CHAPTER 12

Accounting for Short Equity Investments

After studying this chapter you should have a grasp of the following:

- Definition of short equity securities.

- Types of short sales.

- Process of short-selling.

- Risks of short-selling.

- Box position and short-selling.

- Rationale of short-selling.

- Regulatory requirements of short sales.

- Meaning of stock lending and an illustration.

- Participants in securities lending.

- Regulation of securities lending market.

- Trade life cycle of short equity investments for trading purposes.

- Journal entries to be recorded during the different phases of the trade life cycle.

- Illustration of short equity shares trading.

- Preparation of journal entries and general ledger accounts.

- Preparation of income statement and balance sheet after short equity investments are made.

- Illustration of short equity shares with box position in functional currency.

- Illustration of short equity shares with box position in foreign currency.

DEFINITION OF SHORT EQUITY SECURITIES

Short-selling

Short-selling or shorting is the practice of selling securities the seller does not own, in the hope of repurchasing them later at a lower price. This is done with the intention to profit from an expected decline in the price of a security, as opposed to the ordinary investment practice, where an investor buys or goes long in a security in the hope that the price will rise subsequently.

The term short-selling or being short also represents strategies that allow an investor to gain from the decline in price of a security. Such strategies include buying put options.

A put option grants the right but not an obligation to sell an asset at a given price before a specified time. Thus, the buyer of put options benefits when the market price of the asset falls. Similarly, a short position in a futures contract means the holder of the position has the obligation to sell the underlying asset at a specified future date.

Short-selling is the opposite of going long. The short-seller takes a fundamentally bearish view of the market, with the expectation that the price of the stock will fall, which will ultimately enable him to buy the same stock at a lower price, thereby making a profit. The process of buying back the shares that are sold short is called buying to cover. Day traders and hedge funds use investment strategies that include selling short in stocks that are overvalued. Later they buy to cover the short, and make a handsome gain on the transaction.

In order to profit from the stock price going down, investors can borrow a security and sell it, with the expectation that the price will decrease in value so that they can buy it back at a lower price and keep the difference. The short-seller is obliged to deliver the shares to his broker, who usually in turn would have borrowed the shares from some other investor who is in actual possession of the said shares.

In most countries the regulatory requirements are such that if an investor goes short in a cash market, the investor should arrange to borrow the security and deliver the same as if he has sold a security that was in his possession.

Regular Short Sale

Short sales as just described are also known as regular short sales, where the short sale is followed up with proper delivery of the shares after borrowing the same. In most countries regulatory requirements enforce the practice that the short sales are of regular short sales type.

Naked Short Sale

When the seller does not borrow or arrange to borrow the securities in time to make delivery to the buyer within the standard three-day settlement period, then such short sale is known as a naked short sale. The buyer of such shares seldom receives the shares and is technically described as failing to deliver. Failure to deliver occurs routinely on regular long sales as well, due to several genuine reasons. It should be noted that naked short-selling is not necessarily a violation of securities laws so long as the broker-dealers who are market makers of the security are ready to buy and sell the security on a continuous basis at a publicly quoted price, irrespective of the existence of any buyer or seller.

Short-selling stock consists of the following activities:

- An investor borrows shares in which he needs to go short.

- For borrowing, the investor should first ensure that cash, equity, or government securities equivalent in value are on deposit with his brokerage firm as collateral for the initial short margin requirement.

- The investor sells them and the proceeds are credited to his account with the brokerage firm.

- The investor must close out the position by buying back the share, called buy to cover.

- If the price drops, he makes a profit. Otherwise he takes a loss.

- The investor pays a stock lending fee to the broker who has arranged for the securities.

- The investor also surrenders all the benefits received from the stock while he was the temporary owner of the shares to the original owner of the stock.

- The investor finally returns the shares to the lender.

Buying shares has a very different risk profile from selling short. When an investor buys shares, losses are limited as the price can only go down to zero. While going long, gains are theoretically unlimited as there is no limit on how high the price can go. However, in short-selling it is exactly the opposite. The possible gains are limited as the stock can only go down to a price of zero. But the potential loss can be more than the original value of the share, with virtually no upper limit. For this reason, short-selling is best resorted to only as part of a hedge rather than as an investment strategy by itself.

Other risks include the following:

- In short-selling there is no potential for dividend income or interest income, and the return is exclusively from capital gains. In fact, any dividends declared by the company during the short-selling period should be surrendered back by the investor to the lender of the stock.

- There is a potential for the price of the share sold short to rise abnormally due to short squeeze. When the price of a stock rises significantly, the short-sellers will cover their positions, thereby increasing the demand for the stock, which leads to further increase in the price of the shares.

- Sometimes the short-sellers are forced by the broker to close their position to meet a margin call.

- If the person who lent the stock wants to have his shares back, the short-seller may be forced to buy the shares from the market, creating a short squeeze. The short squeeze causes an ever further rise in the price of the stock, which in turn may trigger additional covering.

- Sometimes a short squeeze is also deliberately planned by certain group of players in the market when they notice that there is a significant number of short positions in the market.

BOX POSITION AND SHORT-SELLING

Typically hedge funds resort to selling short to profit from the long position. Selling short against the box means holding a long position on which one enters a short-sell order. The term box refers to the days when a safe deposit box was used to store the physical shares that are long positions. The psychology behind this technique is to lock in paper profits on the long position without having to sell that position. Whether prices increase or decrease, the short position balances the long position and the profits are locked in.

It should be noted that a transaction involving shorting against the box would be deemed by the tax authorities as a constructive sale of the long position, and as such the profits on it are taxable. The exception to this rule is the requirement that the short position be closed out within 30 days of the end of the year, and that the investor must hold his long position, without entering into any hedging strategies, for a minimum of 60 days after the short position has been closed.

Short-sellers are generally treated with animosity as, in the views of many people, they are profiting from the misfortune of others.

However, advocates of short-sellers argue that the practice is a key ingredient of the price discovery mechanism. Noted investors have said that short-sellers actually help the market, as short-sellers are a useful counterweight to the widespread bullishness of the markets. Some believe that short-sellers are useful in uncovering fraudulent accounting and other problems at companies.

REGULATORY REQUIREMENTS OF SHORT SALES

There are several regulatory requirements of short sales in different countries depending upon the current status of the economy. By and large there exists certain fundamental regulation regarding the requirements for short sales which should be adhered to by the market players.

The requirements for the U.S. markets are given here briefly. Note that this is not an exhaustive treatment of the regulatory requirements governing short sales in different countries, but just enough to give the readers an overview of such regulatory requirements.

- Prior to initiating a short sale, the broker-dealers responsible for it must have reasonable grounds to believe that the security can be borrowed so that it can be delivered on the settlement date. This effectively ensures the prevention of failure to deliver.

- Where there is substantial number of extended delivery failures, the broker–dealer must close out the position immediately by making delivery. Typically, these failures to deliver refer to broker–dealers that have open failures for 13 consecutive days in a threshold security.

- Where the broker–dealer has an open fail for 13 consecutive settlement days in a threshold security, no other short sales are allowed until the position is closed out by the broker–dealer.

- Threshold securities are equity securities that have an aggregate fail-to-deliver position for five consecutive settlement days totaling 10,000 shares or more, equal to at least 0.5 percent of the issuer’s total shares outstanding.

Securities lending or stock lending refers to the lending of securities by one party to another. The terms of the loan are governed by a securities lending agreement, which normally requires that the borrower provide the lender with collateral, which could be in the form of either cash or government securities of value equal to or greater than the loaned securities.

Towards the charges for the loan, both the parties negotiate a fee, quoted as an annualized percentage of the value of the loaned securities.

If the collateral provided by the borrower is cash, then the fee is quoted as a rebate. This means that the lender will earn interest on the cash collateral provided by him, and will adjust this as a rebate from the agreed rate of interest to the borrower.

To sum up, securities lending is the temporary transfer of a security by its owner to a short-seller. The title and voting rights are transferred to the borrower, who can use the same towards settling the short position during the life of the loan. Towards this the borrower agrees to return the loaned securities; secure the loan with collateral of not less value than the loaned securities; pay stock loan fees; and remit to the lender any dividends, coupon interest, or other corporate actions that occur during the time the securities are loaned to the borrower. The borrower also collects from the lender an agreed rate of interest on the cash collateral provided to the lender.

As securities lending is an over-the-counter market, it is difficult to estimate precisely the size of this industry. According to the International Securities Lending Association (ISLA), currently the balance of securities on loan exceeds $2 trillion globally. (See www.isla.co.uk.)

Large Security Lenders

| ABN AMRO (New York, London, Hong Kong) |

| Bank of America (New York) |

| Bank of New York (New York) |

| Barclays Global Investors (San Francisco, London, Tokyo) |

| Charles Schwab Corporation (San Francisco) |

| Citibank (New York) |

| Credit Suisse (New York, London) |

| Deutsche Bank (New York) |

| Dresdner Bank (Frankfurt) |

| Fortis Bank (New York, Amsterdam, London, Hong Kong) |

| Goldman Sachs (New York, London, UK) |

| JPMorgan Chase (New York) |

| Mellon Bank (Pittsburgh) |

| Morgan Stanley (New York) |

| Penson Financial Services (New York, Dallas) |

| RBC Dexia (London, Luxembourg, Toronto) |

| Robeco (Rotterdam, the Netherlands) |

| State Street Corporation (Boston, London) |

| The Northern Trust Company (Chicago) |

| UBS (Zürich, Switzerland, London) |

An Illustration of Securities Lending

Assume that a large stock lending firm having a significant position in a particular stock agrees to transfer a particular amount of stock to a hedge fund that has gone short in that security. In exchange for the stock loan, the hedge fund should transfer at least 100 percent of the stock value in cash or government securities as collateral. The cash value of the collateral would be marked-to-market on a daily basis to maintain 100 percent of the market value of the stock shorted.

For example, assume that shares in ABC Company trades at $50 per share. An investor going short in ABC would borrow 100 shares of ABC Company, and then immediately sell those shares in the market for a total of $5,000. If the price of ABC shares subsequently falls to $45 per share, the investor would then buy 100 shares back for $4,500, return the shares to their original owner, and make a $500 profit.

Note that this short-selling has unlimited potential losses as well. If the shares of ABC after selling short went up to $75, the short-seller would have to buy back all the shares at $7,500, thereby losing $2,500.

Regulation of Securities Lending Market

Securities lending is regulated in most of the world’s major securities markets and is perfectly legal. Most markets require that the borrowing of securities be conducted only for specifically permitted purposes that include the following:

- To facilitate settlement of a trade.

- To facilitate delivery of a short sale.

- To finance the security.

- To facilitate a loan to another borrower for one of the permitted purposes listed above.

When a security is loaned, the title of the security is transferred to the borrower. Thus the borrower is entitled to receive all coupon and/or dividend payments, and any other rights such as voting rights. However, these dividends or coupons must be passed back to the lender.

Stock lending was originally resorted to as a means to cover settlement failures. When a seller failed, for whatever reason, to deliver the shares he had sold, he would incur additional costs and penalties due to settlement failure. In those circumstances, the seller would borrow the stock at a fee and deliver it to the buyer. When the seller was able to procure the shares, he would return the same to the lender and pay a fee for the stock borrowed.

However, nowadays the principal reason for borrowing a stock is to take a short position. As the seller is obliged to deliver the shares, the seller should borrow the same by incurring a fee for the same. At the end of the deal, the seller would return an equivalent security to the lender.

Participants in Securities Lending

- Borrowers are typically investment banks, broker/dealers, intermediaries, or hedge funds.

- Lenders with assets in the form of equities and fixed income securities will most commonly participate in the market in one of two ways—either directly or indirectly through an agent.

- Direct lenders tend to be large institutional investors such as pension plans and insurance companies.

- Agent lenders will act for any beneficial owner regardless of size, where the beneficial owner does not wish to, for reasons of cost or size, participate directly. Agent lenders tend to be global custodians or asset managers participating on behalf of a large number of clients.

The International Securities Lending Association (ISLA) is a trade association established in 1989 to represent the common interests of participants in the securities lending industry. ISLA works closely with European regulators and in the United Kingdom has representation on the Securities Lending and Repo Committee, a committee of market practitioners chaired by the Bank of England. The Association has contributed to a number of major market initiatives, including the development of the UK Stock Borrowing and Lending Code of Guidance and the industry standard lending agreement, the Global Master Securities Lending Agreement (GMSLA). ISLA’s priorities for 2007 and 2008 include:

- Working with regulators to provide a safe and efficient framework for securities lending.

- Providing information to members about securities lending market developments.

- Opening up new markets for securities lending.

- Developing good industry practices.

- Reviewing the GMSLA.

- Enhancing the public profile of the securities lending industry.

ISLA has more than 90 members comprising insurance companies, pension funds, asset managers, banks, and securities dealers representing more than 4,000 clients. While based in London, ISLA represents members from more than 20 countries in Europe and North America.

(Source: ISLA website, www.isla.co.uk)

THE TRADE LIFE CYCLE FOR EQUITY SHORT SALES

- Short-sell the share.

- Pay brokerage/commission on the sell transaction.

- Deposit the collateral for the value of short sales.

- Receive the contracted amount for the share.

- Pay the stock lending fees.

- Ascertain the fair value at the end of the reporting period.

- Reverse the mark-to-market.

- Dividend declaration by the company.

- Convey the dividend to the original owner of the shares.

- Receive the interest on cash collateral pledged with the broker.

- Buy to cover the share.

- Pay the brokerage/commission on the buy transaction.

- Pay the consideration.

- Ascertain the profit/loss on the sale.

- Get back the cash collateral from the broker.

- FX revaluation entries.

- FX translation entries.

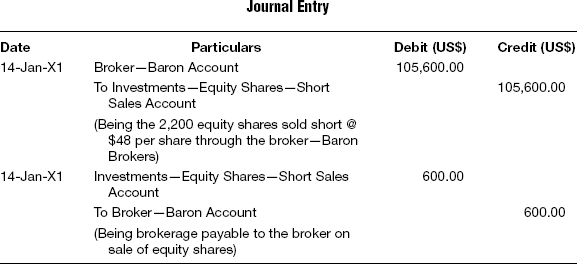

Short-sell the Share

The investor should first ensure that he has made arrangements for delivering the shares that he intends to short. Even though the onus is on the broker-dealer, it is better to ensure this beforehand to avoid any hassles later.

When the net holding of any share is negative—that is, where the shares sold are greater than the shares bought of the same security—it is referred to as short position.

Alan Kimberly Inc. short-sells 1,000 equity shares of Gold Crest at $490 per share through the broker Silver Man on October 3. The accounting entry that is recorded in the books of accounts is as follows:

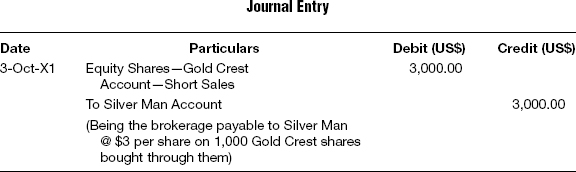

Brokerage/Commission on the Transaction

The broker of the stock exchange charges commission for the services rendered. This is usually settled along with the sale value of the shares. Accounting standards require that this is treated as part of the cost of the shares procured/sold. Hence this is usually built into the cost of purchase/sale of the shares.

On the 1,000 Gold Crest shares purchased through Silver Man, the brokerage payable per share is $3. The accounting entry that is recorded in the books of accounts is as follows:

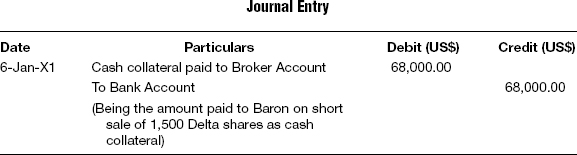

Deposit Cash Collateral with the Broker

The next event in the trade life cycle of short sales is the deposit of collateral with the broker through whom the short sale is effected. It is assumed that the collateral in this case is cash, even though the collateral can be in any acceptable form to the broker, such as government securities. Based on the collateral deposited by the investor, the broker will arrange for procuring the stock loan and deliver the same to the stock exchange on the settlement date.

Assuming that the broker is paid on day T + 2, then the accounting entry that is recorded in the books of accounts is as follows:

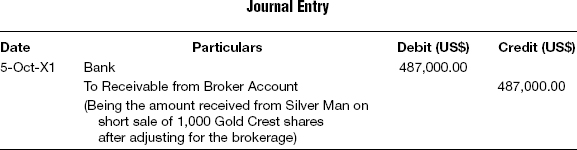

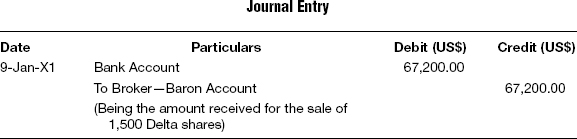

Receive the Contracted Amount for the Share

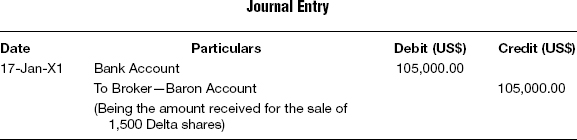

The next event in the trade life cycle of short sales is the receipt of the contracted amount for the shares sold. Usually the delivery of the shares and the receipt for the same happens two days after the date of the trade; this is referred to as T + 2. However, this varies from exchange to exchange.

The shares are usually delivered electronically by the seller and the payment is made by the buyer on the same date. During this stage the actual asset comes into the physical possession of the buyer and the liability created earlier is settled. For exchange-traded securities, the settlement automatically takes place on the settlement date through the clearing system of the exchange concerned. For over-the-counter (OTC) trades, both the parties resort to their own accepted method of settlement to ensure that they effectively avoid each other’s counterparty risk.

Assuming that the broker is paid on T + 2, then the accounting entry that is recorded in the books of accounts is as follows:

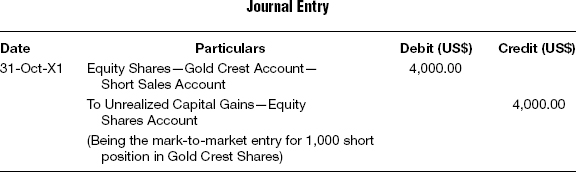

Ascertain the Fair Value at the End of the Reporting Period

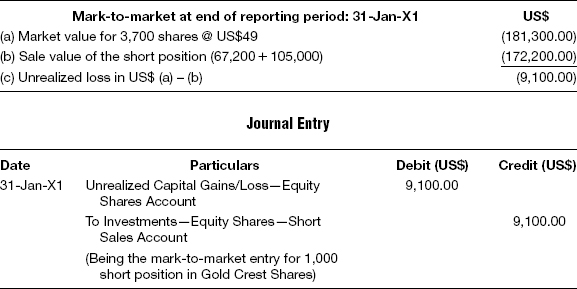

At the end of every reporting period the fair value of the shares is ascertained and the shares are marked-to-market. This process is known as portfolio valuation, when the market rate at the end of the period is determined from the primary stock exchange where the shares are traded.

If there is a decrease in the market rate over and above the sale rate, then such decrease is recognized as a gain on the one hand, and the corresponding amount is reflected as a decrease in the value of short-sold shares. Conversely, if there is an increase in the market rate over and above the sale rate, then such increase is recognized as a loss on the one hand, and the corresponding amount is reflected as an increase in the value of short-sold shares. Note that any increase in the market rate over and above the sale rate can result in additional collateral being deposited by the investor with the broker concerned.

This accounting entry is reversed on the next day or the next valuation date when a fresh entry for the then value is recorded in the books of accounts. Alternatively, the accounting entry can also be recorded only for the incremental value. If the investor follows this incremental value method then there is no need to reverse the entry for mark-to-market recorded earlier.

Assuming that the market rate of Gold Crest as of October 31, which is the next valuation date, is $483, then the accounting entry that is recorded in the books of accounts is as follows:

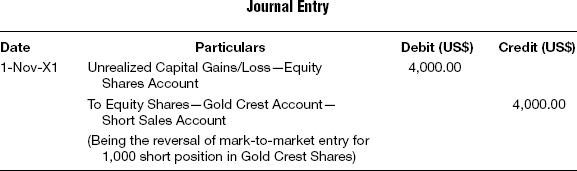

Reversal of Mark-to-market Entry

The accounting entry for mark-to-market is reversed on the next day or the next valuation date when a fresh entry for the then value is recorded in the books of accounts. However, as mentioned earlier, if the investor follows this incremental value method then there is no need to reverse the entry for mark-to-market recorded earlier.

The accounting entry that is recorded in the books of accounts is shown below:

Corporate Action—Dividend Declaration by the Company

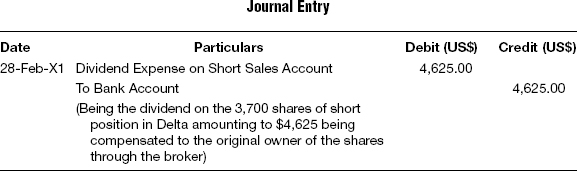

In a short sale, the corporate actions by the issuing company should be surrendered to the original owner of the shares. For example, if a dividend is declared by the company during the time when the short sale is effective, then such dividend must be compensated to the original owner of the shares. Since the shares are not currently held by the investor, the investor will not receive any dividend from the company. Nevertheless, the original owner of the shares is deprived of the dividend declared by the company and hence needs to be compensated by the investor.

It should be noted that technically, the investor will not be at any disadvantage on account of the dividend declared by the company even though the investor is required to compensate the dividend to the original owner without having received anything from the company—the reason being that after such dividend declaration, the market rate of the security effectively stands reduced by the dollar amount of dividend per share, thereby reducing the short sale liability of the investor.

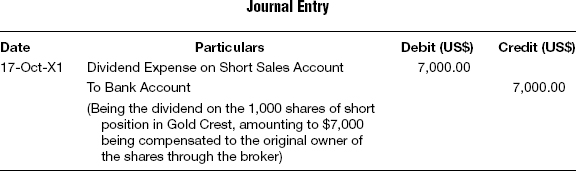

No accounting entry would be recorded in the books of accounts of the investor on account of Gold Crest announcing a dividend of $7 per share, the ex-dividend date being October 17.

Compensate the Dividend to the Original Owner of the Shares

The original owner should be compensated for the dividend forgone by him due to lending the stock to the investor.

Assuming that the actual cash dividend announced by the company amounts to $7 per share, the ex-dividend date being October 17, the accounting entry that is recorded in the books of accounts is as follows:

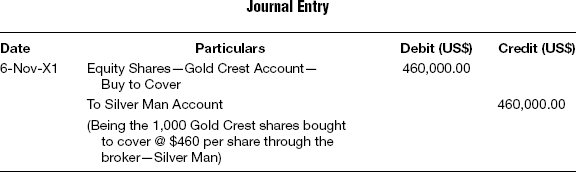

Buy to Cover the Shares

Ultimately the short-sold shares should be covered through a broker of the exchange. An accounting entry is recorded for the contracted amount to be paid on such purchase. Note that this entry will be posted to the account called Equity Shares—Gold Crest Account—Short Sales, just as Long Account and Sell Long Account are posted to the same account.

Assuming that the entire quantity of 1,000 shares of Gold Crest is covered on November 6 for a consideration of $460 each, and assuming the brokerage per share amounts to $4, then the accounting entry that is recorded in the books of accounts is shown as follows:

Brokerage/Commission on the Sell Transaction

Brokerage is paid when the shares are sold and only the net proceeds are taken into account. The accounting entry that is recorded in the books of accounts is shown as follows:

Pay the Consideration

The consideration is paid on day T + 2 or another day based on the exchange concerned. The consideration is paid including brokerage. The accounting entry that is recorded in the books of accounts is shown as follows:

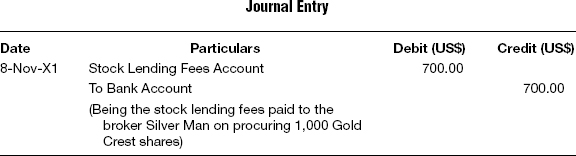

Pay the Stock Lending Fees

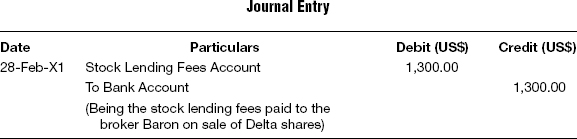

The stock lending fees should be paid to the broker, who in turn has to pay the same to the original owner of the shares. The stock lending fees are arrived at as a percentage per annum on the value of the shares.

Assuming that $700 is paid towards the stock lending fees, the accounting entry that is recorded in the books of accounts is shown as follows:

Receive the Interest on Cash Collateral with the Broker

The cash collateral deposited with the broker earns interest at an agreed-on rate. Assuming in this case the interest on the cash collateral with the broker amounted to $500, the accounting entry that is recorded in the books of accounts is shown as follows:

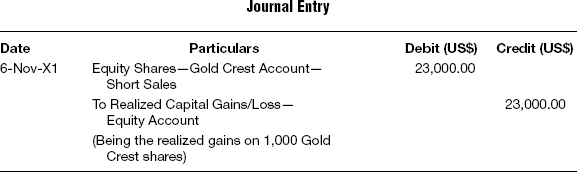

Ascertain the Profit/Loss on the Sale

The profit or loss on liquidation of the shares is ascertained by deducting the cost of sales from the net sale consideration. Cost of sales is arrived at by following first in first out (FIFO), last in first out (LIFO), or weighted average method.

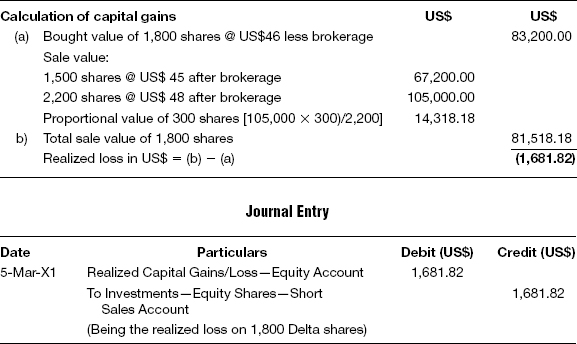

In this case 1,000 shares of Gold Crest were first sold at the rate of $490 and $3 was paid per share towards brokerage, resulting in the net sale realization of Gold Crest shares at $487 per share. This was subsequently bought to cover for a net cost of $464 including brokerage. Hence the profit on each share is $23 and the total profit for the entire lot amounts to $23,000. The profit or loss realized is always recognized on the date of liquidation and not on the date on which the net proceeds are received from the broker.

The accounting entry that is recorded in the books of accounts is shown as follows:

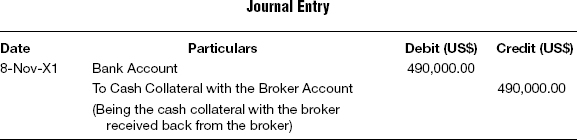

Get Back the Cash Collateral from the Broker

The cash collateral deposited with the broker would be returned by the broker on squaring up of the short position as the shares bought from such short covering would be returned to the original owner of the shares.

The accounting entry that is recorded in the books of accounts is shown as follows:

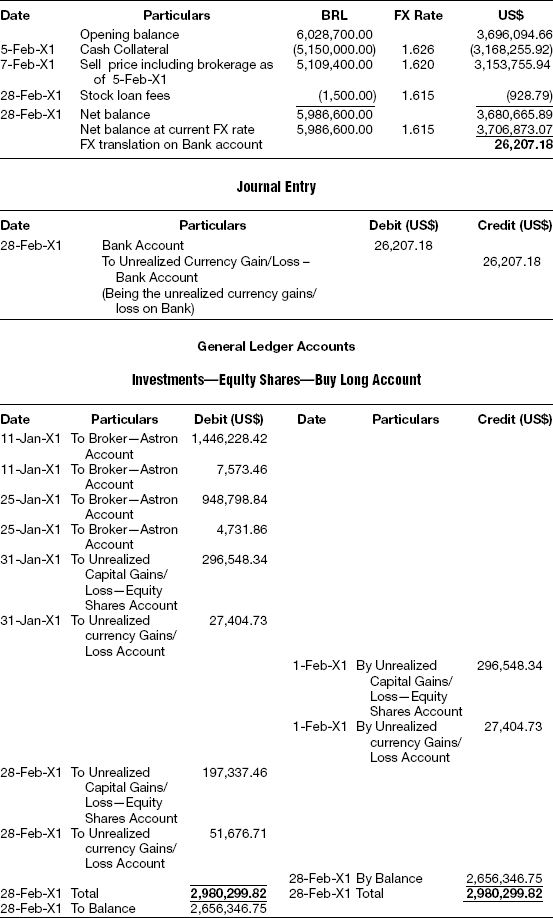

FX Revaluation Entries

All the entries recorded to this point are initially entered in the respective trade currencies. If the functional currency is different from the trade currency, then each and every entry recorded in the trade currency should be entered again in the functional currency by converting the entries at the respective day’s FX rates. In other words, for each trade currency that the investor deals with, there will be a complete set of books representing that trade currency. This includes journal entries, general ledger postings, trial balance, income statement, and balance sheet.

After revaluing each and every journal entry of all the trade currencies into the functional currency, a separate set of books is prepared again comprising all the elements just mentioned: journal entries, general ledger postings, trial balance, income statement, and balance sheet. It should be noted that the ultimate financial reports would be prepared and presented to all the stakeholders based on the financial statements prepared in the functional currency only, as this will encompass all the transactions of the investor in all trade currencies dabbled with. (For illustration and detailed explanation please refer to Chapter 2.)

FX Revaluation Entries

After revaluing all the entries in the functional currency at the respective FX rates for the day concerned, another entry needs to be passed in the books of the functional currency. This is mainly to adjust the currency gains or losses due to the fluctuations in FX rates between the reporting date and the date of recording the original entries. FX translation entries are recorded only for the asset and liability accounts. For income and expense accounts, the amount gets crystallized on the date of passing the FX revaluation entries in the books of the functional currency.

There are fundamentally two types of FX translation entries that are recorded in the books of the functional currency: consummated FX translation entries and transient FX translation entries. (For illustration and detailed explanation please refer to Chapter 2.)

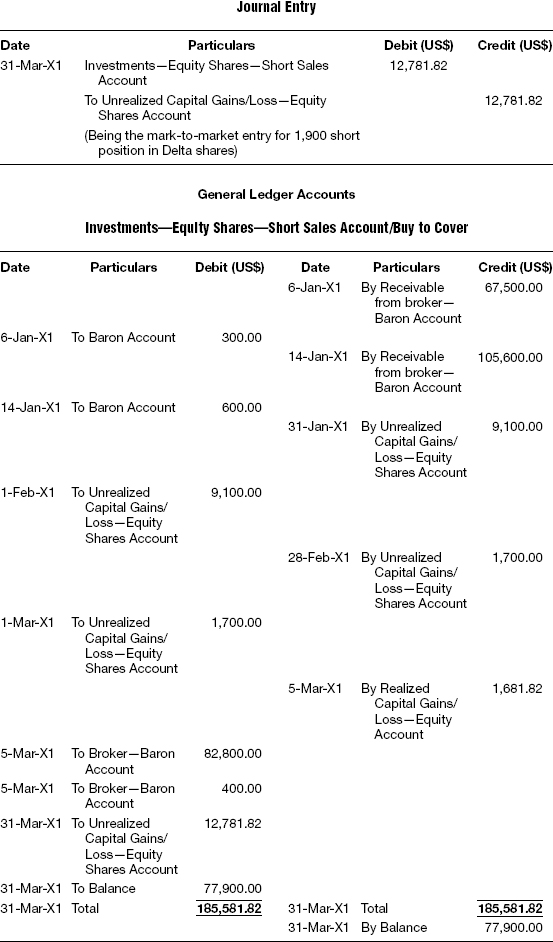

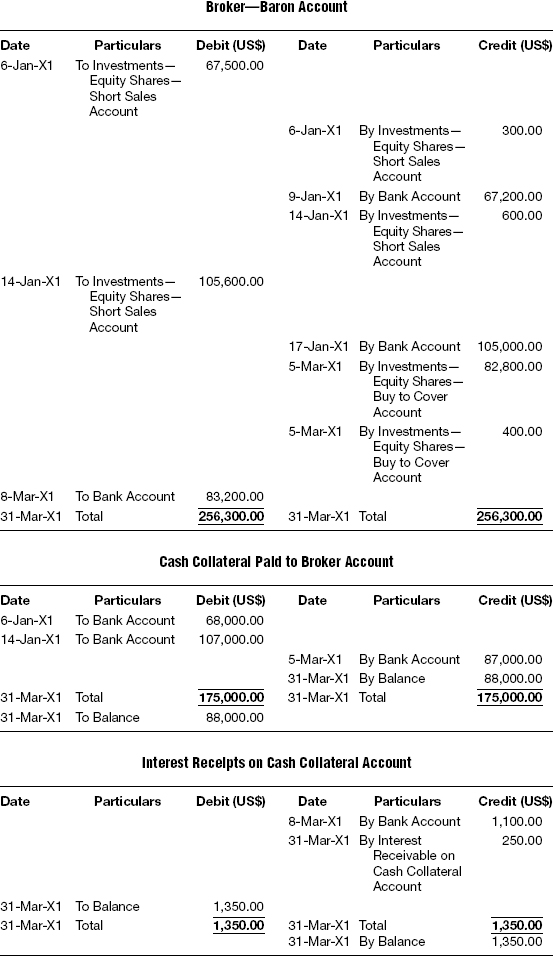

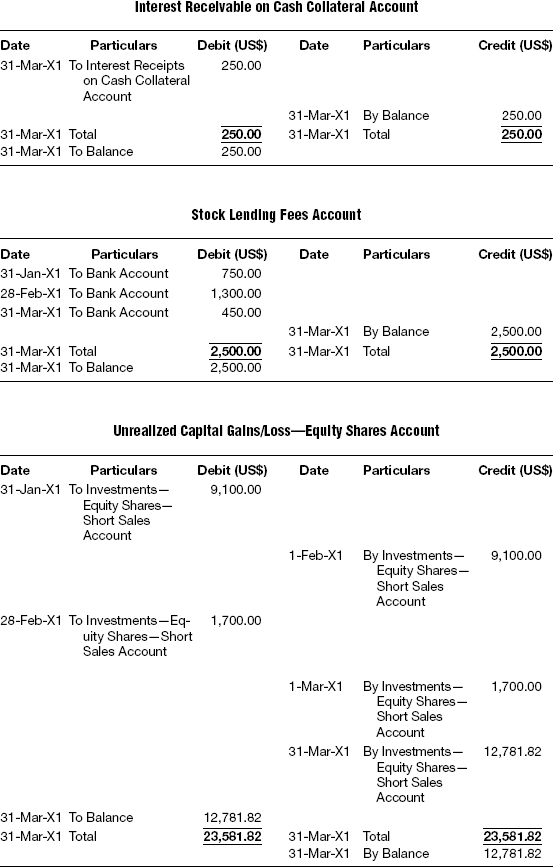

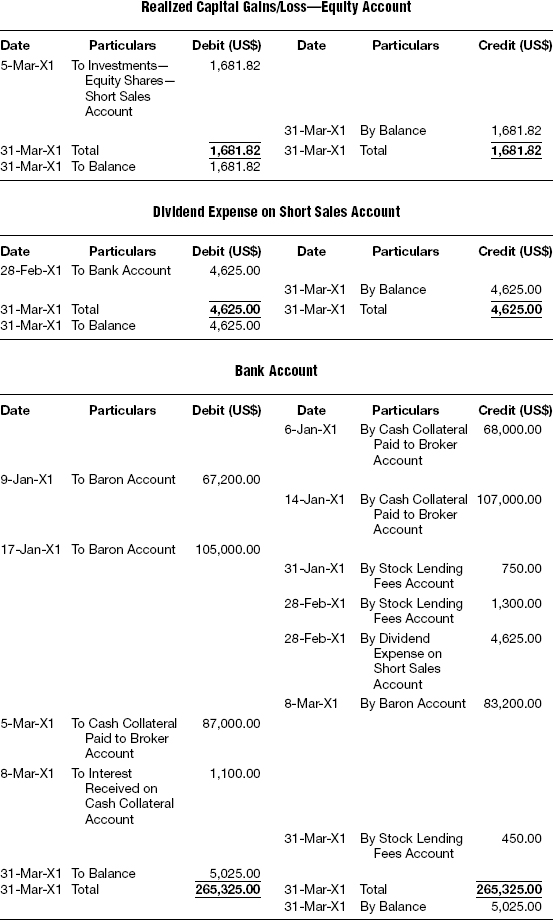

Short Equity Shares—Trading

Crystal Inc. traded in Delta shares in a U.S. stock exchange through Baron Brokers, and the details are as follows:

Trade Details

Other Details

- On February 28 a dividend of $1.25/share is declared by Delta.

- Stock loan fees paid by Crystal on short sales:

- January 31: $750

- February 28: $1,300

- March 31: $450

- Settlement: T + 3

- Crystal Inc. makes a deposit of $68,000 with the broker on January 6 and $107,000 on January 14.

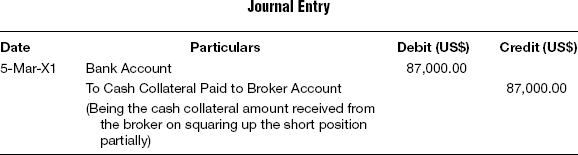

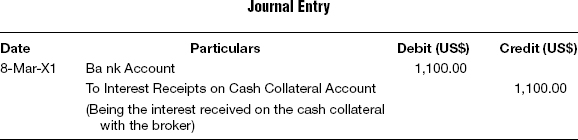

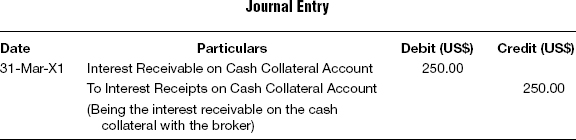

- Broker returns the deposit amounting to $87,000 along with interest of $1,100 to Crystal on March 5. Interest accrued on the deposit with broker as of March 31 is $250.

Liquidation Method

FIFO

Market Rate

January 31: 49.00

February 28: 47.00

March 31: 41.00

Journal entries, general ledgers, trial balance, income statement, and balance sheet for Crystal Inc. for the period January 1 to March 31 are as follows:

Solution

T-1 On Deposit of Cash Collateral with the Broker

T-2 On Short Sale of Equity Shares and Brokerage

T-3 On Receipt of Share Sale Amount from the Broker

T-4 On Deposit of Cash Collateral with the Broker

T-5 On Sale of Equity Shares and Brokerage

T-6 On Receipt of Share Sale Amount from the Broker

T-7 On Payment of Stock Lending Fees

T-8 Mark-to-market at End of Reporting Period Jan X1

T-9 Reversal of Mark-to-market Entry

T-10 On Payment of Stock Lending Fees

T-11 On Compensation of Dividend to the Original Owner of the Shares

T-12 Mark-to-market at End of Reporting Period Feb-X1

T-13 Reversal of Mark-to-market Entry

T-14 On Purchase of Shares—Buy to Cover

Equity shares bought to cover will be posted to the short sales account as this is the liquidation entry for the short sales.

T-15 Brokerage on the Bought-to-Cover Transaction

T-16 Being the Amount Paid on Purchase of Shares

T-17 On Receipt of the Contracted Amount for the Shares

T-18 On Receipt of the Interest on Cash Collateral with the Broker

T-19 On Realizing the Profit/Loss on Liquidation

T-20 Interest Receivable on Cash Collateral with the Broker Booked as Accrual at End of the Reporting Period

T-21 On Payment of Stock Lending Fees

T-22 Mark-to-market at End of Reporting Period Mar-X1

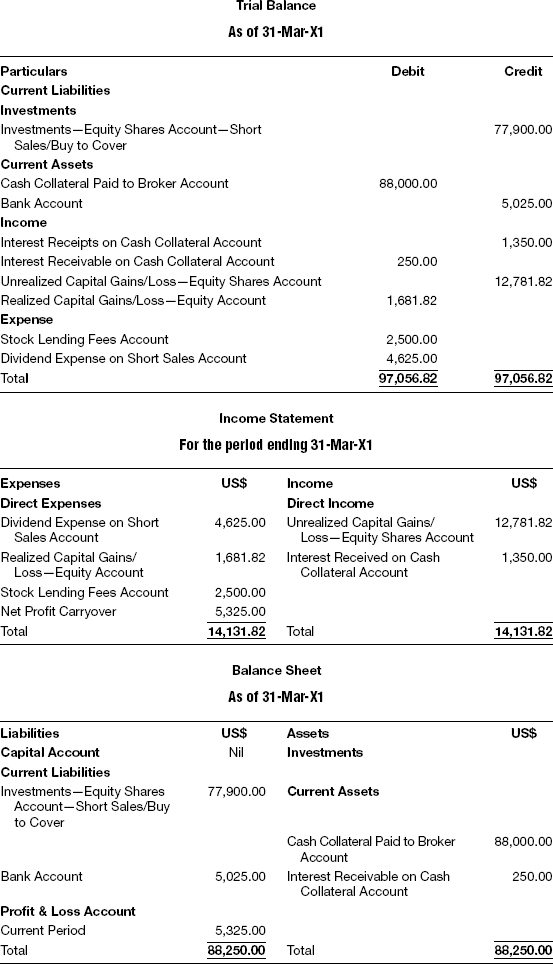

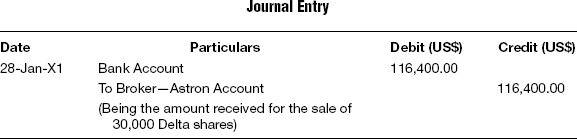

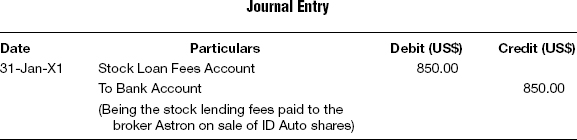

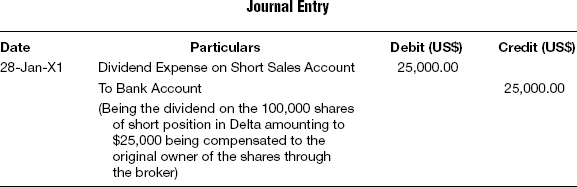

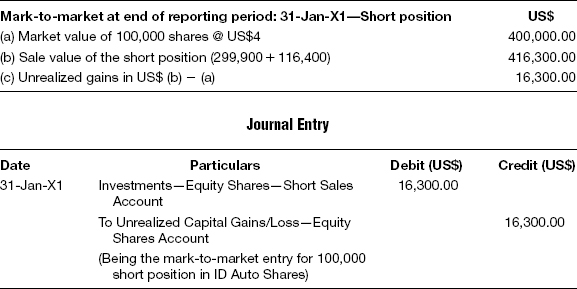

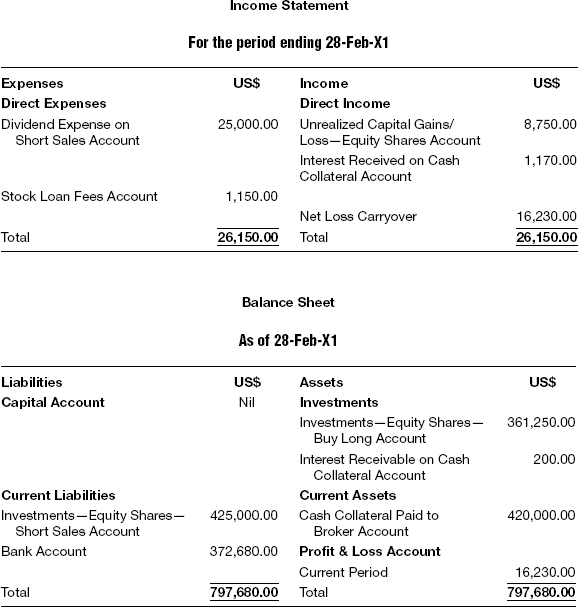

Short Equity Shares—Box Position—US$

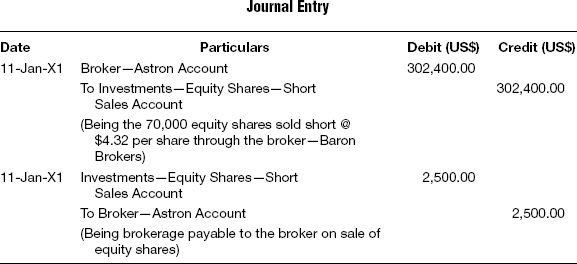

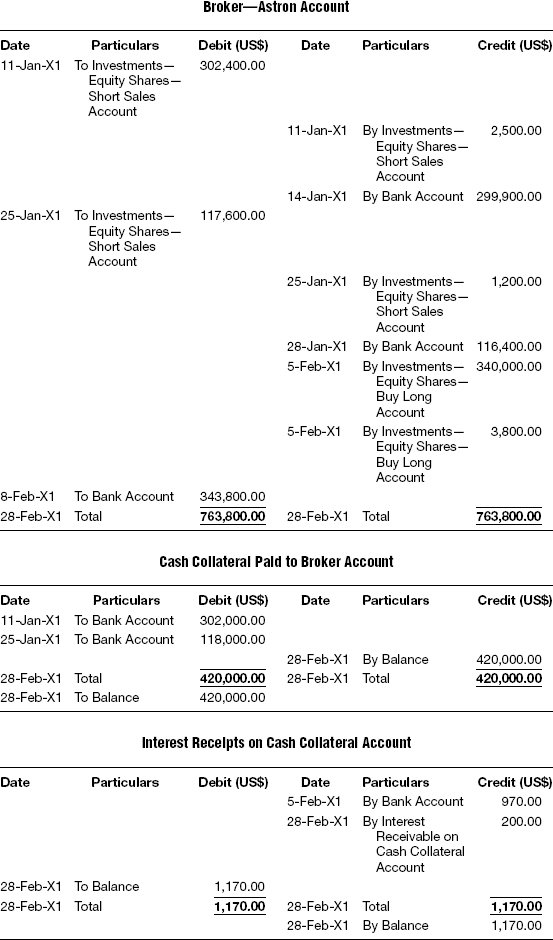

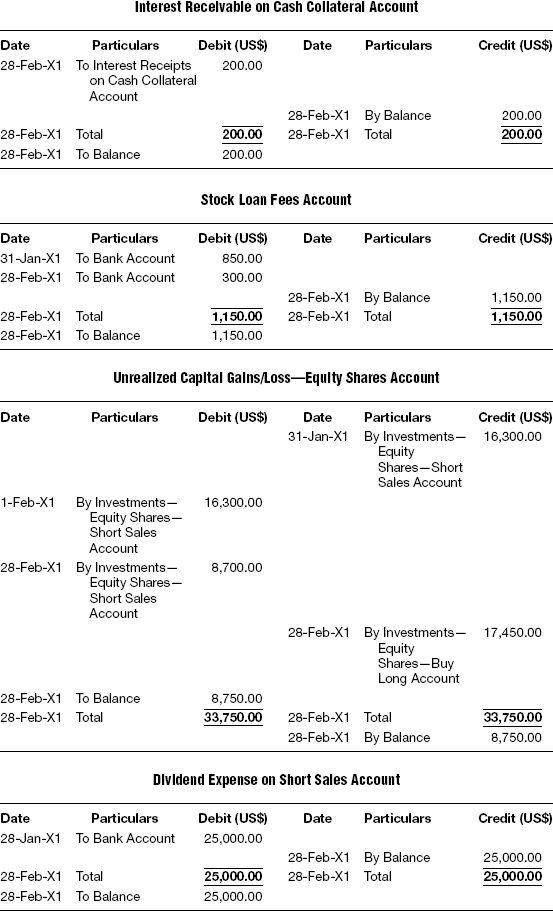

Band Bros Inc. traded in ID Auto shares in a U.S. stock exchange through Astron brokers and the details are as follows:

Trade Details

Other Details

- A dividend declared by ID Auto amounts to $0.25 per share on January 28.

- Stock loan fee by Band Bros on short sales:

- January 31: $850

- February 28: $300

- Settlement: T + 3

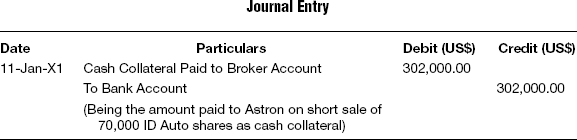

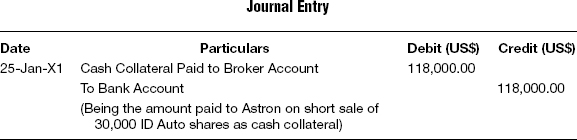

- Band Bros Inc. makes a deposit of $302,000 with the broker on January 11 and $118,000 on January 25.

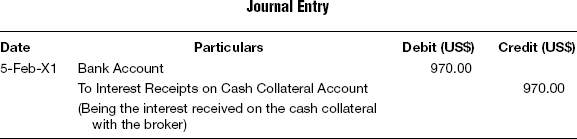

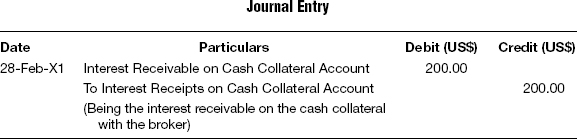

- Broker pays interest of $970 on cash collateral to Band Bros Inc. on February 5. Interest accrued on the cash collateral with broker as of February 28 is $200.

- The bought-long position is not liquidated against the short position and is held as box position.

Market Rate

January 31: 4.00

February 28: 4.25

Journal entries, general ledgers, trial balance, income statement, and balance sheet for Band Brothers Inc. for the period January 1 to February 28 are as follows:

Solution

T-1 On Deposit of Cash Collateral with the Broker

T-2 On Sale of Equity Shares and Brokerage

T-3 On Receipt of Share Sale Amount from the Broker

T-4 On Deposit of Cash Collateral with the Broker

T-5 On Sale of Equity Shares and Brokerage

T-6 On Receipt of Share Sale Amount from the Broker

T-7 On Payment of Stock Loan Fees

T-8 On Payment of Dividend

T-9 Mark-to-market at End of Reporting Period Jan X1

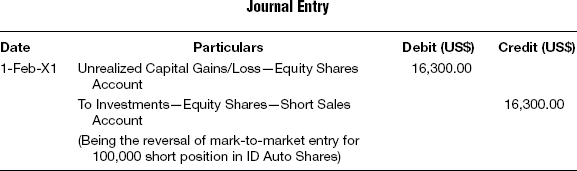

T-10 Reversal of Mark-to-market Entry

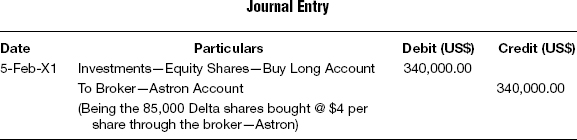

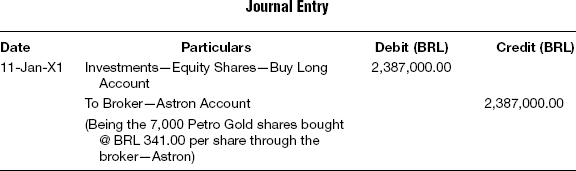

T-11 On Purchase of Shares

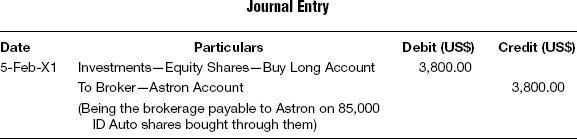

T-12 Brokerage on the Bought Shares

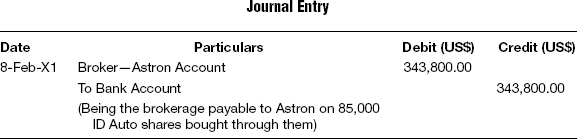

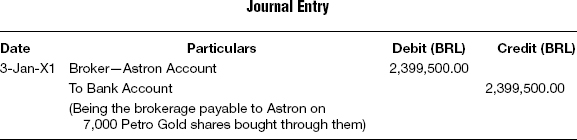

T-13 Being the Amount Paid on Purchase of Shares

T-14 On Receipt of the Interest on Cash Collateral with the Broker

T-15 Interest Receivable on Accrued Interest from Cash Collateral with the Broker

T-16 On Payment of Stock Loan Fees

T-17 Mark-to-market at End of Reporting Period Feb X1

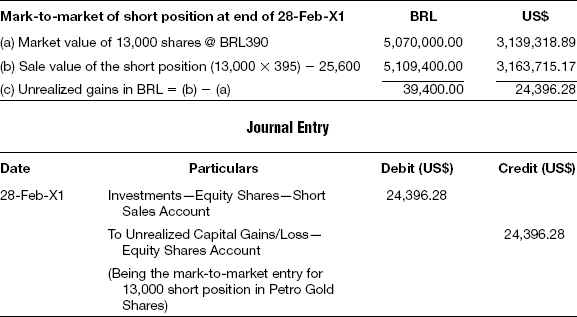

T-18 Mark-to-market at End of Reporting Period Feb-X1

Short Equity Shares—Box Position—BRL

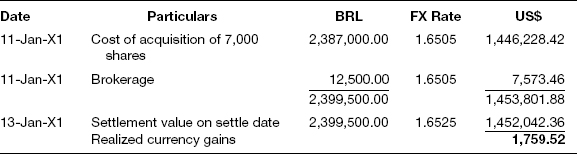

Rosario Inc. traded in Petro Gold shares in a Brazilian stock exchange through Astron brokers and the details are as follows:

Trade Details

Other Details

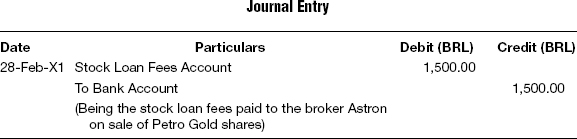

- The stock loan fee paid by Rosario Inc. on short sales on February 28 was BRL1500.

- An investor has introduced an amount of BRL 10 million as share capital on January 1 in the Rosario Inc. fund.

- Settlement: T + 2

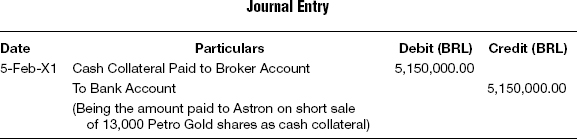

- Rosario Inc. makes a deposit of BRL 5.150 million with the broker on February 5 as collateral.

- Interest accrued on cash collateral amounts to BRL 9,500 due from the broker as of February 28.

FX Rates

| Date | FX Rate |

| 1-Jan-X | 1.6540 |

| 11-Jan-X1 | 1.6505 |

| 13-Jan-X1 | 1.6525 |

| 25-Jan-X1 | 1.6484 |

| 27-Jan-X1 | 1.6444 |

| 31-Jan-X1 | 1.6311 |

| 5-Feb-X1 | 1.6255 |

| 7-Feb-X1 | 1.6201 |

| 28-Feb-X1 | 1.6150 |

Market Rate

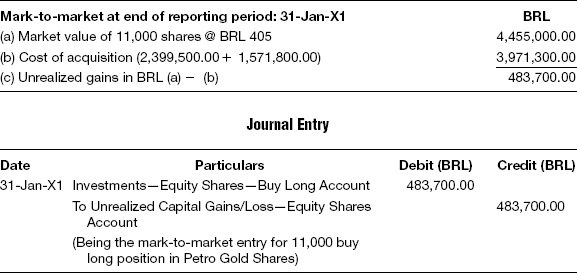

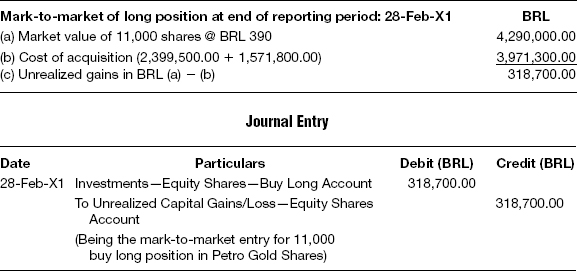

January 31: 405.00

February 28: 390.00

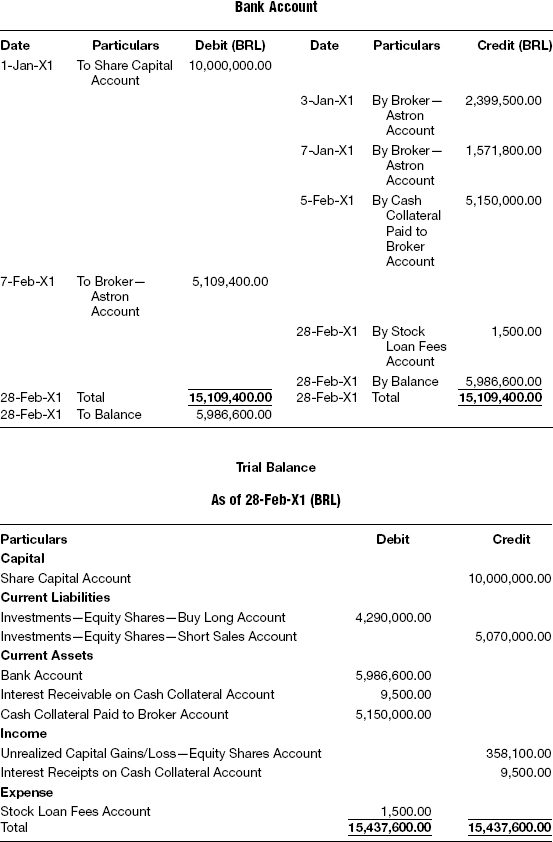

Journal entries, general ledgers, trial balance, income statement, and balance sheet for Rosario Inc., for the period January 1 to March 31 are as follows:

Solution

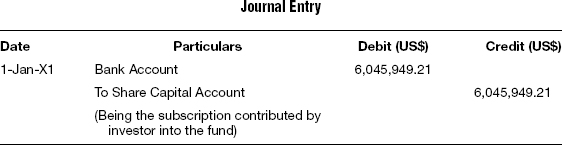

T-1 Capital Introduced by the Fund

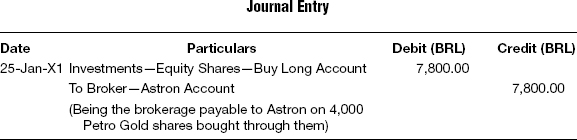

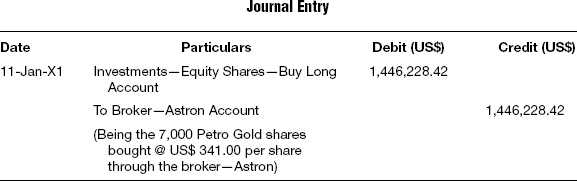

T-2 On Purchase of Shares

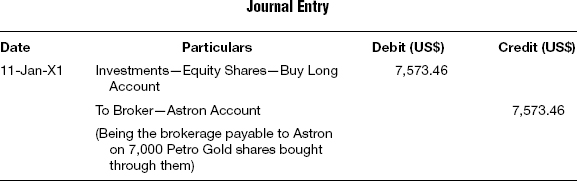

T-3 Brokerage on the Bought Shares

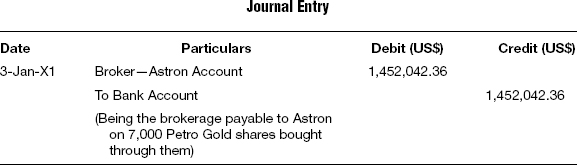

T-4 Being the Amount Paid on Purchase of Shares

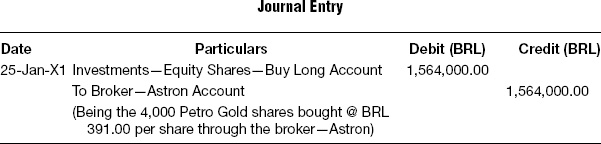

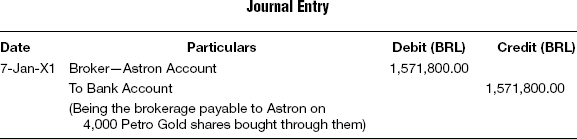

T-5 On Purchase of Shares

T-6 Brokerage on the Bought Shares

T-7 Being the Amount Paid on Purchase of Shares

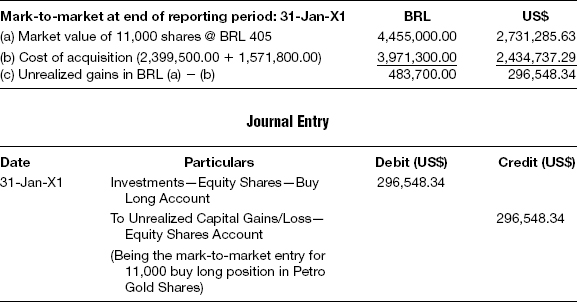

T-8 Mark-to-market at End of Reporting Period Jan X1

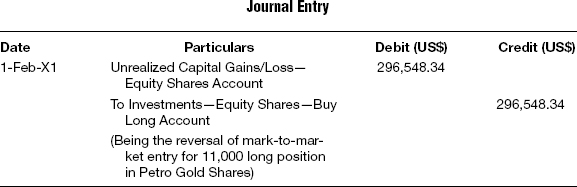

T-9 Reversal of Mark-to-market Entry

T-10 On Deposit of Cash Collateral with the Broker

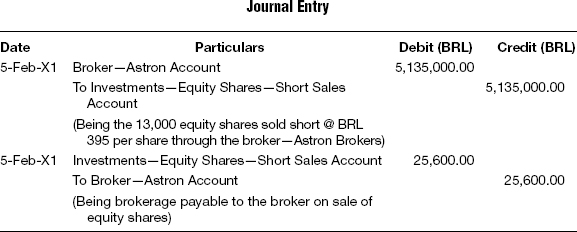

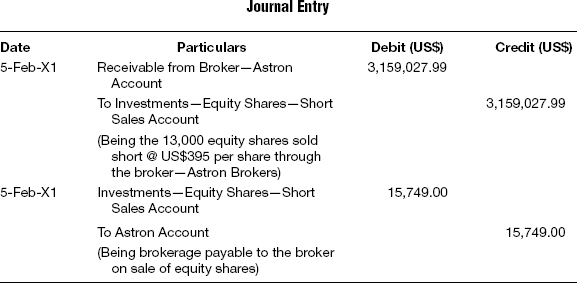

T-11 On Sale of Equity Shares and Brokerage

T-12 On Receipt of Share Sale Amount from the Broker

T-13 On Payment of Stock Loan Fees

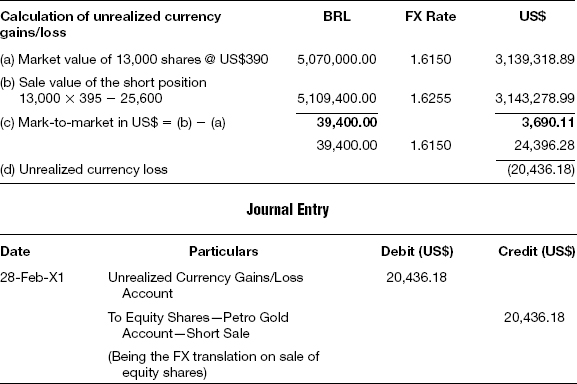

T-14 Mark-to-market at End of Reporting Period Feb X1

T-15 Mark-to-market at End of Reporting Period Feb X1

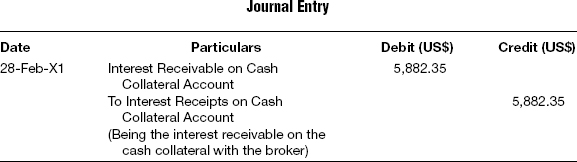

T-16 Interest Receivable on Accrued Interest from Cash Collateral with the Broker

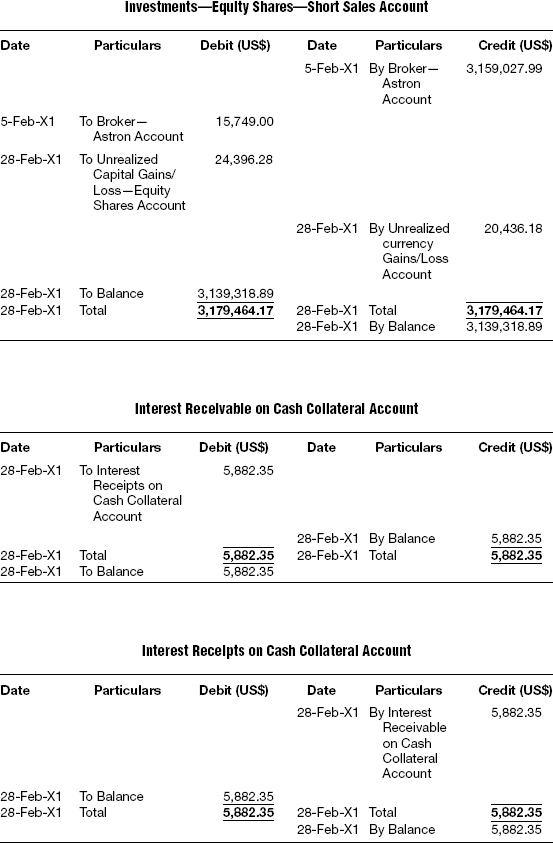

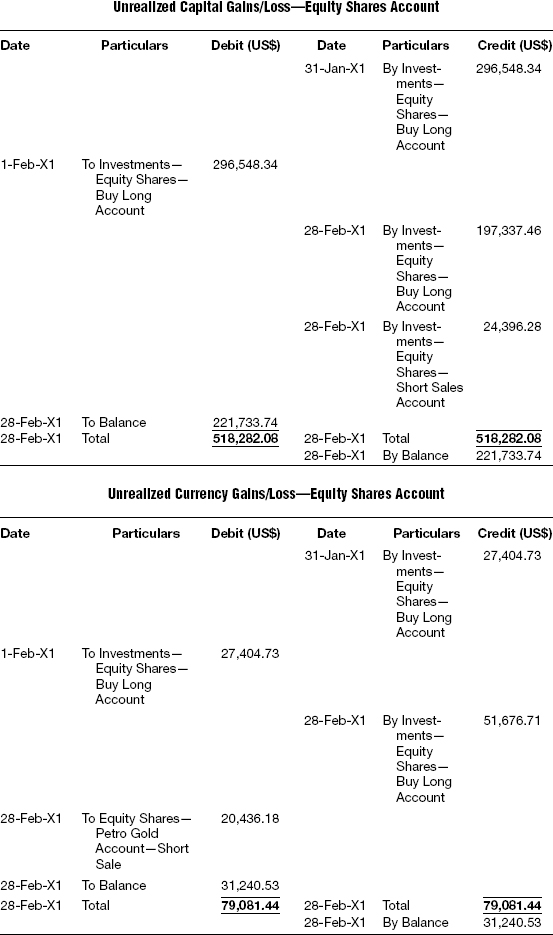

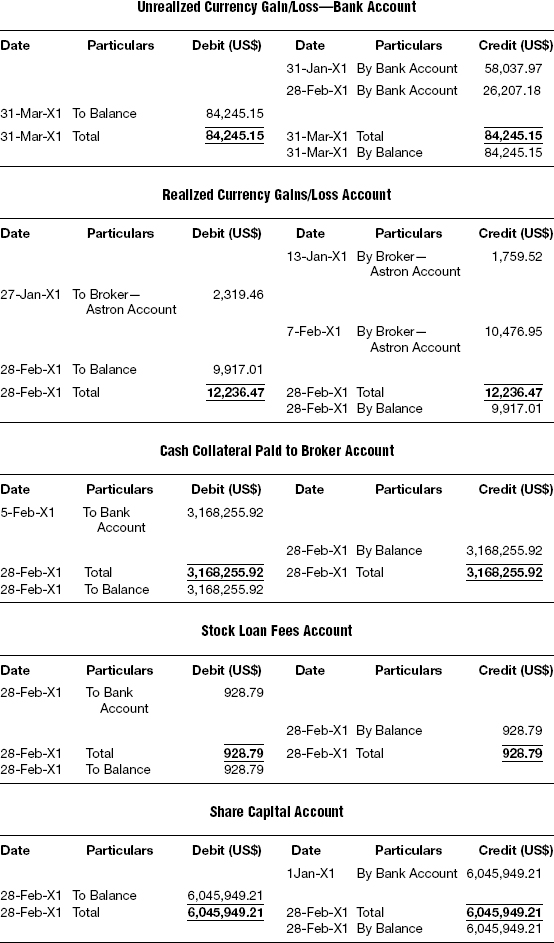

Short Equity Shares—Box Position—BRL to US$

F-1 Capital Introduced by the Fund (T-1 @ FX Rate: 1.6540)

F-2 On Purchase of Shares (T-2 @ FX Rate: 1.6505)

F-3 Brokerage on the Bought Shares (T-3 @ FX Rate: 1.6505)

F-4 Being the Amount Paid on Purchase of Shares (T-4 @ FX Rate: 1.6525)

F-5 FX Translation (Consummated FX Translation Entry)

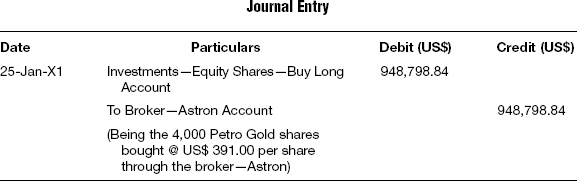

F-6 On Purchase of Shares (T-5 @ FX Rate: 1.6484)

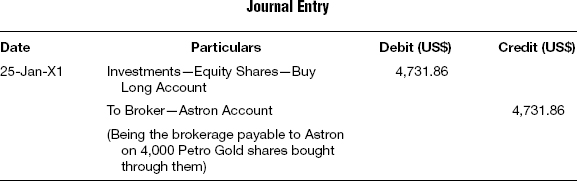

F-7 Brokerage on the Bought Shares (T-6 @ FX Rate: 1.6484)

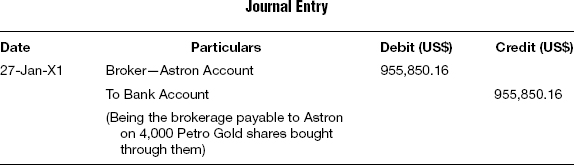

F-8 Being the Amount Paid on Purchase of Shares (T-7 @ FX Rate: 1.6444)

F-9 FX Translation (Consummated FX Translation Entry)

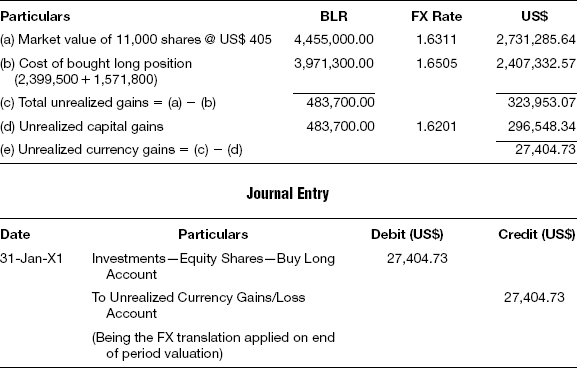

F-10 Mark-to-market at End of Reporting Period Jan X1: (T-8 @ FX Rate: 1.6311)

F-11 Reversal of Mark-to-market Entry (T-9 @ FX Rate: 1.6311)

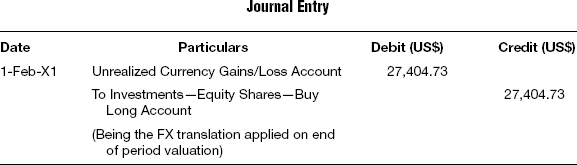

F-12 FX Translation (Transient FX Translation Entry)

F-13 Reversal of FX Gains/Loss

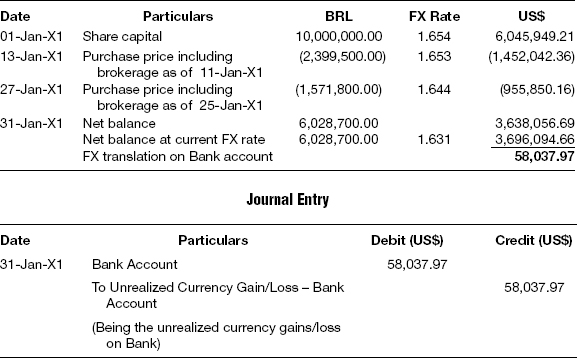

F-14 Currency Gains/Loss—Bank FX (Transient FX translation entry)

F-15 On Deposit of Cash Collateral with the Broker (T-10 @ FX Rate: 1.6255)

F-16 On Short Sale of Equity Shares and Payment of Brokerage (T-11 @ FX Rate: 1.6255)

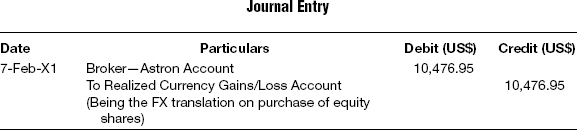

F-17 On Receipt of Share Sale Amount from the Broker (T-12 @ FX Rate: 1.6201)

F-18 FX Translation (Consummated FX Translation Entry)

F-19 On Payment of Stock Loan Fees (T-13 @ FX Rate: 1.6150)

F-20 Mark-to-market at End of Reporting Period Feb X1 (T-14 @ FX Rate: 1.6150)

F-21 FX Translation (Transient FX Translation Entry)

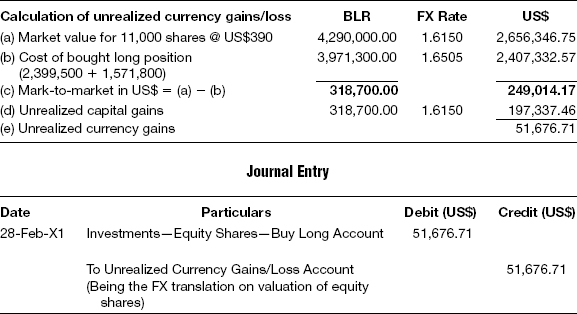

F-22 Mark-to-market at End of Reporting Period Feb X1 (T-15 @ FX Rate: 1.6150)

F-23 FX Translation (Transient FX Translation Entry)

F-24 Interest Receivable on Accrued Interest from Cash Collateral with the Broker (T-16 @ FX Rate: 1.6150)

F-25 Currency Gains/Loss—Bank FX (Transient FX translation entry)

- Short-selling is the practice of selling securities the seller does not own, in the hope of repurchasing them later at a lower price.

- This is done with the intention to profit from an expected decline in the price of a security, as opposed to the ordinary investment practice in which an investor buys or goes long in a security in the hope that the price will rise subsequently.

- In order to profit from the stock price going down, investors can borrow a security and sell it, with the expectation that the price will decrease so that they can buy it back at a lower price and keep the difference.

- The short-seller is obliged to deliver the shares to his broker, who usually in turn would have borrowed the shares from some other investor who is in actual possession of the said shares.

- In most countries, the regulatory requirements are such that if an investor goes short in a cash market, the investor should arrange to borrow the security and deliver the same as if he has sold a security that was in his possession.

- When the seller does not borrow or arrange to borrow the securities in time to make delivery to the buyer with the standard three-day settlement period, the short sale is known as naked short sale. The buyer of such shares seldom receives the shares, and the situation is technically described as failure to deliver.

- The short-selling process involves several steps, starting with borrowing the shares, selling short, buying to cover, and thus closing out the position.

- Short-selling is fraught with several risks and is quite dangerous as an investment strategy, as the investor can get into a short squeeze caused either by market forces or deliberately by any group of market players to corner the investor.

- Hedge funds often resort to short-selling shares in which they already hold long positions, which is also known as a box position. Strictly, box positions do not alter the profits or profitability for the investor except that the accounting for the same gets a little complicated. However, for tax purposes, box position short sales are treated as if the original long position is liquidated.

- In spite of the severe criticism of short-selling, it is not without merits, especially as it is an essential part of the price discovery mechanism. Several leading investors have hailed short-selling as a useful counterweight to the widespread bullishness in the market, and some believe that short-sellers are useful in uncovering fraudulent accounting and other problems at companies.

- There are several regulatory requirements regarding short sales in different countries, depending upon the current status of the economy. By and large there exist certain fundamental regulations regarding the requirements for short sales, which should be adhered to by the market players.

- Securities lending or stock lending refers to the lending of securities by one party to another. The terms of the loan are governed by a securities lending agreement, which normally requires that the borrower provide the lender with collateral, which could be in the form of either cash or government securities of value equal to or greater than the loaned securities.

- Towards the charges for the loan, both the parties negotiate a fee, quoted as an annualized percentage of the value of the loaned securities.

- If the collateral provided by the borrower is cash, then the fee is quoted as a rebate. This means that the lender will earn interest on the cash collateral provided by him, and will adjust this as a rebate from the agreed rate of interest to the borrower.

- Securities lending is legal and regulated in most of the world’s major securities markets. Most markets mandate that the borrowing of securities be conducted only for specifically permitted purposes.

Theory Questions

1. What is short-selling and is it legal?

2. What are the different types of short sales?

3. Outline the process of short-selling.

4. Can an investor short a share without first arranging for the delivery of the shares?

5. What are the potential risks of short-selling? How does it compare with going long on a security?

6. Can an investor simultaneously hold both long and short positions in the same security? If so, will it result in any realized gain from the accounting perspective as well as from the tax authorities’ perspective?

7. Is short-selling good for the stock markets?

8. Describe the rationale behind short-selling.

9. Are there any regulatory requirements of short selling in the U.S. stock markets?

10. What do you understand by securities lending?

11. How are the securities lending market regulated?

12. Who are the participants in securities lending?

Objective Questions

1. Short-selling is preferred by traders based on the expectation that the

a. Price of the security will go up

b. Price of the security will go down

c. Price of the security will remain stable

d. None of the above

2. The strategy allowing the investor to gain from the declining price of security includes

a. Buying call options

b. Selling call options

c. Buying put options

d. None of the above

3. The process of buying back the shares that are sold short is called

a. Buy to square off

b. Buy to cover

c. Buy back to cover

d. None of the above

4. A short sale followed up with proper delivery of shares after borrowing is referred to as a

a. Regular short sale

b. Naked short sale

c. Sale on delivery

d. None of the above

5. A short sale not followed up with proper delivery of shares within the standard three-day settlement period is referred to as a

a. Regular short sale

b. Naked short sale

c. Sale on delivery

d. None of the above

6. In short-selling there is no potential for

a. Dividend income

b. Return from capital gains

c. Profit on sale

d. All of the above

7. The action of lending the security of one person to another is referred to as a

a. Security transfer

b. Corporate action

c. Security lending

d. None of the above

8. When the collateral provided by the buyer to the lender is in the form of cash, the fee is referred to as

a. Brokerage

b. Rebate

c. Lending fee

d. None of the above

9. The permitted purposes of stock borrowing include

a. To facilitate settlement of trade

b. To facilitate delivery of short sale

c. To finance the security

d. All of the above

10. Which of the following is not a participant in security lending?

a. Borrowers

b. Agent lenders

c. Brokers

d. All of the above

Journal Questions

For the following scenario, prepare journal entries, general ledgers, trial balance, income statement, and balance sheet for Abdul Razack Inc. for the period January 1 through February 28.

Box Position—Trade Currency BRL

Abdul Razack Inc. traded in Coca-Cola shares in a Brazilian stock exchange through Pompoodle brokers and the details are as follows:

Trade Details

Other Details

- The stock loan fee paid by Abdul Razack Inc. on short sales on February 28 is BRL4,800.

- An investor has introduced an amount of BRL10 million as share capital on January 1 into the Abdul Razack Inc. fund.

- Settlement: T + 2

- Abdul Razack Inc. makes a deposit of BRL1.05 million with the broker on February 5 as collateral.

- Interest accrued on cash collateral amounts to BRL7,800 due from the broker as of February 28.

FX Rates

| Date | FX Rate |

| 1-Jan-X | 1.6540 |

| 11-Jan-X1 | 1.6505 |

| 13-Jan-X1 | 1.6525 |

| 25-Jan-X1 | 1.6484 |

| 27-Jan-X1 | 1.6444 |

| 31-Jan-X1 | 1.6311 |

| 5-Feb-X1 | 1.6255 |

| 7-Feb-X1 | 1.6201 |

| 28-Feb-X1 | 1.6150 |

Market Rate

January 31: 42.00

February 28: 39.00