CHAPTER 7

Accounting for Equity Stock Futures

After studying this chapter, you should have a grasp of the following:

- The trade life cycle of exchange traded equity stock futures.

- Journal entries to be recorded during the different phases of the trade life cycle.

- FX revaluation and FX translation process for these trades.

- Illustration of long stock futures with FX translation.

- Preparation of journal entries and general ledger accounts.

- Preparation of income statement and balance sheet after the equity futures trades are done.

- Illustration of short stock futures with FX translation.

TRADE LIFE CYCLE FOR EQUITY STOCK FUTURES

The sequence of events for trading in equity stock futures is as follows:

1. If you bought futures, then account for the buy trade of equity stock.

2. If you sold futures, then account for the sell trade of equity stock.

3. Transfer the brokerage/commission on the original trade to stock.

4. Perform the FX revaluation entries.

5. Perform the FX translation entries.

Accounting for a Buy Trade

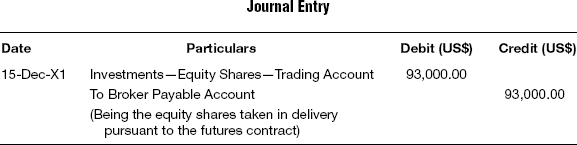

When the investor buys stock futures resulting in physical settlement, then the investor has to pay for the contracted price and take delivery of the stock. The margin money paid will, however, be adjusted against the total money that the investor should pay the exchange. The equity shares will be accounted for as a regular purchase of shares, and the treatment will depend upon whether it is held for trading or as available-for-sale.

Assume that the investor takes delivery of 1,000 shares of Boeing at $93 per share, and assume it is held for trading. The accounting entry that is recorded in the books of accounts is shown as follows:

Accounting for a Sell Trade

Similarly, when the futures are sold and the trade results in physical settlement, then the physical shares should be delivered by the investor to the exchange, and the transaction is recorded like a regular sale of equity shares held by the investor. The profit or loss on account of the sale is determined and accounted for accordingly depending upon whether the shares are held as trading or available-for-sale. Assuming that 1,000 shares of Intel are sold at $24 per share, the accounting entry that is recorded in the books of accounts is shown as follows:

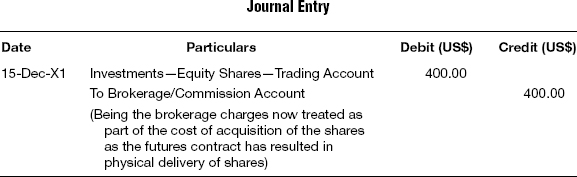

Transferring the Brokerage on the Original Trade to Stock

The brokerage paid on the futures trade would have been directly expensed and not taken as part of the cost of the shares that were to be acquired. Hence, when the futures contract results in physical settlement, then the brokerage originally expensed should be capitalized and taken to the account of the shares concerned. The realized profit or loss will be calculated taking this as part of the cost of shares.

Assume that in the earlier case of purchase of stock futures resulting in physical delivery of shares, the brokerage paid was $400. The accounting entry that is recorded in the books of accounts is shown as follows:

FX Revaluation Entries

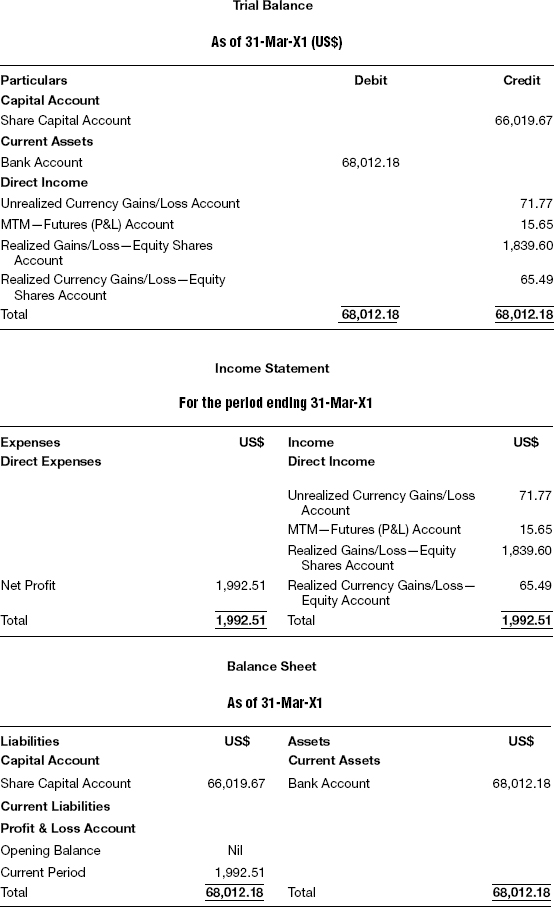

All the entries recorded to this point are initially entered in the respective trade currencies. If the functional currency is different from the trade currency, then each and every entry recorded in the trade currency should be entered again in the functional currency by converting the entries at the respective day’s FX rates. In other words, for each trade currency that the investor deals with, there will be a complete set of books representing that trade currency. This includes journal entries, general ledger postings, trial balance, income statement, and balance sheet.

After revaluing each and every journal entry of all the trade currencies into the functional currency, a separate set of books is prepared comprising all the elements just mentioned: journal entries, general ledger postings, trial balance, income statement, and balance sheet. It should be noted that the ultimate financial reports would be prepared and presented to all the stakeholders based on the financial statements prepared in the functional currency only, as this will encompass all the transactions of the investor in all trade currencies dabbled with. (For illustration and detailed explanation, please refer to Chapter 2.)

FX Revaluation Entries

After revaluing all the entries in the functional currency at the respective FX rates for the day concerned, another entry needs to be passed in the books of the functional currency. This is mainly to adjust the currency gains or losses due to the fluctuations in FX rates between the reporting date and the date of recording the original entries. FX translation entries are recorded only for the asset and liability accounts. For income and expense accounts the amount gets crystallized on the date of passing the FX revaluation entries in the books of the functional currency.

There are fundamentally two types of FX translation entries that are recorded in the books of the functional currency: consummated FX translation entries and transient FX translation entries. (For illustration and detailed explanation, please refer to Chapter 2.)

Consider the following examples.

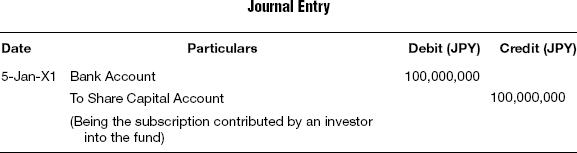

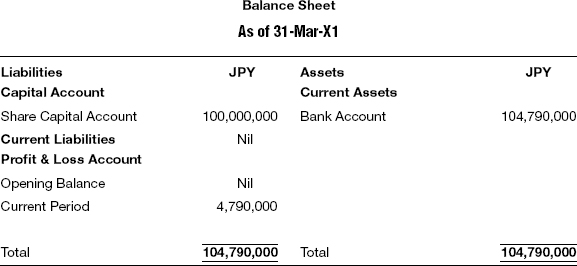

Stock Futures—Long Stock, JPY

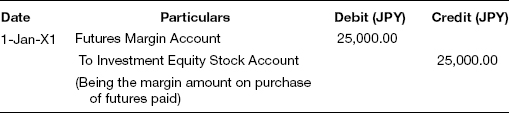

Cerebros Fund had the following trades in ABB in the futures market. The stock exchange requires that a margin of 50 percent of the value of the contract be maintained throughout the life of the contract.

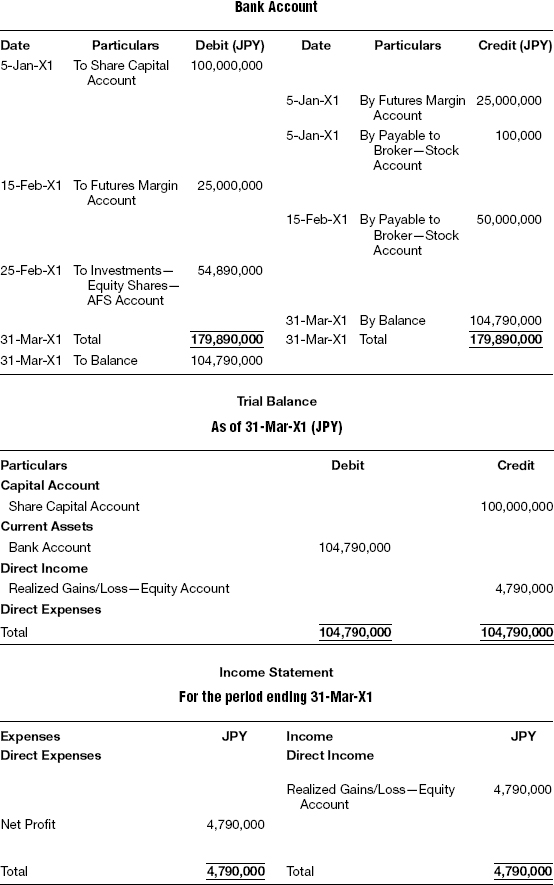

Delivery of the ABB stock was taken on the expiry date of the futures, February 15, when the market rate was JPY 53 per share. Earlier, JPY 100 million was introduced on January 5 as capital into the fund. ABB shares were held with no intention of trading and hence were classified as available-for-sale. Journal entries, general ledgers, trial balance, income statement, and balance sheet must be prepared as follows:

| Date | FX Rate |

| 5-Jan-X1 | 123.805 |

| 31-Jan-X1 | 124.850 |

| 15-Feb-X1 | 124.800 |

| 25-Feb-X1 | 123.560 |

| Date | ABB Market Price |

| 31-Jan-X1 | 52 |

| 15-Feb-X1 | 53 |

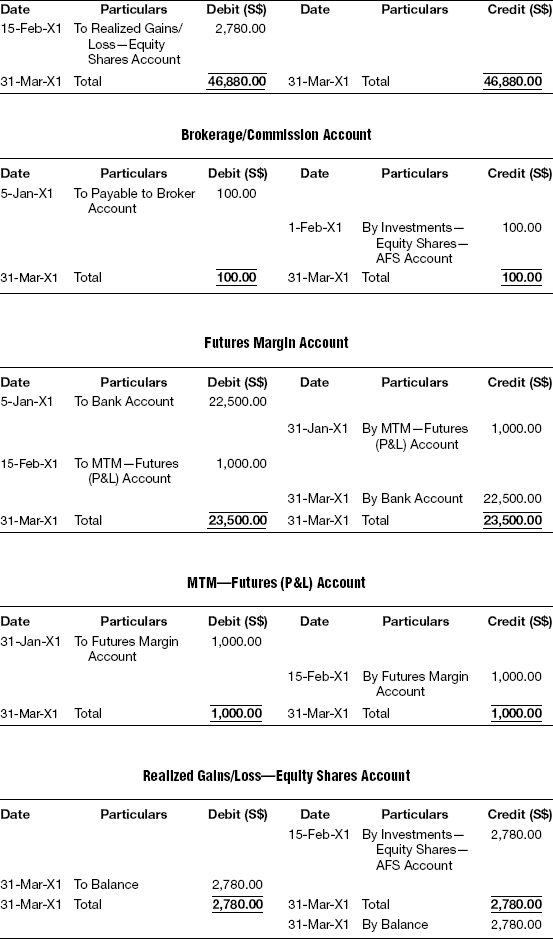

Long Stock Futures—Trade Currency JPY

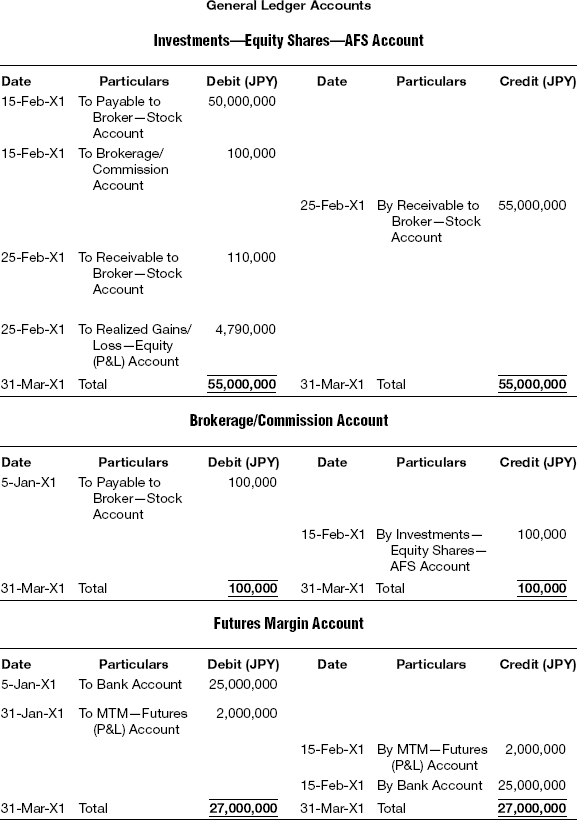

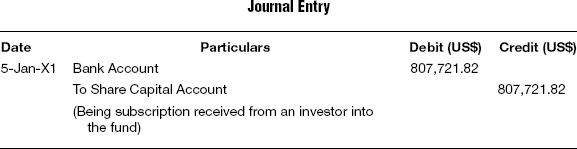

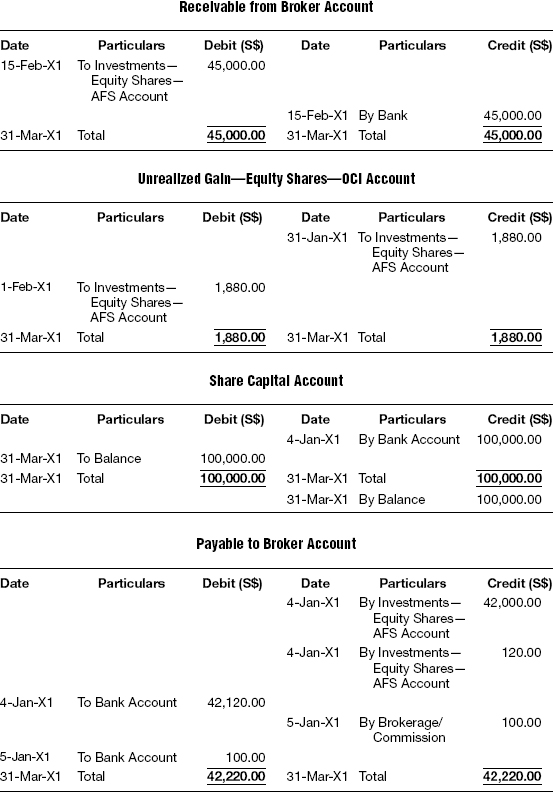

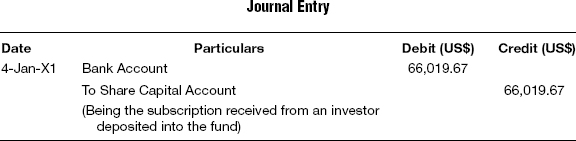

T-1 Capital Introduced by the Fund

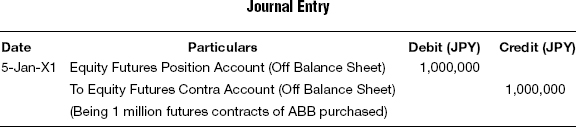

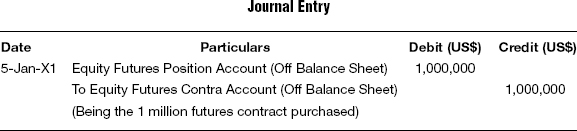

T-2 On Purchasing the Futures

This entry is just an off-balance-sheet entry and thus is not taken into account while preparing the financial statements of the investor. In this illustration, there will not be any postings for this entry.

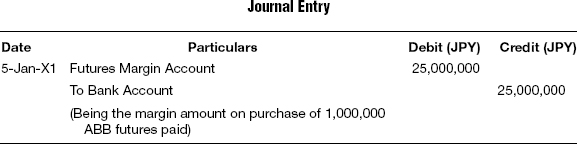

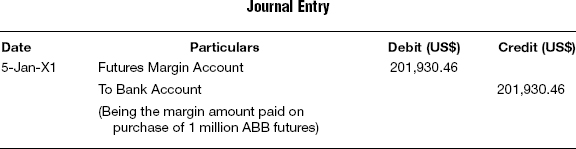

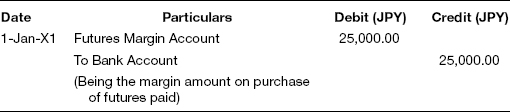

T-3 On Payment of Margin

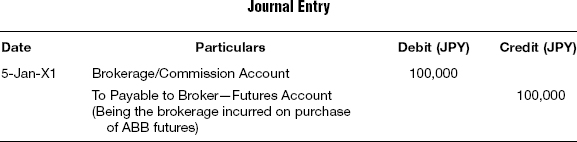

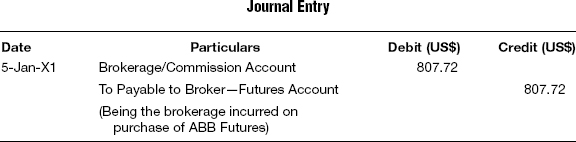

T-4 On Recording the Brokerage/Commission

Brokerage is paid separately. In derivative instruments, it is not treated as part of the cost of acquisition, and hence is directly charged off to the profit and loss account.

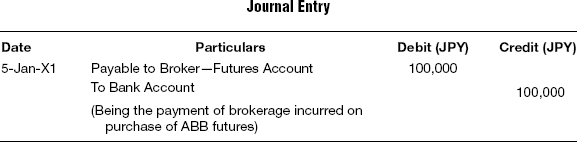

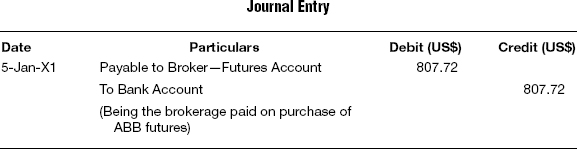

T-5 On Payment of Brokerage/Commission

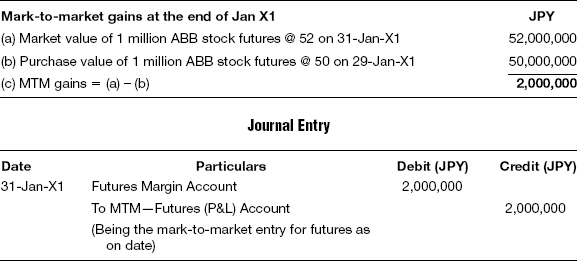

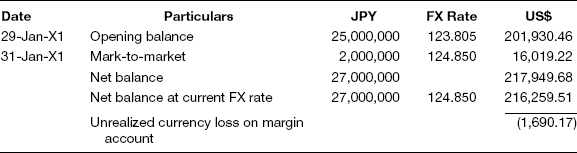

T-6 Mark-to-market at End of Reporting Period

The mark-to-market is computed based on the market rate at the end of each day. However, for this illustration it is assumed that the mark-to-market is computed at the end of the month. If there is a drop in the value of the long position, the same is reduced from the margin account—which eventually is required to be topped up with the erosion in value. Mark-to-market gains are debited to the margin account and the same is credited to the profit and loss account.

T-7 Reversal of Mark-to-market on the Date of Expiry

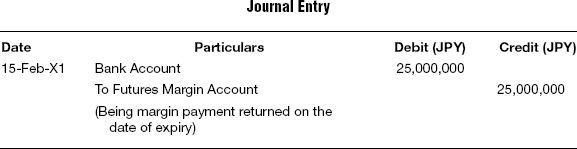

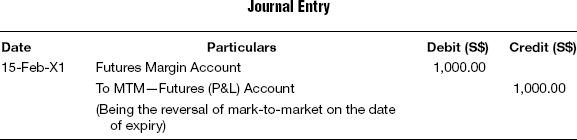

The mark-to-market margin is reversed on the date of expiry of the futures contract as delivery of the underlying stock was taken on the expiry of the futures.

T-8 Margin Payment Returned on the Date of Expiry

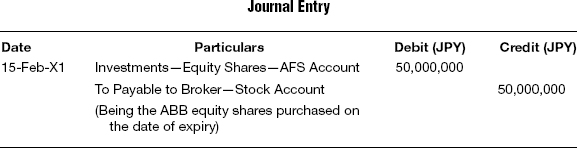

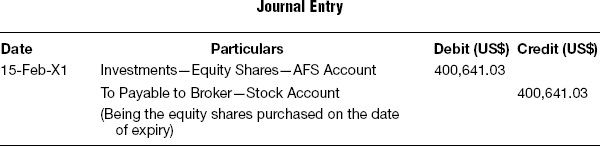

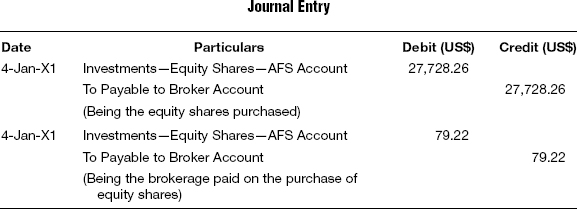

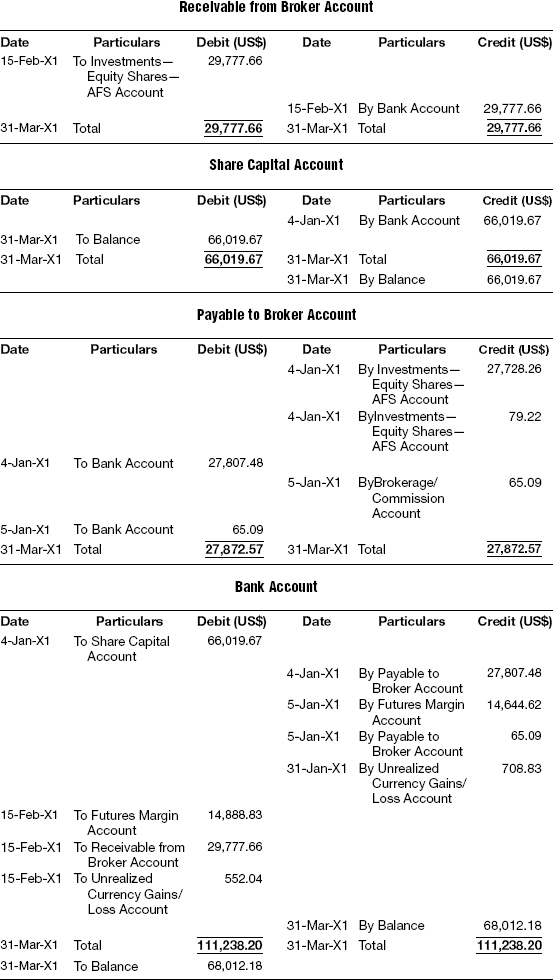

T-9 On Purchase of Equity Shares on the Date of Expiry

Delivery of the underlying shares is taken on the date of expiry of the futures. The equity shares will be recorded at the rate at which the futures are contracted to be bought, as this is the amount that the investor has to pay to acquire the underlying equity shares, irrespective of the market rate of the shares on the date of expiry. In this case, even though the market rate on the date of expiry is 53, the investments account is debited with only 50 as this is the amount that is to be paid to acquire the shares. In the usual practice, the mark-to-market is done on a daily basis and the investments would be marked up to 53, treating the difference of 3 as unrealized capital gains on such investments.

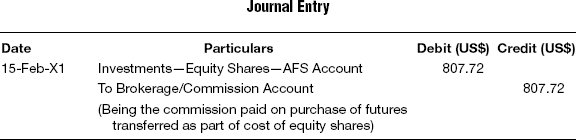

T-10 Commission on Futures Reversed to the Equity Shares

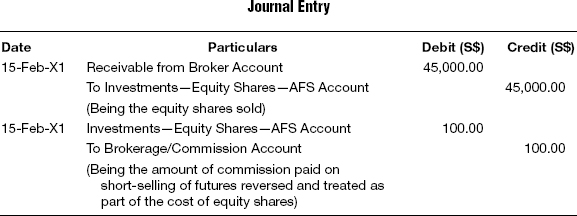

Assuming that the broker does not charge additional commission on taking delivery of the underlying shares on the date of expiry of the futures contract, the commission already paid on the purchase of the futures should be treated as part of the cost of acquisition of the equity shares and hence should be taken to the investments account and the commission account should be reversed.

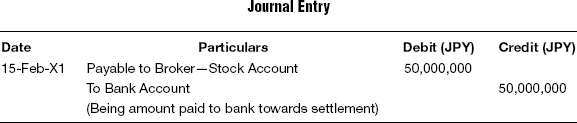

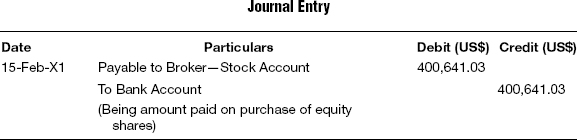

T-11 On Payment for Equity Shares Bought on the Date of Expiry

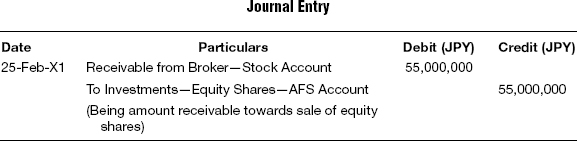

T-12 On Sale of Equity Shares

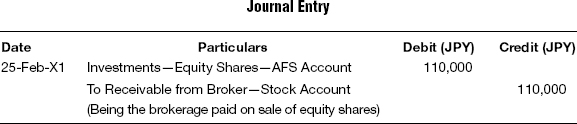

T-13 On Brokerage Paid on Sale of Equity Shares

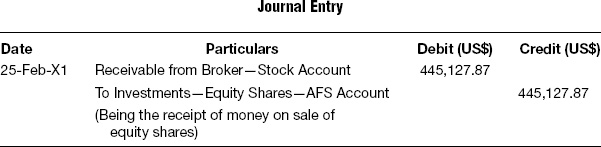

T-14 On Receipt of Money for Sale of Shares

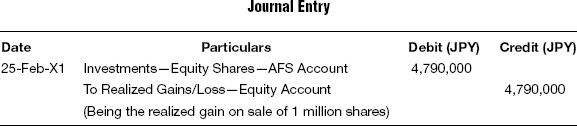

T-15 Recording Profit/Loss on the Sale

Long Stock Futures—Functional Currency US$

The following are the FX revaluation entries in the functional currency converted at the respective FX rate, which is given within parenthesis. FX translation entries are clearly specified, indicating whether each is a consummated FX translation entry or a transient FX translation entry.

F-1 Capital Introduced by the Fund (T-1 @ FX Rate: 123.805)

F-2 On Purchasing the Futures

This entry is just an off-balance-sheet entry and thus is not taken into account while preparing the financial statements of the investor. In this illustration, there will not be any postings for this entry.

F-3 On Payment of Margin (T-3 @ FX Rate: 123.805)

F-4 On Recording the Brokerage/Commission (T-4 @ FX Rate: 123.805)

F-5 On Payment of Brokerage/Commission (T-5 @ FX Rate: 123.805)

F-6 Mark-to-market at End of Reporting Period (T-6 @ FX Rate: 124.850)

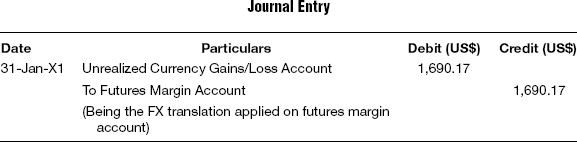

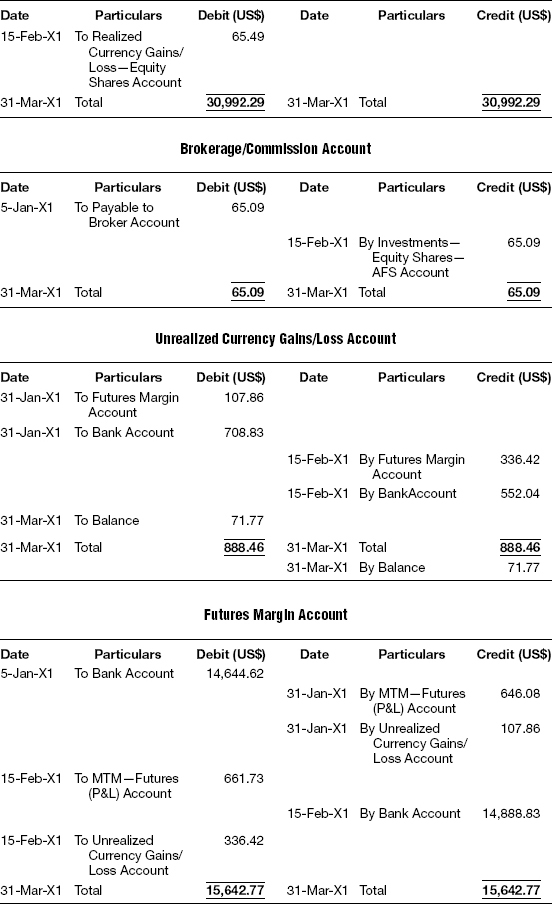

F-7 FX Translation on Futures Margin Account (Transient FX translation entry)

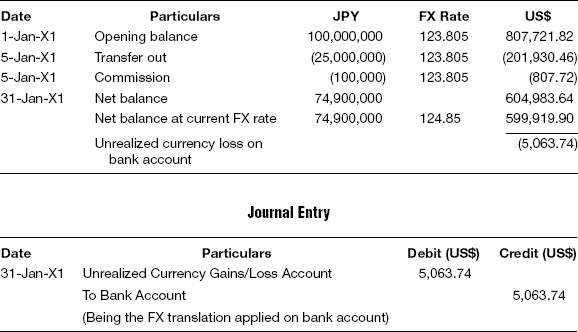

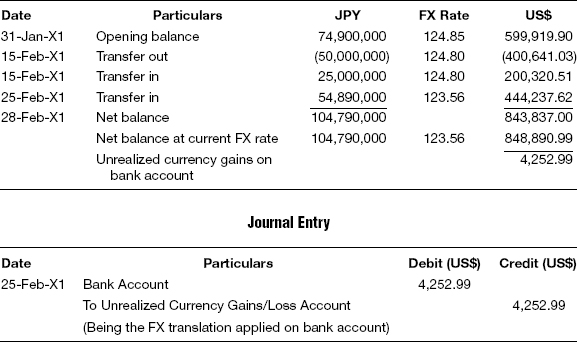

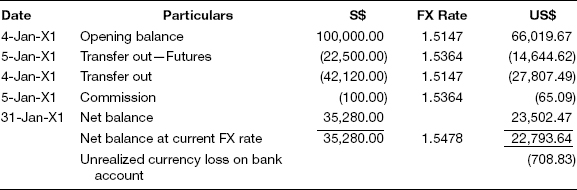

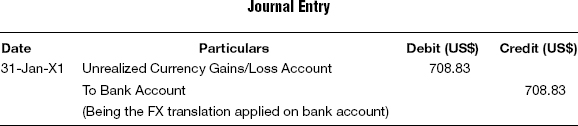

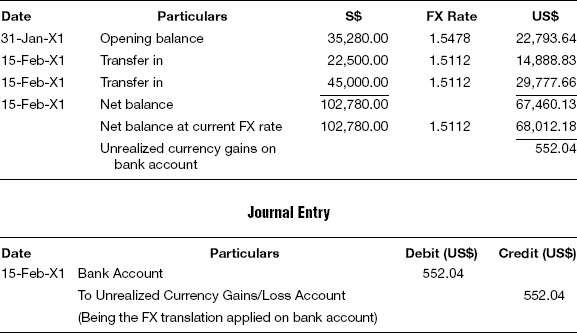

F-8 FX Translation on Bank Account (Transient FX translation entry)

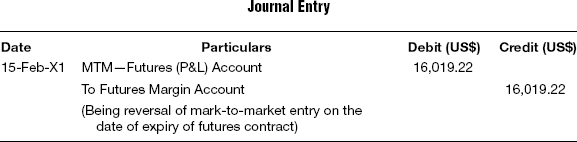

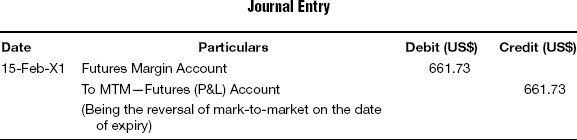

F-9 Mark-to-market Reversal on the Date of Expiry (T-7 @ FX Rate: 124.850)

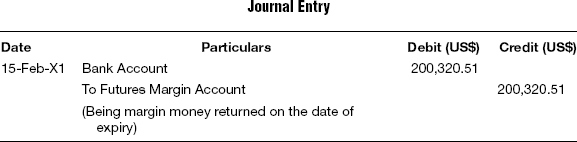

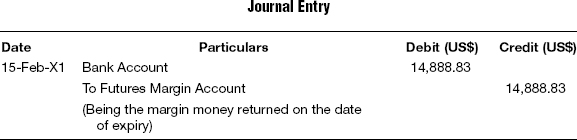

F-10 Margin Payment Returned on the Date of Expiry (T-8 @ FX Rate: 124.800)

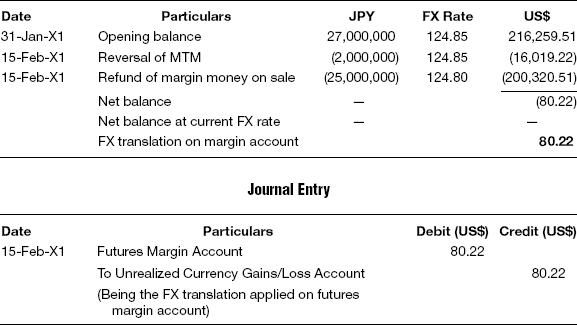

F-11 FX Translation on Futures Margin Account (Transient FX Translation Entry)

F-12 On Purchase of Equity Shares on the Date of Expiry (T-9 @ FX Rate: 124.800)

F-13 Commission on Futures Reversed (T-10 @ FX Rate: 124.800)

F-14 Equity Shares Bought on the Date of Expiry (T-11 @ FX Rate: 124.800)

F-15 Equity Shares Sold (T-12 @ FX Rate: 123.560)

F-16 On Brokerage Paid on Sale of Equity Shares (T-13 @ FX Rate: 123.560)

F-17 On Receipt of Money for Shares Sold (T-14 @ FX Rate: 123.560)

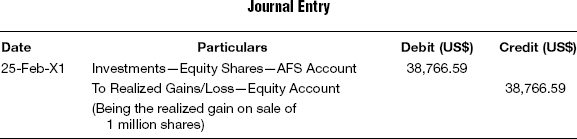

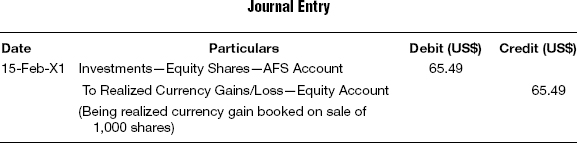

F-18 On Recording Profit/Loss on Sale (T-15 @ FX Rate: 123.560)

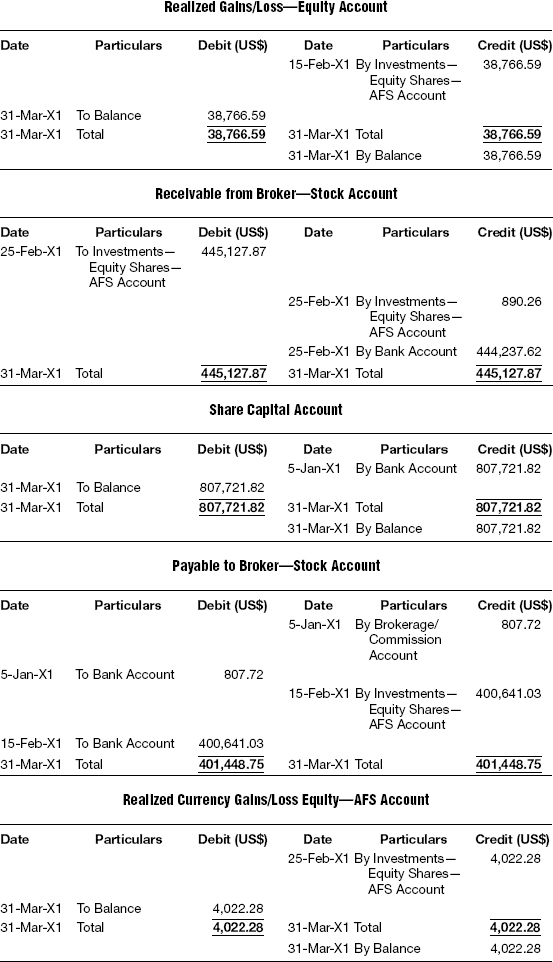

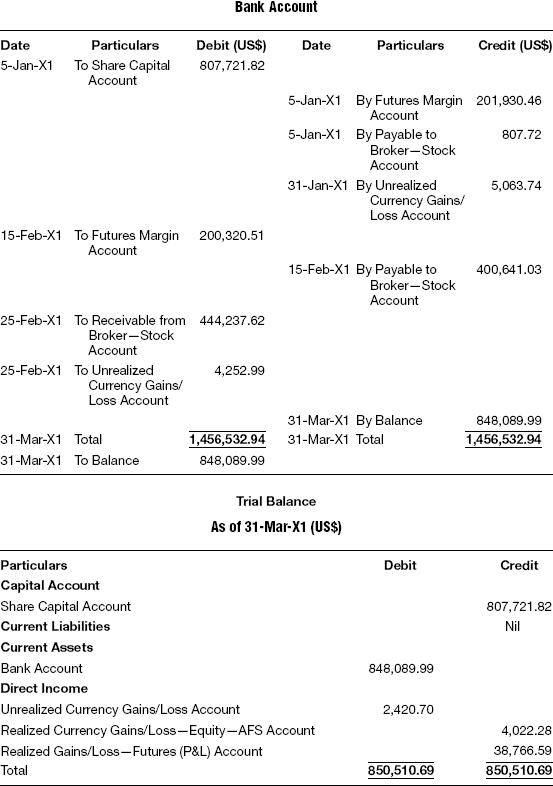

F-19 Realized Currency Gains on Liquidation

F-20 FX Translation on Bank Account (Transient FX Translation Entry)

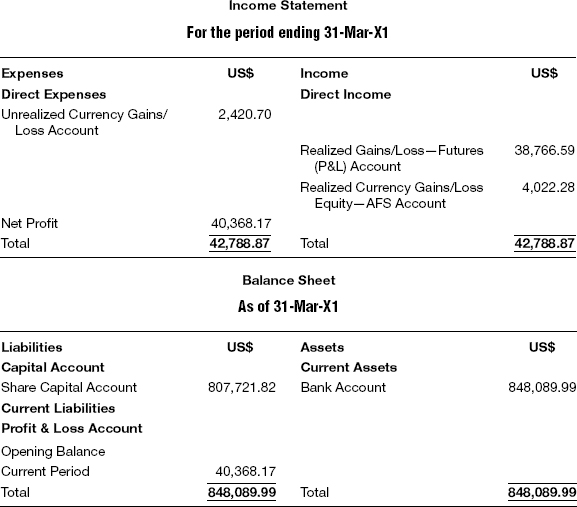

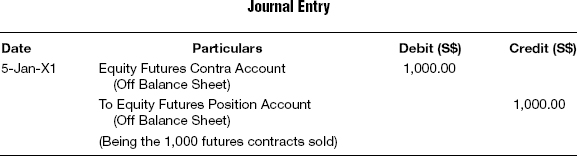

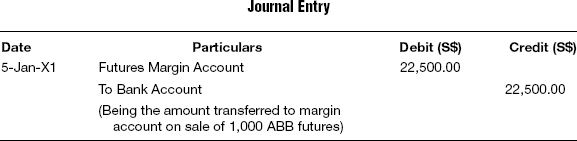

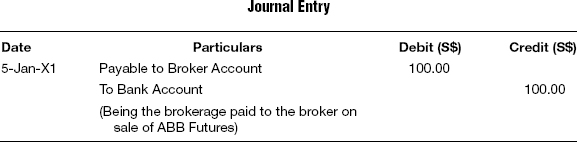

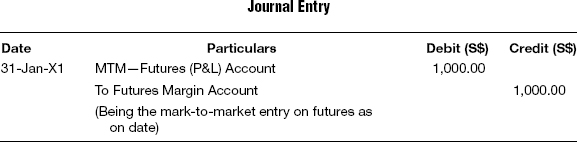

Stock Futures—Short Stock—S$

Cerebros Fund had the following trades in ABB in the futures market. The stock exchange requires that a margin of 50 percent of the value of the contract be maintained throughout the life of the contract.

ABB stock was delivered on the expiry date of the futures, February 15, when the market rate was S$43 each. Earlier, on January 4, the fund introduced S$100,000 as capital. Journal entries, general ledgers, trial balance, income statement, and balance sheet for Cerebros Fund for the period January 1 to February 28 are prepared as follows:

| Date | FX Rate |

| 4-Jan-X1 | 1.5147 |

| 5-Jan-X1 | 1.5364 |

| 31-Jan-X1 | 1.5478 |

| 15-Feb-X1 | 1.5112 |

| Date | Futures Price |

| 31-Jan-X1 | 46 |

| 15-Feb-X1 | 43 |

| 31-Jan-X1 | 44 |

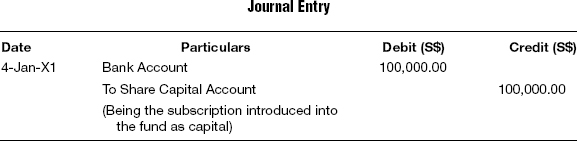

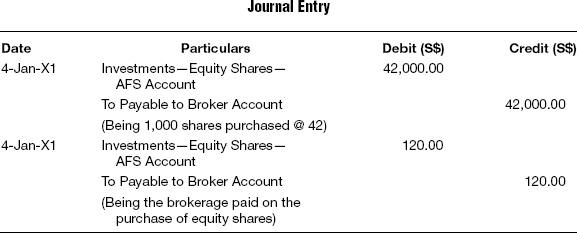

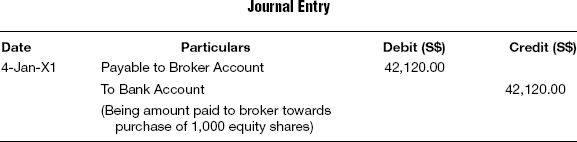

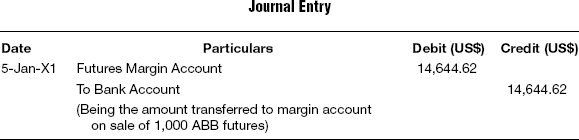

Short Stock Futures—Trade Currency S$

T-1 Capital Introduced by the Fund

T-2 On Purchase of Equity Shares and Brokerage

T-3 On Payment to Broker

T-4 On Sale of Futures Contract

This entry is just an off-balance-sheet entry and thus is not taken into account while preparing the financial statements of the investor. In this illustration, there will not be any postings for this entry.

T-5 On Payment of Margin

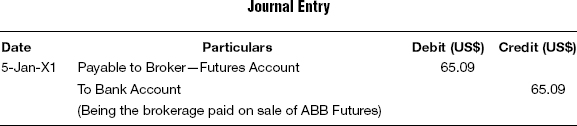

T-6 On Recording the Brokerage/Commission

T-7 On Payment of Brokerage/Commission

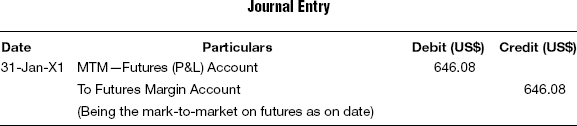

T-8 Mark-to-market at End of Reporting Period—Futures

The mark-to-market is computed based on the market rate at the end of every day. However, for this illustration it is assumed that the mark-to-market is computed at the end of the month. If there is a drop in the value of the long position, the same is reduced from the margin account—which eventually is required to be topped up with the erosion in value. Mark-to-market gains are debited to the margin account and credited to the profit and loss account.

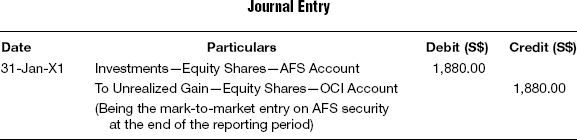

T-9 Mark-to-market at End of Reporting Period—Equity

T-10 Reversal of Mark-to-market on the Next Date for Equity Shares

T-11 Reversal of Mark-to-market on the Date of Expiry

T-12 On Return of Margin Amount on the Date of Expiry

T-13 Equity Shares Sold and Brokerage Paid

T-14 Equity Shares Sold

T-15 Recording Profit/Loss on the Sale

Short Stock Futures—Functional Currency US$

The following are the FX revaluation entries in the functional currency converted at the respective FX rate, which is given within parenthesis. FX translation entries are clearly specified, indicating whether each is a consummated FX translation entry or a transient FX translation entry.

F-1 Capital Introduced by the Fund (T-1 @ FX Rate: 1.5147)

F-2 Equity Shares Purchased and Brokerage Paid (T-2 @ FX Rate: 1.5147)

F-3 On Payment to the Broker on Purchase of Equity Shares (T-3 @ FX Rate: 1.5147)

F-4 On Sale of Futures Contract

F-5 On Payment of Margin (T-5 @ FX Rate: 1.5364)

F-6 On Recording the Brokerage/Commission (T-6 @ FX Rate: 1.5364)

F-7 On Payment of Brokerage/Commission (T-7 @ FX Rate: 1.5364)

F-8 Mark-to-market at End of Reporting Period (T-8 @ FX Rate: 1.5478)

F-9 Mark-to-market at End of Reporting Period—Equity (T-9 @ FX Rate: 1.5478)

F-10 Mark-to-market at End of Reporting Period—Equity (T-10 @ FX Rate: 1.5478)

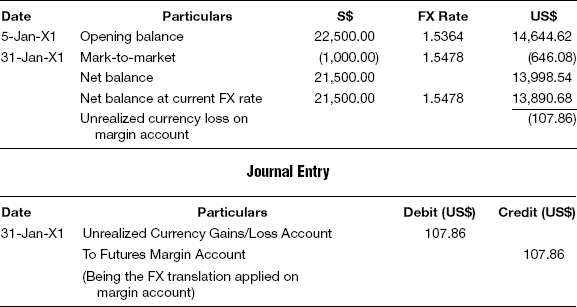

F-11 FX Translation on Futures Margin Account (Transient FX Translation Entry)

F-12 FX Translation on Bank Account (Transient FX Translation Entry)

F-13 Mark-to-market Reversal on the Date of Expiry (T-11 @ FX Rate: 1.5112)

F-14 Margin Amount Returned on the Date of Expiry (T-12 @ FX Rate: 1.5112)

F-15 FX Translation on Futures Margin Account (Transient FX Translation Entry)

F-16 Equity Shares Sold and Brokerage Paid (T-13 @ FX Rate: 1.5112)

F-17 Equity Shares Sold (T-14 @ FX Rate: 1.5112)

F-18 Recording Profit/Loss on the Sale (T-15 @ FX Rate: 1.5112)

F-19 FX Translation—Sale of Equity

F-20 FX Translation on Bank Account

- When the investor buys the stock futures, and if it results in physical settlement, then the investor has to pay the contracted price and take delivery of the stock. The margin money paid will, however, be adjusted against the total money that the investor should pay the exchange.

- The brokerage paid on the futures trade would have been directly expensed and not taken as part of the cost of the shares that was to be acquired.

- When the futures contract results in physical settlement, then the brokerage originally expensed should be capitalized and taken to the concerned shares account.

Objective Questions

1. When an investor buys stock futures, and if it results in physical settlement, then

a. The investor has to pay the margin amount and take delivery of the stock

b. The investor takes the delivery and pays at an agreed upon future date

c. The investor can take the delivery on payment of a meager amount

d. The investor takes the delivery and his broker pays for him

e. The investor has to pay for the contracted price and take delivery of the stock

2. When the stock futures are sold and it results in physical settlement, then the physical shares should be delivered by the investor to

a. The broker

b. The exchange

c. The buyer

d. The custodian of the buyer

e. Any individual who is authorized by the buyer to receive the shares

3. When the futures contract results in physical settlement, then the brokerage originally expensed

a. Should be capitalized and taken to the concerned shares account

b. Should be discounted

c. Should be considered as part of the cost

d. Should be reversed to the investor account

e. Both a and d

4. Which among the following is a correct accounting entry on payment of margin?

a.

b.

c.

d.

e.

5. Assuming a sale of stock futures being liquidation of long stock futures, which among the following is true?

a. Receivable from broker amount will be shown as investments on the asset side of balance sheet

b. Receivable from broker amount will be shown in the P&L account

c. Receivable from broker will be shown as current assets on the balance sheet

d. Receivable from broker shown off balance sheet

e. Receivable from broker will be adjusted to payable to broker

Journal Questions

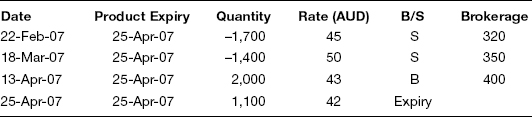

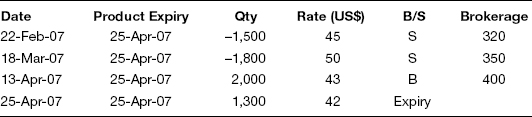

Short Futures—Trade Currency AUD, Functional Currency US$

6. For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet.

XYZ Fund had the following trades in ABB in the futures market. The stock exchange requires that a margin of 20 percent of the value of the contract be maintained throughout the life of the contract.

| Date | FX Rate |

| 22-Feb-07 | 1.18182 |

| 28-Feb-07 | 1.17762 |

| 15-Mar-07 | 1.18322 |

| 31-Mar-07 | 1.17521 |

| 10-Apr-07 | 1.18231 |

| 25-Apr-07 | 1.17425 |

| Date | Market Price |

| 22-Feb-07 | 47 |

| 28-Feb-07 | 55 |

| 31-Mar-07 | 43 |

| 25-Apr-07 | 45 |

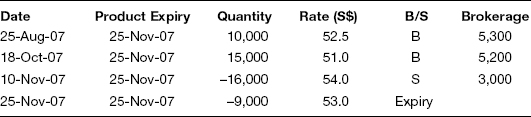

Long Futures—Trade Currency S$, Functional Currency US$

7. For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet.

AA Fund had the following trades in ABC in the futures market. The stock exchange requires that a margin of 10 percent of the value of the contract be maintained throughout the life of the contract.

| Date | FX Rate |

| 25-Aug-07 | 1.5389 |

| 31-Aug-07 | 1.5432 |

| 30-Sep-07 | 1.5535 |

| 18-Oct-07 | 1.5375 |

| 31-Oct-07 | 1.5296 |

| 10-Nov-07 | 1.5431 |

| 25-Nov-07 | 1.5159 |

| Date | Market Price |

| 31-Aug-07 | 49 |

| 30-Sep-07 | 47 |

| 31-Oct-07 | 53 |

| 25-Nov-07 | 57 |

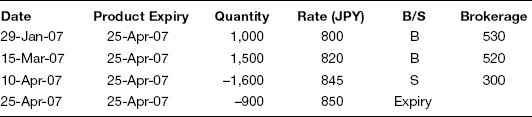

Long Futures—Trade Currency JPY, Functional Currency US$

8. For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet:

AA Fund had the following trades in ABC in the futures market. The stock exchange requires that a margin of 30 percent of the value of the contract be maintained throughout the life of the contract.

| Date | FX Rrate |

| 1-Jan-07 | 123.805 |

| 29-Jan-07 | 124.850 |

| 31-Jan-07 | 125.705 |

| 28-Feb-07 | 124.805 |

| 15-Mar-07 | 125.705 |

| 31-Mar-07 | 125.205 |

| 10-Apr-07 | 124.235 |

| 25-Apr-07 | 124.569 |

| Date | Market Price |

| 31-Jan-07 | 750 |

| 28-Feb-07 | 770 |

| 31-Mar-07 | 855 |

| 25-Apr-07 | 857 |

Short Futures—Functional Currency US$

9. For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet:

ABC Fund had the following trades in IBM in the futures market. The stock exchange requires that a margin of 15 percent of the value of the contract be maintained throughout the life of the contract.

| Date | Market Price |

| 22-Feb-07 | 47 |

| 28-Feb-07 | 55 |

| 31-Mar-07 | 43 |

| 25-Apr-07 | 45 |