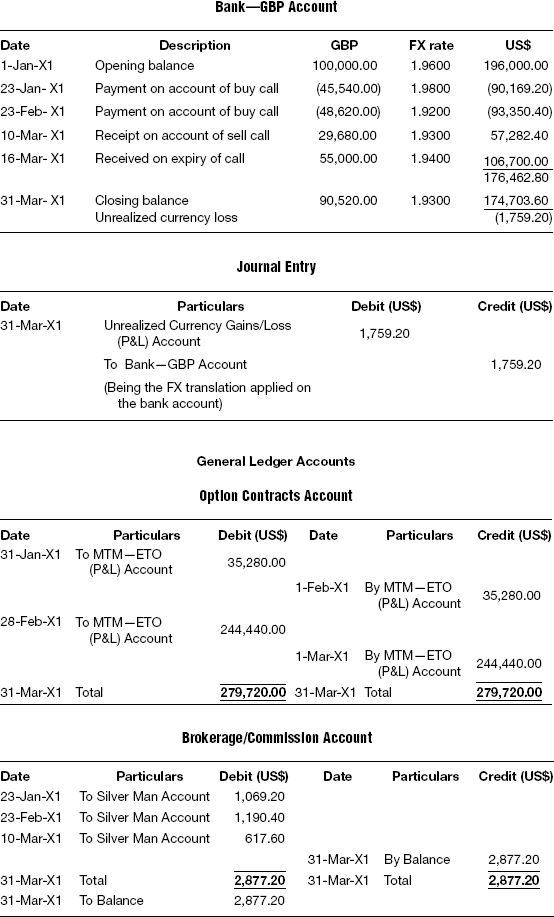

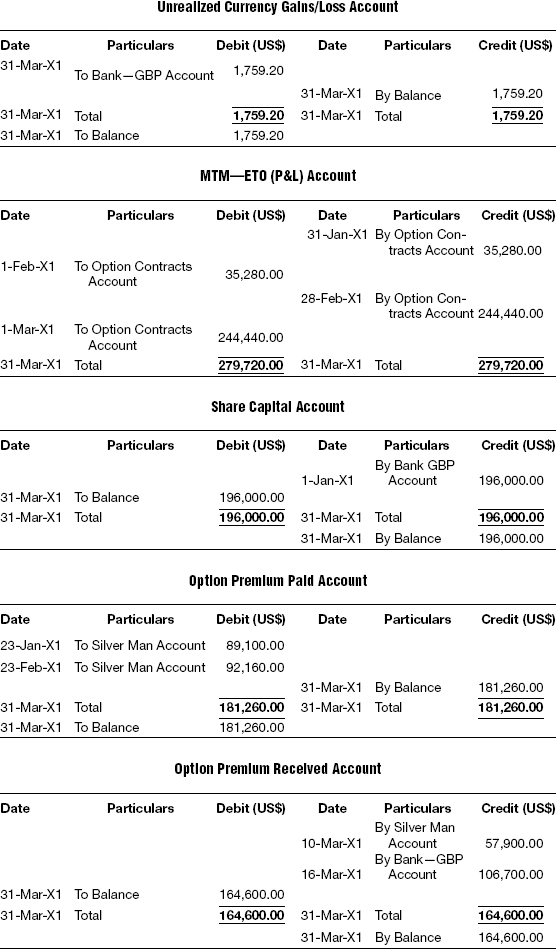

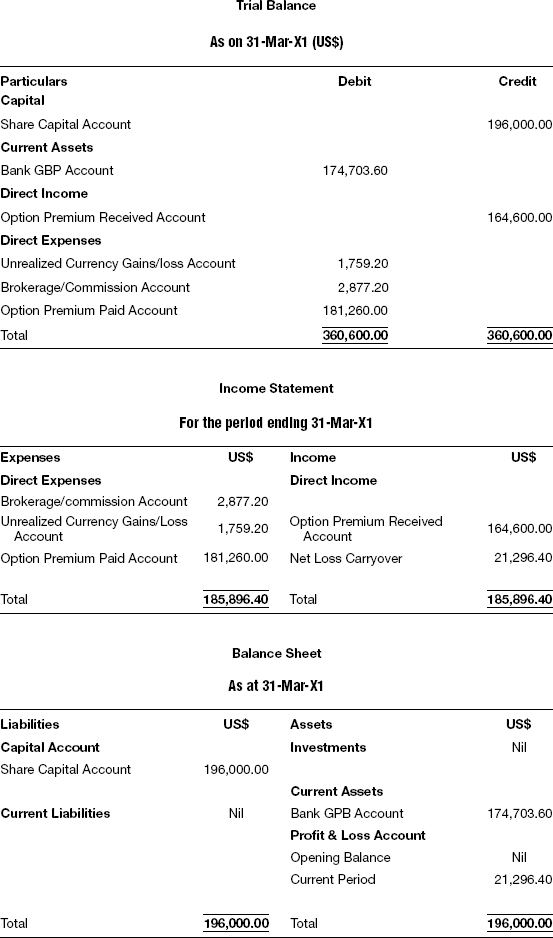

Victory GBP Fund had the following trades in Beacon shares in the options market on the London stock exchange through Silver Man brokers. The stock exchange requires that the writer of the options maintain 10 percent of the value of the contract as margin money throughout the life of the contract. On January 1, GBP100,000 was introduced into the fund as capital. Journal entries, general ledgers, trial balance, income statement, and balance sheet are as follows:

Liquidation Method

FIFO

Market Rate of Underlying Beacon Shares

January 31: GBP40.00

February 28: GBP55.00

March 16-Mar-X1: GBP55.00

Market Rate of Beacon Call Option with Strike Price £50, Expiry March 16

January 31: GBP2

February 28: GBP6.00

Settle Price

March 16: GBP55.00

FX Rates: US$/GBP

| Date | Rate |

| 1-Jan-X1 | 1.9600 |

| 23-Jan-X1 | 1.9800 |

| 31-Jan-X1 | 1.9600 |

| 23-Feb-X1 | 1.9200 |

| 28-Feb-X1 | 1.9400 |

| 10-Mar-X1 | 1.9300 |

| 16-Mar-X1 | 1.9400 |

| 31-Mar-X1 | 1.9300 |

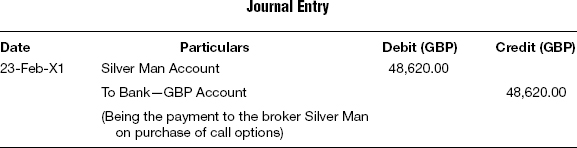

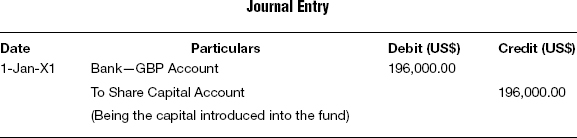

Long Call Options—Trade Currency GBP

T-1 Conversion of US$ into GBP

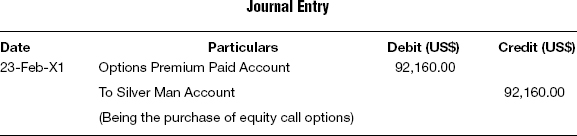

T-2 On Purchase of Call Option

T-3 Brokerage/Commission

T-4 On Payment of Contracted Sum

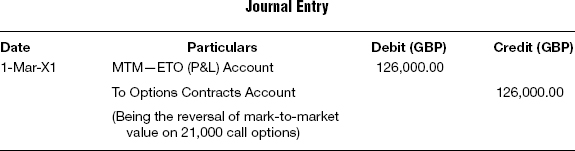

T-5 Market Value at End of Reporting Period

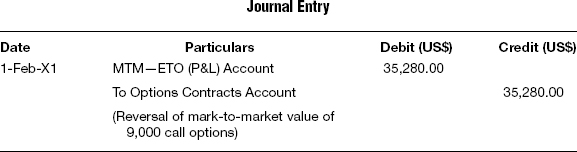

T-6 Reversal of Mark-to-market Value

T-7 On Purchase of Call Option

T-8 Brokerage/Commission

T-9 Payment of Contracted Sum

T-10 Market Value at End of Reporting Period

T-11 Reversal of Mark-to-market

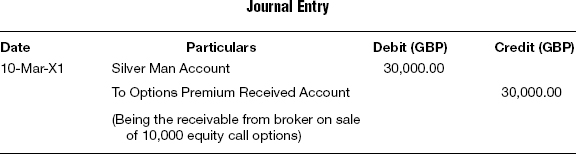

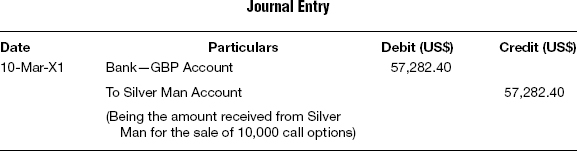

T-12 Sale of the Call Options

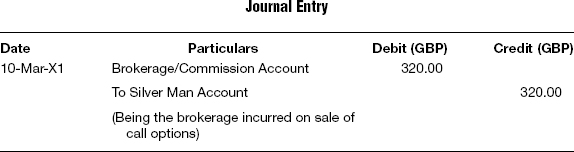

T-13 Brokerage/Commission on Sale

T-14 On Receipt of Sale Proceeds

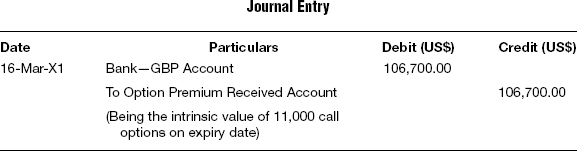

T-15 On Expiry of Call Options

Long Call Options—Functional Currency US$

The following are the FX revaluation entries in the functional currency converted at the respective FX rate, which is given within parenthesis. FX translation entries are clearly specified, indicating whether each is a consummated FX translation entry or a transient FX translation entry.

F-1 Conversion of GBP into US$ (T-1 @ FX Rate: 1.9600)

F-2 On Purchase of Call Options (T-2 @ FX Rate: 1.9800)

F-3 Brokerage/Commission (T-3 @ FX Rate: 1.9800)

F-4 Payment of Contracted Sum (T-4 @ FX Rate: 1.9800)

F-5 Market Value at End of Reporting Period (T-5 @ FX Rate: 1.9600)

F-6 Reversal of Mark-to-market Value (T-6 @ FX Rate: 1.9600)

F-7 On Purchase of Call Options (T-7 @ FX Rate: 1.9200)

F-8 Brokerage/Commission (T-8 @ FX Rate: 1.9200)

F-9 On Payment of Contracted Sum (T-9 @ FX Rate: 1.9200)

F-10 Market Value at End of Reporting Period (T-10 @ FX Rate: 1.9400)

F-11 Reversal of Mark-to-market Value (T-11 @ FX Rate: 1.9400)

F-12 Sale of Call Options (T-12 @ FX Rate: 1.9300)

F-13 Brokerage/Commission on Sale (T-13 @ FX Rate: 1.9300)

F-14 Receipt of Sale Proceeds (T-14 @ FX Rate: 1.9600)

F-15 On Expiry Date of Call Options (T-15 @ FX Rate: 1.9400)

F-16 FX Translation on Bank Account (Transient FX Translation Entry)

TRADE LIFE CYCLE FOR EXCHANGE-TRADED OPTIONS—ON WRITING A CALL OPTION

- Deposit the margin on options to the exchange.

- Writing the call options.

- Brokerage/commission on the transaction.

- Receive the premium on the call options sold.

- Ascertain the fair value at the end of reporting period.

- Margin call.

- Expiry of options.

- Exercise of options.

- Buy back the call options.

- Ascertain the profit/loss on the sale.

- Get back the deposit of margin money.

- FX revaluation entries.

- FX translation entries.

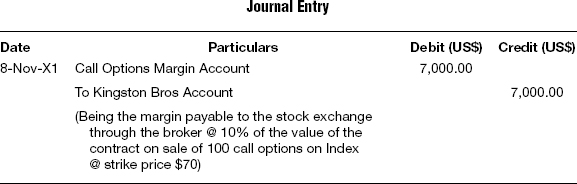

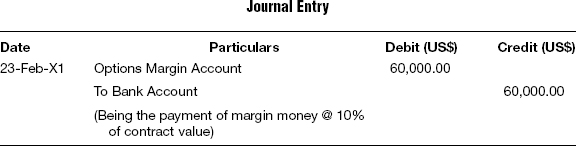

Deposit the Margin on Options

Margin is payable to the exchange if the investor writes the option. For exchange-traded options (ETOs), since the stock exchange has the responsibility of ensuring that both the legs of the transaction are complete, the exchange would insist that the writer of the option deposit a percentage of the value of the contract as margin money. This is because potentially the writer of an option has unlimited risk. The margin money would be adjusted against any reduction in the marked-to-market valuation on a daily basis.

Margin is in effect a good faith deposit. Normally a deposit of about 5 to 10 percent of the total value of the contract would signify the willingness to stand good on any price movements against the seller of an options contract. The percentage of deposit would be smaller for index options and higher for stock options. Since it is merely a deposit, the investor would get the margin money back after the contract is liquidated.

Assume that an investor wants to sell 1,000 call options on an index at $6, strike price being $70, and the stock exchange insists on an up-front margin of 10 percent of the value of the contract from the option writer. Expiry of the contract is December 16, and the broker through whom the trade is executed is Kingston Bros. The margin payable to the exchange through the broker would be 10 percent of $70,000, or $7,000.

The accounting entry that is recorded in the books of accounts is shown as follows:

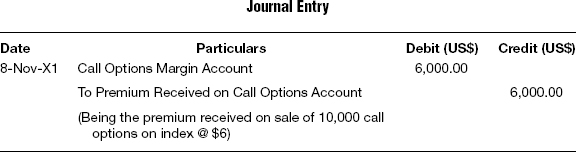

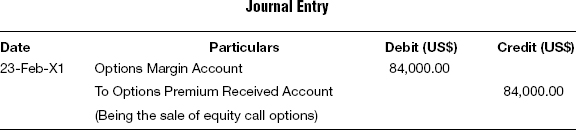

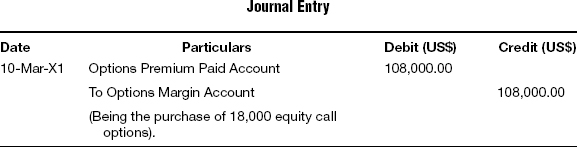

Writing the Call Options

If the investor writes a call option, he receives a premium. The premium is normally credited to the margin account already available with the counterparty on the settlement date of the option contract.

The accounting entry that is recorded in the books of accounts is shown as follows:

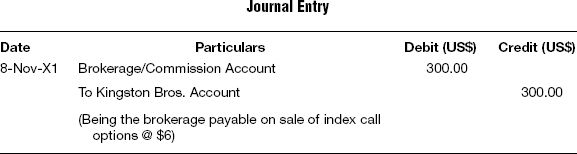

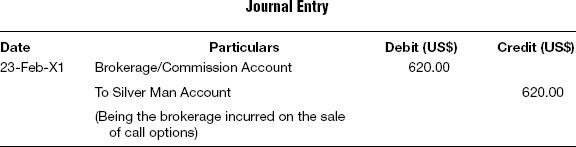

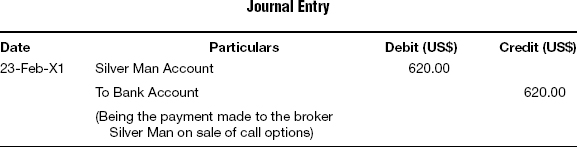

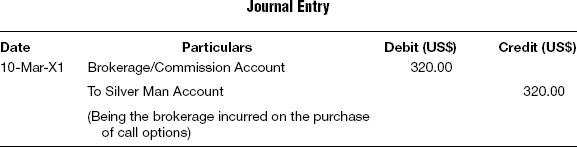

Brokerage/Commission on Sale of Options

The broker charges a commission for the services rendered. For option contracts, the brokerage/commission is not treated as a reduction from the sale consideration of the options contract but instead it is debited to the brokerage/commission account.

Assume that the brokerage payable is $300 for this deal. The accounting entry that is recorded in the books of accounts is shown as follows:

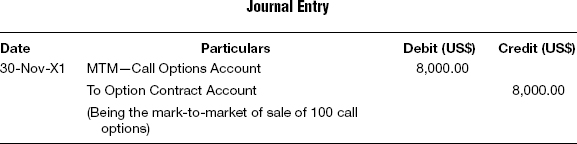

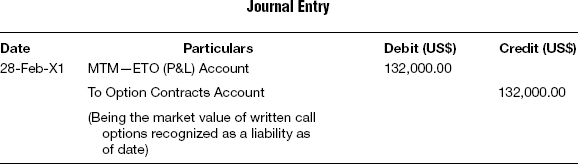

Ascertain the Fair Value at the End of the Reporting Period

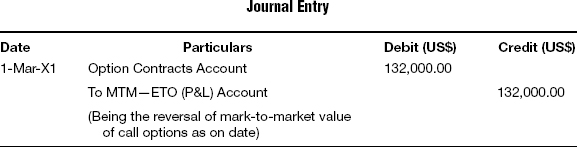

At the end of every reporting period the fair value of the options is ascertained and the options contracts are marked-to-market. This process is known as portfolio valuation, when the market rate at the end of the period is determined from the primary stock exchange where the underlying shares are traded. If there is a decrease in the market rate below the sale rate, then such decrease is recognized as a gain, on the one hand, and the corresponding amount is reflected as a decrease in the liability on account of such options. This accounting entry is reversed on the next day or the next valuation date when a fresh entry for the then value is recorded in the books of accounts. Alternatively, the accounting entry can be recorded only for the incremental value. If the investor follows this incremental value method, then there is no need to reverse the entry for mark-to-market recorded earlier.

Assuming that the market rate of the call options as of November 30, which is the next valuation date, is $8, then the accounting entry that is recorded in the books of accounts is as follows:

Margin Call on Options

If the margin money gets eroded due to unfavorable price movement for the investor, then the exchange would initiate a margin call. This is to ensure that the exchange does not get caught unawares if there is a wide fluctuation in the value of the underlying, causing severe loss to the investor. The stock exchange would require that there be sufficient margin money to take care of this.

Assuming that on November 30, the price of the call options shoots up to $20, then the stock exchange would initiate a margin call to compensate the erosion in the margin account of the investor. The margin amount paid initially, amounting to $7,000, would be completely eroded by this unfavorable price movement to the investor. The investor would be required to pay an amount equal to 10 percent of the value of the position after such price movement in addition to the potential loss as of that date.

In this case, assume that the value of the underlying has moved from $65 on the date of sale of the call options to $95, resulting in the price of the call option going up to $20. Even though the potential loss as of this date in this case is 25,000 calculated as (Strike price − Current market price of the underlying share) × quantity ie (70 − 95) × 1000 = 25,000, the broker concerned is likely to make the margin call calculated based on the actual loss incurred as on date which is (Sale price of option − Market price of option) × quantity ie (6 − 20) × 1000 = 14,000 as increased by 10 percent margin based on the value of the position amounting to 9,500 and reduced by the margin money already paid by the investor of 7,000 resulting in a margin call of 16,500.

The accounting entry that is recorded in the books of accounts is shown as follows:

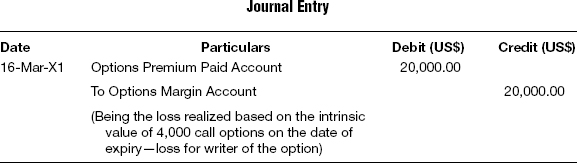

Expiry of Options

The options expire on the expiry date of the contract. For call options that are written, the excess amount of the market value of the underlying over and above the strike price of the options represents the loss for the investor. In such case, the call option is said to expire in-the-money. Conversely, if the call options expire out-of-the-money—that is, if the market value of the underlying is less than the strike price of the option—then the premium received by the investor represents the profit. The maximum profit that could be earned by the investor shorting or writing in a call option can never exceed the premium received on the sale of the call option.

Case 1: When the options expire worthless, there is no need to record any entry in the books of accounts. The option premium received is already treated as an income, and since the options expire worthless there is no need to record any other entry on the expiry date.

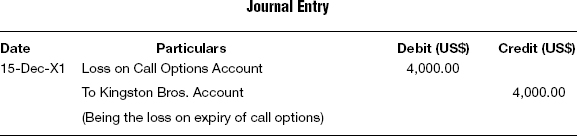

Case 2: When the options expire in-the-money, in other words when the market rate of the underlying is more than the strike price of the option, then the value of the underlying that exceeds the strike price represents the loss accruing to the investor. Assuming that the underlying shares close at $74 on the expiry date, the accounting entry that is recorded in the books of accounts is shown as follows:

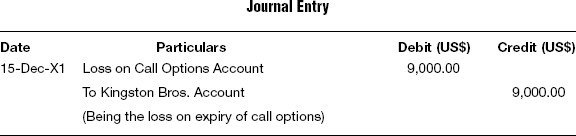

Case 3: The investor incurs a loss when the options expire in-the-money—that is, when the market rate of the underlying is more than the strike price of the option and less than the premium received on the sale of such options. Assuming that the underlying shares close at $79 on the expiry date, the accounting entry that is recorded in the books of accounts is shown as follows:

Exercise of Options

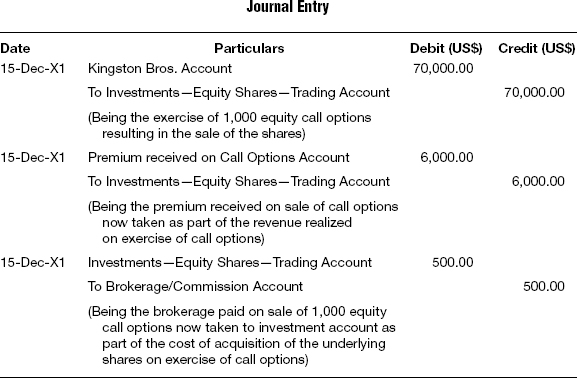

The seller of the call option has the obligation to deliver the underlying at the strike price, if exercised by the buyer of the option. When the call options are exercised, it results in the delivery of the underlying asset. In such a scenario, the investor has to deliver the underlying at the contracted strike price. The actual realization of the underlying asset would then be the strike price of the contract as increased by the premium received on such sale of the call option.

Exercise of options happens only in the case of stock options and not in the case of options on indexes. Assume that the options are exercised on the date of expiry when the price of the underlying share is $80 and the equity shares are held for trading purposes. The accounting entry that is recorded in the books of accounts is shown as follows:

Buy Back the Call Options

The short position of call options could be covered by buying back such options. The buyback results in squaring up of the existing short position. The overall open interest could come down on liquidation of the call option if it is purchased by someone who already has a short position.

Assuming that the call options are bought back at $9 per option, then the accounting entry that is recorded in the books of accounts is shown as follows:

Ascertain the Profit/Loss on the Buyback

Since the premium received and the premium paid are directly accounted for as income and expense, respectively, there is no need to record any separate entry to ascertain the profit or loss on the buyback of the option contract.

Get Back the Deposit of Margin Money

Once the short positions are squared off, the exchange would automatically release the margin money to the investor concerned. The entire amount lying to the debit of the call options margin account will be returned back to the investor.

The accounting entry that is recorded in the books of accounts is shown as follows:

FX Revaluation Entries

All the entries recorded to this point are initially entered in the respective trade currencies. If the functional currency is different from the trade currency, then each and every entry recorded in the trade currency should be entered again in the functional currency by converting the entries at the respective day’s FX rates. In other words, for each trade currency that the investor deals with, there will be a complete set of books representing that trade currency. This includes journal entries, general ledger postings, trial balance, income statement, and balance sheet.

After revaluing each and every journal entry of all the trade currencies into the functional currency, a separate set of books is prepared again comprising all the elements just mentioned: journal entries, general ledger postings, trial balance, income statement, and balance sheet. It should be noted that the ultimate financial reports would be prepared and presented to all the stakeholders based on the financial statements prepared in the functional currency only, as this will encompass all the transactions of the investor in all trade currencies dabbled with. (For illustration and detailed explanation please refer to Chapter 2.)

FX Revaluation Entries

After revaluing all the entries in the functional currency at the respective FX rates for the day concerned, another entry needs to be passed in the books of the functional currency. This is mainly to adjust the currency gains or losses due to the fluctuations in FX rates between the reporting date and the date of recording the original entries. FX translation entries are recorded only for the asset and liability accounts. For income and expense accounts the amount gets crystallized on the date of passing the FX revaluation entries in the books of the functional currency.

There are fundamentally two types of FX translation entries that are recorded in the books of the functional currency: consummated FX translation entries and transient FX translation entries. (For illustration and detailed explanation please refer to Chapter 2.)

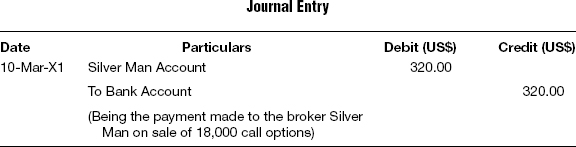

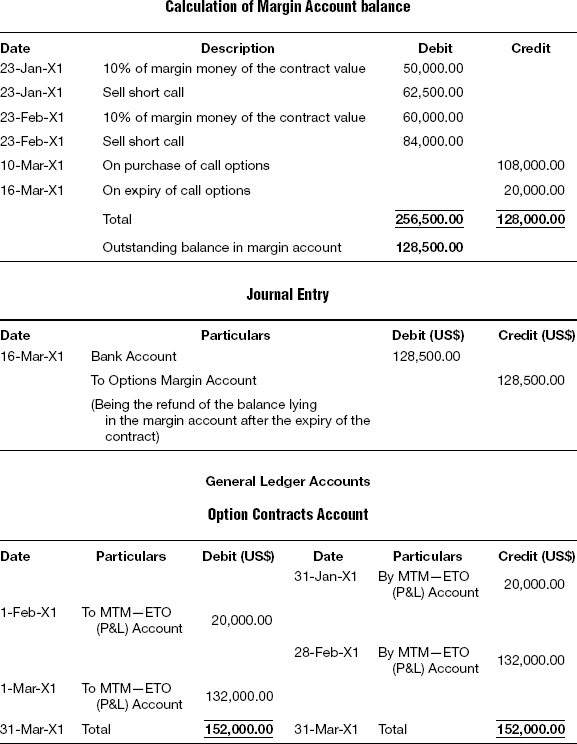

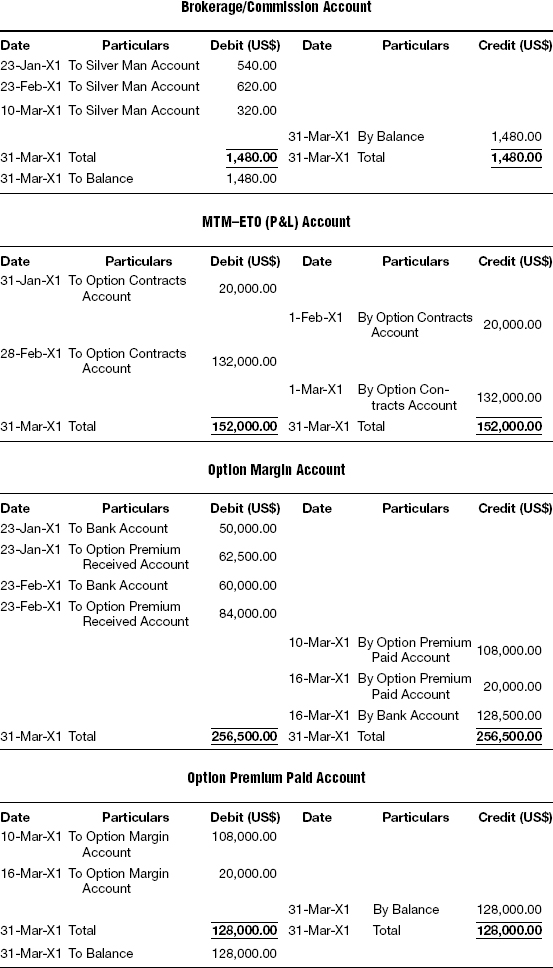

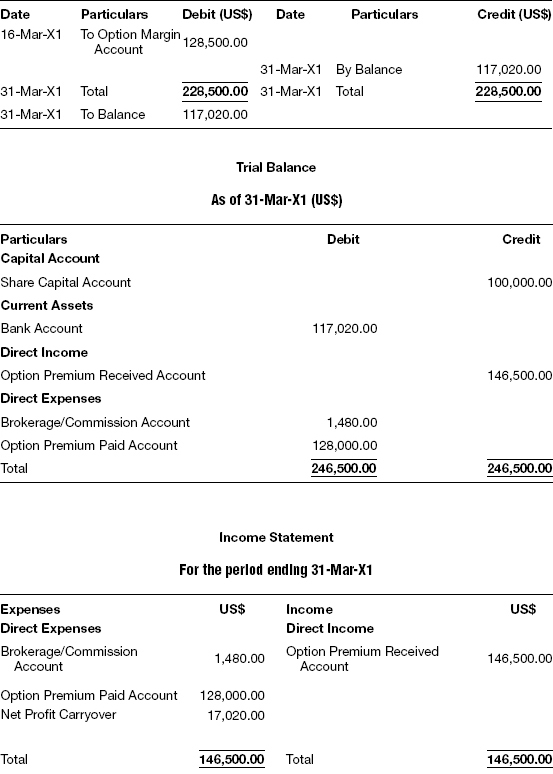

Writing Call Options

Victory Fund had the following trades in Metadata in the options market through Silver Man brokers. The stock exchange requires that the writer of the options maintain 10 percent of the value of the contract as margin money throughout the life of the contract. Victory Fund introduced $100,000 as capital as of January 23. Journal entries, general ledgers, trial balance, income statement, and balance sheet are as follows:

Liquidation Method

FIFO

Market Rate of Underlying Stock, Metadata

31-Jan-X1: $40.00

28-Feb-X1: $55.00

16-Mar-X1: $55.00

Market Rate of Metadata Call Option with Strike Price $50, Expiry March 16

31-Jan-X1: 2.00

28-Feb-X1: 6.00

Exercise Price

16-Mar-X1: $55

Short Call Option—Functional Currency US$

T-1 Capital Brought In

T-2 On Payment of Margin Money

T-3 Sale of the Call Options

T-4 Brokerage/Commission

T-5 Payment of Brokerage

T-6 Market Value at End of Reporting Period

T-7 Reversal of Mark-to-market Value of Call Options

T-8 On Payment of Margin Money

T-9 Sale of the Call Option

T-10 Brokerage/Commission

T-11 Payment of Brokerage

T-12 Market Value at End of Reporting Period

T-13 Reversal of Mark-to-market Value of Options

T-14 On Purchase of Call Options

T-15 Brokerage/Commission on Purchase

T-16 Payment of Brokerage

T-17 On Expiry of Call Options

T-18 Refund of Margin

- The accounting treatment of call options prima facie will depend upon the intention with which the call options are purchased—hedging or speculation (non-hedging).

- If the position is taken as a hedge against some other position, then the relevant accounting standards for hedge accounting will be applicable and there are certain conditions that are to be fulfilled for the same.

- If the call is purchased purely as a speculative trade, then the premium paid towards purchase of the call option is taken to the expense and the premium received on sale of the options is treated as revenue.

- However, the value of the option is written back on the valuation date and shown as an asset in the case of purchase of call options. In effect, the net result of this method of accounting and the one shown for hedging activity would be the same.

Theory Questions

1. Explain the trade life cycle for call options.

2. Is accounting for call options any different if the options were to be held as hedge and not as investment?

Objective Questions

1. Premium paid towards purchase of call options purchased for speculative trade should be treated as

a. Expense

b. Revenue

c. Loss

d. Gain

2. For an options contract, the commission/brokerage paid is treated as follows:

a. Part of the cost of options contract

b. Debited to commission/brokerage account

c. Adjusted later in the broker account at the time of sale

d. None of the above

3. For ascertaining fair value at the end of the reporting period, the value of the entire position will be written back to the

a. Profit and loss account

b. Expense account

c. Income account

d. None of the above

4. Reversal of marked-to-market entry will happen on

a. Next business day

b. Next valuation day

c. Same day itself

d. None of the above

5. For call options (bought), if the market value of the underlying asset is over the strike price of the contact, then the excess amount denotes

a. Profit

b. Loss

c. Breakeven

d. None of the above

6. When the options contract is expired, then the option premium paid denotes

a. Expense

b. Income

c. Gain

d. None of the above

7. Exercising of an options contract means

a. Creation of underlying asset

b. Breaking the options contract

c. Paying the margin amount

d. None of the above

8. Buyback of the call options results in

a. Creating a fresh contract

b. Squaring up of the existing short position

c. Creating a long position

d. None of the above

9. Account treatment for a call options contract is decided based on

a. Position of the contract

b. Intention of the purchase

c. Size of the contract

d. None of the above

10. Assume that a call option with a quantity of 10,000 shares and a premium of $6,000 has a value of $9 at the end of the reporting period. Which of the following amounts is recognized as income which reflects as an asset on the balance sheet?

a. $9,000

b. $96,000

c. $84,000

d. $90,000

e. $9,600

11. The accounting entry for mark-to-market reversal of a call option is not required if the valuation is done using the

a. Reversal method at the end of reporting period

b. Black-Scholes model

c. Incremental value method

d. End of period market price

e. Beginning of period market price

12. When the call options are exercised, the investor has to pay for the underlying at

a. The current market price of the stock

b. The rate at which the exchange decides

c. The contracted strike price

d. The previous day’s closing price

e. None of the above

13. If an investor writes a call option, then the investor ______________ on such writing of the call option.

a. Would pay the premium on the exercise date

b. Would collect the premium on the exercise date

c. Would pay the premium on the settlement date

d. Would collect the premium on the settlement date

e. Would neither collect nor pay any premium

14. When a call margin is initiated the investor would be required to pay an amount equal to ______ of the value of the position in addition to the potential loss as of that date.

a. 8 percent

b. 15 percent

c. 25 percent

d. 12 percent

e. 10 percent

Journal Questions

Journalize the following:

Mr. Berkowitz buys 1,000 equity call options of Normal Electricals for $4 per share for a strike price of $25 on June 12, expiry date being July 16. Brokerage is 0.25 percent and is settled on T + 2 basis. Pass necessary journal entries for the following events:

1. Purchase of the options.

2. Brokerage paid for purchase.

3. At the end of the reporting period, June 30, the shares are quoted at $28 per share and the options were worth $2 per share. Ascertain the fair value at that time and pass entries.

4. Assume the options are exercised on the expiry date and for the price of $27. Pass relevant journal entries on July 16, the expiry date.

Long Call, Non-hedging—Functional Currency US$

Prepare journal entries, general ledgers, trial balance, income statement, and balance sheet for the following scenario.

Freedom Fund had the following trades in GE in the options market through ADC brokers, and on January 1 introduced $100,000 as capital.

Liquidation Method

FIFO

Market Rate of Underlying Stock, GE

January 31: 40.00

February 28: 55.00

March 16: 55.00

Market Rate of GE Call Option with Strike Price $50, Expiry March 16

January 31: 2.00

February 28: 6.00

Functional Currency

US$

Long Call, Non-hedging—Trade Currency AUD

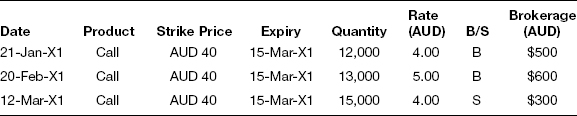

Prepare journal entries, general ledgers, trial balance, income statement, and balance sheet for the following scenario:

AA Fund had the following trades in Metadata in the options market through DDT Man brokers. The stock exchange requires that the writer of the options maintain 10 percent of the value of the contract as margin money throughout the life of the contract. On January 1, AA Fund introduced $100,000 as capital and converted US$50,000 into AUD at the rate of 1.25.

Liquidation Method

FIFO

Market Rate of Underlying Stock, Metadata (AUD)

January 31: 35.00

February 28: 40.00

March 16: 45.00

Market Rate of Metadata Call Option with Strike Price $40, Expiry March 15

January 31: 3.00

February 28: 5.00

FX Rate AUD/US$

January 21: 1.2178

January 31: 1.28964

February 20: 1.26345

February 28: 1.24789

March 12: 1.23645

March 15: 1.27893

Functional Currency

US$

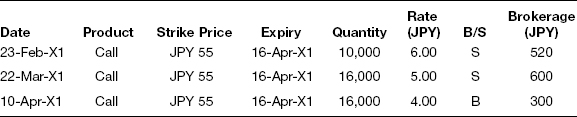

Short Call, Non-hedging—Trade Currency JPY

Prepare journal entries, general ledgers, trial balance, income statement, and balance sheet for the following scenario:

Stone Fund had the following trades in Gamut in the options market through MML brokers. The stock exchange requires that the writer of the options maintain 15 percent of the value of the contract as margin money throughout the life of the contract. On February 1, Stone Fund introduced $150,000 as capital and converted half of it into JPY at 122.50.

Liquidation Method

FIFO

Market Rate of Underlying Stock, Gamut

February 28: 59.00

March 31: 58.00

April 16: 61.00

Market Rate of Gamut Call Option with Strike Price $55, Expiry April 16

February 28: 5.00

March 31: 4.00

FX Rate JPY/US$

February 23: 123.589

February 28:122.569

March 22: 124.587

March 31: 124.7891

April 10: 123.1562

April 16: 123.4569

Functional Currency

US$